James

Fintech writer with a knack for turning complex money and crypto topics into engaging, accessible content. Whether it's demystifying blockchain or breaking down finance trends, he make sure every word counts.

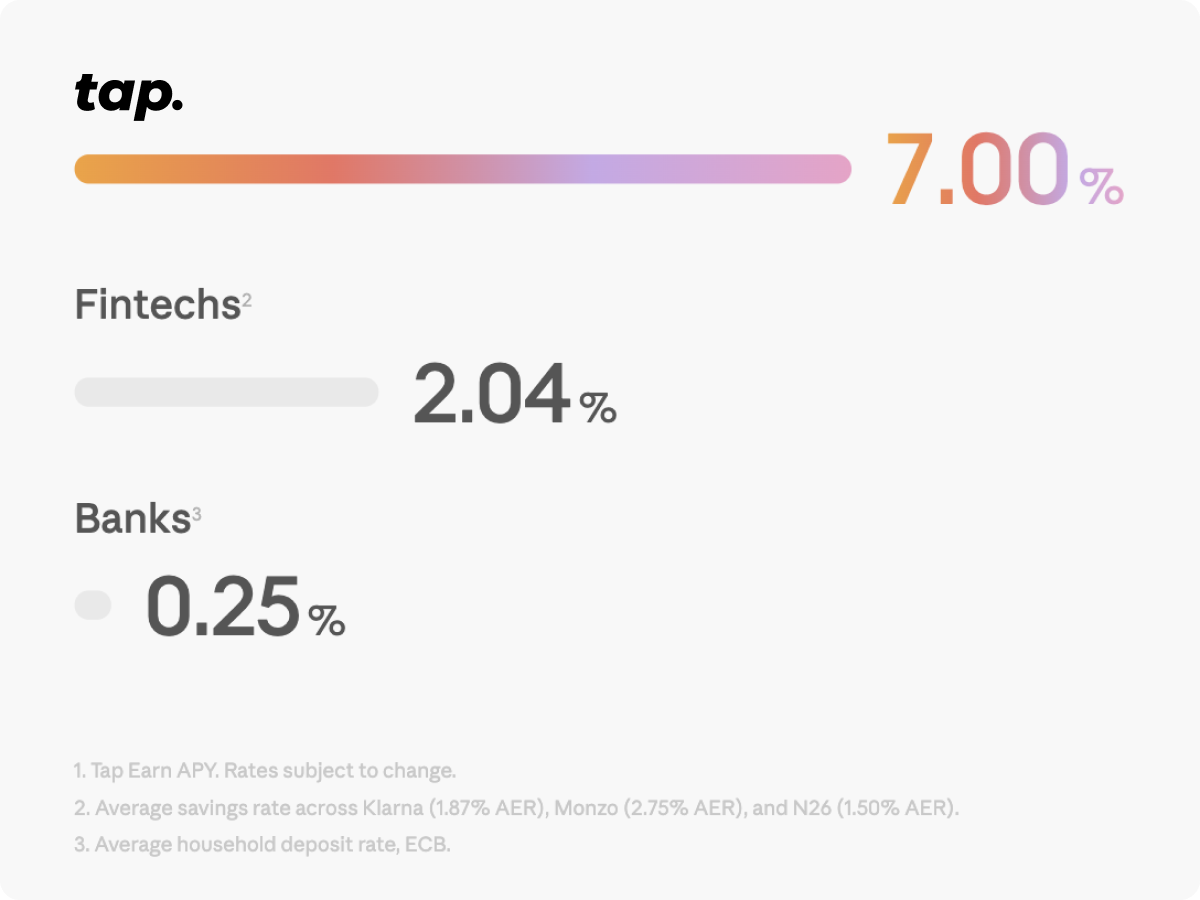

It should be easier to save for your holidays, that nicer car, or your dream house down payment. That's why we built Tap Earn.

Savings accounts haven't changed in decades, but the cost of everything else has. Rent's up. Groceries cost more. A coffee costs what lunch used to. And your savings account? Still paying you next to nothing while the bank lends your money out and keeps the difference.

Most savings accounts pay around 0.4% APY. That's $4 a year on $1,000.Even the fintech "high-yield" ones barely push past 3%, and they still come with the usual catches, fine prints, and withdrawal limits.

Meanwhile, the official inflation rate keeps running higher. When inflation runs higher than your interest rate, you're losing purchasing power every year. Your savings shrink, even if the number in your account slowly ticks up.

It should be easier to save for your holidays, that nicer car, or your dream house down payment. That's why we built Tap Earn.

A Better Way to Earn

Tap Earn offers up to 7% APY, that's nearly 18x what most banks pay and double what fintechs offer out there.

Your interest compounds daily and pays out every week, straight into your balance. No waiting for end-of-month statements, no quarterly or year cycles, no lockup. Every Monday, your balance is higher than it was on Friday. Not a bad way to start the week.

And unlike your bank, you don't have to guess what you've earned. Open the app anytime and see exactly how much interest you've made, down to the cent.

What Can You Earn On?

Tap Earn launches with USDT, USDC, BTC, ETH, XRP, and SOL. More of your favorite assets are on the way.

We're not trying to list everything under the sun. Every asset we add has to meet one standard: can we offer a rate worth your time? If we can't give you a good rate on it, we won't add it just to pad a menu. Quality over quantity. Your earnings come first.

Deposit From Anywhere

Accessibility matters most to us, earning should be easy no matter how you deposit. With Tap, you can deposit money anytime, anywhere, using whatever method you like best. Tap supports bank transfers and debit cards, from majors to stablecoins to the long tail most platforms don't bother supporting. You don't need to move your life around to start earning. Link your existing bank account in minutes and start earning higher rates on your savings without switching banks or opening new accounts here and there.

Your money is yours, and you should be able to access it when you need it. You can withdraw with no penalties, take out what you want, when you want.

Time to Start Earning

Tap is trusted by 400,000+ users across 40+ countries and is publicly listed on the London Stock Exchange. This isn't a startup in someone's garage.

Ready to get started? Download the app, or head to the app and simply find the "Earn" tab from the hub.

It's time to earn what you deserve.

See you inside.

Tap Earn services are provided by Tap Earn Inc and are not regulated by the Gibraltar Financial Services Commission or by the UK Financial Conduct Authority, or covered by the Gibraltar Investor Compensation Scheme or the UK Financial Services Compensation Scheme.

Deja de malabarear con cinco pestañas para seguir el mercado cripto. El Markets Center de Tap reúne precios, gráficos, los activos más activos y noticias en un único lugar dentro de Tap.

Estar al día del mercado de criptomonedas puede llegar a parecer un trabajo a tiempo completo. Una pestaña para los precios. Otra para los gráficos. Un sitio diferente para las noticias. Y luego vuelves a tu aplicación para hacer algo. Antes de que te des cuenta, estás manejando cinco plataformas o más solo para entender qué está pasando.

Ese es exactamente el problema que nos propusimos resolver.

Te presentamos el Markets Center, tu nuevo espacio de referencia dentro de Tap para seguir, explorar y entender el mercado, todo sin salir de la aplicación.

Se acabó el saltar entre pestañas 🫨

Si alguna vez te has encontrado saltando entre aplicaciones solo para consultar precios, tendencias y titulares, no eres el único.

Las criptomonedas se mueven rápido, y mantenerse al día suele implicar depender de múltiples herramientas y plataformas, muchas de las cuales pueden resultar abrumadoras o inconsistentes.

El Markets Center lo reúne todo. En lugar de recopilar información de distintos lugares, ahora puedes obtener una instantánea clara y en tiempo real del mercado en una sola vista, justo donde ya gestionas tus criptomonedas.

Una forma más inteligente de leer el mercado

El Markets Center está diseñado para ofrecerte información de un vistazo, sin ahogarte en complejidad.

Esto es lo que encontrarás:

- Más activos: ve al instante qué activos están registrando los mayores movimientos.

- Mayores subidas y bajadas: entiende rápidamente hacia dónde se dirige el impulso del mercado.

- Nuevos listados: mantente al día de los últimos tokens que entran al mercado.

- Lista completa de activos: navega y ordena por capitalización de mercado, volumen, variaciones de precio y más, adaptado a cómo quieres explorar.

- Feed de noticias integrado: recibe actualizaciones de fuentes fiables, todas en un mismo lugar, sin preocuparte por su credibilidad.

Todo lo que necesitas para estar informado, y algo más.

El pulso del mercado, de un vistazo

Seamos sinceros: demasiados datos pueden ser tan frustrantes como insuficientes.

En el mundo de las criptomonedas, es fácil sentirse abrumado por demasiados indicadores, gráficos y métricas, que pueden ser útiles pero no siempre prácticos para el uso diario.

A veces, lo único que quieres es una respuesta rápida a una pregunta:

"¿Qué está haciendo el mercado ahora mismo?"

Con el Markets Center, esa respuesta está siempre a un toque. Desde las criptomonedas más populares hasta las últimas noticias, puedes hacerte una idea del mercado en segundos, sin necesidad de análisis exhaustivos.

Diseñado pensando en ti

El Markets Center es tu lugar de referencia si quieres:

- Estar informado sin sobrecarga visual

- Seguir el mercado sin cambiar de aplicación

- Filtrar el ruido con un feed de noticias con fuentes selectas

Todo lo que necesitas para ir un paso por delante, sin esfuerzo adicional.

Cómo acceder al Markets Center ✨

Empezar es muy sencillo:

- Abre tu aplicación Tap

- Ve a la pestaña Markets Center (justo al lado de la pestaña Inicio)

- Desplázate y explora los activos más activos, el listado completo y las noticias en un solo lugar

Eso es todo. No se necesita configuración ni ajustes adicionales. Tendrás acceso inmediato a un feed de noticias curado y a datos de mercado en directo.

¿Listo para simplificar tu experiencia cripto?

Con el Markets Center, ya no necesitas tener cinco pestañas abiertas para entender el mercado.

Tanto si quieres analizar los gráficos en detalle como si simplemente quieres tener el dedo en el pulso del mercado, solo tienes que abrir la app y el Markets Center estará listo con todo lo que necesitas. Porque estar al día en cripto no debería ser complicado.

Descubre cómo los on-ramps y off-ramps de stablecoins conectan el dinero fiat tradicional con la blockchain para ofrecer liquidaciones globales casi instantáneas, 24/7.

Mover dinero a nivel internacional no debería sentirse como enviar una carta por correo o usar una paloma mensajera. Sin embargo, para muchas empresas, esa sigue siendo la realidad. A menudo tienen que lidiar con retrasos, comisiones ocultas y poca visibilidad. En los últimos años, las stablecoins han demostrado que este proceso puede ser mucho más eficiente, ofreciendo transferencias globales casi instantáneas. Pero para desbloquear todo su potencial, hay una pieza clave que debe funcionar entre bastidores: los on-ramps y off-ramps.

