Some crypto companies are fully compliant, fully regulated, and still can't keep their bank accounts. Learn why the financial system is quietly freezing them out.

Keep reading

Why can't a fully compliant, regulated crypto business secure a bank account in 2025?

If you're operating in this space, you already know the answer. You've lived through it. You've submitted the documentation, walked through your AML procedures, and demonstrated your regulatory compliance… only to be rejected. Or worse still, waking up to find your existing account frozen, with no real explanation and no path forward.

This isn't about isolated cases or bad actors being weeded out. It's a pattern of systematic risk aversion that's creating real barriers to growth across the entire sector, and it's throttling one of the most significant financial innovations of our generation.

We're Tap, and we're building the infrastructure that traditional banks refuse to provide.

The Economics Behind the Blockade

Let's examine what's actually driving this exclusion, because it's rarely about the reasons banks cite publicly.

The European Banking Authority has explicitly warned against unwarranted de-risking, noting it causes "severe consequences" and financial exclusion of legitimate customers. Yet the practice continues, driven by two fundamental economic pressures that have nothing to do with your business's actual risk profile.

The compliance cost calculation

Financial crime compliance across EMEA costs organizations approximately $85 billion annually. For traditional banks, the math is simple: serving crypto businesses requires specialized expertise, enhanced monitoring, and ongoing due diligence. As a result, it's cheaper to reject the entire sector than to build the infrastructure needed to serve it properly.

The regulatory capital burden

New EU regulations impose a 1,250% risk weight on unbacked crypto assets such as Bitcoin and Ethereum. This isn't a compliance requirement; it's a capital penalty that makes crypto exposure commercially unviable for traditional institutions, regardless of the actual risk individual clients present.

In the UK, approximately 90% of crypto firm registration applications have been rejected or withdrawn, often citing inadequate AML controls. Whether those assessments are accurate or not, they've created the perfect justification for blanket rejection policies.

The result? Compliant businesses are being treated the same as bad actors; not because of what they've done, but because of the sector they're in.

The Real Cost of Financial Exclusion

Financial exclusion isn’t just an hiccup; it creates tangible operational barriers that ripple through every part of running a crypto business.

Firms that have secured MiCA authorization, built robust compliance programs, and met regulatory requirements can find themselves locked out of basic banking services. Essential fiat on-ramps and off-ramps remain inaccessible, slowing payments, limiting growth, and complicating cash flow management.

Individual cases illustrate the problem vividly as well. Accounts are closed because a business receives a payment from a regulated exchange. Others are dropped with vague references to “commercial decisions,” offering no substantive justification. Founders frequently struggle to separate personal and business finances, as both are considered too risky to serve.

The irony is striking. By refusing service to compliant businesses, traditional banks aren’t mitigating risk; they’re amplifying it. Forced to operate through less regulated channels, these legitimate firms face higher operational and compliance risks, slower transactions, and reduced investor confidence. Over time, this slows innovation, and raises the cost of doing business for firms that are legally and technically sound.

Debanking Beyond Europe: U.S. Crypto Firms Face Their Own Challenges

Limited access to banking services isn’t exclusive to Europe. Leading firms in the U.S. crypto industry have faced numerous challenges regarding the banking blockade. Alex Konanykhin, CEO of Unicoin, described repeated account closures by major banks such as Citi, JPMorgan, and Wells Fargo, noting that access was cut off without explanation. Unicoin’s experience echoes a broader sentiment among crypto executives who argue that traditional financial institutions remain wary of digital asset businesses despite recent policy shifts toward a more pro-innovation stance.

Jesse Powell, co-founder of Kraken, has also spoken out about being dropped by long-time banking partners, calling the practice “financial censorship in disguise.” Caitlin Long, founder of Custodia Bank, recounted how her institution was repeatedly denied services. Gemini founders Tyler Winklevoss and Cameron Winklevoss shared similar frustrations.

These experiences reveal a pattern many in the industry interpret as systemic risk aversion. Even in a market as large and mature as the United States, crypto-focused businesses continue to encounter obstacles in maintaining basic financial infrastructure. The issue became especially acute after the collapse of crypto-friendly banks such as Silvergate, Signature, and Moonstone; institutions that once served as key bridges between fiat and digital assets. Their exit left a gap few traditional players have been willing to fill.

Why Tap Exists

The crypto industry has reached an inflection point. Regulatory frameworks like MiCA are providing clarity. Institutional adoption is accelerating. The technology is proven and tested. But the fundamental infrastructure gap remains: access to business banking that actually works for digital asset businesses.

This is precisely why we built Tap for Business.

We provide business accounts with dedicated EUR and GBP IBANs specifically designed for crypto companies and businesses that interact with digital assets. This isn't a side offering or an experiment, it's our core focus.

Our approach is straightforward

We built our infrastructure for this sector

Rather than retrofitting traditional banking systems to reluctantly accommodate crypto businesses, we designed our compliance, monitoring, and operational frameworks specifically for digital asset flows. This means we can properly assess and serve businesses that others automatically reject.

We price in the actual risk, not the sector

Blanket rejection policies exist because they're cheap and simple. We take a different approach: evaluating each business based on their actual controls, compliance posture, and operational reality. It costs more, but it's the only way to serve this market properly.

We're committed to sector normalization

Every time a legitimate crypto business is forced to operate without proper banking infrastructure, it reinforces outdated stigmas. By providing professional financial services to compliant businesses, we're helping demonstrate what should be obvious: crypto companies can and should be served by the financial system.

It isn't about taking on risks that others won't. It's about properly evaluating risks that others refuse to understand.

Moving Forward

The industry is maturing. Regulatory clarity is emerging. Institutional adoption is accelerating. But you can't put your business on hold while traditional banks slowly catch up to reality.

That's not sustainable in the long run.

As a firm, you shouldn't have to beg for a bank account. You shouldn't have to downplay your crypto operations just to access basic financial services. And you certainly shouldn't have to accept that systematic exclusion with little to no explanation other than “It’s just how things are."

The crypto sector is building the future of finance. Your banking partner should believe in that future too. If you're ready to work with financial infrastructure built for your business, not in spite of it, here we are.

Talk today with one of our experts to understand how we can help your business access the banking infrastructure you need.

NEWS AND UPDATES

LATEST ARTICLE

.jpg)

The "redirect to bank" experience is dying. Today's consumers expect financial services to be invisible, integrated, and immediate.

The numbers confirm this story. The global embedded finance market is projected to reach $606 billion this year, growing to $7.2 trillion by 2030. But this isn't just about fintechs disrupting traditional banking anymore. We're witnessing something far more profound: the financialisation of every industry.

In an increasingly competitive landscape, embedded finance has become the new battleground for customer loyalty, operational efficiency, and revenue diversification.

From healthcare providers offering patient financing to property management companies issuing tenant payment cards, businesses across every sector are discovering that controlling the financial experience isn't just about convenience; it's becoming more about survival.

And the companies winning this race aren't necessarily the ones with the deepest financial services expertise. They're the ones that recognise a fundamental truth: every business is becoming a financial services company, whether they realise it or not. Let’s explore this narrative.

