November 2025 could be a turning point for crypto. From ETFs to major network upgrades, here are six catalysts that could shape the market.

Keep reading

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

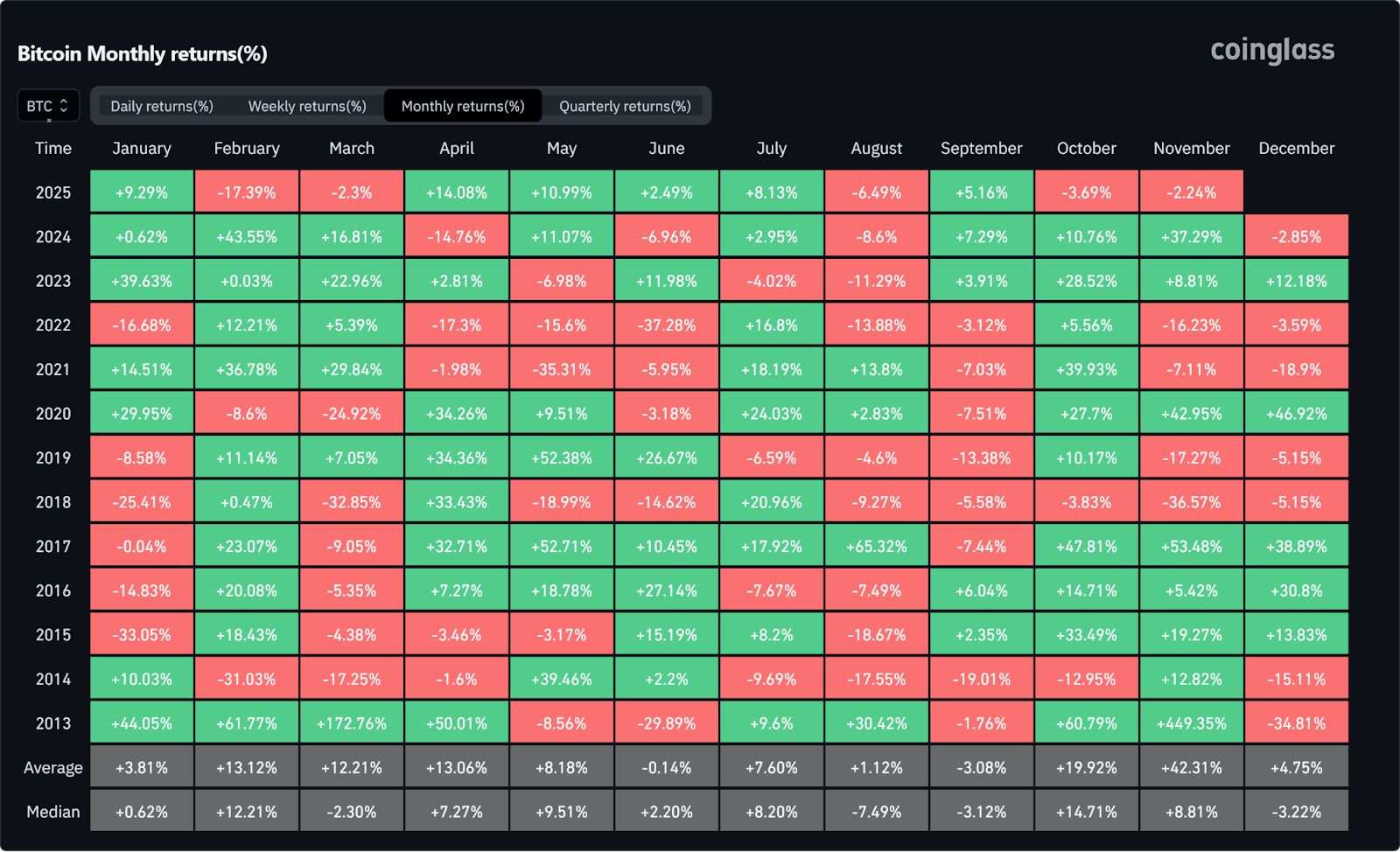

1. Seasonality & Historical Momentum Could Kick In

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

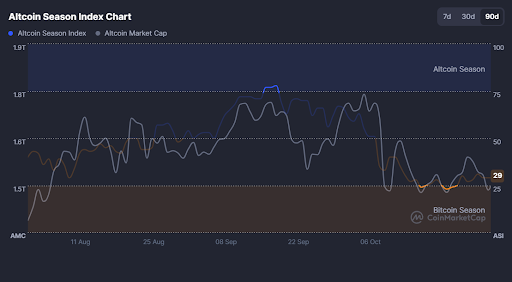

4. Altcoins at an Inflection Point

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

NEWS AND UPDATES

LATEST ARTICLE

Solana is a high-performance blockchain that uses a unique consensus mechanism to achieve high throughput and security. Thanks to its user-friendly nature, the platform is already being used by major companies. As we explore what Solana (SOL) is, we take a look at the project's intentions, successes, and of course why it is often referred to as the leading "Ethereum killer".

Since Bitcoin was created in 2009 an entire crypto ecosystem has emerged, valued at almost $1.2 trillion at the time of writing. While Bitcoin was designed to provide a global payment system to address problems in the traditional financial sector, other platforms like Ethereum and now Solana have been created to facilitate the development of the blockchain industry as a whole through programmable functionalities.

What is Solana (SOL)?

Recognised as being one of the fastest-growing protocols in the DeFi space, Solana offers a platform for developers to build decentralized applications (dapps) and smart contracts, similar to Ethereum. However, what sets Solana apart is its remarkable speed and lower transaction fees.

The project is led by two main entities: the Solana Foundation, a non-profit organization based in Switzerland, focuses on promoting the platform and collaborating with international partners; and Solana Labs, located in San Francisco, takes charge of driving the project's development.

Solana implements a unique approach to support a more environmentally friendly crypto ecosystem. While it utilizes a Proof-of-Stake consensus mechanism to maintain its operations on the platform it also utilises an innovative consensus mechanism called Proof-of-History (PoH), created by one of its founders.

PoH is groundbreaking in the blockchain space, allowing the network to process an impressive 65,000 transactions per second. For context, Ethereum can process 30 transactions a second. PoH is described as being a "timekeeping technique to encode the passage of time within the data structure."

