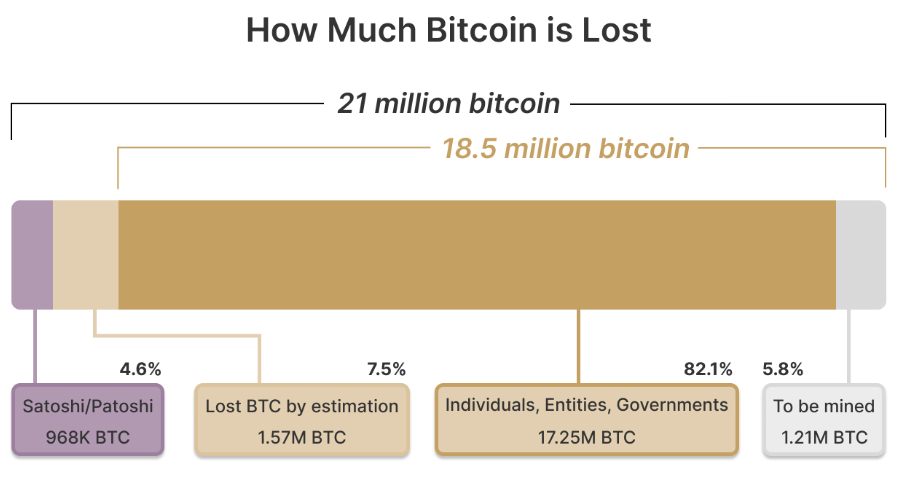

More than a million Bitcoin have vanished because owners didn’t plan ahead. Without a crypto inheritance plan, your family could lose access to your assets forever. Here’s how to safeguard them.

Keep reading

As digital assets become a core part of personal wealth, one uncomfortable question lingers: what will happen to your crypto when you’re gone? Unlike traditional assets that can be managed through banks or brokers, cryptocurrencies are bound entirely to whoever holds their private keys. Lose the keys, and the funds are gone. Permanently.

Each year, millions of dollars in Bitcoin, Ether, and other tokens vanish into the digital void when holders pass away without sharing access. It is estimated that around 1.5 million BTC (roughly 7.5% of total supply) may already be lost forever. With digital wealth now part of countless estates, preparing for the inevitable is no longer optional; it’s the responsible thing to do.

Why Planning for Crypto Inheritance Matters

In traditional finance, wealth transfer is handled through wills, trusts, and custodians. But crypto flips that model: you are the bank. Your heirs can’t simply request a password reset or call customer service. Without private keys, wallets, or access instructions, those assets are unrecoverable for all effects and purposes.

A crypto inheritance plan ensures that your digital assets, from Bitcoin and altcoins to NFTs and DeFi holdings, remain both secure and accessible to the people you choose. It bridges two crucial needs: protecting your funds today and ensuring your legacy tomorrow.

Beyond personal security, inheritance planning also reduces emotional and financial stress for your loved ones. By documenting how and where assets can be accessed, you prevent confusion and potential legal disputes.

Building the Foundation of a Crypto Inheritance Plan

Start with Legal Clarity

Consult an attorney familiar with digital assets. A properly structured will or trust should identify your crypto holdings, list beneficiaries, and outline how they can access those funds. Many jurisdictions still lack explicit laws for digital assets, so expert guidance helps ensure compliance and enforceability.

Secure Your Keys… But Don’t Overshare

The biggest challenge in crypto inheritance is private key management. If you die with your keys, your crypto dies with you. However, leaving keys in plain text within a will or document is just as risky. Instead, consider approaches like:

- Multisignature wallets, which require multiple approvals to move funds.

- Shamir’s Secret Sharing, which means splitting your seed phrase into parts distributed among trusted people.

- Encrypted backups or sealed letters stored in secure, offline locations.

Document recovery procedures in plain language so your heirs can follow them even without technical knowledge.

Choose the Right Executor

A traditional executor may not understand how to navigate crypto. You can appoint a tech-literate executor or designate a digital asset custodian to handle that portion of your estate. This ensures smooth execution and reduces the risk of errors or loss.

In a market driven by innovation and constant change, a well-structured inheritance plan offers something rare in crypto, certainty.

New Tools for a Digital Age

The rise of blockchain-based “death protocols” and smart contract automation adds a new layer of possibilities. Some platforms allow transfers to trigger automatically after certain conditions are met (for example, a verifiable death certificate or extended inactivity).

Ethereum and similar chains already support programmable inheritance systems, but these should complement, not replace, legal documents. Technology can help enforce your intentions, but law remains the foundation of inheritance.

Some investors even use “dead man’s switches”, automated systems that transfer funds if the owner doesn’t log in for a set period. While clever, it might be best to pair them with legal documents to prevent accidental activations.

Protecting Privacy While Planning Ahead

While planning for the future, it’s crucial to maintain security in the present. Avoid including wallet addresses, private keys, or passwords in public wills, which become part of the legal record. Instead, store such details in encrypted files or sealed envelopes accessible only to specific individuals.

Tools like decentralized identifiers (DIDs) and verifiable credentials can also help manage long-term identity and access rights. These systems allow you to define who can access what, and when, without intermediaries.

Custodial vs. Non-Custodial: Finding the Balance

When structuring inheritance, knowing whether your assets are held in custodial or non-custodial wallets makes all the difference.

Custodial services (like major exchanges) manage private keys on your behalf, which simplifies recovery if your heirs can provide proper documentation. However, it introduces third-party risk. Accounts can be frozen, hacked, or shut down.

