After a volatile October, crypto faces a defining moment. Discover what's fueling both the bullish and bearish cases right now.

Keep reading

After a volatile October that saw one of the sharpest two-day liquidations of the year, the crypto market is trying to regain its footing, but conviction remains divided. Bitcoin has stabilized near key support levels, while altcoins fight against selling pressure. With macro, policy, and on-chain factors all in play, the debate between the bull and bear camps is as alive as ever. Let’s unpack the forces shaping both sides of the ledger.

The Bear Case

When Good News Don’t Move Prices

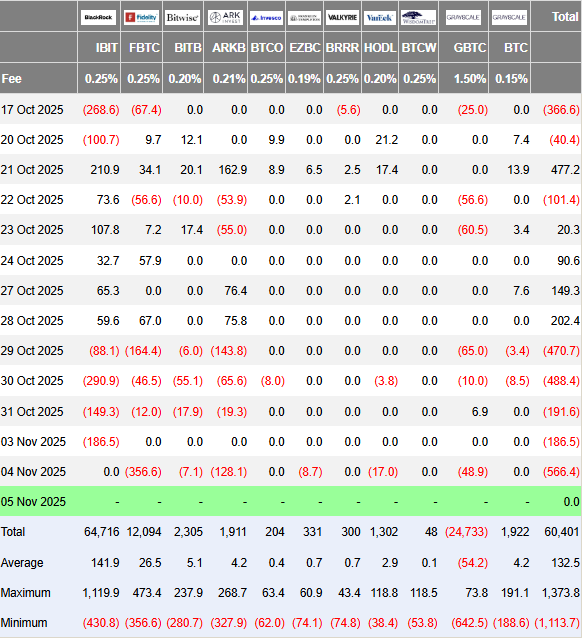

Despite encouraging ETF data and easing rate expectations, crypto failed to rally in late October, a classic warning sign of risk fatigue. According to Farside Investors, U.S. spot Bitcoin ETFs saw outflows of $470 million, $488 million, and $191 million between October 29 and 31, signaling that short-term traders were taking profits or stepping aside after “Uptober” fizzled out.

The AI Narrative

Macro sentiment still casts a long shadow. The tech-heavy equity rally, driven by AI infrastructure and chip stocks, has stirred debate about overvaluation. Nvidia’s brief breach of a $5 trillion valuation in late October triggered flashbacks of the dot-com era. If AI equities begin to deflate, crypto could feel the wealth effect unwind, as liquidity shifts from speculative assets to safer havens.

The 10/10 Crash Aftershock

The October 10 downturn marked one of the largest single-day liquidations in recent memory. Analysts note that this event left traders hunting for “dead entities” and potential hidden losses, injecting caution across the market. Even with recovery underway, scars from that drop remain fresh.

Post-Halving Cycle Timing

Bitcoin’s halving on April 20, 2024 (block 840,000) reset expectations, but it also reignited the age-old question: where are we in the cycle? Historically, the strongest rallies have occurred before or shortly after the halving, not a full year later. Some analysts now argue that the current consolidation could represent a late-cycle phase rather than the start of a new one.

