Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

Let's get one thing straight: most "make money while you sleep" crypto promises are complete nonsense. The internet overflows with schemes promising $10,000 monthly returns that usually end with empty wallets and regret.

But you actually can earn passive income with crypto in 2025. The keyword here is "can," not "will automatically" or "guaranteed to". The difference lies in having realistic expectations. We're talking 3-12% annual returns through legitimate methods, not the 300% fairy tales that flood social media.

Thankfully, the crypto passive income landscape has matured since 2021's wild west era. Those 20,000% APY farms that vanished overnight? They're mostly gone (though some still lurk if you fancy yourself some financial Russian roulette). Today's opportunities are more modest but actually sustainable.

This guide covers seven common methods for earning crypto passive income. You'll find beginner-friendly options yielding 3-8% annually, plus riskier strategies that could hit 15-50% if you know what you're doing. We'll also cover the less exciting but crucial stuff: taxes, risks, and how to avoid losing everything to market volatility.

If you want get-rich-quick schemes, look elsewhere. But if you're interested in building a legitimate income stream while participating in the future of finance, let's explore what's actually possible in 2025.

Let the record state that this is educational only and should not be considered financial, investment, or tax advice. Crypto yields are variable and can result in loss of principal. Verify availability, legality, and rates in your jurisdiction before participating.

Understanding crypto passive income

Before diving into specific methods, let's clarify what we mean by "passive income" in crypto. Traditional passive income might be rental properties or dividend stocks - you invest money, then collect regular payments without active work. Crypto passive income works similarly, but with a digital twist and significantly more volatility.

The fundamental difference? Traditional investments might fluctuate 5-10% annually. Your crypto holdings can swing 50% in a week. This means your "passive" income can be passive in name only if you're constantly checking prices and panicking over market moves.

Here's the reality: crypto passive income exists on a risk spectrum. On the safer end, you have crypto savings accounts offering 2-8% APY - similar to high-yield savings but with crypto.

On the riskier end, there's yield farming, where you might earn 50-200% returns, but you could also lose everything to smart contract bugs or market crashes.

All in all, the crypto passive income market has grown substantially. By 2025, over $150 billion is locked in various DeFi protocols, and some major institutions now offer crypto earning products. This legitimacy doesn't eliminate risk, but it does mean you're not dealing with fly-by-night operations (mostly).

Why do people choose crypto for passive income? Beyond potentially higher returns, it offers 24/7 market access, global opportunities, and the ability to start with small amounts. Plus, there's something satisfying about earning yield on assets you believe will appreciate long-term.

Top 7 common methods used by market participants to earn crypto passive income

Low-complexity options (recommended for beginners)

1. Crypto savings accounts

Think of these as high-yield savings accounts, but for crypto. You deposit your coins in custodial yield products from compliant exchanges (availability varies by jurisdiction), and they lend them out or use them productively, and you earn interest.

How it works: Platforms take your deposits and lend them to institutional borrowers or use them in DeFi strategies. You earn a percentage of the profits.

Realistic returns: Expect 2-8% APY depending on the cryptocurrency and platform. Bitcoin typically offers lower rates (2-4%), while stablecoins might yield 4-8%. Each platform’s APYs will vary, ensure you read all the Ts and Cs.

Getting started: Most platforms require simple KYC verification. Deposit your crypto, choose your earning product, and start accumulating interest daily or weekly.

The catch: Your funds aren't FDIC insured like traditional banks. Platform risk is real (remember Celsius and BlockFi's 2022 collapses). Only deposit what you can afford to lose, and research platform stability before committing any amounts.

2. Staking

Staking is like earning dividends for helping secure a blockchain network. Instead of energy-intensive mining, Proof-of-Stake networks rely on validators who "stake" their coins as collateral to process transactions and secure the network.

Popular staking options:

- Ethereum (ETH): typically around 2-4%

- Solana (SOL): commonly 6-8% effective rate over time (depends on inflation & stake)

- Cardano (ADA): typically around 3-5%

- Polkadot (DOT): unbonding is 28 days; rewards vary (often high-single to low-double digits).

*for accurate, real-time staking rewards, see here.

Two approaches exist: Direct staking requires technical knowledge and sometimes significant minimum amounts. Delegated staking through platforms is simpler but typically offers slightly lower returns due to fees.

Important considerations: Many staking arrangements have lock-up periods, so factor in liquidity needs before committing funds.

Getting started: For beginners, exchange-based staking offers the easiest entry. More advanced users can stake directly through wallets or run their own validators for maximum returns.

Medium-complexity methods

3. Crypto lending

Crypto lending involves loaning your crypto to borrowers in exchange for interest payments. It's more hands-on than savings accounts but potentially more profitable.

Platform lending: Services like Aave, Compound, and Kava allow you to supply liquidity to lending pools. Borrowers pay interest, which gets distributed to lenders minus platform fees.

Expected returns: Highly variable based on demand. Stablecoin lending might yield 5-15% APY, while volatile assets can range from 2-25% depending on market conditions.

Risks to consider: Smart contract vulnerabilities, platform hacks, and borrower defaults can impact returns. The 2022 DeFi winter showed that high yields don't always last.

4. Liquidity pools and providing liquidity

Decentralised exchanges (DEXs) like Uniswap and PancakeSwap need liquidity to function. By providing paired assets to liquidity pools, you earn a share of trading fees.

How it works: You deposit equal values of two cryptocurrencies (like ETH and USDC) into a pool. Traders pay fees to swap between these assets, and you earn a portion based on your pool share.

Earning potential: Returns vary widely based on trading volume and fees. Popular pairs might yield 5-30% APY, but this fluctuates with market activity.

Impermanent loss: The biggest risk unique to liquidity provision. If one asset's price changes significantly relative to its pair, you might end up with less value than if you'd simply held the original assets.

It's "impermanent" because prices could return to original ratios, but it becomes permanent if you withdraw during unfavourable price relationships.

Higher-complexity methods (for experienced DeFi users)

5. Yield farming

Yield farming is DeFi's high-stakes game. You move funds between different protocols, chasing the highest returns through complex strategies involving multiple platforms and tokens.

