Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

This year has proven to be historical both in terms of substantial market fluctuations as well as regulatory development across a wide range of jurisdictions. As leadership around the world gears up to provide a much needed regulatory framework surrounding the blockchain and cryptocurrency industry, we explore the factors these bodies will need to consider in order to find the balance between implementing crypto regulation without stifling innovation.

Why regulation is necessary

There has long been a stigma in the industry against the regulation of cryptocurrencies, with many believing it will hinder the free-world currency. As Bitcoin and subsequent cryptocurrencies were created to oppose the constructs placed on people’s finances by governments and financial institutions, some feel that regulation will disarm the decentralized nature of its use.

This is however untrue. With regulation comes widespread education and, many believe, adoption. With more frameworks in place constituting what one can and cannot do with the digital assets, comes clearer concepts of what the currency can achieve, and more fingers in the pie, so to speak.

At this point, it would be foolish to assume that a wave of regulation is a remote possibility. Governments around the world are in the midst of creating their own regulation and enforcement memorandums, some being more public about it than others.

What factors crypto regulation policymakers need to consider

For many industry insiders, this move is a positive step forward, and a vital one if the industry is to become an integral part of daily life, as anticipated. According to Everett Rogers’ technology adoption lifecycle model, as more investors outside of the blockchain industry turn to digital currencies purely based on the regulation in place, the lifecycle of adoption steadily increases.

As the key goal here is to protect investors from financial losses, there is concern that any stifled, misguided policies will hinder the innovation and prosperity of cryptocurrencies. Hence, here are the following factors that deem most important when walking the tightrope trying to find a balance between the two goals.

- Market Participation

In order to properly understand and implement policies regarding the crypto market, prominent figures in the industry should be consulted. Typically, most governments don’t have a team of crypto-enthusiasts to converse with.

Market participants should be at the centre of their debates and should provide valuable insight as well as vast expertise into how digital payment systems function. Policymakers need to ensure that they are collaborating with appropriate expertise should they wish to get this right.

- Gradual Implementation

While it might seem tempting to build and implement a highly complex regulatory framework around an industry that is just over a decade old overnight, this process needs to be done slowly and intricately if it intends to succeed.

There is little need to rush to impose policies across the board without proper and thorough examination and reflection. Instead of barring the industry with sanctions that might make little sense, policymakers should consider taking a slow and steady approach to build regulation governing the industry, as the consequences of not doing so can be dire.

- Deserved Recognition

Giving credit where credit is due, cryptocurrencies are unique assets and cannot be treated with the same standards as stocks, commodities, etc. The digital currencies process distinctive characteristics that need to be respected and celebrated as opposed to sanctioned by people in power who do not understand their worth.

Therefore, outdated policies need to be rebuilt if they wish to be constructive.

As the first globally decentralized industry, the blockchain and cryptocurrency industry requires a slow and steady implementation of regulation, one that materializes organically as opposed to in a rushed, authoritarian manner. By opening a dialogue between policymakers and private-sector expertise, the process can be developed and debated at a pace that guarantees success.

Regulation Efforts To Date In The US

Considering that an estimated 46 million people in the United States hold cryptocurrency and that the DeFi (decentralized finance) industry has grown by over 6,000% this year alone, a number of regulatory bodies in the US have geared up to take action.

Various bodies have taken different ventures into the crypto regulation space, with the President’s Working Group on Financial Markets studying stablecoins, Congress introducing legislation that ensures “comprehensive” crypto regulation, and the SEC threatening and suing cryptocurrency companies at an alarming rate.

To date, the SEC has been in a complicated legal battle with RippleLabs, the company behind XRP, and scared Coinbase from launching a Lend feature with threats of legal action if they do so. Tom Emmer, a lawmaker interested in blockchain, has called out the SEC for their threatening manner, citing that:

“I disagree with [SEC Head Gary Gensler] strenuously when he suggests that almost all of these [crypto products] are securities. I think the vast majority of cryptocurrency offerings or related offerings are actually currencies or commodities. The SEC is not involved. If the SEC were to deem one of these coins a security, the value of that token would plummet. And those retail investors would be seriously hurt — that’s directly the opposite of his mission and his authority.”

Finally, the international pioneer in combating money laundering, the Financial Action Task Force, has issued a draft guidance report encouraging countries to regulate unhosted wallets in an attempt to hold those who profit from these accountable.

Regulation Efforts To Date In The UK

The United Kingdom has also set about to regulate cryptocurrency trading, however, in a less disruptive manner. The regulatory body, the Financial Conduct Authority (FCA), targeted trading platforms requiring them to present information required in order to verify and certify their company practices.

One of the largest crypto trading platforms failed to do so and subsequently lost the right to provide services to UK citizens. While trading of digital assets in the UK is not strictly prohibited, the platforms offering these services are required to be registered with the FCA and prove that they comply with anti-money laundering rules, particularly in the crypto derivatives market.

