November 2025 could be a turning point for crypto. From ETFs to major network upgrades, here are six catalysts that could shape the market.

Keep reading

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

1. Seasonality & Historical Momentum Could Kick In

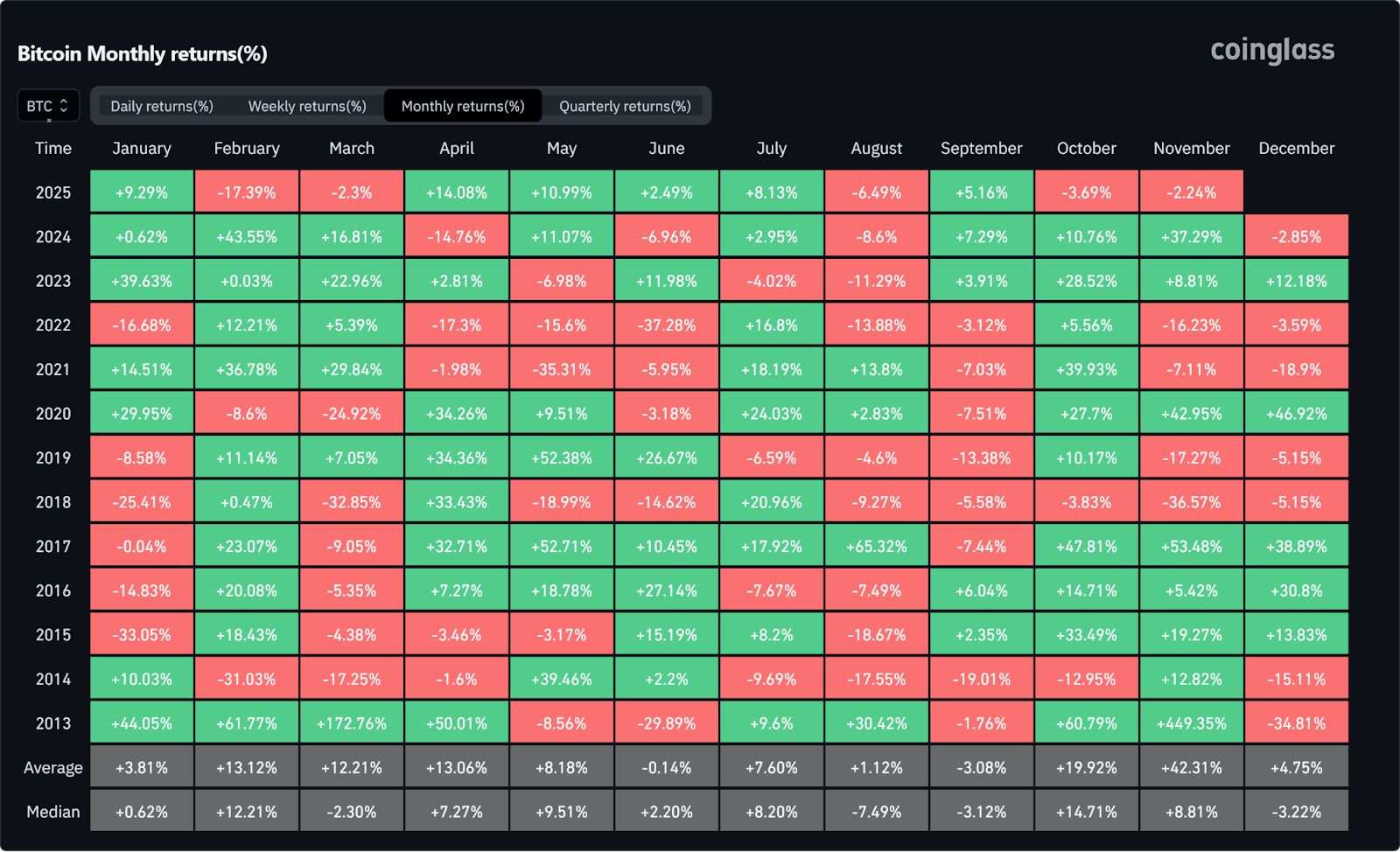

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

4. Altcoins at an Inflection Point

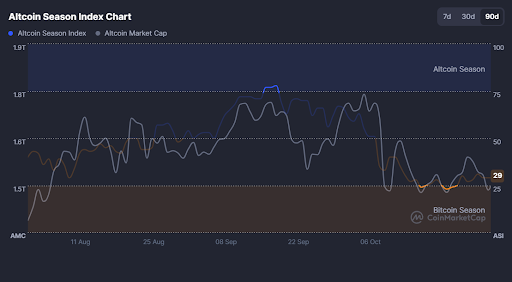

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

NEWS AND UPDATES

LATEST ARTICLE

In a fast-changing world where money moves instantly and borders are fading, Tap stands out as a pioneering fintech platform that unites traditional banking with cryptocurrency management.

