Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

Imagine walking out of the grocery store and realizing you just got paid to buy your weekly groceries. Not with coupons or points that expire, but with actual cash. That’s Cashback!

For example, if you spend $200 at a grocery store with a 2% Cashback credit card, you earn $4 back. Simply put, it’s a rebate on your everyday purchases whether that’s at a supermarket, restaurant, or online shopping website.

So, let’s dive in and learn how Cashback works step by step, the different types of Cashback there are, how to calculate your rewards, and what could be the best option for you!

How Does Cashback Work?

Cashback follows a straightforward process:

- You make a purchase using your credit card.

- The merchant processes the payment through a network like Visa or American Express.

- The issuing bank calculates your reward based on the card’s rates.

- The reward accrues in your account.

Normally, you don’t receive Cashback instantly. Rewards typically appear after your monthly billing cycle closes, not at the moment of payment. If you spend $500 during a month on a 2% card, you earn $10 ($500 × 2% = $10), but you’ll see it added after your statement posts.

Cashback vs. Cash Advance

Although their names may be similar, these are not the same thing.

- Cashback is a reward.

- Cash advance is a short-term loan taken from your credit line, often with an immediate fee and a high interest rate.

Confusing the two can be costly. A cash advance may carry a fee plus instant interest, while Cashback reduces your overall expense.

Cashback vs. Points

Some cards advertise “cashback” but issue points instead. Those points may convert at a fixed rate (for example, 1 point = 1 cent), or they may have variable redemption value depending on how you use them for travel, gift cards, or online shopping. Always check the terms so you understand the true value.

Types of Cashback Cards

Not all Cashback cards work the same way. These are some of the most popular Cashback models you can find:

Flat-Rate Cards

Flat-rate cards offer the same percentage on every purchase. Typical rates range from 1.5% to 2%.

If you spend $1,000 in a month on a 2% flat-rate card, you earn $20 ($1,000 × 2% = $20), regardless of whether you spent it on retail, insurance, or streaming television.

It may be the best choice for people who prefer simplicity.

Fixed or Tiered Category Cards

These cards offer higher rates in specific categories (often grocery stores, gas stations, restaurants, or travel) and a lower rate (commonly 1%) on everything else.

Example:

- 3% at supermarkets → $500 × 3% = $15

- 1% elsewhere → $500 × 1% = $5

Total rewards = $20.

The issuing bank defines which merchants qualify, so it’s important to read the guideline and merchant terms matters.

It’s the best option for consumers with consistent spending patterns.

Rotating Category Cards

These offer 5% in categories that change quarterly, usually capped at a spending limit.

For example:

If the quarterly cap is $1,500 and you spend $1,500 at 5%, you earn $75 ($1,500 × 5% = $75). After that cap, rewards typically drop to 1%.

You must activate the bonus each quarter. Missing activation means earning only the base rate.

It’s best suited for engaged users who track deadlines and spending frequency.

Choose-Your-Own Category Cards

Some cards let you select your bonus category monthly. Others automatically apply a higher rate to your highest spending category.

If you select dining at 3% and spend $400 at restaurants, you earn $12 ($400 × 3% = $12).

It’s best for people whose lifestyle and consumption patterns change regularly.

How to Calculate Your Cashback

The formula is simple:

Amount Spent × Cashback Rate = Reward

Examples:

- $100 × 1% = $1.00

- $1,000 × 1.5% = $15.00

- $500 × 5% = $25.00

- $2,000 × 5% = $100.00

Keep in mind that spending caps and category limits can reduce your effective rate. Always review your card’s terms before assuming you’ll earn the top rate on all purchases.

Is a Cashback Credit Card Worth It?

Cashback cards work best if you pay your balance in full every month. If you carry a balance, interest charges (sometimes 20% or more annually) can easily exceed your rewards.

Pros

- You earn a percentage back on everyday life expenses.

- Rewards have fixed dollar value, unlike variable mile systems.

- Some cards have no annual fee.

- Over time, rewards can offset real costs.

For example, spending $2,000 per month at 2% earns $40 monthly ($2,000 × 2% = $40), or $480 per year.

Cons

- Carrying a balance triggers interest that outweighs rewards.

- Some cards charge annual fees.

- Rotating categories require active management.

- Applying for multiple cards can cause a temporary dip in your credit score due to hard inquiries from agencies like TransUnion.

Also consider the difference between credit and debit. A debit card pulls money directly from your bank account, avoiding interest entirely. A credit card offers rewards and credit-building potential, but it also introduces risk if spending exceeds your budget.

Cashback is an incentive, not free money. It works best when aligned with disciplined personal finance habits.

Tips to Maximise Your Cashback

- Match the card to your real spending. Review recent bank statements before choosing.

- Always pay in full. Interest eliminates profit.

- Activate rotating categories on time.

- Time large purchases strategically.

- Consider pairing cards. A flat-rate card for general purchases plus a category card for groceries or travel can increase total rewards.

- Stack with cash back apps. Services like PayPal shopping offers or cashback websites operate separately from your card rewards.

- Review welcome bonuses carefully. Many cards offer $150–$200 after meeting a spend requirement, but make sure the spending fits your normal budget.

Get Cashback Without the Credit Trap

Cash back credit cards can seem attractive: earn rewards on your spending, build credit, maybe snag some bonus points. But here's what you don’t get told upfront: if you carry a balance, even for a month or two, interest charges can wipe out any rewards you’ve earned. Suddenly that 2% cash back doesn’t look so good.

There's a better way: crypto Cashback on your debit card. Tap’s debit card gives you the rewards without the credit-related hassle. You earn cashback on everyday purchases (groceries, coffee, travel, dining) just like a credit card, but without borrowing, without interest, without the temptation to overspend, and with instant conversions. Your purchases come straight from your account balance, keeping you in control while still earning real rewards.