Dormant Wallets Awakening

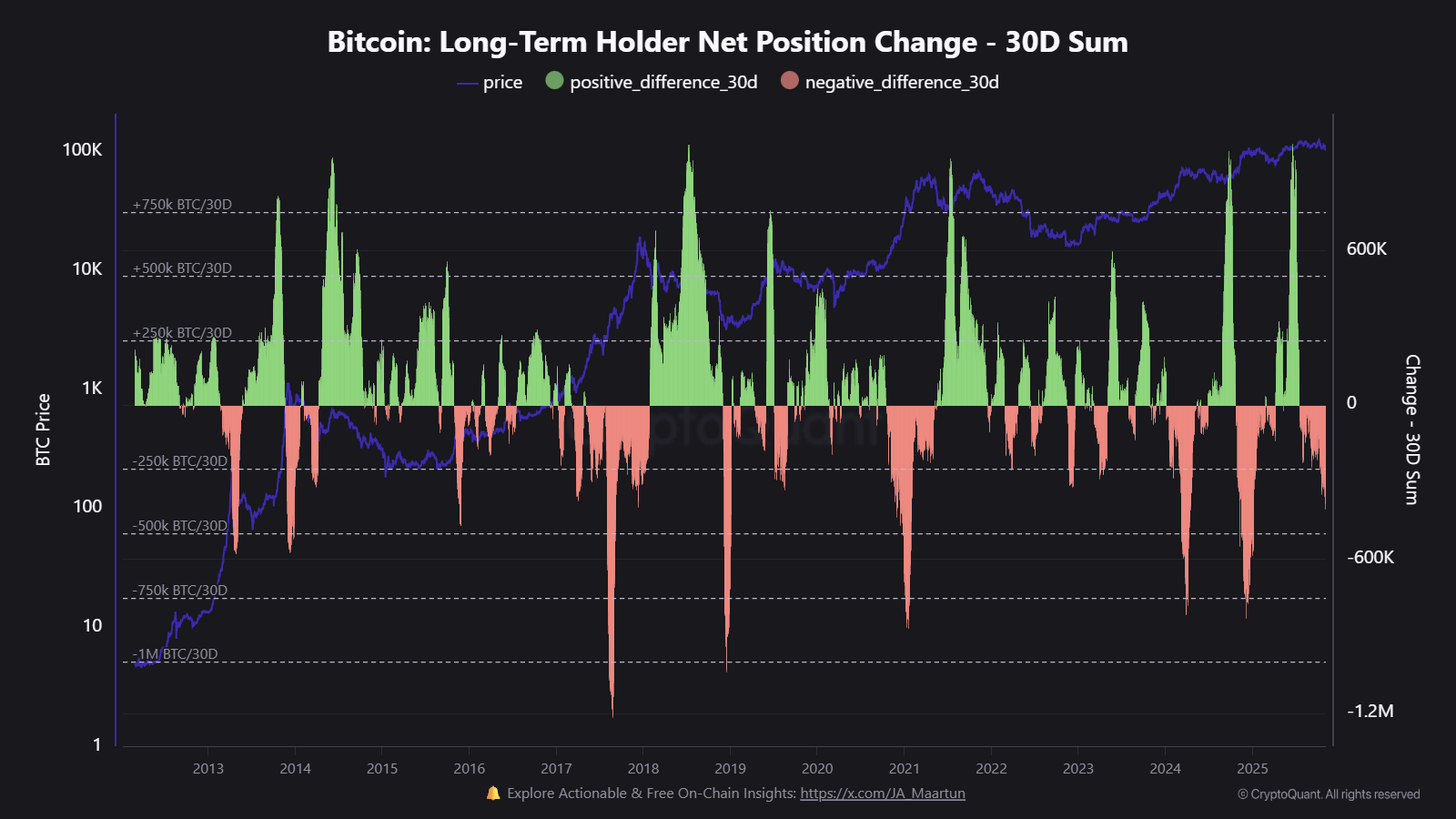

On-chain data from CryptoQuant shows that long-term holders have increased net distribution since mid-October, with tens of thousands of BTC re-entering circulation. Several Satoshi-era wallets have also moved funds, not necessarily bearish in isolation, but enough to add pressure and short-term supply.

The Bull Case

No Signs of Euphoria

Market positioning remains far from overheated. The Crypto Fear & Greed Index currently sits in the 20s, and has been recently hovering between “Fear” and “Neutral.” That’s a far cry from the exuberant 80s to 90s readings that often precede blow-off tops. In practical terms, this suggests there’s still room for sentiment to improve before the market becomes dangerously crowded.

Liquidity Is Turning

Central banks are easing. The European Central Bank has already paused, the Bank of England has begun cutting, and the U.S. Federal Reserve is expected to follow suit with at least one more rate cut by year-end. According to the CME FedWatch Tool, the odds of a 0.25% cut currently stand above 70%. Historically, easing cycles have correlated strongly with renewed crypto uptrends, as lower yields push investors back into risk assets.

Institutional Adoption Keeps Compounding

Spot ETFs remain the biggest driver of credibility and inflows this year. Despite short-term outflows, global crypto investment products reached $921 million as recently as last week. That steady institutional presence gives crypto markets deeper liquidity and a stronger foundation than in previous cycles, where retail speculation dominated.

