Lost crypto to a typo? Spent days chasing invoices? Request Network uses blockchain to get rid of errors, automate accounting, and turn payments into seamless transactions.

Keep reading

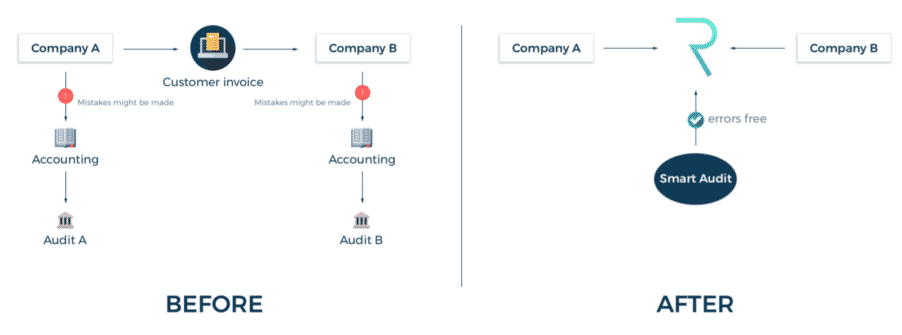

Have you ever sent an invoice and then spent the next week chasing your payment? Or worse… have you ever lost crypto by sending it to the wrong address!? If you have, well, you’re not the only one. And that’s exactly what Request has come to fix.

Traditional systems for the most part still rely on an awkward mix of middlemen, manual data entry, and accounting software that belongs in a different era. On top of all that, human error will always be a factor. Request (REQ) aims to cut through these inefficiencies by offering a blockchain solution for creating, tracking, and settling payments.

Whether you're just dipping your toes into crypto or you're already swimming in the deep end of Web3 finance, Request stands out for more than one reason. So, let’s dive in and find out!

How Request Actually Works (Without Jargon)

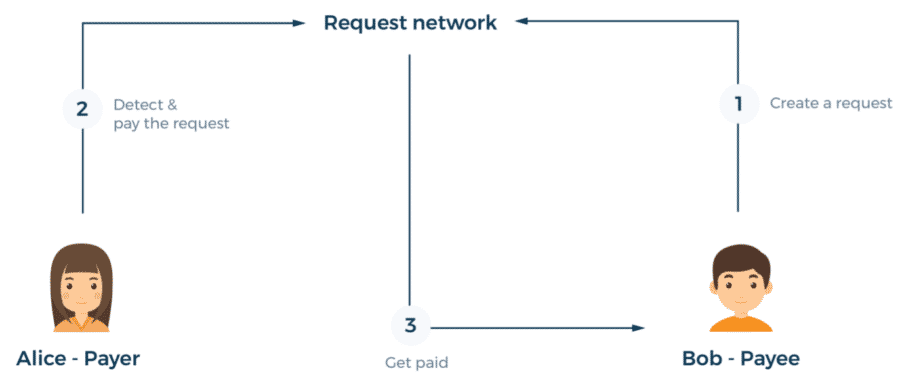

At its core, Request Network allows someone to issue a secure, immutable payment request through blockchain technology. Think of it this way: instead of manually sending funds to a wallet address (which carries the very real risk of one mistyped character sending your money into the digital void), the payee generates an invoice through a smart contract. The payer then approves it with a single transaction. Simple, clean, and significantly less prone to expensive mistakes.

This model reduces common payment errors, improves recordkeeping for everyone involved, and creates what financial people love to call "a single source of truth." Because all payment data lives on-chain, financial histories become independently verifiable without needing to trust third-party payment processors or wade through conflicting records.

It goes without saying, your accountant’s job gets significantly simpler. Payment requests, transaction amounts, due dates, tax information, and complete audit trails can all exist within the same blockchain-based system.

Why Businesses Are Building on Request

Request has become something of an unsung hero in the Web3 infrastructure world. Many blockchain organizations (from DeFi protocols to gaming studios) have adopted it because it addresses challenges that traditional payment systems simply weren't designed to handle.

Here’s what makes it special:

- Reliable audit trails. Every single request is timestamped, immutable, and independently verifiable, an accountant's dream, really.

- Built-in compliance capabilities. Request's architecture naturally supports detailed tax reporting and regulatory workflows, which matters considerably more than it sounds.

- Easy integration options. Businesses can connect Request to existing platforms like WooCommerce through tools such as WooReq, or leverage Request Finance for more sophisticated requirements.

- True scalability. The network handles recurring payments, batch transactions, and multi-chain activity across more than 25 different blockchains without breaking a sweat.

This combination of automation, transparency, and flexibility has made Request valuable for all sorts of teams, no matter the size.

Understanding the REQ Token

While Request Network focuses on simplifying payment infrastructure, the REQ token functions as the operational backbone that keeps everything running smoothly. Rather than serving as the primary transaction currency (i.e., using it to buy a delicious cup of coffee) it works behind the scenes to power the network's various operations.

