With a Fed rate cut nearly certain, these three altcoins are positioned to capitalize on the macro shift, here's what makes them stand out.

Keep reading

Heading into the Federal Open Market Committee’s October session, a high-stakes environment is emerging for crypto markets. With the CME Group’s FedWatch Tool showing about a 96 % chance of a 25-basis-point rate cut, the market is eyeing how digital-asset prices might respond.

With macro liquidity on the radar again, these three altcoins stand out as tokens worth tracking under the spotlight of the Fed’s next move.

1. Chainlink (LINK)

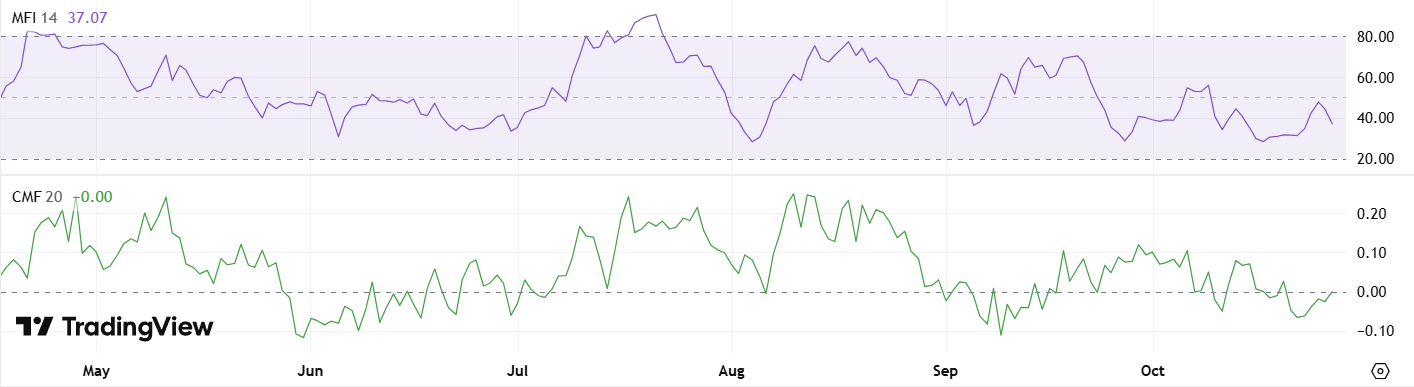

Chainlink has been acting under pressure, trading inside a falling wedge, a pattern which sometimes marks the end of a downtrend. Still, some caution flags remain. Over the past month LINK has been trading downwards, though it’s gained some strength in the last week amid renewed buying interest. The key support around $17.08 remains critical, if LINK closes below that, a drop toward $16 could be triggered.

Conversely, diagnostics like the Money Flow Index (MFI) and Chaikin Money Flow (CMF) are showing signs of life, hinting at growing accumulation from larger holders. Combine this with a potentially dovish Fed decision, and Chainlink could be gearing for something special.

2. Dogecoin (DOGE)

Dogecoin enters the FOMC event with a bit of range-bound suspense. Since October 11, DOGE has been oscillating between $0.17 and $0.20, waiting for a trigger. A clean breakout above $0.21 could open the door to a move back towards $0.27, especially if risk-on sentiment returns.

Volume and whale‐level data add texture to the setup. The Wyckoff volume profile recently flipped from seller control to buyer control, suggesting strategic accumulation may be underway. DOGE may be quieting down before a move, a scenario traders should keep front of mind as the Fed’s decision could stir things.

3. Uniswap (UNI)

Uniswap offers compelling recovery stories entering the FOMC session. The token experienced a sharp drop on October 10, with the RSI falling below 30, classic oversold territory. Since then, UNI has rallied from near $6.20 toward $6.50, supported by strong volume on the breakout. Holding above $6.40 may confirm that buying interest is sustained.

For longer-term watchers, UNI’s former highs at $12.15 in August and $18.71 in December set the stage for what could become a multi-leg recovery if macro conditions cooperate. In a market where liquidity expectations hinge on the Fed, Uniswap's rebound has the potential to accelerate, particularly if altcoin capital begins rotating into DeFi infrastructure.