Estos sistemas actúan como puente entre la banca tradicional y las redes blockchain, permitiendo a las empresas moverse entre monedas fiat (como dólares, euros o libras) y stablecoins. Veamos cómo funcionan y qué pueden aportar a tu negocio.

Cómo las infraestructuras tradicionales siguen marcando el ritmo

Antes de que el dinero llegue a la blockchain, comienza su recorrido en los sistemas bancarios tradicionales. En Europa, esto suele implicar transferencias SEPA, mientras que en el Reino Unido se utilizan Faster Payments. Mover dinero a nivel internacional no debería sentirse como enviar una carta por correo o usar una paloma mensajera. Sin embargo, para muchas empresas, esa sigue siendo la realidad. A menudo tienen que lidiar con retrasos, comisiones ocultas y poca visibilidad. En los últimos años, las stablecoins han demostrado que este proceso puede ser mucho más eficiente, ofreciendo transferencias globales casi instantáneas. Pero para desbloquear todo su potencial, hay una pieza clave que debe funcionar entre bastidores: los on-ramps y off-ramps.

Estos sistemas actúan como puente entre la banca tradicional y las redes blockchain, permitiendo a las empresas moverse entre monedas fiat (como dólares, euros o libras) y stablecoins. Veamos cómo funcionan y qué pueden aportar a tu negocio.

Cómo las infraestructuras tradicionales siguen marcando el ritmo

Antes de que el dinero llegue a la blockchain, comienza su recorrido en los sistemas bancarios tradicionales. En Europa, esto suele implicar transferencias SEPA, mientras que en el Reino Unido se utilizan Faster Payments. Las transferencias SEPA son ampliamente utilizadas en la eurozona y pueden tardar desde unas horas hasta un día laborable completo, dependiendo del banco y el momento. Faster Payments, por su parte, hace honor a su nombre: suele liquidar en segundos y funciona las 24 horas del día, los 7 días de la semana.

Estos sistemas son fiables, pero siguen sujetos a horarios y estructuras bancarias que pueden generar fricción o retrasos. Aquí es donde entran las stablecoins, no necesariamente para reemplazarlos, sino para mejorar lo que ocurre después del movimiento del dinero.

Por qué las stablecoins cambian las reglas del juego

Las stablecoins como USDT y USDC están diseñadas para mantener un valor estable, generalmente vinculado al dólar estadounidense. A diferencia de las transferencias bancarias tradicionales, operan sobre redes blockchain que funcionan continuamente, sin interrupciones ni limitaciones geográficas.

Una vez que los fondos se convierten en stablecoins, pueden transferirse globalmente en segundos, en cualquier momento del día. Esto las convierte en una capa de liquidación ideal para empresas que gestionan pagos internacionales, tesorería o operaciones transfronterizas.

Mientras que USDT suele utilizarse más para liquidez y trading, USDC es preferida en entornos regulados por su transparencia. Ambas cumplen funciones similares, y la elección depende de las necesidades específicas del negocio.

El papel de las cuentas virtuales

Una innovación clave en los on-ramps modernos es el uso de cuentas virtuales. Una cuenta virtual es un identificador digital, similar a un número de cuenta o IBAN.

Cuando llegan los fondos, el sistema identifica automáticamente a quién pertenecen. Esto permite una conciliación instantánea de los pagos entrantes y una escalabilidad sin intervención manual.

Para empresas que gestionan grandes volúmenes de transacciones, esto es fundamental. Garantiza que los fondos puedan rastrearse, asignarse y procesarse antes de convertirse en stablecoins.

El on-ramp: de fiat a stablecoin

El proceso de on-ramp convierte dinero tradicional en activos digitales. Aunque suene complejo, el flujo suele ser sencillo:

- La empresa envía dinero fiat (por ejemplo, EUR o GBP) mediante SEPA o Faster Payments

- Los fondos llegan y se asignan automáticamente mediante una cuenta virtual

- El sistema ejecuta la conversión a una stablecoin como USDT o USDC

- La stablecoin se envía a una wallet designada

Si la transferencia inicial es instantánea (como con Faster Payments), todo el proceso puede completarse en cuestión de minutos. Si no, la parte en blockchain sigue siendo inmediata una vez que los fondos fiat se liquidan.

El off-ramp: de stablecoin a fiat

El proceso inverso permite convertir stablecoins en dinero tradicional:

- El usuario envía stablecoins a la wallet del proveedor

- El sistema confirma la recepción e inicia la conversión

- El dinero fiat se envía a una cuenta bancaria mediante SEPA o Faster Payments

La velocidad final depende del sistema bancario utilizado, aunque la parte blockchain sigue siendo rápida y eficiente.

Dónde sigue existiendo fricción

Aunque las stablecoins eliminan muchas ineficiencias, no eliminan todas.

Los sistemas fiat todavía pueden introducir:

- Retrasos, especialmente fuera del horario bancario

- Controles de cumplimiento que pueden ralentizar operaciones grandes

- Limitaciones regionales según la infraestructura bancaria

Esto significa que, aunque las transferencias en blockchain sean instantáneas, los puntos de entrada y salida siguen dependiendo del sistema tradicional.

Por qué esto es importante para las empresas

La velocidad de liquidación no es solo un detalle técnico, tiene un impacto directo en las finanzas.

Cuando los pagos tardan días en completarse, el capital queda inmovilizado en tránsito. Esto afecta al flujo de caja, reduce la flexibilidad y genera incertidumbre. Muchas empresas compensan esto manteniendo mayores reservas, lo que reduce la eficiencia.

La infraestructura basada en stablecoins cambia esta dinámica. Al permitir liquidaciones casi instantáneas una vez que los fondos están en blockchain, las empresas pueden mover capital más rápido, reducir saldos inactivos y mejorar la visibilidad de sus operaciones.

Para empresas globales, esto supone un cambio fundamental en cómo se mueve el dinero.

Optimiza tus operaciones con stablecoins con Tap

Si tu empresa quiere superar las limitaciones de la banca tradicional y aprovechar la velocidad de las stablecoins, la cuenta cripto para empresas de Tap te ofrece todo en una sola plataforma.

Obtén tu propio IBAN individual y acceso a cuentas en monedas como EUR o GBP, con soporte completo para SEPA Instant y Faster Payments. Esto permite gestionar on-ramps y off-ramps de forma fluida, sin depender de múltiples proveedores ni sufrir retrasos bancarios.

Además, Tap permite trading entre más de 70 criptomonedas, incluidas stablecoins como USDT y USDC. Tanto si necesitas convertir fiat para liquidaciones rápidas como mover capital globalmente, la plataforma está diseñada para adaptarse al ritmo de tu negocio.

¿Listo para experimentar el futuro de los pagos globales? Ponte en contacto con el equipo de Tap aquí.

Si alguna vez te has preguntado por qué enviar criptomonedas a veces es instantáneo y otras lento, o por qué algunas transacciones cuestan céntimos mientras que otras tienen comisiones elevadas, no eres el único.

Detrás de escena, las blockchains no son una única tecnología. Funcionan más bien como un sistema de múltiples niveles interconectados, donde cada capa se encarga de una función distinta.

Piensa en ello como una ciudad: tienes carreteras, sistemas de tráfico, edificios y aplicaciones que te ayudan a moverte. La blockchain funciona de forma similar. Y cuando entiendes estas capas, todo el ecosistema empieza a tener mucho más sentido.

¿Por qué las blockchains necesitan capas?

A primera vista, podrías pensar que una blockchain es simplemente una base de datos que almacena transacciones. Pero en realidad tiene que hacer mucho más:

- Almacenar datos de forma segura

- Validar transacciones

- Comunicarse a nivel global

- Mantenerse descentralizada

- Escalar para millones de usuarios

Intentar hacer todo esto en un solo lugar genera compromisos. Por eso las blockchains se diseñan en capas: para que cada parte del sistema pueda especializarse y mejorar de forma independiente.

Para entender por qué esto es importante, primero hay que conocer el principal desafío de cualquier blockchain.

El trilema de la blockchain

En el centro del diseño de blockchain existe una limitación clave conocida como el trilema de la blockchain.

Cada red intenta equilibrar tres propiedades:

- Seguridad: protección frente a ataques y fraudes

- Descentralización: ausencia de control por una única entidad

- Escalabilidad: capacidad de procesar muchas transacciones de forma rápida y barata

El problema es que es muy difícil maximizar las tres al mismo tiempo.

Imagina pagar un café de 4 € con Bitcoin. Podrías pagar más en comisiones que el propio café y esperar varios minutos. Mientras tanto, una tarjeta tarda segundos. Esto ocurre porque Bitcoin prioriza la seguridad y la descentralización sobre la velocidad.

Las nuevas blockchains intentan mejorar la escalabilidad, pero suelen hacerlo sacrificando otros aspectos. Por eso surgió una nueva idea: dividir responsabilidades en distintas capas.

