With a Fed rate cut nearly certain, these three altcoins are positioned to capitalize on the macro shift, here's what makes them stand out.

Keep reading

Heading into the Federal Open Market Committee’s October session, a high-stakes environment is emerging for crypto markets. With the CME Group’s FedWatch Tool showing about a 96 % chance of a 25-basis-point rate cut, the market is eyeing how digital-asset prices might respond.

With macro liquidity on the radar again, these three altcoins stand out as tokens worth tracking under the spotlight of the Fed’s next move.

1. Chainlink (LINK)

Chainlink has been acting under pressure, trading inside a falling wedge, a pattern which sometimes marks the end of a downtrend. Still, some caution flags remain. Over the past month LINK has been trading downwards, though it’s gained some strength in the last week amid renewed buying interest. The key support around $17.08 remains critical, if LINK closes below that, a drop toward $16 could be triggered.

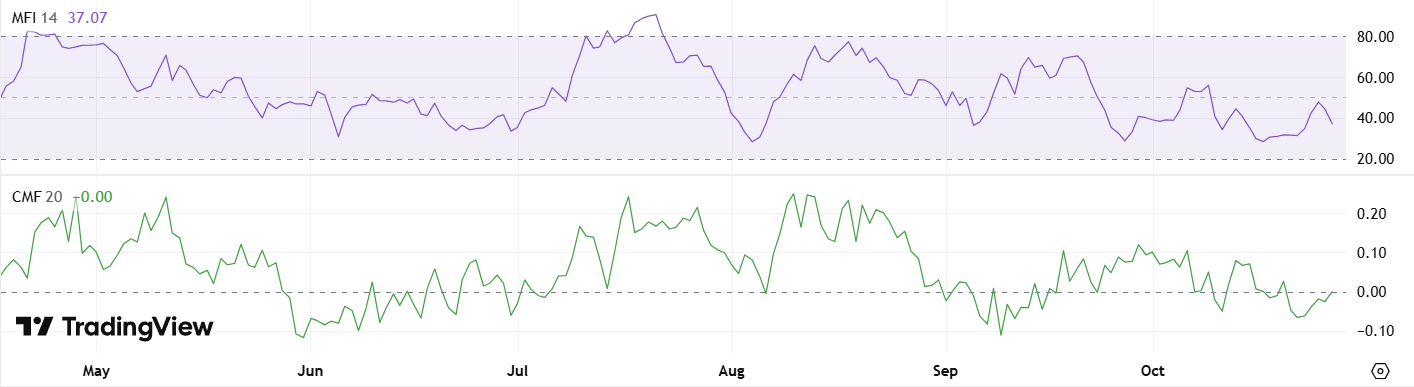

Conversely, diagnostics like the Money Flow Index (MFI) and Chaikin Money Flow (CMF) are showing signs of life, hinting at growing accumulation from larger holders. Combine this with a potentially dovish Fed decision, and Chainlink could be gearing for something special.

2. Dogecoin (DOGE)

Dogecoin enters the FOMC event with a bit of range-bound suspense. Since October 11, DOGE has been oscillating between $0.17 and $0.20, waiting for a trigger. A clean breakout above $0.21 could open the door to a move back towards $0.27, especially if risk-on sentiment returns.

Volume and whale‐level data add texture to the setup. The Wyckoff volume profile recently flipped from seller control to buyer control, suggesting strategic accumulation may be underway. DOGE may be quieting down before a move, a scenario traders should keep front of mind as the Fed’s decision could stir things.

3. Uniswap (UNI)

Uniswap offers compelling recovery stories entering the FOMC session. The token experienced a sharp drop on October 10, with the RSI falling below 30, classic oversold territory. Since then, UNI has rallied from near $6.20 toward $6.50, supported by strong volume on the breakout. Holding above $6.40 may confirm that buying interest is sustained.

For longer-term watchers, UNI’s former highs at $12.15 in August and $18.71 in December set the stage for what could become a multi-leg recovery if macro conditions cooperate. In a market where liquidity expectations hinge on the Fed, Uniswap's rebound has the potential to accelerate, particularly if altcoin capital begins rotating into DeFi infrastructure.

The Verdict

These tokens aren't just compelling because of their individual fundamentals, it's how those fundamentals intersect with the current macro picture. With markets rebounding and rate cuts looking increasingly likely, crypto stands to gain. Lower rates typically fuel risk appetite, unlock liquidity, and drive capital toward speculative plays, creating tailwinds that can supercharge momentum in well positioned altcoins.

That said, the Fed could also surprise with restraint, and even another “standard” 25-basis-point cut may be viewed as lukewarm. In such scenarios, the dollar may strengthen and risk assets could wobble. Traders and investors should therefore approach the market with discipline, track the macro context, and be prepared for either direction.

NEWS AND UPDATES

LATEST ARTICLE

Card programs are no longer just a feature, they’ve become a competitive advantage. From fintech startups to global enterprises, businesses are embedding financial services into their ecosystems to improve customer retention, unlock new revenue streams, and gain a market edge. With embedded finance projected to reach $570.9 billion by 2033, the time to act is probably now.

This comprehensive guide explores the intricacies of card program management and its crucial role in business success.