Every time someone creates or processes a payment request, associated network fees are paid in REQ. These fees are then automatically converted into whichever blockchain currency is needed at that moment (such as ETH for Ethereum network gas fees), allowing Request to operate seamlessly across multiple blockchain ecosystems. Importantly, a portion of the REQ used in these transactions gets burned (or in layman terms, permanently removed from circulation) which creates a natural deflationary pressure over time.

REQ also plays a meaningful role in network governance. Token holders can participate in decisions about protocol upgrades and development priorities. This ensures the network grows through community consensus rather than through centralized decision-making. Moreover, small REQ-based micro-fees help prevent spam and malicious activity by making excessive request creation economically impractical for bad actors.

The token's economic design emphasizes long-term sustainability. With a total supply capped at 1 billion tokens and a relatively decentralized distribution model, the ecosystem sidesteps many of the concentration risks that plague other projects. This structure reduces the likelihood of sudden large-scale token dumps and supports a more stable, resilient market over time.

Why Request Matters in the Crypto Ecosystem

As blockchain technology and the crypto industry as a whole continue to mature, infrastructure projects like Request are becoming increasingly critical to the ecosystem's practical utility. They're not trying to reinvent money itself; they're focused on making financial processes demonstrably smarter.

Who Benefits From Request?

- Major DeFi organizations including Aave, Fantom, and Maker use Request to manage complex multi-token accounting across their operations.

- Traditional enterprises have adopted Request for streamlined tax reporting and regulatory compliance, particularly those operating across multiple jurisdictions.

- Developers rely on Request's API to automate everything from routine payroll processing to recurring subscription billing, eliminating manual intervention.

- Web3 projects leverage Request Finance to manage payments in dozens of different digital assets simultaneously, avoiding the headache of manual conversion and tracking.

The network has also collaborated with Aleo for confidential payroll solutions that maintain compliance while protecting employee financial privacy.

Moreover, Request gained significant mainstream attention in 2021 when The Sandbox (one of the largest NFT gaming platforms) picked Request for its payment infrastructure. This partnership not only drove increased token activity but, more importantly, validated Request as a tool with genuine utility.

Bottom Line

Request shows us what financial infrastructure could be in the Web3 era. It’s transparent, automated, and built for a fast, digital economy. It bridges blockchain's reliability with real-world needs, proving that decentralization is as relevant as it has ever been.

Where to Get REQ

Are you excited about what Request brings to the table? You can get the REQ token directly on the Tap app and start exploring the future of digital payments and invoicing today.

NEWS AND UPDATES

LATEST ARTICLE

Bitcoin Crashes Below $82K in Brutal Sell-Off

After breaking through several support levels, Bitcoin is trading around $82,000, extending a punishing downtrend that has erased more than 30% of its value since October's peak at $126,000.

The cause? A perfect storm of selloffs in U.S. equity markets, which triggered a wave of risk aversion that swept through global markets. Meanwhile, the Federal Reserve's cautious stance on further rate cuts has injected fresh uncertainty into trading floors. Markets still anticipate a 0.25% cut, but with recession fears intensifying, traders are hitting the exits. Crypto found itself directly in the crosshairs of this flight to safety

The damage extended well beyond Bitcoin. Estimates show around $2 billion in crypto positions liquidated, as forced selling and evaporating liquidity accelerated the downturn across digital assets. But here's a twist for you: Bitcoin is now entering territory that has historically preceded major recoveries. Let’s dive in.

Bitcoin Is Officially Oversold… And That Matters

The Relative Strength Index (RSI) has officially moved into oversold territory for the first time in nine months, signaling extreme selling pressure. The last time BTC hit oversold levels was in February, right before a notable rebound. Oversold signals don’t guarantee an immediate reversal, but they often mark the beginning of seller exhaustion.

In the previous oversold event, BTC dropped around an additional 10% before bouncing. If that were to happen again, BTC could briefly dip toward $77,000 before bulls regain momentum. If the current selling eases earlier, a shorter-term bounce could happen sooner.

MVRV Points to Undervaluation

Another key indicator worth looking at is Bitcoin’s MVRV Ratio. This on-chain indicator reveals whether investors are collectively sitting on profits or losses. An MVRV Ratio above 1 means the average holder is in the green; below 1 signals most are underwater.

BTC’s MVRV now sits at 1.5, its lowest level in over two years. When MVRV enters a “opportunity zone”, it suggests two things:

- Many short-term holders are underwater

- Downside selling pressure is approaching exhaustion

Key Levels to Watch

If bearish pressure continues, it’s possible BTC could revisit the $80,000 level, with a deeper support level around $77,000, matching the RSI’s recent historical pattern.

But there’s also a realistic bullish scenario: reclaiming $92,000 could turn the structure decisively bullish, opening the door to the $95,000 region and beyond.

What Can We Expect From BTC This November?

Beyond the indicators, there’s a seasonal angle worth emphasizing: Bitcoin has historically shown strong end-of-year recoveries and rallies. Even during weaker macro environments, Q4 has often delivered rebounds driven by renewed risk appetite and improved liquidity flows.

Combine that with oversold technicals, undervaluation signals, and easing macro uncertainty if the Fed does follow through on cuts, and the current levels could start looking less like panic territory and more like potential opportunity.