The Verdict

These tokens aren't just compelling because of their individual fundamentals, it's how those fundamentals intersect with the current macro picture. With markets rebounding and rate cuts looking increasingly likely, crypto stands to gain. Lower rates typically fuel risk appetite, unlock liquidity, and drive capital toward speculative plays, creating tailwinds that can supercharge momentum in well positioned altcoins.

That said, the Fed could also surprise with restraint, and even another “standard” 25-basis-point cut may be viewed as lukewarm. In such scenarios, the dollar may strengthen and risk assets could wobble. Traders and investors should therefore approach the market with discipline, track the macro context, and be prepared for either direction.

NEWS AND UPDATES

LATEST ARTICLE

When exploring the world of blockchain and its endless possibilities, it’s likely that you’ve come across the term dapps. But what are dapps? In this piece we explore the concept, decipher their place in the industry, and look at several networks that currently support them.

What are dapps?

Decentralized apps, or dapps as they’re more commonly known, are applications that are built on top of peer to peer decentralized networks. Instead of being built on one computer, with one single entity in control, dapps utilize a network of computers based anywhere around the world. With multiple computers operating and maintaining the network, dapps are able to incorporate many streams of content consumption, be it providing content, trading or consuming it.

The advantages of dapps

Compared to standard web apps, like Twitter or Uber, these apps can handle multiple users but only one authority has control over the backend of the app. Dapps provide a more decentralized and secure approach. So while Uber connects passengers to drivers through the app for a portion of the payment, dapps essentially allow the drivers and riders to connect directly, taking no payment for the connection.

Another advantage to the world of dapps is that all transactions are transparent and stored on the blockchain of the network it is built on. Dapps also need a token to operate, which enhances the security of both the dapp and the transactions taking place. Typically dapps are also open source, allowing other developers to view the code and further drive development in the industry.

The disadvantages of dapps

As with anything in life, there are also disadvantages. As the world of dapps is still in its infancy stage, the user base is relatively low. When it comes to blockchain based projects, the more users a network has the higher functioning the network is. Unfortunately, many dapps still have a relatively low user base decreasing the functionality, however that doesn’t speak for all of them. As the blockchain and crypto worlds continue developing and reaching wider audiences, both the usability and users will increase.

Another disadvantage is the potential vulnerability to hacking. As most dapps are created using open source smart contracts, this leaves them open to potential probing from hackers. This isn’t a given, however it has happened in the past that hackers found weaknesses in the network and were able to conduct illicit activities through them.

How many dapps are there?

According to a dapp monitoring website, State Of The Dapps, there are currently roughly 3,500 dapps in the industry. These are spanned across a wide range of networks, including the likes of Ethereum, EOS, TRON, NEO, Steem and more. The website further reports that over $257 million has passed through the dapps industry in just twenty four hours (at the time of writing). Dapps also cover a broad range of subjects, with dapps catering to industries like energy, exchanges, finance, gambling, games, health, identity, insurance, marketplaces, media, property, security, social, storage and wallets. The most widely of which are finance, security and exchanges.

A look into Ethereum dapps

The most widely used network to create dapps on top of, Ethereum has over 2,700 dapps built on its network. Ethereum was the first network designed to provide a blockchain platform on which developers could build their own decentralized applications. Ethereum was also the first network that allowed developers to create and execute their own smart contracts, an essential ingredient to the making of dapps.

According to DappRadar, the three biggest dapps currently on the Ethereum network are DeFi projects and an exchange. Coming in at first place based on its current market cap is Uniswap, a defi protocol (exchange) that facilitates the trading of cryptocurrencies. Uniswap has an estimated 48,950 active users. Also dabbling in the world of DeFi, the second largest dapp on the Ethereum network is compound, a protocol that allows users to lend and borrow crypto. The third largest is MakerDAO, a smart contract that facilitates user interaction with the Dai stablecoin system.

A look into EOS dapps

Similar to Ethereum but with fewer transaction fees, the Entrepreneurial Operating System was designed to provide developers with a platform on which to build their blockchain based endeavours. As the second largest platform on which dapps are currently created, let’s explore the three largest dapps currently operating on the network. Coming in first place is Joule, a dapp which promotes financial inclusion and social change through determining the Global Popularity Index in real time. The next two entries both fall into the DeFi category, being Defibox and VIGOR.