Tap’s Cashback isn’t paid in points or miles with obscure redemption rules. It's paid in the XTP token, deposited directly into your wallet based on the amount of XTP you have staked. Cashback rates range from 0.5% to 8%, scaling with your tier. The more XTP tokens you lock up, the more you earn. Just spend with your debit card, earn rewards automatically. If you value flexibility and financial discipline but still want to be rewarded for smart spending, then Tap’s crypto debit card is built for you!

Ready to earn Cashback the smarter way? Download the Tap app and start turning your spending into crypto rewards today!

Built as the next evolution of DAI, USDS is a stablecoin that operates within the Sky Protocol ecosystem (formerly MakerDAO) and aims to combine price stability, transparency, and decentralization in a single digital asset.

As stablecoins play a growing role in global finance, USDS offers an alternative to centralized options by using crypto-backed collateral and automated smart contracts rather than relying on a single issuing company. Beyond price stability, USDS is designed to integrate seamlessly with decentralized finance applications, offer earning opportunities through protocol incentives, and support a multi-chain future. For users seeking a stable digital dollar without centralized control, USDS represents a modern approach to value storage and transfer.

What Is USDS?

USDS is a crypto-backed stablecoin pegged to the US dollar, meaning its target price is approximately $1 at all times. Unlike traditional digital dollars issued by centralized companies, USDS is governed by smart contracts and decentralized decision-making rather than a single authority.

The foundation of USDS rests on three core principles. First, stability: the protocol is designed to keep USDS close to its dollar peg even during market volatility. Second, decentralization: no single company or government controls issuance, freezing, or redemption. Third, collateralization: every USDS in circulation is backed by crypto assets such as ETH, USDC, and tokenized real-world assets held within the Sky Protocol.

Compared to centralized stablecoins like USDT or USDC, USDS does not depend on corporate bank reserves or off-chain custodians. Compared to DAI, USDS is built for greater scalability and multi-chain functionality. And unlike purely algorithmic stablecoins, USDS relies on tangible collateral rather than market incentives alone. Its purpose is to provide a transparent, resilient digital dollar aligned with decentralized finance values.

How USDS Works

Creation Through Sky Vaults

USDS is created through a system known as Sky Vaults. Users deposit approved collateral assets into automated smart contracts and, in return, mint USDS. A simple way to think about this is like placing valuable assets into a secure digital vault and receiving a dollar-pegged receipt that can be spent or transferred.

Accepted collateral includes cryptocurrencies such as ETH, stable assets like USDC, and certain tokenized real-world assets. Each vault operates under predefined rules that ensure system-wide consistency and security.

Stability and Overcollateralization

To protect the dollar peg, USDS is overcollateralized. This means users must deposit more value than the amount of USDS they generate. If the value of the collateral falls too far, the system automatically sells part of it through a liquidation process to protect overall stability. This safety buffer is a key reason USDS can maintain its peg without relying on a central issuer.

Role Within the Sky Protocol

USDS functions as the cornerstone stablecoin of the Sky Protocol ecosystem. It supports lending, saving, payments, and governance processes across the platform. While governance decisions are handled separately, USDS is tightly integrated into Sky’s broader architecture and incentive structure.

Upgrading from DAI to USDS

Transitioning from DAI to USDS is designed as a simple, user-focused service that reflects best practices in modern decentralized finance and information technology. Through the official Sky website, end users can connect a compatible cryptocurrency wallet and upgrade their DAI to y smart contract software.

From the perspective of user experience, the upgrade emphasizes accessibility, transparency, and efficiency. No centralized authority, bank, or intermediary controls the transaction, and users retain full ownership of their data and digital assets throughout the process.

Once upgraded, USDS holders can immediately access additional tools within the Sky ecosystem, including savings mechanisms and incentive programs. For users in the United States and globally, this upgrade represents not just a technical update, but an improvement in how decentralized stablecoin products deliver value, scalability, and usability.

USDS vs. DAI: What’s Changed?

USDS and DAI share a common history rooted in the MakerDAO system, now operating under the Sky Protocol. Both are decentralized stablecoins pegged to the US dollar and backed by on-chain collateral. However, USDS represents an architectural and strategic evolution focused on scalability, governance, and improved incentives for the end user.

DAI was a foundational product in decentralized finance, enabling users to lock crypto assets in smart contracts and generate a stable digital currency. USDS builds on that model by refining the underlying technology, expanding multi-chain compatibility, and introducing enhanced reward structures that improve capital efficiency and user engagement.

From a risk management and policy standpoint, USDS is designed to better align with regulatory expectations while preserving decentralization. It incorporates lessons learned from market volatility, past crises, and stablecoin design challenges, positioning USDS as a more adaptable cryptocurrency for a rapidly evolving financial ecosystem. In short, DAI laid the groundwork, while USDS applies updated design, governance, and incentive mechanisms to meet modern DeFi needs.

USDS vs. Other Stablecoins

USDS differs from other stablecoins primarily in how control, backing, and transparency are handled.

Centralized stablecoins such as USDT and USDC are issued by companies that manage fiat reserves and can freeze funds if required by policy or regulation. Algorithmic stablecoins rely mainly on market incentives and code-based supply adjustments, which can introduce higher systemic risk.

USDS, by contrast, is decentralized and collateral-backed. Its reserves are visible on-chain, and no single entity has unilateral authority over user funds. This reduces censorship risk and improves transparency, though it does make the system slightly more complex than centralized alternatives. Overall, USDS sits between institutional stablecoins and experimental algorithmic designs, offering a balance of stability and decentralization.