The Seasonal Edge

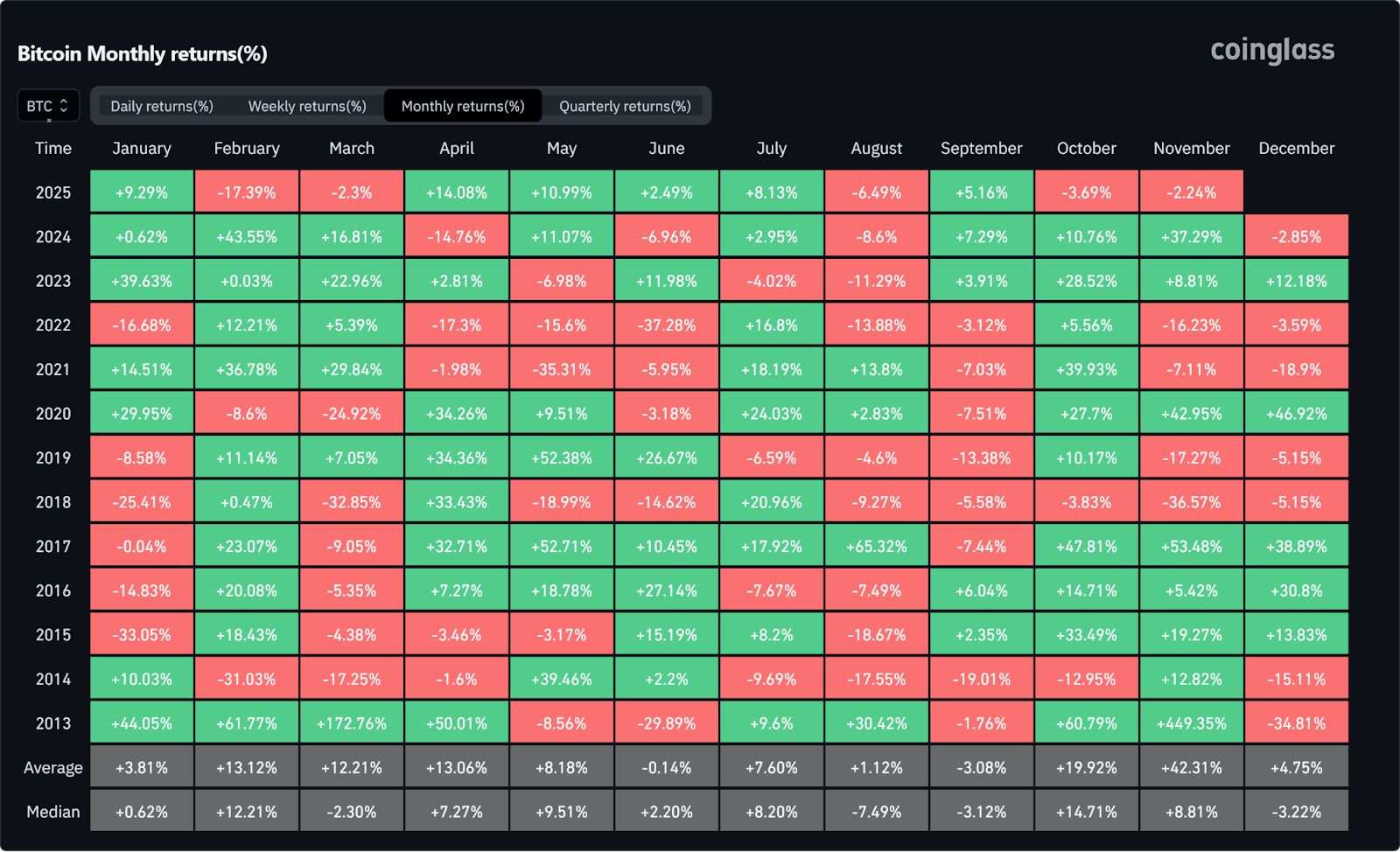

Seasonality adds another bullish data point. Since 2013, Q4 has consistently been Bitcoin’s strongest quarter on average. With November historically delivering above-average performance, many traders see the current consolidation not as a ceiling, but as a potential setup, particularly if macro data softens and ETF inflows resume.

Improving Global Sentiment

Finally, the U.S.–China trade thaw is a quiet but important catalyst. China has agreed to pause 24% tariffs on U.S. goods, marking the most significant de-escalation yet. For global risk assets, that’s a relief valve, potentially restoring confidence in emerging markets and crypto alike.

Final Verdict

Crypto’s tug-of-war between optimism and caution is far from over. The bull camp points to liquidity, policy progress, and institutional growth as evidence of a maturing ecosystem. The bears, on the other hand, warn that cycle timing, macro fragility, and old-wallet selling could cap any short-term rally.