The power of dapps

While many dapps are still in the experimental phase, there is also a large amount of money circulating in the industry and millions of users indicating a promising market. Thanks to dapps’ wide use range and the amount of innovation in the industry at present, the dapp industry is likely to continue growing and become a permanent fixture in many peoples’ lives, whether crypto inclined or not.

As we explore the world of crypto assets, we take a look at the different types of crypto assets on the market and at the wide range of diversity in the new-age industry. As more people enter the market and start exchanging digital assets, the industry grows and expands to allow new variations.

Below we explore the vast diversity in the industry, from crypto assets used as money to ones that reward users for viewing a website. Each business offers a unique solution, and to navigate this we offer you guidance below.

What Are Crypto Assets?

The terms "crypto asset" and "cryptocurrency" can be used interchangeably. They both refer to a digital asset built using blockchain that can be transferred in a direct peer-to-peer manner. The first crypto asset to launch is Bitcoin, which entered (and created) the scene in 2009. Since then thousands of crypto assets have been created, each one with its own unique use case.

The Different Types Of Crypto Assets

While crypto assets might fall into one or more categories, each has its own set of rules and use cases.

Payment-Focused

These crypto assets can be used to pay for everyday goods and services or as a store of value (in some cases). These include the likes of Bitcoin (BTC), Ethereum (ETH), Litecoin (LTC), Bitcoin Cash (BCH), etc.

Stablecoins

Stablecoins are crypto assets that have their value pegged to a fiat currency or commodity. These crypto assets are designed to bypass the volatility synonymous with the crypto market. These include the likes of Tether (USDT) and USD Coin (USDC).

Privacy Coins

Privacy coins are digital assets that hide details of the transaction, such as the origin, destination and amount. These crypto assets offer untraceable monetary transfers. These include the likes of Monero (XMR) and ZCash (ZEC).

CBDCs

Central Bank Digital Currencies (CBDCs) are crypto assets built and maintained by banks. Used as digital currencies alongside the traditional currency, CBDCs are designed to provide a digital version of the local fiat to which the value is pegged.

Governance Tokens

Common among decentralized finance (DeFi) protocols, governance tokens provide holders with a say in the platform and in future updates.

Utility Tokens

Utility tokens will typically provide a service to the holder on the platform on which it was created. Commonly created using the ERC-20 token standard, utility tokens might represent a subscription on a platform or a use case specific to that ecosystem.

Non-Fungible Tokens

Non-fungible tokens, also known as NFTs, are crypto assets that cannot be used interchangeably and instead hold unique and rare properties. Each NFT represents a singular function that cannot be changed.

How Are Crypto Assets Created And Distributed?

Before crypto assets are created the project's intentions are generally circulated through a white paper. In this white paper, the asset's tokenomics will be outlined which will cover how the asset is created and distributed.

Bitcoin, for example, uses a Proof of Work consensus which means that new coins are entered into circulation through miners solving complex mathematical problems. The network was designed to only ever have 21 million coins created, and new coins are slowly entered into the system each time a miner verifies and adds a new block to the blockchain.

Ethereum on the other hand has no limit to the number of ETH that can be created. The platform is currently moving from a PoW to a Proof of Stake consensus, which alters the way in which transactions are verified, however, new coins still enter circulation through verifying transactions.

XRP minted all its coins prelaunch and slowly release them into the system through a central authority while Tether creates USDT on demand. For each $1 sent, 1 USDT is created, which can later be removed from circulation should it be sold.

The Future Of Crypto Assets

With the ICO Boom in 2017, the DeFi boom in 2020 and the more recent NFT Craze, crypto assets aren't going anywhere. With constant innovation and increasing adoption, crypto assets have become an integral part of the modern day financial landscape.

While mainstream adoption is on the rise, a few wrinkles still need to be ironed out. For one, regulatory bodies around the world are working toward creating legal frameworks in which these crypto assets can exist, while centralized banks are exploring whether CBDCs can co-exist with their physical counterparts. While the world seeks to figure these out, one this is for certain: crypto assets are here, and the industry is becoming bigger by the day.