The appeal: Returns can have a wide range - advertised headline APYs can occasionally exceed 50% for short periods, but are highly unstable and often decay quickly.

The reality: Most high-yield farms are unsustainable. They often rely on token rewards that lose value quickly, or they're simply Ponzi-like schemes waiting to collapse.

Who should try this: Only experienced DeFi users who understand smart contract risks, token economics, and can afford total losses. Consider this speculation, not passive income.

6. Dividend-paying tokens

Some crypto projects share profits with token holders, similar to stock dividends.

Examples include:

- KuCoin Token (KCS): pays a bonus from trading fees to eligible holders (terms/eligibility apply)

- NEO: generates GAS for on-chain usage

- VeChain (VET): Produces VTHO tokens for network usage

Returns: Highly variable and dependent on platform success. KCS might yield 2-6% annually in fee sharing, while others provide minimal returns.

7. Masternodes

Masternodes are specialised servers that perform network functions beyond basic transaction processing. They require significant upfront investment but can provide steady returns.

Requirements: Most masternodes need substantial token holdings - often $10,000-$100,000+ worth. You also need technical knowledge to maintain server uptime and security.

For example, Dash requires 1,000 DASH collateral while realised ROI varies with network conditions.

Barriers to entry: High costs, technical requirements, and ongoing maintenance make masternodes unsuitable for most passive income seekers.

Reality check: how much can you actually earn?

Let's crunch some hypothetical numbers based on current market conditions:

Potential $1,000 investment scenarios:

- Crypto savings account (5% APY): $50 annual income

- ETH staking (3.2% APY): $32 annual income

- Stablecoin lending (8% APY): $80 annual income

Potential $10,000 investment scenarios:

- Diversified approach (mix of staking/lending): $400-800 annual income

- Higher-risk DeFi strategies: $1,000-2,000 annual income (with significant loss potential)

Potential $100,000 investment scenarios:

- Conservative crypto portfolio: $4,000-8,000 annual income

- Aggressive yield farming: $10,000-20,000 annual income (extremely high risk)

Compare this to traditional passive income: a 4% dividend stock portfolio on $100,000 yields $4,000 annually. Crypto can potentially beat this, but with much higher volatility and risk.

The volatility factor: Your $10,000 crypto investment might earn $800 in interest, but if the underlying assets drop 30%, you've still lost $2,200 overall. This is why many successful crypto passive income earners focus on stablecoins and accept that they're speculating on both yield and price appreciation.

Tax implications you ought to know

Crypto passive income isn't a tax-free lunch. Most tax authorities treat crypto earnings as regular income, taxed at your ordinary income rate.

Key tax considerations:

- Staking rewards are taxable when received, based on fair market value

- Lending interest counts as ordinary income

- DeFi yields are also taxable, even if paid in obscure tokens

Record-keeping is crucial. Track every reward, airdrop, and interest payment with dates and values. Many platforms provide tax reports, but you're ultimately responsible for accuracy.

International complexity: Tax treatment varies by country. Some nations offer crypto-friendly policies, while others impose heavy taxes or outright bans. Research local regulations or consult professionals for significant amounts.

When to worry: If you're earning more than a few hundred dollars annually in crypto passive income, consider professional tax help. The penalties for getting crypto taxes wrong can be severe.

Risks and how to alleviate them

Crypto passive income isn't just about earning, it's about not losing everything to avoidable risks.

Platform risk: Centralised platforms can fail, get hacked, or freeze withdrawals. Celsius and FTX's collapses wiped out billions in customer funds.

Mitigation: diversify across platforms, research financial health, and never invest more than you can afford to lose.

Smart contract vulnerabilities: DeFi protocols run on code, and code has bugs. Multi-million dollar hacks happen regularly.

Mitigation: stick to audited, established protocols and understand that "decentralised" doesn't mean "safe."

Market volatility: Crypto's wild price swings can eliminate passive income gains quickly.

Mitigation: consider stablecoins for pure yield plays, or accept volatility as part of the crypto investment thesis.

Regulatory risks: Governments can ban or heavily regulate crypto activities overnight.

Mitigation: stay informed about regulatory developments and be prepared to exit positions quickly.

Practical risk management:

- Start small while learning

- Never invest emergency funds

- Diversify across methods and platforms

- Keep detailed records

- Stay informed about protocol changes and risks

Getting started: your first steps

Ready to dip your toes in crypto passive income? Here's a sensible approach:

Start with education: Understand the basics of crypto, wallets, and the specific methods that interest you. Rushing in with poor knowledge is the fastest way to lose money.

Begin conservatively: Try crypto savings accounts or exchange-based staking with small amounts. These offer lower returns but also lower complexity and risk.

Portfolio allocation: Financial advisors often suggest no more than 5-10% of investable assets in crypto, and passive income strategies should be a subset of that. Don't bet the farm.

Platform selection criteria: Look for established companies with good reputations, proper licensing, insurance if available, and transparent fee structures. Avoid platforms promising unrealistic returns.

Security basics: Use hardware wallets for significant amounts, enable two-factor authentication, and never share private keys. The decentralised nature of crypto means lost funds are often gone forever.

Conclusion

Earning passive income with cryptocurrency in 2025 is definitely possible, but it requires realistic expectations and careful risk management. The days of guaranteed 20% returns are over, but legitimate opportunities exist for those willing to do their homework.

The sweet spot for most people lies in conservative strategies: crypto savings accounts, established staking, and perhaps some stablecoin lending. These won't make you rich overnight, but they can provide steady returns while you learn the ecosystem.

Remember that "passive" income in crypto often requires more attention than traditional investments. Stay informed, start small, and never invest money you can't afford to lose. The future of finance is evolving rapidly - earning while you learn might be the smartest approach of all.

The financial world is undergoing a significant transformation, largely driven by Millennials and Gen Z. These digital-native generations are embracing cryptocurrencies at an unprecedented rate, challenging traditional financial systems and catalysing a shift toward new forms of digital finance, redefining how we perceive and interact with money.

This movement is not just a fleeting trend but a fundamental change that is redefining how we perceive and interact with money.