Renowned for being one of the fastest programmable blockchains in the cryptocurrency world, Solana has built a dedicated following. This is evident from the wide range of businesses, from finance to travel, using the platform and the strong interest in SOL tokens, the platform’s native coin.

Key features of Solana

Setting itself apart in the industry and making it a hit among the investor community, Solana offers these key features:

Scalability

The platform is able to handle thousands of transactions per second (TPS), using advanced technologies like parallel processing and mempool-based TPUs for scalability.

Smart contracts

Solana supports smart contracts, allowing developers to create and operate decentralized apps.

Proof of Stake (PoS) consensus

It's unique PoS consensus combines Proof of History (PoH) for speedy transactions, quick validation, and swift block confirmations.

Decentralized finance (DeFi)

Solana's fast, low-cost transactions make it a DeFi favourite, facilitating lending, trading, yield farming, and more.

Who created Solana?

Software engineer, Anatoly Yakovenko, is responsible for creating the Solana platform. He started working on the blockchain project in 2017, three years prior to its launch, alongside his former colleagues, Greg Fitzgerald and Eric Williams. They teamed up with several other former colleagues and together built the programmable network we know today.

Anatoly Yakovenko is also credited with developing the PoH protocol, an innovative contribution to the blockchain space that allows for greater scalability, thereby boosting usability. His expertise has been influential in the industry.

How does Solana differ from Ethereum?

One of the platform's main aims is to improve on several of the Ethereum platform's computing functionalities. Solana stands out by making transactions really fast, while also improving how much the system can handle, scalability, and cost structure. This makes Solana a top choice for efficiency and performance in the world of blockchain.

Scalability

While the project's leads say that Solana will process up to 700,000 transactions per second (TPS) as the network grows, it can currently handle around 65,000 TPS, still a far cry from Ethereum's 30 TPS.

Solana is one of the few layer-one solutions from a computing platform that is able to support thousands of transactions per second without the use of off-chains or second layers.

Cost

Due to the nature of the Solana network, it is able to provide much more cost-effective transactions, generally costing around $0.000125 per transaction. 75% less than that of Ethereum, $0.0005 per transaction at the time of writing.