More recently, the deputy financial stability officer for the Bank of England, Jon Cunliffe, called for crypto regulation to be pursued as a matter of urgency, warning that crypto poses “a rapidly growing threat to the global economy.”

Cunliffe went on to compare the 2008 financial market crash to what could occur should the crypto markets take on a similar crash. He noted that the instigator in the crash, the $1.2 trillion subprime market, was but a tiny portion of the $250 trillion global financial system at the time, and a significantly smaller segment of the market than what the cryptocurrency market is today.

This is largely due to a report released by the IMF (International Monetary Fund), calling for governments to create a regulatory framework around the world. The report further warned that heightened adoption could weaken fiat currencies, destabilise capital flows, and promote tax evasion.

With Regulation Comes Growth

As this technical revolution continues to develop and grow, regulatory bodies around the world must work constructively to build and implement regulations that support the benefits that cryptocurrencies have to offer and allow society to evolve into a superior version of itself as a result.

There is little doubt that the cryptocurrency market is now on the top of the agenda for central bank leaders and finance ministers around the world. While cryptocurrencies weren’t designed to be contained by (government-constructed) laws, regulation is a necessary step forward in the worldwide adoption of digital assets. Regulation should be viewed as an accolade instead of a hindrance.

With more structural framework, comes an indubitable acceptance that cryptocurrencies have entered mainstream financial markets, proving that they are indisputably here to stay.

The crypto markets are in the midst of a serious slump. While bear markets are a natural process within the economic cycles and should not be feared, many look to these times as an opportunity to accumulate cryptocurrencies in what has become known as "buying the dip".

Bitcoin currently undervalued

According to the United States investment company, JPMorgan Chase, who valued Bitcoin at $38,000, the biggest cryptocurrency is currently undervalued. With Bitcoin essentially selling at a "discount", now is a great time to establish whether you should buy the dip.

It is believed that the crypto markets have taken a knock following the war instigated by Russia on Ukraine, the global rising inflation rates, a looming recession and the potential energy crisis that could plague Europe. Despite the global market turmoil, cryptocurrencies have proven to be incredibly resilient over the years.

There are of course a few things to consider, mainly your appetite for risk and your currency income bracket. As the golden rule goes: never invest more than you're willing to lose. Another important component to consider when deciding whether to buy the crypto dip is where you see the cryptocurrency going in the future. Do you believe in the project's fundamentals, and that its user base will continue to grow?

Despite the cryptocurrency being 70% down from its all-time high price achieved in November 2021, industry insiders remain bullish. Chris Brendler, managing director at D.A. Davidson, believes Bitcoin will be trading at $38,000 by the end of the year, and $50,000 by the end of 2023. Jurrien Timmer, director of global macro at Fidelity Investments, on the other hand, believes that it will be worth up to $100,000 in 2024.

Is it the right time to invest in cryptocurrencies?

Since its inception over a decade ago, Bitcoin has amassed a devoted following. However, it's impossible to say now whether Bitcoin will become the world's reserve currency or a universally acknowledged store of value, like gold. Some investors are frightened by the rush of riches or downfall, while others are enthusiastic about the potential for large gains. in the crypto market.

In 2022, Bitcoin is considerably less hazardous than it was in 2012 and is widely regarded as being a revolutionary technology. In today's geopolitical climate, Bitcoin has risen to the forefront. El Salvador's decision to legalize Bitcoin as legal money in 2021 is expected to encourage other nations to do the same, however, others may choose against it out of fear of losing their fiat currency.

Buying Bitcoin, also known as making a Bitcoin investment, like any speculative investment, involves a degree of risk. Bitcoin was the first digital asset to give rise to the contemporary crypto economy. For many years, it had a hidden following of crypto investors who believed it may eventually replace the physical monetary system. As institutions and governments seek to satisfy their customers' growing demand for exposure, Bitcoin has grown.

In order to get the most out of a Bitcoin investment, one must know when to buy. The Bitcoin market is unpredictable and may switch rapidly, with fluctuations ranging from minutes to weeks and even months. As a result, determining the right time to buy one's digital currency is crucial.

There is no such thing as a perfect time to make a crypto investment, however, buying when in a dip or a bear market allows for lower price points.

While Bitcoin remains the biggest cryptocurrency, there are alternative investment options to consider such as Ethereum, the second biggest cryptocurrency. Ethereum was designed as a blockchain platform on which developers could create their own blockchain-based apps, known as decentralized applications (apps). When buying the dip, investors tend to stick to the top-ranked cryptocurrencies.

Buying crypto during a bear market

In the world of cryptocurrencies, a dip is when you buy something after its value has dropped. Buying a dip indicates that you have an opportunity to invest in a digital currency or token whose price has fallen, whether it be short or long-term. A bull market is typically a good time for you to sell Bitcoin, while a bear market is a good time to buy Bitcoin.

