Is USDT safe? Explore how Tether works, what backs it, key risks, and why it remains the most-used stablecoin despite regulatory and transparency concerns.

Keep reading

USDT is everywhere in crypto: powering trades, bridging platforms, and acting as a go-to safe haven when markets turn volatile. Backed by Tether, it promises the stability of a dollar with the speed of digital assets. But how secure is that promise?

In this article, we’ll unpack how USDT works, the risks beneath the surface, and why it remains a key player in the crypto economy.

What is USDT and why it matters

Think of USDT (Tether) as the crypto world's attempt to create digital cash that doesn't give you a heart attack every time you check its price. Launched back in 2014 by a company called Tether Limited, USDT was designed to be a "stablecoin" - a cryptocurrency that maintains a steady 1:1 relationship with a certain fiat currency: the US dollar. One USDT should always equal one dollar. Simple, right?.

Well, like most things in crypto, it's a bit more complicated than that.

USDT has become the utility tool of crypto, offering a fast and flexible option to move in and out of positions without cashing out to traditional fiat. It’s the common language of the crypto ecosystem, enabling smooth transfers, seamless trading, and a place to park value when markets swing.

Tether Limited, the company behind USDT, operates globally, with roots in the British Virgin Islands and operations stretching from Hong Kong to the Bahamas. Unlike central banks, Tether isn’t printing dollars, though: it issues tokens, claiming each one is backed 1:1 by assets in reserve.

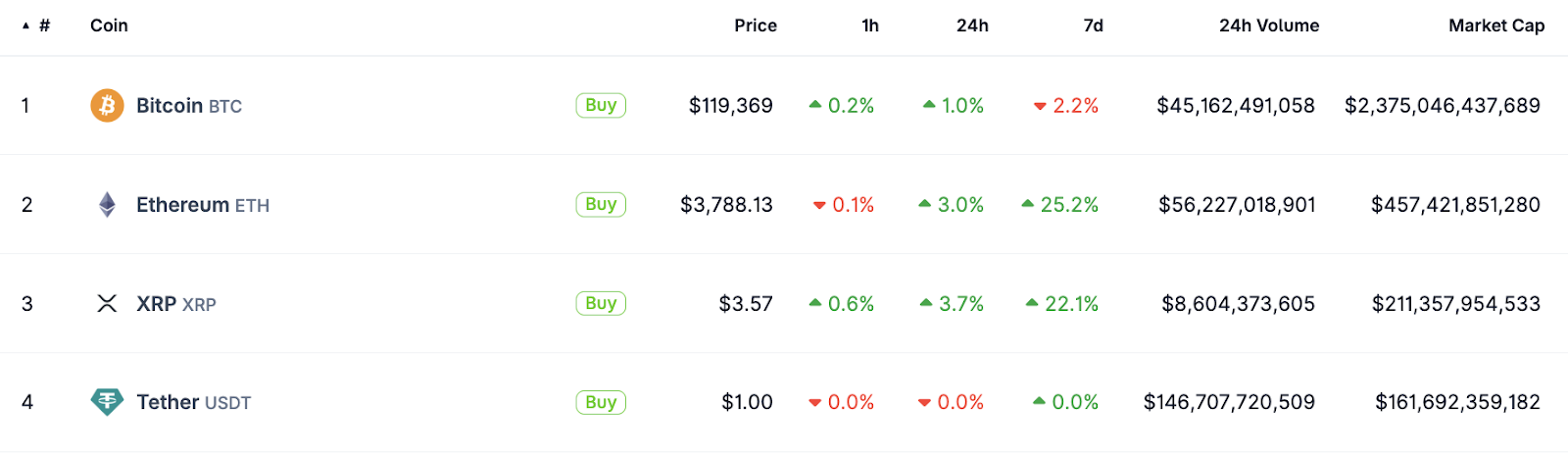

With over $160 billion in circulation as of mid-2025, USDT isn’t just a trading tool, it’s foundational infrastructure for the crypto economy. It’s also the largest stablecoin on the market, based on market cap and 24-hour trading volume.

Top cryptocurrencies by market cap at the time of writing. Source.

Is USDT safe?

The short answer? USDT exists in a grey area between "reasonably safe for what it is" and "proceed with caution."

The slightly longer answer? Here's what you need to know at a glance:

What's working:

- Maintained its dollar peg through multiple market crashes

- Backed by a mix of cash, government securities, and other liquid assets

- Most widely accepted stablecoin across exchanges and platforms

- Regular attestations from accounting firms

What's concerning:

- Limited transparency compared to some competitors

- Regulatory uncertainty and past legal issues

- Concentration risk (too big to fail, too big to save?)

- Not fully backed by cash alone

The reality check: USDT has survived crypto winters, bank runs, and regulatory pressure for nearly a decade. While it's not risk-free (nothing in crypto is), it's proven more resilient than many predicted. For short-term trading and payments, most users find it reliable. For long-term wealth storage? That's where you might want to consider your options more carefully.

How USDT is backed: understanding Tether's reserves

Here’s where things get more complex and where much of the scrutiny around Tether lies.

In simple terms, USDT operates like a digital receipt: you deposit dollars, and in return, you get tokens you can use across the entire crypto ecosystem. But what happens to those dollars? Are they sitting in a vault, or being put to work?