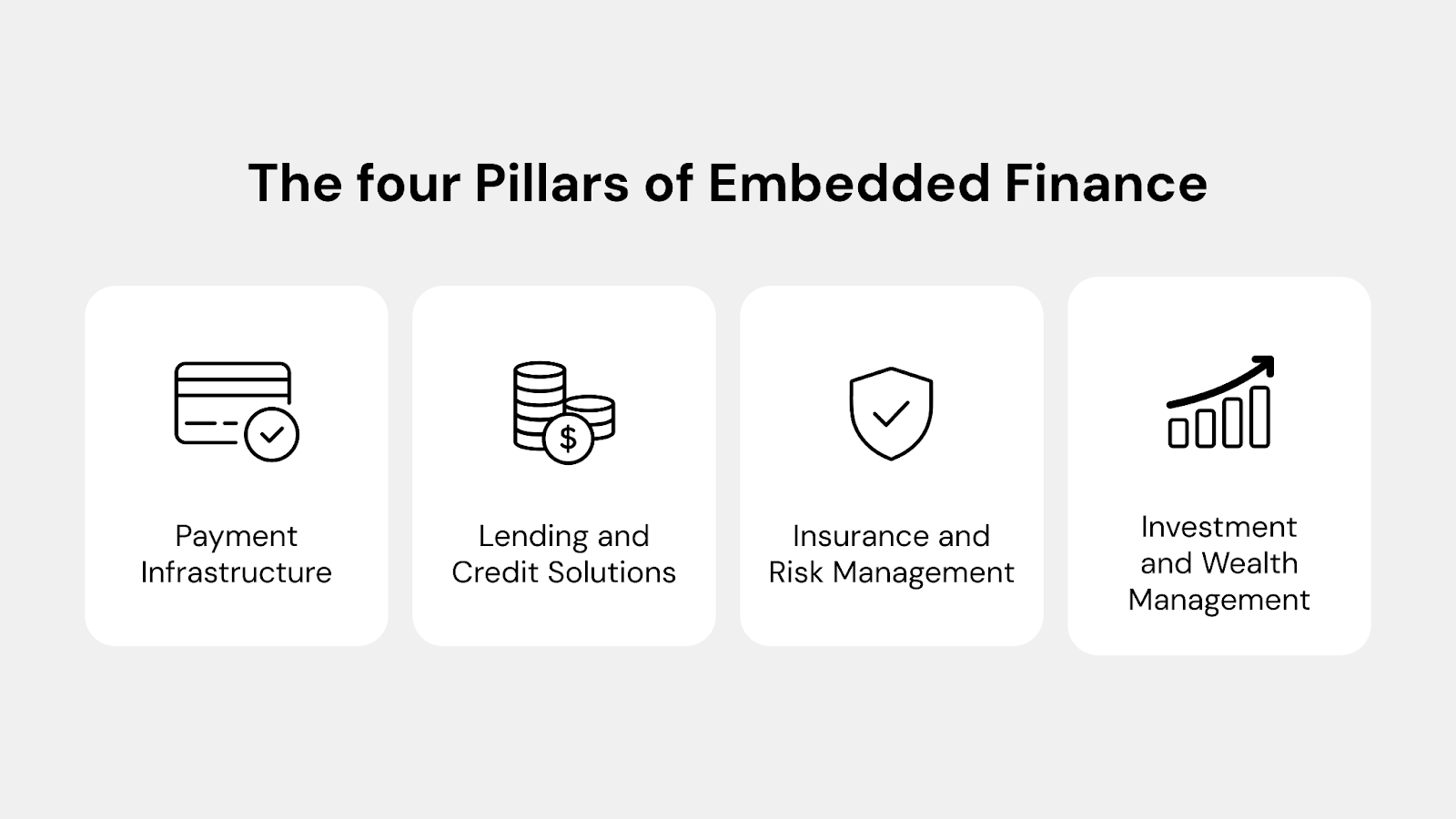

Mapping the embedded finance ecosystem

Understanding embedded finance requires looking beyond just payments to see the full ecosystem of financial services being woven into non-financial platforms. To put it more simply: it’s less about processing transactions and more about creating comprehensive financial experiences.

The four pillars of embedded finance

Payment infrastructure forms the foundation, encompassing everything from card issuing and digital wallets to real-time transfers and cross-border payments. This is where most companies start their embedded finance journey, but it's just the beginning.

Lending and credit solutions represent the next evolution, allowing platforms to offer instant financing, buy-now-pay-later options, and dynamic credit lines. A logistics company might offer cash advances to drivers, while an e-commerce platform provides inventory financing to sellers.

Insurance and risk management services are increasingly embedded into platforms where risk naturally occurs. For instance, ride-sharing apps offer trip insurance, rental platforms provide property protection, and gig economy apps include accident coverage.

Investment and wealth management complete the picture, with platforms offering everything from micro-investing features to full-service wealth management integrated into everyday spending activities.

The technology stack revolution

The magic happens in the middleware, where the API layers connect user-facing apps to complex financial infrastructure. Modern embedded finance platforms take away the complexity of banking operations, compliance frameworks, and regulatory requirements, allowing any company to offer sophisticated financial services through simple API calls.

And making this technology accessible is key. Where banks once had moats built from regulatory expertise and infrastructure investments, today's embedded finance platforms have levelled the playing field.

For instance, a small property management company can now offer the same calibre of financial services as a major corporation, all through cloud-based APIs and white-label solutions.

Industry deep dives: the unexpected financial innovators

The most compelling embedded finance stories are happening in industries you might not expect. Let’s explore how sectors far removed from traditional finance are leveraging embedded financial services to transform their operations:

Healthcare

Healthcare providers are embedding finance to solve patient payment collection challenges. Instead of redirecting patients to external lenders, dental practices now offer instant financing approvals directly within their systems, while telemedicine platforms integrate HSA/FSA payments and prescription processing.

The result: improved patient experience, reduced administrative overhead, and better provider cash flow.

Real estate

Proptech companies are offering customisable debit cards with built-in credit-building rewards and automated reminders, boosting tenant retention and on-time payments. While other property management utilise embedded insurance to replace traditional security deposits.

Real estate platforms can now handle everything from mortgage pre-approval to maintenance payments in one interface, while construction businesses offer instant contractor payments with automated expense tracking.

Education

Educational institutions embed financial services beyond tuition through campus spending cards, instant student aid disbursement, and skill-building microloans.

EdTech platforms offer employer-sponsored training payment cards, while international education programs solve cross-border payment complexity with embedded foreign exchange and instant fund transfers for students abroad.

Supply chain

Manufacturing and supply chain businesses optimise financial flows through embedded supplier financing and inventory funding solutions. Logistics companies provide drivers with instant payouts and controlled fuel cards, while procurement platforms automate cross-border payments and approval workflows, treating money movement as strategically as inventory management.

Entertainment

Lastly, gaming and entertainment platforms create virtual economies connected to real-world branded payment cards, while venues embed payment plans for premium experiences and refund insurance.

Creator economy platforms also provide comprehensive financial services, including instant payments, business banking, tax preparation, and investment opportunities, becoming full-service financial providers for creative professionals.

The business case: ROI beyond revenue

The financial benefits of embedded finance extend far beyond direct revenue generation. More and more businesses are starting to discover that embedded financial services can drive value through several channels at the same time.

Direct financial benefits

- Revenue diversification through interchange fees, transaction processing margins, and financial product revenue sharing can represent significant income streams. A B2B marketplace processing $100 million annually might generate $1-2 million in additional revenue through embedded card programs alone.

- Float management opportunities arise when companies hold customer funds temporarily. Even small balances across large customer bases can generate meaningful interest income when managed professionally.

- Premium service monetisation allows companies to charge higher fees for enhanced financial services while improving the customer experience. Express payment options, enhanced spending controls, and premium support can command price premiums.

Indirect value creation

- Customer lifetime value extension happens when financial services create switching costs and deepen platform engagement. Customers using embedded financial services typically show 20-30% higher retention rates and increased platform usage.

- Operational efficiency gains from automated payment processing, reduced manual reconciliation, and streamlined expense management can reduce operational costs (in midmarket companies) by 30-50% while improving accuracy and reporting capabilities.

- Data insights and behavioural analytics from financial transactions provide thorough visibility into customer behaviour, enabling better product development, pricing optimisation, and risk management decisions.

Implementation strategies & considerations

Successfully implementing embedded finance requires systematic planning and strategic decision-making focused on core business objectives.

Build vs buy vs partner framework

Cost and speed: Internal development takes 18-36 months with significant compliance costs, while white-label solutions launch in 6-12 weeks. Partnering with licensed providers reduces regulatory burden and accelerates time-to-market.

Integration options: API-first architecture enables flexible system integration. White-label solutions offer complete brand control but require more work, while co-branded approaches launch faster with shared visibility.

Implementation strategy: Consider phased rollouts (for instance, starting with basic payments and gradually adding layers such as lending or insurance) to reduce risk while enabling customer feedback integration.

Risk management essentials

Compliance: KYC/AML verification, fraud monitoring, and data security must meet financial services standards. Again, partnering with established platforms provides compliance expertise across multiple jurisdictions while maintaining a seamless user experience.

How to implement embedded finance into your business

Implementing embedded finance successfully requires systematic planning and execution. Companies that take a structured approach are more likely to achieve their objectives while minimising implementation risk.

Assessment phase

Current payment flow analysis should map all existing financial touchpoints and identify friction points, manual processes, and opportunities for improvement. Understanding current state operations provides the foundation for embedded finance strategy.

Customer journey mapping reveals where financial services integration could improve experience and create value. Look for moments where customers currently leave your platform for financial services or where payment friction creates abandonment.

Competitive landscape evaluation helps identify differentiation opportunities and best practices. Understanding how competitors and adjacent industries use embedded finance provides insight into customer expectations and market opportunities.

Strategy development

Use case prioritisation should focus on the highest-impact opportunities that align with your core business objectives. Start with use cases that solve existing problems rather than creating entirely new functionalities.

