Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

Your XTP does more now. A lot more.

You already know XTP unlocks Cashback, lower rates, and higher limits across Tap. Now, with the launch of Tap Earn, your XTP has a new trick up its sleeve — better yield rates on the assets you're already holding!

From the moment you spend, trade, or earn, XTP keeps working to maximize your returns, your XTP now amplifies every move you make across the platform. Take a look at what this new utility brings to the table!

Higher APY, Unlocked by XTP

Premium tiers now unlock higher APY. The key? Your XTP.

If you lock up your XTP, you’ll now access rates up to 7% APY on BTC, ETH, XRP, SOL, USDT, and USDC. The same assets you're already holding. Better returns, just because you're holding XTP alongside them.

The more XTP you lock, the higher your tier. The higher your tier, the more your portfolio earns. No extra steps or need for separate platforms. Just better rates, automatically applied to everything in your Earn vault.

Daily Compounding, Amplified

Your rewards compound daily. That means every day's earnings start earning too.

When combined with the higher APY unlocked through XTP lock-ups, the compounding effect becomes even more powerful. Users can track this growth directly inside the Earn hub through real-time tracking, while weekly payouts keep the process transparent and easy to follow.

This creates a natural portfolio synergy within the Tap ecosystem.

For example:

- Hold stablecoins like USDT or USDC for more predictable yield generation.

- Hold assets like BTC or ETH for long-term growth exposure.

- Use XTP to unlock higher Premium APY tiers across the portfolio.

Together, these components create a more flexible yield strategy without forcing you into lock-up periods or complicated DeFi systems.

Set It Up in Three Steps

Getting started with enhanced Earn utility is extremely simple.

Step 1: Check Your Current Tier and Rates

Open the app to view your current account level and available APY rates.

Step 2: Upgrade Through XTP

Acquire or lock the required amount of XTP to move into a higher Premium tier and unlock enhanced rewards.

Step 3: Watch Your Rewards Come in

Once your Premium tier is active, your Earn vault automatically reflects the updated APY rates, allowing your portfolio to begin compounding at the higher level.

There’s no need for a complicated setup or using multiple platforms.

XTP's Ecosystem Loop

The launch of Earn adds another layer to XTP’s growing ecosystem utility.

You already use XTP to:

- Reduce trading and FX fees.

- Unlock Premium account benefits.

- Increase Cashback rewards through the Tap Mastercard.

- Access higher platform limits and premium features.

Now your XTP also amplifies how much your portfolio earns. This creates a flywheel effect:

- Save money through lower fees.

- Earn Cashback through everyday spending.

- Generate yield through Tap Earn.

- Recycle rewards back into their portfolio for further compounding.

Instead of isolated features, Tap brings an interconnected ecosystem where different utilities reinforce each other over time.

One Token. Every Corner of the App.

You've already been building something. Every trade, every purchase, every time you've held crypto— no matter which one or for how long— it's been adding up.

Tap Earn just makes that mean more.

Now your crypto earns while you hold it. Your XTP unlocks better rates while you live your life. And every reward you compound today is building the portfolio you want tomorrow.

Because utility is not just a feature on a list. It should work in your favour every single day. With Earn now in the mix, your XTP is working harder than ever before.

Let's Talk About Getting Your Crypto to Work While You Sleep

Remember when your grandparents bragged about their 2% savings account? Those days feel like ancient history now that crypto APY percentages are floating around that would make a traditional banker faint. But hold up, before you start dreaming about retiring next month on those sweet, sweet yields, let's dive into what APY actually means and why some of these numbers look like lottery tickets.

What the Is APY, Anyway?

Think of APY as compound interest on steroids. While your bank's savings account sits there earning dust, APY measures how much your money can actually grow in a year when interest keeps building on top of interest. The faucet of passive income is now open.

Here's a reality check: Park $1,000 in your bank at 5% simple interest, and you'll have a whopping $1,050 after a year. Yawn, boring… But that same money with 5% APY compounded monthly? You're looking at $1,051.16.

"Big deal, that's only a dollar!" you might say. But here's where it gets interesting. Over time, that compounding effect turns into a money snowball rolling down a mountain. The difference between simple interest and compound interest isn't just pennies; it's the difference between walking and taking a rocket ship.