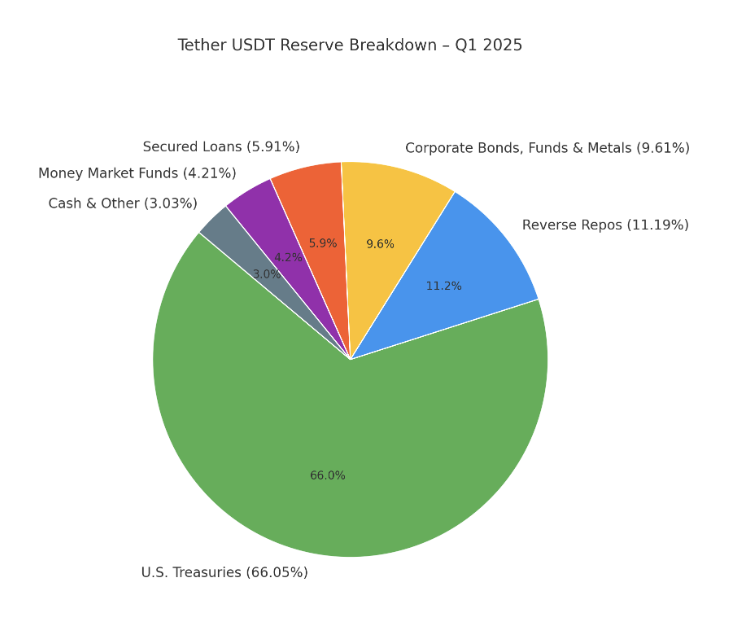

Tether has long opted for the investment route. Instead of holding pure cash, it backs USDT with a diversified portfolio of assets. According to its Q1 2025 attestation from BDO, Tether’s reserves looked roughly like this:

The shift toward U.S. Treasuries and away from riskier assets marked a significant improvement in its reserve quality. While not fully audited, Tether does publish quarterly attestations from BDO, providing some visibility into how reserves are managed. It’s not a full audit, but it’s a step forward from the opaque reporting of earlier years.

That being said, past controversies still shape how Tether is perceived. In 2019, Tether admitted that USDT was not fully backed by cash at all times and revealed it had lent $850 million to Bitfinex, its sister company. This led to a high-profile settlement with the New York Attorney General in 2021, requiring Tether to improve transparency and cease operations in New York.

Again, to put it in simple terms: imagine your bank quietly loaning out customer deposits to a related company without clearly telling you. Not necessarily illegal, but definitely a breach of trust for users expecting a 1:1 backed stablecoin.

Regulatory scrutiny & legal risks

If USDT were a person, it would probably have a thick file folder in regulatory offices around the world. Sure, being the largest stablecoin makes you a big target, but Tether has also found itself in the crosshairs of regulators who are still figuring out how to handle the crypto revolution.

In the United States, Tether operates in something of a regulatory twilight zone. The company has faced pressure from agencies like the Commodity Futures Trading Commission (CFTC), which fined Tether $41 million in 2021 for making false statements about being fully backed by US dollars.

The European Union is taking a more structured approach with its Markets in Crypto-Assets (MiCA) regulation, which will require stablecoins to be backed by highly liquid assets. This could actually work in Tether's favour, as they've already been moving in that direction.

Emerging markets present their own challenges. Some countries have embraced USDT as a hedge against local currency instability, while others have banned it outright, not far from a global game of regulatory whack-a-mole.

For users, the regulatory risks are real but indirect. If major jurisdictions crack down hard on Tether, it could affect the token's liquidity and usability. However, a complete overnight shutdown seems unlikely given USDT's deep integration into the crypto ecosystem.

The bigger risk might be increased compliance requirements that could make using USDT more cumbersome, similar to how traditional banking has become more regulated over time.

How safe is USDT for holding assets?

This is where we need to have an honest conversation about what "safe" means in crypto land.

For short-term use (days to weeks):

USDT works pretty well. If you're trading crypto or need to park funds briefly between investments, it's like using a decent hotel - not your forever home, but comfortable enough for a short stay.

The peg has held remarkably well through various market conditions, and liquidity is excellent across most major platforms.

For medium-term holdings (months):

Here's where things get a bit more nuanced. USDT has survived multiple "stress tests", including the Terra Luna collapse, FTX implosion, and various banking sector scares. However, you're essentially trusting that Tether's reserve management continues to work smoothly and that no major regulatory bombshell disrupts operations.

For long-term wealth storage (years):

This is where many experts start raising eyebrows. Holding large amounts in any stablecoin for extended periods comes with risks that compound over time. You're exposed to regulatory changes, potential company mismanagement, and the general "unknown unknowns" that come with relatively new financial instruments.

Essentially, USDT is like keeping money in a foreign bank account. It might work great for a while, but you're subject to the laws, regulations, and business practices of entities outside your home jurisdiction.

The key insight from the crypto community is diversification. Even USDT supporters rarely recommend putting all your eggs in the Tether basket.

Security best practices when using USDT

Using USDT safely isn't just about trusting Tether - it's also about protecting yourself from the various ways things can go wrong in the crypto world.

Platform risk management: Remember, USDT is only as safe as the platform you're using it on. The token itself might be fine, but if you're holding it on a sketchy exchange that gets hacked or goes bankrupt, you could lose everything. Stick to regulated platforms only.

Diversification strategies: Many crypto users often split their stablecoin holdings across multiple tokens and platforms. Think of it as not putting all your digital eggs in one digital basket. As an example, some might hold 40% USDT, 40% USDC, and 20% in other stablecoins or traditional assets.

For crypto beginners: Start small, learn the ropes, and, if you wish, gradually increase your holdings as you become more comfortable. Use well-established exchanges for your first purchases, enable two-factor authentication on everything, etc. Treat your crypto security like you would your online banking, that's essentially what it is.