Currently, the most realistic view lies somewhere in between these two extremes. After October's flash crash sent shockwaves through the market, a period of recalibration has taken hold. Whenever the next significant high arrives, the current environment may be best described not as peak fear or euphoria, but as consolidation.

NEWS AND UPDATES

LATEST ARTICLE

We are delighted to announce the listing and support of Synthetix (SNX) on Tap!

SNX is now available for trading on the Tap mobile app. You can now Buy, Sell, Trade or hold SNX for any of the other asset supported on the platform without any pair boundaries. Tap is pair agnostic, meaning you can trade any asset for any other asset without having to worries if a "trading pair" is available.

We believe supporting SNX will provide value to our users. We are looking forward to continue supporting new crypto projects with the aim of providing access to financial power and freedom for all.

Synthetix is a groundbreaking decentralized asset protection protocol that permits users to mint, hold, and trade derivatives across different asset classes such as commodities, fiat currencies, stocks, and even cryptocurrencies like Bitcoin.

Synthetix provides a decentralized, permissionless, and censorship-resistant platform that allows users to gain exposure to both crypto and non-crypto assets without the need for ownership of these assets. This enables anyone with an interest in DeFi to join the industry through the use of synthetix assets regardless of whether they hold the actual assets or not.

Get to know more about Syntheticx (SNX) in our dedicated article here.

You’ve probably heard whispers about the "whales" swimming in the crypto seas. But these aren’t your typical marine mammals. They’re the ultra-wealthy folks and organizations holding massive amounts of digital currency.

What Exactly is a Crypto Whale?

So, what makes someone a crypto whale? There’s no hard-and-fast rule, but it generally comes down to owning a huge chunk of a coin’s total supply. If we’re talking over 10% of the available coins for a particular cryptocurrency, then that’s an ocean-sized wallet!

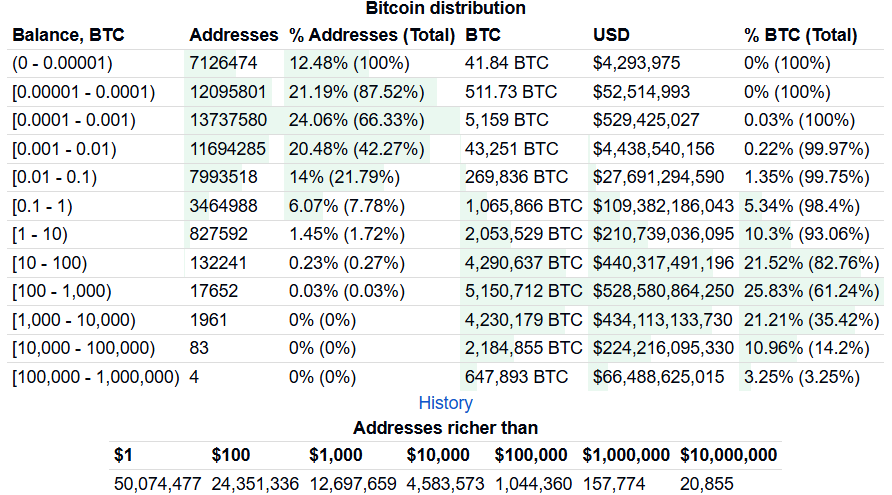

Take Bitcoin, for example. In October 2025, the wealthiest addresses controlled over 14% of all Bitcoin in existence. From Satoshi Nakamoto himself to MicroStrategy. Now that’s some serious whale power!

Bitcoin isn’t the only one with its share of whales. Dogecoin, the beloved meme coin, had a pretty wild concentration too. In 2025, just 3 addresses held over 32% of its total supply. Even Vitalik Buterin, the mastermind behind Ethereum, is considered an Ether whale thanks to his massive stake in the coin he created.

How Much Money Makes You a Crypto Whale?

The exact percentage threshold varies by cryptocurrency, but Bitcoin probably offers the clearest benchmark. Analysts typically define a Bitcoin whale as anyone holding over 1,000 BTC, worth around $100 million USD at recent 2025 market prices.

What About Other Assets?

- Whales usually hold 10,000 ETH or more.

- Generally, 500,000 SOL or more.

These thresholds aren’t clear-cut, and they shift as market value, liquidity, and overall supply and demand evolve. In simple terms, whales are the elite of the cryptocurrency market, capable of moving markets with a single transaction.