ROI modelling and business case development requires realistic assumptions about adoption rates, revenue potential, and implementation costs. Include both direct financial benefits and indirect value creation in ROI calculations.

Partner evaluation and selection should consider platform capabilities, compliance coverage, integration complexity, and long-term strategic alignment. The right partner becomes an extension of your team rather than just a vendor.

Implementation & launch

MVP development and testing allows for learning and iteration before full-scale launch. Start with core functionality and add features based on user feedback and usage patterns.

Pilot program execution with selected customer segments provides real-world validation while limiting risk exposure. Use pilot results to refine processes and optimise user experience.

Scale-up and optimisation based on pilot learnings and market feedback. Successful embedded finance implementations evolve continuously based on customer needs and market opportunities. Be sure to have your finger on the pulse.

The inevitable future

Embedded finance is more than a passing trend: it represents a fundamental shift in business operations. Companies that move early can gain lasting advantages through stronger customer relationships, new revenue streams, and greater efficiency.

The technology to implement it quickly and cost-effectively is already available, and customers increasingly expect seamless financial integration. The real question isn’t if embedded finance will become standard - it’s whether your business will lead or follow.

Don't let competitors control your customers' financial experience. Get in touch with us to explore white-label solutions that can increase retention, reduce costs, and generate new revenue quickly and compliantly. We’re here to help you transform your business in weeks, not years.

.webp)

Ready to cut through traditional banking barriers and dive into the world of crypto payments? From buying falafels at your local cafe to luggage from a store in Japan, crypto payments are fast, cost-effective, and easier than you can imagine.

In this guide, we will walk you through exactly how to pay with crypto - from opening your account to making your first transaction. By the end, you'll have the confidence to make crypto payments anywhere, anytime.

Is paying with crypto legal?

Let's address the elephant in the room first. Paying with crypto is legal in most major markets, including the United States, the European Union, Canada, and the UK. However, some countries, like China and India, have restrictions on crypto transactions.

Here's the global snapshot:

- Fully legal: US, EU, UK, Canada, Australia, Singapore, Switzerland

- Restricted or banned: China, India (limited use), Russia (complex regulations)

- Grey areas: Some developing nations with evolving frameworks

Why does this matter? Operating within legal boundaries protects you from compliance issues and ensures your transactions won't be flagged or reversed. Rest assured, Tap only operates in jurisdictions where crypto payments are fully compliant.

How crypto payments work

Think of crypto payments like sending an email instead of traditional mail. With email, your message goes directly from your computer to the recipient's inbox through the internet.

Similarly, crypto payments travel directly from your cryptocurrency wallet to the merchant's wallet through a blockchain network - no banks or financial middlemen required.

Here's what happens behind the scenes:

- Your payment gets recorded on a decentralised ledger (blockchain)

- Multiple computers verify the transaction

- Once confirmed, the payment is permanent and irreversible

- The entire process typically takes minutes, not days

This system eliminates the need for banks, reduces fees, and works 24/7 globally.

Common payment methods

There are several ways to pay with crypto, each suited for different situations. Here are the two most popular:

On-chain wallet transfers involve scanning a QR code or copying a wallet address to send payments directly from your wallet to theirs. This method works well for peer-to-peer transactions and in-store payments. As a side note: Tap users can enjoy free transfers between users, anywhere in the world.

Tap’s crypto-backed debit card lets you spend your crypto anywhere Mastercard and Visa are accepted. The card automatically converts your crypto to fiat at the point of sale.

Setting up your Tap account

Here’s how to get started:

- Download the app and create your account.

- Complete the quick identity check.

Since Tap is licensed and regulated, we ask for some basic verification - just like any trusted fintech app. It only takes a few minutes. - Once you're approved, you're in.

You’ll be ready to explore the crypto world.

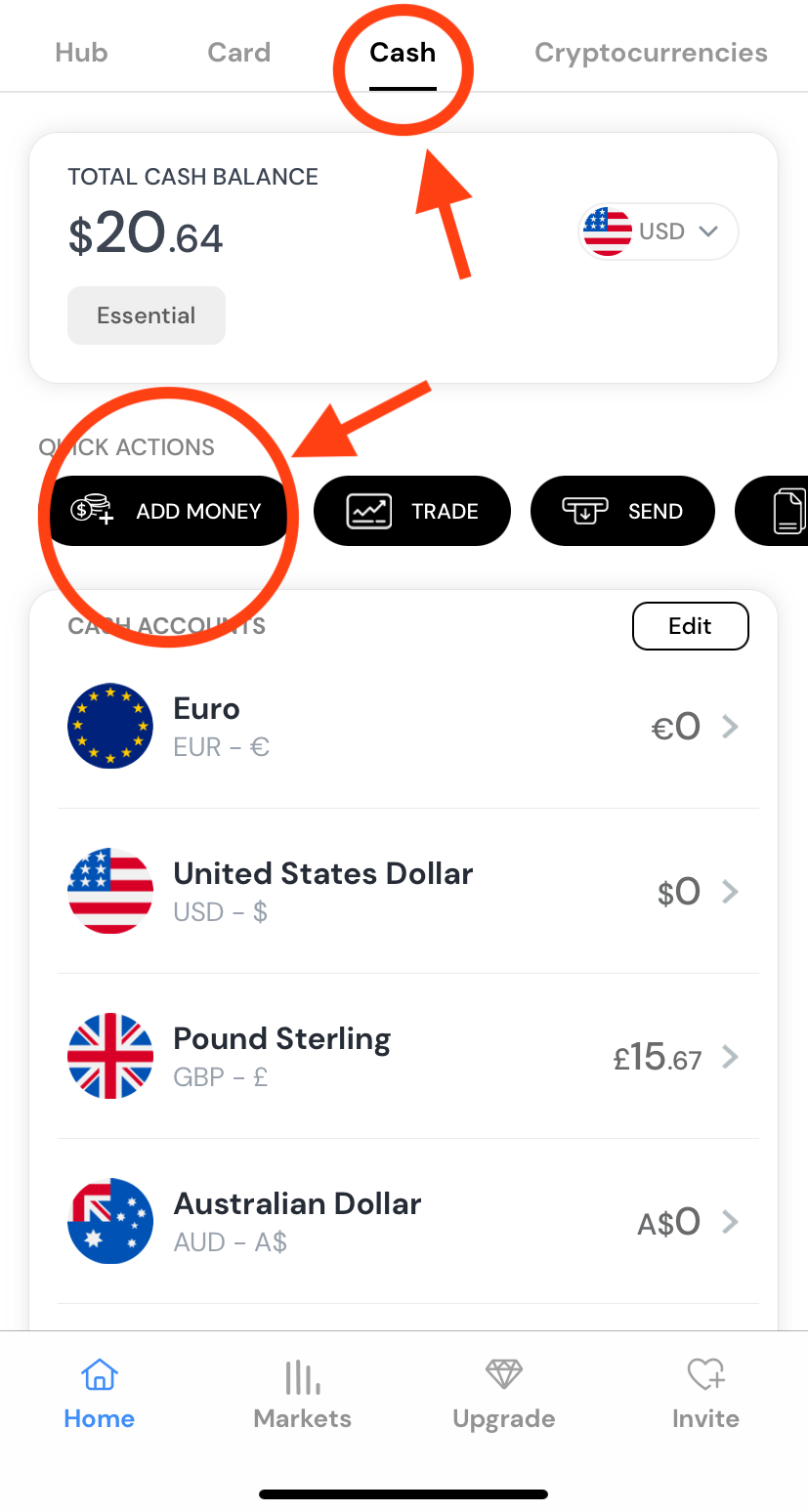

Order your Tap card

Tap the “Card” tab in the app (between Hub and Cash), and follow the steps to order your card. It’ll arrive in a few days, depending on where you are.

Now all you need is crypto.

Topping up your wallet is simple.