Non-custodial wallets, on the other hand, offer maximum control and privacy but demand greater responsibility. If your heirs lose the seed phrase, there’s no backup plan. There’s also the possibility of taking a hybrid approach: keeping long-term holdings in non-custodial storage for security, while using reputable custodians for smaller, more accessible amounts.

Keep It Up to Date

A crypto inheritance plan is not a “set it and forget it” document. Prices change, portfolios evolve, and wallet technologies become obsolete very often. It may be wise to revisit your plan regularly, especially after major life events such as marriage, divorce, or the birth of a child.

It’s also worth keeping track of regulatory updates in your jurisdiction. Laws surrounding digital assets and inheritance are rapidly evolving, and what’s compliant today may not be tomorrow.

Common Inheritance Pitfalls

Even the best intentions can go wrong. Here are the most frequent mistakes to avoid:

- Including seed phrases directly in your will. As we mentioned before, this makes them public and vulnerable.

- Neglecting to educate heirs. Without guidance, even secure plans can fail.

- Relying solely on exchanges. Centralized platforms can fail or freeze funds.

Planning isn’t just about distributing wealth; it’s about ensuring continuity. A clear inheritance strategy preserves your crypto’s value and prevents it from becoming part of the estimated $100 billion in lost digital assets worldwide.

Protecting More Than Just Coins

Preparing a crypto inheritance plan isn’t merely about money; it’s about legacy. For all the talk about decentralization and autonomy, responsibility and forward-thinking remain at the heart of crypto ownership. By taking the time to plan ahead, you safeguard not only your wealth but also your family’s peace of mind.

NEWS AND UPDATES

LATEST ARTICLE

Why can't a fully compliant, regulated crypto business secure a bank account in 2025?

If you're operating in this space, you already know the answer. You've lived through it. You've submitted the documentation, walked through your AML procedures, and demonstrated your regulatory compliance… only to be rejected. Or worse still, waking up to find your existing account frozen, with no real explanation and no path forward.

This isn't about isolated cases or bad actors being weeded out. It's a pattern of systematic risk aversion that's creating real barriers to growth across the entire sector, and it's throttling one of the most significant financial innovations of our generation.

We're Tap, and we're building the infrastructure that traditional banks refuse to provide.

The Economics Behind the Blockade

Let's examine what's actually driving this exclusion, because it's rarely about the reasons banks cite publicly.

The European Banking Authority has explicitly warned against unwarranted de-risking, noting it causes "severe consequences" and financial exclusion of legitimate customers. Yet the practice continues, driven by two fundamental economic pressures that have nothing to do with your business's actual risk profile.

The compliance cost calculation

Financial crime compliance across EMEA costs organizations approximately $85 billion annually. For traditional banks, the math is simple: serving crypto businesses requires specialized expertise, enhanced monitoring, and ongoing due diligence. As a result, it's cheaper to reject the entire sector than to build the infrastructure needed to serve it properly.

The regulatory capital burden

New EU regulations impose a 1,250% risk weight on unbacked crypto assets such as Bitcoin and Ethereum. This isn't a compliance requirement; it's a capital penalty that makes crypto exposure commercially unviable for traditional institutions, regardless of the actual risk individual clients present.

In the UK, approximately 90% of crypto firm registration applications have been rejected or withdrawn, often citing inadequate AML controls. Whether those assessments are accurate or not, they've created the perfect justification for blanket rejection policies.

The result? Compliant businesses are being treated the same as bad actors; not because of what they've done, but because of the sector they're in.

The Real Cost of Financial Exclusion

Financial exclusion isn’t just an hiccup; it creates tangible operational barriers that ripple through every part of running a crypto business.

Firms that have secured MiCA authorization, built robust compliance programs, and met regulatory requirements can find themselves locked out of basic banking services. Essential fiat on-ramps and off-ramps remain inaccessible, slowing payments, limiting growth, and complicating cash flow management.

Individual cases illustrate the problem vividly as well. Accounts are closed because a business receives a payment from a regulated exchange. Others are dropped with vague references to “commercial decisions,” offering no substantive justification. Founders frequently struggle to separate personal and business finances, as both are considered too risky to serve.

The irony is striking. By refusing service to compliant businesses, traditional banks aren’t mitigating risk; they’re amplifying it. Forced to operate through less regulated channels, these legitimate firms face higher operational and compliance risks, slower transactions, and reduced investor confidence. Over time, this slows innovation, and raises the cost of doing business for firms that are legally and technically sound.

Debanking Beyond Europe: U.S. Crypto Firms Face Their Own Challenges

Limited access to banking services isn’t exclusive to Europe. Leading firms in the U.S. crypto industry have faced numerous challenges regarding the banking blockade. Alex Konanykhin, CEO of Unicoin, described repeated account closures by major banks such as Citi, JPMorgan, and Wells Fargo, noting that access was cut off without explanation. Unicoin’s experience echoes a broader sentiment among crypto executives who argue that traditional financial institutions remain wary of digital asset businesses despite recent policy shifts toward a more pro-innovation stance.

Jesse Powell, co-founder of Kraken, has also spoken out about being dropped by long-time banking partners, calling the practice “financial censorship in disguise.” Caitlin Long, founder of Custodia Bank, recounted how her institution was repeatedly denied services. Gemini founders Tyler Winklevoss and Cameron Winklevoss shared similar frustrations.

These experiences reveal a pattern many in the industry interpret as systemic risk aversion. Even in a market as large and mature as the United States, crypto-focused businesses continue to encounter obstacles in maintaining basic financial infrastructure. The issue became especially acute after the collapse of crypto-friendly banks such as Silvergate, Signature, and Moonstone; institutions that once served as key bridges between fiat and digital assets. Their exit left a gap few traditional players have been willing to fill.