Have you heard of the term “altcoin” but not exactly sure what that means? In this article we’re breaking down everything you need to know about altcoins, from the different types of altcoins and how they work, to how you can get your hands on them (buy altcoins). The crypto industry can often feel a little daunting, so we’re here to clear the air and help you establish a strong foundation of insight, knowledge and know how.

Starting at the beginning, what are altcoins? Altcoins are all cryptocurrencies except for Bitcoin. Not too complicated, is it? Circling back to the early days of the crypto industry when there were only a few cryptocurrencies on the scene, any new coin that was introduced was referred to as an “alternative coin” (labelling it as an alternative cryptocurrency to Bitcoin), which was then shortened to altcoin. So when someone refers to an altcoin, know that they are talking about any cryptocurrency that is not the original (Bitcoin). Altcoins are still decentralized networks, with most of them utilizing blockchain technology.

How Many Altcoins Are There?

At the time of writing, CoinMarketCap reports that there are over 9,400 altcoins in the cryptocurrency industry. This number is increasing by the day, however it’s worth mentioning that these 9,400+ altcoins only make up 50% of the entire cryptocurrency market’s value. Bitcoin is still the most dominant cryptocurrency, with Ethereum the next bigger cryptocurrency. Ethereum is currently responsible for holding roughly 14.5% of the entire market’s value. As Ethereum is also an altcoin, this makes the “altcoin industry” worth $1 trillion. In general terms, one would rather just say the crypto industry.

The Different Types Of Altcoins

With an industry worth over $1 trillion, there is bound to be a wide range of variation. This is just the case with the crypto industry. There are a number of categories that have been created over the years, allowing for various altcoins to provide a new service to the industry. You can also expect to see tons of innovation in the altcoin space, as each new altcoin needs to either improve on the last one, or provide a different use case.

Each cryptocurrency is designed to solve a problem, either faced within the blockchain industry or outside of it, however, many of these have created a niche altcoin market. An example of this is altcoins focused primarily on providing anonymous transactions, these altcoins then fall into the Privacy category. We’ve detailed seven of the main categories below to give you an indication of the vast innovation and use case potential within the space.

Payment Focused Altcoins

First and foremost, these cryptocurrencies’ primary aim is to provide a medium of exchange within the digital currency realm. Focusing on payment functionality, these digital currencies are akin to Bitcoin and often were created as a “better” version of BTC (through hark forks on the network). Some examples of this include Litecoin (LTC) and Bitcoin Cash (BCH).

Protocol Focused Altcoins

Protocol focused altcoins are designed to allow developers to work on their blockchain network to create decentralized apps (dapps), smart contracts, and in some cases other cryptocurrencies. They provide space for innovation within the blockchain industry, and empower developers to learn and grow their blockchain understanding. Examples of protocol focused cryptocurrencies include Ethereum (ETH), Tron (TRON) and Neo (NEO).

Privacy Focused Altcoins

As mentioned above, privacy focused cryptocurrencies provide users the opportunity to send private transactions that are entirely encrypted. While these networks often garner a bad name due to them being used for illicit activities, they are in essence not far from what Satoshi Nakamoto originally intended for Bitcoin. Each network uses slightly different protocols, however they all provide the means to send secure, anonymous transactions. Examples of privacy focused cryptocurrencies include Monero (XMR), Zcash (ZEC) and Dash (DASH).

Stablecoins

You’ve likely heard of stablecoins before. They are the digital currencies that are pegged to a fiat currency. Providing a stable market inside of what has become known as a highly volatile market (cryptocurrencies as a whole), stablecoins offer a hedge against market dips as well as an entry point for users who want to get a feel for the crypto industry. Examples of stablecoins include USD Coin (USDC) and Tether (USDT) which are both pegged to the US dollar, trading at a 1:1 ratio (i.e. 1 USDT will always be worth $1). Stablecoins also include cryptocurrencies pegged to the value of commodities such as gold and oil.

