With a Fed rate cut nearly certain, these three altcoins are positioned to capitalize on the macro shift, here's what makes them stand out.

Keep reading

Heading into the Federal Open Market Committee’s October session, a high-stakes environment is emerging for crypto markets. With the CME Group’s FedWatch Tool showing about a 96 % chance of a 25-basis-point rate cut, the market is eyeing how digital-asset prices might respond.

With macro liquidity on the radar again, these three altcoins stand out as tokens worth tracking under the spotlight of the Fed’s next move.

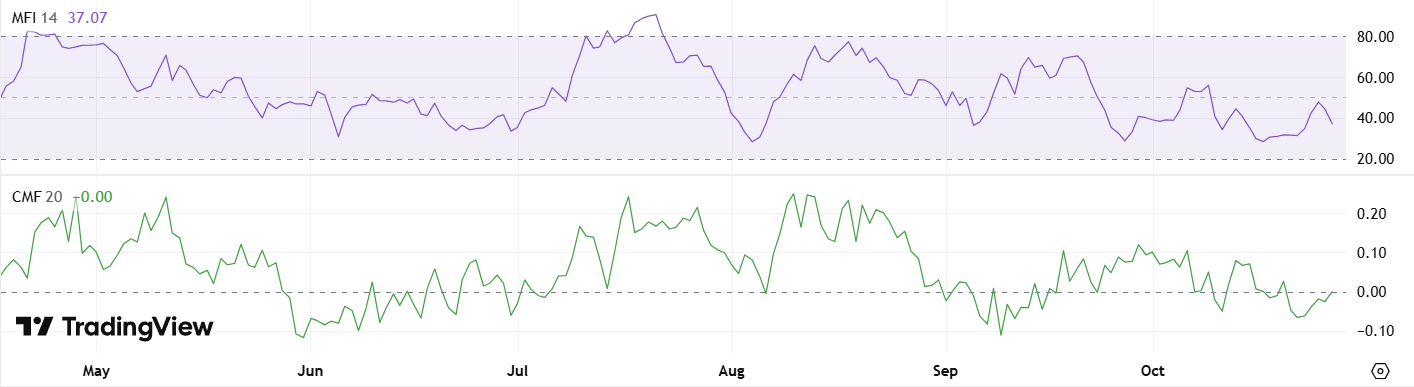

1. Chainlink (LINK)

Chainlink has been acting under pressure, trading inside a falling wedge, a pattern which sometimes marks the end of a downtrend. Still, some caution flags remain. Over the past month LINK has been trading downwards, though it’s gained some strength in the last week amid renewed buying interest. The key support around $17.08 remains critical, if LINK closes below that, a drop toward $16 could be triggered.

Conversely, diagnostics like the Money Flow Index (MFI) and Chaikin Money Flow (CMF) are showing signs of life, hinting at growing accumulation from larger holders. Combine this with a potentially dovish Fed decision, and Chainlink could be gearing for something special.

2. Dogecoin (DOGE)

Dogecoin enters the FOMC event with a bit of range-bound suspense. Since October 11, DOGE has been oscillating between $0.17 and $0.20, waiting for a trigger. A clean breakout above $0.21 could open the door to a move back towards $0.27, especially if risk-on sentiment returns.

Volume and whale‐level data add texture to the setup. The Wyckoff volume profile recently flipped from seller control to buyer control, suggesting strategic accumulation may be underway. DOGE may be quieting down before a move, a scenario traders should keep front of mind as the Fed’s decision could stir things.

3. Uniswap (UNI)

Uniswap offers compelling recovery stories entering the FOMC session. The token experienced a sharp drop on October 10, with the RSI falling below 30, classic oversold territory. Since then, UNI has rallied from near $6.20 toward $6.50, supported by strong volume on the breakout. Holding above $6.40 may confirm that buying interest is sustained.

For longer-term watchers, UNI’s former highs at $12.15 in August and $18.71 in December set the stage for what could become a multi-leg recovery if macro conditions cooperate. In a market where liquidity expectations hinge on the Fed, Uniswap's rebound has the potential to accelerate, particularly if altcoin capital begins rotating into DeFi infrastructure.

The Verdict

These tokens aren't just compelling because of their individual fundamentals, it's how those fundamentals intersect with the current macro picture. With markets rebounding and rate cuts looking increasingly likely, crypto stands to gain. Lower rates typically fuel risk appetite, unlock liquidity, and drive capital toward speculative plays, creating tailwinds that can supercharge momentum in well positioned altcoins.