Why Tap Exists

The crypto industry has reached an inflection point. Regulatory frameworks like MiCA are providing clarity. Institutional adoption is accelerating. The technology is proven and tested. But the fundamental infrastructure gap remains: access to business banking that actually works for digital asset businesses.

This is precisely why we built Tap for Business.

We provide business accounts with dedicated EUR and GBP IBANs specifically designed for crypto companies and businesses that interact with digital assets. This isn't a side offering or an experiment, it's our core focus.

Our approach is straightforward

We built our infrastructure for this sector

Rather than retrofitting traditional banking systems to reluctantly accommodate crypto businesses, we designed our compliance, monitoring, and operational frameworks specifically for digital asset flows. This means we can properly assess and serve businesses that others automatically reject.

We price in the actual risk, not the sector

Blanket rejection policies exist because they're cheap and simple. We take a different approach: evaluating each business based on their actual controls, compliance posture, and operational reality. It costs more, but it's the only way to serve this market properly.

We're committed to sector normalization

Every time a legitimate crypto business is forced to operate without proper banking infrastructure, it reinforces outdated stigmas. By providing professional financial services to compliant businesses, we're helping demonstrate what should be obvious: crypto companies can and should be served by the financial system.

It isn't about taking on risks that others won't. It's about properly evaluating risks that others refuse to understand.

Moving Forward

The industry is maturing. Regulatory clarity is emerging. Institutional adoption is accelerating. But you can't put your business on hold while traditional banks slowly catch up to reality.

That's not sustainable in the long run.

As a firm, you shouldn't have to beg for a bank account. You shouldn't have to downplay your crypto operations just to access basic financial services. And you certainly shouldn't have to accept that systematic exclusion with little to no explanation other than “It’s just how things are."

The crypto sector is building the future of finance. Your banking partner should believe in that future too. If you're ready to work with financial infrastructure built for your business, not in spite of it, here we are.

Talk today with one of our experts to understand how we can help your business access the banking infrastructure you need.

The crypto market just pulled off one of its boldest recoveries in recent memory. What began as a violent sell-off on October 10 has given way to a surprisingly strong rebound. In this piece, we’ll dig into “The Great Recovery” of the crypto market, how Bitcoin’s resilience particularly stands out in this comeback, and what to expect next…

The Crash That Shook It All

On October 10, markets were rattled across the board. Bitcoin fell from around $122,000 down to near $109,000 in a matter of hours. Ethereum dropped into the $3,600 to $3,700 range. The sudden collapse triggered massive liquidations, nearly $19 billion across assets, with $16.7B in long positions wiped out.

That kind of forced selling, often magnified by leverage and thin liquidity, created a sharp vacuum. Some call it a “flash crash”; an overreaction to geopolitical news, margin stress, and cascading liquidations.

What’s remarkable, however, is how quickly the market recovered.

The Great Recovery: Scope and Speed

Within days, many major cryptocurrencies recouped large parts of their losses. Bitcoin climbed back above $115,000, and Ethereum surged more than 8%, reclaiming the $4,100 level and beyond. Altcoins like Cardano and Dogecoin led some of the strongest rebounds.

One narrative gaining traction is that this crash was not a structural breakdown but a “relief rally”, a market reset after overleveraged participants were squeezed out of positions. Analysts highlight that sell pressure has eased, sentiment is stabilizing, and capital is re-entering the market, all signs that the broader uptrend may still be intact.

“What we just saw was a massive emotional reset,” Head of Partnerships at Arctic Digital Justin d’Anethan said.

“I would have another, more positive take: seeing 10B worth of liquidation happen in a flash and pushing BTC prices down 15%+ in less than 24hrs to then see BTC recoup 10% to 110K is a testament to how far we've come and how massive and important BTC has become,” he posted on 𝕏.

Moreover, an important datapoint stands out. Exchange inflows to BTC have shrunk, signaling that fewer holders are moving coins to exchanges for sale. This signals that fewer investors are transferring their Bitcoin from personal wallets to exchanges, which is a common precursor to selling. In layman terms, coins are being held rather than prepared for trade.

Bitcoin’s Backbone: Resilience Under Pressure

Bitcoin’s ability to rebound after extreme volatility has long been one of its defining traits. Friday’s drop admittedly sent shockwaves through the market, triggering billions in liquidations and exposing the fragility of leveraged trading.

Yet, as history has shown, such sharp pullbacks are far from new for the world’s largest cryptocurrency. In its short history, Bitcoin has endured dozens of drawdowns exceeding 10% in a single day (from the infamous “COVID crash” of 2020 to the FTX collapse in 2022) only to recover and set new highs months later.

This latest event, while painful, highlights a maturing market structure. Since the approval of spot Bitcoin ETFs in early 2024, institutional involvement has deepened, creating greater liquidity buffers and stronger institutional confidence. Even as billions in leveraged positions were wiped out, Bitcoin has held firm around the $110,000 zone, a level that has since acted as psychological support.

What to Watch Next

The key question now is whether this rebound marks a short-term relief rally or the start of a renewed uptrend. Analysts are closely watching derivatives funding rates, on-chain flows, and ETF inflows for clues. A sustained increase in ETF demand could provide a steady bid under the market, offsetting the effects of future liquidation cascades. Meanwhile, Bitcoin’s ability to hold above $110,000 (an area of heavy trading volume) may serve as confirmation that investor confidence remains intact.