How Whales Make Waves

With that kind of buying power, whales can really make waves in the crypto marketplace. If a whale decides to sell off a giant chunk of their holdings, it creates a tidal wave of downward pressure on prices due to the sheer volume and lack of liquidity. Other crypto enthusiasts are always on the lookout for signs of an impending "whale dump," closely monitoring exchange inflows to spot potential dangers.

Here’s the twist, though – whales keeping their coins locked away actually reduces trading liquidity in the market since there are fewer coins actively circulating. Their massive idle fortunes are like icebergs weighing down the crypto ocean.

Tracking Whale Movements

Not every whale transaction is a sell-off. These giants could simply be migrating to new wallets, switching exchanges, or making monster-sized purchases. But you can bet experienced crypto folks keep a keen eye on those huge whale wallets, carefully tracking any ripples they make to navigate the ever-shifting tides of the market.

Whale Alert is a popular service that tracks these large transactions and reports them, often on Twitter. Whenever a whale makes a big move, it’s usually publicized quickly, giving everyone a heads-up on potential market changes.

Below is an example from Twitter from Whale Alert:

The Human Side of Whales

Behind these massive holdings are real people and organizations. Some whales are early adopters who bought into Bitcoin or other cryptocurrencies when they were cheap. Others are companies that have invested heavily in the belief that cryptocurrencies will continue to grow in value. For instance, Ethereum’s founder, Vitalik Buterin, is the biggest Ethereum whale because he holds a significant amount of the cryptocurrency he created.

How Whales Affect Crypto's Price

Price volatility can be increased by whales, particularly when they move a significant amount of one cryptocurrency in one go. For example, when an owner tries to sell their BTC for fiat currency, the lack of liquidity and enormous transaction size create downward pressure on Bitcoin's price. When whales sell, other investors become extremely vigilant, looking for hints of whether the whale is "dumping" their crypto (and whether they should do the same).

The exchange inflow mean, also known as the average amount of a certain cryptocurrency deposited into exchanges, is one of the most common indicators crypto investors look for. If the mean transaction volume rises above 2.0, it implies that whales are likely to start dumping if there are a large number of them using the exchange. This can be viewed by regular crypto traders as a time to act before losing any potential profit.

How Whales Affect Liquidity

When it comes to learning about whales and liquidity, one must remember that while whales are generally considered neutral elements in the industry, when a large number of whales hold a particular cryptocurrency, instead of using it, this reduces the liquidity in the market due to there being fewer coins available.

What Crypto Whales Mean to Investors

In terms of the relationship between whales and investors, one must remember that there are various situations in which a person may transfer their cryptocurrency holdings. It's worth mentioning that moving one's assets doesn't always indicate that you're selling them; they might be switching wallets or exchanges, or making a major purchase.

Occasionally, whales may sell portions of their holdings in discrete transactions over a longer period to avoid drawing attention to themselves or generating market anomalies that send the price up or down unpredictably. This is why investors keep an eye on known whale addresses to check for the number of transactions and value. This is not necessarily a task that newbie investors need to actively be involved with, however, understanding the terms and how whale accounts can affect the market is recommended.

Why Whales Matter

Whether you love them or hate them, whales are a formidable force in the crypto world, shaping its dynamics in profound ways. These giants, whether they’re creators, collectors, or traders, have a tremendous impact across the digital waters. When they make a move, it can trigger monumental swells that ripple through the entire market.

By understanding whale activity, anyone involved in cryptocurrency can better navigate these choppy waters. Staying informed about whale movements helps both newbies and seasoned traders make smarter decisions and stay afloat in this ever-changing space. Keep an eye on these behemoths; their actions can significantly influence your crypto journey.

While tracking whale activity can offer valuable insights into the cryptocurrency market, it's important to complement this knowledge with expert advice. Consulting with a financial advisor can help you navigate the complexities of investing and ensure your strategies align with your personal financial goals and risk tolerance.

We are delighted to announce the listing and support of BitDao (BIT) on Tap !

BIT is now available for trading on the Tap mobile app. You can now Buy, Sell, Trade or hold BIT for any of the other asset supported on the platform without any pair boundaries. Tap is pair agnostic, meaning you can trade any asset for any other asset without having to worries if a "trading pair" is available.

We believe supporting BIT will provide value to our users. We are looking forward to continue supporting new crypto projects with the aim of providing access to financial power and freedom for all.