USDT vs other stablecoins

The stablecoin world isn't a one-horse race, and understanding the alternatives helps put USDT's safety in perspective.

USDT vs USDC

USDT dominates in usage and global liquidity. It's the most widely accepted stablecoin across exchanges, DeFi platforms, and payment rails. But it has faced criticism over the years for a lack of full audits and historical opacity around reserves.

USD Coin (USDC), issued by Circle, takes a different approach. It’s often seen as the “regulated” stablecoin, with monthly attestations and a conservative reserve mix (primarily cash and short-term U.S. Treasuries).

- USDT is ideal for fast-moving markets and broad platform compatibility.

- USDC appeals to those who prioritise transparency and regulatory oversight.

USDT vs DAI

DAI takes a completely different route. Issued by MakerDAO, it’s a decentralised stablecoin backed by overcollateralised crypto assets like ETH, not fiat. There’s no single company behind it, just smart contracts and community governance.

While DAI offers full on-chain transparency and avoids centralised custodians, it also comes with higher complexity and potential risks tied to smart contract bugs or extreme market conditions.

- USDT provides speed and simplicity, backed by a traditional corporate structure.

- DAI offers a decentralised alternative, ideal for DeFi-native users.

USDT vs BUSD

BUSD, once a major player backed by Binance and Paxos, was phased out in 2024 due to regulatory pressure. It serves as a reminder that centralised stablecoins depend on both market forces and compliance frameworks, and can be wound down unexpectedly.

While USDT remains standing, BUSD’s sunset reinforces the importance of evaluating who’s behind the stablecoin and how stable their operations really are.

What happens if Tether fails?

Let's play out a hypothetical scenario: what if USDT actually collapsed?

Given USDT's role as the primary trading pair and liquidity source for much of the crypto market, a Tether failure would be like removing a major highway from a city's transportation network. The immediate effects would likely include:

Market chaos: Traders scrambling to exit USDT positions would create massive selling pressure across crypto markets. We're talking about potentially the largest fire sale in crypto history, as billions of dollars worth of USDT holders try to convert to other assets simultaneously.

Liquidity crisis: Many smaller cryptocurrencies rely heavily on USDT trading pairs. Without this liquidity, some tokens might become effectively untradeable, at least temporarily.

Contagion effects: Other stablecoins might face runs as confidence in the entire sector erodes. Even well-managed stablecoins could struggle if everyone tries to redeem at once.

The silver lining: The crypto ecosystem has become more resilient over time. Alternative stablecoins like USDC have grown substantially, providing some redundancy. Additionally, the market has survived previous "extinction-level events" and adapted.

Conclusion: Is USDT worth the risk?

USDT isn’t perfect, but it’s proven its place in the crypto ecosystem. With high liquidity and global acceptance, it’s a practical choice for trading, payments, and short-term value storage.

However, concerns around transparency and regulatory clarity mean it’s not ideal for long-term holding or users who prioritise full visibility. But like any financial tool, its value depends on how you use it.

The smart approach is to understand the trade-offs, diversify across stablecoins, and align your choices with your goals and risk tolerance. As the space evolves, USDT remains useful, but it’s just one part of a broader digital finance strategy.

NEWS AND UPDATES

LATEST ARTICLE

.webp)

Picture this: Bitcoin soaring past previous all-time highs, altcoins experiencing triple-digit gains, and institutional money flooding into digital assets at unprecedented rates. Sound familiar? These are the hallmarks of crypto bull runs that have minted fortunes and reshaped entire industries.

But here's the trillion-dollar question: Is 2025 going to be the year of the next great crypto bull run?

Looking at the facts: Wall Street titans are accumulating Bitcoin through newly approved ETFs. Central banks worldwide are pivoting their monetary policies. Blockchain technology is finally delivering on its promises with real-world applications that extend far beyond simple speculation.

Meanwhile, a new generation of crypto projects is solving actual problems (from decentralising physical infrastructure to tokenising trillion-dollar asset classes).

While we’re witnessing a natural part of any market cycle; we're also observing the meeting of technological maturity, institutional acceptance, and macroeconomic conditions that historically precede the most explosive growth phases in cryptocurrency history.

Let’s explore whether the stage is being set for another “explosive” crypto bull run.

What defines a bull run in crypto?

A crypto bull run represents a sustained period of rising prices across digital assets, typically accompanied by increased trading volumes, heightened retail interest, and positive market sentiment.

Unlike traditional markets, crypto bull runs are often characterised by their intensity and duration, with assets sometimes experiencing gains of several hundred percent over relatively short periods.

Let’s use historical examples for reference: the 2017 bull run saw Bitcoin rise from under $1,000 to nearly $20,000, while the 2021 cycle pushed Bitcoin to over $69,000 and sparked unprecedented growth in alternative cryptocurrencies.

These periods were marked by mainstream media attention, institutional adoption milestones, and significant increases in new wallet creation and transaction volumes.

Key indicators of a bull market include sustained price appreciation across major cryptocurrencies, increased trading volumes, growing total value locked (TVL) in decentralised finance protocols, and heightened retail participation evidenced by exchange sign-ups and social media engagement metrics.

Is 2025 the next bull run year? Current market snapshot

The numbers tell a compelling story. Bitcoin has not only demonstrated remarkable resilience throughout 2025 but has done so while institutional demand reaches new heights. The spot Bitcoin ETFs launched in early 2024 continue to attract substantial capital inflows, creating a direct bridge between Wall Street and digital assets that simply didn't exist in previous cycles.