As the market digests the events of October 10, one lesson stands out. Bitcoin’s recovery isn’t just a matter of luck, it’s a reflection of underlying market structure that can absorb shocks. It is built on a growing base of long-term holders, institutional adoption, and a financial system increasingly intertwined with digital assets. Corrections, however dramatic, are not signs of weakness; they are reminders of a maturing market that is striding towards equilibrium.

Bottom Line

The crash on October 10 was brutal, there’s no denying that. It was one of the deepest and fastest in recent memory. But the recovery has been equally sharp. Rather than exposing faults, the rebound has underscored the market’s adaptability and Bitcoin’s central role.

The market consensus is seemingly leaning towards a reset; not a reversal. The shakeout purged excess leverage, and the comeback underlined demand. If Bitcoin can maintain that strength, and the broader market keeps its footing in the coming days, this could mark a turning point rather than a cave-in.

Let's Talk About Getting Your Crypto to Work While You Sleep

Remember when your grandparents bragged about their 2% savings account? Those days feel like ancient history now that crypto APY percentages are floating around that would make a traditional banker faint. But hold up, before you start dreaming about retiring next month on those sweet, sweet yields, let's dive into what APY actually means and why some of these numbers look like lottery tickets.

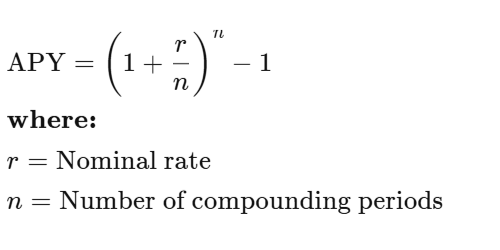

What the Is APY, Anyway?

Think of APY as compound interest on steroids. While your bank's savings account sits there earning dust, APY measures how much your money can actually grow in a year when interest keeps building on top of interest. The faucet of passive income is now open.

Here's a reality check: Park $1,000 in your bank at 5% simple interest, and you'll have a whopping $1,050 after a year. Yawn, boring… But that same money with 5% APY compounded monthly? You're looking at $1,051.16.

"Big deal, that's only a dollar!" you might say. But here's where it gets interesting. Over time, that compounding effect turns into a money snowball rolling down a mountain. The difference between simple interest and compound interest isn't just pennies; it's the difference between walking and taking a rocket ship.

APY vs. APR: The Sibling Rivalry You Need to Understand

Okay, confession time…even seasoned crypto folks mix these up. Here's your cheat sheet:

APY (Annual Percentage Yield): What you earn when you lend out your crypto. The higher, the better for your wallet.

APR (Annual Percentage Rate): What you pay when you borrow crypto. Lower is your friend here.

Think of it this way: APY is the cool cousin who brings you money, while APR is the one who always asks to borrow twenty bucks.

For a more detailed comparison, click here.

Where Does APY Show Up in Crypto?

- Crypto "Savings Accounts"

Some platforms let you deposit your tokens and watch them multiply. It's like putting your crypto to work at a job that actually pays decent wages. Your coins get lent out to traders who need them, and you get a cut of the action.

- Staking: Become a Network Validator

With Proof-of-Stake blockchains like Ethereum or Cardano, you can "stake" your tokens to help secure the network. Think of it as being a digital security guard who gets paid in crypto. The network stays safe, and you earn rewards. Win-win.

- Yield Farming: The Wild West of DeFi

This is where things get interesting, and a bit crazy. You provide liquidity to decentralized exchanges, and in return, you earn trading fees plus shiny new governance tokens. Early yield farmers sometimes see APYs that look like phone numbers, but don't get too excited; those rates have a habit of crashing back to earth.

- Lending Protocols: Become the Bank

Platforms like Aave and Compound let you play banker. You lend your tokens, borrowers pay interest, and you collect the proceeds. APY goes up when everyone wants to borrow your particular flavor of crypto, and down when the demand cools off.

Why Are Crypto APYs So High?

While your bank offers you a measly 0.5%, crypto platforms are throwing around eye-watering numbers like 10%, 50%, or even 1,000%+. Here's why:

Crypto traders will pay premium rates to short a token or execute complex arbitrage strategies. Supply and demand at its finest.

Hype for new projects also plays a role. Fresh projects often throw ridiculous APYs at users to attract liquidity. It's like a grand opening sale, but with more zeros.

Risk gets factored in. Let's be real, crypto can get risky at times. Higher returns compensate for the white-knuckle ride.

Finally, token Incentives can play a role too. Many of those eye-popping APYs come partially from project tokens that could moon... or crater. It's the crypto Russian roulette.

The Math Behind the Magic

Don't worry, we're not about to turn this into a calculus nightmare. The APY formula is actually pretty straightforward:

Example: 10% interest compounded monthly gives you about 10.47% APY. Compound it daily? You're looking at 10.52%. In crypto, some protocols compound every block, which is like compounding every few seconds. Your calculator might start smoking.

The Fine Print

Before you quit your day job and become a full-time yield farmer, let's talk about the risks that nobody likes to mention at crypto parties. First up is volatility. Sure, your APY might be 20%, but if your token's price drops 50%, you're still in the red. Math is cruel like that. Then there's impermanent loss, which sounds harmless but can eat into your gains faster than you can say "automated market maker" when you're providing liquidity and token prices start dancing around.

Don't forget about smart contract risk, either. DeFi protocols are basically computer programs holding billions of dollars, and if they break, funds can disappear into the digital ether without so much as a goodbye note. Platform risk is equally sobering. Remember Celsius? FTX? Sometimes the platforms themselves go belly-up, taking user funds with them like the Titanic.