NFTs

NFTs (non fungible tokens) have had their fair share of mainstream media attention recently, especially after one NFT broke records when sold for millions of dollars. NFTs are actually unique crypto assets that cannot be used in the same way that other digital currencies can be. Each NFT holds unique characteristics that represent a one of a kind product, whether it be a piece of digital art, physical art, a house, or even a luxury handbag. These altcoins cannot be recreated, and hold all their transaction history (previous ownership) on a transparent blockchain. They also cannot be “spent” in the same way as other cryptocurrencies in that one an NFT is created, it has that purpose attached to it for life (unlike BTC which can be spent interchangeably).

CBDCs

CBDCs (central bank digital currencies) are similar to stablecoins but are created and maintained by financial institutions like banks. These currencies’ value is pegged to the local currency, and allow countries to test the efficiency of digital currencies without the volatility. Many countries are in the development phase of CBDCs, however China is leading the pack having recently launched their testing phase.

Utility tokens

Utility tokens are blockchain tokens that are unique to a particular platform. Many cryptocurrency projects have created utility tokens as a means of crowdfunding prior to their launch, while other projects create utility tokens to be used within the platform for goods and services. Typically, utility tokens have been ERC-20 tokens, and might allow a user access to a new level of a game or to a subscription of some sorts.

How to Get Altcoins

Having gained an understanding of altcoins, individuals eager to explore the thriving altcoin market can effortlessly leverage the capabilities of the Tap app. Tap offers seamless access to an extensive spectrum of cryptocurrencies, including notable names such as Ethereum, Litecoin, XRP, and an assortment of others. It's crucial to bear in mind that not all cryptocurrency wallets exhibit compatibility across the board. For instance, attempting to house an altcoin like XRP within your Bitcoin wallet or stow Tron within your Ethereum wallet would not work due to their incompatibility.

Bitcoin and other cryptocurrencies are all about decentralised, worldwide, financial independence and liberty. Cryptocurrencies are borderless, censorship-resistant digital currencies that can be used by anybody with internet access.

As a result, crypto, at least in principle, appears to be the perfect solution for international travellers or "digital nomads." With the added advantage of having the Tap app, users can instantly and seamlessly use their cryptocurrencies as they would regular fiat currencies when travelling around.

With the growth rate of blockchain technology and crypto adoption increasing, it's only natural that we're seeing more options to spend and travel the world using cryptocurrency.

In this article, we'll look at a variety of different ways to spend your crypto while travelling with Tap and how to spend seamlessly with your Tap card. We will explore why people choose to use their crypto to travel and how the exploding $1 trillion travel market is important for the cryptocurrency industry.

Entirely Cashless

The beauty of travelling with crypto is that it is entirely cashless. You won't have to worry about dealing with foreign currency exchanges when entering or leaving a different country as all of your money is kept digitally online in your app.

With the Tap card, users can use their crypto balances to load their card and freely swipe away worldwide. The card allows for seamless payments at millions of merchants around the world, with the merchant none the wiser.

The option to upgrade to more premium accounts allows you to reduce or completely eliminate any FX fees. Get empowered and enjoy the best out of your money wherever you go.

Reduces Risk

Instead of being a target for muggings looking to steal cash, being entirely digital bypasses this risk.

Accessible

Should something happen at home you can easily and quickly send funds back. Operating 24/7 and only requiring an internet connection, sending money back home can be completed at a moment's notice. Send funds to your friends and family via crypto or fiat for free on their Tap account.

Discounts

Last but not least, many companies offer discounts to users paying with cryptocurrencies. From travel to retail, and everything in between, users can enjoy added discounts just by utilising crypto.

Should an event arise that you do need cash, users can easily withdraw cash from a regular ATM using their Tap card. Paying significantly lower fees than you would with your standard bank card, the Tap card allows you to seamlessly integrate into the foreign country with peace of mind.

How To Travel Abroad With Tap

This is the ultimate crypto vacation guide showing you how to buy everything that you might need through the Tap app for that epic crypto vacation abroad.

Flights

CheapAir.com was the first US online travel agency to open its doors to crypto, getting into the game as early as 2013. The company currently allows holidaymakers to make payments using Bitcoin, Litecoin, Bitcoin Cash and Dash.