Digital Natives Leading the Way

Growing up in the digital age, Millennials (born 1981-1996) and Gen Z (born 1997-2012) are inherently comfortable with technology. This familiarity extends to their financial behaviours, with a noticeable inclination toward adopting innovative solutions like cryptocurrencies and blockchain technology.

According to the Grayscale Investments and Harris Poll Report which studied Americans, 44% agree that “crypto and blockchain technology are the future of finance.” Looking more closely at the demographics, Millenials and Gen Z’s expressed the highest levels of enthusiasm, underscoring the pivotal role younger generations play in driving cryptocurrency adoption.

Desire for Financial Empowerment and Inclusion

Economic challenges such as the 2008 financial crisis and the impacts of the COVID-19 pandemic have shaped these generations' perspectives on traditional finance. There's a growing scepticism toward conventional financial institutions and a desire for greater control over personal finances.

The Grayscale-Harris Poll found that 23% of those surveyed believe that cryptocurrencies are a long-term investment, up from 19% the previous year. The report also found that 41% of participants are currently paying more attention to Bitcoin and other crypto assets because of geopolitical tensions, inflation, and a weakening US dollar (up from 34%).

This sentiment fuels engagement with cryptocurrencies as viable investment assets and tools for financial empowerment.

Influence on Market Dynamics

The collective financial influence of Millennials and Gen Z is significant. Their active participation in cryptocurrency markets contributes to increased liquidity and shapes market trends. Social media platforms like Reddit, Twitter, and TikTok have become pivotal in disseminating information and investment strategies among these generations.

The rise of cryptocurrencies like Dogecoin and Shiba Inu demonstrates how younger investors leverage online communities to impact financial markets2. This phenomenon shows their ability to mobilise and drive market movements, challenging traditional investment paradigms.

Embracing Innovation and Technological Advancement

Cryptocurrencies represent more than just investment opportunities; they embody technological innovation that resonates with Millennials and Gen Z. Blockchain technology and digital assets are areas where these generations are not only users but also contributors.

A 2021 survey by Pew Research Center indicated that 31% of Americans aged 18-29 have invested in, traded, or used cryptocurrency, compared to just 8% of those aged 50-64. This significant disparity highlights the generational embrace of digital assets and the technologies underpinning them.

Impact on Traditional Financial Institutions

The shift toward cryptocurrencies is prompting traditional financial institutions to adapt. Banks, investment firms, and payment platforms are increasingly integrating crypto services to meet the evolving demands of younger clients.

Companies like PayPal and Square have expanded their cryptocurrency offerings, allowing users to buy, hold, and sell cryptocurrencies directly from their platforms. These developments signify the financial industry's recognition of the growing importance of cryptocurrencies.

Challenges and Considerations

While enthusiasm is high, challenges such as regulatory uncertainties, security concerns, and market volatility remain. However, Millennials and Gen Z appear willing to navigate these risks, drawn by the potential rewards and alignment with their values of innovation and financial autonomy.

In summary

Millennials and Gen Z are redefining the financial landscape, with their embrace of cryptocurrencies serving as a catalyst for broader change. This isn't just about alternative investments; it's a shift in how younger generations view financial systems and their place within them. Their drive for autonomy, transparency, and technological integration is pushing traditional institutions to innovate rapidly.

This generational influence extends beyond personal finance, potentially reshaping global economic structures. For industry players, from established banks to fintech startups, adapting to these changing preferences isn't just advantageous—it's essential for long-term viability.

As cryptocurrencies and blockchain technology mature, we're likely to see further transformations in how society interacts with money. Those who can navigate this evolving landscape, balancing innovation with stability, will be well-positioned for the future of finance. It's a complex shift, but one that offers exciting possibilities for a more inclusive and technologically advanced financial ecosystem. The financial world is changing, and it's the young guns who are calling the shots.

Money talks, but some currencies whisper so quietly you need a magnifying glass to hear them. In the grand theatre of global finance, not all currencies are created equal, while some strut around like peacocks (looking at you, Kuwaiti Dinar), others shuffle about with the confidence of a wet paper bag.

The Lebanese Pound (LBP) currently holds the unfortunate distinction of being the world's weakest currency in 2025, with an exchange rate so low that one U.S. dollar equals approximately 89,500 Lebanese pounds. To put this in perspective, you'd need a small suitcase to carry the equivalent of $100 in Lebanese pounds, assuming you could find enough physical notes.

Currency weakness isn't just about having a lot of zeros after the decimal point. It reflects a complex web of economic factors, including inflation rates, political stability, monetary policy decisions, and investor confidence. This guide on the world's weakest currencies in 2025, explores the economic stories behind their struggles and what it means for the countries (and the people) who use them.

Top 10 weakest currencies in the world (2025)

Here's the lineup of currencies that make your wallet feel surprisingly heavy when travelling abroad:

Exchange rates are approximate and fluctuate daily. Data compiled from multiple financial sources as of July 2025.

What makes a currency weak?

Before we roll our eyes at long strings of zeros, let’s get clear on what actually drives currency weakness.

Exchange rates show how much of one currency you need to buy another, usually measured against the U.S. dollar. But a low exchange rate isn’t automatically a red flag. Just like shoe sizes, bigger numbers aren’t necessarily worse, they’re just different.

The real reasons a currency weakens?

- Persistent inflation that eats away at value

- Short-term monetary policies that undermine long-term confidence

- Trade imbalances and shrinking foreign reserves

- Political instability that rattles investor trust

When investors lose faith, money moves fast, and exchange rates feel the impact. In short, weak currencies aren’t a punchline, they’re a signal of deeper economic tension.

Country spotlights - case studies behind the weakest currencies

Lebanon | A financial collapse without precedent

Lebanon’s currency crisis is a case study in how not to run an economy. As of mid-2025, the Lebanese pound trades at over 89,500 LBP per USD, making it one of the weakest currencies in the world.

The collapse stemmed from a banking sector that functioned like a state-sponsored Ponzi scheme: banks attracted deposits with sky-high interest rates, only to lend most of those funds to a debt-laden government. When confidence evaporated, the system imploded. Add in the 2019 mass protests and the devastating 2020 Beirut port explosion, and the result was economic freefall.