And this institutional momentum is rippling across the broader cryptocurrency ecosystem. Major altcoins have posted impressive year-to-date gains, while the regulatory pipeline remains packed with additional ETF applications, including potential products for XRP, Dogecoin, and other established digital assets. Each approval expands the on-ramp for traditional capital seeking cryptocurrency exposure.

Meanwhile, the underlying infrastructure is showing clear signs of renewed vitality. DeFi protocols have witnessed a resurgence in total value locked, signalling that users are actively deploying capital into decentralised financial services rather than merely holding tokens.

Exchange volumes have also consistently remained elevated compared to the bear market lows, indicating sustained engagement from both retail traders and institutional participants.

Perhaps most tellingly, this activity is occurring without the speculative frenzy that characterised previous market peaks, suggesting a more mature, sustainable foundation for potential growth ahead.

Top signals indicating a bull market in 2025

Several key indicators suggest the cryptocurrency market may be entering or approaching a bull phase in 2025. As mentioned above, institutional adoption continues to accelerate, with traditional financial institutions expanding their cryptocurrency offerings. The ongoing discussion around national Bitcoin reserves and sovereign wealth fund allocations also represents a significant shift in how institutions are thinking about digital assets.

Macroeconomic factors also appear supportive, with central bank policies potentially creating favourable conditions for alternative assets. And the expansion of global liquidity and discussions around interest rate trajectories could have an effect on investor appetite for higher-risk, higher-reward assets like cryptocurrencies.

Stablecoin market capitalisation has also grown substantially, serving as a proxy for capital ready to be deployed into crypto markets.

Looking at technical indicators, these suggest a potential shift from Bitcoin dominance toward increased altcoin activity, historically a characteristic of bull market phases. This rotation often signals broader market participation and the beginning of what market participants call "altcoin season."

People also asked: key questions around 2025's bull run

What is driving the 2025 crypto market recovery?

It’s not just hype, it’s momentum backed by major shifts. Spot Bitcoin ETFs have cracked open the door to institutional money, and regulatory clarity has turned question marks into green lights.

On top of that, governments are exploring Bitcoin as a treasury asset, and legacy industries are weaving blockchain into their tech stacks - and the result appears to be a market increasingly shaped by adoption, real-world applications, and broader institutional engagement.

Is it too late to invest in crypto in 2025?

Not necessarily. If historical patterns hold, there could still be opportunities within the current cycle, though past performance is not a guarantee of future results. Bear in mind that crypto markets tend to move in waves, and each wave brings fresh opportunities across different sectors and tokens.

With the market now more mature and diversified, investors are no longer limited to chasing just Bitcoin. Timing the top is nearly impossible, but missing the entire ride? That’s a choice.

What are the top altcoins to watch in 2025?

We’re not here to give financial advice. What we can encourage you to look out for are platforms demonstrating real-world usage, developer activity, and institutional partnerships, particularly ones that have garnered increased attention.

Let’s take a look at the developmental space as an example: Ethereum's continued evolution through its layer-2 scaling solutions, Solana's growing application ecosystem, and Cardano's academic approach to blockchain development represent different approaches to solving scalability and adoption challenges.

It's safe to say that investors in 2025 are paying close attention to utility, partnerships, and ecosystem depth, not just price charts.

Will regulation help or hurt the bull run?

Regulatory developments present both opportunities and risks for the cryptocurrency market. Clear frameworks can provide institutional investors with the confidence needed to allocate capital, while overly restrictive measures could dampen innovation and adoption.

The ongoing development of stablecoin regulations and international coordination on cryptocurrency policies will likely continue to influence market dynamics throughout 2025. Keep reading, keep staying informed.

Top narratives fueling the 2025 bull run

A range of powerful tech trends and adoption themes are currently driving renewed momentum in the cryptocurrency space. Here’s a closer look at what’s gaining traction:

The intersection of AI and blockchain

The integration of artificial intelligence and blockchain is opening up new frontiers with AI-driven applications built on blockchain networks, enabling more secure, transparent, and decentralised data processing.

This fusion is attracting significant venture capital and top-tier development talent, particularly in areas like decentralised machine learning, predictive analytics, and trustless automation.

Decentralised infrastructure: the rise of DePIN

Decentralised Physical Infrastructure Networks (DePIN) are creating new economic models for real-world infrastructure. By using blockchain incentives, these projects decentralise everything from wireless connectivity to energy grids.

Instead of relying on centralised providers, DePIN networks reward individuals and communities for building and maintaining critical infrastructure, laying the groundwork for more resilient systems.

Web3 gaming and the evolving metaverse

Web3 gaming continues to mature, shifting away from early speculation toward sustainable economic models and improved user experiences. Games are integrating NFTs and tokenised assets in ways that enhance gameplay, rather than distract from it. This evolution is drawing interest from both mainstream users and institutional investors, as gaming platforms begin to offer real value ownership and more immersive digital economies.

Tokenisation of Real-World Assets (RWAs)

Real-world asset tokenisation is becoming a key area of focus for both crypto-native projects and traditional financial institutions.

By bringing assets like real estate, bonds, and equities onto the blockchain, these initiatives are unlocking liquidity and improving access to previously siloed markets. This has the potential to bridge traditional finance (TradFi) and decentralised finance (DeFi), while creating more transparent, efficient systems for asset management and trading.