Last but not least, there’s APY whiplash. That jaw-dropping 100% APY you bookmarked yesterday? It might be 15% today because crypto moves fast. Rates fluctuate based on demand, new competition, token economics, and sometimes just because the crypto gods felt like shaking things up.

What's a "Good" APY?

- Conservative. Sticking to blue-chip assets and reputable platforms for 3-8% APY. For the faint of heart.

- Moderate. Staking some altcoins or providing liquidity for 10-20% APY. There’s some excitement, but not heart-attack levels.

- High (YOLO). Chasing new DeFi projects for 50-100%+ APY. It’s worth keeping in mind there’s a non-zero chance your tokens might become expensive digital art.

Remember, if an APY looks too good to be true, it's probably attached to risks that would make a hedge fund manager nervous.

Crystal Ball Time: The Future of APY in Crypto

Here's where things get interesting. As crypto grows up, APYs are starting to act less like lottery tickets and more like actual financial products. Big institutions are getting into staking, regulators are paying attention, and the wild west is slowly becoming a proper town with actual roads.

It’s likely crypto will keep offering better yields than traditional finance. It's just that the 10,000% APY days are likely becoming a fond memory.

The Bottom Line

APY in crypto is the same mathematical concept your finance professor taught you, just dressed up in digital clothing and offering significantly better rates. Whether you're staking, lending, or yield farming, understanding APY helps you separate the wheat from the chaff and the legitimate opportunities from dubious schemes.

APY isn't a cheat code to infinite money. It's a tool that, when used wisely, can help your crypto actually work for you instead of just sitting in your wallet looking pretty. But like everything in crypto, it comes with risks that deserve respect and careful consideration.

It’s worth remembering the best APY in the world is worthless if the underlying project disappears into the digital sunset. Choose wisely, diversify smartly, and may your compounds be ever in your favor.

Picture this: You're scrolling through DeFi platforms, and suddenly you see two different projects. One screams "12% APR!" while another boasts "12% APY!" Your brain probably thinks, "Same, right?"

Wrong. Very wrong.

When it comes to comparing interest rates, APR and APY might look like twins… but they’re not. Far from it. The difference between them can determine whether you grow your savings or overpay on a loan. In this guide, we’ll break down what APR and APY really mean, how they work in banking, lending, and crypto, and how understanding them can help you make smarter financial decisions.

Key Takeaways

- APR (Annual Percentage Rate) shows the yearly cost of borrowing, including interest and certain fees.

- APY (Annual Percentage Yield) reflects your total yearly return, factoring in compounding.

- For borrowers, lower APR = lower total cost. For savers, higher APY = higher returns.

- In crypto and DeFi, compounding frequency can turn modest APRs into much higher APYs.

APY vs APR: The Essential Difference

At a glance, APR tells you how much interest you’ll pay (or earn) over a year, without compounding. APY, on the other hand, includes compounding, the process where interest earns more interest over time.

When comparing financial products, whether a credit card, savings account, or staking pool, this distinction matters. For borrowers, APR reveals the true cost of debt, while for investors, APY highlights the power of compound growth.

TL;DR. APR is about cost, APY is about growth. Knowing which one applies helps you choose between competing offers with confidence.

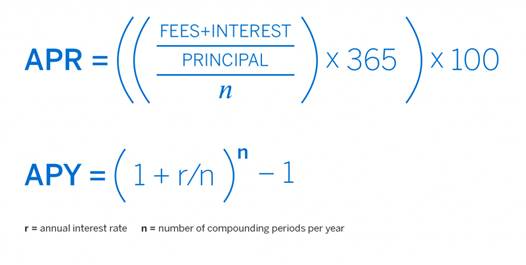

What Is APR (Annual Percentage Rate)?

APR represents the yearly interest rate charged to borrow money, or the rate you earn before compounding if you lend it. It includes interest and certain fees, helping you understand the total cost of credit.

APR is widely used in credit cards, personal loans, mortgages, and auto financing. For example, if your credit card has an 18% APR, you’ll pay 18% interest on any carried balance. Fixed-rate loans maintain the same APR, while variable-rate loans fluctuate with market conditions and Federal Reserve changes.

Example: Borrow $10,000 at 10% APR for one year. You’ll owe $1,000 in interest. Simple and transparent, without compounding surprises.

What Is APY (Annual Percentage Yield)?

APY measures how much your money grows over a year, including compounding. It reflects how often your interest is added to your balance (daily, monthly, or annually) which then generates more interest.

This is the standard metric for savings accounts, money market accounts, and certificates of deposit (CDs). Banks and digital financial platforms often advertise APY because it paints a more complete picture of earning potential.

Example: Deposit $10,000 in an account with a 5% APY, compounded monthly. After one year, your balance grows to $10,511, slightly higher than a flat 5% APR return.

The more frequent the compounding, the greater the growth, especially important in DeFi protocols that compound every few minutes.

APR vs APY in Different Financial Products

Credit Cards and Loans (APR)

When borrowing, APR helps you understand the true borrowing cost. For instance, if a mortgage advertises a 6.5% APR, that includes both the interest and certain closing costs.

Car loans, student loans, and credit cards use APR to keep comparisons straightforward across lenders. The key? Lower APR = less expensive borrowing.

Savings and Investment Accounts (APY Focus)

If your goal is wealth building, APY is your guide. A high-yield savings account with 4.5% APY grows faster than one with 4% because compounding quietly amplifies returns.

For certificates of deposit (CDs) or fixed deposits, APY helps you compare the real impact of compounding frequency.

Cryptocurrency and DeFi (Both APR and APY)

In crypto lending, staking, or yield farming, both metrics appear and can be easily confused.