The Takeaway

Bitcoin's slide doesn’t appear to be driven by broken fundamentals; it's the result of macro turbulence, risk-off positioning, and temporary sentiment shifts. Short-term chop may persist, but on the flip side, key indicators are flashing oversold conditions which have historically marked turning points.

Corrections are part of Bitcoin's DNA. It has survived far steeper crashes and consistently emerged more resilient. Whether the bounce starts today or after one final shake-out, the pattern is familiar: selling exhaustion plants the seeds for the next rally. Patient holders have seen this pattern many times, and more often than not, their patience has been rewarded.

A Maturing Market in 2025

The world of cryptocurrencies in 2025 looks nothing like it did a year ago, and that's saying something in an industry that has seen it all. It has been a year of thrilling highs but also unexpected lows. Institutional money is flooding in through newly approved ETFs. Regulatory fog is dissipating in the United States, which gives both builders and investors clearer ground to stand on. Meanwhile, breakthroughs in DeFi, tokenization, and blockchain scalability are pushing the technology well beyond the realm of hype and speculative investments.

It’s clear the world of cryptocurrencies is evolving; the real question is which projects are spearheading that evolution. Whether you're a seasoned holder or just starting to pay attention, here are five digital assets that are worth your attention as the year draws to a close.

1. Bitcoin (BTC): The Golden Standard

You saw this one coming, didn’t you? To this very day, Bitcoin remains the anchor of the crypto ecosystem, influencing market sentiment, trading activity, and liquidity conditions across the whole industry. Following the April 2024 halving, BTC’s reduced issuance has contributed to renewed scarcity and a shift in mining economics.

Why You Should Watch BTC in 2025

- Institutional adoption: Bitcoin ETFs continue to attract interest, and they have managed to keep positive flows for most of the year. As time goes on, BTC integrates into portfolios and retirement products across traditional finance.

- Macro factors: With interest rates stabilizing, BTC remains a popular hedge against inflation, currency volatility, and macro uncertainty.

- Layer-2 scalability: Lightning Network improvements and new rollup-based solutions are enhancing transaction efficiency and expanding utility.

As of November 2025, BTC trades around $97,000 with a market capitalization near $2 trillion, having recently just reached an impressive new all-time high of $126,198. In spite of a recent downturn, it maintains its position as the dominant digital asset and a core indicator of broader market sentiment.

2. Ether (ETH): The Smart Contract Juggernaut

The Ethereum network continues to lead in smart contracts, decentralized applications, and tokenization initiatives. In that regard, nothing has changed. The network’s upgrades have reinforced its position as a scalable, energy-efficient computing platform.

Why You Should Watch ETH in 2025

- Post-merge efficiency: Proof-of-stake and extensive Layer-2 adoption significantly reduce fees and improve throughput.

- Enterprise adoption: Institutions and fintech companies are increasingly using Ethereum for settlement, Real-World Assets (RWAs), and programmable finance. Institutional ETH reserves have gone from less than a million ETH to more than 6 million during the course of this year.

- ETF exposure: ETH-based exchange-traded products have broadened access for retail and professional investors.

ETH trades near $3,200 after a historic rally that briefly took ETH to brand-new highs. It still ranks second in market value while maintaining the largest developer ecosystem in Web3.

3. XRP: The Cross-Border Connector

XRP continues to play a central role in modernizing international settlement, powered by Ripple’s growing partnerships with banks and payment platforms.

Why You Should Watch XRP in 2025

- Regulatory clarity: Positive rulings this year have strengthened confidence in XRP’s legal status across several jurisdictions.

- Bank integrations: Adoption in fast-growing regions supports higher transaction volume and utility.

- New payment corridors: Ripple’s liquidity network now enables transfers across a wide range of fiat and digital currencies.

XRP trades near $2.3 after almost reaching its all-time high earlier this year, and remains a top-tier cryptocurrency by market capitalization. It embodies the intersection of blockchain and traditional financial services now more than ever.

4. Solana (SOL): The High-Speed Contender

Solana has become known for speed and efficiency, enabling high-performance applications across gaming, DeFi, and NFTs. After earlier scalability issues, the network’s reliability has improved significantly.

Why You Should Watch SOL in 2025

- Institutional attention: The solana network is increasingly used for tokenized assets and real-time transactions.

- Ecosystem expansion: Developers continue launching new dApps, games, and decentralized exchanges capitalizing on fast settlement.

- Technical upgrades: Recent engineering improvements have boosted uptime and reduced network congestion.

Much like XRP, SOL came really close to reaching its all-time high but fell short. Currently, it trades near $142, solidifying itself as a major competitor in the Layer-1 landscape.

5. Chainlink (LINK): Powering the Data Economy

Chainlink remains the leading oracle solution, enabling secure data transfer between blockchains and the outside world. It’s essential for smart contracts, RWAs, and financial automation.

Why You Should Watch LINK in 2025

- RWA adoption: Banks and asset managers increasingly rely on Chainlink to support tokenized bonds, funds, and commodities.

- Cross-chain innovation: CCIP enables seamless interoperability across networks like Ethereum, Avalanche, Polygon, and Solana.