Scalability and utility: Layer-2s and liquid staking

Scalability and network efficiency remain essential to long-term adoption. Layer-2 scaling solutions (for example, rollups) are dramatically improving transaction speeds and lowering costs on networks like Ethereum, without compromising security.

At the same time, liquid staking protocols are enabling users to earn staking rewards while retaining access to their assets, making it easier to participate in network security without locking up funds. These solutions are pushing blockchain closer to mainstream usability.

Historical patterns: what past bull runs teach us

Cryptocurrency markets have historically followed cyclical patterns, often aligned with Bitcoin's four-year halving schedule. These cycles typically feature a period of accumulation following major price corrections, followed by gradual recovery and eventual explosive growth phases.

Analysis of past bull runs shows a thread of common characteristics, usually including progressive institutional adoption, mainstream media coverage, and the emergence of new use cases and applications. Technical indicators such as relative strength index (RSI) and exponential moving averages (EMA) have also been known to provide useful insights into market momentum and potential turning points.

The maturation of cryptocurrency markets has led to some evolution in these patterns, with increased institutional participation potentially leading to less volatile but more sustained growth phases compared to earlier cycles.

Risks and contrarian views

Despite positive indicators, there are, of course, several factors that could derail or delay a potential bull market. Regulatory uncertainty remains a significant risk, particularly regarding potential restrictions on cryptocurrency trading, staking, or mining activities. Changes in monetary policy or unexpected macroeconomic shocks could also redirect capital flows away from risk assets, as we’ve seen happen in recent months.

While the outlook for crypto in 2025 is promising, it’s important to stay grounded. History shows that periods of rapid growth can also attract speculative excess, which often leads to sharp corrections. Given crypto’s relatively small market size compared to traditional asset classes, it remains particularly sensitive to shifts in sentiment and large capital flows.

On the technology front, challenges still exist. Security vulnerabilities, scaling bottlenecks, or network failures can quickly erode trust, not just in individual projects, but across the ecosystem.

Meanwhile, the growing development of central bank digital currencies (CBDCs) presents a new kind of competition. Their potential to reshape how people interact with digital money could influence how (and where) cryptocurrencies find their place in the global financial system.

Final thoughts: How to prepare for a potential bull market in 2025

For those looking to enter or expand their position in crypto, education and risk management should take priority over chasing short-term gains. A clear understanding of how the technology works, how regulations are evolving, and what drives market cycles is essential to navigating this space with confidence.

Diversifying across different sectors, from infrastructure and DeFi to gaming and real-world asset tokenisation, can help balance risk while keeping exposure to growth potential. Just as important is keeping your assets secure in a market where transactions can’t be reversed.

Crypto is steadily moving toward institutional maturity, with greater regulatory clarity and more traditional players entering the market. That said, it remains a space defined by both innovation and volatility, factors that continue to attract interest from participants willing to engage with long-term uncertainty.

Whether 2025 becomes a landmark year for digital assets or simply another phase in a longer journey, the building blocks for long-term value are clearly taking shape.

Ultimately, success in this market often comes down to staying informed, staying patient, and having a strategy rooted in long-term thinking rather than short-term speculation. Crypto continues to reward those who approach it with diligence and discipline, especially when others are distracted by the noise.

If you're looking for a smart way to get more out of your money, here's a little insider tip: locking XTP tokens in the Tap app could be a game-changer. It’s a quick, no-fuss move that unlocks premium features, slashes your fees, and gives you access to exclusive perks (just for being a savvy user). We’re all about helping make your money work harder for you, without jumping through hoops.

Let’s talk about it: the power of premium tiers

Locking your XTP isn’t just about holding onto digital assets, it’s your key to real, everyday savings. Essentially, the more XTP you lock, the more perks you unlock. It really is just a straightforward tiered system that rewards you.

Real-world savings: where you'll see the difference

Lower trading fees

Every transaction costs less when you lock XTP for a premium account, creating significant savings for active traders. The higher your tier, the more you save on each trade, keeping more profits in your wallet where they belong.

Example: A trader making €10,000 in monthly transactions could save hundreds in fees annually by moving from Essential to Plus tier, and thousands by reaching Premier or higher tiers.

Cashback rewards that add up

Getting up to 8% Cashback on your purchases isn’t just a nice-to-have - it’s like getting a discount every time you spend. No extra steps, just more value back in your pocket.

- Coffee runs: Daily €5 coffee becomes €4.60 with the Prestige tier (8% back)

- Weekly groceries: €200 shopping trip returns €16 with Platinum tier (6% back)

- Major purchases: €1,000 electronics purchase gives you €40 back with Premier tier (4% back)

Even at the Plus tier (€300 worth of XTP locked), your 1.5% Cashback quickly adds up, especially for regular spenders.

Fee-free ATM withdrawals

Premium tiers include greater ATM withdrawal limits, saving you those pesky fees that add up quickly:

- Prestige: Unlimited free withdrawals

- Platinum: €1,000 free monthly withdrawals

- Other Premium Tiers: free monthly withdrawals up to €500.

This benefit alone can save hundreds annually for frequent travellers or cash users.

Foreign exchange rate advantages

As a premium member, you get access to exclusive exchange rates when you're travelling or shopping internationally. The higher your tier, the better the rates, meaning you can save big on every global purchase you make.

Maximising your XTP strategy

Step 1: Calculate your spending patterns

Analyse your monthly expenses across categories like everyday purchases, trading activity, and ATM usage to determine which tier offers you the best return on your locked XTP.