That said, the Fed could also surprise with restraint, and even another “standard” 25-basis-point cut may be viewed as lukewarm. In such scenarios, the dollar may strengthen and risk assets could wobble. Traders and investors should therefore approach the market with discipline, track the macro context, and be prepared for either direction.

NEWS AND UPDATES

LATEST ARTICLE

Galxe is a Web3 credential infrastructure platform transforming how digital identity and community engagement function within the blockchain ecosystem. By creating a decentralised platform where users can build, manage, and monetise their digital credentials, Galxe bridges the gap between blockchain projects, communities, and individual users.

In a digital landscape where trust and verifiable achievements are increasingly important, Galxe is here to provide a transparent, user-owned solution that allows both projects and participants to engage in meaningful ways. Let’s explore how Galxe is shaping the Web3 space.

TLDR

- Credential infrastructure: Galxe provides a decentralised platform for creating, managing, and monetising digital credentials.

- Community engagement: Enables blockchain projects to reward and incentivise user participation through verifiable achievements.

- Multi-chain support: Operates across multiple blockchain networks, enhancing interoperability and accessibility.

What is Galxe all about?

Galxe was founded in 2021 by Harry (Hay) Jiang and Kevin Wang to improve how digital identities and community contributions are recognised in blockchain networks. Traditional social and professional networks often struggle to reflect the decentralised nature of Web3 communities, and Galxe aims to bridge this gap.

The platform helps blockchain projects build stronger, more engaged communities by providing transparent and verifiable ways to reward user participation. Unlike traditional loyalty programs, Galxe’s credential system gives users full ownership of their achievements, ensuring a fair and user-focused approach to digital identity.

How does the Galxe platform work?

Galxe’s architecture revolves around several key components that work together to create a comprehensive credential ecosystem:

Credential Protocol

At the heart of Galxe is its Credential Protocol, which allows projects to design and issue both on-chain and off-chain credentials. These credentials represent a wide range of achievements, from completing specific tasks to maintaining long-term community participation.

The platform employs a decentralised storage mechanism for these credentials, ensuring they remain secure and resistant to centralised control or manipulation. Additionally, each credential is cryptographically signed, guaranteeing authenticity and preventing tampering.

GAL Token

GAL, the token for Galxe (formerly Project Galaxy), is an Ethereum-based ERC-20 token, meaning it operates on the Ethereum blockchain. The native token, used for both governance and utility, allows holders to vote on platform decisions, stake their tokens, and unlock various features.

Unlike regular utility tokens, GAL is designed to benefit everyone, from projects and developers to community members, by creating a fair and rewarding system for all.

Galxe ID

Galxe ID is a unique digital identity system that aggregates a user’s credentials across multiple blockchain networks. Think of it as a comprehensive, blockchain-based resume that showcases your Web3 journey and achievements. This identity system provides users with a portable and verifiable digital reputation, making it easier for them to leverage their credentials across different ecosystems.

How does Galxe protect user data and credentials?

Galxe prioritises user privacy and data security through several innovative ways:

- Decentralised storage: Credentials are stored across distributed networks, preventing single points of failure and ensuring long-term data integrity.

- Cryptographic verification: Each credential is cryptographically signed, which prevents tampering and guarantees authenticity.

- User control: Users have complete ownership over their credentials, deciding what to share and with whom. This approach eliminates reliance on centralised entities, giving individuals greater control over their digital identity.

The advantages of the Galxe platform

Galxe offers several compelling advantages for both blockchain projects and individual users:

- Enhanced community engagement: Projects can design targeted incentive programs that genuinely reward meaningful participation, increasing user retention and interaction.

- Portable identity: Users can carry their achievements across different platforms and blockchain networks, making their digital credentials more valuable and widely recognised.

- Monetisation opportunities: Developers can create credential-based marketplaces and innovative reward systems, enabling new economic models in the Web3 space.

- Low barrier to entry: The platform is designed to be user-friendly, with intuitive tools that make Web3 more accessible to newcomers without requiring extensive technical knowledge.

GAL use cases

The Galxe network supports a variety of use cases across different domains:

- Blockchain projects: Create loyalty programs, airdrops, and community engagement initiatives using verifiable credentials.

- NFT communities: Verify and reward active community members, improving engagement and long-term participation.