APY vs. APR: The Sibling Rivalry You Need to Understand

Okay, confession time…even seasoned crypto folks mix these up. Here's your cheat sheet:

APY (Annual Percentage Yield): What you earn when you lend out your crypto. The higher, the better for your wallet.

APR (Annual Percentage Rate): What you pay when you borrow crypto. Lower is your friend here.

Think of it this way: APY is the cool cousin who brings you money, while APR is the one who always asks to borrow twenty bucks.

For a more detailed comparison, click here.

Where Does APY Show Up in Crypto?

- Crypto "Savings Accounts"

Some platforms let you deposit your tokens and watch them multiply. It's like putting your crypto to work at a job that actually pays decent wages. Your coins get lent out to traders who need them, and you get a cut of the action.

- Staking: Become a Network Validator

With Proof-of-Stake blockchains like Ethereum or Cardano, you can "stake" your tokens to help secure the network. Think of it as being a digital security guard who gets paid in crypto. The network stays safe, and you earn rewards. Win-win.

- Yield Farming: The Wild West of DeFi

This is where things get interesting, and a bit crazy. You provide liquidity to decentralized exchanges, and in return, you earn trading fees plus shiny new governance tokens. Early yield farmers sometimes see APYs that look like phone numbers, but don't get too excited; those rates have a habit of crashing back to earth.

- Lending Protocols: Become the Bank

Platforms like Aave and Compound let you play banker. You lend your tokens, borrowers pay interest, and you collect the proceeds. APY goes up when everyone wants to borrow your particular flavor of crypto, and down when the demand cools off.

Why Are Crypto APYs So High?

While your bank offers you a measly 0.5%, crypto platforms are throwing around eye-watering numbers like 10%, 50%, or even 1,000%+. Here's why:

Crypto traders will pay premium rates to short a token or execute complex arbitrage strategies. Supply and demand at its finest.

Hype for new projects also plays a role. Fresh projects often throw ridiculous APYs at users to attract liquidity. It's like a grand opening sale, but with more zeros.

Risk gets factored in. Let's be real, crypto can get risky at times. Higher returns compensate for the white-knuckle ride.

Finally, token Incentives can play a role too. Many of those eye-popping APYs come partially from project tokens that could moon... or crater. It's the crypto Russian roulette.

The Math Behind the Magic

Don't worry, we're not about to turn this into a calculus nightmare. The APY formula is actually pretty straightforward:

Example: 10% interest compounded monthly gives you about 10.47% APY. Compound it daily? You're looking at 10.52%. In crypto, some protocols compound every block, which is like compounding every few seconds. Your calculator might start smoking.

The Fine Print

Before you quit your day job and become a full-time yield farmer, let's talk about the risks that nobody likes to mention at crypto parties. First up is volatility. Sure, your APY might be 20%, but if your token's price drops 50%, you're still in the red. Math is cruel like that. Then there's impermanent loss, which sounds harmless but can eat into your gains faster than you can say "automated market maker" when you're providing liquidity and token prices start dancing around.

Don't forget about smart contract risk, either. DeFi protocols are basically computer programs holding billions of dollars, and if they break, funds can disappear into the digital ether without so much as a goodbye note. Platform risk is equally sobering. Remember Celsius? FTX? Sometimes the platforms themselves go belly-up, taking user funds with them like the Titanic.

Last but not least, there’s APY whiplash. That jaw-dropping 100% APY you bookmarked yesterday? It might be 15% today because crypto moves fast. Rates fluctuate based on demand, new competition, token economics, and sometimes just because the crypto gods felt like shaking things up.

What's a "Good" APY?

- Conservative. Sticking to blue-chip assets and reputable platforms for 3-8% APY. For the faint of heart.

- Moderate. Staking some altcoins or providing liquidity for 10-20% APY. There’s some excitement, but not heart-attack levels.

- High (YOLO). Chasing new DeFi projects for 50-100%+ APY. It’s worth keeping in mind there’s a non-zero chance your tokens might become expensive digital art.

Remember, if an APY looks too good to be true, it's probably attached to risks that would make a hedge fund manager nervous.

Crystal Ball Time: The Future of APY in Crypto

Here's where things get interesting. As crypto grows up, APYs are starting to act less like lottery tickets and more like actual financial products. Big institutions are getting into staking, regulators are paying attention, and the wild west is slowly becoming a proper town with actual roads.