Step 2: Consider your lock-up timeline

The beauty of XTP locking is flexibility - you're not permanently parting with your assets but rather unlocking access to a full suite of premium features while still maintaining full control.. Note that the lock-in time frame is one year.

Step 3: Start your journey

Begin with a tier that matches your comfort level and upgrade as you experience the benefits firsthand:

- Download the Tap app and verify your account

- Buy your desired amount of XTP

- Select Upgrade from the bottom menu on the home screen

- Choose your desired plan and follow the instructions.

Additional premium perks

Your locked XTP doesn't just save you money, it elevates your entire financial experience:

- Priority support: Direct access to premium fast track assistance when you need it

- Higher spending limits: Up to €30,000 monthly card spending limits for Prestige members

- Exclusive market insights: Premium crypto market newsletters and insights

- Multi-currency capabilities: Seamless management of various currencies

The bottom line

Whether you're a casual user or power trader, there's a premium tier designed to put more money back in your pocket through reduced fees, enhanced Cashback, and exclusive benefits that add real value to your financial journey.

For those willing to stake their claim in the premium territory, the rewards are clear: reduced fees, elevated features, and an experience built for those who demand more from their money.

Galxe is a Web3 credential infrastructure platform transforming how digital identity and community engagement function within the blockchain ecosystem. By creating a decentralised platform where users can build, manage, and monetise their digital credentials, Galxe bridges the gap between blockchain projects, communities, and individual users.

In a digital landscape where trust and verifiable achievements are increasingly important, Galxe is here to provide a transparent, user-owned solution that allows both projects and participants to engage in meaningful ways. Let’s explore how Galxe is shaping the Web3 space.

TLDR

- Credential infrastructure: Galxe provides a decentralised platform for creating, managing, and monetising digital credentials.

- Community engagement: Enables blockchain projects to reward and incentivise user participation through verifiable achievements.

- Multi-chain support: Operates across multiple blockchain networks, enhancing interoperability and accessibility.

What is Galxe all about?

Galxe was founded in 2021 by Harry (Hay) Jiang and Kevin Wang to improve how digital identities and community contributions are recognised in blockchain networks. Traditional social and professional networks often struggle to reflect the decentralised nature of Web3 communities, and Galxe aims to bridge this gap.

The platform helps blockchain projects build stronger, more engaged communities by providing transparent and verifiable ways to reward user participation. Unlike traditional loyalty programs, Galxe’s credential system gives users full ownership of their achievements, ensuring a fair and user-focused approach to digital identity.

How does the Galxe platform work?

Galxe’s architecture revolves around several key components that work together to create a comprehensive credential ecosystem:

Credential Protocol

At the heart of Galxe is its Credential Protocol, which allows projects to design and issue both on-chain and off-chain credentials. These credentials represent a wide range of achievements, from completing specific tasks to maintaining long-term community participation.

The platform employs a decentralised storage mechanism for these credentials, ensuring they remain secure and resistant to centralised control or manipulation. Additionally, each credential is cryptographically signed, guaranteeing authenticity and preventing tampering.

GAL Token

GAL, the token for Galxe (formerly Project Galaxy), is an Ethereum-based ERC-20 token, meaning it operates on the Ethereum blockchain. The native token, used for both governance and utility, allows holders to vote on platform decisions, stake their tokens, and unlock various features.

Unlike regular utility tokens, GAL is designed to benefit everyone, from projects and developers to community members, by creating a fair and rewarding system for all.

Galxe ID

Galxe ID is a unique digital identity system that aggregates a user’s credentials across multiple blockchain networks. Think of it as a comprehensive, blockchain-based resume that showcases your Web3 journey and achievements. This identity system provides users with a portable and verifiable digital reputation, making it easier for them to leverage their credentials across different ecosystems.

How does Galxe protect user data and credentials?

Galxe prioritises user privacy and data security through several innovative ways:

- Decentralised storage: Credentials are stored across distributed networks, preventing single points of failure and ensuring long-term data integrity.

- Cryptographic verification: Each credential is cryptographically signed, which prevents tampering and guarantees authenticity.

- User control: Users have complete ownership over their credentials, deciding what to share and with whom. This approach eliminates reliance on centralised entities, giving individuals greater control over their digital identity.

The advantages of the Galxe platform

Galxe offers several compelling advantages for both blockchain projects and individual users:

- Enhanced community engagement: Projects can design targeted incentive programs that genuinely reward meaningful participation, increasing user retention and interaction.

- Portable identity: Users can carry their achievements across different platforms and blockchain networks, making their digital credentials more valuable and widely recognised.

- Monetisation opportunities: Developers can create credential-based marketplaces and innovative reward systems, enabling new economic models in the Web3 space.

- Low barrier to entry: The platform is designed to be user-friendly, with intuitive tools that make Web3 more accessible to newcomers without requiring extensive technical knowledge.

GAL use cases

The Galxe network supports a variety of use cases across different domains:

- Blockchain projects: Create loyalty programs, airdrops, and community engagement initiatives using verifiable credentials.

- NFT communities: Verify and reward active community members, improving engagement and long-term participation.

- DeFi platforms: Design reputation-based lending or staking mechanisms, reducing risks for both lenders and borrowers.

- Gaming: Implement achievement systems with real, transferable value, allowing players to monetise their in-game progress.

How to Buy GAL

Users looking to buy or sell GAL can do so through the Tap app, provided you have a verified account. Simply download the app, complete the account set-up and verification process, and begin trading GAL using your preferred crypto or fiat currency.