- APR shows base rewards (without compounding).

- APY assumes you’re constantly reinvesting.

Example: A DeFi pool may show 100% APR, but with daily compounding, it becomes 171% APY. The key is understanding how often you can claim rewards and whether gas fees make compounding worthwhile.

How to Calculate APR vs APY

To compare offers correctly, you can calculate one from the other:

Example: 12% APR compounded monthly

APY = (1 + 0.12/12)^12 - 1 = 12.68%

Compounding more frequently increases APY slightly each time.

Which Should You Focus On?

- If you’re borrowing, prioritize APR. It reflects the total cost of debt.

- If you’re saving or investing, look at APY. It shows how compounding boosts earnings.

- In crypto, check both. APR tells you the base reward, APY reveals potential if you reinvest.

When comparing offers, always read the fine print; frequency, fees, and conditions can shift the real value dramatically.

Common Misconceptions and Pro Tips

Myth: “APY is always better.”

Reality: Only if compounding happens, or if you reinvest earnings.

Myth: “APR ignores compounding, so it’s useless.”

Reality: APR helps borrowers compare costs clearly.

Pro Tip: Use online APR-to-APY calculators for quick comparisons. They’re free and eliminate guesswork.

The Bottom Line

APR and APY aren't just different ways of saying the same thing, they represent two different approaches to measuring returns.

When you see APR, you're looking at simple interest calculated over a year. When you see APY, you're seeing what happens when earnings get reinvested and compound over time. Both are valid measurements, just showing different scenarios.

This distinction becomes more noticeable with higher interest rates. A 50% APR becomes closer to 65% when compounded daily. The higher the base rate, the bigger the difference between these two numbers becomes.

Understanding which one you're looking at helps you compare options accurately. APR gives you the base rate, while APY shows the potential with compounding factored in.

Once you get the hang of spotting the difference, those financial offers suddenly make a lot more sense. No more squinting at numbers wondering why similar-sounding deals seem to work out so differently. It's like finally understanding why some recipe measurements are in cups and others in ounces - same concept, different scales, and knowing which is which makes all the difference.

From Comedy Gold to Digital Ghost Town

Memecoins were once the beating heart of retail-driven speculation in cryptocurrency markets. From Dogecoin's Elon Musk-fueled rallies to the lightning-fast ascent of tokens like Shiba Inu and Pepe, these internet-born digital assets transformed online jokes into substantial market capitalizations, at least for those who managed to time the hype cycles correctly. But moving into late 2025, the atmosphere has shifted dramatically. Prices have experienced significant declines, trading liquidity has diminished considerably, and the frenzied enthusiasm that characterized previous market cycles appears to be a distant memory.

The question facing the cryptocurrency community now is whether memecoins represent a fading trend from the previous bull market, or whether they still retain potential for unexpected resurgence, like many internet phenomena before them.

When Chaos Became Currency: The Memecoin Genesis

The emergence of memecoins remains inseparable from broader internet culture and social media dynamics. Unlike Bitcoin or Ethereum, which originated from detailed technical documentation and comprehensive visions for decentralized finance, memecoins typically began as internet humor, sustained by community engagement, viral content, and grassroots enthusiasm.

Dogecoin, widely recognized as the original memecoin, launched in 2013 as a deliberate parody of cryptocurrency speculation. Despite its humorous origins, it eventually achieved a multi-billion-dollar market capitalization through sustained community support and high-profile endorsements by the likes of Elon Musk. This success established a template that numerous subsequent projects attempted to replicate, often promising rapid returns without substantial underlying fundamentals.

During the market cycles of 2021 and 2024, memecoins transcended their status as mere digital assets to become cultural phenomena. Social media platforms amplified hype cycles exponentially, and retail traders participated en masse, with some small initial positions growing into substantial returns. However, as with most speculative market movements, the inevitable correction followed the euphoric peaks.