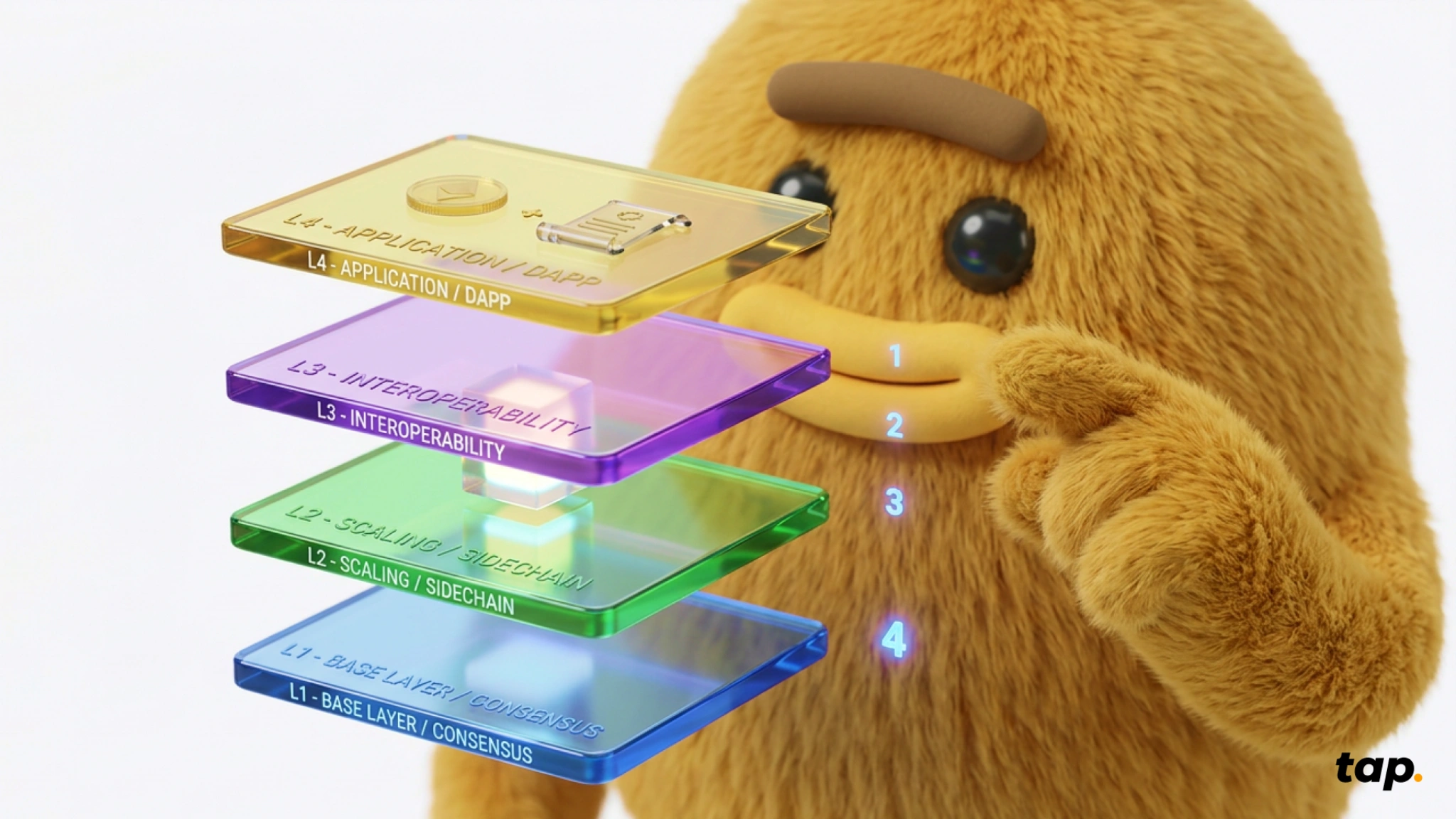

Las 5 capas fundamentales de la blockchain

Antes de hablar de Layer 1 o Layer 2, conviene entender la estructura básica:

1. Capa de infraestructura (la base)

Es el soporte físico de la red:

- Ordenadores (nodos)

- Servidores distribuidos globalmente

Estos nodos almacenan datos y mantienen la red funcionando continuamente.

2. Capa de datos (donde viven las transacciones)

Aquí se almacena toda la información:

- Transacciones

- Bloques

- Timestamps

- Firmas criptográficas

Garantiza transparencia (todo es verificable) e inmutabilidad (no se puede alterar).

3. Capa de red (comunicación)

Permite que los nodos se comuniquen entre sí:

- Comparte datos de transacciones

- Propaga nuevos bloques

Sin esta capa, la red no estaría sincronizada.

4. Capa de consenso (acuerdo)

Aquí se toman decisiones:

- Determina qué transacciones son válidas

- Define qué bloques se añaden

Ejemplos:

- Proof of Work (Bitcoin)

- Proof of Stake (Ethereum)

Es clave para mantener la confianza sin autoridad central.

5. Capa de aplicación (lo que ve el usuario)

Es la capa con la que interactúan los usuarios:

- Wallets

- Plataformas DeFi

- NFTs

- Juegos

Aquí ocurre todo lo que el usuario percibe.

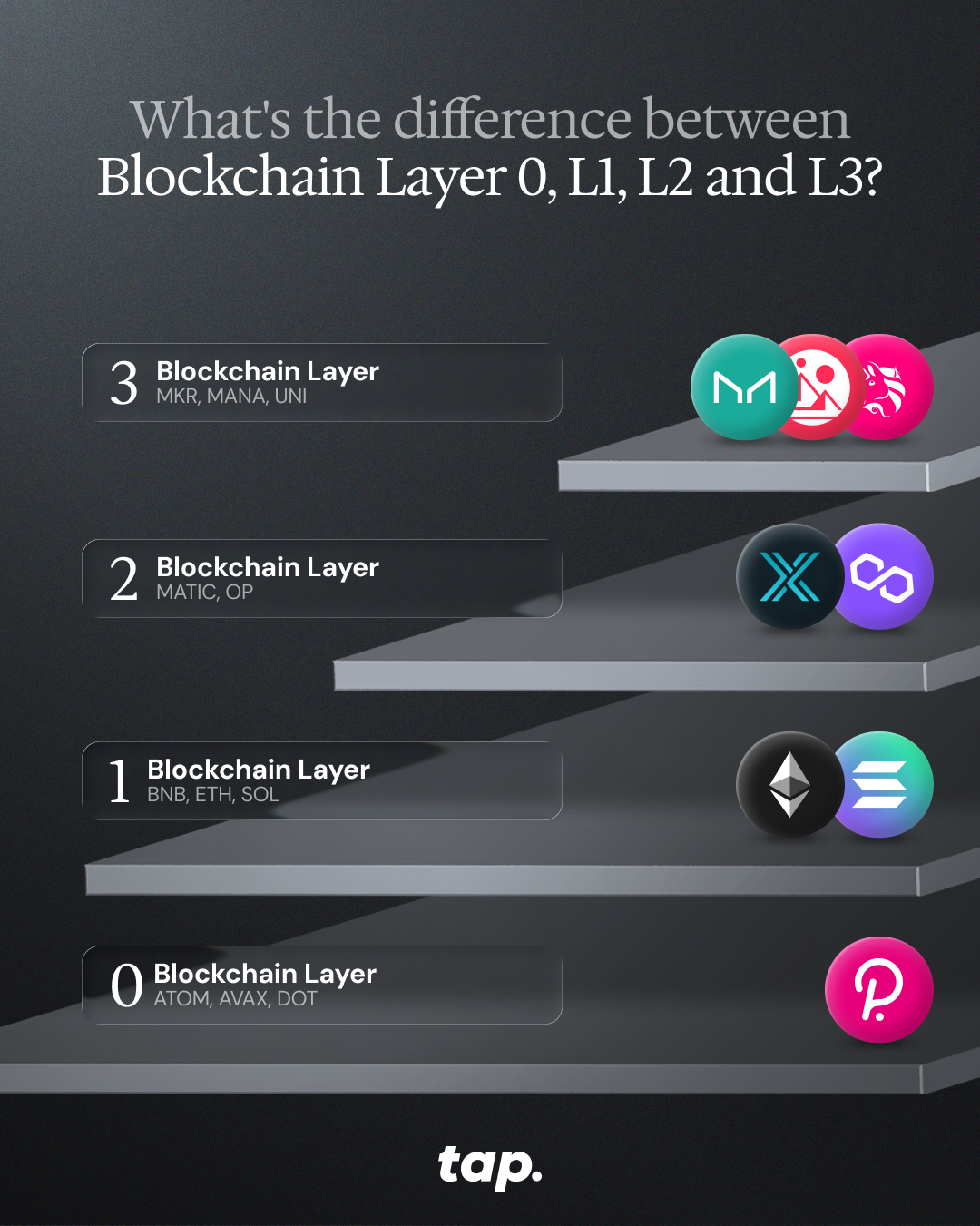

Layer 0, 1, 2 y 3: otra forma de entender las capas

Además de la estructura interna, el término “capas” también se usa para clasificar soluciones dentro del ecosistema.

Layer 0: conexión entre blockchains

Se centra en la interoperabilidad.

Proyectos como Polkadot permiten:

- Comunicación entre blockchains

- Infraestructura compartida

- Creación de nuevas redes

Es como el “internet de las blockchains”.

Layer 1: la base

Es la blockchain principal:

- Bitcoin

- Ethereum

Proporciona:

- Seguridad

- Consenso

Limitaciones:

- Baja capacidad de transacciones

- Comisiones altas

- Lentitud en momentos de congestión

Layer 2: escalabilidad

Se construye sobre Layer 1 para mejorar rendimiento.

Funcionamiento:

- Procesa transacciones fuera de la cadena

- Agrupa datos

- Envía resultados a Layer 1

Ejemplos:

- Lightning Network (Bitcoin)

- Rollups (Ethereum)

Beneficios:

- Mayor velocidad

- Menores costes

- Mejor escalabilidad

Layer 3: aplicaciones

Es donde interactúan los usuarios:

- DeFi (Uniswap, Aave)

- NFTs

- Apps sociales

- Juegos

Aquí es donde la blockchain se vuelve tangible.

Por qué las capas son más importantes que nunca

A medida que crece la adopción, también aumenta la necesidad de:

- Mejor rendimiento

- Menores costes

- Mejor experiencia de usuario

La arquitectura por capas permite:

- Innovación sin comprometer seguridad

- Escalabilidad

- Especialización

En lugar de un solo sistema haciendo todo, múltiples capas trabajan juntas.

Conclusión

Las capas de blockchain pueden parecer complejas, pero la idea es sencilla: dividir un sistema complejo en partes más eficientes.

Desde la infraestructura hasta las aplicaciones que usas cada día, cada capa cumple un papel esencial para que la blockchain sea segura, descentralizada y escalable.

Explora el mundo blockchain

Tanto si te interesan redes Layer 1 como Bitcoin o Ethereum, soluciones de escalado Layer 2 o nuevos ecosistemas Layer 0, entender cómo funcionan estas capas te ayudará a moverte con mayor confianza en el mundo cripto.

En la app puedes acceder a más de 70 criptomonedas, desde proyectos consolidados hasta plataformas DeFi innovadoras, todo en un solo lugar.

Imagina salir del supermercado y darte cuenta de que te han pagado por hacer la compra semanal. No con cupones ni puntos que caducan, sino con dinero real. Eso es el Cashback.

Por ejemplo, si gastas 200 $ en un supermercado con una tarjeta que ofrece un 2% de Cashback, recibes 4 $ de vuelta. En pocas palabras, es un reembolso sobre tus compras diarias, ya sea en un supermercado, restaurante o tienda online.

Vamos a ver paso a paso cómo funciona el Cashback, los distintos tipos de tarjetas que existen, cómo calcular tus recompensas y cuál puede ser la mejor opción para ti.

¿Cómo funciona el Cashback?

El proceso es sencillo:

- Realizas una compra con tu tarjeta de crédito.

- El comercio procesa el pago a través de una red como Visa o American Express.

- El banco emisor calcula la recompensa según el porcentaje de tu tarjeta.

- La recompensa se acumula en tu cuenta.

Normalmente, el Cashback no se recibe al instante. Las recompensas suelen reflejarse al cerrar el ciclo mensual de facturación. Si gastas 500 $ en un mes con una tarjeta al 2%, ganarás 10 $ (500 × 2% = 10 $), que aparecerán tras el cierre del extracto.