Today, Lebanese citizens navigate a surreal economy where ATMs limit withdrawals to tiny amounts, and many businesses have shifted to unofficial dollar pricing. A shadow economy thrives alongside the official one, proof that when trust in institutions fails, people find their own workarounds.

Iran | Sanctions, inflation, and isolation

The Iranian rial now trades at over 1,000,000 IRR per USD (yes, that's six zeros). Sanctions have cut Iran off from the global financial system, leaving its oil-rich economy unable to fully monetise its most valuable resource.

It's like owning a garage full of Ferraris with no keys to drive them. In response, Iran has attempted to bypass sanctions with crypto experiments and barter agreements, but none have stabilised the currency.

Inflation routinely exceeds 40%, and as a result Iranians have turned to gold, property, and U.S. dollars to preserve what little value they can. In a country known for its resilience, the rial’s collapse remains a stark reminder of the long-term costs of economic isolation.

Vietnam | Weak by design, not disaster

The Vietnamese dong trades at around 26,000 VND per USD, but that doesn’t signal a crisis, it actually reflects deliberate policy. Vietnam maintains a weaker currency to keep exports competitive, a strategy known as competitive devaluation.

This has helped transform Vietnam into a global manufacturing hub, attracting companies looking to diversify away from China. It's like running a permanent sale on your national output - foreign buyers love the prices, and Vietnamese factories stay busy.

The challenge lies in balance. The government works to avoid the inflation traps that have plagued other countries on this list, proving that not all weak currencies come from failure, some are tools of long-term economic strategy.

Laos | Trapped by debt and dependency

The Laotian kip now trades at around 21,800 LAK per USD, weighed down by inflation above 25% and a debt-to-GDP ratio over 125%. Much of that debt is owed to China, tied to major infrastructure projects that haven’t yet paid off economically.

Laos is a landlocked nation with limited industrial capacity and high import dependence, leaving its currency exposed whenever commodity prices shift. With little monetary wiggle room, the kip’s trajectory reflects deeper economic vulnerabilities.

Sierra Leone | A currency redefined, but still fragile

In 2022, Sierra Leone redenominated its currency, removing three zeros from the leone to simplify transactions. But even the new leone remains weak due to decades of disruption: civil war, the Ebola outbreak, COVID-19, and swings in diamond prices.

This is an economy that's faced shock after shock, and recovery is slow. The mining sector, especially diamonds, still dominates, leaving the leone vulnerable to commodity price drops.

Healthcare challenges and limited infrastructure add even more pressure, reducing productivity and increasing fiscal strain. The leone’s weakness tells the story of a country rebuilding piece by piece, with its currency reflecting both the past and the uphill path ahead.

Why some countries choose to keep their currency weak

Believe it or not, some countries actually prefer their currencies to be weaker - and for good economic reasons. It's counterintuitive, like preferring to drive in the slow lane, but the strategy can be remarkably effective.

Export competitiveness represents the primary motivation. A weaker currency makes domestic products cheaper for foreign buyers, essentially providing a permanent discount. German cars might be excellent, but if Vietnamese motorcycles cost 70% less due to currency differences, guess which ones developing countries will buy?

Countries like China famously maintained an artificially weak currency for decades, helping fuel their manufacturing boom. The strategy worked so well that other countries accused them of "currency manipulation" - the economic equivalent of being too good at a game and getting accused of cheating.

However, this approach carries significant risks. Import costs rise dramatically, making everything from oil to smartphones more expensive for domestic consumers

Long-term currency weakness can also trigger capital flight, where wealthy citisens move their money abroad. When your own citisens don't trust your currency, convincing foreigners becomes considerably more challenging.

Does a weak currency mean a weak economy?

We’ve established that a weak currency doesn't automatically signal economic disaster,sometimes it's just a reflection of different economic structures and historical circumstances.

Indonesia and Vietnam serve as the best examples of countries with numerically weak currencies but relatively strong economies. Both nations have achieved consistent growth, reduced poverty, and built increasingly diversified economies despite their currencies requiring calculators to count properly.

The key lies in purchasing power parity - what matters isn't how many zeros follow your currency symbol, but what those zeros can actually buy. A Vietnamese worker earning 10 million dong monthly isn't necessarily poor if that amount provides a comfortable living standard within the Vietnamese economy.

The real measure of economic health involves factors like employment rates, productivity growth, infrastructure development, and living standards. A country with a weak currency but growing wages, improving infrastructure, and expanding opportunities may be economically healthier than a nation with a strong currency but declining industries and rising unemployment.

What are the consequences of a weak currency?

In essence, a weak currency makes daily life more expensive, with rising prices on imports like food, fuel, and electronics. Added into the mix, Inflation erodes savings, and capital flight accelerates as people move their money into more stable currencies.

Over time, foreign currencies may replace the local one in everyday use, limiting government control. Internationally, weak currencies hurt credit ratings and investor confidence, reinforcing instability.

Final thoughts

Currency weakness is more than just numbers, it’s a signal. We’ve learnt above that it can both expose deep economic flaws or reflect deliberate strategies for growth. Lebanon and Iran highlight how instability and isolation can erode value fast, while Vietnam shows how weakness can fuel exports and development.

These disparities then shape the country’s trade, capital flows, and financial stability worldwide, causing a wider ripple effect. In a global economy, no currency moves alone; each affects the rest. And behind every weak currency are real people navigating inflation, opportunity, or uncertainty.

In this article, we're covering what transaction fees are and taking a look at which cryptocurrencies offer the lowest transaction fees in 2025.

While long-term traders are less likely to be affected by transaction fees, short-term traders and people actively using cryptocurrencies continue to be plagued by excessive fee structures.

This ongoing concern has accelerated the adoption of layer 2 solutions, where transactions can be executed more quickly and cost-effectively, as well as the development of new blockchain platforms entirely.

We've also seen increased focus on zero-fee alternatives and innovative consensus mechanisms that eliminate traditional mining costs. Sounds good, right? Let’s get into it.

What are transaction fees?