Founded in 2019, Tap’s goal is to simplify how people store, send, and spend both fiat money and digital assets, all from one secure, user-friendly app. The platform’s native ERC-20 token, XTP, powers an integrated ecosystem where users can trade, earn rewards, and unlock premium benefits.

More than a digital wallet or an exchange, Tap represents a bridge between two worlds: the speed of decentralized finance and the reliability of traditional finance. Whether you’re new to crypto or looking for smarter ways to manage global payments, Tap helps users stay in control without complexity.

XTP is what holds that bridge together. Here’s how.

How Does Tap Work?

At its core, Tap combines traditional money management and modern crypto services into a single, intuitive platform. Built for flexibility and ease, and as a solution to the founder's initial problem, our platform allows users to manage both fiat and digital currencies from a single interface, without needing multiple tools or accounts.

Once verified, users unlock access to Tap's multi-currency wallets, which support 60+ cryptocurrencies alongside major fiat currencies. Crypto can be bought using bank transfers or debit cards, and external wallets can be connected to bring funds into the platform. Users can also sell crypto and withdraw fiat directly to their bank account, or use any funds within the app to pay external bank accounts.

One of Tap's standout features is its Tap Mastercard, available in both physical and virtual formats. The card connects directly to your Tap wallet, letting you spend crypto or fiat in real time, taking care of currency conversions behind the scenes. It works globally for ATM withdrawals and in-store or online purchases, with competitive FX rates and no hidden surprises. Depending on the user’s tier, transactions can earn up to 8% Cashback, making Tap practical for daily use.

Last but not least, Tap allows for instant crypto-to-fiat conversion. That means no waiting, no manual exchanges, and no disruption at checkout ; your digital assets are as spendable as your local currency. All transactions are protected with advanced security features and encryption, keeping your money and data safe every step of the way.

Key Features That Make Tap Unique

Tap distinguishes itself in the crowded fintech landscape through several innovative features that address real-world financial challenges.

The platform's instant transfer capability within the Tap2Tap network allows users to send money and cryptocurrencies to other Tap users completely free of charge, honoring Bitcoin's initial peer-to-peer intention and making international remittances more accessible than ever before.

Real-time transaction alert system

The real-time transaction alert system ensures users maintain complete visibility over their financial activities. Every transaction, whether it's a crypto purchase, card payment, or fund transfer, triggers immediate notifications, providing peace of mind and enabling proactive account management.

Debit card directly linked to account

Global accessibility represents another cornerstone of Tap's unique value proposition. The integrated Mastercard enables ATM withdrawals and purchases worldwide, while the platform's foreign exchange conversion rates ensure users can spend confidently regardless of their location. This global functionality makes Tap particularly valuable for frequent travelers, digital nomads, and anyone conducting international business.