A bear market is any decline in the market price of at least 20% over a set period of time. The December 2017 Bitcoin price crash is one such example, in which the price of Bitcoin fell from $20,000 to $3,200 in just a few days. According to folklore, the term "bear" is said to derive from a bear's fighting style, which involves using its claws in a downward motion. Others speculate that it has to do with bears going into hibernation in the winter.

Traders prefer to acquire assets during a bear market, particularly when they are at low prices. However, determining when a bear market has come to an end makes it difficult for investors to take the risk of buying a low-value cryptocurrency that may or may not recover.

When investors learn about unfavorable circumstances involving a specific cryptocurrency or asset, the market price commonly drops. As a result of the negative spiral, more people delay investing because they believe that more terrible news is on the way and that they should prepare for the worst.

This causes the market to lose more ground as a result of panic selling and contributes to the downward trend in crypto prices. Bear markets eventually subside when investors gradually regain their confidence and buy Bitcoin, ushering in a new bull cycle.

Bear markets are a great time for Bitcoin investors to take advantage of the price swings. When Bitcoin funds are low, this typically equates to lower fees on Bitcoin transactions as well, which can help to propel Bitcoin adoption.

Is now the right time for a Bitcoin investment?

We must first assess the market's overall attitude to determine whether now is a good time to invest in Bitcoin.

According to the crypto Fear and Greed Index, it is currently positioned on "extreme fear" indicating that it is trading well below its intrinsic values.

The "Bitcoin Monthly" report issued by Ark Invest reported that 'Hodlers,' are more powerful than ever before, with 66% of Bitcoin's supply remaining unchanged for almost a year. This illustrates the market's long-term dedication.

According to Glassnode data, short-term investments dropped -35% below the breakeven price in the third quarter. These statistics were last seen in January 2022, July 2020, and March 2020. The aggregate long- and short-term holdings are still above the breakeven price, implying that widespread capitulation has not occurred.

Trading Bitcoin in the current crypto market conditions

Finally, it all boils down to whether or not you feel comfortable putting your money into the current market conditions. There is no easy solution to when is the best time to invest in Bitcoin. We are still early in the game, and Bitcoin, as well as the entire sector, has a lot of room for development. This implies that the investment opportunities for investors will likely continue.

Disclaimer: This article is intended for communication purposes only, you should not consider any such information, opinions or other material as financial advice. This information is specific to that of the Bitcoin market and should not be translated to the traditional stock markets. The crypto market is an entirely different asset class and crypto holdings should be treated as such.

The information herein does not constitute an offer to sell or the solicitation to purchase/invest in any crypto assets and is not to be taken as a recommendation that any particular investment or trading approach is appropriate for any specific person.

There is a possibility of risk in investing in crypto assets and investors are exposed to fluctuations in the crypto asset market. This communication should be read in conjunction with Tap's Terms and Conditions.

Disclaimer: This article is intended for communication purposes only, you should not consider any such information, opinions or other material as financial advice. This communication should be read in conjunction with Tap’s Terms and Conditions.

Crypto lending might be the hot new product in the cryptocurrency space, but before you dive in be sure to first understand what it entails. The concept grew great traction with the rise of the decentralized finance (DeFi) movement, with platforms offering users high yields for borrowing crypto assets.

Let’s get started with what crypto lending is, and then explore how the product works.

What is crypto lending?

Crypto lending is a traditional banking service curated to the crypto world. With the DeFi space remains largely unregulated, many crypto exchanges and other platforms have started offering these services, with added security.

Crypto lending involves a user lending crypto assets to a platform in return for interest, which allows other users to then borrow said crypto assets, paying interest on the amount borrowed. The platform will then take a small percentage of the interest paid.

Depending on the platform and other factors, crypto lending platforms may be centralized or decentralized and offer exceptionally high-interest rates, with annual percentage yields (APYs) of 15% or more. With the interest rates being higher than traditional bank accounts, lenders gain access to much greater yields, increasing their returns.

Another advantage to crypto lending is that users are still exposed to price gains in the market. Meaning that if you deposit your Bitcoin when it's worth $20,000 and the price rises in value to $50,000, you are still able to realize these returns and earn interest for the duration of the loan.

Note that interest rates might fluctuate with market conditions on some platforms, increasing when the prices increase and decreasing when markets are down.

How does crypto lending work?

Cryptocurrency lending platforms function as middlemen connecting lenders to borrowers. Lenders deposit their digital currency into high-interest lending accounts, and borrowers utilize the lending platform to acquire loans. These systems then lend money utilizing the crypto that investors have provided them.

The platform controls its net interest margins by establishing the interest rates for both lending and borrowing.

Rates on platforms differ from cryptocurrency to cryptocurrency, some platforms might offer higher interest rates to lenders willing to commit to a certain time frame. There is no standard interest rate for cryptocurrencies, as each platform has its own set of rules.