It’s likely crypto will keep offering better yields than traditional finance. It's just that the 10,000% APY days are likely becoming a fond memory.

The Bottom Line

APY in crypto is the same mathematical concept your finance professor taught you, just dressed up in digital clothing and offering significantly better rates. Whether you're staking, lending, or yield farming, understanding APY helps you separate the wheat from the chaff and the legitimate opportunities from dubious schemes.

APY isn't a cheat code to infinite money. It's a tool that, when used wisely, can help your crypto actually work for you instead of just sitting in your wallet looking pretty. But like everything in crypto, it comes with risks that deserve respect and careful consideration.

It’s worth remembering the best APY in the world is worthless if the underlying project disappears into the digital sunset. Choose wisely, diversify smartly, and may your compounds be ever in your favor.

Let's get one thing straight: most "make money while you sleep" crypto promises are complete nonsense. The internet overflows with schemes promising $10,000 monthly returns that usually end with empty wallets and regret.

But you actually can earn passive income with crypto in 2026. The keyword here is "can," not "will automatically" or "guaranteed to". The difference lies in having realistic expectations. We're talking 3-12% annual returns through legitimate methods, not the 300% fairy tales that flood social media.

Thankfully, the crypto passive income landscape has matured since 2021's wild west era. Those 20,000% APY farms that vanished overnight? They're mostly gone (though some still lurk if you fancy yourself some financial Russian roulette). Today's opportunities are more modest but actually sustainable.

This guide covers seven common methods for earning crypto passive income. You'll find beginner-friendly options yielding 3-8% annually, plus riskier strategies that could hit 15-50% if you know what you're doing. We'll also cover the less exciting but crucial stuff: taxes, risks, and how to avoid losing everything to market volatility.

If you want get-rich-quick schemes, look elsewhere. But if you're interested in building a legitimate income stream while participating in the future of finance, let's explore what's actually possible in 2026.

Let the record state that this is educational only and should not be considered financial, investment, or tax advice. Crypto yields are variable and can result in loss of principal. Verify availability, legality, and rates in your jurisdiction before participating.

Understanding crypto passive income

Before diving into specific methods, let's clarify what we mean by "passive income" in crypto. Traditional passive income might be rental properties or dividend stocks - you invest money, then collect regular payments without active work. Crypto passive income works similarly, but with a digital twist and significantly more volatility.

The fundamental difference? Traditional investments might fluctuate 5-10% annually. Your crypto holdings can swing 50% in a week. This means your "passive" income can be passive in name only if you're constantly checking prices and panicking over market moves.

Here's the reality: crypto passive income exists on a risk spectrum. On the safer end, you have crypto savings accounts offering 2-8% APY - similar to high-yield savings but with crypto.

On the riskier end, there's yield farming, where you might earn 50-200% returns, but you could also lose everything to smart contract bugs or market crashes.

All in all, the crypto passive income market has grown substantially. By 2025, over $150 billion was locked in various DeFi protocols, and some major institutions now offer crypto earning products. This legitimacy doesn't eliminate risk, but it does mean you're not dealing with fly-by-night operations (mostly).

Why do people choose crypto for passive income? Beyond potentially higher returns, it offers 24/7 market access, global opportunities, and the ability to start with small amounts. Plus, there's something satisfying about earning yield on assets you believe will appreciate long-term.

Top 7 common methods used by market participants to earn crypto passive income

Low-complexity options (recommended for beginners)

1. Crypto savings accounts

Think of these as high-yield savings accounts, but for crypto. You deposit your coins in custodial yield products from compliant exchanges (availability varies by jurisdiction), and they lend them out or use them productively, and you earn interest.

How it works: Platforms take your deposits and lend them to institutional borrowers or use them in DeFi strategies. You earn a percentage of the profits.

Realistic returns: Expect 2-8% APY depending on the cryptocurrency and platform. Bitcoin typically offers lower rates (2-4%), while stablecoins might yield 4-8%. Each platform’s APYs will vary, ensure you read all the Ts and Cs.

Getting started: Most platforms require simple KYC verification. Deposit your crypto, choose your earning product, and start accumulating interest daily or weekly.

The catch: Your funds aren't FDIC insured like traditional banks. Platform risk is real (remember Celsius and BlockFi's 2022 collapses). Only deposit what you can afford to lose, and research platform stability before committing any amounts.