Why businesses are integrating white-label card programs

Beyond branding benefits, white-label card programs provide businesses with complete control over the customer journey, access to valuable transaction data, and new revenue opportunities. Thanks to advancements in fintech infrastructure, companies can integrate financial services seamlessly without requiring a financial license.

However, the timing is optimal. With the potential to increase top-line revenue, white label cards enable businesses to:

- Own the complete customer journey

- Gather valuable transaction data

- Differentiate their offering

- Create new customer touchpoints

As industry leaders increasingly make white-label cards central to their digital transformation, the opportunity for competitive advantage grows.

What is card program management?

Starting with the basics, card program management involves overseeing and coordinating payment card services, from design to day-to-day operations. This ensures that cards run smoothly and meet regulatory standards.

Key responsibilities of program managers:

- Strategic planning – Defining objectives, market positioning, and growth strategies.

- Compliance & risk management – Ensuring adherence to PCI DSS, AML, and KYC while mitigating fraud risks.

- Operational oversight – Managing banks, processors, and card networks for seamless transactions.

- Customer experience optimisation – Enhancing user experience with smooth onboarding, rewards, and support.

Program managers also go beyond administrative tasks by setting up risk frameworks, enforcing compliance controls, and improving customer experiences, while managing costs. They play a balancing act between regulatory demands and business goals, while managing relationships with service providers, like card manufacturers and tech vendors.

By connecting all these elements, program managers create a seamless, well-functioning payment card ecosystem that delivers success and efficiency.

The strategic importance of card program management

The complexity of launching and managing a card program extends far beyond just simple payment processing. Modern businesses require robust management systems and abilities that address multiple critical areas, including:

Compliance and regulatory management

Card program management plays a crucial role in navigating the complex regulatory landscape. This includes ensuring adherence to:

- Payment Card Industry Data Security Standard (PCI DSS) requirements

- Anti-Money Laundering (AML) protocols

- Know Your Customer (KYC) standards.

These crucial compliance measures protect both the business and its customers while maintaining the integrity of the financial system.

Risk and fraud prevention

In an era of sophisticated financial crimes, comprehensive risk management is paramount. Effective card program management incorporates advanced fraud detection systems, real-time transaction monitoring, and efficient dispute resolution processes.

This proactive approach helps minimise financial losses while maintaining customer trust.

Operational excellence

Managing relationships with multiple third-party providers requires sophisticated coordination. Typically, a team of program managers oversee interactions with issuing banks, card networks, and processors, ensuring smooth operations across the entire payment ecosystem.

Customer experience enhancement

Successful card programs focus on more than just functionality — they prioritise exceptional customer experiences. This includes smooth onboarding, responsive support, and value-added features like rewards and personalised services that drive engagement and loyalty.

How card program management works

The successful implementation of a card program requires a collaborative approach between program managers and the client organisation. The following is an example of a framework that is structured to ensure seamless execution while maintaining compliance and operational excellence.

Program design and implementation

This foundational phase requires active participation from both parties:

Client organisation responsibilities:

- Define target user groups and program objectives

- Provide branding assets and guidelines

- Establish internal governance structure

- Determine program budget and KPIs

Program manager deliverables:

- Configure program features and parameters

- Implement compliance frameworks

- Set up risk management systems

- Design operational workflows

Technical integration and onboarding

The integration phase combines technical expertise with organisational readiness:

Client organisation responsibilities:

- Designate technical integration team

- Complete required compliance documentation

- Establish internal user management processes

Program manager deliverables:

- Secure BIN (bank identification number) sponsorship

- Implement digital wallet integration

- Configure secure account setup processes

- Set up fraud prevention systems

Program monitoring and optimisation

Ongoing program success relies on collaborative oversight:

Client organisation access:

- Real-time dashboard monitoring

- Custom report generation

- User activity tracking

- Expense management tools

Program manager services:

- Transaction monitoring and analysis

- Fraud detection and prevention

- Performance optimisation recommendations

- Compliance and risk assessment

This structured approach ensures the program manager provides the technical infrastructure and expertise, while the client organisation maintains control over strategic decisions and user management.

The key players in card program management

Effective card program management relies on the collaboration of key stakeholders, each playing a crucial role in ensuring seamless operations and compliance. These include:

Issuing banks

These regulated financial institutions hold the necessary licenses and provide the fundamental banking infrastructure that enables card issuance and transaction processing.

Card networks

Organisations like Visa and Mastercard maintain the payment networks that enable global card acceptance and establish operating rules that govern transaction processing.

Issuer processors

These technology providers handle the complex backend operations of transaction processing, settlement, and compliance management.

Card manufacturers

Specialised vendors are responsible for producing physical cards and implementing secure virtual card solutions.

At Tap, our white-label card services take care of all of the above, liaising with you on the finer details.

Choosing your management approach

Organisations must carefully consider their approach to card program management:

Self-managed programs

Maximum control but high complexity. Ideal for businesses with in-house regulatory and tech expertise.

Outsourced management

Faster to market with lower operational costs. A great option for businesses looking to launch quickly without building infrastructure.

Hybrid solutions

A flexible approach that allows businesses to maintain control over key functions while outsourcing technical or regulatory aspects. Tap’s white-label solutions cater to businesses seeking a balance between control and convenience.

