After a volatile October, crypto faces a defining moment. Discover what's fueling both the bullish and bearish cases right now.

Keep reading

After a volatile October that saw one of the sharpest two-day liquidations of the year, the crypto market is trying to regain its footing, but conviction remains divided. Bitcoin has stabilized near key support levels, while altcoins fight against selling pressure. With macro, policy, and on-chain factors all in play, the debate between the bull and bear camps is as alive as ever. Let’s unpack the forces shaping both sides of the ledger.

The Bear Case

When Good News Don’t Move Prices

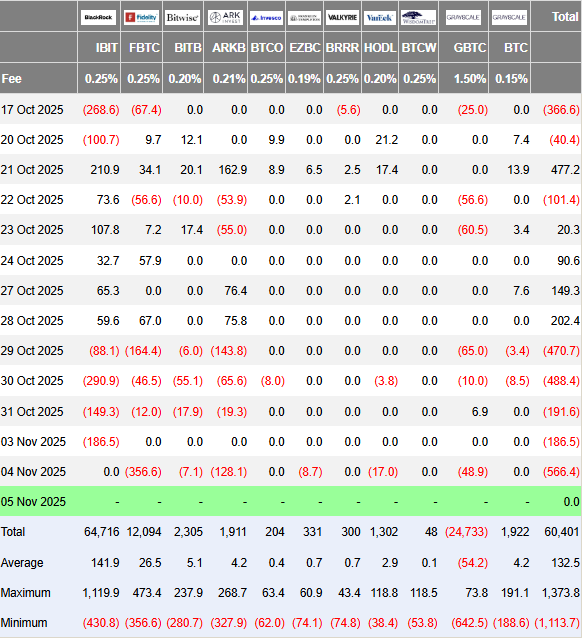

Despite encouraging ETF data and easing rate expectations, crypto failed to rally in late October, a classic warning sign of risk fatigue. According to Farside Investors, U.S. spot Bitcoin ETFs saw outflows of $470 million, $488 million, and $191 million between October 29 and 31, signaling that short-term traders were taking profits or stepping aside after “Uptober” fizzled out.

The AI Narrative

Macro sentiment still casts a long shadow. The tech-heavy equity rally, driven by AI infrastructure and chip stocks, has stirred debate about overvaluation. Nvidia’s brief breach of a $5 trillion valuation in late October triggered flashbacks of the dot-com era. If AI equities begin to deflate, crypto could feel the wealth effect unwind, as liquidity shifts from speculative assets to safer havens.

The 10/10 Crash Aftershock

The October 10 downturn marked one of the largest single-day liquidations in recent memory. Analysts note that this event left traders hunting for “dead entities” and potential hidden losses, injecting caution across the market. Even with recovery underway, scars from that drop remain fresh.

Post-Halving Cycle Timing

Bitcoin’s halving on April 20, 2024 (block 840,000) reset expectations, but it also reignited the age-old question: where are we in the cycle? Historically, the strongest rallies have occurred before or shortly after the halving, not a full year later. Some analysts now argue that the current consolidation could represent a late-cycle phase rather than the start of a new one.