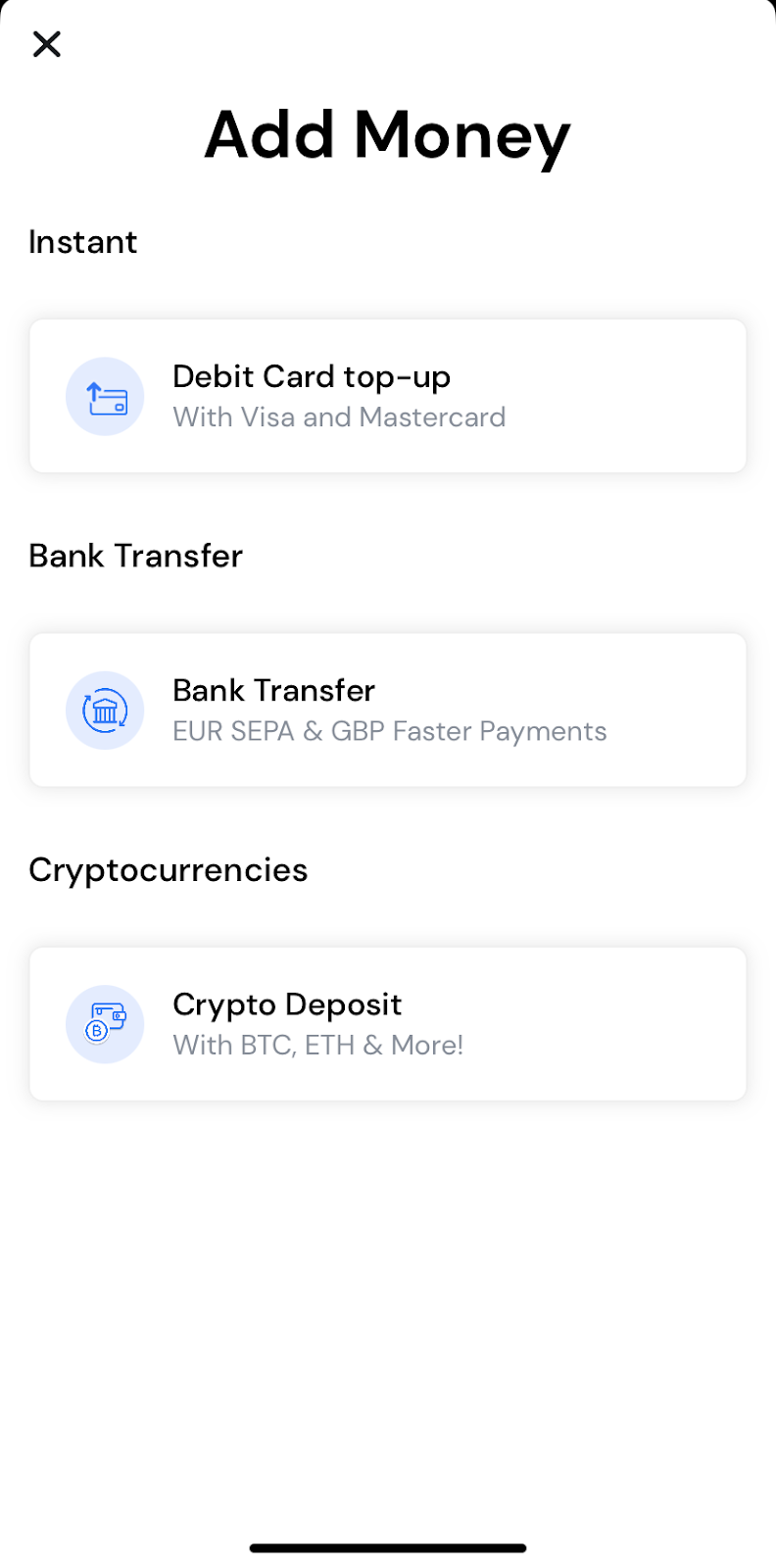

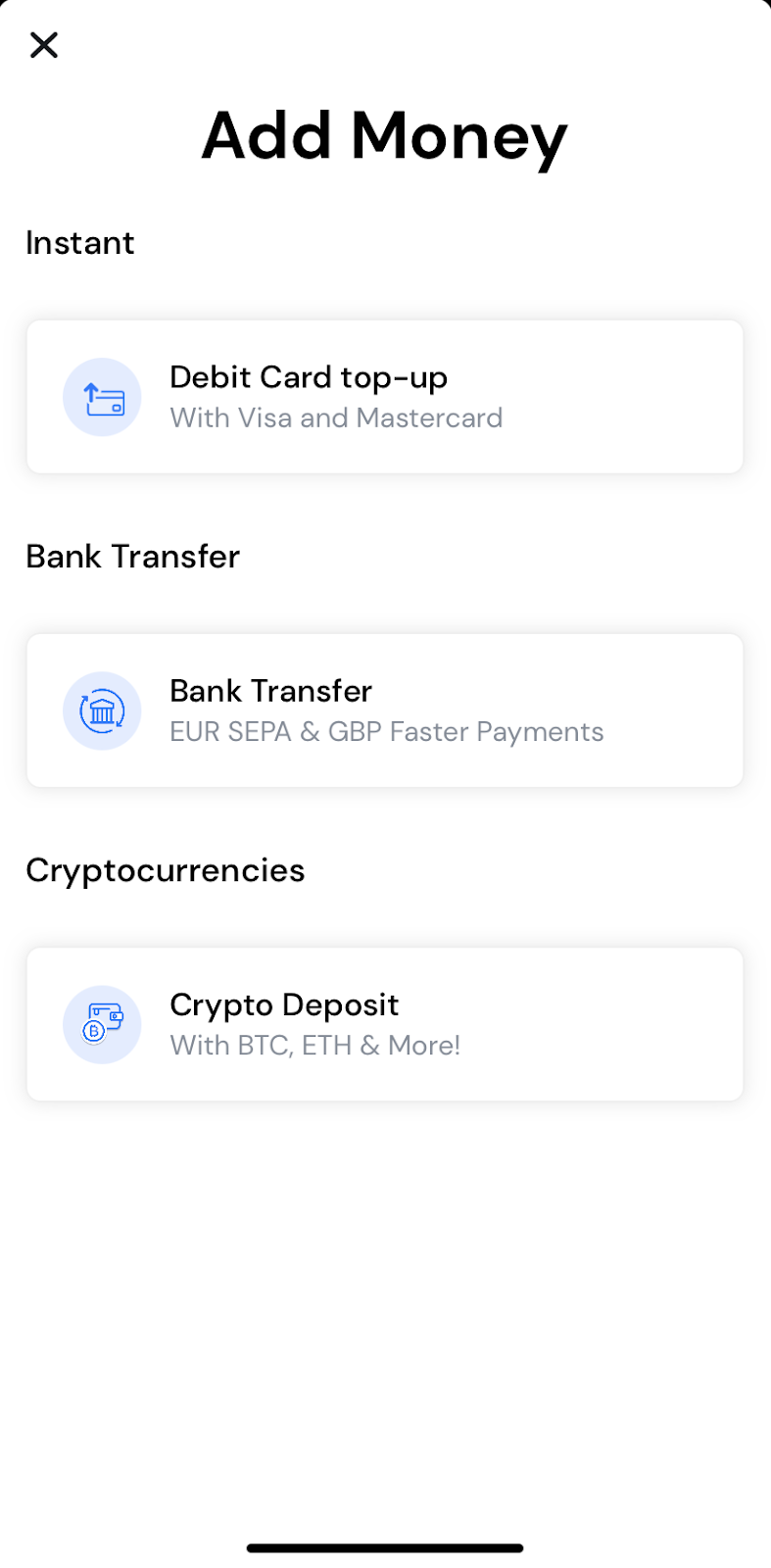

To load fiat (USD, EUR, GBP, AUD, CAD, CHF, JPY), tap “Cash” in the top menu and hit the black “Add Money” button. Choose your preferred method and follow the instructions.