How to Get and Use USDS

There are several ways to acquire and use USDS, depending on user experience level.

The simplest method is purchasing USDS on a decentralized exchange using another cryptocurrency. This option is generally best for beginners. Existing DAI holders may also be able to convert DAI to USDS at a one-to-one ratio through supported platforms. More advanced users can mint USDS directly by depositing collateral into Sky Vaults.

Once acquired, USDS can be used as a stable store of value, a trading pair within DeFi markets, or a payment method for transferring value without exposure to price volatility. It also plays a role in liquidity provision and lending protocols across the decentralized finance ecosystem.

Earning With USDS

USDS offers earning opportunities through the Sky Protocol. One option is the Sky Savings Rate, which allows users to lock USDS in a smart contract and earn variable rewards over time. This approach is similar in concept to a savings account, though returns fluctuate based on protocol conditions.

Another mechanism is Sky Token Rewards, which provide additional incentives for users who actively participate in the ecosystem. These rewards are subject to change and are not guaranteed, but they offer an added layer of value for engaged users. As with all DeFi yield mechanisms, returns depend on market conditions and governance decisions.

USDS in the Sky Protocol Ecosystem

The Sky Protocol is a decentralized finance platform built on the legacy of MakerDAO. Within this ecosystem, USDS serves as the primary unit of value transfer. It interacts with governance processes, incentive programs, and other decentralized applications supported by Sky. While governance tokens and protocol upgrades play a role behind the scenes, users do not need deep technical knowledge to benefit from USDS. Its design prioritizes usability while remaining aligned with decentralized principles and transparent system architecture.

Bottom Line

USDS is a decentralized stablecoin designed to offer a reliable digital dollar without centralized control. As the successor to DAI, it builds on a proven model while introducing improved scalability and ecosystem integration through the Sky Protocol. By combining crypto-backed collateral, automated risk management, and on-chain transparency, USDS provides an alternative to both centralized and algorithmic stablecoins. As DeFi continues to evolve, USDS represents a practical option for users seeking price stability with decentralized governance.

You’ve probably heard of MakerDAO, the system behind MKR and the stablecoin DAI. Now, meet what’s next. Sky is the rebranded ecosystem behind MakerDAO, one of the most established projects in decentralized finance. Launched in 2024, Sky represents the evolution of Maker’s stablecoin and governance system, with a stronger focus on accessibility, usability, and end-user experience.

Sky builds on MakerDAO’s long-standing role in DeFi by introducing a refreshed ecosystem centered around governance and decentralized control of digital assets. So, let’s dive in and see what’s new!

What Is Sky? The MakerDAO Rebrand Explained

Sky is the new identity of MakerDAO, the decentralized finance project best known for creating DAI, now evolved into the USDS stablecoin. The rebrand reflects a broader strategic shift toward improving governance participation, streamlining business processes, and enhancing the overall user experience across the ecosystem.

The Sky ecosystem operates on the Ethereum blockchain and focuses on two core assets: USDS, a decentralized stablecoin pegged to the United States dollar, and SKY, the governance token that replaced MKR. USDS is used for savings, payments, and financial transactions, while SKY enables voting, decision-making, and long-term protocol governance.

This evolution was driven by the need for better scalability, clearer incentives, and improved accessibility for both new and existing users. By lowering governance barriers and modernizing its design, Sky aims to serve as a more intuitive decentralized application while maintaining the risk management, transparency, and stability that made MakerDAO a foundational DeFi project.

Sky vs. Skycoin: Clearing Up the Confusion

Despite the similar name, Sky (SKY) and Skycoin (SKY) are entirely different cryptocurrency projects. Sky is the rebranded MakerDAO ecosystem focused on decentralized finance, stablecoins, and governance on Ethereum. Skycoin, on the other hand, is a separate blockchain project with its own computing platform, token economics, and development team.

They differ in use case, market value, technology, and community. Sky’s primary function is enabling decentralized savings, loans, and governance through USDS and SKY, while Skycoin targets network architecture and alternative blockchain infrastructure. Their prices, market capitalization, and trading volume are also unrelated.

Understanding this distinction is important for investors and end users to avoid confusion when researching exchanges, market trends, or investment opportunities.

How Sky Works: Key Features

Sky operates as a decentralized finance service with no central authority controlling user funds. One of its core features is USDS staking, where users deposit USDS into the protocol to earn yield through mechanisms such as the Sky Savings Rate and Sky Token Rewards. This allows users to generate interest on a dollar-pegged digital currency while retaining full control of their assets.

Governance is handled through the SKY token. Token holders participate in voting on protocol upgrades, fee adjustments, collateral policies, and risk management decisions. This voting process ensures transparency and community-led decision-making across the ecosystem.

Sky also introduces a modular structure known as Sky Stars, independent projects that operate within the broader ecosystem while maintaining autonomy. This design supports innovation, scalability, and faster development, all while preserving alignment with Sky’s core financial services.