Future trends shaping card program management

The future of card program management is being shaped by several key trends:

Embedded finance

The integration of payment solutions into non-financial products and services is creating new opportunities for businesses to enhance their value propositions and generate additional revenue streams.

Advanced analytics and AI

Artificial intelligence and machine learning are revolutionising fraud prevention and customer experience optimisation, enabling more sophisticated risk management and personalisation capabilities.

Digital-first solutions

The increasing preference for virtual cards and mobile payments is driving innovation in digital payment solutions and program management approaches.

Conclusion

Effective card program management has become a crucial capability for businesses seeking to compete in today's digital economy. Whether through self-managed programs, outsourced solutions, or hybrid approaches, organisations must carefully consider their options and choose strategies that align with their business objectives and operational capabilities.

Success in card program management requires a comprehensive understanding of the ecosystem, strong attention to compliance and risk management, and a commitment to delivering exceptional customer experiences. As the payment landscape continues to evolve, businesses that master these elements will be well-positioned to capitalise on new opportunities and drive sustainable growth.

Launching a successful card program requires the right expertise, technology, and compliance framework. At Tap, we handle the complexities so that you can focus on growth. Ready to elevate your business with a white-label card program? Contact us to explore how our white-label solutions can fit your business needs.

Imagine walking into your favourite store and finding everything 10% cheaper than last month. Sounds great, right? But what if your salary also dropped by 15%, and your home's value plummeted by 20%? Welcome to the complex world of deflation – an economic phenomenon that turns the simple act of waiting to make a purchase into a nationwide economic strategy, and not in a good way.

While we often worry about prices going up, deflation shows us why prices going down can be just as threatening to our economic well-being. In this guide, we'll uncover why some lose sleep over falling prices, explore real-world examples that have shaped nations, and understand why a healthy economy is all about finding the right balance.

What is deflation?

Deflation is when prices of goods and services decrease across the economy over time. It's essentially the opposite of inflation, which is what we're more familiar with (when prices going up year after year).

To put it simply: if inflation means your dollar buys less tomorrow than it does today, deflation means your dollar will buy more tomorrow than it does today.

Imagine walking into your local grocery store and noticing that milk costs $3.50 this month, down from $3.75 last month. Then next month, it drops to $3.25. If this pattern happens across many products and services throughout the economy, that's deflation in action.

Is deflation good or bad?

It's tempting to think deflation is great news (spending less on groceries does sound like the dream). Unfortunately, the reality is more complicated.

The good side:

- Your purchasing power increases

- Your savings are worth more without doing anything

- Essential goods become more affordable

The not-so-good side:

- People delay purchases (why buy today if it'll be cheaper tomorrow?)

- Businesses earn less revenue, leading to potential layoffs

- Debt becomes more burdensome (you owe the same amount, but money is worth more)

The biggest danger is what economists call the "deflationary spiral." This is when falling prices lead to lower production, which causes job losses, which reduces spending power, which pushes prices down further... and the cycle continues downward.

What causes deflation?

Deflation doesn't just happen randomly. There are several key triggers:

1. Contraction in money supply

When there's less money circulating in the economy relative to the goods and services available, prices tend to fall. This can happen when central banks tighten monetary policy or when credit markets freeze up during financial crises.

2. Decreased consumer demand

When people spend less, whether due to economic uncertainty, rising unemployment, or shifting preferences, businesses often respond by lowering prices to attract customers.

3. Increased productivity or efficiency

Sometimes deflation happens for positive reasons. When companies find ways to produce more goods with fewer resources (like through technological innovation), they can pass those savings on as lower prices. Yes, for profit-hungry companies - this is rare, but it’s still possible.

4. Government and central bank policies

Certain fiscal and monetary decisions can inadvertently trigger deflation, especially if they're too restrictive during economic downturns.

How is deflation measured?

Just like inflation, deflation is typically measured using price indexes, with the Consumer Price Index (CPI) being the most common. When the CPI shows a negative percentage change over time, that's deflation.

It's important to distinguish between:

- Deflation: A general decrease in prices (negative inflation rate)

- Disinflation: When inflation slows down but prices are still rising, just at a slower rate

- Inflation: A general increase in prices over time

Economists look at various sub-indexes too, as deflation might affect different sectors differently. For example, technology products have experienced their own form of deflation for decades, even during periods of overall inflation.

What are the effects of deflation?

Short-term benefits for consumers

In the immediate term, consumers might celebrate as their money stretches further. Essential goods cost less, and savings seem to grow in value automatically.

Long-term consequences

The longer-term picture is where things get problematic:

- Delayed purchases: Consumers postpone buying non-essential items, expecting even lower prices in the future.

- Business challenges: Companies face declining revenues while many of their costs remain fixed.

- Job market impact: As businesses struggle with reduced profits, layoffs often follow, increasing unemployment.

- Wage deflation: Eventually, wages start to decrease too, offsetting any benefit from lower prices.

The deflationary spiral explained

The most feared consequence is the deflationary spiral:

- Prices fall

- Consumption decreases (as people wait for even lower prices)

- Production cuts follow

- Unemployment rises

- Less money is spent in the economy

- Prices fall further

- Repeat

This vicious cycle is what turned the 1929 stock market crash into the Great Depression, which is why central banks are typically quick to fight even hints of deflation.