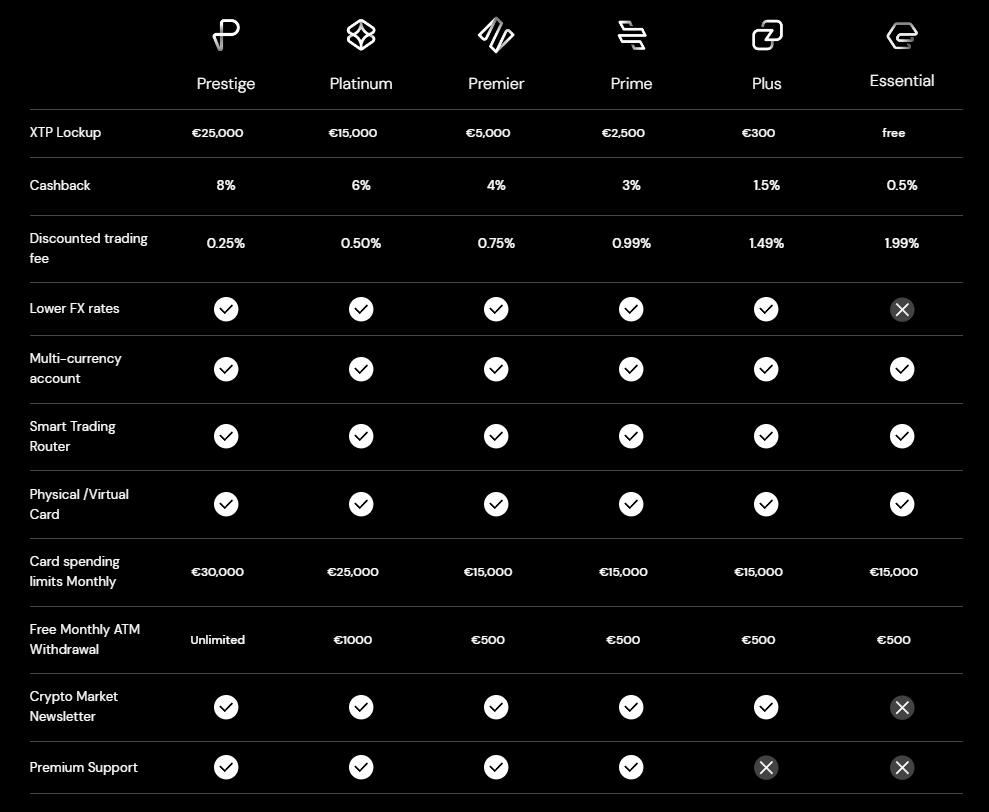

By holding and utilizing XTP tokens, users can access premium features including up to 8% Cashback on spending, reduced trading fees, decreased foreign exchange fees, higher card spending limits, and exclusive market insights. This tiered system creates tangible value for token holders while incentivizing platform engagement.

This sophisticated system scans multiple exchanges and liquidity providers in real-time, automatically finding the optimal available prices for crypto transactions. This feature ensures all users receive top rates without needing to manually compare prices across different platforms.

What Is the XTP Token Used for?

XTP is the native utility token of the Tap platform, built on Ethereum (ERC-20) and designed to enhance your experience across crypto and traditional finance.

- Reduced crypto trading and FX fees for token holders, including lower costs when converting between crypto and fiat currencies, allowing for a seamless on and off ramping experience.

- Unlock premium tiers with perks such as Cashback on purchases made with the Tap Mastercard, higher limits, and priority support.

- Instant, feeless peer-to-peer payments within the Tap network, ideal for remittances and cross-border transfers.

- Access to premium features such as increased limits, newsletters, and exclusive rewards.

By holding XTP, users not only save on fees but also gain deeper integration within Tap’s ecosystem, encouraging long-term participation.

Tap (XTP) Key Growth Factors

Tap's success directly correlates with user acquisition and platform engagement. Increased adoption of the Mastercard, growth in Tap2Tap network usage, and expansion into new geographic markets could positively impact demand for XTP.

Collaborations with financial institutions, crypto exchanges, and fintech companies could enhance platform utility and drive token value appreciation.

Favorable regulatory developments in key markets, particularly regarding crypto integration with traditional banking services, could significantly boost platform adoption and token utility.

Continued platform development, including enhanced security features, expanded crypto support, and improved user experience, supports long-term growth prospects.

How to Buy Tap (XTP)

You can buy XTP tokens in two main ways, whether you're new to crypto or already have some experience.

Buy XTP with crypto

If you already own Bitcoin, Ethereum, or stablecoins like USDT, you can swap them for XTP on exchanges like Uniswap or ProBit. Just create an account, deposit your crypto, and make the trade. Or alternatively, you can buy directly through the Tap app, where the smart trading engine scans multiple exchanges to find the top prices automatically.

Buy XTP with fiat money

Prefer using your debit card or bank account? Download the Tap app, complete verification, and buy XTP directly with traditional currency. It's the easiest route for beginners as everything happens in one place.

Pro tip for storage

While the Tap app works great for daily use, consider a hardware wallet like Ledger or Trezor if you're planning to hold larger amounts long-term. Think of it like keeping small bills in your regular wallet but storing larger amounts in a safe.

Tap's Ecosystem at a Glance

Tap brings together everything you need to manage money, whether crypto or fiat, into one seamless platform. Each feature is designed to solve everyday financial challenges, from spending to exchanging to sending money abroad.

Multi-currency wallet

Store and manage 60+ cryptocurrencies and major fiat currencies in one secure, easy-to-use wallet. Tap ensures safety with encryption and full regulatory compliance.