- Expanding integrations: Growth in enterprise adoption strengthens Chainlink’s role in decentralized finance and Web3 infrastructure.

LINK trades close to $14.2. Although still far from its all-time high, LINK has shown resilience during the current market downturn compared to other altcoins. Beyond price action, LINK underpins critical data processes across the digital asset ecosystem, which earns it the last sport on the list.

Why the End of 2025 Matters

So far, 2025 has been a pivotal year in the short history of crypto, and for better or worse, its last chapters seem to be following the same tone. Post-halving dynamics, ETF inflows, shifting liquidity conditions, and seasonal trading patterns all influence price movements and market behavior.

Past cycles have also set an exciting precedent. Historically, Q4 has shown higher volatility and stronger market participation compared to other quarters

Key Themes and Sectors to Follow

Beyond the charts, you can expect to hear more about these narratives, which tie directly to the cryptocurrencies highlighted above, making them important indicators of broader tech trends.

- Tokenization of real-world assets: Financial institutions increasingly use blockchain to issue and settle assets.

- AI-driven finance: Artificial intelligence is playing a larger role in trading tools, automation, and risk modeling.

- Layer-2 scaling: Growing demand for faster and cheaper transactions across multiple networks.

- Interoperability: Bridging networks to create unified digital ecosystems.

These narratives tie directly to the cryptocurrencies highlighted above, making them important indicators of broader technological and economic trends.

Conclusion

The final stretch of 2025 is undoubtedly shaping up to be a pivotal moment for the digital asset market. Bitcoin’s leadership, Ethereum’s scalable infrastructure, XRP’s global payment integrations, Solana’s high-speed capabilities, and Chainlink’s data-driven utility each contribute to a maturing ecosystem.

Whether the market consolidates or gears up for new highs, one thing is certain: the world of crypto will provide exciting developments to watch, as the hectic and unpredictable space we came to know and love steps further into a new age of widespread acceptance.

Something's shifting in crypto, and it's not just the charts. After weeks of sideways action and uncertainty, major developments out of the United States could be the catalyst that many were hoping for.

The timing couldn't be more interesting. Retail appetite is quietly building, whales are accumulating aggressively (especially in XRP), and macro conditions are starting to tilt back in crypto's favor. Individually, each of these catalysts matters. Combined, they set the stage for the kind of conditions that have historically preceded major shifts. Here's what you need to know, and why the next few weeks might be more important than most people realize.

1. U.S. Tariff Dividend

One of the biggest stories to watch is the “tariff dividend” President Donald Trump announced, a direct payment that could reach around $2,000 per person. The idea is that funds collected from higher import tariffs could be redistributed to citizens, effectively a form of economic stimulus. This could inject billions into consumer wallets, creating new liquidity across markets.

If history is any guide, such payouts can ripple into crypto. During the 2020 stimulus-era, Bitcoin saw a sharp uptick as retail investors channeled part of their checks into digital assets. The same pattern could repeat if a new wave of disposable income reaches American households, especially with crypto platforms now far more accessible than they were five years ago.

2. U.S. Government Shutdown Ending

Another factor lifting sentiment is the prospect of the U.S. government reopening. Political gridlock has weighed on markets, but signs of resolution have already sparked rallies across equities and digital assets alike. The relief comes as investors regain confidence that key economic functions will resume smoothly.

The last comparable event came in 2019, when a record-long U.S. shutdown ended after 35 days. Shortly afterward, Bitcoin began a sustained recovery, climbing from roughly $3,500 in late January 2019 to over $13,000 by mid-year. While correlation doesn’t imply causation, renewed fiscal clarity and market confidence often coincide with higher risk-appetite, the environment where crypto tends to thrive.

3. Pending ETF Approvals: Keep an Eye on XRP

Finally, the next big trigger could come from the regulatory side. Several new spot crypto ETF applications are nearing decision windows, with assets like XRP and Solana drawing heavy attention. The success of Bitcoin and Ethereum ETFs has already shown how much institutional demand can reshape liquidity and credibility in the space.

In particular, XRP could be one of the biggest winners. According to recent on-chain data, whales have accumulated more than $560 million worth of XRP in the past few weeks, a sign of growing confidence ahead of potential ETF approval. Broader adoption through regulated investment vehicles could finally unlock fresh capital inflows for alternative crypto assets beyond Bitcoin and Ethereum.

Bottom Line

Nothing is set in stone in crypto. But when liquidity, regulatory progress, and accumulation all start pointing in the same direction? That's when things get very interesting.

We're heading into the final stretch of 2025 with more aligned positive factors than we've seen in months. So, for anyone involved in crypto, whether you're trading daily or holding, now's the time to stay plugged in.

After a volatile October that saw one of the sharpest two-day liquidations of the year, the crypto market is trying to regain its footing, but conviction remains divided. Bitcoin has stabilized near key support levels, while altcoins fight against selling pressure. With macro, policy, and on-chain factors all in play, the debate between the bull and bear camps is as alive as ever. Let’s unpack the forces shaping both sides of the ledger.