BitDAO is building a decentralized token economy open to everybody. Managed by BIT token holders and one of the largest decentralized autonomous organizations (DAOs), BitDAO is committed to growing the DeFi ecosystem through partner projects and a decentralized economy.

BitDAO is governed and administered by the holders of BIT tokens. It works on the DAO mechanism, a common governance structure within the crypto space. The DAO framework gives BIT token holders power over BitDAO decisions and actions through a system of voting on proposals.

Get to know more about BitDao (BIT) in our dedicated article here.

.png)

BitDAO is building a decentralized token economy open to everybody. Managed by BIT token holders and one of the largest decentralized autonomous organizations (DAOs), BitDAO is committed to growing the DeFi ecosystem through partner projects and a decentralized economy.

What Is BitDAO?

BitDAO aims to create an accessible tokenized economy that provides support, such as research and development, liquidity bootstrapping and funding, to a wide range of partner projects across the DeFi, DAO, NFT and gaming space. Through co-development offers and token swaps, BitDAO aims to attract developer talent and build a sustainable treasury of top crypto coins.

BitDAO's ultimate goal is to create products that will not only improve BitDAO's efficiency and effectiveness, but also other DAOs. The core product comprises a series of both on-chain and off-chain governance solutions and products; with the latter, DAO treasury management would be able to deploy and monitor assets in order to earn yield.

Moreover, BitDAO plans on providing grants to different teams within the crypto industry for research or development purposes, all of which are voted on by members and given for the public good of cryptocurrency communities worldwide.

Through its DAO structure, the company does not rely on a traditional hierarchy to operate, instead, it is run by a group of token holders that contribute to the platform's development. Token holders are then rewarded in BIT tokens for participating.

Changes to the BitDAO protocol are proposed to the BIT token holders who then have the power to vote on whether these changes are implemented or rejected. While the platform's vision has been outlined, where it ends up will be decided on by governance suggestions and forum participation.

To sum it up, the people who hold BitDAO's tokens, investors, and members of its community will help shape BitDAO's vision which includes dedicating both financial and human resources to support DeFi's development.

What is the BitDAO Treasury?

Controlled by BIT token holders, the BitDAO Treasury is responsible for allocating funds as per decisions made by BIT token holders. The BitDAO Treasury also undertakes token swaps with emerging and existing projects with the intention to support them and incentivize the project's contribution to their success.

The BitDAO Treasury allocation was 30% of the projects initial 10 billion BIT total supply. Monthly contributions from Bybit and varying contributions from DeFi partners, determined by smart contracts, also contribute to the DAO treasury management solutions.

Who created the BitDAO platform?

In a unique move, the BitDAO platform has no founders. While being supported by big names such as Bybit, Peter Thiel, Pantera, Founders Fund and more, the project is entirely run by contributors holding BIT tokens. Bybit is recorded as being an early contributor and is believed to have contributed over $1 billion in funding to the initiative.

Taking the notion of decentralization to a new level, the project has no teams, leaders or companies behind its operations. All changes are proposed by individuals within the community and then voted on by BIT token holders.

How do the BitDAO core protocols work?

BitDAO is governed and administered by the holders of BIT tokens. It works on the DAO mechanism, a common governance structure within the crypto space. The DAO framework gives BIT token holders power over BitDAO decisions and actions through a system of voting on proposals.

The platform supports the following measures, which will only be executed if the proposal receives a positive vote through the DAO system.

- Financing or milestone development grants for development teams and R&D centers who create BitDAO solutions or assist partnered existing and emerging projects.

- Upgrades to BitDAO's fundamental protocols, notably governance and treasury management.

- Token swaps for current and new initiatives.

- The Treasury will deploy funds based on various tactics.

- Grants will be made available for blockchain technology projects, educational programs, as well as other services related to blockchain.

- Support in the way of cash flow through existing assets will be provided to partner initiatives.

There are three ways to get involved with BitDAO: contributing to the project, becoming a partner, or holding the tokens. Contributors and partners can be any DeFi or CeFi project looking to build the BitDAO ecosystem while token holders are considered to "own" the platform as they have the power to recommend and vote on BitDAO's growth strategies as well as the allocation of BitDAO's treasury resources.

Non-token holders are defined as community members and can have their say through the forum and social media channels. Here they can pitch their ideas, which BIT token holders can then choose to embrace.

What is the BIT token?