2. Staking

Staking is like earning dividends for helping secure a blockchain network. Instead of energy-intensive mining, Proof-of-Stake networks rely on validators who "stake" their coins as collateral to process transactions and secure the network.

Popular staking options:

- Ethereum (ETH): typically around 2-4%

- Solana (SOL): commonly 6-8% effective rate over time (depends on inflation & stake)

- Cardano (ADA): typically around 3-5%

- Polkadot (DOT): unbonding is 28 days; rewards vary (often high-single to low-double digits).

*for accurate, real-time staking rewards, see here.

Two approaches exist: Direct staking requires technical knowledge and sometimes significant minimum amounts. Delegated staking through platforms is simpler but typically offers slightly lower returns due to fees.

Important considerations: Many staking arrangements have lock-up periods, so factor in liquidity needs before committing funds.

Getting started: For beginners, exchange-based staking offers the easiest entry. More advanced users can stake directly through wallets or run their own validators for maximum returns.

Medium-complexity methods

3. Crypto lending

Crypto lending involves loaning your crypto to borrowers in exchange for interest payments. It's more hands-on than savings accounts but potentially more profitable.

Platform lending: Services like Aave, Compound, and Kava allow you to supply liquidity to lending pools. Borrowers pay interest, which gets distributed to lenders minus platform fees.

Expected returns: Highly variable based on demand. Stablecoin lending might yield 5-15% APY, while volatile assets can range from 2-25% depending on market conditions.

Risks to consider: Smart contract vulnerabilities, platform hacks, and borrower defaults can impact returns. The 2022 DeFi winter showed that high yields don't always last.

4. Liquidity pools and providing liquidity

Decentralised exchanges (DEXs) like Uniswap and PancakeSwap need liquidity to function. By providing paired assets to liquidity pools, you earn a share of trading fees.

How it works: You deposit equal values of two cryptocurrencies (like ETH and USDC) into a pool. Traders pay fees to swap between these assets, and you earn a portion based on your pool share.

Earning potential: Returns vary widely based on trading volume and fees. Popular pairs might yield 5-30% APY, but this fluctuates with market activity.

Impermanent loss: The biggest risk unique to liquidity provision. If one asset's price changes significantly relative to its pair, you might end up with less value than if you'd simply held the original assets.

It's "impermanent" because prices could return to original ratios, but it becomes permanent if you withdraw during unfavourable price relationships.

Higher-complexity methods (for experienced DeFi users)

5. Yield farming

Yield farming is DeFi's high-stakes game. You move funds between different protocols, chasing the highest returns through complex strategies involving multiple platforms and tokens.

The appeal: Returns can have a wide range - advertised headline APYs can occasionally exceed 50% for short periods, but are highly unstable and often decay quickly.

The reality: Most high-yield farms are unsustainable. They often rely on token rewards that lose value quickly, or they're simply Ponzi-like schemes waiting to collapse.

Who should try this: Only experienced DeFi users who understand smart contract risks, token economics, and can afford total losses. Consider this speculation, not passive income.

6. Dividend-paying tokens

Some crypto projects share profits with token holders, similar to stock dividends.

Examples include:

- KuCoin Token (KCS): pays a bonus from trading fees to eligible holders (terms/eligibility apply)

- NEO: generates GAS for on-chain usage

- VeChain (VET): Produces VTHO tokens for network usage

Returns: Highly variable and dependent on platform success. KCS might yield 2-6% annually in fee sharing, while others provide minimal returns.

7. Masternodes

Masternodes are specialised servers that perform network functions beyond basic transaction processing. They require significant upfront investment but can provide steady returns.

Requirements: Most masternodes need substantial token holdings - often $10,000-$100,000+ worth. You also need technical knowledge to maintain server uptime and security.

For example, Dash requires 1,000 DASH collateral while realised ROI varies with network conditions.

Barriers to entry: High costs, technical requirements, and ongoing maintenance make masternodes unsuitable for most passive income seekers.

Reality check: how much can you actually earn?