Centralized crypto lending means putting your money in the hands of a corporation or other entity to manage and make the process easier. Accounts are created for borrowers and lenders, and loans may be requested by applicants.

Lenders and borrowers may connect their cryptocurrency wallets to a decentralized crypto lending protocol, which uses smart contracts to automate the lender-borrower relationship. Smart contracts are automated digital agreements that execute once certain criteria is met.

The advantages of crypto lending

There are several benefits to crypto lending when comparing it to a regular bank account.

Borrowers have access to these financial services without having to pass a credit check, making it more financially inclusive than traditional banking services. They are also exposed to lower interest rates than regular banking loans.

Lenders that give loans in the form of cryptocurrencies can make a lot more money from their crypto assets than savings accounts. It may also be a more adaptable choice to crypto staking, which requires users to lock up their cryptocurrency and submit it to a blockchain security method. Depending on the platform, lending usually gives users access to their funds.

The downside to crypto lending

The agreement with crypto loan companies is generally made on individual terms by institution borrowers. As interest rates vary across platforms and cryptocurrencies, each company is different.

There have been several cases where lending platforms have been hit by severe liquidity crisis, notably Celsius, Voyager Digital, and BlockFi. Glenn Huybrecht, COO of Cake DeFi, said, “Some lending providers have been very generous with low collateral requirements, which then puts them in hot water when one of their customer's defaults.”

Due to the ongoing regulation battles, these crypto services are also not backed by government safety nets, like the traditional banks are. However, some platforms do hold insurance and the necessary regulatory accreditations so be sure to seek one that has all of the above.

Closing thoughts

Crypto lending platforms differ greatly from one another so be sure to check each platform, their interest rates for all the various currencies supported, and if there are any lock-up periods or fees payable.

The 49 country code is your gateway to connecting with Germany from anywhere in the world, whether you're calling a business in Berlin, family in Munich, or that cozy hotel in Bavaria you're hoping to book.

Getting the dialling format right can save you from failed calls, unexpected charges, and the frustration of hearing that dreaded "the number you have dialled cannot be completed" message.

This guide breaks down everything you need to know about calling Germany, from basic dialling steps to troubleshooting common problems that trip up even the most experienced international callers.

What is the 49 country code?

The 49 country code is Germany's designated number in the international telephone system. When you want to call any German phone number from outside Germany, you must start your call with this two-digit code.

Country codes are part of a global system managed by the International Telecommunication Union (ITU) that ensures your call reaches the right country. Think of it as an international postal code for phone calls - without it, the global telephone network wouldn't know where to route your call. The 49 code covers all of Germany, including both landline and mobile numbers.

How to call Germany from the U.S. (or abroad)

Calling Germany follows a straightforward four-step process that works from any country:

Step-by-step dialing format:

- Dial your country's international exit code

- From the U.S./Canada: 011

- From most European countries: 00

- From many Asian countries: 00

- Dial Germany's country code: 49

- Dial the German area code (drop the leading zero)

- Berlin becomes 30 (not 030)

- Munich becomes 89 (not 089)

- Dial the local phone number

Complete examples:

Calling a Berlin landline from the U.S.: 011 49 30 12345678

Calling a Munich mobile from the UK: 00 49 171 1234567

Mobile phone shortcut: Most smartphones let you use the + symbol instead of your country's exit code. Just hold down the 0 key until + appears, then dial: +49 30 12345678

The key mistake many people make? Including that leading zero from the German area code. German numbers start with 0 when dialled domestically (like 030 for Berlin), but you must drop this zero for international calls.

Common area codes in Germany

Germany uses a logical area code system where major cities have shorter, memorable codes:

Remember: When calling from abroad, always use the shorter version without the leading zero.

Smaller cities and towns have longer area codes, sometimes with 4 or 5 digits. The rule remains the same - drop that leading zero when calling internationally.

Calling German mobile numbers

German mobile numbers are easy to spot once you know the pattern. They typically start with these prefixes:

- 015x (various carriers)

- 016x (O2, E-Plus)

- 017x (T-Mobile, Vodafone)

How to call a German mobile:

Format: +49 [mobile prefix] [7-digit number]

Example: +49 171 1234567

Unlike landlines, mobile numbers don't use city-based area codes. The three-digit prefix (like 171) identifies the mobile carrier, and you'll always get seven digits after that.

Cost-saving tip: Many Germans use WhatsApp extensively, so if you're calling friends or family, ask if they prefer a WhatsApp call instead. It's free with a good internet connection and often has better sound quality than traditional international calls.