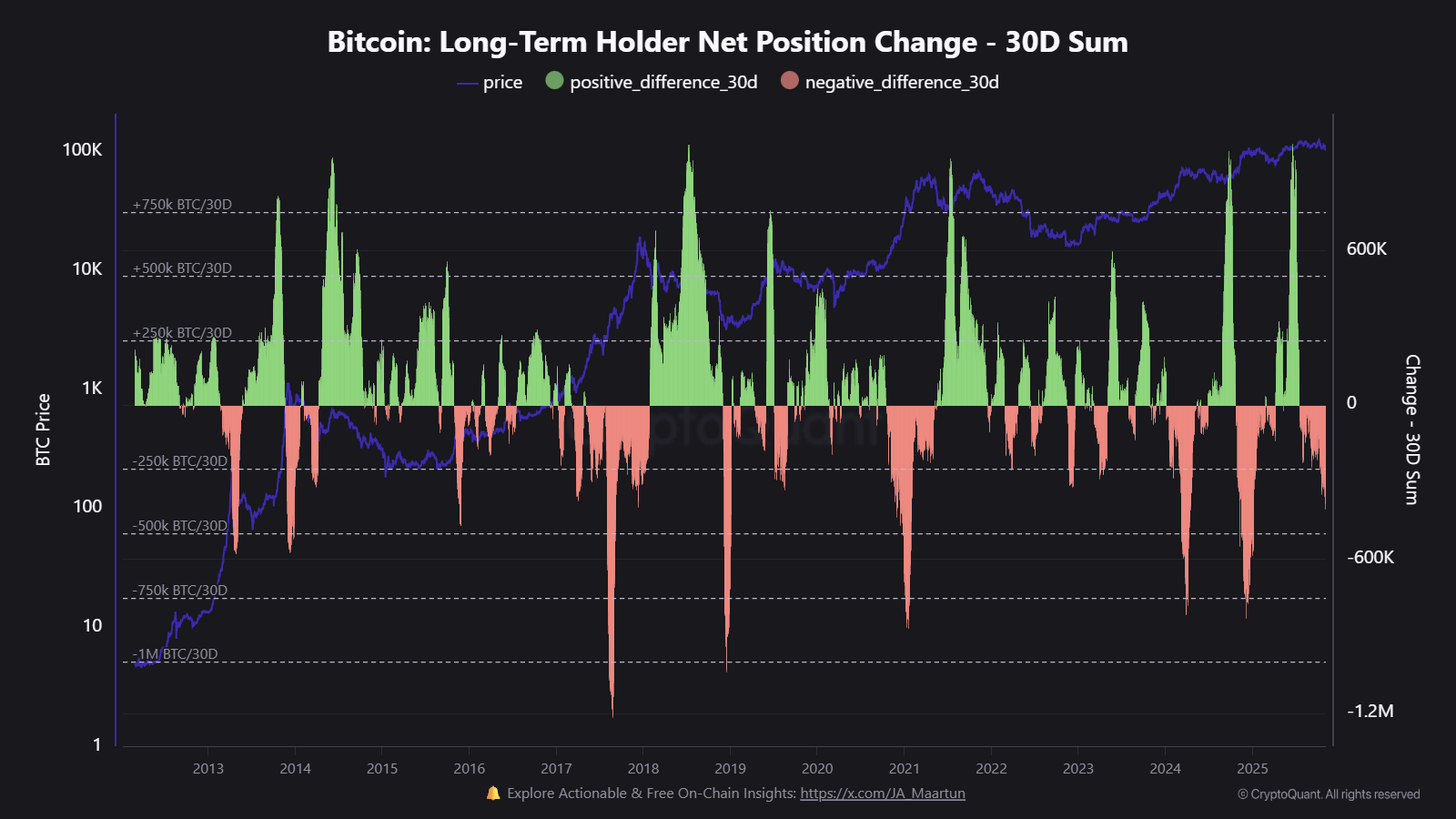

Dormant Wallets Awakening

On-chain data from CryptoQuant shows that long-term holders have increased net distribution since mid-October, with tens of thousands of BTC re-entering circulation. Several Satoshi-era wallets have also moved funds, not necessarily bearish in isolation, but enough to add pressure and short-term supply.

The Bull Case

No Signs of Euphoria

Market positioning remains far from overheated. The Crypto Fear & Greed Index currently sits in the 20s, and has been recently hovering between “Fear” and “Neutral.” That’s a far cry from the exuberant 80s to 90s readings that often precede blow-off tops. In practical terms, this suggests there’s still room for sentiment to improve before the market becomes dangerously crowded.