What is SOL?

SOL is the native cryptocurrency to the Solana platform powering its scalability and reduced cost structure. The cryptocurrency acts as a utility token, used to pay for transactions on the network and to secure the network through staking.

SOL is a proof-of-stake cryptocurrency, which means that it is secured by network participants who stake their SOL tokens. The price of SOL is impacted by conventional factors like project updates, investment market sentiment, exchange activity, and the overall economy, alongside variables such as the token's inflation rate, burning amount, and the expansion of the Solana ecosystem.

How Can I Buy SOL?

If you're looking to diversify your crypto portfolio with the likes of Solana, you’ve come to the right place. Tap allows users to seamlessly buy, sell, trade, and store SOL through the convenience of the Tap app. Using crypto or fiat money, users can tap into this growing market and become part of the Solana-driven blockchain revolution. For more content on how to trade Solana, see here on the Tap website.

Risk in trading is the chance that something might negatively impact an investment. Before engaging in any trading activities it is important to evaluate your appetite for risk, determining whether you are able to handle more risk or are more risk averse.

Measuring risk will be dependent on the type of asset you are investing in, the amount of capital you have to use, and the time frames in which you expect to see results. Different assets and trading strategies hold different amounts of risk.

For example, investing in an index fund is considered a low-risk investment and is better advised to investors looking to make a slow and steady return over a longer period of time. Index funds aggregate the performance of the 100 companies listed on a particular stock exchange and pay back dividends accordingly. Because they are large companies the growth is often more likely to be smaller yet consistent.

With a little more appetite for risk, in the crypto markets, the same could be said about choosing to invest in an emerging altcoin versus established cryptocurrencies like Bitcoin or Ethereum. An emerging asset would encompass a higher risk higher reward ratio, however, no returns are guaranteed.

You can speak to a financial advisor to get a sense of your risk appetite.

Slippage is a natural part of trading that happens when there’s a difference between the price you expect to pay for an asset and the price you actually get. It’s common across all markets, from crypto to forex, stocks, and commodities, and it reflects the gap between your order request and the execution price.

Understanding how slippage works helps investors manage expectations, avoid unnecessary losses, and choose smarter trading strategies. In this guide, we’ll explore what causes slippage, how to calculate it, and how to minimize its impact in real trading scenarios.

What Is Slippage In Trading?

Slippage is when an investor opens a trade but between creating the trade and executing the trade; the price changes due to price movements in the greater market. This can often be a costly problem in the financial sector and particularly when trading digital currencies on crypto exchanges.

How Does Slippage Occur?

The two main causes of slippage are volatility and liquidity, outlined in more information below.

Volatility is when the price changes rapidly, as is common in cryptocurrency markets, and as a result the price changes between the time of creating the buy or sell order and the time of execution.

Liquidity concerns on the other hand are when the coin you are trading is not traded very often and the range between the lowest ask and the highest bid is wide. This can cause sudden and dramatic price changes, resulting in slippage. Fewer people trading an asset results in fewer asking prices, resulting in less favourable prices.

This is common among altcoins with low volume and liquidity. While slippage can occur in forex and stock markets too, it is much more prevalent in crypto markets, particularly on decentralized exchanges (DEXs).

There are two types of slippages:

Positive Slippage

Positive slippage is when a trader creates a buy order and the executed price is lower than the price initially expected. This will result in the trader getting a better rate. The same is true for a sell order that experiences a higher price point at trade execution, resulting in more favourable value for the trader. Positive slippage banks profits.

Negative Slippage

Negative slippage is when the trader loses out on the trade, with the price of the buy order higher than expected at the time of execution. The opposite is true for sell orders, meaning that the execution price is lower at the time of execution, similarly resulting in losses for the trader..

How To Calculate Slippage

Slippage can be calculated in two ways, either in dollar amount or percentage. Although to work out the percentage, you will first need the dollar amount. This is calculated by subtracting the price you expected to pay from the price you actually paid. This amount will indicate if you incurred a positive or negative slippage.

Most exchanges express this amount in percentages. This is calculated by dividing the dollar amount of slippage by the difference between the price you expected to get and the limit price. Then multiply that by 100.