Let's crunch some hypothetical numbers based on current market conditions:

Potential $1,000 investment scenarios:

- Crypto savings account (5% APY): $50 annual income

- ETH staking (3.2% APY): $32 annual income

- Stablecoin lending (8% APY): $80 annual income

Potential $10,000 investment scenarios:

- Diversified approach (mix of staking/lending): $400-800 annual income

- Higher-risk DeFi strategies: $1,000-2,000 annual income (with significant loss potential)

Potential $100,000 investment scenarios:

- Conservative crypto portfolio: $4,000-8,000 annual income

- Aggressive yield farming: $10,000-20,000 annual income (extremely high risk)

Compare this to traditional passive income: a 4% dividend stock portfolio on $100,000 yields $4,000 annually. Crypto can potentially beat this, but with much higher volatility and risk.

The volatility factor: Your $10,000 crypto investment might earn $800 in interest, but if the underlying assets drop 30%, you've still lost $2,200 overall. This is why many successful crypto passive income earners focus on stablecoins and accept that they're speculating on both yield and price appreciation.

Tax implications you ought to know

Crypto passive income isn't a tax-free lunch. Most tax authorities treat crypto earnings as regular income, taxed at your ordinary income rate.

Key tax considerations:

- Staking rewards are taxable when received, based on fair market value

- Lending interest counts as ordinary income

- DeFi yields are also taxable, even if paid in obscure tokens

Record-keeping is crucial. Track every reward, airdrop, and interest payment with dates and values. Many platforms provide tax reports, but you're ultimately responsible for accuracy.

International complexity: Tax treatment varies by country. Some nations offer crypto-friendly policies, while others impose heavy taxes or outright bans. Research local regulations or consult professionals for significant amounts.

When to worry: If you're earning more than a few hundred dollars annually in crypto passive income, consider professional tax help. The penalties for getting crypto taxes wrong can be severe.

Risks and how to alleviate them

Crypto passive income isn't just about earning, it's about not losing everything to avoidable risks.

Platform risk: Centralised platforms can fail, get hacked, or freeze withdrawals. Celsius and FTX's collapses wiped out billions in customer funds.

Mitigation: diversify across platforms, research financial health, and never invest more than you can afford to lose.

Smart contract vulnerabilities: DeFi protocols run on code, and code has bugs. Multi-million dollar hacks happen regularly.

Mitigation: stick to audited, established protocols and understand that "decentralised" doesn't mean "safe."

Market volatility: Crypto's wild price swings can eliminate passive income gains quickly.

Mitigation: consider stablecoins for pure yield plays, or accept volatility as part of the crypto investment thesis.

Regulatory risks: Governments can ban or heavily regulate crypto activities overnight.

Mitigation: stay informed about regulatory developments and be prepared to exit positions quickly.

Practical risk management:

- Start small while learning

- Never invest emergency funds

- Diversify across methods and platforms

- Keep detailed records

- Stay informed about protocol changes and risks

Getting started: your first steps

Ready to dip your toes in crypto passive income? Here's a sensible approach:

Start with education: Understand the basics of crypto, wallets, and the specific methods that interest you. Rushing in with poor knowledge is the fastest way to lose money.

Begin conservatively: Try crypto savings accounts or exchange-based staking with small amounts. These offer lower returns but also lower complexity and risk.

Portfolio allocation: Financial advisors often suggest no more than 5-10% of investable assets in crypto, and passive income strategies should be a subset of that. Don't bet the farm.

Platform selection criteria: Look for established companies with good reputations, proper licensing, insurance if available, and transparent fee structures. Avoid platforms promising unrealistic returns.

Security basics: Use hardware wallets for significant amounts, enable two-factor authentication, and never share private keys. The decentralised nature of crypto means lost funds are often gone forever.

Conclusion

Earning passive income with cryptocurrency in 2026 is definitely possible, but it requires realistic expectations and careful risk management. The days of guaranteed 20% returns are over, but legitimate opportunities exist for those willing to do their homework.

The sweet spot for most people lies in conservative strategies: crypto savings accounts, established staking, and perhaps some stablecoin lending. If you're looking for a starting point, Tap Earn offers yield on major assets (including BTC, ETH, XRP, and more) with full withdrawal flexibility.

Remember that "passive" income in crypto often requires more attention than traditional investments. Stay informed, start small, and never invest money you can't afford to lose. The future of finance is evolving rapidly, earning while you learn might be the smartest approach of all.

So you decided to go deeper into the fundamentals of investing and learn what an APY is. You've come to the right place, let's get you started with this perplexing "APY" term.

What Is APY?

In conventional finance, a savings account frequently offers both a low-interest rate and an annual percentage yield (APY). Let's look at what they are and what they mean.

