.jpg)

The "redirect to bank" experience is dying. Today's consumers expect financial services to be invisible, integrated, and immediate.

The numbers confirm this story. The global embedded finance market is projected to reach $606 billion this year, growing to $7.2 trillion by 2030. But this isn't just about fintechs disrupting traditional banking anymore. We're witnessing something far more profound: the financialisation of every industry.

In an increasingly competitive landscape, embedded finance has become the new battleground for customer loyalty, operational efficiency, and revenue diversification.

From healthcare providers offering patient financing to property management companies issuing tenant payment cards, businesses across every sector are discovering that controlling the financial experience isn't just about convenience; it's becoming more about survival.

And the companies winning this race aren't necessarily the ones with the deepest financial services expertise. They're the ones that recognise a fundamental truth: every business is becoming a financial services company, whether they realise it or not. Let’s explore this narrative.

Mapping the embedded finance ecosystem

Understanding embedded finance requires looking beyond just payments to see the full ecosystem of financial services being woven into non-financial platforms. To put it more simply: it’s less about processing transactions and more about creating comprehensive financial experiences.

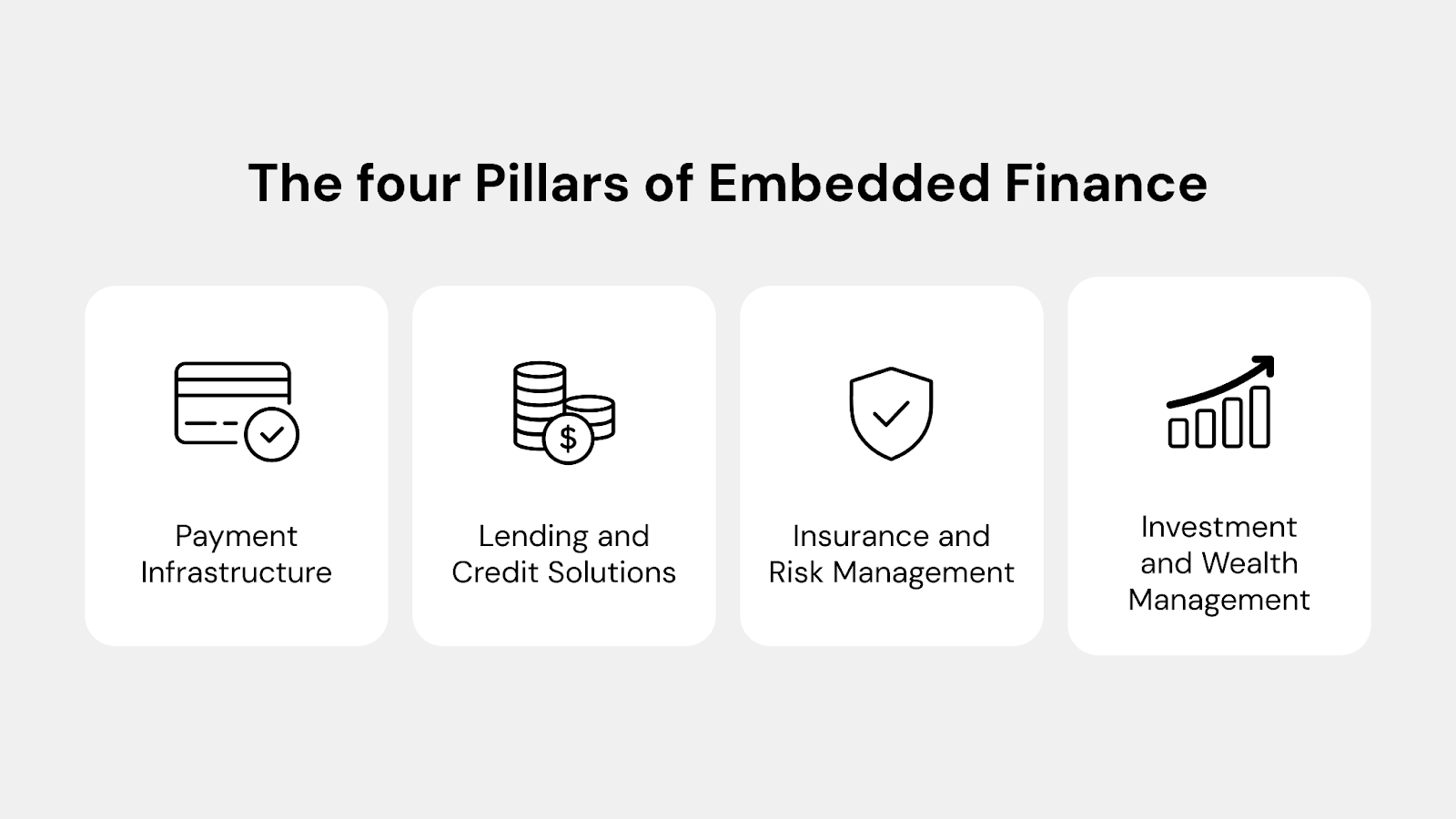

The four pillars of embedded finance

Payment infrastructure forms the foundation, encompassing everything from card issuing and digital wallets to real-time transfers and cross-border payments. This is where most companies start their embedded finance journey, but it's just the beginning.

Lending and credit solutions represent the next evolution, allowing platforms to offer instant financing, buy-now-pay-later options, and dynamic credit lines. A logistics company might offer cash advances to drivers, while an e-commerce platform provides inventory financing to sellers.

Insurance and risk management services are increasingly embedded into platforms where risk naturally occurs. For instance, ride-sharing apps offer trip insurance, rental platforms provide property protection, and gig economy apps include accident coverage.

Investment and wealth management complete the picture, with platforms offering everything from micro-investing features to full-service wealth management integrated into everyday spending activities.

The technology stack revolution

The magic happens in the middleware, where the API layers connect user-facing apps to complex financial infrastructure. Modern embedded finance platforms take away the complexity of banking operations, compliance frameworks, and regulatory requirements, allowing any company to offer sophisticated financial services through simple API calls.

And making this technology accessible is key. Where banks once had moats built from regulatory expertise and infrastructure investments, today's embedded finance platforms have levelled the playing field.

For instance, a small property management company can now offer the same calibre of financial services as a major corporation, all through cloud-based APIs and white-label solutions.