Cashback vs. anticipo de efectivo

Aunque suenen parecido, no son lo mismo:

- Cashback es una recompensa.

- Anticipo de efectivo (cash advance) es un préstamo sobre tu línea de crédito, generalmente con comisión inmediata y alto interés.

Confundirlos puede resultar caro. El anticipo genera intereses desde el primer día, mientras que el Cashback reduce tu gasto efectivo.

Cashback vs. puntos

Algunas tarjetas anuncian “cashback” pero en realidad otorgan puntos. Estos pueden convertirse a una tasa fija (por ejemplo, 1 punto = 1 céntimo) o tener valor variable según cómo los uses (viajes, tarjetas regalo, compras online). Siempre revisa las condiciones para entender el valor real.

Tipos de tarjetas con Cashback

No todas funcionan igual. Estos son los modelos más habituales:

Tarjetas de tasa fija

Ofrecen el mismo porcentaje en todas las compras, normalmente entre el 1,5% y el 2%.

Si gastas 1.000 $ al mes con una tarjeta al 2%, ganarás 20 $ (1.000 × 2% = 20 $), sin importar el tipo de gasto.

Son ideales para quienes buscan simplicidad.

Tarjetas por categorías fijas o escalonadas

Ofrecen mayor porcentaje en categorías específicas (supermercados, gasolineras, restaurantes, viajes) y un porcentaje más bajo (generalmente 1%) en el resto.

Ejemplo:

- 3% en supermercados → 500 $ × 3% = 15 $

- 1% en otros gastos → 500 $ × 1% = 5 $

- Total = 20 $

El banco define qué comercios califican, por lo que conviene revisar las condiciones.

Son adecuadas para quienes tienen patrones de gasto constantes.

Tarjetas con categorías rotativas

Ofrecen un 5% en categorías que cambian cada trimestre, normalmente con límite de gasto.

Ejemplo:

Si el límite trimestral es 1.500 $ y gastas esa cantidad al 5%, ganarás 75 $ (1.500 × 5% = 75 $). Después del límite, suele aplicarse el 1%.

Es necesario activar la categoría cada trimestre. Si no lo haces, solo se aplica el porcentaje base.

Son ideales para usuarios atentos y organizados.

Tarjetas con categoría elegible

Permiten seleccionar la categoría de bonificación cada mes o aplican automáticamente el mayor porcentaje a la categoría donde más gastas.

Si eliges restaurantes al 3% y gastas 400 $, ganarás 12 $ (400 × 3% = 12 $).

Son adecuadas para estilos de vida cambiantes.

Cómo calcular tu Cashback

La fórmula es simple:

Importe gastado × porcentaje de Cashback = recompensa

Ejemplos:

- 100 $ × 1% = 1 $

- 1.000 $ × 1,5% = 15 $

- 500 $ × 5% = 25 $

- 2.000 $ × 5% = 100 $

Ten en cuenta los límites de gasto y condiciones de categoría, que pueden reducir el porcentaje efectivo.

¿Merece la pena una tarjeta con Cashback?

Funciona mejor si pagas el saldo completo cada mes. Si mantienes deuda, los intereses (a veces superiores al 20% anual) pueden superar fácilmente las recompensas.

Ventajas

- Ganas un porcentaje sobre gastos habituales.

- Valor fijo en dinero, a diferencia de sistemas de millas variables.

- Algunas tarjetas no tienen comisión anual.

- Con el tiempo, puede compensar gastos reales.

Por ejemplo, gastar 2.000 $ al mes al 2% genera 40 $ mensuales (2.000 × 2% = 40 $), es decir, 480 $ al año.

Desventajas

- Mantener saldo genera intereses que superan las recompensas.

- Algunas tarjetas tienen cuota anual.

- Las categorías rotativas requieren gestión activa.

- Solicitar varias tarjetas puede afectar temporalmente a tu puntuación crediticia.

También conviene considerar la diferencia entre crédito y débito. La tarjeta de débito utiliza tu propio dinero y evita intereses. La de crédito ofrece recompensas y posibilidad de construir historial crediticio, pero implica riesgo si gastas más de lo que puedes pagar.

El Cashback es un incentivo, no dinero gratis. Funciona mejor cuando forma parte de una planificación financiera disciplinada.

Consejos para maximizar el Cashback

- Elige la tarjeta según tus gastos reales. Revisa tus extractos antes de decidir.

- Paga siempre el saldo completo.

- Activa las categorías rotativas a tiempo.

- Planifica compras grandes estratégicamente.

- Combina tarjetas: una de tasa fija para gastos generales y otra por categorías puede aumentar tus recompensas.

- Complementa con apps o webs de Cashback independientes.

- Evalúa bien los bonos de bienvenida para asegurarte de que el gasto requerido encaja con tu presupuesto habitual.

Obtén Cashback sin caer en la trampa del crédito

Las tarjetas de crédito con Cashback pueden parecer atractivas, pero si mantienes saldo pendiente, los intereses pueden eliminar cualquier beneficio.

Existe una alternativa: el Cashback cripto con tarjeta de débito. La tarjeta de débito de Tap te permite obtener recompensas sin endeudarte. Ganas Cashback en compras cotidianas (supermercado, café, viajes, restaurantes) sin pedir dinero prestado, sin intereses y sin riesgo de sobreendeudamiento.

Las recompensas se pagan en el token XTP y se depositan directamente en tu wallet según la cantidad de XTP que tengas bloqueada (staked). Las tasas de Cashback van del 0,5% al 8%, dependiendo del nivel. Cuantos más XTP bloquees, mayor será tu recompensa.

Si valoras la disciplina financiera y quieres obtener recompensas por tus gastos, la tarjeta de débito cripto de Tap puede ser una alternativa interesante.

¿Listo para ganar Cashback de forma más inteligente? Descarga la app de Tap y empieza a convertir tus compras en recompensas cripto hoy mismo.

Creada como la evolución natural de DAI, USDS es una stablecoin que opera dentro del ecosistema Sky Protocol (anteriormente MakerDAO) y busca combinar estabilidad de precio, transparencia y descentralización en un único activo digital.

A medida que las stablecoins desempeñan un papel cada vez más importante en las finanzas globales, USDS ofrece una alternativa a las opciones centralizadas mediante el uso de colateral respaldado por criptoactivos y smart contracts automatizados, en lugar de depender de una única empresa emisora. Más allá de la estabilidad de precio, USDS está diseñada para integrarse sin fricciones en aplicaciones de finanzas descentralizadas, ofrecer oportunidades de rendimiento a través de incentivos del protocolo y respaldar un futuro multi-chain. Para quienes buscan un dólar digital estable sin control centralizado, USDS representa un enfoque moderno para el almacenamiento y la transferencia de valor.

¿Qué es USDS?

USDS es una stablecoin respaldada por criptoactivos y vinculada al dólar estadounidense, lo que significa que su precio objetivo es aproximadamente 1 dólar en todo momento. A diferencia de los dólares digitales tradicionales emitidos por empresas centralizadas, USDS está gobernada por smart contracts y por un proceso de toma de decisiones descentralizado, en lugar de una autoridad única.

La base de USDS se sustenta en tres principios fundamentales. Primero, la estabilidad: el protocolo está diseñado para mantener a USDS cerca de su paridad con el dólar incluso en periodos de volatilidad del mercado. Segundo, la descentralización: ninguna empresa o gobierno controla su emisión, congelación o redención. Tercero, la colateralización: cada USDS en circulación está respaldado por activos cripto como ETH, USDC y activos tokenizados del mundo real depositados dentro del Sky Protocol.

En comparación con stablecoins centralizadas como USDT o USDC, USDS no depende de reservas bancarias corporativas ni de custodios off-chain. En comparación con DAI, USDS está diseñada para ofrecer mayor escalabilidad y funcionalidad multi-chain. Y a diferencia de las stablecoins puramente algorítmicas, USDS se apoya en colateral tangible en lugar de depender únicamente de incentivos de mercado. Su propósito es proporcionar un dólar digital transparente y resiliente alineado con los valores de las finanzas descentralizadas.

Cómo funciona USDS

Creación a través de Sky Vaults

USDS se crea mediante un sistema conocido como Sky Vaults. Los usuarios depositan activos de colateral aprobados en smart contracts automatizados y, a cambio, acuñan USDS. Una forma sencilla de entenderlo es imaginar que se depositan activos valiosos en una bóveda digital segura y se recibe a cambio un recibo vinculado al dólar que puede gastarse o transferirse.

El colateral aceptado incluye criptomonedas como ETH, activos estables como USDC y ciertos activos tokenizados del mundo real. Cada bóveda opera bajo reglas predefinidas que garantizan coherencia y seguridad en todo el sistema.

Estabilidad y sobrecolateralización

Para proteger la paridad con el dólar, USDS está sobrecolateralizada. Esto significa que los usuarios deben depositar más valor del que generan en USDS. Si el valor del colateral cae por debajo de ciertos umbrales, el sistema vende automáticamente parte de los activos mediante un proceso de liquidación para proteger la estabilidad general. Este margen de seguridad es una de las razones por las que USDS puede mantener su paridad sin depender de un emisor central.

Papel dentro del Sky Protocol

USDS funciona como la stablecoin central del ecosistema Sky Protocol. Da soporte a préstamos, ahorro, pagos y procesos de gobernanza dentro de la plataforma. Aunque las decisiones de gobernanza se gestionan por separado, USDS está profundamente integrada en la arquitectura y el sistema de incentivos de Sky.

Actualización de DAI a USDS

La transición de DAI a USDS está diseñada como un proceso sencillo y centrado en el usuario, alineado con las mejores prácticas de las finanzas descentralizadas modernas y la tecnología de la información. A través del sitio web oficial de Sky, los usuarios pueden conectar una wallet compatible y actualizar sus DAI a USDS mediante smart contracts.

Desde la perspectiva de la experiencia de usuario, el proceso enfatiza accesibilidad, transparencia y eficiencia. Ninguna autoridad central, banco o intermediario controla la transacción, y los usuarios conservan la plena propiedad de sus datos y activos digitales en todo momento.

Una vez completada la actualización, los holders de USDS pueden acceder de inmediato a herramientas adicionales dentro del ecosistema Sky, incluidos mecanismos de ahorro e incentivos. Para usuarios en Estados Unidos y a nivel global, esta actualización no es solo un cambio técnico, sino una mejora en cómo los productos de stablecoins descentralizadas ofrecen valor, escalabilidad y usabilidad.

USDS vs. DAI: ¿Qué ha cambiado?