- The Annual Percentage Yield (APY) is the annual return from the principal and accumulated interest on investments or savings, expressed as a percentage.

- The simple interest rate is the amount earned on the original deposit.

Assume an account at a bank offers a yearly interest rate of 5%. If someone deposits €2,000 into the account, it will be worth €2,100 after a year with the 5% yearly interest rate.

The Difference Between Interest Rate, APY and APR

The APY takes into account the impact of compounding, whereas the interest rate does not. The APY is the projected rate of return earned annually on a deposit after taking compound interest into account.

Compounding interest is the interest that a person accrues from their initial deposit, as well as the interest they earn from their original investment (or in other words, the initial deposit amount plus the interest generated).

The terms APY and APR are frequently used interchangeably, although they represent two different things. These words are sometimes confused due to their close resemblance. However, APY and APR aren't the same things.

The APR (annual percentage rate) is a formula that determines how much interest you'll pay when borrowing money and is the rate of return earned if your funds are invested in an interest-bearing account.

When a person takes out a loan, their lender sets an APR that varies based on the loan. APRs are either fixed or fluctuating depending on the type of loan the user requires. However, the APR is a rather basic interest rate and does not take compounding into account, unlike APY.

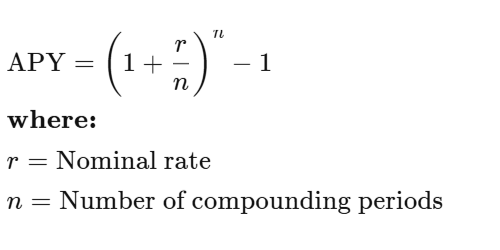

How Is APY Calculated?

APY represents your rate of return, also known as the amount of earnings or profit you can make. Of course, your ultimate earnings will vary depending on how long you keep your assets invested while the holding period will influence how much you will earn.

APY measures the rate of the annual return earned on any amount of money or investment after taking into account compounding interest.

The following is the formula for calculating APY:

APY = (1 + p/n)ⁿ − 1

Where:

p = periodic rate of return (or annual APR)

n = number of compounding periods each year

Bear in mind that an APY can be calculated in a variety of ways depending on the provider.

The Bottom Line

APY is one of the most useful numbers in finance once you know how to read it. It tells you not just what rate you're earning, but what your money actually grows to after compounding does its work, which is always more than the headline interest rate suggests. The higher the compounding frequency, the more that gap widens.

In crypto, APY figures can vary significantly depending on the asset, the platform, and market conditions. That makes it worth comparing carefully rather than taking advertised rates at face value.

If you want to see APY in practice, Tap Earn offers yield on assets including BTC, ETH, SOL, USDT, and USDC, with no lock-up periods and no minimum commitment. Deposit what you want, earn on your terms, withdraw whenever you like.

If you're looking to tap into the world of earning passive income in the cryptocurrency space, you've come to the right place. While both yield farming and staking provide this service, they offer slightly different means of getting there. In this article, we're exploring yield farming vs staking, and how to get started.

Both yield farming and staking fall under the DeFi (decentralized finance) umbrella. This aspect of the industry allows users to lend and borrow cryptocurrencies, similar to the traditional banking system. DeFi lending platforms and liquidity pools provide users with an alternative way to earn passive income, offering varying interest rates and methods of doing so.

What Is Yield Farming?

Yield farming involves users lending their tokens to DeFi lending platforms. Investors can decide which cryptocurrencies they would like to use, and where they would like to invest their funds. The options range from lending platforms like Compound and Aave to decentralised exchanges (DEXs) like PancakeSwap and Uniswap.

On a lending platform, the process typically involves a user depositing their funds on the platform, receiving both an APY (annual percentage yield) and tokens native to the platform.

On DEXs, this alters slightly in that users need to provide one of the pair of coins as per the liquidity pool they wish to engage in. Users will then receive a percentage of the rewards of the pool based on the amount provided.

Passive income from yield farms comes from the interest paid to the borrower or the users of the liquidity pool. Yield farming is considered to be a more reliable option than trading cryptocurrency as yield farming uses smart contracts or automated market makers (AMM) to facilitate all trades. Top yield farms can be found on Ethereum, Polygon, Binance Smart Chain (BSC) and Fantom.

What Is Staking?