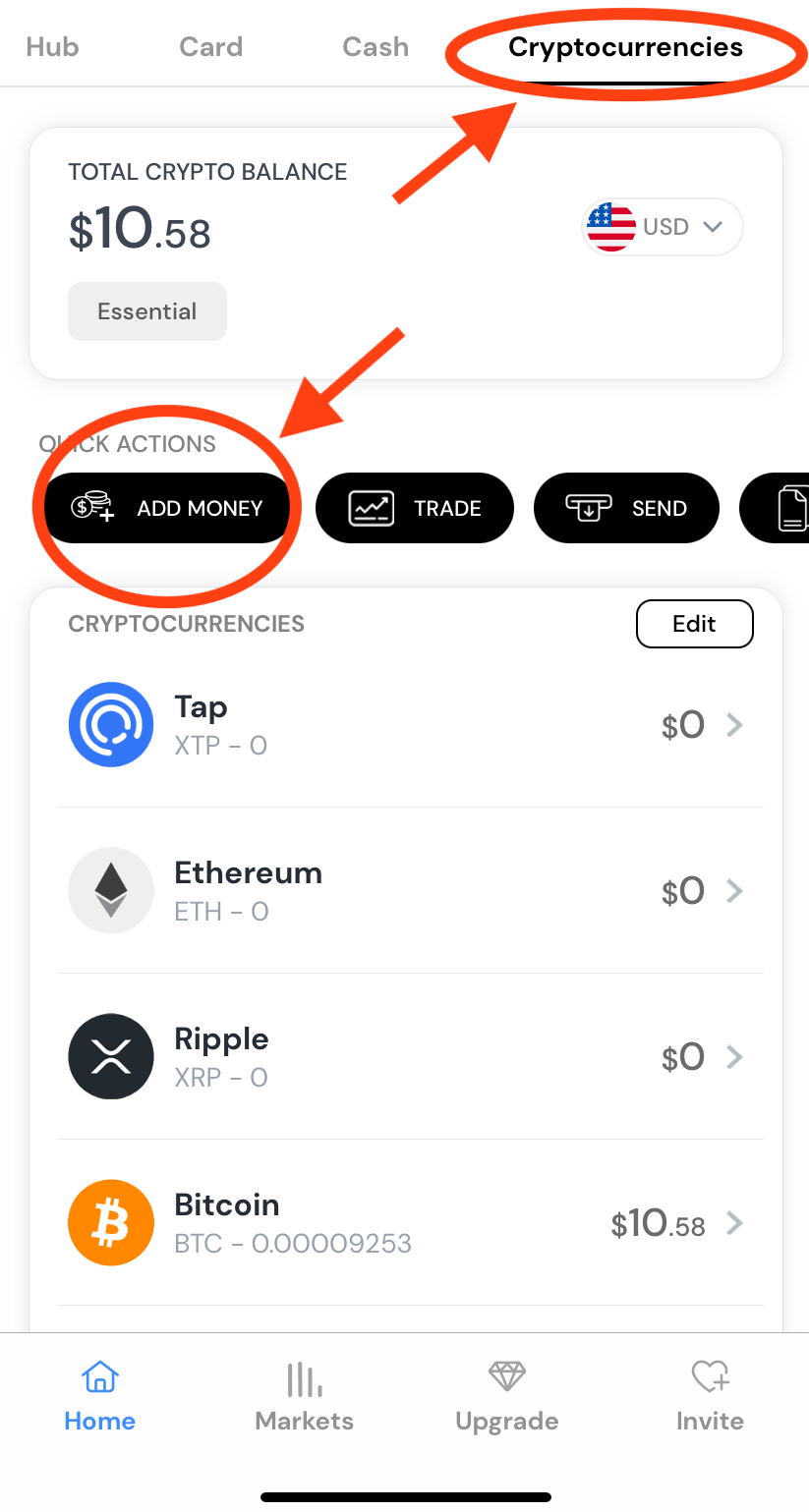

If you already have crypto, select Cryptocurrencies from the top menu, Add Money, and then the last option (Crypto Deposit). It’ll take a few minutes to clear (depending on the network).

When your card arrives, move funds to the Card section of your wallet, and you’re all set.

Step-by-step: how to make a crypto payment with Tap

Ready to make your first crypto payment? Let’s get stuck in:

Step 1: Take your Tap card out of your wallet.

Step 2: Swipe or tap at the merchant.

That’s it. Couldn’t be simpler.

Making a crypto payment through the app

If you don’t have a card or are waiting for it to arrive, here is the alternative option:

Step 1: Go to the “Cryptocurrencies” section of the app.

Step 2: Tap on “Send”.

Step 3: Choose “Crypto Withdrawal”.

Step 4: Pick the crypto you’d like to use.

Step 5: Tap the blue + New icon in the upper right corner.

Step 6: Choose “External Beneficiary” and carefully enter the wallet address.

Step 7: To complete the transfer, select the Beneficiary you just added and initiate the transfer.

Most payments are confirmed within minutes, though some networks may take longer during high-traffic periods.

Converting crypto to fiat & using crypto cards

Not every merchant accepts crypto directly, but that doesn't limit your spending power. Tap offers seamless conversion options that bridge the gap between crypto and traditional payments.

Our instant conversion feature lets you convert crypto to fiat currencies within your Tap account. Simply select the amount you want to convert, choose your target currency, and confirm the transaction. The converted funds appear in your fiat balance immediately.

The Tap Card takes this further by allowing you to spend crypto anywhere Mastercard and Visa are accepted. When you make a purchase, the card automatically converts the required amount from your crypto balance to fiat at competitive exchange rates. You can use it for online shopping, in-store purchases, or ATM withdrawals globally. Simply load the money onto your card through the app, and we’ll handle the rest.

Conversion happens in real-time, so you always get current market rates. *For real-time FX rates, click on your profile picture on the homepage and scroll down to “FX Calculator".

Fees, speeds & network choices

Understanding fees helps you make cost-effective payment decisions. There are two types of fees to consider:

Network fees go to blockchain validators who process your transaction. These vary by network and have nothing to do with Tap.

Bitcoin during peak times might cost $10-50, while networks like Polygon often cost under $0.01. Lightning Network Bitcoin payments typically cost less than a penny.

Tap fees are transparent and competitive. We charge a small percentage for conversions and premium features, but basic payments between Tap users are free.

Confirmation times depend on your chosen network:

- Lightning Network: Instant

- Ethereum: 1-5 minutes

- Bitcoin: 10-60 minutes

- Polygon: Under 1 minute

Best practice: For small, everyday purchases, use fast, low-cost networks like Lightning or Polygon. For larger transactions where security is important, Bitcoin's main network offers maximum security despite higher fees.

Security & common pitfalls

Crypto payments are irreversible, making security crucial. Here are the main risks and how to avoid them:

Wrong addresses are the top cause of lost payments. Always double-check recipient addresses and use QR codes when possible. Try to avoid typing wallet addresses manually unless necessary.

Phishing attacks trick users into entering wallet details on fake websites. Always bookmark legitimate sites and verify URLs carefully. Do not follow links from emails or text messages.

Rug pulls and scam projects promise unrealistic returns. Stick to established cryptocurrencies and verified merchants when making payments.

Tap's built-in safeguards include two-factor authentication and automated AML checks that flag suspicious transactions.

Tax & reporting considerations

Here's something many users overlook: spending crypto is a taxable event in most jurisdictions. When you use crypto to buy goods or services, you're technically selling that crypto, which may trigger capital gains tax.

How it works: If you bought Bitcoin at $30,000 and spent it when Bitcoin was $40,000, you owe tax on the $10,000 gain, even though you used it for a purchase rather than selling for cash.

Record-keeping is essential. To stay on the safe side, keep records of your transactions that include purchase dates, sale dates, amounts, and calculated gains or losses.

Regional differences matter:

- United States: IRS treats crypto spending as taxable events with capital gains implications

- European Union: VAT applies to crypto purchases, but capital gains treatment varies by country

- Other regions: Consult local tax advisors as regulations continue evolving

We recommend consulting with a crypto-savvy accountant to ensure you’re on the right side of your local tax obligations.

Why choose Tap to pay with crypto

We've built Tap specifically to solve the pain points of crypto payments. Here's what sets us apart:

Instant settlement means merchants receive payments immediately, not after blockchain confirmations. This solves the biggest barrier to crypto adoption for businesses.

Multi-chain support lets you use Bitcoin, Ethereum, stablecoins, and 60+ other cryptocurrencies through a single platform. No need to manage multiple wallets or apps.

Built-in compliance handles KYC/AML requirements automatically, so you can focus on payments rather than paperwork. We operate within regulatory frameworks.

Global reach without the complexity of international banking. Accept payments from anywhere, settle in your preferred currency, and expand your market instantly.

Ready to start paying with crypto? Download the Tap app and join the future of digital payments.

Need to call someone in the United Kingdom from abroad? You'll need to use the 44 country code to connect successfully. Whether you're reaching friends, family, or business contacts in England, Scotland, Wales, or Northern Ireland, understanding how to properly dial UK numbers is essential for international communication.

What is the 44 country code?

The 44 country code is the international dialling code assigned to the UK by the International Telecommunication Union (ITU). When you're calling from any other country, you must prefix the local UK number with 44 to route your call through the international telephone network.

Here's what you need to know about country code 44:

- Covers the entire UK: England, Scotland, Wales, and Northern Ireland

- Must replace the leading zero: UK numbers start with 0 domestically, but you drop this when using 44

- Works for all UK numbers: landlines, mobiles, and business lines

- Required for international calls: You cannot reach UK numbers from abroad without using 44

The key rule to remember is that when you use country code 44, you must omit the leading '0' that appears in all UK phone numbers when dialled domestically. For example, a London number that appears as 020 7946 0958 within the UK becomes +44 20 7946 0958 when called internationally.