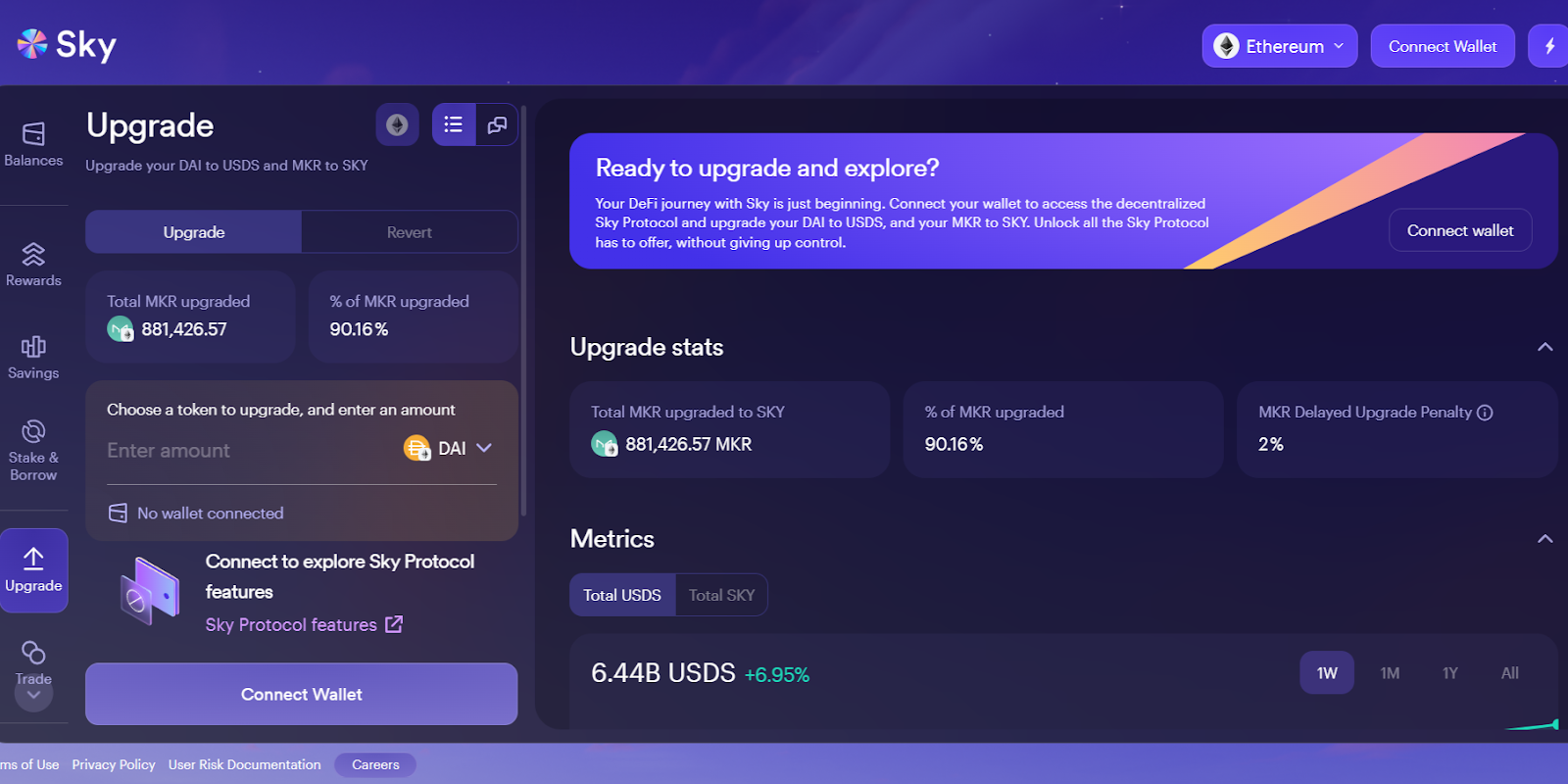

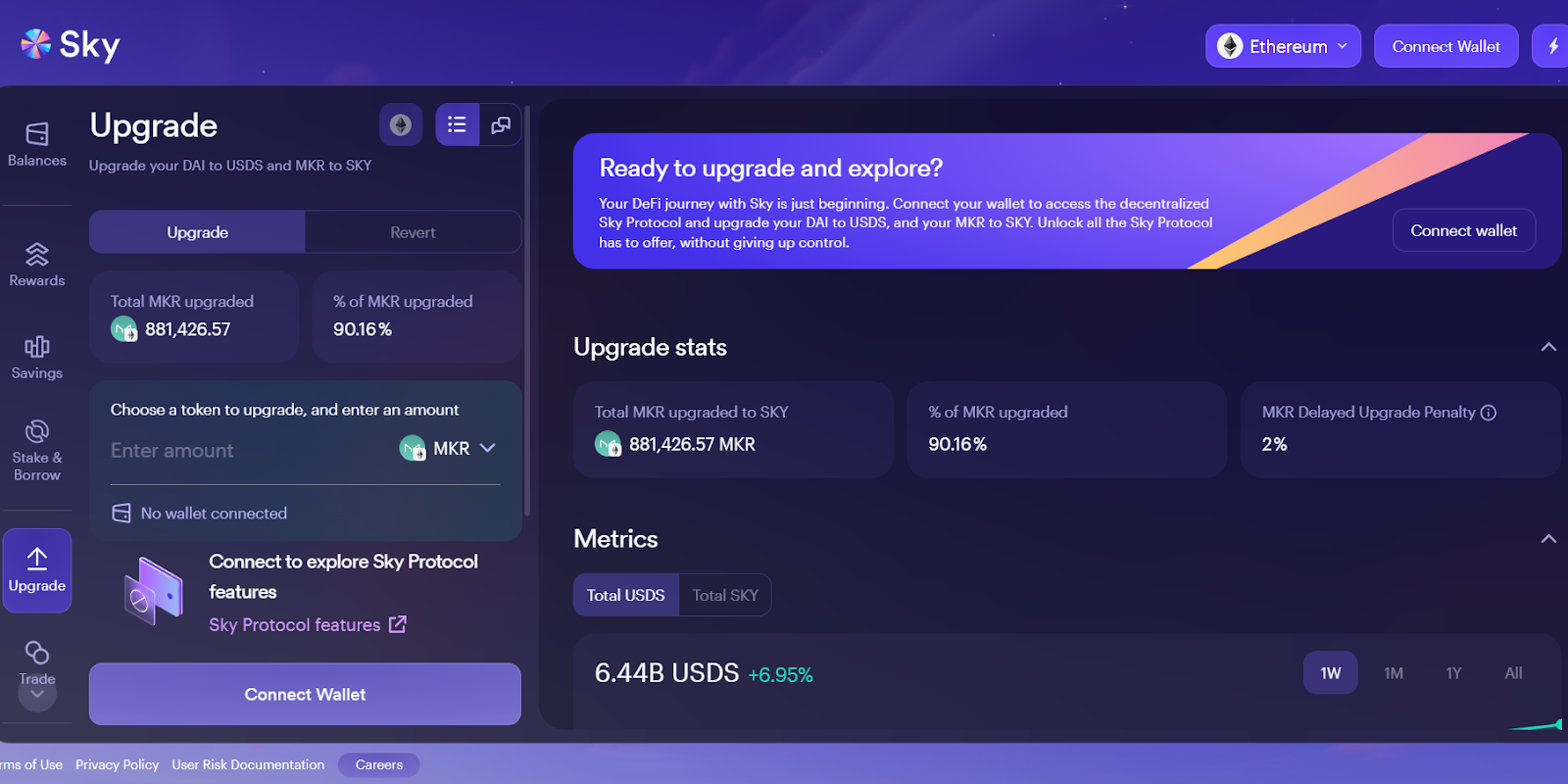

How to Upgrade from MKR to SKY

As part of the MakerDAO rebrand, MKR has been replaced by SKY as the sole governance token of the Sky Protocol. While MKR may continue to trade on secondary markets, only SKY grants access to governance, staking, and participation in the Sky ecosystem.

The upgrade process is handled directly through Sky’s official website, ensuring a non-custodial and user-controlled experience. Users simply connect their Ethereum wallet, initiate the upgrade, and convert MKR to SKY at the fixed ratio of 1 MKR = 24,000 SKY. Throughout the process, users retain full control of their assets.

Upgrading is strongly encouraged for anyone who wants to continue voting, delegating, or interacting with Sky’s governance and reward mechanisms. Holding SKY unlocks features such as protocol voting, participation in decision-making, and access to staking-related functionality tied to the Sky ecosystem.

It’s also important to note that the protocol introduces a time-based penalty for delayed upgrades. Starting September 18, 2025, the amount of SKY received per MKR will gradually decrease, beginning with a 1% reduction and increasing over time. Upgrading before this date ensures users receive the full conversion value with no penalty.

In short, while MKR remains a recognizable asset, SKY is the token that will power the Sky ecosystem going forward, and upgrading is the recommended path for anyone looking to stay aligned with the protocol’s future development.

Sky Token (SKY) Current Value & Market Performance

The SKY token plays a central role in governance and protocol incentives. Following the rebranding, MKR was converted into SKY at a 1:24,000 ratio, significantly lowering the unit price and improving accessibility for individual participants.

At the time of writing, its market capitalization places it in the top 50 cryptocurrencies, among well-established DeFi governance tokens. However, like all cryptocurrencies, SKY experiences price volatility influenced by broader market conditions and DeFi adoption trends.

Bottom Line

Sky is the next chapter of MakerDAO, reimagined to deliver a more accessible and scalable decentralized finance ecosystem. By combining USDS for savings and transactions with SKY for governance and decision-making, Sky aims to empower users with greater control, transparency, and financial autonomy.

Imagine you suddenly need money for a medical emergency, a business opportunity, or an unexpected expense. You own a house, some stocks, and a savings account. Which one can you turn into cash by tomorrow without losing value?