The BIT token is the native token of the BitDAO ecosystem. The governance token allows for off-chain vote aggregation and delegated voting and provides the opportunity for switching to on-chain governance in the future. The BIT token can best be compared to the COMP token in the Compound Finance ecosystem.

There is a maximum supply of 10,000,000,000 BIT tokens, with the BitDAO Treasury allocation accounting for 30% of these. Token holders technically possess these treasury tokens based on their share of BIT. I.e. if someone holds 10% of the total BIT supply, they have ownership of 10% of the Treasury's 30% supply, equating to an additional 1%.

How BIT token holders can leverage Tap

You can now easily incorporate BitDAO (BIT) into your crypto portfolio by using the Tap app. The Tap app has recently added BIT to the list of supported crypto tokens, allowing anyone to conveniently and securely access the BitDAO market and safely store their BIT tokens.

Users can buy BitDAO (BIT) with fiat currency or engage in token swaps with other supported cryptocurrencies on the platform, or they can use traditional payment methods like bank transfers. The integrated wallets on the platform also make it easy for users to store and manage their BIT cryptocurrency.

Getting paid in cryptocurrencies has opened the global gig economy to endless opportunities. Gone are the days of needing to be in the same country, or even on the same continent, as your employer. Cryptocurrency jobs are not only more accessible but also more acceptable.

In this article, we’re breaking down where you can find jobs that specifically pay in cryptocurrencies. Before we do though, let’s touch base on the advantages the new digital currency realm is offering.

The Advantages Of Being Paid With Blockchain Technology

The ever-evolving blockchain industry is now integrating cryptocurrencies into traditional job markets, from temporary gigs to full-time jobs, anyone can now get paid in crypto.

The decentralized world of cryptocurrencies provides many demographics with many advantages. For employees, these advantages allow the job market to be blown wide open as international payments are now easily accessible and don’t come with high transaction costs and delays.

Due to the nature of crypto transactions, payments can be executed in a matter of minutes with minimal transaction fees offering a quick and cost-effective solution to moving money across borders. The minimal transaction fees also allow freelancers to take on many smaller projects, an opportunity otherwise impossible with international fiat transactions.

Arguably the biggest advantage to cryptocurrency jobs is that anyone anywhere can now work for anyone anywhere, as borders are no longer a consideration. With many freelancers turning to remote work after the pandemic, the opportunity to work on international projects and be conveniently paid for doing so has increased dramatically.

No matter your skill set or ability, there is likely a business out there willing to hire you.

Where Job Seekers Can Connect With A Crypto Job Board

LaborX is a job board-style website that connects employers with employees, covering everything from small temporary jobs to full-time ones, from data scientists to marketing managers. The platform also offers a wide range of cryptocurrencies as payment options.

LaborX is owned and operated by a blockchain company that also offers HR software solutions, which makes it feel more accountable and solid.

Despite what the name suggests, Jobs4Bitcoins offers a range of crypto-paying jobs. Run as a Reddit channel, r/Jobs4Bitcoins, the forum allows anyone to post a job they require or skills they can provide.

While not run in the traditional job-seeking website sense, the opportunities for finding work and self-promotion are endless. There is obviously no vetting of employees or employers, however, so bear this in mind when engaging on the platform.

Blocklancer matches job seekers with job providers and pays in Ethereum. If you’re not fond of Ethereum, no problem, you can easily trade it for another cryptocurrency or fiat currency through the Tap app once you have received the funds.

The platform covers a wide range of jobs, from research analyst to content creator to experts in the field of blockchain and ICOs. It also offers an option allowing users to help mediate disputes.

If the formal job market is not what you are looking for, you can earn tips in Bitcoin for offering suggestions. Not only Bitcoin, you can also earn Bitcoin Cash, NANO, and Tezos.

Users post their questions and then should they find your idea or suggestion helpful, will tip you.

PompCryptoJobs was created to connect job seekers with providers within the crypto space. The platform caters to an extremely wide range of fully-paid crypto positions, from writer to product designer to data scientist.

The platform is professional, neat and informative, and is used by some of the biggest companies in the crypto space.

Whether you're a research analyst, marketing manager or data scientists, there are plenty of job opportunities that pay in crypto.

Final Thoughts: How To Get Paid In Crypto

If you’re unsure on how to go about getting an account that enables you to be paid in Bitcoin or other cryptocurrencies, look no further than Tap.