Tap Mastercard

Spend crypto or fiat anywhere Mastercard is accepted - online, in-store, or at ATMs. Choose a physical or virtual card and earn as much as 8% Cashback for premium users.

Trade any supported currency without limits. Tap's built-in smart engine scans multiple exchanges in real-time to find the optimal rates for trades automatically.

Community & Support

Join the active Telegram and X channels for updates, tips, and support. Premium users get access to exclusive market insights and help here.

A smarter alternative to traditional banking

While Tap isn't a bank, it offers many things banks can't - like instant crypto-to-fiat spending, global transfers with lower fees, and real-time access to digital assets. By combining these tools in one app, Tap simplifies money management for a new generation of digital natives.

Is XTP Worth Your Attention?

In a nutshell, Tap is a publicly listed and regulated fintech platform that integrates traditional banking features with crypto services. It offers secure asset storage, global spending via Mastercard, competitive exchange rates, and peer-to-peer transfers through its Tap2Tap network.

Appealing to a wide range of user groups, Tap offers travelers benefits like favourable currency exchange rates and card acceptance, cross-border users can enjoy free transfers between users in app, and crypto traders can make use of the seamless spending experience. While the interface and onboarding processes are made really accessible to both newcomers and active traders.

The XTP token serves a functional role within the ecosystem, supporting platform utility rather than speculation. However, users should consider the volatility of crypto markets, regulatory variability, and competition from both banks and fintech firms.

For those seeking an all-in-one platform that connects traditional finance with crypto, Tap presents a cheap, practical and user-friendly option.

In today's interconnected global economy, the ability to manage finances across multiple currencies and cryptocurrencies is becoming increasingly important. New financial technologies are emerging to address this need, offering tools that simplify cross-border transactions and bridge the gap between traditional and digital currencies.

Streamlined Euro Payments

The Single Euro Payments Area (SEPA) system has revolutionised euro transactions across Europe. This standardised framework allows for efficient and cost-effective transfers between participating countries. Tap leverages this system to provide users with an exceptionally easy and affordable way to send EUR. With Tap, transferring euros becomes as simple as a few taps on your smartphone, making cross-border transactions more accessible than ever.

GBP Transactions with Faster Payments Service

In the UK, the Faster Payments Service (FPS) has transformed the speed of domestic transactions. Tap integrates this system to offer users a remarkably simple, fast, and cheap method for sending GBP. Whether you're splitting a bill with friends or paying a supplier, Tap's FPS integration ensures your pounds are transferred almost instantly, 24/7, with minimal associated costs.

The Power of Stablecoins for International Transfers

Stablecoins have emerged as a crucial bridge between traditional currencies and the volatile world of cryptocurrencies. Tap offers the convenient option of converting Fiat or cryptocurrencies to stablecoins, providing a cost-effective and lightning-fast alternative to traditional SWIFT transfers for international payments. This feature is particularly valuable for those looking to avoid the delays and high fees often associated with cross-border bank transfers.

John, a London-based entrepreneur, shares her experience: “For urgent payments to my international suppliers, Tap's stablecoin transfer feature is an absolute godsend. I can swiftly convert my pounds to USDT and send payments anytime, with the assurance that they'll be processed almost instantly. It's made dealing with international payments an absolute doddle. Brilliant stuff, really.”

Exploring Cryptocurrency Options

For users who are comfortable with cryptocurrencies, Tap offers another layer of flexibility. The platform supports a wide range of cryptocurrencies, allowing users to send and receive various digital assets if that's their preferred method of transaction. This feature caters to crypto enthusiasts and those looking to leverage the unique benefits of blockchain-based transfers.

Integrating Traditional and Digital Finance

As the lines between traditional and digital finance continue to blur, Tap stands out by seamlessly handling both. This integrated solution offers several advantages:

1. Simplified management of diverse assets in one place

2. Easier conversion between traditional currencies and cryptocurrencies

3. Potential for reduced fees through the use of blockchain technology

4. Enhanced financial flexibility for global transactions

The Tap Network: Free Transactions Within the Ecosystem

One of Tap's most compelling features is its in-app Tap2Tap Network. This innovative system allows users to send both cryptocurrencies and fiat currencies to other Tap users in the app completely free of charge. By facilitating fee-free transactions within its ecosystem, Tap not only saves users money but also encourages a more interconnected financial community.