Why deflation makes debt worse

One of deflation's cruellest effects is on debt. Here's why:

When prices and potentially wages fall, but your debt stays the same, the real burden of that debt actually increases. Imagine you have a $250,000 mortgage:

- During inflation: Your income likely rises over time, making that fixed payment feel smaller in proportion to your earnings.

- During deflation: Your income might decrease, but your mortgage payment remains unchanged, taking a bigger bite out of your budget.

Plus, the value of the asset you purchased (like a house) might decrease during deflation, potentially leading to negative equity (owing more than the asset is worth).

This debt burden effect can ripple through the economy, leading to increased defaults, foreclosures, and bankruptcies.

How does deflation affect the economy?

The broader economic impacts of deflation can be severe:

Recession and depression risks

Extended periods of deflation are strongly associated with economic contractions. The most famous example is the Great Depression, when U.S. prices fell by roughly 25% between 1929 and 1933.

Reduced business investment

When companies expect falling prices and revenues, they're less likely to invest in new projects, equipment, or employees. Why expand when you expect smaller returns?

Central bank challenges

Fighting deflation can be harder than fighting inflation. While central banks can always raise interest rates to combat inflation, there's a limit to how far they can cut rates to fight deflation (known as the "zero lower bound" problem).

Banking system stress

As borrowers struggle with the increasing real value of their debts, loan defaults rise, potentially threatening financial stability.

Can deflation ever be a good thing?

Yes, in certain contexts, deflation isn't necessarily bad:

Technological deflation

The consistent price drops in electronics like TVs, computers, and smartphones represent a form of "good deflation." These price decreases stem from innovation and efficiency gains, not economic distress.

Sector-specific benefits

Some industries might benefit from deflation in their input costs. For example, manufacturing businesses might enjoy lower raw material prices even if it creates challenges elsewhere.

Short-term vs. structural deflation

Brief episodes of mild deflation don't always spell disaster. It's the persistent, economy-wide deflation that raises red flags for economists.

The key difference is the cause: deflation from increased productivity and technological advancement is generally positive, while deflation from collapsed demand is problematic.

How do governments and central banks fight deflation?

When deflation threatens, policymakers have several tools at their disposal:

Monetary policy tools

- Lowering interest rates: Making borrowing cheaper to encourage spending and investment

- Quantitative Easing (QE): Central banks purchase assets like government bonds to increase money supply

- Forward Guidance: Promising to keep policies accommodative for extended periods to build confidence

Fiscal policy approaches

- Government spending: Increased public expenditure on infrastructure and services

- Tax cuts: Reducing tax burdens to boost consumer spending power

- Direct payments: Stimulus checks or universal basic income proposals

What happens to investments during deflation?

Different asset classes perform very differently during deflationary periods:

Cash and high-quality bonds

Cash and government bonds often perform well during deflation because their fixed returns become more valuable as prices fall. However, if deflation leads to a severe economic crisis, even government bonds could face risks.

Stocks and real estate

Equities and property typically struggle during deflation because:

- Corporate profits decline as prices fall

- Real estate values drop while mortgage debt remains unchanged

- Dividend payments may be reduced as companies conserve cash

Defensive investment strategies

Some approaches that might help protect portfolios include:

- Focus on companies with strong cash positions and minimal debt

- Prioritise businesses selling essential goods with inelastic demand

- Consider some allocation to Treasury bonds as a hedge

- Look for companies with pricing power that can maintain margins even in challenging environments

The bottom line

While falling prices might sound appealing at first glance, deflation presents serious economic challenges that can affect everyone from homeowners to business owners to workers. Understanding these dynamics helps explain why economists and policymakers go to such lengths to maintain a small but positive inflation rate.

Rather than hoping for prices to fall, most experts suggest that the healthiest economy is one with stable, low inflation, allowing for gradual price increases while avoiding the deflation trap that can be so difficult to escape.

Cashback is essentially getting paid to shop for things you'd buy anyway. Whether you're a seasoned rewards hunter or just curious about making your money work harder, this guide explores how savvy consumers are earning while spending, without changing their shopping habits. Ready to turn your everyday purchases into extra cash? Let's dive in.

What is cashback?

Cashback is a rewards program that gives you a percentage of your money back when you make purchases using eligible credit cards, debit cards, or shopping platforms. Think of it as a small rebate on what you spend, typically ranging from 1% to 5% of your purchase amount.

In recent years, cashback has increased in popularity across financial services and retail, becoming one of the most straightforward and appealing customer incentives (no guesses why).

Unlike complicated points systems or airline miles, cashback offers a simple proposition: spend money and get some of it back. Cashback transforms everyday spending into an opportunity to save, whether through your credit card statement, a bank transfer, or an app balance.

How does cashback work?

At its core, cashback operates on a simple principle: when you spend money, you earn a percentage back. This percentage - known as the cashback rate - determines how much you'll receive. For example, a 2% cashback rate means you'll get $2 back for every $100 you spend.

Here's what happens behind the scenes:

- You make a purchase with your cashback-enabled card or through a cashback platform.

- The transaction is processed and qualified against the program's terms.

- Cashback is calculated based on the purchase amount and applicable rate.