That question captures the essence of liquidity.

In finance, liquidity refers to how quickly and easily an asset can be converted into cash without significantly affecting its price. It applies to individuals, businesses, investors, and entire markets. Whether you are trading in the stock market, managing a company’s cash flow, or planning your personal finance strategy, liquidity plays a central role. In this article, we’ll learn what liquidity means, the main types of liquidity, how to measure it, and why it matters.

The ABC of Liquidity

So, what is liquidity in simple terms?

Liquidity is the ability to convert an asset into cash quickly, at a fair value, without a large loss. The faster and easier the conversion, the more liquid the asset is.

Cash is the most liquid asset because it is already money. You can use it immediately for payment, saving, or investment. There is no need to sell or negotiate its price.

Now think of liquidity as a spectrum. On one end, you have highly liquid assets such as cash in a deposit account or funds in a bank. On the other end, you have illiquid assets like real estate, a land lot, or collectibles. These may take months to sell and often require compromise on price.

For example, if you need $10,000 tomorrow, selling shares on a stock exchange is usually faster than selling an apartment or commercial property. Liquidity is not a yes-or-no concept. It is about speed, cost, and value preservation during conversion.

The Three Main Types of Liquidity

When people ask, “What are the three types of liquidity,” they are usually referring to market liquidity, accounting liquidity, and asset liquidity.

1. Market Liquidity

Market liquidity describes how easily an asset can be bought or sold in a market without causing a major change in its price.

In a highly liquid market, such as the stock market or the cryptocurrency market, there are many buyers and sellers. High trading volume and tight bid-ask spreads signal strong supply and demand. This allows traders to execute a trade quickly and close to the asset’s fair value. In contrast, the real estate market is less liquid. Selling a house or commercial property can take months, and the final sales price may differ significantly from the initial listing.

2. Accounting Liquidity

Accounting liquidity focuses on a company’s ability to meet short-term obligations such as payroll, debt payments, insurance premiums, and supplier invoices.