Liquidity Is Turning

Central banks are easing. The European Central Bank has already paused, the Bank of England has begun cutting, and the U.S. Federal Reserve is expected to follow suit with at least one more rate cut by year-end. According to the CME FedWatch Tool, the odds of a 0.25% cut currently stand above 70%. Historically, easing cycles have correlated strongly with renewed crypto uptrends, as lower yields push investors back into risk assets.

Institutional Adoption Keeps Compounding

Spot ETFs remain the biggest driver of credibility and inflows this year. Despite short-term outflows, global crypto investment products reached $921 million as recently as last week. That steady institutional presence gives crypto markets deeper liquidity and a stronger foundation than in previous cycles, where retail speculation dominated.

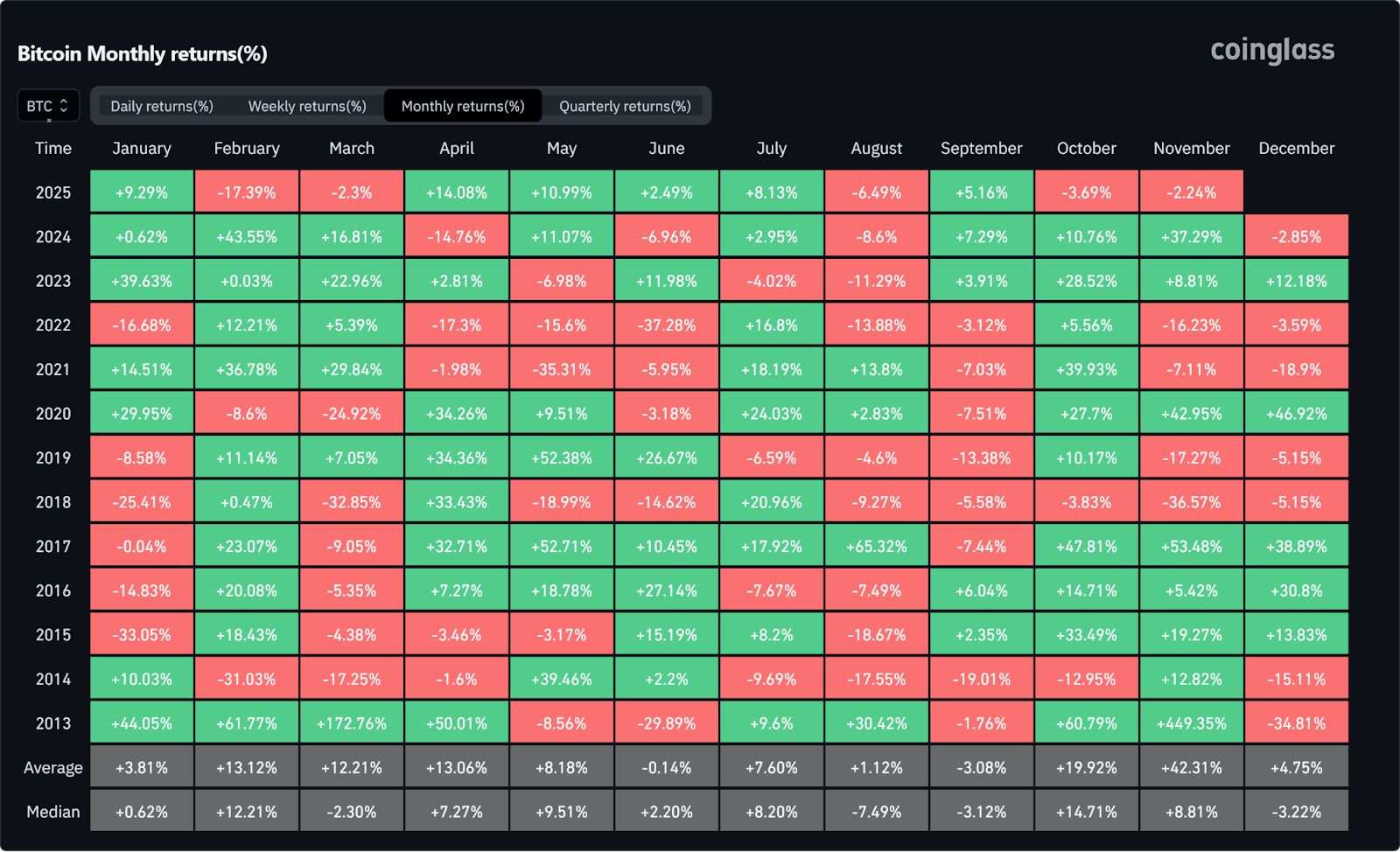

The Seasonal Edge

Seasonality adds another bullish data point. Since 2013, Q4 has consistently been Bitcoin’s strongest quarter on average. With November historically delivering above-average performance, many traders see the current consolidation not as a ceiling, but as a potential setup, particularly if macro data softens and ETF inflows resume.

Improving Global Sentiment

Finally, the U.S.–China trade thaw is a quiet but important catalyst. China has agreed to pause 24% tariffs on U.S. goods, marking the most significant de-escalation yet. For global risk assets, that’s a relief valve, potentially restoring confidence in emerging markets and crypto alike.

Final Verdict

Crypto’s tug-of-war between optimism and caution is far from over. The bull camp points to liquidity, policy progress, and institutional growth as evidence of a maturing ecosystem. The bears, on the other hand, warn that cycle timing, macro fragility, and old-wallet selling could cap any short-term rally.

Currently, the most realistic view lies somewhere in between these two extremes. After October's flash crash sent shockwaves through the market, a period of recalibration has taken hold. Whenever the next significant high arrives, the current environment may be best described not as peak fear or euphoria, but as consolidation.