- DeFi platforms: Design reputation-based lending or staking mechanisms, reducing risks for both lenders and borrowers.

- Gaming: Implement achievement systems with real, transferable value, allowing players to monetise their in-game progress.

How to Buy GAL

Users looking to buy or sell GAL can do so through the Tap app, provided you have a verified account. Simply download the app, complete the account set-up and verification process, and begin trading GAL using your preferred crypto or fiat currency.

Conclusion

Galxe is a platform designed to enhance digital identity and community participation in the blockchain space. By offering a transparent, user-owned credential system, it allows projects and individuals to create verifiable digital experiences and correlate that information across the entire ecosystem.

As blockchain technology develops, credential-based systems like Galxe may play a pivotal role in shaping Web3 interactions. It provides tools for developers, project owners, and users to engage with blockchain ecosystems in a structured way.

We want to inform you that XTP trading will be temporarily paused starting today on the Tap app. We’ll be temporarily pausing XTP trading on the Tap app. This short pause will give us the time we need to complete the integration of ProBit, an exchange that continues to support XTP trading.

We sincerely apologise for any inconvenience caused by the Bitfinex delisting. XTP was removed alongside several other major tokens, and the short notice left limited time to implement an alternative solution. We moved quickly, and the integration with ProBit an exchange that supports XTP is already in progress.

Here’s what you need to know:

- XTP trading will be paused for a few days

- We’re integrating ProBit into our trading engine

- Once that’s done, XTP trading will resume as usual in the app

- We’re also in active talks with several other exchanges to expand access to XTP

We know how important XTP is to many of you, and it’s at the heart of the Tap ecosystem. Thank you for your patience and continued trust. We’ll keep you updated and let you know the moment trading goes live again.

The Tap Team

Dear Tap Community,

We want to share an important update regarding the XTP token and Bitfinex. As part of a broader internal review, Bitfinex has decided to delist several tokens, including XTP along with other notable projects like The Graph (GRT), Notcoin (NOT), and seven others as part of their platform review. This appears to be a broader shift in Bitfinex's listing strategy rather than something specific to XTP.

What’s Next for XTP

The good news? XTP remains at the heart of everything we do! 💙 Our token continues to power all the awesome features you love - our tier structure, rewards, and the entire Tap ecosystem. This change doesn't affect our exciting roadmap or our vision for the future.

Here’s what we’re doing to keep things moving forward:

ProBit Integration in Progress:

Our dev team is already working on integrating ProBit (where XTP currently trades) into our Trading Engine. This will create a seamless trading experience right within our platform!

New Exchange Adventures:

We're in exciting talks with several exchanges to give XTP even more trading homes! While we need to keep the details under wraps for now (those NDAs, am I right?), know that we're pushing hard to create more options for our community.

Community First:

Remember to withdraw your tokens from Bitfinex before July 15, 2025, if you haven't already. We're here to help if you need guidance on this!

The Road Ahead 🛣️

Even in challenging markets, we see incredible opportunities for growth! Here's what's cooking:

- More XTP Utility: We're whipping up new ways for XTP to shine in our ecosystem

- Cool New Features: Q2 is going to bring some exciting platform upgrades

- Let's Talk More: We'll be sharing updates more frequently so you're always in the loop

We're so grateful for this amazing community! 🙏 Together, we've weathered challenges before, and we'll come out stronger this time too. The crypto landscape is always evolving, and we're evolving with it.

We’re deeply invested in the future of XTP - and we’re just getting started. 👏

The Tap Team

.webp)

70% of consumers prefer brands that make loyalty easier - card-linked programs make this process seamless. In today’s fast-moving market, forward-thinking businesses are leveraging co-branded payment cards to boost customer loyalty, increase lifetime value, and, as a bonus, unlock new revenue streams.

Whether you’re in retail, travel, fintech, or beyond, co-branded cards offer a strategic, low-risk way to deepen customer relationships and expand your brand’s financial ecosystem - without the heavy lift of building payment infrastructure from scratch.

In this guide, we’ll break down what co-branded cards are, why they’re a game-changer for businesses, and how you can implement one to drive growth.

What are co-branded cards?

Co-branded cards are payment cards that merge two brands: your business and the financial institution that issues the card. Unlike traditional credit or debit cards that solely display the bank's branding, co-branded cards prominently showcase your company's identity through logos, colours, and design elements that reinforce brand recognition with every transaction.