Staking involves locking your cryptocurrencies in a smart contract. In order to properly understand staking one will need to have a brief understanding of the Proof-of-Stake (PoS) consensus.

While Bitcoin uses a Proof-of-Work mechanism to validate transactions through miners solving computational problems, PoS instead uses a less energy-intensive mechanism based on validators staking their cryptocurrency and generating new blocks. This is typically done in a selective process, with each validator getting a turn based on the amount that they stake. By staking in the network the validators are providing collateral to prove they are not bad actors. Ethereum is currently moving to a PoS consensus, with several other big cryptocurrencies already there.

To earn a passive income through staking users can opt to become validators on a network or participate in liquidity pools, alternatively, they can do so through a wallet or exchange that supports such activities. Pools vary in their conditions, lock-in periods (the amount of time the funds are required to stay there) and APYs.

As each staking process changes from cryptocurrency to platform, ensure that you do thorough research on the one you wish to take part in. Here are a few of the top staking coins: Ethereum (ETH), Cardano (ADA), PancakeSwap (CAKE), and Polygon (MATIC).

Yield Farming vs Staking

While both offer excellent means of earning a passive income in the crypto space, the main difference is that yield farming involves depositing one's funds onto a DeFi platform while staking typically involves using one's funds to support a blockchain network or help validate transactions.

Profits

Staking usually yields profits of around 5% and is expressed with a definite APY. Yield farming on the other hand can provide up to 100% returns but will require a well throughout investment strategy.

Rewards

Staking rewards are given to validators as incentives for generating new blocks while yield farming rewards fluctuate with the token's price changes and are determined by the liquidity pool.

Lock-In Periods

Some staking pools require users to lock in their funds for a certain period of time, often also stipulating a minimum amount. Yield farming does not require either of these.

A third option worth noting, a product like Tap Earn offers yield on assets including BTC, ETH, and SOL with no lock-up periods whatsoever and no minimum deposit, combining the flexibility of yield farming with considerably less complexity.

Security

Staking criteria are determined by the network and tied to the blockchain's consensus, users staking their funds are only at risk of losing them if they have ill intentions or act badly. Yield farming is less secure in that it relies on smart contracts and DeFi protocols, which can be susceptible to hackers if not created correctly.

Which Is Better: Yield Farming vs Staking?

Both yield farming and staking provide options in which one can earn passive income in the crypto space. While each has its advantages and disadvantages, the one offers a safer course while the other a more high-risk high reward endeavour. When it comes to deciding between the two, users should first establish how much risk they are willing to take and how comfortable they are in the DeFi space, followed by what kind of investors they would like to be.

Picture this: You're scrolling through DeFi platforms, and suddenly you see two different projects. One screams "12% APR!" while another boasts "12% APY!" Your brain probably thinks, "Same, right?"

Wrong. Very wrong.

When it comes to comparing interest rates, APR and APY might look like twins… but they’re not. Far from it. The difference between them can determine whether you grow your savings or overpay on a loan. In this guide, we’ll break down what APR and APY really mean, how they work in banking, lending, and crypto, and how understanding them can help you make smarter financial decisions.

Key Takeaways

- APR (Annual Percentage Rate) shows the yearly cost of borrowing, including interest and certain fees.

- APY (Annual Percentage Yield) reflects your total yearly return, factoring in compounding.

- For borrowers, lower APR = lower total cost. For savers, higher APY = higher returns.

- In crypto and DeFi, compounding frequency can turn modest APRs into much higher APYs.

APY vs APR: The Essential Difference

At a glance, APR tells you how much interest you’ll pay (or earn) over a year, without compounding. APY, on the other hand, includes compounding, the process where interest earns more interest over time.

When comparing financial products, whether a credit card, savings account, or staking pool, this distinction matters. For borrowers, APR reveals the true cost of debt, while for investors, APY highlights the power of compound growth.

TL;DR. APR is about cost, APY is about growth. Knowing which one applies helps you choose between competing offers with confidence.

What Is APR (Annual Percentage Rate)?

APR represents the yearly interest rate charged to borrow money, or the rate you earn before compounding if you lend it. It includes interest and certain fees, helping you understand the total cost of credit.

APR is widely used in credit cards, personal loans, mortgages, and auto financing. For example, if your credit card has an 18% APR, you’ll pay 18% interest on any carried balance. Fixed-rate loans maintain the same APR, while variable-rate loans fluctuate with market conditions and Federal Reserve changes.