Transaction fees are fees paid to the miner or validator of the network to execute the transaction. While some networks differ in how they operate, transaction fees are consistent across the board (Proof of Work mechanisms use miners, while Proof of Stake ones use validators).

How transaction fees work on Proof of Work networks

Looking at Bitcoin as an example, when a user sends BTC the transaction is entered into a pool of pending transactions known as a mempool.

The miner will then pick up a batch of transactions and validate them, checking to see whether the original wallet does, in fact, have the funds to send and if the wallet addresses are valid. Once the transaction is executed, the data relevant to the transaction is added to a block, which is chronologically added to the blockchain.

As compensation to the miner for their time and electricity, they earn a small crypto transaction fee from each transaction, as well as a reward for adding the block, known as a miner's reward. This process also ensures the safety and integrity of the network.

When the networks are very busy, the cost of sending a transaction increases. Users can then choose to pay a higher crypto transaction fee in order to prioritise their transaction in the mempool.

How transaction fees work on Proof of Stake networks

Proof of Stake (PoS) networks operate differently from traditional Proof of Work systems like Bitcoin. In PoS networks, validators are chosen to propose and validate blocks based on their stake (the amount of crypto they hold and have locked up) rather than computational power. When you send a transaction on a PoS network, validators collect and validate these transactions in exchange for transaction fees and block rewards.

The key difference is that PoS networks typically consume much less energy since they don't require intensive computational work. This often results in lower transaction fees compared to Proof of Work networks, as validators don't need to cover the same electricity costs. Popular PoS networks include Ethereum (since its transition in 2022), Solana, Cardano, and Polkadot.

Like PoW networks, when networks are very busy, the cost of sending a transaction also typically increases. Users can then also choose to add a higher crypto transaction fee to prioritise their transaction in the mempool.

Transaction fees for smart contracts are mostly much higher, as they are based on how much electricity will be needed to complete the task.

Note: generally speaking, the terms “transaction fee” and “network fee” can be used interchangeably. They both refer to the transaction fee necessary by the network for the transaction to get processed.

Exchange fees refer to something else entirely. Exchange fees are fees charged by the exchange in order to conduct the service. Be sure to check before executing a transaction on an exchange, as you might be required to pay a transaction fee (or network fees) as well as exchange fees.

How to pay less for transaction fees

A transaction fee is imperative to your transaction getting executed on most networks, so it cannot be avoided entirely. However, there are several ways to reduce the amount you need to pay.

Transaction fees increase when networks are busy, so sending your transaction during quieter periods is a great way to reduce costs. Typically, busier periods occur during business hours in major trading regions like the United States and Asia.

Look out for the Lightning Network for Bitcoin, layer-2 scaling solutions for Ethereum (such as Polygon, Arbitrum, and Optimism), and consider cryptocurrencies with inherently low fees or zero-fee architectures. These provide cost-effective solutions to high transaction costs.

Which cryptocurrency has the lowest average transaction fee?

Let’s look at some of the lowest-fee cryptocurrencies and their average transaction costs at the time of writing in 2025.

Nano (NANO) - Near $0 per transaction

Nano stands out as a cryptocurrency with zero transaction fees, making it the most cost-effective option for users seeking to avoid transaction costs entirely. Thanks to its unique block-lattice structure that doesn't rely on miners, Nano provides almost instant transaction speeds while maintaining complete fee elimination. This makes it a common go-to for frequent micro-transactions and real-world payments where every cent counts.

Stellar (XLM) - $0.00001 per transaction

Stellar charges a tiny $0.00001 per transaction, commonly used for cheap international payments. Designed specifically for cross-border transactions and financial inclusion, Stellar's minimal fees and fast settlement times have made it a favourite among payment providers and individuals sending money globally.

XRP - $0.0002 per transaction

Ripple (XRP) charges $0.0002 fees with impressively fast global transfers. Developed by Ripple Labs, XRP remains optimised for fast, affordable cross-border payments, with a continued focus on serving financial institutions and remittance providers.

Its minimal costs and consistent 4-second transaction times have made it a common choice for users and institutions alike.

Solana (SOL) - $0.00025 per transaction

Solana is known for being one of the lowest gas fee cryptos, costing close to $0.00025 per transaction. The network stands out for its lightning-fast transactions, typically wrapping up in about 2.5 seconds.

Thanks to its scalable design, Solana can handle many transactions simultaneously, making it widely adopted by dapps and major blockchain projects. This efficiency has maintained Solana's position as a top-10 crypto by market cap throughout 2025.

Bitcoin Cash (BCH) - $0.01 per transaction

Bitcoin Cash maintains its position with an attractive $0.01 average transaction fee. As a Bitcoin fork, BCH continues to be engineered for faster, more affordable transfers via its larger block sizes.

The consistently low fees on Bitcoin Cash have helped BCH remain in use as a cost-effective blockchain and low-cost market entry option.

Litecoin (LTC) - $0.05 per transaction

Litecoin continues to stand out as one of the cheapest crypto options, maintaining its average cost of around $0.01 - $0.05 per transfer.

As an early pioneer in the space, Litecoin was designed with speedy 2.5-minute transaction times and affordable payments in mind, building upon and refining Bitcoin's underlying technology.

Dogecoin (DOGE) - $0.055 per transaction

Despite its meme origins, DOGE offers practical benefits for crypto users, particularly in terms of transaction costs. The average transaction fee for Dogecoin is approximately $0.055, making it an economical choice for small-scale and frequent transactions.

With fast 1-minute transaction times and continued community support, Dogecoin is often used for micro-transactions like tipping and donations.

Trade smart, trade with Tap

Users can trade all the tokens mentioned above with equally impressive low-cost exchange fees directly on the Tap app. Adding to the cost-effective nature of the platform, it also offers heightened security and added convenience.If you’re looking to trade these tokens, Tap offers low exchange fees with added security and convenience. Learn more in the Tap app.