In 2020, Travala and Expedia merged to give users access to millions of hotels and villas worldwide payable in over 30 popular types of cryptocurrencies. There is also Destinia.com in Spain, airBaltic in Latvia, Surf Air in the US, and Peach Aviation in Japan.

Conveniently buy everything you need with your Tap app by scanning the company’s QR code and confirming the transaction. Alternatively, you can make online purchases using your Tap card.

Accommodation

Travala, CheapAir.com and Destinia all allow users to book flights and accommodation in one smooth transaction. On Destinia look out for the GoCoin merchant plugin.

Booking.com has partnered with flight planner, A Bit Sky, to provide a location with both flight and accommodation options.

Savvy accommodation-seekers can look to Airbnb-style crypto startups like 99Flats in India or CryptoCribs on Reddit, or head over to XcelTrip,a decentralized travel ecosystem, which provides access to 400 airlines and 1.5 million hotels.

Food and Drink

CoinMap is an app for anyone and everyone wanting to find crypto-friendly companies. Felix Weis, as well as numerous other cryptocurrency influencers, has credited CoinMap with being the saviour for finding the closest cafe, bar, or restaurant that accepts Bitcoin, including international chains such as Subway and local providers who use crypto merchants. Say goodbye to walking around with boatloads of cash and just take your Tap app along instead.

Holidaymakers can also look to using crypto to buy a gift card which can be purchased online through Gyft or eGifter, with eGifter offering a 5% discount for purchases made with Bitcoin. eGifter offers gift cards to restaurants like Papa John, Taco Bell, Dunkin’ Donuts, TGI Fridays, UberEats and more.

Getting Around

Expedia, A Bit Sky, Destinia, and CheapAir all offer access to transfers or car rentals in their services, while Gyft and eGifter offer Uber vouchers. There is also SpendBitcoin.com, which locates different crypto-accepting services in an area, simply chose the car filter option.

Things To Do

Again, Gyft and eGifter provide access to options like Groupon where you can find local activities on offer, or head to purse.io for any last-minute Amazon purchases (snorkel, anyone?).

Travel The Tap Way

Both the Tap card and the Tap app can provide a seamless and cost-effective solution to using both fiat and cryptocurrencies when travelling. Simply load your wallet with crypto and fiat currencies, and pay directly from the app or use the card to pay at millions of merchants around the world. Say hello to easy travel and plenty of discounts.

With a range of coins on offer and an integrated smart engine that ensures the best possible prices in real time, travelling with cryptocurrencies and Tap is as smooth a ride as it gets.

With a range of coins on offer and an integrated smart router, Tap lets you store and manage your digital assets wherever, whenever. There are no border delays or inconvenient payment processes to worry about while travelling with crypto only speed and convenience. Tap is as seamless a journey as it gets.

Cryptocurrencies have truly sparked a revolution, haven't they? It feels like just yesterday they were the secret of tech enthusiasts and visionaries. Now, they’ve transformed into a bustling digital marketplace that’s open to everyone. It’s incredible to see how businesses, both big and small, are embracing these technologies, eager to be part of this vibrant growth story.

Crypto technologies are here to stay. The era where crypto was only for a specific circle of people is over and more companies are taking advantage of this steadily growing market. More large corporations than ever before are willing to develop and invest in the advantageous market of cryptocurrencies.

The crypto-world is blooming with new developments, and it seems that developers in this field can't stop pumping out innovative updates. Skilled developers and talented specialists in this field are making exchanges more accessible with their innovative work, by turning simple tasks into ease of access for users around the globe.

Crypto banking has been the go-to for many people in need of an alternative to conventional banking. With its lack of certain features, it still provides all that is needed with crypto limitations taken care of and more! Here's a look at some advantages of using this service over fiat currency.

The first thing you'll notice when comparing bank services side by side is how similar they can be despite being different types altogether; one might not work without another if both suit your needs well enough

Crypto banking is a revolutionary new way of doing banking. It has many advantages and disadvantages when compared with regular fiat banking. Let’s explore in more detail and analyse what are the advantage and disadvantages of crypto- banking.