- The reward is credited to your account (either immediately or after a designated period).

Cashback rewards are typically issued as:

- Statement credits (reducing what you owe on your credit card)

- Direct deposits to your bank account

- Digital wallet credits within an app

- Gift cards or vouchers for specific retailers

Most cashback programs are funded through transaction fees that merchants pay to credit card companies (typically 2-3% of each purchase). The card issuer then shares a portion of these fees with you as cashback. For retailer programs and cashback apps, the incentive is funded through marketing budgets as they benefit from increased customer spending and loyalty.

Different types of cashback programs

Credit card cashback

Credit cards are a common way to earn cashback, generally structured in three main formats:

- Flat-rate cashback cards

These cards offer the same cashback rate on all purchases, regardless of category. For example, the Citi® Double Cash Card offers up to 2% on all purchases (1% when you buy, 1% when you pay). Note that rewards are earned as ThankYou® Points, which can be redeemed for cash back or other options.

- Tiered/category cashback cards

These offer higher cashback rates in specific categories and lower rates elsewhere. For instance, the Blue Cash Preferred® Card from American Express offers 6% back at U.S. supermarkets (up to $6,000 per year), 6% on select U.S. streaming services, 3% on transit and U.S. gas stations, and 1% on everything else.

- Rotating category cards

These cards offer higher cashback (often 5%) in categories that change each quarter, such as restaurants, gas stations, or online shopping.

For example, The Chase Freedom Flex℠ and Discover it® cash back programs require users to activate these categories each quarter, from where they can earn up to 5% cashback on purchases.

Debit card cashback

Differing from the credit card structure above, debit card cashback typically comes in two forms:

- Bank-offered cashback programs

Rewards for using your debit card for purchases. These are often tied to premium or business accounts and offer lower rates than credit cards (typically 0.5%-1%) since banks don't earn the same merchant fees that credit card companies do.

Examples include: Discover Cashback Debit offering 1% on up to $3,000 in monthly purchases; while some neobanks or fintechs offer promotional cashback for debit use, but these are often time-limited (Not at Tap).

- Cash back at checkout

This feature allows you to withdraw cash alongside your purchase at certain retailers (e.g., Walmart, Walgreens, or pharmacies), essentially getting "cash back" at the point of sale. This isn't a reward but a convenience service.

Retailer-specific programs

Many stores offer their own cashback programs:

- Store loyalty programs

These provide rebates on purchases, often tracked through a membership account. Examples include Target Circle, which offers 1% in rewards on qualifying purchases, or Kohl's Cash, which gives you $10 in store credit for every $50 spent during promotional periods.

- Receipt scanning programs

Apps like Ibotta and Checkout 51 offer cashback when users upload receipts or link loyalty cards. Offers vary by retailer and product.

Cashback websites and apps

These third-party platforms connect shoppers with retailers and share the commission they receive:

- Cashback websites

Websites like Rakuten, TopCashback, and BeFrugal offer rebates when you shop at partner retailers through their portal. These sites earn commissions from retailers for referring customers and share a portion with you.

- Browser extensions

Honey (owned by PayPal) and Capital One Shopping apply coupons and may offer cashback (called “Honey Gold” or Capital One Shopping Credits), though amounts and eligibility vary.

However, these platforms often come with caveats:

- Cashback typically pays out quarterly rather than immediately

- Minimum payout thresholds may apply (often $5-$25)

- Some offers are region-specific or limited-time

How much cashback can you earn?

Cashback earnings vary widely across programs:

Typical credit card rates range from 1% to 2% as a baseline, with category bonuses reaching 3% to 6%. Premium cards may offer higher rates but often carry annual fees.

Sign-up bonuses can significantly boost initial earnings, sometimes offering $150-$300 back after spending a certain amount in the first few months.

Cashback apps and websites typically offer higher percentages (often 2%-10%) but on a more limited selection of retailers.

Most programs include some limitations:

- Spending caps that limit cashback on certain categories (e.g., 6% on groceries up to $6,000 yearly)

- Minimum spend requirements before cashback activates

- Redemption thresholds requiring you to accumulate a minimum amount (often $20-$25) before cashing out

- Quarterly or annual payment schedules rather than immediate rewards

How much cashback can you earn with Tap?

Looking for a cashback program that gives you Cashback rewards on your your spendings and not just at specific brands or places? Tap makes it easy. By using your Tap card, you earn Cashback rewards on your spending, from groceries to fuel and even holidays.

How much can you earn? With Tap’s flexible premium tiers, cashback rewards are tailored to fit your lifestyle: earn from 0.5% up to 8% on every eligible purchase made with your Tap card. The more you spend, the more you earn—simple as that.

Pros and cons of cashback programs

Pros

- Simplicity: Cash rewards are straightforward to understand and use

- Flexibility: Unlike points or miles, cash can be used for anything

- Automatic earnings: Most programs require minimal effort beyond using the right card

- No devaluation: Unlike travel points, a dollar of cashback remains a dollar

- Immediate value: No need to save up for specific redemptions

Cons

- Potential for overspending: The promise of cashback can encourage unnecessary purchases

- Hidden costs: Cards with generous cashback may have higher annual fees or interest rates

- Category restrictions: Many programs limit higher cashback to specific merchant types

- Reward caps: Many programs limit how much you can earn in bonus categories

- Redemption delays: Some programs only pay out quarterly or when you reach certain thresholds

Is Cashback really free money?