Why your call to Germany might not be working

Nothing's more frustrating than a call that won't connect. Here are the most common culprits and their fixes:

Common issues:

Wrong exit code: Using 00 instead of 011 from the U.S., or vice versa

- Fix: Check your country's correct international exit code

Including the leading zero: Dialling 011 49 030 instead of 011 49 30

- Fix: Always drop the first zero from German area codes

Missing country code: Trying to dial German numbers without the 49

- Fix: Never skip the country code when calling internationally

Incorrect mobile format: Treating mobile numbers like landlines

- Fix: Remember mobile numbers don't use city area codes

Network restrictions: Your carrier blocks international calls

- Fix: Contact your provider to enable international calling

Time zone confusion: Calling during German night hours

- Fix: Germany is GMT+2, be sure to check what the time is there before trying to call

Quick troubleshooting:

Try calling a German directory service first (like +49 11833) to test if your international dialling is working properly.

Alternative ways to call Germany

Traditional phone calls aren't your only option. Several modern alternatives can save you money and often provide better call quality:

Internet-based options:

WhatsApp: Extremely popular in Germany, free voice and video calls

Google Voice: Competitive international rates from the U.S.

Viber: Free app-to-app calling with good European coverage

FaceTime: Free for iPhone/Mac users calling other Apple devices

VoIP Providers:

Companies like Vonage, RingCentral, and 8x8 offer business-grade international calling with flat-rate plans that can be cost-effective for frequent callers.

Pros and cons:

Pros: Often free or very cheap, better call quality, video calling options

Cons: Requires internet connection, both parties might need the same app

What other country codes are similar to 49?

If you're travelling in German-speaking regions or neighbouring countries, these codes might come in handy:

- Austria: +43 (German-speaking)

- Switzerland: +41 (German is one of four official languages)

- France: +33 (borders Germany)

- Netherlands: +31 (Germany's northern neighbour)

- Belgium: +32 (close to the German border)

- Denmark: +45 (borders northern Germany)

Travel tip: Some mobile carriers offer European roaming packages that can be more cost-effective than international calling if you're travelling between these countries.

Conclusion

Calling Germany doesn't have to be complicated once you understand the basics. Remember the golden rule: use 49 as your country code, drop that leading zero from area codes, and don't forget your international exit code (011 from the U.S.).

And if in doubt, those internet-based calling options can be both your wallet's and your connection quality's best friend.

Guten Tag and happy calling!

Need to call Ireland but not sure how to dial correctly? You're in the right place. Ireland's country code is +353, and knowing how to use it properly can save you from those awkward moments when your call doesn't go through (and your phone bill doesn't thank you either).

Whether you're calling family in Dublin, conducting business in Cork, or trying to reach that charming B&B in Galway, this guide covers everything you need to know about dialling Ireland correctly. We'll walk you through the step-by-step process, common mistakes to avoid, and even some free calling options that won't break the bank.

What is the country code for Ireland?

Ireland's country code is 353. This three-digit number is what you need to dial when calling Ireland from any other country around the world.

Country codes are part of the international telephone numbering system, designed to route calls to the correct country. Think of them as postal codes for phone calls - they tell the network exactly where your call needs to go. Ireland's 353 code has been in use since the country established its modern telecommunications system.

For reference, Ireland's ISO country codes are IE (alpha-2) and IRL (alpha-3), which you might see used in forms, websites, or official documentation.

How to call Ireland from abroad

Calling Ireland follows a simple three-step formula that works from anywhere in the world:

International Access Code → Country Code → Local Number

Here's how it breaks down:

- Dial your country's international access code (011 from the US/Canada, 00 from most European countries)

- Add Ireland's country code: 353

- Dial the local number, dropping the initial "0"

Examples in Action:

From the US to Dublin: 011 353 1 234 5678

From the UK to Cork: 00 353 21 234 5678

From Germany to Galway: 00 353 91 234 5678

The key thing to remember? Always drop that initial "0" from Irish area codes when calling from abroad. Irish numbers start with 0 when dialled domestically (like 01 for Dublin), but you skip this zero for international calls.

Ireland area codes (most common by city)

Here are the most important area codes you'll need when calling different parts of Ireland:

City/region - area code

Dublin - 01

Cork - 21

Limerick - 61

Galway - 91

Waterford - 51

Drogheda - 41

Dundalk - 42

Wexford - 53

Kilkenny - 56

Athlone - 90

Sligo - 71

Letterkenny - 74

Tralee - 66

Ennis - 65

Carlow - 59

Important note: Irish mobile numbers (starting with 08) don't use area codes. You simply dial the full mobile number after the country code.

How to call Ireland from a mobile phone

Mobile phones make international calling even simpler. Instead of remembering different international access codes, you can use the universal + symbol:

Format: +353 [area code] [local number]

Examples:

- To Dublin mobile: +353 87 123 4567

- To Cork landline: +353 21 234 5678

Most smartphones automatically recognise the + symbol when you hold down the "0" key. This method works regardless of which country you're calling from - no need to remember whether it's 011, 00, or something else.