These customised financial products can take various forms—debit cards, prepaid cards, or even digital payment solutions—all carrying your brand's distinct identity at the forefront of Tap’s financial infrastructure.

Why co-branded cards drive business growth

The strategic advantages of co-branded cards extend far beyond simple brand visibility:

Enhanced customer loyalty is perhaps the most significant benefit. By offering exclusive rewards, discounts, or perks tied directly to your products or services, co-branded cards incentivise repeat business while creating emotional connections with cardholders.

Revenue diversification comes through interchange fees, where businesses receive a percentage of each transaction made with the card. This creates a passive income stream completely separate from your core offerings.

Valuable customer insights are another bonus that emerges from transaction data (within regulatory compliance), providing unprecedented visibility into spending patterns and preferences. These insights can inform product development, marketing strategies, and shape personalised offers.

How co-branded cards work

Co-branded cards are successful when each entity works in harmony with the others. Below we break down the various elements of the strategic partnership:

Role of the retailer, financial institution, and payment network

Each partner in a co-branded card arrangement brings unique capabilities to the table. The retailer or brand contributes its customer base, loyalty program infrastructure, and distinctive rewards offerings tied to its products or services.

Meanwhile, the financial institution handles the critical banking functions (underwriting, credit approval, payment processing, and regulatory compliance) leveraging its expertise in financial services management.

Completing this ecosystem, payment networks provide the technical infrastructure that enables worldwide acceptance, transaction security, and fraud protection.

This three-way collaboration creates a seamless experience where consumers simply see and interact with their favourite brand, while sophisticated financial operations run invisibly in the background.

Open-loop vs closed loop cards

Co-branded cards typically fall into two major categories that determine their versatility and reach:

Open-loop cards function anywhere the payment network (Visa, Mastercard, etc.) is accepted, giving cardholders maximum flexibility to earn rewards regardless of where they shop. This widespread acceptance makes these cards particularly attractive for everyday spending beyond the brand's own ecosystem.

Closed-loop cards, on the other hand, can only be used at specific retailers or within a limited network of businesses. While more restrictive, these cards often deliver enhanced rewards and benefits when used within their designated ecosystem, creating powerful incentives for loyal customers to concentrate their spending with the brand.

Common types of co-branded cards

The co-branded card landscape spans numerous industries, with each sector leveraging unique value propositions to attract and retain customers:

Travel-based (airlines, hotels, cruise lines)

Travel co-branded cards are a perfect example of the potential of strategic partnerships. Airline cards typically offer accelerated miles earning on ticket purchases, free checked bags, priority boarding, and pathways to elite status.

Hotel cards similarly provide point accumulation for property stays, automatic status tier upgrades, and free nights each year, while cruise line cards offer perks like onboard credits, discounts, and exclusive experiences for cardholders

The common thread connecting these offerings is their ability to transform ordinary spending into exceptional travel experiences, creating emotional connections far stronger than traditional rewards programs.

Retail-based (Amazon, Walmart, department stores)

Retail giants leverage co-branded cards to deepen their relationship with frequent shoppers. These cards typically feature enhanced cashback or points on purchases made within their stores or websites, special financing options for larger purchases, and exclusive cardholder events or early access to sales.

E-commerce leaders like Amazon have revolutionised this space by combining digital-first experiences with substantial rewards on platform purchases, creating a virtuous cycle that drives both card usage and marketplace spending.

Fuel & auto-related cards

Targeting specific spending categories, fuel and automotive co-branded cards deliver maximum value in areas where consumers have consistent, necessary expenses. These offerings typically feature significant rebates on fuel purchases, maintenance services, and automotive accessories, sometimes with tiered rewards that increase with spending volume.

For frequent drivers or commuters, these specialised cards transform unavoidable expenses into meaningful rewards, building brand loyalty through practical everyday savings.

Pros & cons of co-branded cards

As with any financial product, co-branded cards come with distinct advantages and considerations that businesses should evaluate against their strategic objectives:

Pros: rewards, discounts, brand perks, status upgrades

The rewards ecosystem represents perhaps the most compelling advantage for consumers. Co-branded cards typically offer accelerated earning rates on brand-specific purchases, creating a powerful incentive for cardholders.