Cashback isn't exactly "free", it's better understood as a discount on your spending. The funding comes from several sources:

Debit and Credit card cashback is funded by interchange fees paid by merchants (typically 1.5%-3.5% of each transaction). Card issuers share a portion of these fees with cardholders to encourage more spending.

Retail cashback programs are essentially marketing expenses designed to drive sales and customer loyalty.

Cashback apps and websites earn affiliate commissions from retailers and share a portion with users.

The most important caveat: cashback on credit cards only makes financial sense if you pay your balance in full each month. If you carry a balance, the interest charges (often 15%-25% APR) will quickly exceed any cashback earned.

How to choose the right cashback option

Finding the best cashback program depends on your spending patterns and preferences:

Analyse your spending habits: Review your monthly expenses to identify where you spend the most. If groceries and gas dominate your budget, a card with bonus rewards in those categories makes sense. If your spending is diverse, a flat-rate card might be better.

Consider fees vs rewards: Some cards with higher cashback rates charge annual fees. Calculate whether your typical spending will earn enough extra cashback to offset any fees.

Evaluate redemption options: Consider how and when you can access your cashback. Some programs offer automatic redemption, while others require manual redemption or have minimum thresholds.

For businesses: Business-specific cashback cards often offer higher rewards on categories like office supplies, internet services, and travel. If you're a business owner, these specialised options may provide better value than consumer cards.

Tips to maximise cashback

Strategically use multiple cards: You can use different cards for different categories based on which offers the highest rate for each spending type.

Stack rewards programs: Combine a cashback credit card with a cashback app or website for double dipping. For example, make a purchase through Rakuten using a cashback credit card.

Activate bonus categories: Many cards require quarterly activation of rotating bonus categories - set calendar reminders so you don't miss out.

Pay bills with cashback cards: Set up utilities, subscriptions, and other regular payments on your best cashback card (if there's no processing fee).

Watch for promotional offers: Many programs offer limited-time enhanced cashback rates or bonus categories.

Avoid carrying balances: Always pay your credit card bill in full to avoid interest charges that negate cashback benefits.

In conclusion

Cashback rewards offer a practical way to earn while you spend on everyday purchases. Unlike complicated reward systems, cashback provides straightforward value that anyone can understand and use.

Choose cards and apps that reward your existing spending patterns rather than changing your habits to chase rewards. Also, try maximising cashback benefits by matching the right programs to your spending habits and being disciplined about your purchasing behaviour.

Remember: the best cashback strategy is one that fits naturally into your financial life, providing rewards without encouraging overspending or complicating your finances.

Tired of complicated cashback programs tied to specific brands? Discover our simple Cashback program that rewards you when you spend with your Tap card, learn more here.

.webp)

Hey Tap community

If you’ve been wondering why things have seemed a little quiet lately, it’s because we’ve been hard at work behind the scenes, and today, We are excited to finally share the full story and what’s coming next.

Laying the groundwork for the next wave of features

Over the past five years, Tap’s fast-paced, lean approach helped us grow quickly. But growth brought challenges.

Our infrastructure, built for a much smaller platform, was starting to hold us back, especially during big launches or promotions. It wasn’t scaling the way you, our community, deserved.

Rather than continue patching and stretching it, we made the bold decision to rebuild Tap’s core systems from the ground up, upgrading to a modern, flexible architecture built for real growth.

It wasn’t easy. It meant months of intense work, rewriting large parts of our platform. That’s why new features slowed down, because we were laying a much stronger foundation for the future.

Now, we're Ready to start the rollout

After months of development and testing, we’re kicking off Phase 1 of the migration to our new infrastructure.

📅 Maintenance Window

- Starts: Wednesday, May 7, 2025 at 21:30 UTC

- Ends: Thursday, May 8, 2025 at 07:30 UTC

- Impact: Tap services will be temporarily unavailable for about 10 hours

This maintenance allows us to move our internal Tap team to the new system, a critical step before we start migrating you, our users.

We've scheduled it overnight to minimise disruption, and our team will be working around the clock to ensure everything runs smoothly.

What happens after this?

Once internal testing is complete, we'll begin carefully moving users over in phases:

- Phase 2: Migrate select groups of users, monitor closely, fine-tune.

- Phase 3: Roll out to all users, officially retiring the old system.

Each phase brings us closer to a faster, more reliable Tap, one that’s ready to scale with our growing community and deliver new features faster than ever.

The future starts now

This upgrade unlocks a future where downtime, failed sign-ups, and app slowdowns are things of the past. Thank you for sticking with us through this transition.

Your patience means everything. We can't wait to show you what’s coming next. The quiet period is ending, and Tap’s next chapter is just beginning.

Stay tuned,

The Tap Team.

Near Protocol represents a new generation of blockchain platforms focused on usability and scalability. Launched in 2020, it offers a faster, more efficient alternative to earlier blockchain networks while maintaining robust security.

After several years of implementation, Near Protocol has established itself as a notable player in the layer-1 blockchain space.