Whether you're sending euros across Europe, pounds within the UK, stablecoins for international transfers, or cryptocurrencies to fellow enthusiasts, Tap provides a comprehensive solution that combines speed, simplicity, and cost-effectiveness. The platform's integration of traditional banking systems, stablecoin functionality, and cryptocurrency support, all united under the fee-free Tap2Tap Network, represents a significant step forward in accessible, flexible global finance.

To experience the benefits of integrated currency and cryptocurrency management firsthand, consider exploring Tap. This innovative financial app combines support for SEPA and FPS transactions with a wide range of cryptocurrency options, including stablecoins and popular tokens. Visit www.withtap.com to learn more about how you can optimise your financial transactions across borders and digital assets, and start enjoying fee-free transfers within the Tap2Tap Network today.

As the head of design at Tap, I'm thrilled to pull back the curtain and share the inspiration and creative journey behind our latest card design. This isn't just any card - it's a statement piece that embodies the ambitious, bold lifestyle of our customers.

The Napkin Where It All Began

Like many brilliant ideas, this card design was first sketched out on a humble diner napkin one night at the office. I'll never forget it - there we were, sipping a late-night coffee and suddenly struck by the notion of combining modern high-contrast colours in an unexpectedly cool way. Just a rudimentary doodle at first, but the seeds of inspiration were planted.

From there, the concept evolved into an obsession. Our small team of designers got utterly consumed, pushing the limits with edgy colour experiments and painstaking material studies. We'd be hunched over our workstations deep into the night, pursuing that elusive blend of premium aesthetics and sleek functionality. Fuelled by imagination (and probably too much caffeine), we knew this card design had to be more than just beautiful- it needed to perfectly capture our customers' sense of style and ambition.

The Eternal Cool of Black

When we began sketching ideas, one colour immediately emerged as a must-have: black. There's just something undeniably cool about black. It exudes confidence, sophistication, and an edge that can't be matched. We envisioned our card cutting a striking presence whenever it emerged from a wallet or handbag to effortlessly handle a transaction.

Black is also the perfect blank canvas that allows the secondary colour to really pop. And for that accent shade, we wanted something vibrant, energetic and daring - qualities our customers embrace every day as go-getters and trailblazers.

The Energy of Orange Awakens

Enter the brilliant idea of orange. This hue is associated with creativity, success, and an adventurous spirit. Just as important, that bright orange complements the black's depth in an unmistakably modern way. Together, these two colours create a bold, unified statement that demands to be noticed.

Bringing the Vision to Life

With the colour palette locked in, our designers got to work on the physical card itself. We went through dozens of iterations and material tests to achieve just the right texture - a soft-touch matte finish with subtle crosshatching that makes it satisfying to slide across a surface.

The type facing was an equally considered process to strike that elusive balance between simplicity and distinctiveness. We opted for a clean, straightforward font that's extremely legible but with slightly elongated letters that exude a spirit of forward movement.

A Long-Awaited Arrival

After weeks of intense collaboration and refinement, the day finally arrived for us to inspect the first physical prototypes. I'll never forget the moment I held that initial batch in my hands. While the renderings and digital mockups offered a hint of the final vision, there was no substituting the visceral experience of running your fingers across the soft-touch black matte finish with precise orange accents.

You could tell instantly this was a card designed with incredible thoughtfulness and an unwavering commitment to crafting something special. From the orange pips along the edge that emanate energy to the embossed numbers with that sublime crosshatching you can feel - every detail resonated a passion for purposeful, meticulous design work.

Chasing Perfection

Then finally, after weeks of progressive iterations, sample reviews, and more than a few disagreements (designers are a fervently opinionated bunch!), we landed on that iconic scheme: The unmatched smoothness of a soft-touch black matte body, highlighted by piercing streaks of brilliant orange - both afterbursting colours that demand attention but remain timelessly cool.

I'll never forget the thrill of receiving those first physical prototypes and running my fingertips across the finished product. The subtle crosshatching pattern, the premium weights and ridges - it all came vibrantly to life in a way digital mockups could never replicate. This labor of love transcended the realm of "just another card" into something undeniably beautiful yet purposefully compact and functional.

Designing a Lifestyle

At the end of the day, this card represents so much more than just the material product. It's a symbol of a modern lifestyle - one defined by ambition, taste, and an appreciation for quality. By combining bold colour choices with premium textural elements and sleek typography, we've created a card designed to embody the brilliant mindset of our customers.

Whether making a designer purchase or simply indulging in an everyday transaction, pulling out this card is an event in itself. It's a piece of industrial design meant to inspire confidence and pride in every interaction.