Example: Borrow $10,000 at 10% APR for one year. You’ll owe $1,000 in interest. Simple and transparent, without compounding surprises.

What Is APY (Annual Percentage Yield)?

APY measures how much your money grows over a year, including compounding. It reflects how often your interest is added to your balance (daily, monthly, or annually) which then generates more interest.

This is the standard metric for savings accounts, money market accounts, and certificates of deposit (CDs). Banks and digital financial platforms often advertise APY because it paints a more complete picture of earning potential.

Example: Deposit $10,000 in an account with a 5% APY, compounded monthly. After one year, your balance grows to $10,511, slightly higher than a flat 5% APR return.

The more frequent the compounding, the greater the growth, especially important in DeFi protocols that compound every few minutes.

APR vs APY in Different Financial Products

Credit Cards and Loans (APR)

When borrowing, APR helps you understand the true borrowing cost. For instance, if a mortgage advertises a 6.5% APR, that includes both the interest and certain closing costs.

Car loans, student loans, and credit cards use APR to keep comparisons straightforward across lenders. The key? Lower APR = less expensive borrowing.

Savings and Investment Accounts (APY Focus)

If your goal is wealth building, APY is your guide. A high-yield savings account with 4.5% APY grows faster than one with 4% because compounding quietly amplifies returns.

For certificates of deposit (CDs) or fixed deposits, APY helps you compare the real impact of compounding frequency.

Cryptocurrency and DeFi (Both APR and APY)

In crypto lending, staking, or yield farming, both metrics appear and can be easily confused.

- APR shows base rewards (without compounding).

- APY assumes you’re constantly reinvesting.

Example: A DeFi pool may show 100% APR, but with daily compounding, it becomes 171% APY. The key is understanding how often you can claim rewards and whether gas fees make compounding worthwhile.

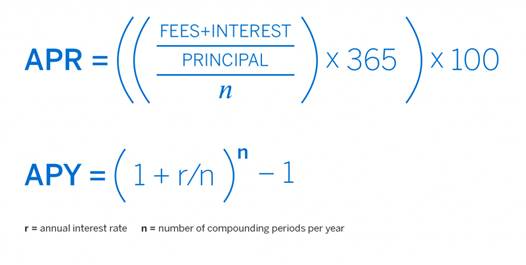

How to Calculate APR vs APY

To compare offers correctly, you can calculate one from the other:

Example: 12% APR compounded monthly

APY = (1 + 0.12/12)^12 - 1 = 12.68%

Compounding more frequently increases APY slightly each time.

Which Should You Focus On?

- If you’re borrowing, prioritize APR. It reflects the total cost of debt.

- If you’re saving or investing, look at APY. It shows how compounding boosts earnings.

- In crypto, check both. APR tells you the base reward, APY reveals potential if you reinvest.

When comparing offers, always read the fine print; frequency, fees, and conditions can shift the real value dramatically.

Common Misconceptions and Pro Tips

Myth: “APY is always better.”

Reality: Only if compounding happens, or if you reinvest earnings.

Myth: “APR ignores compounding, so it’s useless.”

Reality: APR helps borrowers compare costs clearly.

Pro Tip: Use online APR-to-APY calculators for quick comparisons. They’re free and eliminate guesswork.

The Bottom Line

APR and APY aren't just different ways of saying the same thing, they represent two different approaches to measuring returns.

When you see APR, you're looking at simple interest calculated over a year. When you see APY, you're seeing what happens when earnings get reinvested and compound over time. Both are valid measurements, just showing different scenarios.

This distinction becomes more noticeable with higher interest rates. A 50% APR becomes closer to 65% when compounded daily. The higher the base rate, the bigger the difference between these two numbers becomes.

Understanding which one you're looking at helps you compare options accurately. APR gives you the base rate, while APY shows the potential with compounding factored in.

Once you get the hang of spotting the difference, those financial offers suddenly make a lot more sense. No more squinting at numbers wondering why similar-sounding deals seem to work out so differently. It's like finally understanding why some recipe measurements are in cups and others in ounces.

If you want to put that knowledge to work, Tap Earn lets you earn APY on assets like BTC, ETH, SOL, and stablecoins, with no lock-up periods, so you stay in control of your funds.

.webp)

.webp)