Slippage Example in Practice

Imagine you plan to buy 1 BTC for $50,000, but by the time your market order executes, the price has risen to $50,250. You’ve experienced negative slippage of $250.

Now imagine you place a limit order at $50,000, and the order executes at $49,900, that’s positive slippage, meaning you paid less than expected.

To calculate slippage:

Slippage amount = Executed Price − Expected Price

Slippage percentage = (Slippage ÷ Expected Price Difference) × 100

For example, if your expected buy was £50,000 and you paid £50,250, slippage = £250 (0.5%).

This simple math helps traders evaluate execution quality and whether slippage is within acceptable limits.

Slippage Across Different Markets

Crypto Markets:

Crypto markets operate 24/7 and can swing several percent in seconds. On decentralised exchanges (DEXs) like Uniswap, prices depend on liquidity pools; so if liquidity is low, large trades can move the price dramatically. Tokens with small trading volumes, like new altcoins, are particularly prone to high slippage.

Forex Markets:

In the foreign exchange market, slippage often occurs during news releases (e.g., interest rate decisions). Liquidity is usually high, but during volatile moments, even major pairs like GBP/USD can slip several pips.

Stock Markets:

Stock slippage tends to appear at market open or close, when volatility spikes. During major events (earnings reports, Fed meetings) even large-cap shares can gap before orders fill.

Across all asset classes, slippage is most noticeable during low liquidity or high volatility, two conditions traders should always monitor.

How To Avoid Slippage

While one can't eradicate slippage entirely, there are several measures one can take to better manage slippage, as regularly falling victim to negative slippages can result in losing a lot of money.

Create limit orders:

Instead of creating market orders, traders can instead create limit orders as these types of trades don't settle for unfavourable prices. Market orders are designed to execute a trade service as quickly as possible at the current available price.

Set a slippage percentage:

Traders can create a slippage percentage that eliminates trades happening outside of the predetermined range. This can range from 0.1% to 5%, however, if the slippage percentage is too low this could lead to the trade not being executed and the trader missing out on large drops/jumps.

Understand the coin's volatility:

When in doubt, get educated. Learn about the coin's volatility as well as the volatility on the trading platform you are using. Understanding more about previous patterns can assist in making more informed decisions on when to open and close a position, and avoiding negative slippages.

Bottom Line

Slippage is inevitable but manageable. Whether you’re trading crypto, forex, or equities, some gap between expected and actual execution is normal. The goal isn’t to eliminate slippage, but to understand it, anticipate it, and minimize unnecessary exposure.

By combining timing awareness and education, traders can protect profits and execute more confidently, even in fast-moving markets.

An unpredictable trend emerged in 2021 where dog-themed cryptocurrencies made a barking appearance, with Shiba Inu gaining much of the spotlight (and the value). Originally labelled a meme token, the network had much more in store for its increasingly growing following on the internet. As we explore what Shiba Inu is and how it originated, you can learn the ropes about one of the digital money coins with the biggest gains in market cap 2021.

When it came to crypto investing in 2021 the community was largely behind meme tokens. Heavily influenced by the likes of Elon Musk, Dogecoin and other spin-off cryptocurrencies saw an impressive increase in market value. As the main rival to Dogecoin, Shiba Inu is worth knowing about.

What is the Shiba inu coin?

Stemming from the logo of Dogecoin based off of a Shiba Inu dog from a meme, Shiba Inu was designed with the same dog in mind. The decentralized network was originally created in 2020 as an alternative to Dogecoin, but based on the Ethereum network.

The coin behind the network, SHIB, is based on an ERC-20 token standard and is only a small offering of the Shiba Inu network. There is also an exchange called ShibaSwap, where users can trade SHIB and other cryptocurrencies. Utilizing many dog references, the project's "woofpaper" (whitepaper) explains that users can also "bury" the tokens in smart contracts to earn interest, "dig" in the Puppy Pools to provide liquidity and utilize the networks other two tokens, Doge Killer (LEASH) and Bone ShibaSwap (BONE).

There is also an NFT game called Shiboshi Game and an NFT art incubator called Shiba Artist Incubator.

Why has Shiba inu been so popular?