The Bear Case

When Good News Don’t Move Prices

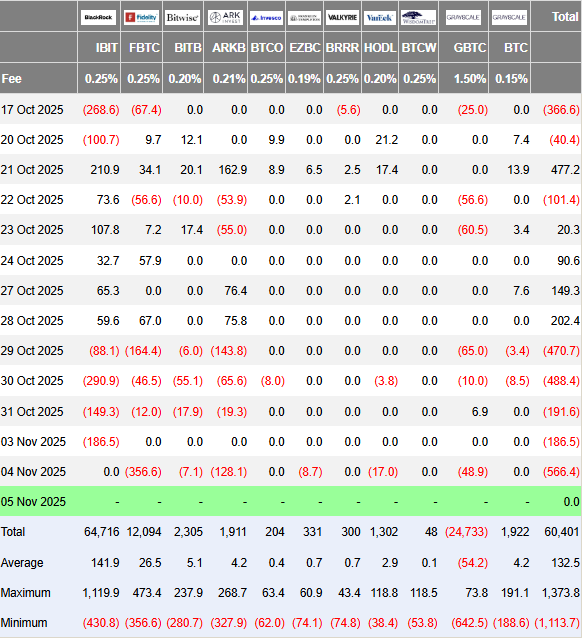

Despite encouraging ETF data and easing rate expectations, crypto failed to rally in late October, a classic warning sign of risk fatigue. According to Farside Investors, U.S. spot Bitcoin ETFs saw outflows of $470 million, $488 million, and $191 million between October 29 and 31, signaling that short-term traders were taking profits or stepping aside after “Uptober” fizzled out.

The AI Narrative

Macro sentiment still casts a long shadow. The tech-heavy equity rally, driven by AI infrastructure and chip stocks, has stirred debate about overvaluation. Nvidia’s brief breach of a $5 trillion valuation in late October triggered flashbacks of the dot-com era. If AI equities begin to deflate, crypto could feel the wealth effect unwind, as liquidity shifts from speculative assets to safer havens.

The 10/10 Crash Aftershock

The October 10 downturn marked one of the largest single-day liquidations in recent memory. Analysts note that this event left traders hunting for “dead entities” and potential hidden losses, injecting caution across the market. Even with recovery underway, scars from that drop remain fresh.

Post-Halving Cycle Timing

Bitcoin’s halving on April 20, 2024 (block 840,000) reset expectations, but it also reignited the age-old question: where are we in the cycle? Historically, the strongest rallies have occurred before or shortly after the halving, not a full year later. Some analysts now argue that the current consolidation could represent a late-cycle phase rather than the start of a new one.