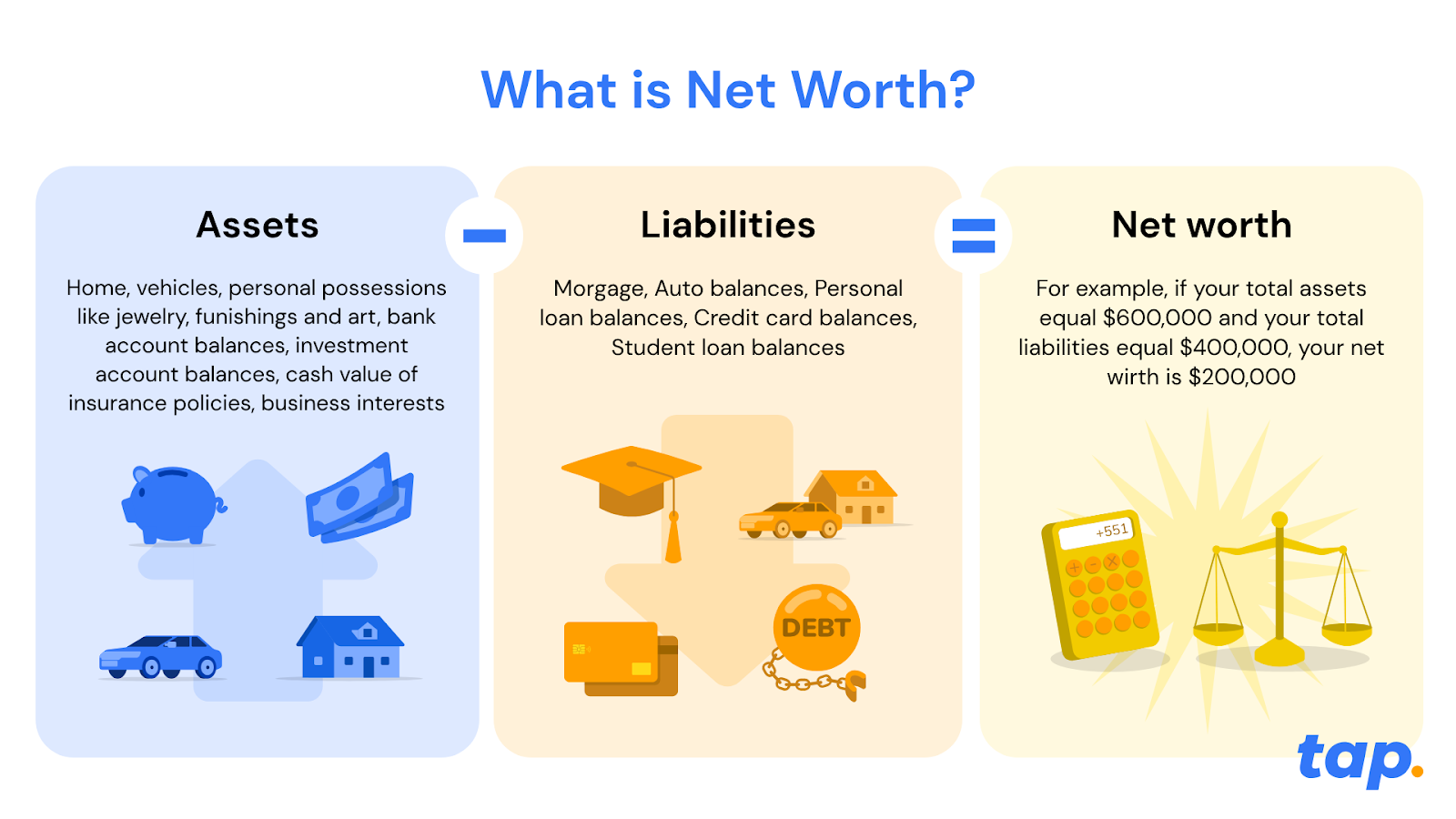

Ever wondered if you're winning or losing the money game? Your net worth holds the answer - and it's easier to calculate than you think.

What is net worth? (and why should you care?)

Think of net worth as your financial report card. It's the ultimate measure of your financial health - not how much you earn, but how much you're actually worth.

Here's the simple truth: net worth = what you own - what you owe

Unlike your salary (which just shows your monthly income), net worth gives you the big picture. It's like comparing a snapshot to a full movie of your financial life.

Why net worth beats income every time

You might earn $100,000 a year, but if you owe $150,000 in debt with only $20,000 in assets, your net worth is actually negative $130,000. Meanwhile, someone earning $50,000 with $200,000 in assets and $50,000 in debt has a net worth of $150,000. Who's really ahead?

The net worth formula

Assets (the good stuff you own)

- Real Estate: Your home, investment properties, land

- Investments: Stocks, bonds, mutual funds, crypto

- Retirement accounts: pension funds

- Cash & savings: Bank accounts, CDs, money market accounts

- Valuable possessions: Cars, jewellery, art, collectables

- Business interests: Ownership stakes, equipment

Liabilities (what's draining your wealth)

- Mortgages: Home loans, investment property loans

- Student loans: Education debt

- Credit cards: Outstanding balances

- Auto loans: Car payments

- Personal loans: Any other borrowed money

- Outstanding bills: Medical debt, taxes owed

How to calculate your net worth (3 simple steps)

Step 1: List your assets

Add up everything valuable you own. Be honest but don't undervalue quality items.

Step 2: Total your liabilities

List every debt, loan, and outstanding balance. Yes, even that store credit card.

Step 3: Do the maths

Assets - liabilities = your net worth

Real-world examples: Meet Sarah and Mark

Sarah's success story

Assets:

- Home: $400,000

- Savings: $50,000

- Investment Portfolio: $150,000

- 401(k): $200,000

- Vehicle: $20,000

- Total Assets: $820,000

Liabilities:

- Mortgage: $200,000

- Student Loan: $30,000

- Total Liabilities: $230,000

Sarah's net worth: $590,000

Sarah's doing great! Her assets significantly outweigh her debts.

Mark's comeback journey

Assets:

- Car: $10,000

- Personal Items: $5,000

- Total Assets: $15,000

Liabilities:

- Student Loans: $50,000

- Credit Cards: $8,000

- Medical Bills: $3,000

- Total Liabilities: $61,000

Mark's net worth: -$46,000

Mark has negative net worth, but this is his starting point, not his destiny.