USDS y DAI comparten una historia común en el sistema MakerDAO, ahora bajo el Sky Protocol. Ambas son stablecoins descentralizadas vinculadas al dólar y respaldadas por colateral on-chain. Sin embargo, USDS representa una evolución arquitectónica y estratégica centrada en escalabilidad, gobernanza e incentivos mejorados para el usuario final.

DAI fue un producto fundacional en DeFi, permitiendo a los usuarios bloquear activos cripto en smart contracts para generar una moneda digital estable. USDS perfecciona ese modelo mediante mejoras tecnológicas, compatibilidad multi-chain ampliada y nuevas estructuras de recompensas que aumentan la eficiencia del capital y la participación de los usuarios.

Desde una perspectiva de gestión de riesgos y políticas, USDS está diseñada para alinearse mejor con expectativas regulatorias sin perder su carácter descentralizado. Incorpora lecciones aprendidas de la volatilidad del mercado, crisis anteriores y desafíos en el diseño de stablecoins. En resumen, DAI sentó las bases; USDS aplica mecanismos actualizados de diseño, gobernanza e incentivos para responder a las necesidades actuales de DeFi.

USDS frente a otras stablecoins

USDS se diferencia principalmente en cómo gestiona el control, el respaldo y la transparencia.

Las stablecoins centralizadas como USDT y USDC son emitidas por empresas que gestionan reservas fiat y pueden congelar fondos si la normativa lo exige. Las stablecoins algorítmicas dependen principalmente de incentivos de mercado y ajustes de oferta basados en código, lo que puede introducir mayor riesgo sistémico.

USDS, por el contrario, es descentralizada y respaldada por colateral. Sus reservas son visibles on-chain y ninguna entidad individual tiene autoridad unilateral sobre los fondos de los usuarios. Esto reduce el riesgo de censura y mejora la transparencia, aunque también hace que el sistema sea algo más complejo que las alternativas centralizadas. En conjunto, USDS se sitúa entre las stablecoins institucionales y los diseños algorítmicos experimentales, ofreciendo un equilibrio entre estabilidad y descentralización.

Cómo obtener y utilizar USDS

Existen varias formas de adquirir y usar USDS, dependiendo del nivel de experiencia del usuario.

La forma más sencilla es comprar USDS en un exchange descentralizado utilizando otra criptomoneda, opción generalmente adecuada para principiantes. Los holders de DAI pueden convertir DAI a USDS en una proporción uno a uno a través de plataformas compatibles. Los usuarios más avanzados pueden acuñar USDS directamente depositando colateral en los Sky Vaults.

Una vez adquirida, USDS puede utilizarse como reserva estable de valor, como par de trading en mercados DeFi o como medio de pago para transferir valor sin exposición a la volatilidad de precios. También desempeña un papel en la provisión de liquidez y en protocolos de préstamo dentro del ecosistema DeFi.

Generar rendimiento con USDS

USDS ofrece oportunidades de rendimiento dentro del Sky Protocol. Una opción es la Sky Savings Rate, que permite bloquear USDS en un smart contract para obtener recompensas variables con el tiempo. Este enfoque es similar a una cuenta de ahorro, aunque los rendimientos fluctúan según las condiciones del protocolo.

Otro mecanismo son las Sky Token Rewards, que proporcionan incentivos adicionales a los usuarios que participan activamente en el ecosistema. Estas recompensas pueden cambiar y no están garantizadas, pero añaden una capa adicional de valor para usuarios comprometidos. Como ocurre con todos los mecanismos de rendimiento en DeFi, los retornos dependen de las condiciones de mercado y de decisiones de gobernanza.

USDS dentro del ecosistema Sky Protocol

Sky Protocol es una plataforma de finanzas descentralizadas construida sobre el legado de MakerDAO. Dentro de este ecosistema, USDS actúa como unidad principal de transferencia de valor. Interactúa con procesos de gobernanza, programas de incentivos y otras aplicaciones descentralizadas compatibles con Sky.

Aunque los tokens de gobernanza y las actualizaciones del protocolo operan en segundo plano, los usuarios no necesitan conocimientos técnicos profundos para beneficiarse de USDS. Su diseño prioriza la usabilidad manteniéndose fiel a principios descentralizados y a una arquitectura transparente.

Conclusión

USDS es una stablecoin descentralizada diseñada para ofrecer un dólar digital fiable sin control centralizado. Como sucesora de DAI, se apoya en un modelo probado al tiempo que introduce mejoras en escalabilidad e integración dentro del Sky Protocol.

Al combinar colateral respaldado por criptoactivos, gestión de riesgos automatizada y transparencia on-chain, USDS ofrece una alternativa tanto a las stablecoins centralizadas como a las algorítmicas. A medida que DeFi continúa evolucionando, USDS representa una opción práctica para usuarios que buscan estabilidad de precio con gobernanza descentralizada.

Probablemente hayas oído hablar de MakerDAO, el protocolo detrás de MKR y la stablecoin DAI. Ahora llega su siguiente etapa: Sky.

Sky es la nueva identidad del ecosistema MakerDAO, uno de los proyectos más consolidados de las finanzas descentralizadas (DeFi). Lanzado en 2024, representa la evolución del sistema de stablecoin y gobernanza de Maker, con un enfoque más claro en accesibilidad, usabilidad y experiencia del usuario.

Sky mantiene el papel histórico de MakerDAO en DeFi, pero introduce un ecosistema renovado centrado en gobernanza y control descentralizado de activos digitales.

Sky vs. Skycoin: aclarando la confusión

A pesar de la similitud en el nombre, Sky (SKY) y Skycoin (SKY) son proyectos de criptomonedas completamente diferentes. Sky es el ecosistema renombrado de MakerDAO, centrado en finanzas descentralizadas, stablecoins y gobernanza en Ethereum. Skycoin, por otro lado, es un proyecto blockchain independiente con su propia plataforma de computación, economía de tokens y equipo de desarrollo.

Difieren en caso de uso, valor de mercado, tecnología y comunidad. La función principal de Sky es facilitar el ahorro descentralizado, los préstamos y la gobernanza a través de USDS y SKY, mientras que Skycoin se enfoca en la arquitectura de red y una infraestructura blockchain alternativa. Sus precios, capitalización bursátil y volumen de negociación tampoco guardan relación alguna.

Entender esta distinción es importante tanto para inversores como para usuarios finales a fin de evitar confusiones al investigar en exchanges, tendencias de mercado u oportunidades de inversión.

¿Cómo funciona Sky? Características principales

Sky opera como un servicio de finanzas descentralizadas sin ninguna autoridad central que controle los fondos de los usuarios. Una de sus funciones principales es el staking de USDS, mediante el cual los usuarios depositan USDS en el protocolo para obtener rendimiento a través de mecanismos como la Tasa de Ahorro de Sky y las Recompensas en Token Sky. Esto permite a los usuarios generar intereses sobre una divisa digital anclada al dólar manteniendo el control total de sus activos.

La gobernanza se gestiona a través del token SKY. Los titulares del token participan en la votación sobre actualizaciones del protocolo, ajustes de comisiones, políticas de colateral y decisiones de gestión de riesgos. Este proceso de votación garantiza la transparencia y una toma de decisiones liderada por la comunidad en todo el ecosistema.

Sky también presenta una estructura modular conocida como Sky Stars, proyectos independientes que operan dentro del ecosistema más amplio manteniendo su autonomía. Este diseño favorece la innovación, la escalabilidad y un desarrollo más ágil, todo ello manteniendo la alineación con los servicios financieros centrales de Sky.

Cómo actualizar de MKR a SKY

Como parte del cambio de marca de MakerDAO, MKR ha sido reemplazado por SKY como el único token de gobernanza del Protocolo Sky. Si bien MKR podría seguir negociándose en mercados secundarios, solo SKY otorga acceso a la gobernanza, al staking y a la participación en el ecosistema Sky.

El proceso de actualización se gestiona directamente a través del sitio web oficial de Sky, garantizando una experiencia no custodiada y controlada por el usuario. Los usuarios simplemente conectan su monedero de Ethereum, inician la actualización y convierten MKR a SKY con la proporción fija de 1 MKR = 24.000 SKY. Durante todo el proceso, los usuarios mantienen el control total de sus activos.

Se recomienda encarecidamente la actualización a cualquier persona que desee seguir votando, delegando o interactuando con los mecanismos de gobernanza y recompensas de Sky. Poseer SKY desbloquea funcionalidades como la votación en el protocolo, la participación en la toma de decisiones y el acceso a funcionalidades relacionadas con el staking vinculadas al ecosistema Sky.

También es importante señalar que el protocolo introduce una penalización temporal por actualizaciones demoradas. A partir del 18 de septiembre de 2025, la cantidad de SKY recibida por cada MKR disminuirá gradualmente, comenzando con una reducción del 1% y aumentando con el tiempo. Actualizar antes de esta fecha garantiza que los usuarios reciban el valor de conversión completo sin penalización alguna.

En resumen, aunque MKR sigue siendo un activo reconocible, SKY es el token que impulsará el ecosistema Sky en el futuro, y la actualización es la vía recomendada para quienes deseen mantenerse alineados con el desarrollo futuro del protocolo.

Valor actual del token SKY y desempeño de mercado

El token SKY desempeña un papel central en la gobernanza y en los incentivos del protocolo. Tras el cambio de marca, MKR se convirtió en SKY con una proporción de 1:24.000, lo que redujo significativamente el precio unitario y mejoró la accesibilidad para los participantes individuales.

En el momento de redactar este artículo, su capitalización bursátil la sitúa entre las 50 criptomonedas principales, junto a tokens de gobernanza DeFi bien consolidados. Sin embargo, como todas las criptomonedas, SKY experimenta volatilidad de precios influenciada por las condiciones generales del mercado y las tendencias de adopción de DeFi.

Conclusión

Sky es el siguiente capítulo de MakerDAO, reinventado para ofrecer un ecosistema de finanzas descentralizadas más accesible y escalable. Al combinar USDS para ahorros y transacciones con SKY para la gobernanza y la toma de decisiones, Sky pretende empoderar a los usuarios con un mayor control, transparencia y autonomía financiera.

En 2025, millones de personas dejaron de esperar a que el sistema financiero ofreciera alternativas más rápidas y baratas para los pagos. Simplemente empezaron a usar otra cosa. Millones de usuarios en 15 países han comenzado a recibir parte de sus ingresos en stablecoins, y no piensan volver atrás.

Stablecoins: una moneda de uso cotidiano

Una nueva encuesta realizada por YouGov a 4.658 usuarios cripto y potenciales holders aporta datos concretos a lo que antes era más anecdótico que estadístico. Los resultados dibujan una imagen de las stablecoins muy distinta de la percepción especulativa y volátil que tradicionalmente se asocia al mundo cripto.