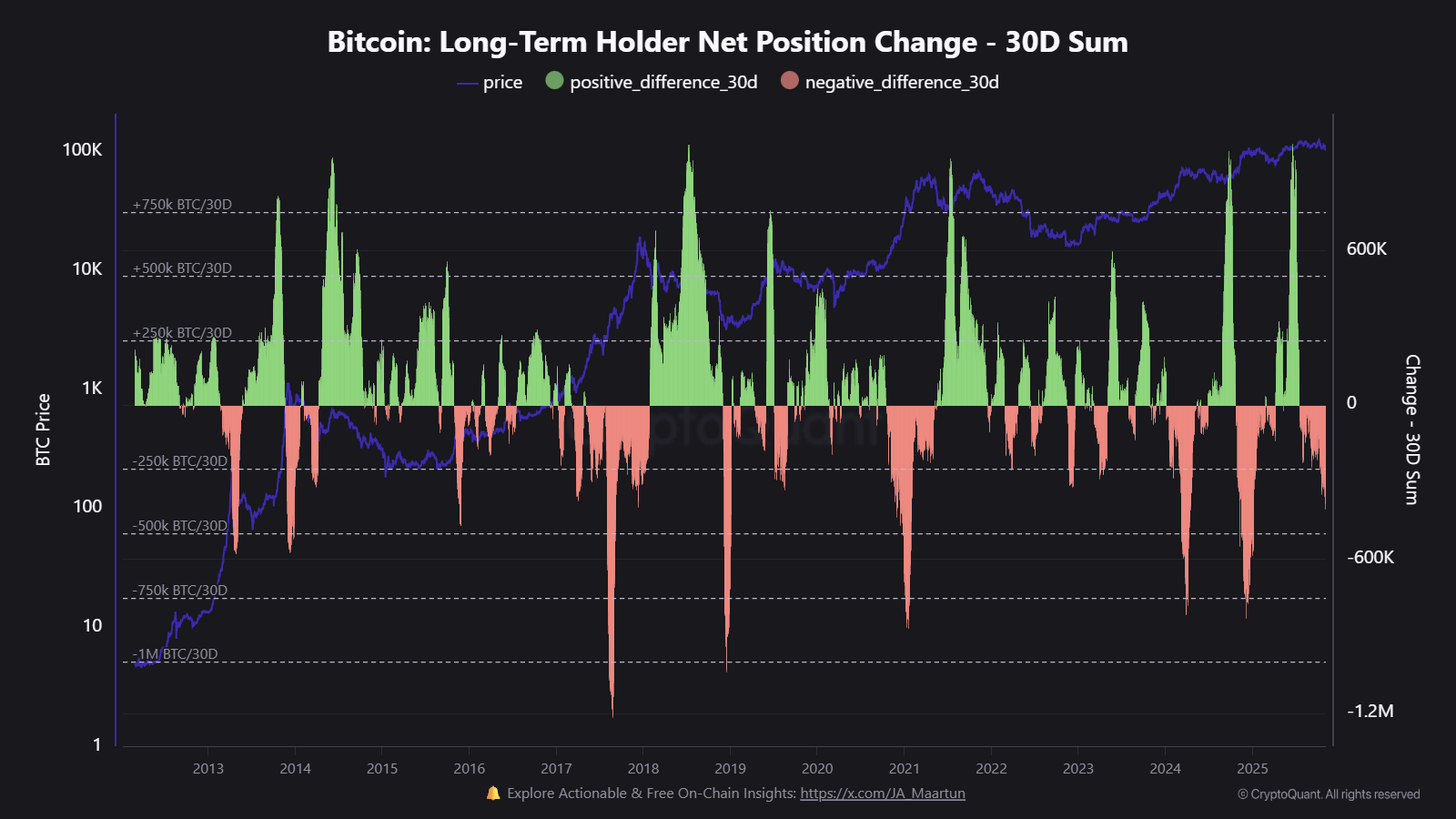

Dormant Wallets Awakening

On-chain data from CryptoQuant shows that long-term holders have increased net distribution since mid-October, with tens of thousands of BTC re-entering circulation. Several Satoshi-era wallets have also moved funds, not necessarily bearish in isolation, but enough to add pressure and short-term supply.

The Bull Case

No Signs of Euphoria

Market positioning remains far from overheated. The Crypto Fear & Greed Index currently sits in the 20s, and has been recently hovering between “Fear” and “Neutral.” That’s a far cry from the exuberant 80s to 90s readings that often precede blow-off tops. In practical terms, this suggests there’s still room for sentiment to improve before the market becomes dangerously crowded.

Liquidity Is Turning

Central banks are easing. The European Central Bank has already paused, the Bank of England has begun cutting, and the U.S. Federal Reserve is expected to follow suit with at least one more rate cut by year-end. According to the CME FedWatch Tool, the odds of a 0.25% cut currently stand above 70%. Historically, easing cycles have correlated strongly with renewed crypto uptrends, as lower yields push investors back into risk assets.

Institutional Adoption Keeps Compounding

Spot ETFs remain the biggest driver of credibility and inflows this year. Despite short-term outflows, global crypto investment products reached $921 million as recently as last week. That steady institutional presence gives crypto markets deeper liquidity and a stronger foundation than in previous cycles, where retail speculation dominated.

