Picture this: You're scrolling through DeFi platforms, and suddenly you see two different projects. One screams "12% APR!" while another boasts "12% APY!" Your brain probably thinks, "Same, right?"

Wrong. Very wrong.

When it comes to comparing interest rates, APR and APY might look like twins… but they’re not. Far from it. The difference between them can determine whether you grow your savings or overpay on a loan. In this guide, we’ll break down what APR and APY really mean, how they work in banking, lending, and crypto, and how understanding them can help you make smarter financial decisions.

Key Takeaways

- APR (Annual Percentage Rate) shows the yearly cost of borrowing, including interest and certain fees.

- APY (Annual Percentage Yield) reflects your total yearly return, factoring in compounding.

- For borrowers, lower APR = lower total cost. For savers, higher APY = higher returns.

- In crypto and DeFi, compounding frequency can turn modest APRs into much higher APYs.

APY vs APR: The Essential Difference

At a glance, APR tells you how much interest you’ll pay (or earn) over a year, without compounding. APY, on the other hand, includes compounding, the process where interest earns more interest over time.

When comparing financial products, whether a credit card, savings account, or staking pool, this distinction matters. For borrowers, APR reveals the true cost of debt, while for investors, APY highlights the power of compound growth.

TL;DR. APR is about cost, APY is about growth. Knowing which one applies helps you choose between competing offers with confidence.

What Is APR (Annual Percentage Rate)?

APR represents the yearly interest rate charged to borrow money, or the rate you earn before compounding if you lend it. It includes interest and certain fees, helping you understand the total cost of credit.

APR is widely used in credit cards, personal loans, mortgages, and auto financing. For example, if your credit card has an 18% APR, you’ll pay 18% interest on any carried balance. Fixed-rate loans maintain the same APR, while variable-rate loans fluctuate with market conditions and Federal Reserve changes.

Example: Borrow $10,000 at 10% APR for one year. You’ll owe $1,000 in interest. Simple and transparent, without compounding surprises.

What Is APY (Annual Percentage Yield)?

APY measures how much your money grows over a year, including compounding. It reflects how often your interest is added to your balance (daily, monthly, or annually) which then generates more interest.

This is the standard metric for savings accounts, money market accounts, and certificates of deposit (CDs). Banks and digital financial platforms often advertise APY because it paints a more complete picture of earning potential.

Example: Deposit $10,000 in an account with a 5% APY, compounded monthly. After one year, your balance grows to $10,511, slightly higher than a flat 5% APR return.

The more frequent the compounding, the greater the growth, especially important in DeFi protocols that compound every few minutes.

APR vs APY in Different Financial Products

Credit Cards and Loans (APR)

When borrowing, APR helps you understand the true borrowing cost. For instance, if a mortgage advertises a 6.5% APR, that includes both the interest and certain closing costs.

Car loans, student loans, and credit cards use APR to keep comparisons straightforward across lenders. The key? Lower APR = less expensive borrowing.

Savings and Investment Accounts (APY Focus)

If your goal is wealth building, APY is your guide. A high-yield savings account with 4.5% APY grows faster than one with 4% because compounding quietly amplifies returns.

For certificates of deposit (CDs) or fixed deposits, APY helps you compare the real impact of compounding frequency.

Cryptocurrency and DeFi (Both APR and APY)

In crypto lending, staking, or yield farming, both metrics appear and can be easily confused.

- APR shows base rewards (without compounding).

- APY assumes you’re constantly reinvesting.

Example: A DeFi pool may show 100% APR, but with daily compounding, it becomes 171% APY. The key is understanding how often you can claim rewards and whether gas fees make compounding worthwhile.

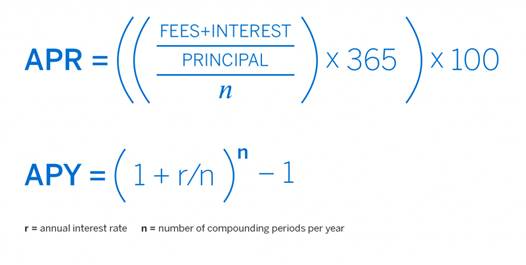

How to Calculate APR vs APY

To compare offers correctly, you can calculate one from the other:

Example: 12% APR compounded monthly

APY = (1 + 0.12/12)^12 - 1 = 12.68%

Compounding more frequently increases APY slightly each time.

Which Should You Focus On?

- If you’re borrowing, prioritize APR. It reflects the total cost of debt.

- If you’re saving or investing, look at APY. It shows how compounding boosts earnings.

- In crypto, check both. APR tells you the base reward, APY reveals potential if you reinvest.

When comparing offers, always read the fine print; frequency, fees, and conditions can shift the real value dramatically.

Common Misconceptions and Pro Tips

Myth: “APY is always better.”

Reality: Only if compounding happens, or if you reinvest earnings.

Myth: “APR ignores compounding, so it’s useless.”

Reality: APR helps borrowers compare costs clearly.

Pro Tip: Use online APR-to-APY calculators for quick comparisons. They’re free and eliminate guesswork.

The Bottom Line

APR and APY aren't just different ways of saying the same thing, they represent two different approaches to measuring returns.

When you see APR, you're looking at simple interest calculated over a year. When you see APY, you're seeing what happens when earnings get reinvested and compound over time. Both are valid measurements, just showing different scenarios.

This distinction becomes more noticeable with higher interest rates. A 50% APR becomes closer to 65% when compounded daily. The higher the base rate, the bigger the difference between these two numbers becomes.

Understanding which one you're looking at helps you compare options accurately. APR gives you the base rate, while APY shows the potential with compounding factored in.

Once you get the hang of spotting the difference, those financial offers suddenly make a lot more sense. No more squinting at numbers wondering why similar-sounding deals seem to work out so differently. It's like finally understanding why some recipe measurements are in cups and others in ounces.

If you want to put that knowledge to work, Tap Earn lets you earn APY on assets like BTC, ETH, SOL, and stablecoins, with no lock-up periods, so you stay in control of your funds.

This article is for general information purposes only and is not intended to constitute legal, financial or other professional advice or a recommendation of any kind whatsoever and should not be relied upon or treated as a substitute for specific advice relevant to particular circumstances. We make no warranties, representations or undertakings about any of the content of this article (including, without limitation, as to the quality, accuracy, completeness or fitness for any particular purpose of such content), or any content of any other material referred to or accessed by hyperlinks through this article. We make no representations, warranties or guarantees, whether express or implied, that the content on our site is accurate, complete or up-to-date.