It is typically measured using liquidity ratios derived from the balance sheet:

- Current Ratio = Current Assets ÷ Current Liabilities

- Quick Ratio = (Current Assets − Inventory) ÷ Current Liabilities

- Cash Ratio = Cash and Cash Equivalents ÷ Current Liabilities

Current assets may include cash, accounts receivable, inventory, and short-term financial instruments. Current liabilities include short-term debt, payroll obligations, and other expenses due within a year. A company with strong accounting liquidity has sufficient working capital and cash flow to manage operations without facing solvency problems.

3. Asset Liquidity

Asset liquidity refers to how easily a specific asset can be converted into cash.

Here is a simplified typology of asset liquidity:

- Cash and currency

- Deposit accounts and certificates of deposit

- Stocks and exchange-traded funds

- Bonds and mutual funds

- Real estate and private equity

- Collectibles and rare items

Factors that affect asset liquidity include market conditions, trading volume, regulation, demand, and industry trends. For example, a widely traded coin in the cryptocurrency market is typically more liquid than shares in a private company.

Examples of Liquid vs. Illiquid Assets

Highly liquid assets include:

- Cash and funds in a bank

- Money market instruments

- Stocks listed on major stock exchanges

- Government bonds and high-grade securities

These assets benefit from strong supply and demand, transparent pricing, and active trading volume.

Illiquid assets include:

- Real estate such as a house or apartment

- Commercial property

- Private company shares

- Rare collectibles or specialized financial instruments

If you need $10,000 within 24 hours, selling a stock or bond is usually realistic. Selling real property within a day, without heavy discounting, is not.

Liquidity directly affects speed, cost, and value during sales.

How to Measure Liquidity

Liquidity can be measured differently depending on context.

For Individual Assets

Investors and traders look at:

- Trading volume

- Bid-ask spread

- Time required for conversion

- Price stability

High volume and narrow spreads usually signal strong market liquidity.

For Companies

Liquidity ratios provide structured measurement tools:

Current Ratio

Current Assets ÷ Current Liabilities

A ratio above 1 suggests the company can meet short-term obligations.

Quick Ratio

(Current Assets − Inventory) ÷ Current Liabilities

This excludes inventory, offering a stricter view of liquidity risk.

Cash Ratio

Cash & Cash Equivalents ÷ Current Liabilities

The most conservative measure, focusing only on immediately available money.

These tools help management, investors, and lenders assess financial health, credit risk, and solvency.

Why Liquidity Matters to Investors and Traders

Liquidity offers flexibility. You can respond quickly to market opportunities, reduce exposure during volatility, or handle emergencies. In liquid markets, traders benefit from:

- Lower transaction costs

- Reduced slippage

- More accurate price discovery

- Greater transparency

Without liquidity, even valuable assets can become difficult to use.

Liquidity vs. Profitability: Understanding the Difference

Does liquidity mean profit? The short answer, no.

Liquidity refers to the ability to meet short-term obligations or convert assets into cash. Profitability refers to the ability to generate revenue and long-term wealth.

A company can be profitable but face liquidity problems. For example, strong sales revenue combined with slow-paying accounts receivable can create cash flow shortages. Conversely, a company may hold significant cash reserves but struggle to generate profit.

Both liquidity and profitability are essential, but they serve different purposes in finance and business management.

The Risks of Low Liquidity

Low liquidity introduces several risks:

- Price slippage when executing large trades

- Wider bid-ask spreads

- Increased volatility

- Difficulty exiting positions

- Liquidity risk during market stress

In extreme cases, businesses may face a liquidity crisis, meaning they cannot meet debt or liability payments despite owning valuable assets. It’s possible to manage liquidity risk by maintaining emergency reserves, diversifying across asset classes, and evaluating market conditions before making large trades.

Liquidity in Different Market Conditions

In bull markets, liquidity tends to rise. Higher participation increases trading volume and narrows spreads.

In bear markets or during a recession, liquidity can shrink rapidly. Investors may rush toward cash, a behavior sometimes called a “flight to liquidity.”

During financial stress, illiquid assets often experience larger price swings and discounting. Strategic planning and risk management become especially important in these periods.

Key Takeaways

Liquidity allows us to convert an asset into cash quickly and without major loss of value. It exists on a spectrum, from highly liquid money in a bank to illiquid real estate or private investments.

There are three main types of liquidity: market liquidity, accounting liquidity, and asset liquidity. Each plays a distinct role in finance, from trading efficiency to business solvency.

Liquidity does not mean profit, but it directly impacts financial health, flexibility, and risk management. Whether you are an individual trader, a business owner, or anything in between, understanding liquidity can protect you against emergencies and help you seize new opportunities.

If you have ever researched a new cryptocurrency, you have likely encountered a lengthy PDF filled with technical language, diagrams, and bold claims about innovation. That document is called a white paper, and in crypto, it is often the first and most important source of information about a project.

So, what is crypto white paper exactly? In simple terms, a crypto white paper is a detailed document published by a blockchain project that explains its purpose, technology, economic model, and long-term strategy. It serves as both a technical explanation and a research tool for investors, developers, and the wider community.

Understanding how to read and evaluate a white paper is a key skill in cryptocurrency research. It can help you separate serious projects from hype-driven ventures and make more informed decisions. Let’s dive in and figure out what it is all about!

What Is a Crypto White Paper?

A white paper, in general business and information technology contexts, is a formal document that explains a problem and proposes a solution. Companies often use white papers in marketing, engineering, or finance to present research, methodology, and technical insight.

In the cryptocurrency space, a white paper is a foundational document that outlines how a blockchain project works and why it exists. It is usually published before or during a token launch, sometimes alongside fundraising efforts such as an initial coin offering (ICO).