TLDR

Scalable & developer-friendly: Near Protocol is a decentralised, layer-1 blockchain designed for high scalability and user-friendly dapp development.

Sharding & low fees: It uses a unique sharded Proof-of-Stake mechanism (Nightshade) to process transactions efficiently while keeping costs low.

Cross-chain interoperability: The Rainbow Bridge enables seamless asset transfers between Near and Ethereum, enhancing blockchain connectivity.

Native token (NEAR): NEAR powers the ecosystem, used for transactions, staking, and governance, with a total supply cap of 1.23 billion tokens.

What is Near Protocol (NEAR)?

Near Protocol is a decentralised blockchain platform designed to be user-friendly and highly scalable. The platform supports the development of dapps (decentralised applications) with a particular focus on usability for both developers and end users.

The platform utilises a Delegated Proof-of-Stake (DPoS) consensus mechanism called "Nightshade," which implements a technique known as sharding to significantly improve transaction throughput. This approach allows Near to process thousands of transactions per second while maintaining low transaction costs and reducing the environmental impact compared to Proof-of-Work blockchains.

A distinctive feature of Near Protocol is its human-readable account names, eliminating the need for users to interact with long, complex wallet addresses. The platform also incorporates a developer-friendly environment with WebAssembly (WASM) support and tools that make building dapps more accessible.

The platform has gained significant attention for its cross-chain interoperability solutions, particularly through the Rainbow Bridge, which enables asset transfers between Near and Ethereum. The platform has attracted numerous projects across DeFi, NFTs, gaming, and social applications.

Who Created Near Protocol?

Near Protocol was founded by Erik Trautman, an entrepreneur whose background includes experience on Wall Street and founding Viking Education.

Trautman partnered with two technical co-founders: Illia Polosukhin, a seasoned software developer with over a decade of industry experience including a three-year tenure at Google, and Alexander Skidanov, a computer scientist whose career path led from Microsoft to memSQL, where he rose to become Director of Engineering.

This founding team combined financial market knowledge, machine learning expertise, and distributed systems experience to address the scalability challenges facing blockchain technology.

The project was conceptualised in 2018 when the founders recognised the scalability limitations of existing blockchain networks. They set out to build a platform that could deliver the performance needed for mainstream adoption while maintaining security and decentralisation.

The Near team has expanded to include numerous contributors from around the world, with the protocol's development being overseen by the Swiss-based Near Foundation, which provides governance and supports ecosystem growth.

How Does Near Protocol Work?

Consensus Mechanism and Architecture

Near Protocol operates on a sharded architecture called Nightshade, which divides the network into multiple segments (shards) that process transactions in parallel. This design allows the network to scale horizontally as demand increases and enhances transaction throughput.

This design allows the network to process a high number of transactions per second while maintaining low fees and reducing environmental impact.

Additionally, Near utilises a mechanism called "Doomslug" for block finalisation, achieving near-instant transaction finality. This means that once transactions are confirmed, they are immediately considered final, unlike some other blockchains that require multiple confirmations.

Near achieves consensus through its unique sharded Proof-of-Stake mechanism, where token holders can stake their NEAR or delegate it to validators who help secure the network.

Smart Contract Support

The platform supports smart contracts written in Rust and JavaScript, compiled to WebAssembly (WASM) through the AssemblyScript framework. This flexibility enables developers to build complex applications with familiar programming languages.

User-Friendly Features

Near's account model features human-readable account names, simplifying interactions by eliminating the need for complex wallet addresses. The platform also offers account abstraction, allowing for recoverable accounts, multi-signature control, and the ability for users to cover transaction fees on behalf of others, facilitating gasless transactions.

Cross-Chain Interoperability

Near has developed the Rainbow Bridge, enabling seamless asset transfers between Near and Ethereum. This cross-chain interoperability expands the utility of assets and enhances the interconnectedness of the blockchain ecosystem.

What Is NEAR?

NEAR is the native token of the Near Protocol ecosystem. It serves multiple purposes within the network, including:

- Paying for transaction fees and storage on the blockchain

- Staking to participate in network security and earn rewards

- Voting in governance decisions to determine the future direction of the protocol

The token follows an inflationary model with a maximum supply cap of 1.23 billion tokens, of which approximately 1.18 billion are already in circulation at the time of writing.

How can I buy and sell NEAR?

If you're interested in exploring NEAR, you can do so easily through the Tap app. The app supports buying, selling, trading, and storing NEAR tokens, allowing users to manage NEAR alongside other digital assets.

In today's digital-first economy, businesses across all sectors are seeking innovative financial solutions to drive efficiency, enhance customer experiences, and unlock new revenue streams. One compelling strategy is the implementation of co-branded credit cards, which have been shown to significantly boost customer loyalty and spending.

Notably, 75% of financially stable consumers prefer co-branded cards for their rewards and benefits, indicating a strong alignment between these card programs and consumer desires.

By collaborating with financial institutions to offer co-branded cards, businesses can create tailored payment solutions that meet customer expectations and reinforce brand loyalty. This approach transforms the payment infrastructure from a mere operational necessity into a strategic asset that fuels growth.

For instance, the co-branded credit card market is projected to grow from $13.41 billion in 2023 to $25.72 billion by 2030, reflecting a compound annual growth rate (CAGR) of 9.74%.