Industry deep dives: the unexpected financial innovators

The most compelling embedded finance stories are happening in industries you might not expect. Let’s explore how sectors far removed from traditional finance are leveraging embedded financial services to transform their operations:

Healthcare

Healthcare providers are embedding finance to solve patient payment collection challenges. Instead of redirecting patients to external lenders, dental practices now offer instant financing approvals directly within their systems, while telemedicine platforms integrate HSA/FSA payments and prescription processing.

The result: improved patient experience, reduced administrative overhead, and better provider cash flow.

Real estate

Proptech companies are offering customisable debit cards with built-in credit-building rewards and automated reminders, boosting tenant retention and on-time payments. While other property management utilise embedded insurance to replace traditional security deposits.

Real estate platforms can now handle everything from mortgage pre-approval to maintenance payments in one interface, while construction businesses offer instant contractor payments with automated expense tracking.

Education

Educational institutions embed financial services beyond tuition through campus spending cards, instant student aid disbursement, and skill-building microloans.

EdTech platforms offer employer-sponsored training payment cards, while international education programs solve cross-border payment complexity with embedded foreign exchange and instant fund transfers for students abroad.

Supply chain

Manufacturing and supply chain businesses optimise financial flows through embedded supplier financing and inventory funding solutions. Logistics companies provide drivers with instant payouts and controlled fuel cards, while procurement platforms automate cross-border payments and approval workflows, treating money movement as strategically as inventory management.

Entertainment

Lastly, gaming and entertainment platforms create virtual economies connected to real-world branded payment cards, while venues embed payment plans for premium experiences and refund insurance.

Creator economy platforms also provide comprehensive financial services, including instant payments, business banking, tax preparation, and investment opportunities, becoming full-service financial providers for creative professionals.

The business case: ROI beyond revenue

The financial benefits of embedded finance extend far beyond direct revenue generation. More and more businesses are starting to discover that embedded financial services can drive value through several channels at the same time.

Direct financial benefits

- Revenue diversification through interchange fees, transaction processing margins, and financial product revenue sharing can represent significant income streams. A B2B marketplace processing $100 million annually might generate $1-2 million in additional revenue through embedded card programs alone.

- Float management opportunities arise when companies hold customer funds temporarily. Even small balances across large customer bases can generate meaningful interest income when managed professionally.