NEWS AND UPDATES

LATEST ARTICLE

When Satoshi Nakamoto created Bitcoin, he designed it in such a way that should the value increase dramatically, there would still be an inclusive decimal value for the masses. Satoshis could one day be how we buy a cup of coffee anywhere in the world, using the same currency from Britain to Japan.

How Many Satoshis Are in One Bitcoin?

Often shortened to SAT, Satoshi is the smallest unit of Bitcoin, the world’s first and most popular cryptocurrency. Just like the U.S. dollar divides into cents, Bitcoin divides into Satoshis, but on a much finer scale. One Bitcoin equals 100,000,000 Satoshis (0.00000001 BTC).

This structure ensures that Bitcoin remains usable for everyday financial transactions, even as its market value rises. Whether someone is investing a few dollars or buying a cup of coffee, the Bitcoin network allows precise division and ownership down to a single Satoshi, making the digital currency accessible to everyone.

Why Satoshis Matter

Bitcoin’s price often exceeds tens of thousands of U.S. dollars, creating a psychological barrier for newcomers who assume they must buy an entire coin. Satoshis remove that barrier by enabling fractional ownership.

This level of accessibility supports financial inclusion, allowing individuals from all backgrounds (including those in developing markets) to participate in the cryptocurrency economy.

From micropayments to online services, Satoshis make purchasing small products, tipping creators possible, etc. As adoption grows, the ability to transact in Satoshis could become a standard part of personal finance and global economic development.

How to Convert Satoshis

Because 1 BTC = 100,000,000 SATs, converting between the two is very simple math:

Satoshis = Bitcoin × 100,000,000

Bitcoin = Satoshis ÷ 100,000,000

For instance, if Bitcoin trades at $60,000, then:

- 1 SAT = $0.0006

- 10,000 SATs = $6

- 100,000 SATs = $60

To simplify conversions, users can access Satoshi calculators or adjust display preferences within their cryptocurrency wallet or favorite platform. Many platforms also allow price displays in SATs to improve user experience and accuracy.