El 39% de los encuestados afirmó que ya recibe ingresos en stablecoins, representando de media aproximadamente el 35% de sus ganancias anuales. No se trata necesariamente de ingresos secundarios: para muchos, es su fuente principal.

El uso en el día a día también está creciendo. Más de una cuarta parte de los holders de stablecoins (27%) las utiliza para compras habituales, manteniendo una media de unos 200 dólares en sus wallets digitales para transacciones cotidianas. Más de la mitad declaró haber elegido deliberadamente un comercio por aceptar stablecoins. En mercados emergentes, esa cifra asciende al 60%.

La geografía de la adopción es reveladora. La propiedad es mayor en economías de ingresos bajos y medios: el 60% de los encuestados en esas regiones posee stablecoins, frente al 45% en países más ricos. África destaca especialmente, con la tasa de propiedad más alta a nivel mundial (79%) y el mayor crecimiento interanual.

El patrón tiene lógica: donde los bancos son lentos, las remesas costosas y las divisas inestables, un activo digital vinculado al dólar que viaja de forma instantánea y barata deja de ser una novedad para convertirse en una herramienta esencial. Los usuarios que realizan transferencias internacionales afirmaron ahorrar aproximadamente un 40% en comisiones frente a los servicios tradicionales de remesas. Esa cifra cobra especial relevancia cuando se envía dinero a casa cada mes.

Las razones para utilizar stablecoins no son ideológicas. Los principales motivos son menores costes de transacción, mayor seguridad y accesibilidad global. No se trata de un movimiento impulsado por idealistas cripto, sino de un cambio pragmático por parte de personas que han encontrado una herramienta que funciona mejor para su realidad.

La demanda de una mayor integración con el sistema financiero tradicional también es evidente. El 77% de los encuestados afirmó que abriría una wallet de stablecoins si su banco o proveedor fintech principal la ofreciera, y el 71% querría una tarjeta de débito vinculada a su saldo en stablecoins. La brecha de infraestructura entre cripto y banca convencional es, al parecer, algo que muchos usuarios estarían encantados de ver desaparecer.

Expansión estable

El momento también es clave. La aprobación de la GENIUS Act en Estados Unidos y la implementación de la regulación MiCA en Europa han aportado un marco regulatorio que está acelerando los movimientos corporativos en el sector. La plataforma de nóminas Deel anunció recientemente que ofrecerá pagos en stablecoins, comenzando por trabajadores en Reino Unido y la Unión Europea antes de expandirse a Estados Unidos.

El cambio también es visible on-chain, con un aumento drástico en el volumen de transacciones con stablecoins en los últimos años, alcanzando cifras de billones. El mercado total de stablecoins ronda actualmente los 307.000 millones de dólares, frente a los 260.000 millones en el momento en que se aprobó la GENIUS Act.

La trayectoria es difícil de ignorar, y no muestra señales de desaceleración. El crecimiento es real y, cada vez más, también lo son las nóminas pagadas en stablecoins.

Conclusión

Lo que comenzó como una herramienta de nicho para traders cripto se ha convertido en una columna vertebral financiera para millones de personas en todo el mundo: más rápida, más barata y más accesible que los sistemas que empieza a reemplazar.

Con mayor claridad regulatoria a ambos lados del Atlántico, empresas e instituciones ya no permanecen al margen. Bancos, fintechs y plataformas de nómina están entrando en el ecosistema, y los usuarios están preparados para recibirlos. Para ellos, las stablecoins ya no son un experimento. Son simplemente la forma en que funciona el dinero hoy.

En un ecosistema blockchain donde la transparencia suele ser la norma, la privacidad sigue siendo uno de los mayores desafíos de Web3. COTI, acrónimo de Currency Of The Internet, se posiciona como una de las capas de privacidad más rápidas y ligeras de Web3, diseñada para permitir transacciones financieras confidenciales sin sacrificar velocidad, usabilidad ni cumplimiento normativo. Construido como una plataforma de computación de Capa 2 sobre Ethereum, COTI permite a empresas, instituciones y usuarios finales trabajar con datos privados mientras se benefician de la seguridad de la blockchain.

En este artículo exploraremos qué es COTI, cómo funciona su tecnología y por qué su enfoque en privacidad, escalabilidad y cumplimiento regulatorio está ganando interés en el ámbito de las finanzas descentralizadas, aplicaciones empresariales e industrias reguladas.

¿Qué es COTI?

COTI (Currency Of The Internet) es una infraestructura de privacidad de Capa 2 construida sobre Ethereum que permite transacciones y smart contracts confidenciales y programables. Lanzado originalmente en 2017 como una red enfocada en pagos, COTI ha evolucionado significativamente. Con su actualización V2, el protocolo dio un giro hacia capacidades avanzadas de privacidad y computación.

Hoy en día, COTI funciona como software de aplicación y herramienta blockchain diseñada para soportar actividad financiera privada, intercambio de datos conforme a la normativa y procesos empresariales escalables.

Al combinar compatibilidad con Ethereum y computación que preserva la privacidad, COTI permite a desarrolladores e instituciones crear aplicaciones DeFi, sistemas de stablecoins y servicios empresariales donde información sensible como saldos, precios o identidades de usuario permanece protegida.

¿Cómo funciona COTI?

En el núcleo de la tecnología de COTI se encuentra una metodología criptográfica llamada Garbled Circuits, una forma de computación segura multiparte (secure multiparty computation). En términos sencillos, esta técnica permite que un programa procese datos cifrados sin revelar las entradas, variables o atributos subyacentes. Es decir, la lógica de una transacción puede ejecutarse de forma privada mientras produce resultados verificables.

En comparación con soluciones tradicionales como las pruebas de conocimiento cero (zero-knowledge proofs), el enfoque de COTI prioriza eficiencia y velocidad. Los Garbled Circuits permiten cálculos hasta 3.000 veces más rápidos que sistemas basados en ZK-SNARK, con menor latencia y menores requisitos de almacenamiento. Este rendimiento hace que COTI sea adecuado para servicios reales que requieren pagos rápidos, lógica de precios y experiencias de usuario escalables.

Desde el punto de vista arquitectónico, COTI opera como una red de Capa 2 que procesa transacciones off-chain para garantizar privacidad y eficiencia, y posteriormente liquida los resultados finales en Ethereum. Este diseño aprovecha la seguridad y descentralización de Ethereum evitando congestión y comisiones elevadas. Además, al mantener compatibilidad con la EVM, los desarrolladores pueden desplegar contratos inteligentes en Solidity e integrar COTI en flujos Web3 ya existentes.

La privacidad en COTI es programable. Los datos pueden mantenerse completamente privados, divulgarse selectivamente para auditorías o compartirse con reguladores e instituciones cuando sea necesario. Este equilibrio entre protección de datos y cumplimiento normativo es clave en su propuesta de valor.

Características y beneficios clave

La principal característica de COTI es la privacidad programable, que permite a los desarrolladores definir quién puede acceder a determinada información dentro de una transacción financiera o proceso empresarial. Esto resulta especialmente relevante para bancos, fintechs y modelos de negocio basados en suscripción que deben proteger datos de clientes cumpliendo normativas.

La velocidad y la escalabilidad son también beneficios centrales. Al procesar datos off-chain y minimizar la carga computacional, COTI admite alto volumen de transacciones y experiencias fluidas en aplicaciones móviles. Su arquitectura está pensada para pagos, programas de fidelización, wallets digitales y plataformas empresariales.

Además, el diseño de COTI favorece la gobernanza y la transparencia. Aunque los detalles de las transacciones permanezcan privados, el sistema puede proporcionar pruebas verificables cuando sea necesario, facilitando gestión de riesgos, protección del consumidor y adopción institucional.

¿Qué problemas resuelve COTI?

Las blockchains públicas exponen por defecto los datos de las transacciones, lo que genera desafíos para empresas, proveedores sanitarios, bancos y usuarios que necesitan confidencialidad. Esta transparencia puede revelar estrategias de precios, saldos bancarios, límites de crédito o información médica y financiera sensible.

COTI aborda este problema al permitir transacciones financieras privadas que siguen siendo auditables y conformes a la normativa. En DeFi, posibilita que los usuarios negocien, presten o gestionen stablecoins sin exponer saldos o estrategias. En entornos empresariales, facilita contabilidad confidencial, gestión de tesorería y compartición segura de datos en cadenas de suministro.

Su tecnología también ha despertado interés institucional, incluyendo colaboraciones con bancos centrales y empresas que exploran sistemas de moneda digital regulada. La capacidad de equilibrar privacidad, velocidad y cumplimiento hace que COTI sea relevante para tokenización de activos del mundo real, gestión de datos sanitarios e integración empresarial.

El token COTI

La criptomoneda COTI es el activo digital nativo que impulsa la red. Se utiliza para pagar comisiones de transacción, participar en la gobernanza y realizar staking dentro del ecosistema. COTI existe en múltiples redes, incluyendo su Trustchain nativa y Ethereum como token ERC-20, lo que ofrece flexibilidad en almacenamiento y uso.

Con un suministro total aproximado de 2.600 millones de tokens, COTI incentiva la participación en la red y alinea el uso a largo plazo con la demanda de computación privada y servicios financieros. El token desempeña un papel central en la seguridad de la red y en la alineación de intereses de los participantes.

¿Cómo empezar con COTI?

COTI está disponible en varios exchanges de criptomonedas de gran relevancia. La mayoría de plataformas admiten la versión ERC-20, que puede almacenarse en wallets compatibles, tanto hardware como software.

Para desarrolladores y empresas interesadas en integrarse con la red, COTI ofrece herramientas, documentación y recursos técnicos que permiten desplegar contratos inteligentes privados, sistemas de pago y aplicaciones descentralizadas utilizando flujos de desarrollo Web3 conocidos.

Conclusión

COTI representa un enfoque práctico hacia la privacidad en blockchain, combinando computación rápida, arquitectura escalable y diseño consciente de la regulación. Al aprovechar Garbled Circuits y la tecnología de Capa 2 de Ethereum, permite transacciones financieras confidenciales y procesamiento de datos sin sacrificar eficiencia ni cumplimiento normativo.

A medida que la privacidad adquiere mayor relevancia en DeFi, servicios empresariales e industrias reguladas, el equilibrio entre velocidad, gobernanza y usabilidad de COTI lo posiciona como una capa de infraestructura relevante dentro del ecosistema Web3 en evolución.

El intercambio de activos digitales en blockchains públicas ha sido uno de los grandes desafíos de las finanzas descentralizadas: ¿cómo permitir un trading eficiente peer-to-peer sin depender de intermediarios centralizados? En Ethereum, los primeros exchanges descentralizados se enfrentaron a comisiones de gas elevadas, liquidaciones lentas y liquidez fragmentada. 0x Protocol nació precisamente para resolver ese problema.