Tap offer to freelancers and self employed accounts, enabling you to receive payments in both crypto and fiat currencies. When creating an account, you will immediately gain access to a number of crypto wallets, as well as dedicated money accounts from where you can access the individual wallet addresses. Simply send the wallet address to your employer and the funds will clear in minutes (depending on the network).

On top of that, Tap also allows enables you to pay your bills and everyday purchases with your Tap card to spend your fiat and cryptocurrencies in a swipe of the wrist.

The post-pandemic working world is a different place entirely. These days, many people have given up their nine to five jobs to work from home, joining the gig economy where projects are more short-term and schedules are flexible. After all, all one needs is a reliable internet connection and a space to work.

These temporary projects allow for more freedom when it comes to creative license, time constraints and living a life best suited to the individual. And they just got a whole lot easier thanks to the electronic cash system that is Bitcoin (and other crypto assets).

The Gig Economy Meets Blockchain

There are plenty of upsides to working in the gig economy, most notably that you can pick your own hours. As you are in control of your schedule you can choose your vacation times, you’re your own boss, and you get to choose what jobs you take on.

In the UK alone the gig economy between 2016 and 2019 doubled in size, equating to a staggering 4.7 million workers. Meanwhile, in the European Union, the number of freelancers rose by 24% between 2008 and 2015, from 7.7 million to 9.6 million people.

The U.S. Bureau of Labor Statistics reported that 36% of all employees in the United States are part of the gig economy, approximately 57 million people. Unfortunately of these 57 million, 58% reported that they have not been paid for work that has been completed.

This problem could be solved through the use of blockchain and smart contracts. Smart contracts are digital agreements that automatically execute once the criteria have been met. Say you agree to complete a project within a certain time frame, once the project is completed and submitted, the payment is released. No need to request or accept payment, the funds are cleared and deposited directly into the relevant account.

Another positive to merging the gig economy with blockchain technology is the use of cryptocurrencies.

4 Reasons Why Getting Paid In Crypto Just Makes Sense

While smart contracts would need to be made in order for them to smoothen out the wrinkles of unpaid jobs, cryptocurrencies are available right now. The benefits of crypto transactions when it comes to working remotely just make sense.

1) Cryptocurrency transactions are fast and cheap

While the thought of using Bitcoin payments might sound scary, they are in fact incredibly simple to send, receive and withdraw. With the use of blockchain technology and the Bitcoin network, international transactions can be completed in minutes with considerably fewer fees. Not just Bitcoin, all digital currencies for that matter.

All you need to do is pick a cryptocurrency, share your wallet address and wait for the crypto transaction to clear. Through the Tap mobile app you can then use the funds to pay bills or sell them for fiat currencies and send them to your personal Tap account to spend as you please or directly to your bank account.

2Anyone can make crypto payments

While opening a bank account is typically a very tedious task, opening a crypto account is very easy. Anyone anywhere in the world can easily create an account, add funds, and start transacting. As the network is entirely digital, employees and employers based anywhere in the world can tap into this and effortlessly make crypto payments.

3) You can work from anywhere

On that note, cryptocurrencies give you the freedom to work anywhere in the world as there are no constraints on receiving payments allowing you to sell your skills in the global market. There has also been an increase in jobs looking for freelancers that are willing to accept Bitcoin, goodbye central banks and hello digital assets

4)Low transaction fees make small jobs worth it

If you've ever been hesitant about accepting small jobs, this is the one for you. When small jobs pay less, the payments might frequently be entirely overwhelmed by the transaction fees associated with receiving your payment for the job.

That is not the case when it comes to some cryptocurrencies, with Litecoin for example charging merely $0.02 per transaction.

How To Get Paid In Cryptocurrencies

If you’ve decided to take the plunge, you can either request that your employer pays in crypto, or specifically look for crypto-paying jobs (more on this below). The next step is to set up an account from where you can receive said crypto.

The Tap mobile app will tick all the boxes, and opening an account is incredibly simple. First, you will need to download the app and then register. You’ll be asked to fill in some personal information and then verify your identity with a government-issued identity document. This is all very normal and is required by law.

Once you are verified, head to the home page, select the Crypto wallet and choose a cryptocurrency you would like to receive / the cryptocurrency you will be paid in. Then select Receive and send the wallet address to your employer/contractor. You will get a notification when the funds arrive in your account.

If you’re looking for jobs that specifically pay in crypto, look to Purse.io, Ethlance and Coinality. These are part of the gig economy and pay in cryptocurrencies. Good luck out there, it will 100% be worth it!