How to call Ireland for free

Who doesn't love a good bargain? Several apps and services let you call Ireland without traditional phone charges:

Internet-based calling:

- WhatsApp: Free voice and video calls (both parties need the app)

- FaceTime: Free for Apple users calling other Apple devices

- Google Meet: Free voice and video calling

- Viber: Free app-to-app calls worldwide

Pros and cons:

Pros: Completely free (just uses your internet data), often better call quality than traditional calls Cons: Both parties need the same app and a reliable internet connection

These options work brilliantly for staying in touch with friends and family, though you might still need traditional calling for businesses or official services.

Common reasons why calls to Ireland fail

Nothing's more frustrating than a call that won't connect. Here are the usual suspects and quick fixes:

Wrong country code: Double-check you're using 353, not 533 or any other combination Incorrect area code: Check that the area code matches the city you're calling

Missing digits: Irish landlines typically have 7 digits after the area code, mobiles have 7 digits after 08

Forgot to drop the zero: Remember to skip the initial "0" when calling from abroad

No international plan: Check with your provider; some plans block international calls by default

Network issues: Try calling from a different location or wait and try again

Pro tip: If you're still having trouble, try calling an Irish directory service first to test your connection.

What time is best to call Ireland?

Ireland follows Greenwich Mean Time (GMT) in winter and Irish Standard Time (GMT+1) during daylight saving time (March to October).

For business calls: Aim for 9 AM to 5 PM Irish time, Monday through Friday

For personal calls: Consider that Irish folks often have dinner around 6-7 PM, so early evening can work well

Always use a time zone converter when scheduling important calls - there's nothing quite like waking up your Irish colleague at 3am because you miscalculated the time difference.

Emergency and service numbers in Ireland

In case you ever need them, here are Ireland's essential service numbers:

- 112 and 999: Emergency services (police, fire, ambulance)

- 116000: Missing child helpline

- 116123: Emotional support helpline

These numbers are free to call from any phone in Ireland and should only be used for genuine emergencies or crises.

Conclusion

Calling Ireland is straightforward once you know the basics: use country code 353, remember to drop the initial zero from area codes, and don't forget about free internet-based calling options. Whether you're planning a business call to Dublin or want to check in with a B&B in the countryside, following these simple steps will ensure your calls connect smoothly.

For the best experience, double-check the local time before calling and keep a time zone converter handy. With these tools in your back pocket, you'll be chatting away like a pro in no time. Sláinte to successful calls!

.jpg)

The "redirect to bank" experience is dying. Today's consumers expect financial services to be invisible, integrated, and immediate.

The numbers confirm this story. The global embedded finance market is projected to reach $606 billion this year, growing to $7.2 trillion by 2030. But this isn't just about fintechs disrupting traditional banking anymore. We're witnessing something far more profound: the financialisation of every industry.

In an increasingly competitive landscape, embedded finance has become the new battleground for customer loyalty, operational efficiency, and revenue diversification.

From healthcare providers offering patient financing to property management companies issuing tenant payment cards, businesses across every sector are discovering that controlling the financial experience isn't just about convenience; it's becoming more about survival.

And the companies winning this race aren't necessarily the ones with the deepest financial services expertise. They're the ones that recognise a fundamental truth: every business is becoming a financial services company, whether they realise it or not. Let’s explore this narrative.

Mapping the embedded finance ecosystem

Understanding embedded finance requires looking beyond just payments to see the full ecosystem of financial services being woven into non-financial platforms. To put it more simply: it’s less about processing transactions and more about creating comprehensive financial experiences.