After launching in 2020 the coin was dubbed the "Dogecoin killer" and gained mass interest on social media platforms (as well as the mainstream news). In early 2021, Coinbase added the coin to its list of supported cryptocurrencies prompting investors to send the price soaring over 40% in just two days. 2021 saw unbelievable gains for SHIB, including its ranking in the top 10 biggest cryptocurrencies by market cap.

Following a string of media announcements concerning Dogecoin (largely by Tesla founder Elon Musk), the platform leveraged on its mentions and in November 2021 recorded gains of over 60,000,000% since January of that same year. While Musk has mentioned SHIB on Twitter he has admitted to not actually owning any.

Who created Shiba inu?

Shiba Inu was created by an anonymous entity going by the name of Ryoshi, much like Satoshi Nakamoto behind the creation of Bitcoin. The network has an interesting story behind its total supply, with 1 quadrillion tokens minted at launch. It currently has a circulating supply of 549 trillion SHIB coins.

Ryoshi decided to lock 50% of the total supply in Uniswap for liquidity purposes and sent the remaining 500 trillion SHIB to Ethereum founder Vitalik Buterin. Buterin went on to burn 90% of his share and donated the remaining 10% to a Covid relief fund in India. This burning event saw an increase in market price, and of course, gained much media and website attention within the crypto community.

How does Shiba inu work?

The ShibSwap platform itself operates as a decentralized exchange, with earning capabilities via interest-bearing smart contracts. SHIB can be traded much like any other cryptocurrency and can be stored in any wallet that supports ERC-20 tokens.

The LEASH token was originally designed as a stablecoin linked to the Dogecoin price but was later changed to an ERC-20 token that allows users to stake their tokens in the liquidity pool and earn xLEASH as rewards.

The BONE token on the other hand is a governance token that is designed to provide users with voting rights on upcoming proposals on Doggy DAO.

The platform also launched 10,000 "Shiboshi" NFTs on the Ethereum blockchain in October 2021, made available for trade.

While it is often referred to as a rival to Dogecoin, the network presents many more use cases than simply a digital money system.

What is SHIB?

SHIB is the native cryptocurrency to the Shiba Inu platform. Currently (at the time of writing) holding a position in the top 20 biggest cryptocurrencies based on market cap, Shiba Inu has seen impressive results in the two years it has been on the market.

Where can I get Shiba inu?

To get your hands on SHIB you can simply buy the cryptocurrency through your Tap app. Using a range of cryptocurrencies and fiat currencies on offer, users can simply execute the trade and store of the SHIB in the unique wallet linked directly to your account.

Risk management involves identifying and analysing the risks involved, and then choosing whether to accept this risk or make changes to avoid the risk. This process is one we carry out daily, from crossing the street to engaging with a stranger, however, in this realm we’re looking at it from a finance/investment point of view.

If you have a fund manager or financial adviser, they will generally be responsible for calculating and communicating the risks associated with any type of investment. This will cover the potential returns as well as the potential risks to your capital.

For example, investing in an emerging asset will hold a lot more risk than buying the stocks of a well-established institution. It’s worth noting that high risk doesn’t necessarily equate to a negative, typically assets with higher levels of risk bring about higher levels of return (high risk, high reward).

Each person’s level of risk will vary from one to another and should be decided prior to making any investments. Once this is established, your investment portfolio will work within those realms so as to manage that level of risk.

A common go-to for investors looking to diversify their crypto portfolios, Ripple is arguably one of the most interesting cryptocurrencies. With plenty of controversies and headline visibility, Ripple is pioneering a new path for cryptocurrencies and receiving as much acclaim as it is backlash. Let’s explore what is Ripple (XRP) and why it’s often caught in the spotlight.

What Is Ripple (XRP)?

When understanding what Ripple is it is necessary to understand the three pillars:

- Ripple Labs is the company managing the various products available.

- RippleNet is the network that facilitates global payments between financial institutions that operate on top of the distributed ledger database called XRP Ledger.

- XRP is the cryptocurrency fueling the network and providing a more cost-effective and faster means of transacting money.

In essence, Ripple is a digital payments platform that facilitates faster and cheaper international payment settlement, remittance systems, and asset exchange. The company provides several products catering to a wide range of financial institutions, essentially building a bridge between the blockchain world and the traditional financial sector.