An Ode to Tappers

So while formidable talent and teamwork were required to bring this product to life, the inspiration arguably came from you - our remarkable users. With this latest creation, we hope to infuse your daily transactions with a sense of pride, beauty, and modernity that inspires you to perpetually chase your daring ambitions.

So while the path to get here involved the passionate work of so many industrial designers, colour experts, and other creative minds, we hope you'll agree the final product was more than worth the effort. This new card is truly where functional utility meets individuality and self-expression.

Welcome to a lifestyle where confidence meets individuality. This one's for you.

We can't wait to see it energising your daily life.

If you’re in the process of applying for a passport chances are strong that you already know the importance of needing one. Whether you’re in a terrible hurry because you forgot to check the expiry date before booking your trip or maybe lost your passport ahead of an urgent cross-border meeting, we’ve got you covered. The UK offers a service that allows applicants to fast-track their application.

Find everything you need to know about the process below, including the fees involved. And why might we, a fintech platform, be informing you about fast-tracking passports? Because we’re in the business of travel. With our world-friendly app that allows users to seamlessly switch between currencies as they swipe their cards around the world, we understand not every process is this simple. Now that we’ve covered that, let’s get into why you’re really here.

How to fast-track your passport application

Getting a passport in the UK can sometimes be a lengthy process, but luckily there are options available to speed things up. Normally, it can take up to 10 weeks to receive a new passport through the standard application process. While it may be quicker in some cases, it's always best to be prepared for a wait.

The one-week fast-track option

The first option is the 1 week Fast Track service. This service allows you to renew an adult or child passport, replace a lost or stolen passport, or update your details. You can book an appointment for this service up to 3 weeks in advance and will need a debit or credit card.

How to apply

To apply for the 1 week Fast Track service, follow these steps:

1. Visit your local Post Office branch to obtain an application form (these are not available online).

2. Book your fast-track passport appointment online.

3. Pay the fee.

4. Take your completed application form and the required supporting documents to your appointment. There is a booklet accompanying the application form that provides a list of the necessary documents.

5. Once you have completed these steps, your new passport will be delivered to your home address within a week of your appointment. It's important to note that someone needs to be present to sign for the passport upon delivery.

The costs*

The cost for the 1 week Fast Track service is £155 for an adult passport and £126 for a child passport.

The same-day fast-track option

If you need your passport even faster, there is also the Online Premium service. With this service, you can collect your new passport on the same day as your appointment. However, please note that this service is only available for adult passport renewals issued after 31 December 2001.

If you have an adult passport issued before this date, you will need to use the one-week fast-track service or the standard application process.

How to apply

To use the Online Premium service, you can simply apply and book an appointment online. The earliest appointment you can get is 2 days after applying.

The cost*

The cost of this service is £193.50 for an adult passport.

Who can use these services?

It's important to know if you are eligible for these fast-track passport services. If you are applying for your very first UK passport, unfortunately, you won't be able to use either of the fast-track services (unless applying for a child's first-time passport in which case you can use the one-week fast-track option). For everything else, you will have to go through the standard application process instead.

In conclusion

Remember, it's always best to plan ahead and apply for your passport in advance to avoid any last-minute stress and government regulation curveballs. However, if you do find yourself in need of a passport urgently, these fast-track services can be a lifesaver.

If you have any further questions or need additional assistance, don't hesitate to reach out to the appropriate passport office or visit their website for more information (listed below). They will be able to provide you with the most up-to-date details and guidance regarding the fast-track process.

*Please note that the fees were correct at the time of writing and are subject to change. Check the website page listed below to find the relevant information.

References:

- GOV.UK - Passport application service

- GOV.UK - 1 week Fast Track service

- GOV.UK - Online Premium service

Private label cards are branded payment solutions that enable businesses to offer customized rewards, incentives, and financing options to their customers and employees. These cards serve as powerful tools for driving customer loyalty, improving cash flow management, and gaining valuable spending insights. In this article, we'll guide you through the concept of private label cards, their key benefits for businesses, and delve into how they work.

What are private label cards?

Private label cards are branded payment cards issued by businesses to their customers or employees, allowing them to make purchases or access funds within a specific ecosystem or network. Unlike traditional debit or credit cards issued by a bank, private label cards are a product tailored to the branding and specific needs of the issuing company.