The Seasonal Edge

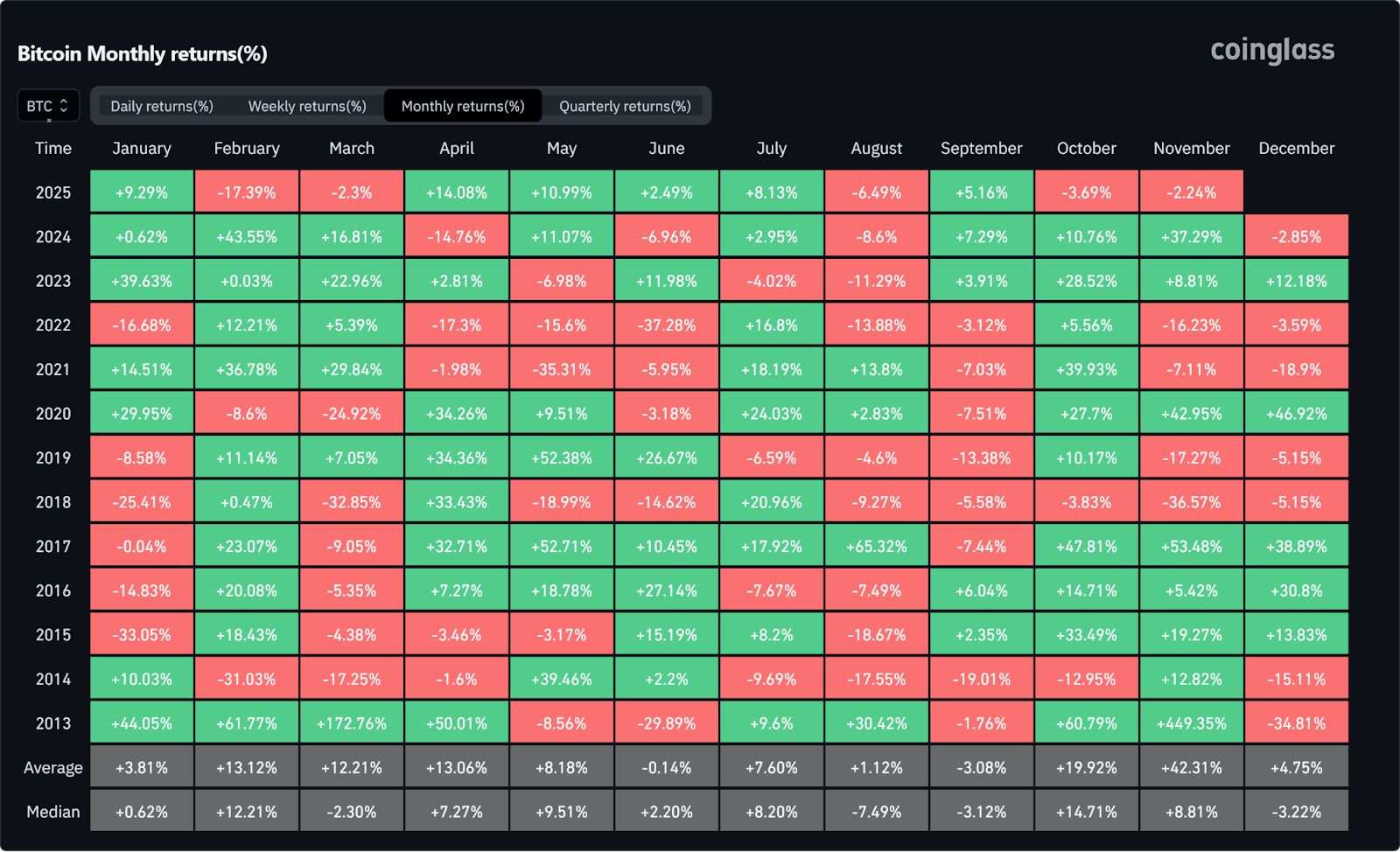

Seasonality adds another bullish data point. Since 2013, Q4 has consistently been Bitcoin’s strongest quarter on average. With November historically delivering above-average performance, many traders see the current consolidation not as a ceiling, but as a potential setup, particularly if macro data softens and ETF inflows resume.

Improving Global Sentiment

Finally, the U.S.–China trade thaw is a quiet but important catalyst. China has agreed to pause 24% tariffs on U.S. goods, marking the most significant de-escalation yet. For global risk assets, that’s a relief valve, potentially restoring confidence in emerging markets and crypto alike.

Final Verdict

Crypto’s tug-of-war between optimism and caution is far from over. The bull camp points to liquidity, policy progress, and institutional growth as evidence of a maturing ecosystem. The bears, on the other hand, warn that cycle timing, macro fragility, and old-wallet selling could cap any short-term rally.

Currently, the most realistic view lies somewhere in between these two extremes. After October's flash crash sent shockwaves through the market, a period of recalibration has taken hold. Whenever the next significant high arrives, the current environment may be best described not as peak fear or euphoria, but as consolidation.

As digital assets become a core part of personal wealth, one uncomfortable question lingers: what will happen to your crypto when you’re gone? Unlike traditional assets that can be managed through banks or brokers, cryptocurrencies are bound entirely to whoever holds their private keys. Lose the keys, and the funds are gone. Permanently.

Crypto Vanishes All the Time

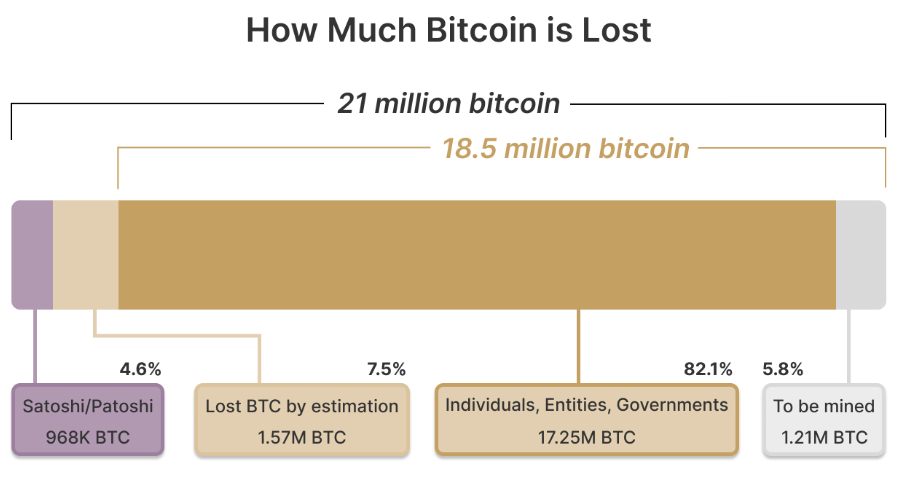

Each year, millions of dollars in Bitcoin, Ether, and other tokens vanish into the digital void when holders pass away without sharing access. It is estimated that around 1.5 million BTC (roughly 7.5% of total supply) may already be lost forever. With digital wealth now part of countless estates, preparing for the inevitable is no longer optional; it’s the responsible thing to do.

Why Planning for Crypto Inheritance Matters

In traditional finance, wealth transfer is handled through wills, trusts, and custodians. But crypto flips that model: you are the bank. Your heirs can’t simply request a password reset or call customer service. Without private keys, wallets, or access instructions, those assets are unrecoverable for all effects and purposes.