The Great Memecoin Correction of 2025

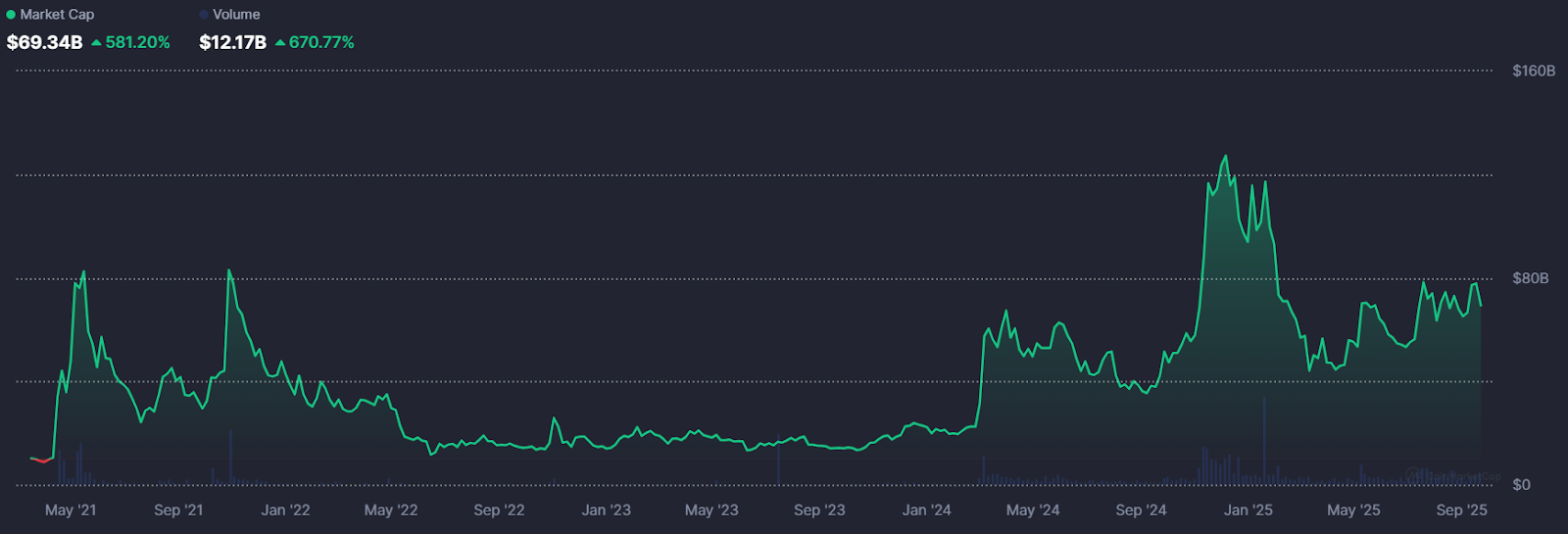

Since the speculative peaks of late 2024, memecoin markets have experienced sustained downward pressure. Market capitalizations that previously reached tens of billions of dollars have retraced by 60-90% across the sector. Data from CoinMarketCap indicates that aggregate memecoin market capitalization has declined from over $120 billion in December 2024 to just under $70 billion as of the time of writing, with many individual tokens experiencing severe liquidity constraints.

This market correction has highlighted the fundamental challenge facing the memecoin sector: without strong technological foundations or clear utility cases, these assets depend almost entirely on viral attention and consistent liquidity inflows. When these supporting factors diminish, price performance typically follows suit.

Many retail participants who entered positions near market peaks now hold assets that may not recover their previous valuations, and the collective market enthusiasm that previously drove exponential price increases has largely dissipated.

It Was Funnier the First Time Around: Why Most Memes Don't Make It

One primary factor contributing to memecoin market instability is what market analysts describe as the flash flood phenomenon. Cryptocurrency hype cycles don't typically develop gradually. They tend to surge rapidly and intensively, overwhelming normal market dynamics. However, this attention often disappears just as quickly, leaving limited lasting impact.

This dynamic creates a predictable pattern that most memecoins follow:

- Viral launch accompanied by community-driven price appreciation

- Explosive price movement that attracts new buyers

- Rapid attention fatigue as focus shifts to newer projects

- Market collapse within weeks or months

Some Memes Never Get Old: What Separates Winners from Losers

What distinguishes long-term survivors like Dogecoin and Shiba Inu, which maintain ongoing recognition, from the thousands of forgotten tokens? Market analysts describe this as the authority gap: the difference between temporary viral attention and sustained market credibility.

Successful memecoins typically manage to establish cultural relevance or practical utility that extends beyond initial market mania. Dogecoin has maintained its position as an internet cultural staple with a dedicated holder base and continued mainstream references. Shiba Inu expanded its ecosystem to include staking mechanisms and decentralized applications, positioning itself closer to legitimate alternative cryptocurrencies.

Without these elements, even the most viral initial launches tend to fade into market obscurity. The underlying meme concept alone appears insufficient for long-term sustainability, projects must develop narratives that communities and market participants can support even after speculative excitement subsides.

Could Lightning Strike Twice?

Despite current market pessimism, not everyone believes memecoins have reached their final conclusion. Market observers like Darkfost suggest that memecoin dominance within the broader alternative cryptocurrency market is approaching levels historically associated with trend reversals.

The memecoin dominance ratio, which compares memecoin market capitalization to other alternative cryptocurrencies, has been trending near technical support levels that previously marked significant turning points. If speculative capital rotates back toward high-risk digital assets, which is a common occurrence during liquidity-driven bull markets, memecoins could potentially experience another explosive growth phase.

The underlying logic remains straightforward: speculative capital typically seeks volatility opportunities, and few digital asset categories provide volatility comparable to memecoins. For market participants willing to accept associated risks, the possibility of disproportionate returns continues to exist.

The Many Pitfalls of Memeland: The Risks Never Go Away

Even assuming a potential market rebound, memecoins remain among the highest-risk positions within cryptocurrency markets. Unlike Bitcoin, which has established scarcity characteristics, or Ethereum, which powers decentralized application ecosystems, most memecoins lack intrinsic utility propositions. Their market value remains almost entirely dependent on narrative and sentiment factors.

This dynamic means that timing becomes critically important. Market participants who enter positions early and exit strategically can potentially achieve remarkable returns. However, hesitation often converts profitable positions into losses, as exponential rallies frequently reverse with minimal advance warning.

For newcomers to this market segment, the implications are clear: memecoins may provide entertainment and occasional opportunities, but they should not constitute foundational portfolio elements. Effective risk management practices, and the willingness to accept complete capital loss, remain essential when stepping into Memeland.

Curtain Call or Just Intermission?

So has the meme coin era truly concluded? The answer isn’t simple. Examining the thousands of failed token projects, the sector certainly resembles a digital graveyard. Most projects were never designed for long-term sustainability, and their decline represents the natural consequence of speculative excess.

Yet historical patterns suggest caution in declaring memecoins permanently finished. Their cyclical nature, driven by internet culture and speculative market dynamics, indicates they often resurface when liquidity conditions and risk appetite shift favorably. Whether through traditional meme-based narratives or emerging AI-enhanced strategies, future market cycles could still produce unexpected developments.

For market participants, the key takeaway remains consistent: memecoins are not traditional financial assets. They represent speculative instruments capable of both extraordinary gains and losses. The underlying joke isn’t over… but anyone who’s still in on the joke should remain prepared for the punchline.