Ripple is not based on blockchain technology, and instead uses proprietary distributed ledger technology. It was designed to provide a digital monetary payment alternative to the likes of SWIFT, catering to international and remittance markets.

What is XRP?

Launched in 2013, 100 billion XRP were minted and to date 52 billion are in circulation. These coins remain in the custody of the company and are released into the system gradually (using a different mechanism to mining).

While XRP is the native coin to the XRP Ledger, the distributed ledger technology can facilitate transactions in multiple currencies. XRP is used to provide a quick conversion between currencies.

History of XRP

Ripple was first conceived as an online payments company in 2004 by Ryan Fugger in Vancouver. Several years later and with the advent of cryptocurrencies, two developers approached Fugger to merge their concepts and create a cryptocurrency of their own. As a result, OpenCoin was established in 2012 by Chris Larsen and Jed McCaleb, with Fugger on the team.

In September 2013, OpenCoin became Ripple Labs, which was later rebranded to Ripple in 2015. A year later, the company received one of four Bitlicences, a licence required by the state of New York to provide virtual currency activities.

How does Ripple work?

Ripple uses a more complex means of maintaining the network, dissimilar to how other cryptocurrencies like Bitcoin and Ethereum operate. The RippleNet’s ledger is essentially maintained by the XRP community and can process transactions every 3-5 seconds.

The network is made up of independent validator nodes which verify transactions through a consensus. These nodes are typically made up of a long list of financial institutions, universities and companies outside of the blockchain realm.

The payment system provides products and services to payment companies around the world and has been integrated into banking systems to improve outdated fiat processes.

For instance, Ripples’s xCurrent technology was used to launch One Pay FX, a mobile app for international payments from the Spanish banking group Santander. It was also used to power MoneyTap, a mobile app in Japan that effectively connected 61 banks on a mobile app to facilitate domestic payments. Ripple’s products are consistently being implemented around the world.

Ripple and the SEC

In 2020 one of the biggest lawsuits in the crypto world was ignited when the U.S. Securities and Exchange Commission (SEC) filed a lawsuit against Ripple and two executives claiming that they violated investor protection laws. The SEC barred all US exchanges from trading XRP immediately, and a lengthy court case began.

The court case revolves around whether Ripple is a security, with the SEC claiming the company unlawfully raised $1.3 billion in an unregistered security offering. As the case continues, each party has had their fair share of triumphs and blows, and the case is set to create a precedent for future cryptocurrency trials of similar nature.

This landmark case has been significant in the crypto world due to its potential implications for other cryptocurrencies. If the SEC's view that XRP is a security, rather than a currency, prevails, then other digital currencies could also potentially be classified as securities, subjecting them to additional regulation.

In a recent ruling in the three year case, the U.S. District Judge Analisa Torres ruled that XRP was “not necessarily a security on its face,” partially contradicting the SEC’s claims, and that the company did not break federal securities laws by selling XRP on public exchanges.

The recent decision made by Torres marked the first major triumph for a cryptocurrency firm in a lawsuit filed by the SEC. However, it is important to note that the SEC also achieved a partial success in the case with the judge stating that a portion of the token sales to institutional buyers did qualify as securities transactions.

While the SEC reviews the rulings, Ripple Chief Executive Brad Garlinghouse said that the ruling was "a huge win for Ripple but more importantly for the industry overall in the U.S."

Ripple vs Bitcoin

When comparing XRP with the first and biggest cryptocurrency, Bitcoin, one must understand their different use cases.

Bitcoin was designed to provide the world with a digital peer-to-peer payment system and store of value while XRP was designed to facilitate international transactions providing a faster and cheaper alternative to fiat transactions.

While Bitcoin was created to be decentralized and exempt from government and banking controls, Ripple is designed to include the centralized banking sectors in the benefits of the cryptocurrencies and provide them with the services to facilitate these benefits.

While Bitcoin uses the process of mining through a Proof-of-Work consensus, Ripple uses a network of validators that are established outside of the cryptosphere. Its consensus system is designed to make transaction verification faster and, in the process, uses less energy.

How To Buy XRP

If you’re interested in incorporating XRP into your crypto portfolio, look no further than Tap. As a recent addition to the Tap mobile app, XRP can be bought, sold, traded and stored on the app securely and conveniently.