- Premium service monetisation allows companies to charge higher fees for enhanced financial services while improving the customer experience. Express payment options, enhanced spending controls, and premium support can command price premiums.

Indirect value creation

- Customer lifetime value extension happens when financial services create switching costs and deepen platform engagement. Customers using embedded financial services typically show 20-30% higher retention rates and increased platform usage.

- Operational efficiency gains from automated payment processing, reduced manual reconciliation, and streamlined expense management can reduce operational costs (in midmarket companies) by 30-50% while improving accuracy and reporting capabilities.

- Data insights and behavioural analytics from financial transactions provide thorough visibility into customer behaviour, enabling better product development, pricing optimisation, and risk management decisions.

Implementation strategies & considerations

Successfully implementing embedded finance requires systematic planning and strategic decision-making focused on core business objectives.

Build vs buy vs partner framework

Cost and speed: Internal development takes 18-36 months with significant compliance costs, while white-label solutions launch in 6-12 weeks. Partnering with licensed providers reduces regulatory burden and accelerates time-to-market.

Integration options: API-first architecture enables flexible system integration. White-label solutions offer complete brand control but require more work, while co-branded approaches launch faster with shared visibility.

Implementation strategy: Consider phased rollouts (for instance, starting with basic payments and gradually adding layers such as lending or insurance) to reduce risk while enabling customer feedback integration.

Risk management essentials

Compliance: KYC/AML verification, fraud monitoring, and data security must meet financial services standards. Again, partnering with established platforms provides compliance expertise across multiple jurisdictions while maintaining a seamless user experience.

How to implement embedded finance into your business

Implementing embedded finance successfully requires systematic planning and execution. Companies that take a structured approach are more likely to achieve their objectives while minimising implementation risk.

Assessment phase

Current payment flow analysis should map all existing financial touchpoints and identify friction points, manual processes, and opportunities for improvement. Understanding current state operations provides the foundation for embedded finance strategy.

Customer journey mapping reveals where financial services integration could improve experience and create value. Look for moments where customers currently leave your platform for financial services or where payment friction creates abandonment.

Competitive landscape evaluation helps identify differentiation opportunities and best practices. Understanding how competitors and adjacent industries use embedded finance provides insight into customer expectations and market opportunities.

Strategy development

Use case prioritisation should focus on the highest-impact opportunities that align with your core business objectives. Start with use cases that solve existing problems rather than creating entirely new functionalities.

ROI modelling and business case development requires realistic assumptions about adoption rates, revenue potential, and implementation costs. Include both direct financial benefits and indirect value creation in ROI calculations.

Partner evaluation and selection should consider platform capabilities, compliance coverage, integration complexity, and long-term strategic alignment. The right partner becomes an extension of your team rather than just a vendor.

Implementation & launch

MVP development and testing allows for learning and iteration before full-scale launch. Start with core functionality and add features based on user feedback and usage patterns.

Pilot program execution with selected customer segments provides real-world validation while limiting risk exposure. Use pilot results to refine processes and optimise user experience.

Scale-up and optimisation based on pilot learnings and market feedback. Successful embedded finance implementations evolve continuously based on customer needs and market opportunities. Be sure to have your finger on the pulse.

The inevitable future

Embedded finance is more than a passing trend: it represents a fundamental shift in business operations. Companies that move early can gain lasting advantages through stronger customer relationships, new revenue streams, and greater efficiency.

The technology to implement it quickly and cost-effectively is already available, and customers increasingly expect seamless financial integration. The real question isn’t if embedded finance will become standard - it’s whether your business will lead or follow.

Don't let competitors control your customers' financial experience. Get in touch with us to explore white-label solutions that can increase retention, reduce costs, and generate new revenue quickly and compliantly. We’re here to help you transform your business in weeks, not years.

This article is for general information purposes only and is not intended to constitute legal, financial or other professional advice or a recommendation of any kind whatsoever and should not be relied upon or treated as a substitute for specific advice relevant to particular circumstances. We make no warranties, representations or undertakings about any of the content of this article (including, without limitation, as to the quality, accuracy, completeness or fitness for any particular purpose of such content), or any content of any other material referred to or accessed by hyperlinks through this article. We make no representations, warranties or guarantees, whether express or implied, that the content on our site is accurate, complete or up-to-date.