A crypto white paper typically includes these key elements:

- A clear problem statement

- A proposed solution using blockchain technology

- Technical architecture and system design

- Details about consensus mechanisms, cryptography, and distributed computing

- Tokenomics, including supply, distribution, and incentives

- A development roadmap and timeline

- Information about the founding team

Unlike a brochure or simple website page, a white paper aims to provide comprehensive detail. It blends technology, business strategy, and economic modeling into a single well-structured document. Because it is self-published by the project team, its credibility depends on the transparency and clarity it provides.

The Bitcoin White Paper: Where It All Started

The concept of a crypto white paper began with Bitcoin.

On October 31, 2008, an individual or group using the name Satoshi Nakamoto published a nine-page document titled “Bitcoin: A Peer-to-Peer Electronic Cash System.” This white paper introduced a new model for digital money that removed the need for a bank or centralized authority.

It described a peer-to-peer network where financial transactions are verified through cryptography and recorded on a distributed ledger. It also proposed a consensus mechanism that prevents double-spending without relying on trust.

Although short, the Bitcoin white paper combined technical precision with a clear use case: electronic cash that operates independently of traditional financial institutions. It set the standard for future blockchain documentation and remains one of the most influential documents in modern finance and technology.

The Ethereum White Paper: Another Milestone

After Bitcoin, other projects built on its ideas while addressing perceived limitations.

In 2014, the Ethereum whitepaper was published by a young developer named Vitalik Buterin and titled “Ethereum whitepaper: A Next Generation Smart Contract & Decentralized Application Platform.”

In the whitepaper, Vitalik outlines how the intentions of the Ethereum platform differ from Bitcoin’s. The whitepaper outlined how the platform would allow developers to create and launch decentralized applications (now commonly known as DApps) and included technological solutions that backed these goals, such as the Ethereum Virtual Machine and smart contracts.

Other Notable Crypto White Papers

Litecoin presented itself as a faster alternative to Bitcoin, adjusting transaction speed and mining parameters. Similarly, XRP focused on cross-border payments and improving efficiency in global finance.

Each of these white papers reflects an evolution in blockchain innovation. They identify specific market problems, propose technical solutions, and refine the structure of crypto documentation.

White Papers vs. Litepapers

Not every project releases a lengthy technical document. Some publish a “litepaper,” which is a shorter and more accessible version of a white paper.

A traditional white paper may span 20 to 100 pages and include detailed engineering explanations, diagrams, and token distribution models. It often targets developers, analysts, and experienced investors.

A litepaper is typically 5 to 10 pages long. It provides a high-level overview of the project’s purpose, utility, and strategy without going deeply into cryptography or distributed computing architecture.

Neither format is inherently better. Complex blockchain infrastructure projects may require extensive technical writing, while simpler applications may communicate effectively with a concise document. Some projects publish both versions to serve different audiences.

What to Look For in a Crypto White Paper

When evaluating a cryptocurrency project, the white paper should be your starting point. However, reading it critically is essential.

First, review the problem statement. Does the project clearly identify a real market need? Strong white papers define a specific issue in finance, technology, or another industry and explain why existing solutions are insufficient.

Next, examine the proposed solution. Does blockchain genuinely improve the process, or is decentralization being used unnecessarily? A credible project demonstrates why distributed computing, cryptography, and tokenization add value.

Technical credibility is another key factor. The document should provide sufficient detail about architecture, consensus mechanisms, and scalability without hiding behind jargon. Diagrams, statistics, and structured explanations often signal thoughtful engineering.

Tokenomics also deserves careful analysis. Look at how tokens are distributed, whether supply is fixed or inflationary, and what incentives drive participation. A clear economic model supports long-term sustainability.

Team transparency is equally important. Are the founders identified? Do they have relevant experience in software development, finance, or entrepreneurship? Finally, watch for red flags. Overly promotional language, guaranteed returns, vague promises, plagiarism, or unrealistic timelines can undermine credibility.

How to Read and Analyze a Crypto White Paper

Approach a white paper as you would any serious research document.

Begin with the abstract or executive summary. This section provides an overview of the project’s purpose and proposed solution. Check the publication date to ensure the information is current, especially in a rapidly evolving market.

As you read, focus on understanding the core concept rather than every technical detail. You do not need advanced knowledge of algorithms or cryptography to grasp whether the project addresses a meaningful problem.

Ask critical questions. Does this project need to exist? Is the solution feasible? Can it compete with established alternatives? What risks might arise from regulation, competition, or technological limitations?

Compare the project with similar initiatives in the blockchain ecosystem. Differentiation matters in a competitive industry shaped by innovation and rapid product development.

Beyond the white paper, conduct broader due diligence. Review the project’s website, examine code repositories if available, analyze community discussions, and research team members’ professional backgrounds. A white paper is a foundation for understanding, not the final word.

Why Crypto White Papers Matter

For investors, a white paper is often the primary research document before committing capital. It provides insight into the project’s structure, goals, and potential risks. It also creates a benchmark: progress can later be compared against the original roadmap and promises.

For the broader crypto ecosystem, white papers encourage transparency and knowledge sharing. They document new approaches to consensus, tokenization, decentralized finance, and application software design. Over time, they contribute to the historical evolution of blockchain innovation.

For project teams, writing a white paper forces strategic planning and clarity. It requires defining objectives, outlining methodology, and articulating value. A well-written document can build confidence within a competitive market.

Despite the rapid growth of blogs, social media, and promotional content, white papers remain relevant. Serious projects continue to treat them as essential documentation.

What Does a Crypto White Paper Look Like?

A typical crypto white paper is a professionally formatted PDF, usually between 10 and 100 pages. It often begins with an introduction and abstract, followed by sections on the problem statement, technical architecture, tokenomics, roadmap, and team.

You may see diagrams illustrating network structure, charts explaining token distribution, and occasionally mathematical formulas or code snippets. References or citations sometimes appear at the end.