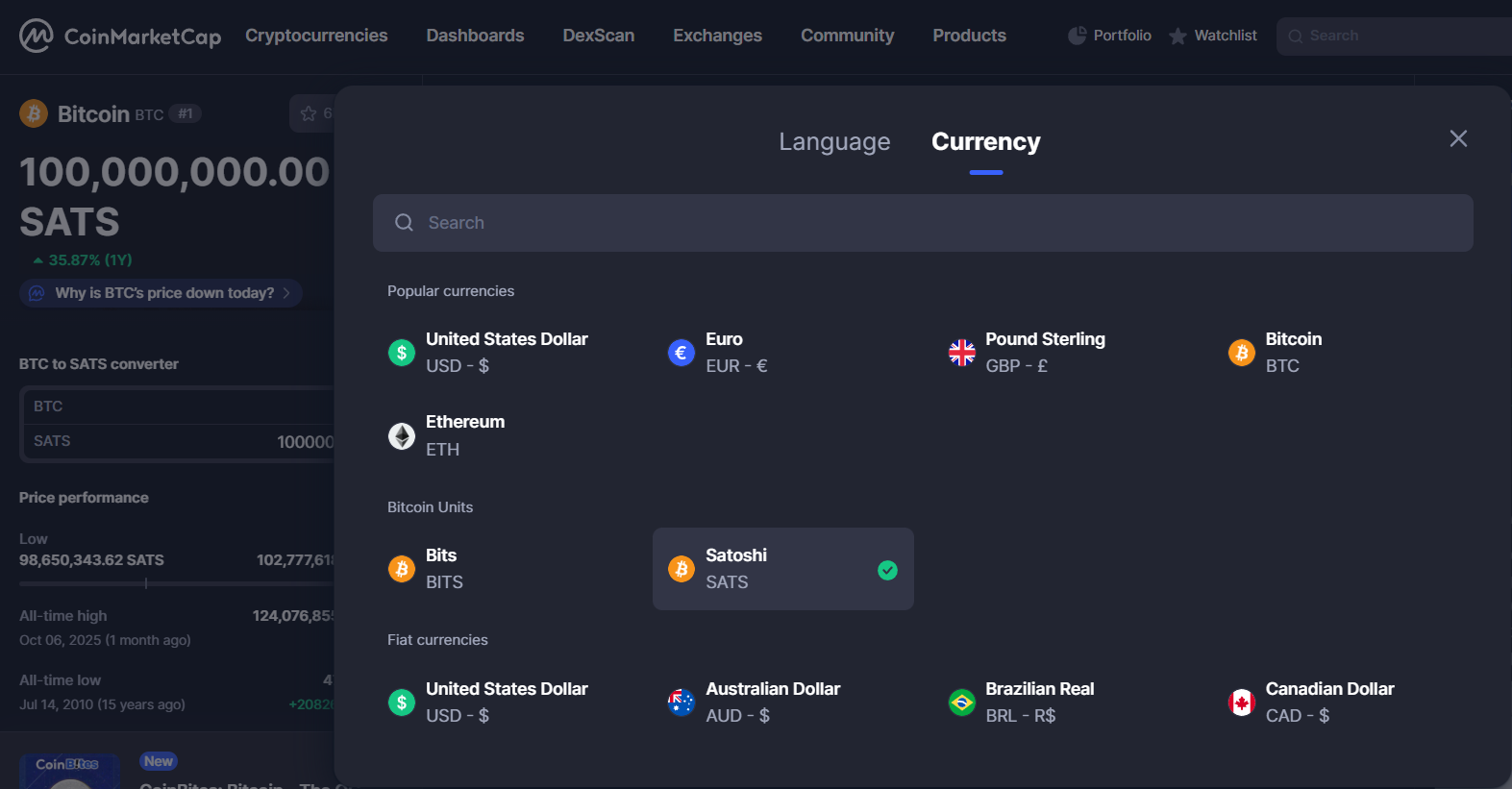

For instance, on CoinMarketCap, you can change the default currency to SATs by selecting the currency drop down option in the top right-hand corner. Select the Satoshi option under Bitcoin units. This will then display all values as Satoshis.