Beyond points and cashback, exclusive discounts available only to cardholders create a sense of "insider status" that deepens brand affinity. Many programs also include unique perks tailored to the brand experience, for example: priority services, exclusive access, or enhanced customer support, that transform the traditional transaction into a premium relationship.

For aspirational brands, especially in travel and luxury sectors, status upgrades included with card membership provide a taste of premium experiences that often convert customers into long-term brand advocates.

Cons: high APRs, limited redemption, brand lock-in

Despite their advantages, co-branded cards typically carry higher interest rates than no-frills financial products. For customers who occasionally carry balances, these elevated APRs can potentially offset the value of earned rewards.

Redemption limitations also present potential friction points. Many programs restrict how and where rewards can be used, creating occasional frustration when consumers encounter blackout dates or availability constraints, particularly in travel-focused programs.

Perhaps the most significant strategic consideration is brand lock-in risk. Tying rewards too exclusively to your own ecosystem might boost short-term engagement but could create vulnerability if competitive offers emerge or if your brand experiences challenges. The most sustainable programs balance brand-specific value with flexibility that acknowledges diverse consumer needs.

By carefully weighing these factors against your business objectives and customer preferences, you can design a co-branded card program that delivers meaningful value while avoiding common pitfalls that undermine long-term success.

Ensure that you understand the particular offerings of the card program management system you intend on using to see how these cons might affect your decisions.

How to implement a successful co-branded card program

Launching an effective co-branded card initiative requires partnering with the right provider - one offering white-label solutions that can be customised to your specific needs while handling the complex regulatory and operational requirements.

The implementation process typically involves:

- Designing card aesthetics that reinforce your brand identity

- Creating a compelling rewards structure aligned with your business goals

- Developing marketing strategies to drive card adoption

- Establishing systems to track program performance

The most successful programs treat co-branded cards not as mere payment tools but as extensions of their customer experience strategy.

With Tap, we work closely with the company launching the product, from an intricate overview of the process to ironing out the finer details to handling all technical and regulatory elements. Contact us here for a clearer look at how your business can leverage the benefits of co-branded cards.

Why now is the time to consider co-branded cards

As digital transformation accelerates across industries, the companies that create seamless, value-added experiences for customers gain significant competitive advantages. Co-branded cards represent a unique opportunity to extend your brand presence into your customers' everyday financial lives.

With flexible white-label solutions now available, businesses of all sizes can implement sophisticated card programs without massive infrastructure investments. The barrier to entry has never been lower, while the potential benefits remain substantial.

Whether your goal is strengthening customer relationships, opening new revenue channels, or gathering deeper customer insights, co-branded cards offer a versatile solution that delivers across multiple business objectives.

By partnering with the right payment solution provider, you can transform ordinary transactions into powerful brand touchpoints - converting each swipe, tap, or digital payment into another opportunity to reinforce your relationship with customers, and potentially earn revenue too.

Want to expand your brand, boost customer loyalty, and unlock new revenue streams - without the cost or complexity of building your own financial infrastructure? White label card solutions do all this (and, you guessed it, more).

These fully customisable payment products, from physical to digital cards, let businesses seamlessly enter the world of embedded finance. In an era where speed, innovation, and customer experience set market leaders apart, offering your own branded payment cards can give you the competitive edge you need.

How do white label card solutions work?

White label card solutions operate through partnerships between businesses and specialised card issuance platforms that handle the technical and regulatory aspects of payment cards.

These solutions typically involve collaboration between the business (program manager), a banking partner (the licensed issuer), and a technology provider that manages the card program infrastructure (in this case, Tap).

The process typically follows these steps:

- A business partners with a white label card provider (Tap)

- The provider handles backend infrastructure, compliance, and processing

- The business applies its branding and determines card features

- Cards are issued to customers under the business's brand

Different types of white label cards serve various business needs:

- Debit cards link to customer accounts and withdraw funds directly

- Credit cards provide revolving credit lines with various repayment options

- Prepaid cards allow customers to load funds in advance for future spending

Modern white label solutions leverage robust APIs for seamless integration with existing business systems, enabling customisation of everything from application processes to transaction notifications and rewards programs.

The strategic advantage of branded cards

When businesses implement branded cards into their service portfolio, they're doing more than just adding a payment option – they're creating an extension of their brand that customers interact with daily.

These white-label card solutions allow companies to maintain complete brand consistency while leveraging sophisticated payment technology that would otherwise require significant investment to develop internally.