Lanzado en 2017 por Will Warren y Amir Bandeali, 0x Protocol es un proyecto de infraestructura blockchain de código abierto diseñado para potenciar el trading descentralizado de criptomonedas. En lugar de funcionar como un marketplace propio, 0x proporciona las herramientas y estándares necesarios para que desarrolladores creen exchanges descentralizados, wallets y aplicaciones financieras.

En esencia, 0x permite transacciones financieras peer-to-peer manteniendo el control de los activos en manos del usuario. El protocolo está gobernado por su token nativo ERC-20, ZRX, que desempeña un papel en la gobernanza y en los incentivos de liquidez. Aunque 0x Labs, la empresa desarrolladora original, recibió una sanción regulatoria en 2023, el protocolo continúa operando como infraestructura descentralizada dentro del ecosistema Ethereum.

Cómo funciona 0x Protocol

La arquitectura híbrida explicada

0x utiliza una arquitectura híbrida que separa la coordinación del trade de su liquidación. Este diseño equilibra eficiencia y seguridad, dos prioridades que a menudo compiten en las finanzas basadas en blockchain.

Las órdenes de compra y venta se crean y comparten off-chain, es decir, no se registran inmediatamente en la blockchain de Ethereum. Esto reduce significativamente los costes de transacción y la congestión de la red. Sin embargo, la liquidación final del trade se realiza on-chain mediante smart contracts, garantizando transparencia, cifrado y ejecución sin necesidad de confianza.

Una analogía útil sería un tablón de anuncios digital: las ofertas se publican y descubren fuera de la cadena, pero cuando ambas partes aceptan, el intercambio final se registra en la blockchain de forma segura.

Makers, Takers y Relayers

0x define tres roles principales dentro de su metodología de exchange descentralizado:

- Makers: crean órdenes de trade, especificando el par de activos, precio y cantidad. Contribuyen a la liquidez del mercado.

- Takers: ejecutan esas órdenes aceptando el precio especificado.

- Relayers: aplicaciones o servicios que alojan libros de órdenes y facilitan la distribución de las mismas. No custodian fondos ni ejecutan trades; simplemente ayudan a descubrir órdenes y pueden cobrar comisiones.

Flujo de ejecución de una operación

- Un maker crea y firma una orden off-chain.

- La orden se comparte directamente o a través de un relayer.

- Un taker envía la orden a la blockchain de Ethereum.

- Un smart contract de 0x verifica firmas, condiciones de precio y variables de liquidación.

- Los activos se intercambian de forma atómica entre wallets.

Este enfoque permite a 0x soportar alto volumen de trading manteniendo descentralización y seguridad.

El token ZRX en profundidad

Derechos de gobernanza

ZRX es el token de gobernanza nativo de 0x Protocol. Fue lanzado mediante una ICO en agosto de 2017 y sigue el estándar ERC-20 de Ethereum.

Los poseedores pueden votar en propuestas de mejora del protocolo, conocidas como ZEIPs (0x Improvement Proposals). Estas propuestas abarcan actualizaciones técnicas, ajustes de parámetros y decisiones relacionadas con la tesorería. La votación se realiza off-chain para evitar costes de gas, utilizando un sistema de snapshot para prevenir manipulaciones. Cada token equivale a un voto.

Staking e incentivos de liquidez

ZRX también incentiva la provisión de liquidez. Los market makers pueden hacer staking de ZRX para recibir recompensas derivadas de las comisiones generadas por el protocolo. Estas comisiones se liquidan en ETH y se distribuyen en función del volumen de trading.

A diferencia de sistemas proof-of-stake que recompensan la validación de bloques, el staking en 0x incentiva la participación activa en mercados descentralizados. Los holders pueden delegar sus ZRX en pools gestionados por market makers y compartir recompensas.

Base técnica de 0x Protocol

0x está construido sobre la blockchain de Ethereum y utiliza smart contracts escritos en Solidity. Sus contratos principales son open-source, auditables públicamente y sometidos a pruebas rigurosas para minimizar vulnerabilidades.

El protocolo es compatible con wallets Ethereum estándar y soporta tokens ERC-20, stablecoins como Tether y otros activos tokenizados. Ofrece herramientas para desarrolladores, como la 0x API y librerías JavaScript, que facilitan su integración en aplicaciones, páginas web y marketplaces.

Aunque Ethereum es su capa principal de liquidación, 0x ha mostrado interés en expandirse a entornos multi-chain a medida que evoluciona la infraestructura blockchain.

Casos de uso y ecosistema

0x funciona como infraestructura financiera más que como producto de consumo directo. Sus servicios están integrados en numerosas aplicaciones descentralizadas.

Casos de uso habituales incluyen:

- Agregadores DEX como Matcha

- Swaps integrados en wallets

- Mesas OTC

- Protocolos DeFi con funcionalidad de trading integrada

- Marketplaces NFT y plataformas de gaming

Los desarrolladores valoran 0x por su diseño abierto, acceso a liquidez agregada (incluyendo fuentes como Uniswap) y su liquidación eficiente en gas. Con el tiempo, el protocolo ha facilitado miles de millones de dólares en volumen acumulado, consolidándose como infraestructura clave de DeFi.

Ventajas y limitaciones

Beneficios

- Reducción de costes gracias a órdenes off-chain

- Liquidación segura on-chain

- Modelo no custodial: los usuarios mantienen control de sus activos

- Diseño modular que facilita integración

- Código abierto y gobernanza comunitaria

Desafíos

- Dependencia de un ecosistema activo de relayers para mantener liquidez

- Riesgo inherente a smart contracts

- Incertidumbre regulatoria

- Competencia creciente de otros protocolos DEX y agregadores

Tokenomics de ZRX

ZRX tiene un suministro máximo de 1.000 millones de tokens, con aproximadamente 847 millones en circulación. Su capitalización y precio fluctúan según tendencias del mercado cripto y el uso del protocolo.

Desde su ICO en 2017, el token ha experimentado alta volatilidad, reflejando ciclos del mercado más amplios. Está disponible en exchanges importantes como Binance, Coinbase y Kraken.

Como cualquier activo digital, ZRX conlleva riesgos asociados a demanda de mercado, regulación y evolución tecnológica. Esta información no constituye asesoramiento financiero ni legal.

Situación regulatoria y perspectivas

En 2023, ZeroEx, Inc. resolvió una acción regulatoria relacionada con actividad de trading no registrada y pagó una multa. Sin embargo, el protocolo 0x no fue cerrado y continúa operando como infraestructura descentralizada gobernada por su comunidad. De cara al futuro, 0x compite en un entorno DeFi cada vez más dinámico, pero mantiene relevancia como capa neutral de liquidez y liquidación. Su evolución dependerá de la adopción por desarrolladores, decisiones de gobernanza y el desarrollo regulatorio global.

Conclusión

0x Protocol ocupa una posición única en las finanzas descentralizadas como capa de intercambio peer-to-peer. Su arquitectura híbrida off-chain/on-chain aborda retos históricos de eficiencia y coste sin sacrificar seguridad ni descentralización.

El token ZRX alinea la participación de la comunidad con el crecimiento del protocolo. A pesar de presiones regulatorias pasadas, 0x sigue siendo una pieza clave de infraestructura Web3 que permite a desarrolladores construir servicios financieros flexibles y escalables en Ethereum y más allá.

¿Dónde conseguir ZRX?

Si te interesa ZRX y su papel en la infraestructura de exchanges descentralizados y el trading on-chain, puedes encontrarlo en la app, junto a una amplia gama de otras criptomonedas.

El mercado cripto se mueve rápido, pero hay un componente que ha moldeado silenciosamente la forma en que se realiza el trading hoy en día: los automated market makers. Mucho antes de que los AMM se convirtieran en el estándar, Bancor Network introdujo una nueva forma de automatizar la liquidez, reducir el deslizamiento y permitir intercambios sin depender de libros de órdenes. Hoy, a medida que las finanzas descentralizadas evolucionan, Bancor sigue siendo uno de los sistemas más influyentes del sector, valorado no solo por su historia, sino también por su innovación continua en diseño de liquidez, tokenización y control de riesgos.

Tanto si estás explorando aplicaciones descentralizadas por primera vez como si llevas años interactuando con activos digitales, entender Bancor te ayuda a comprender cómo funciona la infraestructura de liquidez moderna que opera detrás de escena.

¿Qué es Bancor Network (BNT)?

Bancor Network es un protocolo de liquidez descentralizado diseñado para optimizar el intercambio de tokens mediante automatización, en lugar del emparejamiento tradicional de órdenes. La plataforma permite a los usuarios intercambiar criptomonedas directamente desde sus wallets, utilizando smart contracts en lugar de intermediarios. En vez de depender de compradores y vendedores que coincidan en tiempo real, Bancor emplea un modelo matemático para mantener la liquidez del mercado, regular la oferta y la demanda y permitir un volumen de trading continuo.

En el centro de este sistema se encuentra Bancor Network Token (BNT), la criptomoneda nativa del protocolo que actúa como activo conector central. BNT ayuda a unificar la liquidez entre pools, contribuye a una ejecución más estable de las operaciones y es un componente clave del diseño de liquidez inteligente de Bancor. El proyecto fue lanzado por un equipo de innovadores que imaginó una forma más eficiente de operar los mercados digitales, mucho antes de que el DeFi se consolidara a nivel global.

Cómo funciona Bancor Network

Automated market making (AMM) y liquidez inteligente

Bancor se basa en el concepto de automated market making, donde los pools de liquidez, y no los traders humanos, determinan los tipos de cambio. Cuando un usuario intercambia un token por otro, un smart contract ajusta automáticamente los balances y los precios según la oferta disponible en el pool.

Bancor fue pionero en este modelo a través de lo que originalmente denominó Smart Tokens, un mecanismo que mantenía uno o varios activos de reserva y utilizaba una fórmula para calcular los cambios de precio. Este diseño permitió liquidaciones instantáneas, mejorando la eficiencia general y reduciendo la fricción asociada a los mercados tradicionales.

Liquidez unificada a través de BNT

Uno de los elementos que distingue a Bancor es el uso de BNT como activo central. Cada vez que se realiza una operación, el sistema utiliza BNT como puente entre los pares. Esta estructura:

- Garantiza liquidez incluso para tokens con menor capitalización

- Reduce el deslizamiento al distribuir la liquidez de forma más eficiente

- Facilita estrategias de trading automatizadas y actividades de arbitraje

Gracias a esta arquitectura, Bancor actúa como un motor de liquidez que escala con la demanda y mantiene una ejecución fluida para los usuarios finales.