Most projects make their white papers available for download on their official website. The layout should appear structured and consistent, reflecting attention to detail and technical writing standards.

Conclusion

A crypto white paper is much more than a marketing document. It is a structured explanation of a blockchain project’s vision, technology, and economic model. If you are exploring cryptocurrency as an opportunity or simply expanding your understanding of the industry, reading white papers is essential. They help you evaluate credibility, assess risk, and compare multiple solutions for different issues.

However, a white paper is only the starting point. Independent, constant research remains necessary in a fast-moving and innovative market. By learning how to interpret these documents carefully, you equip yourself with one of the most valuable tools for decision-making in the crypto sphere.

Your portfolio is flashing red red. The news keeps saying “correction,” “crash,” and "recession,” etc. You keep hearing one word everywhere: bear market. But what does it actually mean?

A bear market is a sustained market trend in which asset prices fall 20% or more from recent highs, typically across a major stock market such as the S&P 500, NASDAQ, or Dow Jones Industrial Average. Unlike short-term volatility, a bear market reflects a broader shift in market sentiment, where pessimism replaces confidence and investors begin selling shares in large volumes.

Whether markets are officially in a bear phase depends on current price levels and economic data. Bear markets are defined by measurable declines, not headlines alone. The term “bear” dates back to 18th-century finance, inspired by the downward swipe of a bear’s paw, symbolizing falling prices.

However, while fear often dominates during these periods, history shows that bear markets are a normal part of economics and long-term investment cycles.

What Causes a Bear Market?

A bear market often begins when many investors sell at the same time, pushing prices lower. This selling pressure can be triggered by slowing economic growth, rising unemployment, falling corporate profit, or concerns about recession.

External shocks also play a role. A financial crisis, policy changes in the United States, geopolitical tensions, or global events like the recent pandemic can weaken confidence. As prices fall, pessimism spreads, reinforcing further sales. This feedback loop (declining prices fueling fear and more selling) can accelerate the downward market trend.

Bear Market vs. Recession: What’s the Difference?

A bear market refers specifically to declining prices in the stock market or other financial markets. A recession, by contrast, describes a broader economic slowdown marked by falling GDP, rising unemployment, and reduced business activity.

They often occur together, but not always. Historically, some bear markets have happened without a formal recession. Conversely, economic slowdowns do not always trigger a 20% market decline.

In general, a recession affects the entire economy (employment, industry output, and consumer spending) while a bear market focuses on asset valuation. However, sustained declines in market value can signal expectations of weaker economic performance ahead.

How Long Do Bear Markets Last?

Bear markets occur roughly every six years on average, though timing varies. The median decline has historically been around 33% from peak to trough.

Duration can range from weeks to several years. The COVID-19 pandemic bear market in 2020 lasted only weeks before recovery began, while the 2007–2009 financial crisis extended over more than a year. The longest modern bear market followed the Great Depression beginning in 1929.

Despite differences in severity and duration, one consistent historical result stands out: markets have eventually recovered. Every past bear market has been followed by a new bull cycle, though the timeline can test investor patience.

Famous Bear Market Examples

Several well-known downturns illustrate how bear markets unfold:

- The Great Depression (1929–1932): One of the most severe collapses in market history.

- The 1970s stagflation period: High inflation and slow growth pressured equities.

- The Dot-com bubble (2000–2002): Technology share valuations collapsed after speculative excess.

- The Financial Crisis (2007–2009): Triggered by credit risk and housing market instability.

- The COVID-19 crash (2020): A rapid decline followed by an unusually fast recovery.

- The 2022 bear market: Driven by inflation and interest rate hikes.

What Can You Do in a Bear Market?

Bear markets raise practical questions. Because individual circumstances differ, responses vary too. People often have to decide between several approaches:

Buying vs. Selling

Some choose to continue purchasing assets during downturns, viewing lower prices as discounting opportunities. Dollar-cost averaging (which is investing fixed amounts at regular intervals) can reduce the emotional pressure of trying to time the bottom.

Others may reduce exposure to limit further losses. However, selling during panic can lock in declines, especially if markets recover sooner than expected. Timing exact turning points is historically difficult, even for experienced traders.

Emergency Savings and Planning

During economic uncertainty, individuals often review saving levels. Maintaining several months of expenses in a secure account can provide financial protection and reduce the likelihood of forced selling.

Maintaining an Investment Strategy

Long-term contributors to retirement plans such as a 401(k) frequently continue funding accounts despite market volatility. Lower prices can mean acquiring more shares for the same contribution, though results depend on long-term recovery.

Reviewing Risk Tolerance

Bear markets sometimes reveal mismatches between risk tolerance and portfolio allocation. Rebalancing (i.e., adjusting the mix of equity, bond, or exchange-traded fund exposure) can align investments with comfort levels.

Defensive Investments

Some investors shift toward traditionally defensive economic sectors such as utilities, healthcare, or consumer staples. Government bonds and diversified funds are also commonly discussed as lower-volatility alternatives. Each carries its own risks, including inflation or interest-rate sensitivity.

These are only possibilities. Decisions ultimately depend on personal goals, time horizon, and a solid financial plan.

Conclusion: What Goes Up Must Come Down

A bear market is a sustained decline of 20% or more in asset prices, typically linked to weakened confidence and economic concerns. While volatility can feel unsettling, bear markets are a recurring feature of the global economy.

History shows that markets have recovered from financial crisis, recession, economic bubble bursts, and even pandemic shocks. Preparation often matters more than prediction. A diversified portfolio, thoughtful planning, and a long-term perspective have historically helped many investors navigate downturns.

Understanding how bear markets work can transform fear into smart decision-making, grounded not in panic, but in knowledge.

.webp)

.webp)