Financial service providers aren't the only businesses benefiting from this approach. Companies across sectors – from retail and travel to healthcare and professional services – are discovering how branded cards can transform customer relationships and create new revenue streams.

Key benefits of white label card solutions

Branding and customisation

White label cards serve as powerful brand reinforcement tools through both physical and digital card designs that maintain visual identity. Every transaction becomes a brand interaction, increasing visibility and recognition. Businesses can customise card designs, packaging, and digital experiences to create a cohesive brand ecosystem.

Fast market deployment

Traditional card program development can take years and millions in investment. White label solutions compress this timeline dramatically, allowing businesses to launch card programs in weeks rather than years, accelerating time-to-market and competitive advantage.

Increased revenue streams

Beyond enhancing customer experience, branded cards also create tangible financial benefits. Companies implementing these solutions typically see:

- Revenue from interchange fees

- Increased customer retention and lifetime value

- Higher average transaction values

- Reduced customer acquisition costs through enhanced service offerings

These financial advantages often make branded card programs self-sustaining or even profitable in their own right, transforming what might be considered a cost center into a revenue generator.

Customer loyalty and engagement

Custom rewards programs aligned with specific business offerings create powerful incentives for continued engagement. By connecting card usage with core business services, companies create virtuous cycles that strengthen both payment card usage and primary service engagement.

Data insights and analytics

White label card programs provide comprehensive data insights on customer spending patterns and preferences. These insights allow businesses to refine offerings, personalise marketing, and identify new opportunities based on actual customer behaviour.

Beyond traditional banking: the evolution of card solutions

The fintech revolution has democratised what was once the exclusive domain of traditional banks. Today's white-label card solutions offer businesses unprecedented flexibility and control. These capabilities allow businesses to not just participate in the financial ecosystem but to actively shape it according to their unique value proposition.

White label card security and compliance

Security and regulatory compliance form the foundation of successful white label card programs. Modern solutions incorporate multiple layers of protection:

- Advanced security features: EMV chips, tokenisation, and 3D Secure technology protect transactions from fraudulent activity

- Regulatory compliance: Established providers handle complex requirements including PCI DSS, KYC/AML regulations, and financial licensing

- Custom controls: Businesses can implement specific spending rules, transaction limits, and merchant category restrictions

- Real-time monitoring: Sophisticated fraud detection systems identify unusual patterns and potential threats before they result in losses

Working with experienced white label providers ensures these critical security and compliance components are properly managed while allowing businesses to focus on their core competencies.

Creating seamless customer experiences

Modern consumers expect frictionless experiences across all touchpoints with a brand. Branded cards enable businesses to extend this seamless experience into payment interactions, whether online or in person. By controlling the card experience, companies can ensure consistency at every stage of the customer journey.

This seamless integration becomes particularly valuable when businesses can connect card usage with their core services. For example, a travel company's branded card might offer enhanced rewards for bookings, creating a virtuous cycle that strengthens both card usage and primary service engagement.

Comparison: White label vs. custom-built card solutions

Businesses considering card issuance typically evaluate two approaches:

White label solutions:

- Lower upfront investment

- Faster implementation (weeks/months vs. years)

- Reduced regulatory burden

- Ongoing operational support

- Limited by provider's capabilities

Custom-built solutions:

- Complete control over features

- Potentially lower per-transaction costs at scale

- Greater differentiation potential

- Significant expertise required

- Higher regulatory and compliance burden

For most businesses, white label solutions provide the optimal balance between customisation and practicality, allowing them to focus resources on their core competencies while still delivering compelling financial products.

In terms of timelines, Tap’s streamlined process takes your white label card solution from concept to delivery in just 12 weeks.

How to choose the right white label card provider

Selecting the right partner for your white label card program requires careful evaluation of several factors:

- Customisation depth: How much control will you have over card appearance, features, and user experience?

- Technical integration: Does the provider offer robust APIs and documentation that align with your technical capabilities?

- Compliance expertise: What regulatory requirements will the provider handle, and what remains your responsibility?

- Scalability: Can the solution grow with your business and accommodate increasing transaction volumes?

- Support structure: What level of ongoing assistance is available for both technical and operational issues?

Leading providers differ in their strengths, with some focusing on specific verticals or use cases. The right choice depends on your specific business needs, technical resources, and growth objectives.