6 reasons why it’s beneficial to grow your net worth

Financial security

Increasing your net worth provides a foundation of financial security. As your net worth grows, you have a greater buffer against unexpected expenses, job loss, or economic downturns. It offers a safety net to navigate through challenging times and helps you maintain stability in your financial life.

Achieving financial goals

A higher net worth enables you to achieve your financial goals and aspirations. Whether it's buying a home, starting a business, funding education, or retiring comfortably, a growing net worth provides the necessary resources and financial freedom to pursue your dreams.

Building wealth

Net worth is a measure of your wealth accumulation over time. By actively growing your net worth, you increase your overall wealth and improve your financial position. It allows you to build a stronger foundation for yourself and potentially leave a legacy for future generations.

Better financial opportunities

A higher net worth opens doors to better financial opportunities. It improves your borrowing capacity, allowing you to secure favourable loan terms and interest rates when needed. Additionally, a strong net worth can attract investment opportunities and partnerships that can further boost your wealth.

Flexibility and choices

Increasing your net worth provides you with more flexibility and choices in life. It affords you the freedom to make decisions based on what aligns with your long-term goals and values, rather than being constrained by financial limitations. A growing net worth expands your options and empowers you to take calculated risks or make life-changing decisions with confidence.

Peace of mind

Knowing that your net worth is growing can bring peace of mind. It reduces financial stress and anxiety, allowing you to focus on other aspects of your life. A positive net worth provides a sense of control over your financial well-being and offers peace of mind that you are on the right track towards a secure financial future.

Tips for increasing your net worth

Boost your income

- Level up your career: Ask for raises, pursue promotions, learn high-value skills

- Create side hustles: Freelancing, online businesses, passive income streams

- Invest in yourself: Education and skills that increase your earning power

Supercharge your assets

- Diversify smartly: Don't put all eggs in one basket

- Think long-term: Focus on assets that appreciate over time

- Get professional help: Financial advisors can spot opportunities you might miss

- Review regularly: Markets change - your strategy should too

Crush your debt

- Target high-interest debt first: Credit cards are wealth killers

- Consider consolidation: Lower interest rates = more money for you

- Create a payoff plan: Set deadlines and stick to them

- Avoid new debt: Unless it's for appreciating assets

Master the long game

- Emergency fund: 3-6 months of expenses (minimum!)

- Retirement planning: Start early, contribute consistently

- Professional guidance: Sometimes paying for advice saves you thousands

- Track progress: What gets measured gets improved

The bottom line: your financial transformation starts now

Your net worth isn't just a number; it's your financial GPS, showing exactly where you stand and where you're headed. Whether you're starting with negative net worth like Mark or building on a solid foundation like Sarah, the principles remain the same.

Remember: Every financial giant started with a single step. Your current net worth is just your starting line, not your finish line.

Start tracking your net worth today, and watch as this simple practice transforms not just your bank account, but your entire relationship with money. Your future self will thank you!

Ready to take control of your financial destiny? Calculate your net worth this week and set your first wealth-building goal. The journey to financial freedom starts with knowing where you stand.

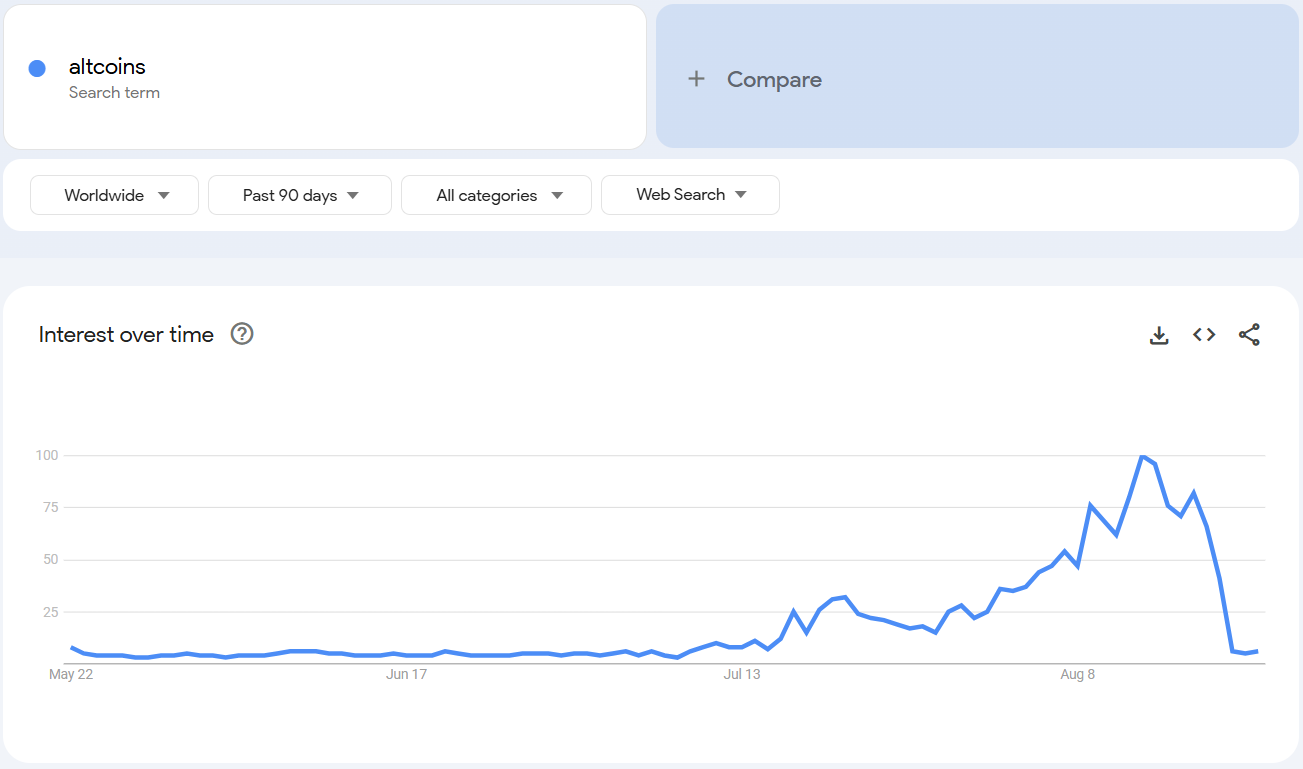

For a fleeting moment, it looked like altcoin season was finally here. Google searches for “altcoins” skyrocketed to record highs, 𝕏 was buzzing, and retail excitement seemed to return in full force. But within a week, that hype fizzled out almost as quickly as it appeared, leaving traders wondering if the long-awaited alt season was just a mirage.