Whether you're in retail, SaaS, or manufacturing, a tailored card program could be the key to transforming how your business engages with customers—and how you scale.

What is card program management?

Card program management encompasses the end-to-end process of designing, implementing, and optimising payment card solutions tailored to your business. From corporate expense cards that streamline internal processes to branded payment cards that enhance customer loyalty, these programs offer versatility that can benefit virtually any organisation looking to modernise its financial operations.

As businesses continue to navigate increasingly complex markets, those equipped with flexible financial tools gain a significant competitive advantage. The right card program doesn't just process payments—it generates valuable data, reduces administrative burden, and creates opportunities for deeper engagement with both employees and customers.

Why it matters

At its core, card program management involves overseeing all aspects of a payment card ecosystem—from issuing and distribution to transaction processing, reporting, and compliance. Modern card program management platforms provide businesses with the infrastructure to create customised payment solutions while maintaining visibility and control.

This matters because traditional payment methods often create friction points that slow business growth. Manual expense reporting, limited payment visibility, and rigid financial systems can drain resources and limit innovation.

However, a well-managed card program addresses these pain points by automating processes, enhancing security, and providing greater flexibility.

Key benefits for businesses across sectors

Streamlined operations

Card programs dramatically reduce administrative overhead by automating expense tracking, simplifying reconciliation, and eliminating paper-based processes. This operational efficiency translates directly to cost savings and allows your team to focus on strategic initiatives rather than transaction management.

Enhanced Customer Experience

For businesses that implement customer-facing card programs, the benefits extend to experience enhancement. Branded payment cards can strengthen loyalty, while instant issuance capabilities meet modern expectations for immediacy.

From hospitality to healthcare, organisations are using card programs to differentiate their service offerings.

Data-driven insights

Perhaps the most overlooked advantage of modern card program management is the wealth of data it generates. Every transaction becomes a data point that can inform business decisions, reveal spending patterns, and identify opportunities for optimisation. This business intelligence becomes increasingly valuable as programs scale.

Scalability and flexibility

As your business grows, your card program can evolve alongside it. Whether you're expanding into new markets or adding new product lines, a well-designed card program adapts to changing requirements without requiring complete system overhauls.

The implementation process simplified

Implementing a card program doesn't have to be overwhelming. The process typically follows these key steps:

- Assessment and strategy development: Evaluate your current payment ecosystem and define clear objectives for your card program.

- Platform selection and integration: Choose a card program management solution that aligns with your technical requirements and business goals, then integrate it with your existing systems.

- Program launch and optimisation: Deploy your program with proper training and support, then continuously refine based on performance data and user feedback.

Real-World Impact

Across industries, businesses are leveraging card program management to solve specific challenges:

- Retail companies are implementing instant digital card issuance to capture sales opportunities.

- Healthcare providers are using specialised payment cards to simplify patient financial assistance.

- Manufacturing firms are deploying corporate card programs with custom spending controls to streamline procurement.

The common thread? Each organisation is using card program management as a strategic tool rather than just a payment method.

How Tap can help

Navigating the complexities of card program management requires expertise and the right technology partner. Tap's comprehensive platform brings together cutting-edge technology with industry-specific knowledge to help businesses design, implement, and optimise card programs that deliver measurable results.

Our solution addresses common challenges like regulatory compliance, security concerns, and integration complexities, allowing you to focus on the strategic benefits rather than implementation hurdles.

Ready to explore how card program management could transform your business operations and drive growth? Connect with Tap's team of specialists for a personalised consultation and discover the potential of a tailored card program for your organisation.

Article Framework: Card Program Management

Tone & Perspective

- Tone: Professional, informative, and authoritative.

- Perspective: Written from an expert viewpoint, educating businesses on launching and managing a successful card program.

Priority Headings & Structure

1. Introduction

- What is card program management?

- Why businesses need effective card program management.

- Overview of key stakeholders (issuers, networks, processors, etc.).

2. How Card Program Management Works

- Key components: issuing, processing, compliance, and risk management.

- The role of a program manager (self-managed vs. outsourced).

- The relationship between issuing banks, networks, and program managers.

3. Core Elements of a Successful Card Program

- Program Design: Choosing card types (prepaid, debit, credit), network selection (Visa, Mastercard), and branding.

- Issuance & Account Management: BIN sponsorship, account setup, and customer onboarding.

- Compliance & Risk Management: KYC, AML, PCI DSS, and fraud prevention strategies.

- Transaction Processing & Settlement: How funds flow through the ecosystem.

- Customer Experience & Support: Ensuring smooth cardholder interactions.

4. Self-Managed vs. Partner-Managed Card Programs

- Benefits and challenges of managing in-house.

- When outsourcing makes sense.

- How third-party program managers add value.

5. Key Considerations Before Launching a Card Program

- Business goals and revenue model.

- Regulatory and security requirements.

- Time-to-market considerations.

6. Trends & Future of Card Program Management

- Embedded finance & BaaS (Banking-as-a-Service).

- AI-driven fraud detection and risk management.

- Open banking and API-driven solutions.

7. Conclusion & Next Steps

- Recap of key insights.

- How businesses can get started with a card program.

- Contact a program management expert.