The advantages:

Independent system

Cryptocurrency, as a whole, is set to be free of reliance on outdated and archaic centralized economies allowing users to manage every aspect of it while giving them full control over its finance. There are no strings attached to trap you into a quagmire of peculiar circumstances.

Low withdrawal fees

Banks are generally charging a fee whenever you withdraw cash from an ATM or the terminal, while crypto banking enables you to withdraw cash for free up to a certain amount.

Withdrawal fees with crypto banking are one of the best features and a major step towards the future, they charge users as low as 0.01% for their transactions no matter how big the amount you try to withdraw is compared to conventional banks.

Openness

Crypto banking platforms have created opportunities for people who were previously shut out of traditional financial services. If you've credit score is low, it'll be hard to find a loan that's affordable and most banks don't offer good interest rates on their saving accounts either.

Higher returns rate

Crypto platforms offer high-yield savings accounts with rates that far exceed traditional ones, enabling their users to beat the inflationary effects. They also provide secured loans without a credit check and other financial services for people in need who are not considered eligible elsewhere.

Currency exchange

So, you’re exchanging your currency for another one? Well, that could cost as much as 4% - applied to a large amount that could be as high as 40£ for every 1000£ that you are converting! Crypto banking, on the other hand, provides an opportunity for you to exchange between various cryptos with a commission as low as 0.1% and conduct rapid peer-to-peer transfers that can be, depending on your plan, free of charge.

The cons

Online-based

Crypto banking is based and operated online. It’s all about convenience with a quick and easy app for your smart device to control any of your operations in real-time. However, they might not be the best option for seniors or customers who are challenged with using these online services as they often need more personal attention than what this system offers them.

Assets volatility

While cryptocurrencies have gained in popularity over the years, they remain volatile assets. Thankfully you can now use fiat currencies and stable coins with many crypto banking providers in order to eliminate this risk.

Conclusion:

In conclusion, crypto banking became an essential part of the global financial transformation happening worldwide. In view of the advancement pace it evolved at, we wouldn’t be surprised to see it prosper in the coming years, and infiltrate every aspect of our everyday life.

Bitcoin has become a household name around the world, for very good reasons. The same way gold became the standard of currency, bitcoin is doing the same. With the rise of gold, we also saw a gold rush, as people flocked to the mines to find every flake of gold they could. Something similar is happening to bitcoin right now as the cryptocurrency mining rush has begun, with the world hiking up their ASIC miners to process as fast as possible.

Especially with talk of Elon Musk considering reinstating Bitcoin payments once the carbon emissions and energy consumption associated with bitcoin mining are decreased. But why the sudden rush? it is not just another bubble, it is about global economic sustainability and excelling cryptocurrencies.

Where is the Bitcoin mining rush happening?

Although the whole world may be captivated by the potential of cryptocurrency, China has always been a top contender for miners. Despite the repeat FUD spreading around China and its acceptance of digital currency, China bitcoin mining once accounted for more than 70% of mining power. But this summer's sweeping crackdown in China has greatly increased profits for miners outside of the world's second-largest economy, with counties such as the USA, Russia, and Iran making up for lost blocks. These regulations won’t stop Chinese miners from doing what they need, they just may no longer be doing it within the borders of China.

It was 2 months ago that Beijing made moves to crack down on cryptocurrency. One of the steps was halting the supply of power to bitcoin farms, giving Chinese miners no choice but to pack their bags for more crypto-friendly countries. Chinese researchers express data portraying excess use of electricity consumption, especially in these stressful times.

What is Chinas’ issue with digital currency mining?

China has had numerous issues with cryptocurrencies over the years, first stating they didn’t want their economic wealth flooding into a global currency. They have potentially solved this problem as they announce their own digital currency created by a group of specialist. China’s digital currency, the digital yuan, is controlled by its central bank which will issue the new currency. Now they may have created a digital form of currency, but it is nowhere near cryptocurrency, aside from some computational comparisons. China plans to strip away the anonymity so beloved within Blockchain, and inside track and control where their digital currency goes. Nonetheless, their first issue has been fixed, so what is their problem now?