These cards differ from traditional cards in several ways. Firstly, they are not tied to a specific financial institution but rather to the company's brand and loyalty program. Secondly, they often offer unique rewards and incentives tailored to the business's products or services. Additionally, private label cards provide businesses with valuable customer data and insights, enabling targeted marketing efforts and personalized experiences.

Private label cards and fintechs

In recent years, fintech platforms have revolutionized the issuance and management of private label cards. These technology-driven companies act as program managers, handling the end-to-end process of card issuance, transaction processing, and compliance adherence.

By partnering with fintech platforms like Tap, businesses can efficiently launch and manage their private label card programs, leveraging advanced technologies, scalability, and industry expertise without the need for extensive in-house resources.

How private label cards benefit businesses

Private label cards empower businesses to strengthen customer relationships, optimize financial operations, and gain a competitive edge through tailored rewards, data-driven insights, and robust security measures. Let’s explore some of these concepts below:

Drive business

Private label cards offer businesses a range of benefits that can drive customer loyalty, enhance brand recognition, and streamline operations. By offering customizable rewards and loyalty programs tailored to their products or services, businesses can incentivize customers to make repeat purchases while simultaneously collecting data on customer preferences, fostering long-term relationships and brand advocacy.

Cash flow management

Private label cards provide businesses with a valuable tool for cash flow management. By encouraging customers to use their branded cards, companies can receive payments more quickly, improving their working capital and financial flexibility.

Collect data and analytics

One of the key advantages of private label cards is the wealth of data and analytics they provide. Businesses can gain insights into customer spending patterns, preferences, and behaviours, enabling data-driven decision-making and targeted marketing strategies.

Security benefits

Additionally, private label card programs prioritize security and fraud prevention measures. Fintech platforms offering these solutions employ advanced technologies and protocols to safeguard customer information and transactions, providing businesses and their customers with peace of mind.

The differences between private label and co-branded cards

Private label cards are issued by a single retailer or business, bearing their branding and tailored rewards program. Co-branded cards, however, involve a partnership between a merchant and a major card network (Visa, Mastercard), carrying dual branding.

In general, private label cards offer more customization and control for the merchant but may have limited acceptance outside their network. They can also drive stronger loyalty but require more resources to manage.

Co-branded cards, on the other hand, have wider acceptance but less flexibility in terms of rewards/benefits. As they leverage an existing card network's infrastructure, they offer less differentiation.

The choice depends on the merchant's goals; private label are beneficial for deeper customization and loyalty while co-branded cards off wider acceptance and shared resources with a card network partner.

How private label cards work

Private label cards are issued through a collaborative process involving businesses and fintech platforms. Businesses define the card program's features, branding, and reward structure, while fintech platforms handle the technical and operational aspects. As program managers, fintech companies then oversee card issuance, transaction processing, and data management, leveraging their expertise and scalable technologies.

The importance of compliance and adherence to regulatory requirements cannot be underestimated or overlooked when looking at the issuance of private label cards. Fintech platforms need to ensure that card programs comply with industry standards, data privacy laws, and anti-fraud measures, providing businesses with a secure and reliable payment solution.

Regular audits and risk assessments are conducted to maintain compliance and mitigate potential risks. Businesses must always do their research before engaging in private label card issuance with a fintech platform.

Examples of use cases

Private label cards can offer a range of use cases across various industries. See several examples below:

Retail and e-commerce

In the retail and e-commerce sectors, they serve as powerful loyalty tools, incentivizing customers with tailored rewards and exclusive offers. Businesses can leverage these cards to drive repeat purchases and foster brand loyalty. An example would be the Amazon Store Card.

Corporate expense management

Corporate organizations utilize private label cards for streamlined expense management, enabling employees to make authorized purchases while providing detailed spending data for analysis and budgeting purposes.

These cards also facilitate employee incentive and recognition programs, rewarding high-performers with customized benefits and privileges. An example of this would be a company card issued to employees to use for company expenses.

Specific purposes

Additionally, private label cards can be issued as prepaid cards for specific purposes, such as payroll disbursements, gift cards, or restricted-use cards for controlled spending. This versatility allows businesses to tailor card programs to their unique needs, ensuring efficient fund management and targeted usage.

An example of this could be a corporate-branded preloaded gift card for promotional purposes allowing holders to buy something in-store using the card.

How to create a private label card for your business

With Tap, you can seamlessly integrate private label card programs into your operations. Tap streamlines the entire card issuance and management process, allowing companies to leverage off their advanced technologies and industry expertise.