How to call the UK from abroad

The standard format for calling UK numbers internationally follows this pattern:

[International Exit Code] + [44] + [Area Code without 0] + [Local Number]

Your international exit code depends on which country you're calling from:

From the United States or Canada:

- Dial: 011 + 44 + UK number (without the leading 0)

- Example: To call London number 020 7946 0958, dial 011 44 20 7946 0958

From European Union countries:

- Dial: 00 + 44 + UK number (without the leading 0)

- Example: From Germany to the same London number, dial 00 44 20 7946 0958

From India:

- Dial: 00 + 44 + UK number (without the leading 0)

- Example: 00 44 20 7946 0958

From Australia:

- Dial: 0011 + 44 + UK number (without the leading 0)

- Example: 0011 44 20 7946 0958

Hot tip: Most modern smartphones allow you to use the '+' symbol instead of your country's exit code. Simply dial +44 followed by the UK number without the leading zero.

UK area codes you need to know (landlines)

Understanding UK area codes for landline numbers helps you identify which region you're calling and ensures you dial correctly. Here are the major UK area codes you'll encounter:

Remember that these area codes appear after the 44 country code and never include the initial 0 that you see in domestic UK dialling.

Common mistakes when dialling UK numbers

Avoid these frequent mistakes that prevent successful connections to UK numbers:

Including the leading zero: The most common mistake is dialling +44 0 followed by the rest of the number. This creates an invalid number format that won't connect.

Using incorrect exit codes: Each country has its own international exit code. Using 00 when calling from the US (which requires 011) will result in call failure.

Incomplete area codes: Some callers truncate area codes, especially longer ones like Birmingham's 121. Always include the complete area code after 44.

Network restrictions: Your mobile carrier or VoIP service might block international calls by default. Check with your provider if calls aren't connecting despite correct dialling.

Time zone confusion: Calling during UK nighttime hours may result in unanswered calls, even if your dialling format is correct.

How to call UK mobile numbers using 44

UK mobile numbers follow a specific format that's important to understand for international calling. All UK mobile numbers begin with 07 when dialled domestically, which becomes 447 in international format.

UK Mobile Number Structure:

- Domestic format: 07XXX XXXXXX

- International format: +44 7XXX XXXXXX

Examples of calling UK mobile numbers:

- From US: 011 44 7700 900123

- From EU: 00 44 7700 900123

- Using + symbol: +44 7700 900123

When saving UK mobile numbers in your phone's contacts, use the international format (+44 7XXX XXXXXX) so the number works whether you're calling domestically within the UK or internationally from abroad.

Free ways to call the UK

Before paying for expensive international calls, consider these free alternatives:

Voice over Internet Protocol (VoIP) Apps:

- WhatsApp: Free voice and video calls over WiFi or data

- FaceTime: Free for iPhone/iPad/Mac users

- Google Meet: Free video calls with phone dial-in options

- Viber: Free calls between Viber users

When VoIP works best:

- Both parties have stable internet connections

- Calling friends or family who use smartphones

- Non-urgent conversations where call quality fluctuations are acceptable

When traditional calling is better:

- Emergency situations requiring immediate connection

- Business calls where professional quality is essential

- Calling landlines or people without smartphones

- Areas with poor internet connectivity

Emergency numbers and special codes in the UK

Understanding UK number types helps you dial correctly and know what to expect:

Emergency Numbers:

- 999: Primary emergency number (police, fire, ambulance)

- 112: European emergency number (works in UK)

- 101: Non-emergency police contact

When calling emergency numbers from abroad, you still need to use +44, but these calls receive priority routing. However, for true emergencies while visiting the UK, calling locally using 999 or 112 is faster than international routing.

Best time to call the UK from other countries

Timing your calls appropriately ensures better connection rates and recipient availability:

UK Time Zone: Greenwich Mean Time (GMT) in winter, British Summer Time (BST/GMT+1) in summer

Business Hours: Generally 9:00 AM to 5:00 PM, Monday through Friday

Optimal Calling Windows by Region:

From US East Coast:

- UK morning (9 AM-12 PM) = US early morning (4 AM-7 AM)

- UK afternoon (1 PM-5 PM) = US morning (8 AM-12 PM)

From US West Coast:

- UK morning = US very early morning (1 AM-4 AM)

- UK afternoon = US early morning (5 AM-9 AM)

From India:

- UK morning = India afternoon (2:30 PM-5:30 PM)

- UK evening = India late evening (9:30 PM-12:30 AM)

From Australia (Sydney):

- UK morning = Australia evening (8 PM-11 PM)

- UK evening = Australia early morning (2 AM-5 AM)

Lastly

Understanding the 44 country code system ensures your international calls to the UK connect successfully every time. Whether you're calling London business contacts, relatives in Edinburgh, or friends in Cardiff, following these guidelines will help you communicate effectively across international boundaries.

Ever stared at your keyboard, spotted that little € symbol next to the 4, pressed it confidently, and watched a stubborn $ appear instead? You're not alone. This familiar frustration has a simple solution that flows smoother than you'd expect.

How to type the euro symbol (€) on a UK keyboard

The magic combination is Alt Gr + 4. Hold down the Alt Gr key (that's the right-hand Alt key) and tap 4. Like clockwork, your € appears.

Can't find Alt Gr? No worries. Ctrl + Alt + 4 delivers the same result. These shortcuts work regardless of whether the euro symbol actually appears on your 4 key - many UK keyboards show it, but the method works universally.

This common keyboard quirk happens because your system defaults to the dollar sign, but the euro lives just beneath the surface, waiting for the right key combination to unleash its glory.

Euro symbol keyboard shortcuts (Windows & Mac)

Windows Users

- Alt Gr + 4 – The primary method

- Ctrl + Alt + 4 – Alternative when Alt Gr feels awkward

- Alt + 0128 – Number pad method (requires NumLock on)

Mac Users

- Option + 2 – Clean and simple

- Option + Shift + 2 – For US keyboard layouts

- Unicode method: Type 20AC, then press Enter for instant conversion

Each method has its rhythm. Find the one that feels natural for you and let muscle memory take over.

No euro key? Here's what to do

Keyboard layouts dance to different beats. Some show € next to the E key, others place it on 5, and some hide it entirely. Where it sits doesn't matter – the shortcuts still work their magic.

Trust the Alt Gr + 4 combination even when your eyes can't see the symbol. Your keyboard knows where the euro lives.

For keyboards without Alt Gr, the Alt + 0128 using your number pad becomes your reliable backup. Just ensure NumLock glows green before you begin.

Using the Character Map or Word Processor features

Sometimes you need to take the scenic route through your software's built-in tools.

Windows Character Map

Navigate to Start Menu → Character Map. Type "euro" in the search box, select €, and click Insert. It flows directly into your active document.

Microsoft Word & Google Docs

Head to Insert → Symbol (Word) or Insert → Special Characters (Google Docs). The euro symbol sits waiting in the currency section, ready for a simple click.

AutoCorrect Shortcut

Create your own shortcut by setting AutoCorrect to replace "EUR" with "€". Type three letters, watch them transform automatically into the symbol you need.

Typing the euro sign on mobile devices

Mobile keyboards simplify the process beautifully. Switch to your symbols or numbers keyboard, then long-press the $ symbol. A menu of currency options will come up, then select €.

This method works consistently across iOS and Android devices, making currency symbols as accessible as regular letters.

Copy and paste the euro symbol

When shortcuts fail or time runs short, the simplest solution often proves most efficient: € Copy this symbol and paste it wherever needed..

What does the euro symbol (€) mean?

For those looking to learn something new today: the euro symbol is based on the Greek letter epsilon (ε), representing both Europe and economic stability. The two horizontal lines symbolise the currency's strength and unity.

The European Commission selected this design in 1995, choosing a symbol that would flow naturally alongside other currency marks while maintaining its distinctive European identity.

Does the euro sign go before or after the number?

The euro symbol sits before the number with no space between: €10, €250, €1,000.

This placement follows the standard European layout, keeping things clean, easy to read, and making the numbers flow better for readers worldwide.

Money talks, but some currencies whisper so quietly you need a magnifying glass to hear them. In the grand theatre of global finance, not all currencies are created equal, while some strut around like peacocks (looking at you, Kuwaiti Dinar), others shuffle about with the confidence of a wet paper bag.

The Lebanese Pound (LBP) currently holds the unfortunate distinction of being the world's weakest currency in 2025, with an exchange rate so low that one U.S. dollar equals approximately 89,500 Lebanese pounds. To put this in perspective, you'd need a small suitcase to carry the equivalent of $100 in Lebanese pounds, assuming you could find enough physical notes.