Conclusion

Galxe is a platform designed to enhance digital identity and community participation in the blockchain space. By offering a transparent, user-owned credential system, it allows projects and individuals to create verifiable digital experiences and correlate that information across the entire ecosystem.

As blockchain technology develops, credential-based systems like Galxe may play a pivotal role in shaping Web3 interactions. It provides tools for developers, project owners, and users to engage with blockchain ecosystems in a structured way.

We want to inform you that XTP trading will be temporarily paused starting today on the Tap app. We’ll be temporarily pausing XTP trading on the Tap app. This short pause will give us the time we need to complete the integration of ProBit, an exchange that continues to support XTP trading.

We sincerely apologise for any inconvenience caused by the Bitfinex delisting. XTP was removed alongside several other major tokens, and the short notice left limited time to implement an alternative solution. We moved quickly, and the integration with ProBit an exchange that supports XTP is already in progress.

Here’s what you need to know:

- XTP trading will be paused for a few days

- We’re integrating ProBit into our trading engine

- Once that’s done, XTP trading will resume as usual in the app

- We’re also in active talks with several other exchanges to expand access to XTP

We know how important XTP is to many of you, and it’s at the heart of the Tap ecosystem. Thank you for your patience and continued trust. We’ll keep you updated and let you know the moment trading goes live again.

The Tap Team

Dear Tap Community,

We want to share an important update regarding the XTP token and Bitfinex. As part of a broader internal review, Bitfinex has decided to delist several tokens, including XTP along with other notable projects like The Graph (GRT), Notcoin (NOT), and seven others as part of their platform review. This appears to be a broader shift in Bitfinex's listing strategy rather than something specific to XTP.

What’s Next for XTP

The good news? XTP remains at the heart of everything we do! 💙 Our token continues to power all the awesome features you love - our tier structure, rewards, and the entire Tap ecosystem. This change doesn't affect our exciting roadmap or our vision for the future.

Here’s what we’re doing to keep things moving forward:

ProBit Integration in Progress:

Our dev team is already working on integrating ProBit (where XTP currently trades) into our Trading Engine. This will create a seamless trading experience right within our platform!

New Exchange Adventures:

We're in exciting talks with several exchanges to give XTP even more trading homes! While we need to keep the details under wraps for now (those NDAs, am I right?), know that we're pushing hard to create more options for our community.

Community First:

Remember to withdraw your tokens from Bitfinex before July 15, 2025, if you haven't already. We're here to help if you need guidance on this!

The Road Ahead 🛣️

Even in challenging markets, we see incredible opportunities for growth! Here's what's cooking:

- More XTP Utility: We're whipping up new ways for XTP to shine in our ecosystem

- Cool New Features: Q2 is going to bring some exciting platform upgrades

- Let's Talk More: We'll be sharing updates more frequently so you're always in the loop

We're so grateful for this amazing community! 🙏 Together, we've weathered challenges before, and we'll come out stronger this time too. The crypto landscape is always evolving, and we're evolving with it.

We’re deeply invested in the future of XTP - and we’re just getting started. 👏

The Tap Team

.webp)

70% of consumers prefer brands that make loyalty easier - card-linked programs make this process seamless. In today’s fast-moving market, forward-thinking businesses are leveraging co-branded payment cards to boost customer loyalty, increase lifetime value, and, as a bonus, unlock new revenue streams.

Whether you’re in retail, travel, fintech, or beyond, co-branded cards offer a strategic, low-risk way to deepen customer relationships and expand your brand’s financial ecosystem - without the heavy lift of building payment infrastructure from scratch.

In this guide, we’ll break down what co-branded cards are, why they’re a game-changer for businesses, and how you can implement one to drive growth.

What are co-branded cards?

Co-branded cards are payment cards that merge two brands: your business and the financial institution that issues the card. Unlike traditional credit or debit cards that solely display the bank's branding, co-branded cards prominently showcase your company's identity through logos, colours, and design elements that reinforce brand recognition with every transaction.

These customised financial products can take various forms—debit cards, prepaid cards, or even digital payment solutions—all carrying your brand's distinct identity at the forefront of Tap’s financial infrastructure.

Why co-branded cards drive business growth

The strategic advantages of co-branded cards extend far beyond simple brand visibility:

Enhanced customer loyalty is perhaps the most significant benefit. By offering exclusive rewards, discounts, or perks tied directly to your products or services, co-branded cards incentivise repeat business while creating emotional connections with cardholders.

Revenue diversification comes through interchange fees, where businesses receive a percentage of each transaction made with the card. This creates a passive income stream completely separate from your core offerings.

Valuable customer insights are another bonus that emerges from transaction data (within regulatory compliance), providing unprecedented visibility into spending patterns and preferences. These insights can inform product development, marketing strategies, and shape personalised offers.

How co-branded cards work

Co-branded cards are successful when each entity works in harmony with the others. Below we break down the various elements of the strategic partnership:

Role of the retailer, financial institution, and payment network

Each partner in a co-branded card arrangement brings unique capabilities to the table. The retailer or brand contributes its customer base, loyalty program infrastructure, and distinctive rewards offerings tied to its products or services.

Meanwhile, the financial institution handles the critical banking functions (underwriting, credit approval, payment processing, and regulatory compliance) leveraging its expertise in financial services management.

Completing this ecosystem, payment networks provide the technical infrastructure that enables worldwide acceptance, transaction security, and fraud protection.

This three-way collaboration creates a seamless experience where consumers simply see and interact with their favourite brand, while sophisticated financial operations run invisibly in the background.