By partnering with Tap, you gain access to a scalable and flexible solution, enabling you to launch and adapt card programs efficiently, tailored to your company’s specific needs. Tap's platform offers robust features, real-time analytics, and end-to-end support, empowering every businesses to deliver tailored payment experiences while ensuring compliance and security.

With Tap, you have the power to not only launch and adapt your card programs efficiently but also to customise the fees charged to your users. Our approach is entirely flexible, allowing you to set charges that align with your clientele's needs. Our platform offers unparalleled freedom, allowing you to tailor your card programs precisely to your company's needs and goals.

Conclusion

In summary, private label cards empower businesses with a versatile payment solution that promotes customer loyalty, optimizes operations, and delivers valuable data insights. Whether for retail, corporate, or specific use cases, private label cards offer a competitive edge through tailored rewards, data-driven strategies, and enhanced customer experiences - paving the way for business growth.

Please contact xxx for further information on setting up your private label card.

Did you know that there are five different ways we express our love through money? Below we break down the original five love languages and then explain how these can be integrated into a financial setting. Knowledge is power, after all.

The original five love languages

The original five love languages were first introduced by Dr. Gary Chapman in his book "The 5 Love Languages: The Secret to Love that Lasts" offering insight into how we convey our love and how we hope to receive it. The five love languages are:

Words of affirmation

Expressing love and appreciation through verbal or written compliments, praise, and kind words.

Quality time

Showing love by giving undivided attention and spending meaningful quality time together.

Receiving gifts

Demonstrating love through thoughtful and meaningful gifts, usually involves around both giving and receiving gifts.

Acts of service

Expressing love by performing acts of kindness and service for the other person.

Physical touch

Showing affection and love through physical touch, such as hugs, kisses, and holding hands.

These love languages help individuals understand how they prefer to give and receive love. The book also states that recognizing and speaking each other's love languages can strengthen relationships.

What are the financial love languages?

Taking the original pillars, we’ve created five money love languages to give you an idea of how you financially show up in relationships (family, love or otherwise). Whether you share a flat with your brother, a business with a friend, or a joint account with a partner, everyone will be able to relate to these financial love languages. Afterall, managing money in a positive light is the cornerstone of any healthy relationship.

The five financial love languages

There’s value in being attuned to your own patterns, and to those of the ones you love. By recognising your partner's money love language you might get a better objective of how to create more harmony in the relationship by understanding what drives them to spend money. Without further adieu, let’s get into the five money love languages.

Open communication

While there are few topics less pleasant to talk about than money, having open and honest communication when it comes to the benjamins is not only valuable but essential. Having the skill, or having honed the skill should we say, to speak about financial matters with a loved one is an accolade, and for some, the most natural money love language. These chats will likely make you feel empowered and more connected to those around you, making it easier to be on the same page.

Acts of service: money edition

While the original acts of service encompass doing things that make the lives of those you love a little easier, in this context acts of service relate to money-related tasks such as taxes or budgeting. Having someone do your taxes as an act of love might be a bit ambitious, so let’s look at alternatives. It could be organising the holiday budget or creating an action plan to get your friend out of debt, or simply fixing something for you in order to save you money.

Love in savings

While it doesn’t sound like the sexiest option, planning for the future and having financial security is an invaluable act of love. Whether through investments, retirement plans, or even an emergency fund, what doesn’t say “I love you” if not “let’s make a financial decision to grow old together.” Some people's love language is expressing affection through providing, so why not let them put their planning skills and diligence to the test and shower you with their love? It might even help you reach your financial goals that much faster.

Experiencing something together

This person’s money love language is expressing their fondness through experiences and quality time, spending money on taking a trip, going on an exciting date night, or simply a new adventure. Through investing in time and experiences, you are quite simply saying I value spending time with you more than I value monetary gains.

The art of gifting

The last money love language we have for you today centers around gift-giving. Are you someone who likes to shower friends with presents, or love to spoil your significant other with something wonderful? Then this one’s for you. While this shouldn’t ever involve draining your bank account, pouring your love (and money) into an appropriate gift is a great way to show affection. Remember, it’s often the thought that counts rather than the price tag.

Which is your money love language?

Which of these do you most resonate with? Sometimes by identifying these intrinsic needs, we are able to better understand not only ourselves but our expectations of others. Whatever your financial love language might be, be sure to pour the greatest amount of love into your own finances and steadily work toward reaching your financial goals.