Currency weakness isn't just about having a lot of zeros after the decimal point. It reflects a complex web of economic factors, including inflation rates, political stability, monetary policy decisions, and investor confidence. This guide on the world's weakest currencies in 2025, explores the economic stories behind their struggles and what it means for the countries (and the people) who use them.

Top 10 weakest currencies in the world (2025)

Here's the lineup of currencies that make your wallet feel surprisingly heavy when travelling abroad:

Exchange rates are approximate and fluctuate daily. Data compiled from multiple financial sources as of July 2025.

What makes a currency weak?

Before we roll our eyes at long strings of zeros, let’s get clear on what actually drives currency weakness.

Exchange rates show how much of one currency you need to buy another, usually measured against the U.S. dollar. But a low exchange rate isn’t automatically a red flag. Just like shoe sizes, bigger numbers aren’t necessarily worse, they’re just different.

The real reasons a currency weakens?

- Persistent inflation that eats away at value

- Short-term monetary policies that undermine long-term confidence

- Trade imbalances and shrinking foreign reserves

- Political instability that rattles investor trust

When investors lose faith, money moves fast, and exchange rates feel the impact. In short, weak currencies aren’t a punchline, they’re a signal of deeper economic tension.

Country spotlights - case studies behind the weakest currencies

Lebanon | A financial collapse without precedent

Lebanon’s currency crisis is a case study in how not to run an economy. As of mid-2025, the Lebanese pound trades at over 89,500 LBP per USD, making it one of the weakest currencies in the world.

The collapse stemmed from a banking sector that functioned like a state-sponsored Ponzi scheme: banks attracted deposits with sky-high interest rates, only to lend most of those funds to a debt-laden government. When confidence evaporated, the system imploded. Add in the 2019 mass protests and the devastating 2020 Beirut port explosion, and the result was economic freefall.

Today, Lebanese citizens navigate a surreal economy where ATMs limit withdrawals to tiny amounts, and many businesses have shifted to unofficial dollar pricing. A shadow economy thrives alongside the official one, proof that when trust in institutions fails, people find their own workarounds.

Iran | Sanctions, inflation, and isolation

The Iranian rial now trades at over 1,000,000 IRR per USD (yes, that's six zeros). Sanctions have cut Iran off from the global financial system, leaving its oil-rich economy unable to fully monetise its most valuable resource.

It's like owning a garage full of Ferraris with no keys to drive them. In response, Iran has attempted to bypass sanctions with crypto experiments and barter agreements, but none have stabilised the currency.

Inflation routinely exceeds 40%, and as a result Iranians have turned to gold, property, and U.S. dollars to preserve what little value they can. In a country known for its resilience, the rial’s collapse remains a stark reminder of the long-term costs of economic isolation.

Vietnam | Weak by design, not disaster

The Vietnamese dong trades at around 26,000 VND per USD, but that doesn’t signal a crisis, it actually reflects deliberate policy. Vietnam maintains a weaker currency to keep exports competitive, a strategy known as competitive devaluation.

This has helped transform Vietnam into a global manufacturing hub, attracting companies looking to diversify away from China. It's like running a permanent sale on your national output - foreign buyers love the prices, and Vietnamese factories stay busy.

The challenge lies in balance. The government works to avoid the inflation traps that have plagued other countries on this list, proving that not all weak currencies come from failure, some are tools of long-term economic strategy.

Laos | Trapped by debt and dependency

The Laotian kip now trades at around 21,800 LAK per USD, weighed down by inflation above 25% and a debt-to-GDP ratio over 125%. Much of that debt is owed to China, tied to major infrastructure projects that haven’t yet paid off economically.

Laos is a landlocked nation with limited industrial capacity and high import dependence, leaving its currency exposed whenever commodity prices shift. With little monetary wiggle room, the kip’s trajectory reflects deeper economic vulnerabilities.

Sierra Leone | A currency redefined, but still fragile

In 2022, Sierra Leone redenominated its currency, removing three zeros from the leone to simplify transactions. But even the new leone remains weak due to decades of disruption: civil war, the Ebola outbreak, COVID-19, and swings in diamond prices.

This is an economy that's faced shock after shock, and recovery is slow. The mining sector, especially diamonds, still dominates, leaving the leone vulnerable to commodity price drops.

Healthcare challenges and limited infrastructure add even more pressure, reducing productivity and increasing fiscal strain. The leone’s weakness tells the story of a country rebuilding piece by piece, with its currency reflecting both the past and the uphill path ahead.

Why some countries choose to keep their currency weak

Believe it or not, some countries actually prefer their currencies to be weaker - and for good economic reasons. It's counterintuitive, like preferring to drive in the slow lane, but the strategy can be remarkably effective.

Export competitiveness represents the primary motivation. A weaker currency makes domestic products cheaper for foreign buyers, essentially providing a permanent discount. German cars might be excellent, but if Vietnamese motorcycles cost 70% less due to currency differences, guess which ones developing countries will buy?

Countries like China famously maintained an artificially weak currency for decades, helping fuel their manufacturing boom. The strategy worked so well that other countries accused them of "currency manipulation" - the economic equivalent of being too good at a game and getting accused of cheating.

However, this approach carries significant risks. Import costs rise dramatically, making everything from oil to smartphones more expensive for domestic consumers

Long-term currency weakness can also trigger capital flight, where wealthy citisens move their money abroad. When your own citisens don't trust your currency, convincing foreigners becomes considerably more challenging.

Does a weak currency mean a weak economy?

We’ve established that a weak currency doesn't automatically signal economic disaster,sometimes it's just a reflection of different economic structures and historical circumstances.

Indonesia and Vietnam serve as the best examples of countries with numerically weak currencies but relatively strong economies. Both nations have achieved consistent growth, reduced poverty, and built increasingly diversified economies despite their currencies requiring calculators to count properly.

The key lies in purchasing power parity - what matters isn't how many zeros follow your currency symbol, but what those zeros can actually buy. A Vietnamese worker earning 10 million dong monthly isn't necessarily poor if that amount provides a comfortable living standard within the Vietnamese economy.

The real measure of economic health involves factors like employment rates, productivity growth, infrastructure development, and living standards. A country with a weak currency but growing wages, improving infrastructure, and expanding opportunities may be economically healthier than a nation with a strong currency but declining industries and rising unemployment.

What are the consequences of a weak currency?

In essence, a weak currency makes daily life more expensive, with rising prices on imports like food, fuel, and electronics. Added into the mix, Inflation erodes savings, and capital flight accelerates as people move their money into more stable currencies.

Over time, foreign currencies may replace the local one in everyday use, limiting government control. Internationally, weak currencies hurt credit ratings and investor confidence, reinforcing instability.

Final thoughts

Currency weakness is more than just numbers, it’s a signal. We’ve learnt above that it can both expose deep economic flaws or reflect deliberate strategies for growth. Lebanon and Iran highlight how instability and isolation can erode value fast, while Vietnam shows how weakness can fuel exports and development.

These disparities then shape the country’s trade, capital flows, and financial stability worldwide, causing a wider ripple effect. In a global economy, no currency moves alone; each affects the rest. And behind every weak currency are real people navigating inflation, opportunity, or uncertainty.

Currency strength shapes global trade, investment flows, and your real-world spending power. But strength isn’t just about flashy exchange rates. It’s backed by low inflation, investor trust, and governments that don’t spontaneously combust.

In this guide, we break down the top 10 strongest currencies in the world for 2025. You'll learn what drives their dominance, why some currencies outperform others, and what this means for markets, businesses, and travellers alike.

Spoiler: it's not always the ones you expect.

Before we begin: Currency strength is measured by exchange rate value against major currencies like the USD and GBP, combined with factors including economic stability, inflation rates, trade balances, and investor demand.

The strongest currencies typically emerge from countries with sound fiscal policies, political stability, strong export economies, and substantial foreign reserves.

Top 10 strongest currencies in the world (2025 ranking)

The following currencies dominate global markets by exchange rate value against the USD and GBP. These rankings reflect the current market conditions at the time of writing.

1. Kuwaiti Dinar (KWD)

Exchange Rate: 1 KWD = 3.25 USD | 2.44 GBP

The Kuwaiti Dinar isn’t just strong - it’s consistently the world’s strongest. Fueled by vast oil reserves and a government that actually knows how to manage money, Kuwait punches well above its weight. A small population + massive petroleum wealth = eye-watering per capita income, and a currency that commands global respect.