A Spike That Vanished Overnight

Search interest for “altcoin” on Google Trends hit its highest score ever in early August, only to fall back to baseline levels within days. Globally, the same pattern played out, with scores dropping from 100 to just 16 in a week, mimicking a “pump and dump” pattern that you would expect from a memecoin.

Market cap data told the same story. The total value of altcoins (excluding Bitcoin and Ethereum) briefly climbed by $100 billion before giving it all back, leaving investors wondering whether the hype had any real weight behind it.

Naturally, some saw the collapse as proof that the altcoin season had ended before it really began. Others, however, like analyst Cyclop, argue the spike shows something deeper: that “altcoin” has become the mainstream term retail uses today, replacing “crypto” in 2021. In his view, this isn’t the peak. Rather, it’s just the beginning of broader interest.

Why Google Trends Doesn’t Tell the Whole Story

Relying on Google searches to measure retail demand may no longer work the way it used to. With AI tools increasingly replacing traditional search, and with concepts like “altcoins” now part of everyday investor vocabulary, Trends data might not be capturing where and how money is really flowing.

Instead, analysts point to on-chain and trading activity as better indicators of where momentum is building. And in August, that momentum was fragmented.

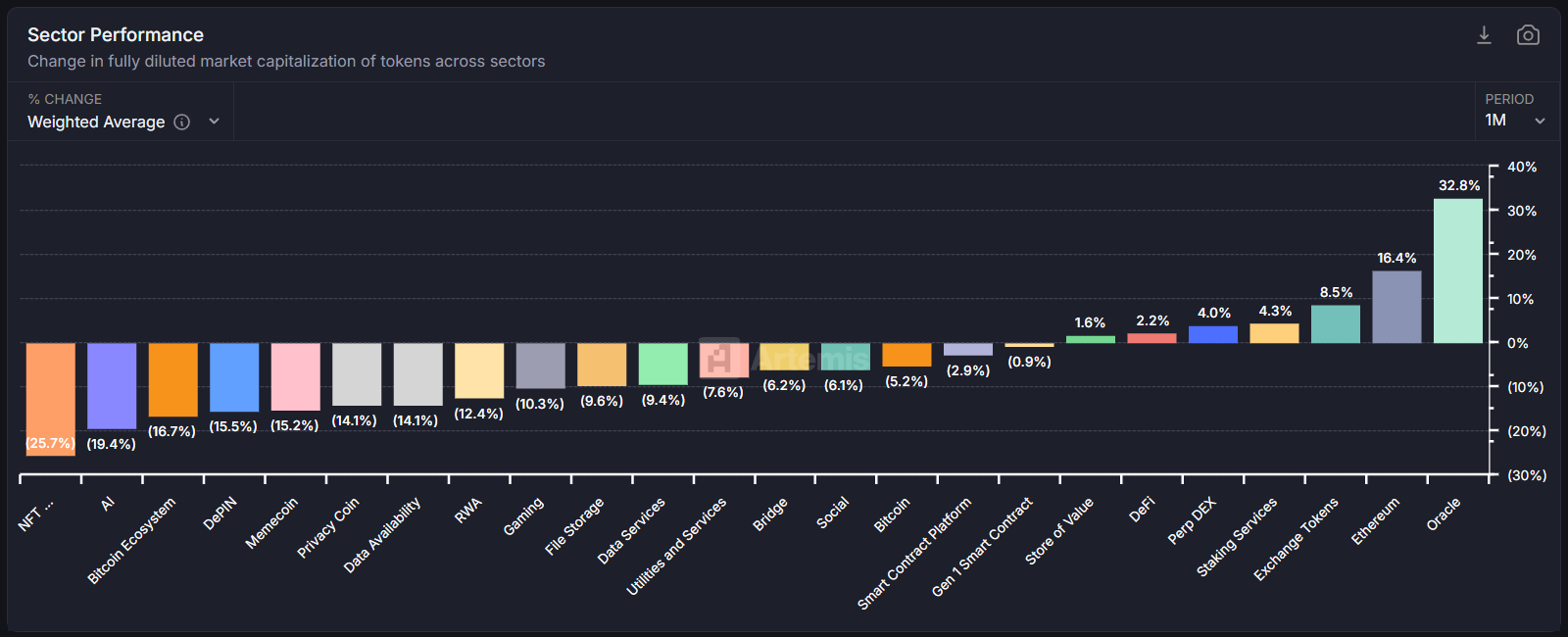

A Season of Winners and Losers

Data from Artemis showed only a few categories outperforming last month: Ethereum, exchange tokens, and oracles.

Beyond these bright spots, however, most altcoins struggled. The result? A patchwork “mini season” rather than the explosive, across-the-board surge that retail and social media had been hoping for.

Polygon’s co-founder Sandeep put it bluntly: "Retail is searching, but institutions aren't buying the narratives yet. Old altcoin seasons were driven by speculation and promises and narratives and marketing. Institutional money is smarter money. It cares about real utility and cash flows. The next "alt season" won't look like 2017 or 2021. It’ll be fewer tokens with actual usage, not just tokens with better marketing." Sandeep said.

The Road Ahead

That doesn’t mean altcoin season is dead, it probably just means it’s evolving. Coinbase has suggested that the next true wave could arrive as early as September, but that it likely won’t be a full-scale altcoin season.

Bottom line? The altcoin season isn’t gone; it’s just different. It’s maturing. And the next leg up may not belong to every token in the market, but only to the select few proving they can deliver value beyond mere speculation.

.webp)

.webp)