A crypto inheritance plan ensures that your digital assets, from Bitcoin and altcoins to NFTs and DeFi holdings, remain both secure and accessible to the people you choose. It bridges two crucial needs: protecting your funds today and ensuring your legacy tomorrow.

Beyond personal security, inheritance planning also reduces emotional and financial stress for your loved ones. By documenting how and where assets can be accessed, you prevent confusion and potential legal disputes.

Building the Foundation of a Crypto Inheritance Plan

Start with Legal Clarity

Consult an attorney familiar with digital assets. A properly structured will or trust should identify your crypto holdings, list beneficiaries, and outline how they can access those funds. Many jurisdictions still lack explicit laws for digital assets, so expert guidance helps ensure compliance and enforceability.

Secure Your Keys… But Don’t Overshare

The biggest challenge in crypto inheritance is private key management. If you die with your keys, your crypto dies with you. However, leaving keys in plain text within a will or document is just as risky. Instead, consider approaches like:

- Multisignature wallets, which require multiple approvals to move funds.

- Shamir’s Secret Sharing, which means splitting your seed phrase into parts distributed among trusted people.

- Encrypted backups or sealed letters stored in secure, offline locations.

Document recovery procedures in plain language so your heirs can follow them even without technical knowledge.

Choose the Right Executor

A traditional executor may not understand how to navigate crypto. You can appoint a tech-literate executor or designate a digital asset custodian to handle that portion of your estate. This ensures smooth execution and reduces the risk of errors or loss.

In a market driven by innovation and constant change, a well-structured inheritance plan offers something rare in crypto, certainty.

New Tools for a Digital Age

The rise of blockchain-based “death protocols” and smart contract automation adds a new layer of possibilities. Some platforms allow transfers to trigger automatically after certain conditions are met (for example, a verifiable death certificate or extended inactivity).

Ethereum and similar chains already support programmable inheritance systems, but these should complement, not replace, legal documents. Technology can help enforce your intentions, but law remains the foundation of inheritance.

Some investors even use “dead man’s switches”, automated systems that transfer funds if the owner doesn’t log in for a set period. While clever, it might be best to pair them with legal documents to prevent accidental activations.

Protecting Privacy While Planning Ahead

While planning for the future, it’s crucial to maintain security in the present. Avoid including wallet addresses, private keys, or passwords in public wills, which become part of the legal record. Instead, store such details in encrypted files or sealed envelopes accessible only to specific individuals.

Tools like decentralized identifiers (DIDs) and verifiable credentials can also help manage long-term identity and access rights. These systems allow you to define who can access what, and when, without intermediaries.

Custodial vs. Non-Custodial: Finding the Balance

When structuring inheritance, knowing whether your assets are held in custodial or non-custodial wallets makes all the difference.

Custodial services (like major exchanges) manage private keys on your behalf, which simplifies recovery if your heirs can provide proper documentation. However, it introduces third-party risk. Accounts can be frozen, hacked, or shut down.

Non-custodial wallets, on the other hand, offer maximum control and privacy but demand greater responsibility. If your heirs lose the seed phrase, there’s no backup plan. There’s also the possibility of taking a hybrid approach: keeping long-term holdings in non-custodial storage for security, while using reputable custodians for smaller, more accessible amounts.

Keep It Up to Date

A crypto inheritance plan is not a “set it and forget it” document. Prices change, portfolios evolve, and wallet technologies become obsolete very often. It may be wise to revisit your plan regularly, especially after major life events such as marriage, divorce, or the birth of a child.

It’s also worth keeping track of regulatory updates in your jurisdiction. Laws surrounding digital assets and inheritance are rapidly evolving, and what’s compliant today may not be tomorrow.

Common Inheritance Pitfalls

Even the best intentions can go wrong. Here are the most frequent mistakes to avoid:

- Including seed phrases directly in your will. As we mentioned before, this makes them public and vulnerable.

- Neglecting to educate heirs. Without guidance, even secure plans can fail.

- Relying solely on exchanges. Centralized platforms can fail or freeze funds.

Planning isn’t just about distributing wealth; it’s about ensuring continuity. A clear inheritance strategy preserves your crypto’s value and prevents it from becoming part of the estimated $100 billion in lost digital assets worldwide.

Protecting More Than Just Coins

Preparing a crypto inheritance plan isn’t merely about money; it’s about legacy. For all the talk about decentralization and autonomy, responsibility and forward-thinking remain at the heart of crypto ownership. By taking the time to plan ahead, you safeguard not only your wealth but also your family’s peace of mind.

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

1. Seasonality & Historical Momentum Could Kick In

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

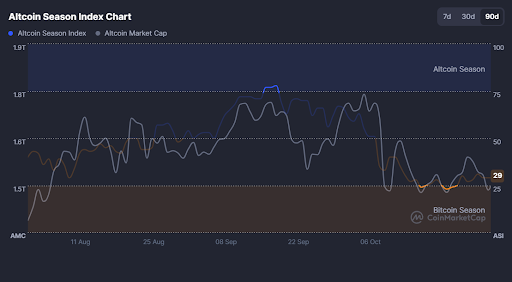

4. Altcoins at an Inflection Point

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.