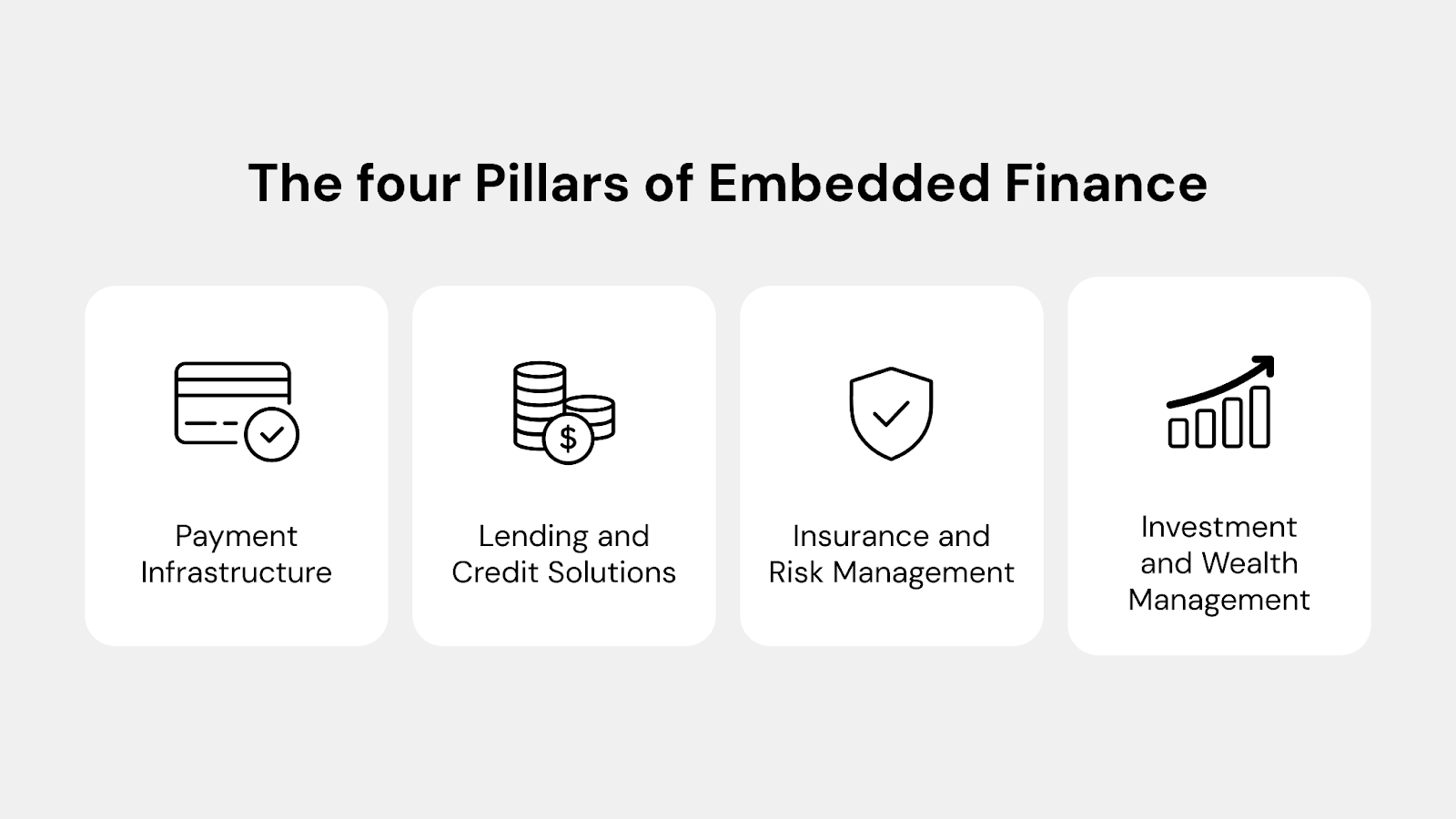

The four pillars of embedded finance

Payment infrastructure forms the foundation, encompassing everything from card issuing and digital wallets to real-time transfers and cross-border payments. This is where most companies start their embedded finance journey, but it's just the beginning.

Lending and credit solutions represent the next evolution, allowing platforms to offer instant financing, buy-now-pay-later options, and dynamic credit lines. A logistics company might offer cash advances to drivers, while an e-commerce platform provides inventory financing to sellers.

Insurance and risk management services are increasingly embedded into platforms where risk naturally occurs. For instance, ride-sharing apps offer trip insurance, rental platforms provide property protection, and gig economy apps include accident coverage.

Investment and wealth management complete the picture, with platforms offering everything from micro-investing features to full-service wealth management integrated into everyday spending activities.

The technology stack revolution

The magic happens in the middleware, where the API layers connect user-facing apps to complex financial infrastructure. Modern embedded finance platforms take away the complexity of banking operations, compliance frameworks, and regulatory requirements, allowing any company to offer sophisticated financial services through simple API calls.

And making this technology accessible is key. Where banks once had moats built from regulatory expertise and infrastructure investments, today's embedded finance platforms have levelled the playing field.

For instance, a small property management company can now offer the same calibre of financial services as a major corporation, all through cloud-based APIs and white-label solutions.

Industry deep dives: the unexpected financial innovators

The most compelling embedded finance stories are happening in industries you might not expect. Let’s explore how sectors far removed from traditional finance are leveraging embedded financial services to transform their operations:

Healthcare

Healthcare providers are embedding finance to solve patient payment collection challenges. Instead of redirecting patients to external lenders, dental practices now offer instant financing approvals directly within their systems, while telemedicine platforms integrate HSA/FSA payments and prescription processing.

The result: improved patient experience, reduced administrative overhead, and better provider cash flow.

Real estate

Proptech companies are offering customisable debit cards with built-in credit-building rewards and automated reminders, boosting tenant retention and on-time payments. While other property management utilise embedded insurance to replace traditional security deposits.

Real estate platforms can now handle everything from mortgage pre-approval to maintenance payments in one interface, while construction businesses offer instant contractor payments with automated expense tracking.

Education

Educational institutions embed financial services beyond tuition through campus spending cards, instant student aid disbursement, and skill-building microloans.

EdTech platforms offer employer-sponsored training payment cards, while international education programs solve cross-border payment complexity with embedded foreign exchange and instant fund transfers for students abroad.