Future trends in white label card solutions

The white label card industry continues to evolve rapidly with several emerging trends:

- Digital-first cards: Virtual cards becoming primary with physical cards as optional supplements

- Crypto integration: Adding crypto capabilities to traditional card products

- Buy Now, Pay Later: Incorporating flexible payment options within white label offerings

- AI-enhanced features: Sophisticated spending insights and fraud detection through artificial intelligence

- Embedded finance expansion: Cards becoming entry points to broader financial service ecosystems

For forward-thinking businesses, the question isn't whether to explore branded card offerings – it's how quickly they can be implemented to capture the substantial benefits they provide.

Getting started without the complexity

The technical complexity that once made card issuance prohibitively difficult has been eliminated by modern fintech platforms. Today's white-label solutions handle regulatory compliance, fraud prevention, and technical integration, allowing businesses to focus on what they do best.

By partnering with the right platform, companies can launch branded card programs quickly, creating lasting competitive advantages that will be increasingly difficult for latecomers to overcome.

To learn more about how white label card solutions can influence your specific business, fill in your details here and a specialised account manager will walk it through with you.

Looking for a competitive edge? White-label card programs let SMEs launch branded payment cards - without the hassle of becoming a financial institution.

This guide breaks down how white-label cards work and how they can boost revenue, enhance customer loyalty, and streamline operations - all while keeping you in control.

Introduction to card issuing for SMEs

Traditionally, only banks could issue payment cards. But fintech innovation has changed that - now, SMEs can launch their own branded cards with white-label solutions, without the complexity of obtaining a banking license.

This isn’t just about processing payments - it’s about unlocking new revenue, strengthening customer relationships, and ensuring top-tier security and compliance. With the right partner, you get all the benefits of card issuing without the complexity of a banking license.

Understanding card issuing for SMEs

The process of implementing a white-label card program is more straightforward than many businesses realise. By partnering with a trusted card issuing platform like Tap, SMEs can easily launch their own branded cards without having to worry about things like technical infrastructure and regulatory requirements.

These platforms provide robust APIs and intuitive dashboards that allow SMEs to manage their card programs effectively.

In a nutshell: modern card issuing platforms act as a bridge between your business and the complex financial infrastructure required for card issuance. They handle the heavy lifting of payment processing, security protocols, and regulatory compliance while allowing you to maintain control over the customer experience and branding.

Benefits of card issuing for SMEs

White-label card programs offer numerous advantages for growing businesses:

Increased revenue opportunities

By offering branded payment cards, businesses can generate additional revenue through interchange fees, subscription models, and value-added services.

Enhanced brand visibility

Custom-branded cards serve as a constant reminder of your business in customers' wallets, strengthening brand recognition and loyalty.

Improved financial control

Advanced reporting and monitoring tools provide real-time insights into spending patterns and financial flows, enabling better business decisions.

Superior customer experience

White-label cards can be seamlessly integrated with your existing services, providing customers with a unified, branded experience across all touchpoints.

Best practices for managing card issuing

Success with white-label card programs requires careful attention to several key areas:

Financial planning

Consider not just the initial setup costs but ongoing operational expenses. Many platforms offer scalable pricing models that grow with your business.

Integration strategy

Choose a platform that easily integrates with your existing systems, from accounting software to customer relationship management tools.

Brand consistency

Leverage customisation options to ensure your cards reflect your brand identity while maintaining professional design standards.

Security infrastructure

Implement robust security measures from day one, including encryption, tokenisation, and real-time fraud monitoring.

Compliance and regulations

Regulatory compliance is a critical aspect of card issuing that quality white-label solutions should handle seamlessly. Your platform provider should ensure:

- Automatic updates to comply with changing regulations

- Built-in KYC (Know Your Customer) and AML (Anti-Money Laundering) protocols

- Regular security audits and certifications

- Clear documentation of compliance procedures

Fraud prevention

Modern white-label card solutions incorporate sophisticated fraud prevention measures:

- Real-time transaction monitoring

- Machine learning algorithms for fraud detection

- Customisable spending controls and limits

- Instant card freeze capabilities

- Automated alerts for suspicious activities

Seamless card issuing, maximum business growth

White-label card programs give SMEs the power to expand services, boost revenue, and build stronger customer loyalty, without the hassle of managing financial infrastructure. With the right platform partner, launching a branded payment card is faster and easier than ever.

Tap takes care of the complexities so you can focus on growth. Ready to get started? Contact us today and let’s bring your white-label card program to life.