Liquidez continua sin libros de órdenes

La mayoría de los exchanges, incluidos algunos descentralizados, dependen de libros de órdenes que emparejan compras y ventas de forma dinámica. Bancor sustituye este modelo por:

- Precios programáticos

- Cálculos en tiempo real

- Balanceo automático de liquidez

Este enfoque mejora la accesibilidad y hace que el trading se sienta más intuitivo, similar a una experiencia de clic y ejecución, en lugar de una herramienta financiera compleja.

Principales características de Bancor Network

Menor deslizamiento y mejor liquidez de mercado

Al mantenerse la liquidez activa en todo momento, los usuarios pueden realizar intercambios con menor deslizamiento en comparación con exchanges descentralizados de bajo volumen. El protocolo ajusta los precios automáticamente según la oferta y la demanda, permitiendo transiciones de valor más suaves.

Acceso sin permisos

Bancor opera como una aplicación descentralizada y de código abierto. Cualquier persona puede:

- Intercambiar tokens

- Proporcionar liquidez

- Seguir el rendimiento de los pools

- Participar en la gobernanza

No se requieren documentos de identidad, registros de cuenta ni aprobaciones centralizadas, lo que refuerza los principios de transparencia y autonomía del ecosistema cripto.

Incentivos de liquidez

Los usuarios que aportan activos a los pools de liquidez reciben recompensas generadas por las comisiones de trading. Esto crea:

- Un mecanismo de ingresos pasivos para proveedores de liquidez

- Pools más sólidos para los traders

- Un ecosistema más resiliente en general

Diseño cross-chain

Aunque se originó en Ethereum, la infraestructura de Bancor se ha diseñado con la interoperabilidad en mente. Esto encaja con la evolución del sector, donde los activos digitales necesitan moverse entre redes de forma flexible para fomentar la eficiencia y la innovación.

Seguridad, auditorías y gestión de riesgos

La seguridad es un elemento central en el diseño del protocolo. Bancor emplea:

- Verificación formal

- Auditorías continuas de smart contracts

- Programas de recompensas por detección de errores

- Revisiones de seguridad a nivel de aplicación

Estos sistemas ayudan a proteger a los proveedores de liquidez, refuerzan la integridad de la red y garantizan la fiabilidad de los datos a lo largo del tiempo.

Como en cualquier protocolo de liquidez, existen riesgos, principalmente relacionados con la volatilidad, las fluctuaciones del mercado y la pérdida impermanente. Bancor ha desarrollado históricamente mecanismos para mitigar estas exposiciones, aunque ningún sistema puede eliminar por completo los riesgos en entornos de mercado inciertos.

Uso de Bancor: wallets, trading y experiencia de usuario

Al ser un token ERC-20, BNT es compatible con una amplia variedad de wallets de criptomonedas en Android, iOS, macOS y entornos de escritorio. Los usuarios suelen elegir entre:

- Wallets físicas para máxima seguridad

- Wallets de software para un uso cotidiano más cómodo

- Wallets web para intercambios rápidos y ajustes de portafolio

Una vez conectados, pueden realizar intercambios, consultar gráficos de rendimiento, gestionar posiciones de liquidez o explorar funciones de gobernanza. La interfaz de Bancor está diseñada para reducir la fricción y adaptarse tanto a usuarios nuevos como a perfiles más experimentados.

Por qué Bancor sigue siendo relevante en un mercado DeFi competitivo

Bancor fue uno de los primeros proyectos en demostrar cómo los sistemas de trading automatizados podían transformar los mercados digitales. Hoy, su influencia se refleja en gran parte del ecosistema DeFi.

Entre sus principales aportes se incluyen:

- El establecimiento de la metodología AMM

- La mejora en el diseño de liquidez

- La demostración del trading descentralizado en tiempo real

- La evolución de modelos modernos de tokenomics

- Un modelo de referencia para la liquidez multi-chain

En un entorno donde la innovación avanza rápidamente, Bancor continúa adaptando sus versiones de software, actualizando su infraestructura y refinando su sistema de gobernanza. Su permanencia refleja una comunidad activa, desarrollo constante y un compromiso sostenido con la transparencia.

Conclusión

Bancor Network sigue siendo uno de los pilares más importantes de las finanzas descentralizadas modernas. Al introducir el automated market making, la liquidez unificada y el descubrimiento de precios mediante smart contracts, ayudó a definir cómo funcionan hoy los mercados cripto. Su infraestructura sigue evolucionando, su comunidad permanece activa y su modelo continúa influyendo en el diseño de numerosos protocolos de liquidez.

Para quienes desean comprender cómo funciona realmente la liquidez automatizada, o simplemente explorar un proyecto DeFi con una trayectoria sólida, Bancor combina relevancia histórica con utilidad continua en un entorno altamente competitivo.

Dónde conseguir BNT

Si estás explorando el enfoque de Bancor sobre la liquidez automatizada, te interesa cómo su diseño AMM respalda el ecosistema DeFi o simplemente quieres conocer uno de los primeros innovadores en market making descentralizado.

Digital ownership en la era Web3

La propiedad digital se ha convertido en una de las ideas centrales de Web3, especialmente a medida que los juegos, los coleccionables y las economías virtuales se trasladan a la blockchain. Sin embargo, para que estos activos digitales sean realmente utilizables a gran escala, las blockchains deben ofrecer transacciones rápidas y de bajo coste sin comprometer la seguridad.

Immutable (IMX) es uno de los proyectos líderes que aborda este desafío, ofreciendo una Layer 2 de alto rendimiento diseñada específicamente para gaming, creación de activos y ecosistemas impulsados por NFTs. A medida que crece el interés por los juegos basados en blockchain y los desarrolladores buscan infraestructuras más eficientes, Immutable se ha consolidado como un actor clave en el debate sobre la escalabilidad de Web3 y la propiedad digital.

What Is Immutable (IMX)?

Immutable es una solución de escalado Layer 2 de nueva generación creada para potenciar la actividad de gaming y activos digitales en Ethereum. Opera sobre la Layer 1 de Ethereum, heredando su seguridad mientras resuelve una de sus principales limitaciones: las transacciones lentas y costosas.

Gracias a la tecnología de zero-knowledge rollups, Immutable procesa la actividad fuera de la cadena, agrupa miles de acciones y envía una única prueba de validez a Ethereum. El resultado es una red capaz de manejar hasta 9.000 transacciones por segundo, ofreciendo comisiones de gas cero para la creación y el intercambio de NFTs.

El término “Immutable” puede referirse a la empresa, al ecosistema en general, a la red Layer 2 (Immutable X) o al propio token IMX. El proyecto pone el foco en la velocidad, la escalabilidad y una infraestructura neutra en carbono, diseñada para crear un entorno sin fricciones para el gaming Web3. Respaldado por alianzas sólidas en la industria y un conjunto de herramientas en rápida expansión para desarrolladores, Immutable aspira a convertirse en la principal Layer 2 enfocada en gaming dentro del mercado cripto.

How Immutable Works

La infraestructura de Immutable se basa en los ZK-rollups, sistemas criptográficos que permiten procesar grandes volúmenes de actividad fuera de la cadena mientras se demuestra su validez en la blockchain. Cada lote de transacciones incluye una prueba matemática que verifica su corrección, lo que permite a Ethereum confiar en el resultado sin necesidad de recalcular los datos subyacentes.

Este enfoque reduce drásticamente la congestión, minimiza los costes y desbloquea el entorno rápido y fluido que requieren los juegos modernos. Cuando un usuario crea un NFT, intercambia un objeto o interactúa con un marketplace, la transacción se procesa dentro del entorno Layer 2 de Immutable con finalidad casi instantánea. Posteriormente, la red publica una prueba comprimida en Ethereum, actualizando el estado de forma segura.

Al eliminar la necesidad de pagar gas en la cadena principal, Immutable permite a los juegos soportar millones de microtransacciones sin fricción, algo que las blockchains tradicionales no pueden ofrecer de forma eficiente.

Key Features and Benefits

La ventaja más distintiva de Immutable es su capacidad para escalar ecosistemas de gaming basados en NFTs manteniendo seguridad de nivel Ethereum. Su modelo de creación sin comisiones permite a los desarrolladores ofrecer verdadera propiedad digital sin exigir a los jugadores que paguen costes de red.

Immutable también pone un fuerte énfasis en la sostenibilidad. Su enfoque neutro en carbono compensa el consumo energético de su infraestructura, abordando una de las críticas más habituales a la tecnología blockchain. Junto con un ecosistema de wallets, APIs, marketplaces y herramientas para desarrolladores, la red ofrece todo lo necesario para que grandes estudios y creadores independientes puedan construir con éxito.

The Role of the IMX Token

IMX es el token de utilidad nativo que impulsa el ecosistema Immutable. Se utiliza para gobernanza del protocolo, mecanismos de staking y determinadas comisiones o recompensas dentro de la red. Cuando los usuarios interactúan con marketplaces o crean activos, una parte del valor de la transacción se paga en IMX y puede destinarse a pools de staking o incentivos para desarrolladores.

La gobernanza permite a los holders de IMX influir en decisiones del protocolo, como modelos de comisiones o asignaciones de fondos para el ecosistema. Aunque la participación es opcional, aporta descentralización y voz comunitaria a medida que la red crece. El token también juega un papel clave en la recompensa a quienes aportan liquidez, desarrollan juegos o generan actividad dentro del ecosistema.

Ecosystem and Partnerships

Immutable se ha posicionado como una de las redes de gaming más amigables para desarrolladores en Web3. Sus alianzas incluyen grandes estudios, proveedores de infraestructura y plataformas especializadas en gaming. Gracias a integraciones listas para usar, los desarrolladores pueden lanzar marketplaces, wallets y sistemas de creación de NFTs sin enfrentarse a la complejidad técnica de la blockchain.

Esto ha dado lugar a una biblioteca en rápida expansión de juegos y economías digitales que utilizan IMX y las herramientas de Immutable. Los títulos abarcan múltiples géneros, desde juegos de estrategia y cartas coleccionables hasta experiencias multijugador, todos beneficiándose de transacciones rápidas y bajos costes operativos.

How Immutable Stands Out in the Crypto Landscape

El espacio de las Layer 2 está cada vez más concurrido, pero el enfoque de Immutable en gaming le da una identidad clara. Mientras que otras L2 de propósito general buscan soportar todo tipo de aplicaciones descentralizadas, Immutable está optimizada específicamente para la propiedad de activos y el trading de alto volumen.

Esta especialización le permite ofrecer soluciones directas a los principales problemas de jugadores y desarrolladores, como comisiones cero, procesos de onboarding simplificados y flujos de creación de NFTs sin fricción. Además, su uso de ZK-rollups le proporciona una finalidad más rápida y garantías criptográficas más sólidas en comparación con otros enfoques.

Why Immutable (IMX) Matters in 2025