Supply chain

Manufacturing and supply chain businesses optimise financial flows through embedded supplier financing and inventory funding solutions. Logistics companies provide drivers with instant payouts and controlled fuel cards, while procurement platforms automate cross-border payments and approval workflows, treating money movement as strategically as inventory management.

Entertainment

Lastly, gaming and entertainment platforms create virtual economies connected to real-world branded payment cards, while venues embed payment plans for premium experiences and refund insurance.

Creator economy platforms also provide comprehensive financial services, including instant payments, business banking, tax preparation, and investment opportunities, becoming full-service financial providers for creative professionals.

The business case: ROI beyond revenue

The financial benefits of embedded finance extend far beyond direct revenue generation. More and more businesses are starting to discover that embedded financial services can drive value through several channels at the same time.

Direct financial benefits

- Revenue diversification through interchange fees, transaction processing margins, and financial product revenue sharing can represent significant income streams. A B2B marketplace processing $100 million annually might generate $1-2 million in additional revenue through embedded card programs alone.

- Float management opportunities arise when companies hold customer funds temporarily. Even small balances across large customer bases can generate meaningful interest income when managed professionally.

- Premium service monetisation allows companies to charge higher fees for enhanced financial services while improving the customer experience. Express payment options, enhanced spending controls, and premium support can command price premiums.

Indirect value creation

- Customer lifetime value extension happens when financial services create switching costs and deepen platform engagement. Customers using embedded financial services typically show 20-30% higher retention rates and increased platform usage.

- Operational efficiency gains from automated payment processing, reduced manual reconciliation, and streamlined expense management can reduce operational costs (in midmarket companies) by 30-50% while improving accuracy and reporting capabilities.

- Data insights and behavioural analytics from financial transactions provide thorough visibility into customer behaviour, enabling better product development, pricing optimisation, and risk management decisions.

Implementation strategies & considerations

Successfully implementing embedded finance requires systematic planning and strategic decision-making focused on core business objectives.

Build vs buy vs partner framework

Cost and speed: Internal development takes 18-36 months with significant compliance costs, while white-label solutions launch in 6-12 weeks. Partnering with licensed providers reduces regulatory burden and accelerates time-to-market.

Integration options: API-first architecture enables flexible system integration. White-label solutions offer complete brand control but require more work, while co-branded approaches launch faster with shared visibility.

Implementation strategy: Consider phased rollouts (for instance, starting with basic payments and gradually adding layers such as lending or insurance) to reduce risk while enabling customer feedback integration.

Risk management essentials

Compliance: KYC/AML verification, fraud monitoring, and data security must meet financial services standards. Again, partnering with established platforms provides compliance expertise across multiple jurisdictions while maintaining a seamless user experience.

How to implement embedded finance into your business

Implementing embedded finance successfully requires systematic planning and execution. Companies that take a structured approach are more likely to achieve their objectives while minimising implementation risk.

Assessment phase

Current payment flow analysis should map all existing financial touchpoints and identify friction points, manual processes, and opportunities for improvement. Understanding current state operations provides the foundation for embedded finance strategy.

Customer journey mapping reveals where financial services integration could improve experience and create value. Look for moments where customers currently leave your platform for financial services or where payment friction creates abandonment.

Competitive landscape evaluation helps identify differentiation opportunities and best practices. Understanding how competitors and adjacent industries use embedded finance provides insight into customer expectations and market opportunities.

Strategy development

Use case prioritisation should focus on the highest-impact opportunities that align with your core business objectives. Start with use cases that solve existing problems rather than creating entirely new functionalities.

ROI modelling and business case development requires realistic assumptions about adoption rates, revenue potential, and implementation costs. Include both direct financial benefits and indirect value creation in ROI calculations.

Partner evaluation and selection should consider platform capabilities, compliance coverage, integration complexity, and long-term strategic alignment. The right partner becomes an extension of your team rather than just a vendor.

Implementation & launch

MVP development and testing allows for learning and iteration before full-scale launch. Start with core functionality and add features based on user feedback and usage patterns.

Pilot program execution with selected customer segments provides real-world validation while limiting risk exposure. Use pilot results to refine processes and optimise user experience.

Scale-up and optimisation based on pilot learnings and market feedback. Successful embedded finance implementations evolve continuously based on customer needs and market opportunities. Be sure to have your finger on the pulse.

The inevitable future

Embedded finance is more than a passing trend: it represents a fundamental shift in business operations. Companies that move early can gain lasting advantages through stronger customer relationships, new revenue streams, and greater efficiency.

The technology to implement it quickly and cost-effectively is already available, and customers increasingly expect seamless financial integration. The real question isn’t if embedded finance will become standard - it’s whether your business will lead or follow.

Don't let competitors control your customers' financial experience. Get in touch with us to explore white-label solutions that can increase retention, reduce costs, and generate new revenue quickly and compliantly. We’re here to help you transform your business in weeks, not years.

.webp)

.webp)