Back in 2007, Kuwait ditched its US dollar peg for a currency basket, a bold move that gave it more control and resilience. Add in one of the largest sovereign wealth funds on the planet and a no-nonsense approach to spending oil money, and you’ve got a textbook case in currency strength.

2. Bahraini Dinar (BHD)

Exchange Rate: 1 BHD = 2.65 USD | 2.05 GBP

The Bahraini Dinar may not get the headlines, but it holds its ground thanks to a rock-solid USD peg and a thriving financial sector. As a gateway to the Gulf, Bahrain has built a reputation as a banking and investment hub, with the regulatory chops to back it up.

While oil still plays a role, the kingdom’s smart pivot into finance, tourism, and services has given the BHD more than one leg to stand on. Add close ties to Saudi Arabia and deep integration with the wider Gulf economy, and you've got a currency that’s quietly powerful and built to last.

3. Omani Rial (OMR)

Exchange Rate: 1 OMR = 2.60 USD | 1.92 GBP

Oman’s currency doesn’t just ride the oil wave - it’s powered by long-term vision. While crude still plays a role, the Omani Rial stands tall thanks to the country’s steady shift toward tourism, logistics, and manufacturing, all part of its ambitious Vision 2040 roadmap.

In a region known for volatility, Oman sets itself apart with political stability, disciplined fiscal policy, and a refreshingly balanced economic game plan. The result? A currency that’s not just strong, but built on more than just barrels.

4. Jordanian Dinar (JOD)

Exchange Rate: 1 JOD = ~1.41 USD | 1.08 GBP

Jordan doesn’t have oil fields or massive exports, but it does have one of the most stable currencies in the region. Pegged to the USD since 1995, the Jordanian Dinar has held firm through geopolitical shocks and economic headwinds.

What’s the secret? A central bank that plays it straight, a government that manages its books carefully, and a commitment to stability - even while supporting large refugee populations and navigating limited natural resources. In short: smart policy over raw power.

5. British Pound Sterling (GBP)

Exchange Rate: 1 GBP = 1.35 USD

As the world’s oldest currency still in circulation, the British Pound carries serious legacy power, but it’s more than just tradition. Backed by the UK’s diversified economy and London’s role as a global finance heavyweight, the pound remains one of the most widely held reserve currencies on the planet.

Let’s call a spade a spade. While Brexit brought its fair share of turbulence, the fundamentals haven’t changed: a strong legal system, deep capital markets, and world-class financial infrastructure keep the GBP firmly in the heavyweight league.

6. Cayman Islands Dollar (KYD)

Exchange Rate: 1 KYD = ~1.20 USD | 0.89 GBP

With more registered companies than people, the Cayman Islands punch way above their weight in global finance. The KYD benefits from this offshore powerhouse status, where financial services and tourism drive steady demand.

Pegged to the US dollar, the currency stays stable, while the islands’ investor-friendly regulations and tax perks keep international capital flowing. It’s a niche economy, but a well-oiled one, and the KYD reflects that strength.

7. Gibraltar Pound (GIP)

Exchange Rate: 1 GIP = 1 GBP (perfect parity)

The Gibraltar Pound holds a 1:1 peg with the British Pound, giving it the full weight of UK monetary policy with a distinctly local twist. It’s a territorial currency that does more than just mirror the GBP; it powers a compact but strategic economy.

Perched at the gateway to the Mediterranean, Gibraltar leverages its prime location and tight financial regulation to attract investment and business. The result? A stable, trusted currency backed by both geography and governance.

8. Swiss Franc (CHF)

Exchange Rate: 1 CHF = ~1.10 USD | 0.88 GBP

Listen, the Swiss Franc doesn’t just symbolise stability - it sets the standard. Backed by political neutrality, low inflation, and one of the world’s most trusted banking systems, the CHF is where capital goes when things get shaky.

The Swiss National Bank’s conservative approach and Switzerland’s strict fiscal discipline make the Franc a magnet for investors seeking security. In times of global turbulence, the CHF doesn’t flinch, it holds.

9. Euro (EUR)

Exchange Rate: 1 EUR = ~1.05 USD | 0.84 GBP

The Euro ties together 20 EU countries under one economic flag, creating a currency backed by a collective economy even bigger than the U.S. Despite political bumps and economic contrasts across member states, the EUR holds its ground as the world’s second-most traded currency.

What keeps it strong? The European Central Bank’s monetary oversight, the eurozone’s combined economic weight, and the Euro’s deep role in global trade and reserves. It’s not just shared money, it’s shared strength.

10. United States Dollar (USD)

The global standard

The USD may not top the exchange rate charts, but some might argue that it owns the global stage. Involved in nearly 88% of all forex trades and held as the primary reserve currency by central banks worldwide, the dollar is the backbone of international finance.

Its strength isn’t necessarily about value per unit, it’s about reach. From oil pricing to cross-border deals, the USD is the language of global trade, powered by the world’s largest economy and the deepest capital markets on earth.

What makes a currency strong?

Strong currencies aren’t just about optics: they’re built on trust, economic fundamentals, and global demand. The world’s top performers all share a few key traits that keep investors confident and capital flowing.

So, what drives currency strength?

At the core, it’s about stability and credibility. Countries with steady politics, transparent institutions, and clear economic policies tend to attract global investment. High interest rates - when balanced with low inflation - pull in foreign capital, while low inflation protects the currency’s real-world value.

Trade matters too. When a country exports more than it imports, global buyers need the local currency, driving demand and pushing up value. Large foreign exchange reserves also give central banks firepower to defend their currency when markets wobble.

Debt is another big one. Lower debt-to-GDP ratios signal fiscal discipline and room to manoeuvre during economic shocks, key ingredients for long-term currency trust.

Pegged vs floating exchange rates

Currencies typically fall into two camps: pegged or floating.

- Pegged currencies (like the Bahraini Dinar or Jordanian Dinar) lock their value to another, usually the US dollar - yes, just like stablecoins. This provides predictability for trade and investment, but demands strict monetary control and healthy reserves to keep the peg in place.

- Floating currencies (like the Swiss Franc or British Pound) let market forces do the work. That means more volatility, but also more flexibility when shocks hit, if central banks know what they’re doing.

Both systems have their strengths. The key is whether the country can maintain trust through smart policy, solid reserves, and consistent economic performance.

Honourable mentions

While these currencies didn’t make the top 10, they still offer stability, liquidity and are backed by solid economic fundamentals.

These currencies benefit from resource wealth, strong institutions, or strategic economic positions that support their value in global markets.

How is currency value measured?

Currency strength isn’t measured in a vacuum, it’s always relative. Exchange rates compare one currency against another (like USD/EUR), and those prices shift constantly based on supply, demand, and investor sentiment.

In deep, liquid markets, these rates reflect what the world thinks about a country’s economy, stability, and future outlook. Big trades happen fast and without much friction because major currencies have enough volume to absorb them.

Central banks keep a close eye on all this. In floating systems, they rarely intervene unless things get choppy. But day to day, it’s market forces that drive currency values, shaped by fundamentals and the collective mood of global finance.

What is the most stable currency in the world?

No drama, no surprises: the Swiss Franc is the gold standard for currency stability. Backed by political neutrality, low inflation, and ultra-consistent monetary policy, the CHF has earned its reputation as a safe-haven asset.

The Swiss National Bank doesn’t chase headlines. Instead, it focuses on one thing: price stability. And it’s done that with surgical precision for decades. Add in a political system designed for consensus and slow, steady change, and you get a currency that markets trust, especially when things get rough.

In times of crisis, global capital flows to the Franc. That trust? It reinforces the CHF’s strength, year after year.

What is the most traded currency in the world?

Likely no surprises here either: The dollar is (currently) the backbone of the world’s financial system. Accounting for nearly 90% of all forex trading, it’s the go-to for everything from central bank reserves to international commodity pricing.

Around 60% of global foreign exchange reserves are held in USD, and even countries with no direct US ties use the dollar to price and settle trades. This widespread use creates powerful network effects - the more the dollar flows, the more stable and liquid it becomes, drawing in even more users.

It’s a self-reinforcing cycle, fueled by the sheer size and strength of the US economy.

Conclusion

Currency strength goes beyond daily exchange rates. It’s a reflection of a nation’s economic health, fiscal discipline, and political stability. While rates bounce around day-to-day, the core drivers of strength are built to last.

Knowing what fuels currency power isn’t just academic, it’s critical for smart investing, international business, and even planning your next trip. The strongest currencies aren’t just the ones with high numbers, they’re the ones backed by solid economics and trusted institutions that keep value steady over time.