Open-loop vs closed loop cards

Co-branded cards typically fall into two major categories that determine their versatility and reach:

Open-loop cards function anywhere the payment network (Visa, Mastercard, etc.) is accepted, giving cardholders maximum flexibility to earn rewards regardless of where they shop. This widespread acceptance makes these cards particularly attractive for everyday spending beyond the brand's own ecosystem.

Closed-loop cards, on the other hand, can only be used at specific retailers or within a limited network of businesses. While more restrictive, these cards often deliver enhanced rewards and benefits when used within their designated ecosystem, creating powerful incentives for loyal customers to concentrate their spending with the brand.

Common types of co-branded cards

The co-branded card landscape spans numerous industries, with each sector leveraging unique value propositions to attract and retain customers:

Travel-based (airlines, hotels, cruise lines)

Travel co-branded cards are a perfect example of the potential of strategic partnerships. Airline cards typically offer accelerated miles earning on ticket purchases, free checked bags, priority boarding, and pathways to elite status.

Hotel cards similarly provide point accumulation for property stays, automatic status tier upgrades, and free nights each year, while cruise line cards offer perks like onboard credits, discounts, and exclusive experiences for cardholders

The common thread connecting these offerings is their ability to transform ordinary spending into exceptional travel experiences, creating emotional connections far stronger than traditional rewards programs.

Retail-based (Amazon, Walmart, department stores)

Retail giants leverage co-branded cards to deepen their relationship with frequent shoppers. These cards typically feature enhanced cashback or points on purchases made within their stores or websites, special financing options for larger purchases, and exclusive cardholder events or early access to sales.

E-commerce leaders like Amazon have revolutionised this space by combining digital-first experiences with substantial rewards on platform purchases, creating a virtuous cycle that drives both card usage and marketplace spending.

Fuel & auto-related cards

Targeting specific spending categories, fuel and automotive co-branded cards deliver maximum value in areas where consumers have consistent, necessary expenses. These offerings typically feature significant rebates on fuel purchases, maintenance services, and automotive accessories, sometimes with tiered rewards that increase with spending volume.

For frequent drivers or commuters, these specialised cards transform unavoidable expenses into meaningful rewards, building brand loyalty through practical everyday savings.

Pros & cons of co-branded cards

As with any financial product, co-branded cards come with distinct advantages and considerations that businesses should evaluate against their strategic objectives:

Pros: rewards, discounts, brand perks, status upgrades

The rewards ecosystem represents perhaps the most compelling advantage for consumers. Co-branded cards typically offer accelerated earning rates on brand-specific purchases, creating a powerful incentive for cardholders.

Beyond points and cashback, exclusive discounts available only to cardholders create a sense of "insider status" that deepens brand affinity. Many programs also include unique perks tailored to the brand experience, for example: priority services, exclusive access, or enhanced customer support, that transform the traditional transaction into a premium relationship.

For aspirational brands, especially in travel and luxury sectors, status upgrades included with card membership provide a taste of premium experiences that often convert customers into long-term brand advocates.

Cons: high APRs, limited redemption, brand lock-in

Despite their advantages, co-branded cards typically carry higher interest rates than no-frills financial products. For customers who occasionally carry balances, these elevated APRs can potentially offset the value of earned rewards.

Redemption limitations also present potential friction points. Many programs restrict how and where rewards can be used, creating occasional frustration when consumers encounter blackout dates or availability constraints, particularly in travel-focused programs.

Perhaps the most significant strategic consideration is brand lock-in risk. Tying rewards too exclusively to your own ecosystem might boost short-term engagement but could create vulnerability if competitive offers emerge or if your brand experiences challenges. The most sustainable programs balance brand-specific value with flexibility that acknowledges diverse consumer needs.

By carefully weighing these factors against your business objectives and customer preferences, you can design a co-branded card program that delivers meaningful value while avoiding common pitfalls that undermine long-term success.

Ensure that you understand the particular offerings of the card program management system you intend on using to see how these cons might affect your decisions.

How to implement a successful co-branded card program

Launching an effective co-branded card initiative requires partnering with the right provider - one offering white-label solutions that can be customised to your specific needs while handling the complex regulatory and operational requirements.

The implementation process typically involves:

- Designing card aesthetics that reinforce your brand identity

- Creating a compelling rewards structure aligned with your business goals

- Developing marketing strategies to drive card adoption

- Establishing systems to track program performance

The most successful programs treat co-branded cards not as mere payment tools but as extensions of their customer experience strategy.

With Tap, we work closely with the company launching the product, from an intricate overview of the process to ironing out the finer details to handling all technical and regulatory elements. Contact us here for a clearer look at how your business can leverage the benefits of co-branded cards.

Why now is the time to consider co-branded cards

As digital transformation accelerates across industries, the companies that create seamless, value-added experiences for customers gain significant competitive advantages. Co-branded cards represent a unique opportunity to extend your brand presence into your customers' everyday financial lives.

With flexible white-label solutions now available, businesses of all sizes can implement sophisticated card programs without massive infrastructure investments. The barrier to entry has never been lower, while the potential benefits remain substantial.

Whether your goal is strengthening customer relationships, opening new revenue channels, or gathering deeper customer insights, co-branded cards offer a versatile solution that delivers across multiple business objectives.

By partnering with the right payment solution provider, you can transform ordinary transactions into powerful brand touchpoints - converting each swipe, tap, or digital payment into another opportunity to reinforce your relationship with customers, and potentially earn revenue too.