Managing payments across borders remains one of the biggest operational challenges for expanding businesses. While digital transformation has touched nearly every aspect of commerce, international banking is currently lagging behind with separate systems for crypto and traditional currency transactions, creating unnecessary complexity.

Tap solves this problem by offering each business a multi-currency account with a dedicated IBAN that functions as a bridge between these two financial worlds. For businesses handling both crypto and fiat currencies, this means one unified system rather than juggling multiple accounts and conversion processes. This isn't just convenient - it directly impacts your bottom line by reducing transaction fees, speeding up settlements, and simplifying reconciliation.

If you're handling international payments or considering crypto adoption, this could significantly streamline your financial operations. Here's what you need to know.

What is a business IBAN?

An IBAN (International Bank Account Number) serves as your business's financial passport - a standardised identifier recognised across 78+ countries. Unlike traditional account numbers, a Business IBAN follows a structured format that includes country codes, bank identifiers, and your unique account number.

What sets Tap's approach apart is the integration of this established banking standard with crypto functionality. Instead of operating in parallel financial universes, your transactions (whether in euros, dollars, or Bitcoin) flow through a single identifiable channel.

For finance teams, this means the end of reconciliation nightmares. For your customers and partners, it means one consistent payment destination regardless of their preferred currency.

How Business IBANs Work

The mechanics behind modern business transactions

A Business IBAN functions as the digital coordinates for your company's financial location in the global banking ecosystem. When properly implemented, it creates a frictionless path for money to flow into and out of your business regardless of currency type or originating country.

Sending and receiving payments

When receiving payments, your Business IBAN acts as a universal identifier that works across different payment systems. Clients simply enter your IBAN (and sometimes BIC code) into their banking platform, eliminating the confusion of different account number formats across countries.

For outgoing payments, the process works in reverse. You provide the recipient's IBAN, specify the amount, and Tap's platform handles the routing complexities behind the scenes. This standardisation prevents the common errors that lead to payment delays and rejection fees.

What separates Tap's system from conventional banking is the integration layer that works with both crypto and traditional currencies. When a client pays in Bitcoin, for example, you can choose to receive it as cryptocurrency or have it automatically converted to your preferred fiat currency before it reaches your account.

Banking networks demystified

Business IBANs interact with several key payment networks:

SEPA (Single Euro Payments Area): Covering 36 European countries, SEPA processes euro-denominated transfers typically within one business day at low fixed costs. Your Business IBAN automatically routes euro payments through this network without requiring a separate setup.

SWIFT (Society for Worldwide Interbank Financial Telecommunication): The backbone of international banking, SWIFT connects over 11,000 financial institutions worldwide.

Real-world transaction example

Consider a UK-based e-commerce business receiving payment from a German customer:

- The customer initiates a €5,000 payment to the merchant's business IBAN

- The transaction enters the SEPA network and arrives in the merchant's Tap account within hours

- The merchant can either keep the funds in euros or convert to GBP at their preferred timing

- If choosing to convert, Tap executes the exchange at market rates with minimal spread

- The funds become available for business operations, supplier payments, or withdrawal

This same process that once required multiple accounts, banking relationships, and days of processing now happens automatically through a single business IBAN. For businesses managing dozens or hundreds of such transactions monthly, the efficiency gains and cost savings compound significantly.

The ability to handle these complex financial pathways through one unified system represents the core value proposition of modern business IBANs - simplicity on the surface, sophisticated routing underneath.

Cross-border advantages that impact your bottom line

The practical benefits of a business IBAN become immediately apparent in cross-border transactions:

- Reduced rejection rates: correctly formatted IBANs virtually eliminate payment failures due to incorrect account details

- Faster settlement times: direct routing through the SEPA network for European transactions

- Lower transaction costs: fewer intermediaries means fewer fees eating into your margins

- Simplified compliance: clearer transaction trails for more straightforward reporting

Bridging crypto and traditional finance

The crypto market now represents a $2 trillion opportunity that many businesses struggle to tap into due to technical and operational barriers. A business account with Tap eliminates these obstacles by providing:

- Seamless conversion between crypto and fiat currencies

- Consolidated financial reporting across all currency types

- Regulatory compliance built into the platform

- Reduced exposure to crypto volatility through instant conversion options

For businesses cautiously exploring crypto acceptance, this hybrid approach offers a low-risk entry point without requiring major infrastructure changes.

Implementation without disruption

Setting up a business account through Tap requires minimal operational changes:

- Fill in the contact form to initiate a callback

- Complete the business account set-up and verification process

- Receive your unique account with IBAN

- Update payment details with clients and suppliers

- Integrate with your existing accounting systems

The entire process typically takes less than 48 hours, with Tap's team handling the technical heavy lifting.

Is a Tap business account right for your growth strategy?

It's worth considering a business account if your company:

- Operates in multiple countries or currencies

- Needs to reduce payment processing costs

- Wants to accept crypto payments without complexity

- Are looking to streamline financial operations

As payment landscapes continue evolving, businesses that implement flexible, future-proof solutions gain a significant competitive advantage in customer experience and operational efficiency.

Explore how a business IBAN could fit into your financial infrastructure by visiting Tap's business solutions page, from where a dedicated account manager can discuss potential savings based on your specific transaction patterns.

The business world won't wait for outdated payment systems to catch up. The question isn't whether you need more efficient payment solutions - it's how quickly you can implement them.

Let’s make your cross-border payments simple. Schedule a chat with our expert team and explore how Tap can work for your business.