Supposably carbon emissions and energy consumption in the country are rising, due to cryptocurrency, not the masses staying at home. Regardless of if their reasoning and intent are pure, we know carbon emission due to cryptocurrency is a very real and impending issue. This theory has been confirmed by Tesla's Elon Musk halting bitcoin payments until the carbon emission issue is resolved, rightfully so as the guy selling low carbon emission electric cars.

What is next for Chinese miners?

Bitcoin mining is one of the most lucrative major industries in the world, yet many people don't know that Bitcoin mining generates just as much revenue as gold and silver extraction. The old Gold Rush might be waning, but Bitcoin miners are reaping the rewards of a new gold rush. The current generation shows entrepreneurial spirit unlike many before it, especially as the online era continues to expand.

They see the market and trend associated with cryptocurrency and are ensuring they are involved in as many ways as possible. From trading on an exchange, accepting bitcoin for services, or using their computer to mine crypto. Blockchain technology is proving to be a leader in so many industries, even emission avoidance, so no issue should or will stop people from accepting and collecting it.

Renewable energy countries

The solution to China's electricity and energy consumption issues is not to stop cryptocurrency mining altogether, but rather for miners to move to more power conscious countries. This may not be so appealing for China itself, but it is proving to be the best option for miners. Miners may take a lot of energy and computer processing, but they also run very hot.

So miners are looking for a country with a cheaper electricity cost to move to, with the added benefit of them being cold for an additional cooling process. Most countries that use renewable energy find their costs a lot lower than those that do not, this was even seen in China. Miners would run to the mountains of Sichuan, where abundant hydroelectric power made electricity services costs exceptionally cheaper per unit.

Colder climates like Germany, Sweden, and Scotland are becoming increasingly more desirable countries of residency for crypto miners. Sweden is planning to be the world's first fossil fuel free country by the year 2040. Denmark has broken a wind power record, showing 43% of its electricity consumption being covered by wind; they also plan to be fossil fuel free by 2050.

Germany is a leader in renewable energy, and in the first half of 2018 they proved that, by producing enough renewable electricity to power every household in the country for a year. Scotland is also joining the ranks of the greatest renewable energy countries. Scotland plans to build the worlds’ largest floating wind turbine farm, as wind power can generate 98% of Scotland’s electricity needs.

These are all brilliant, and cold countries can easily fit the needs of any cryptocurrency miner, with cheaper watts and a cooler climate to cut down even more on watts.

Risk of regulations

While the above-mentioned countries are great candidates for cryptocurrency and bitcoin mining, there are other problems to be wary of. Crypto regulations are just an issue among crypto miners, but also for exchange services. Each country has taken its own approach to enforcing cryptocurrency into its economy, but some may be trickier than others. VISAs are also another thing to take into consideration. Holiday VISAs are easily acquired, but moving your entire mining farm across borders may not be as easy.

Would you need a work VISA? A residency VISA? That is up to each miner to find out. Germany has shown positive sentiment to cryptocurrency, considering it as legal tender, and allowing institutional funds to hold up to 20% in cryptocurrency. Denmark and Scotland have also shown interest in cryptocurrencies, considering tax policies to help their native traders and the economy. Miners may be susceptible to taxation, and VISA regulations, but they do not have to worry about being in a country that wants to get rid of cryptocurrency. This alone, in addition to renewable energy, are benefits to any crypto enthusiast.

Bettering the blockchain process

Not only does renewable energy mining save the world and miners money, but it also advances blockchain in general. Projects and people are more likely to accept cryptocurrency and Blockchain when it doesn’t have such a high economic and environmental burden. Using a terawatt of renewable energy is far more efficient and cost-effective than using electricity powered by fossil fuels and coal. With the bitcoin and cryptocurrency mining rush continuing to rally up troops, we in the community need to make conscious decisions for both cryptocurrency and our planet.

The process of excelling bitcoin and bitcoin mining starts at finding a computing process that consumes less energy. Whether the miners in China, or around the world, have this intent is not the issue, as long as the rest of the planet pushes them towards more eco-friendly options. It doesn’t start with the miners, they are simply the suppliers, its starts with what we demand, as seen by Mr. Musk. Let us make better choices for Blockchain, earth, and our national economies.