The History Behind the Name

The name “Satoshi” honors Satoshi Nakamoto, the mysterious programmer who invented Bitcoin and published its white paper in 2008.

The term was first proposed in 2010 on the BitcoinTalk forum by a user named Ribuck, who suggested defining a smaller Bitcoin unit for microtransactions. The community endorsed it, and “Satoshi” became the standard reference for Bitcoin’s smallest fraction.

This naming not only pays tribute to Bitcoin’s anonymous creator but also reflects the peer-to-peer and community-driven nature of the blockchain project.

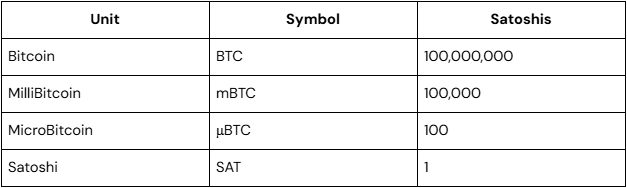

Bitcoin Unit Hierarchy Explained

Bitcoin can be divided into several measurement units, which make it easier to display or calculate different values depending on trade size or market purpose:

Users can choose their preferred unit in most cryptocurrency wallets or mobile apps, which helps reduce confusion when managing balances. This hierarchical structure is part of Bitcoin’s software design, ensuring precision, scalability, and transparency across every financial service or exchange that integrates it.

Real-World Applications of Satoshis

The use of Satoshis extends far beyond calculations. They play a vital role in everyday transactions and digital finance. Examples include:

- Micropayments. Paying for an article, video, or song online using fractions of Bitcoin.

- Remittances. Sending money across borders with minimal fees and no intermediary banks.

- Retail payments. Buying coffee, subscriptions, or services priced in SATs.

- Mining rewards. Bitcoin miners earn Satoshis as rewards for validating blocks on the blockchain.

- Lightning Network transactions. Enables instant, low-cost peer-to-peer payments denominated in milli- or micro-Satoshis.

These use cases show us how cryptocurrency adoption supports faster, cheaper, and more inclusive financial transactions, which helps bridge gaps between traditional fiat money and the digital economy. Satoshis make it easier to represent these small, day-to-day amounts.

Satoshis vs Other Cryptocurrency Units

Other blockchains have their own smallest units. For example, Ethereum uses the Wei, where 1 ETH = 1,000,000,000,000,000,000 Wei (18 decimal places). While Ethereum’s extreme divisibility helps with DeFi and smart contract operations, Bitcoin’s 8-decimal precision balances usability and simplicity. The Satoshi system keeps values easy to calculate, supports market liquidity, and provides enough granularity for future adoption.

This approach makes Bitcoin user-friendly, maintaining accuracy and precision in every financial transaction without overwhelming users with excessive mathematical complexity.

Considerations

Despite its simplicity, using the Satoshi unit can bring some hurdles too:

- Many newcomers are unfamiliar with terms like “Satoshi” or how to interpret BTC in fractional units.

- Since Bitcoin’s price fluctuates, the value of a Satoshi changes constantly, affecting everyday purchasing power.

- Not all wallets and exchanges display Satoshis by default, creating potential confusion for the end user.

- While some companies and fintech platforms already support SAT-based payments, widespread retail exposure is still limited.

Overcoming these hurdles will require better user experience design, educational content, and standardized software development practices across the industry.

The Future of Satoshis

As Bitcoin adoption expands, Satoshis may play an even bigger role in daily finance. With the Lightning Network, users can already transact in milli-satoshis, enabling high-speed, low-cost microtransactions far below one SAT.

In the long term, Bitcoin’s fractional-reserve capabilities and tokenization could make it a backbone for financial services, virtual payments, and cross-border trade. For emerging economies, Satoshis could represent economic empowerment, offering a stable, global currency that anyone around the world can use.

In short, Satoshis are not just a mathematical fraction. They are the mathematical foundation of a global peer-to-peer financial system that continues to evolve.

Key Takeaways

- 1 Satoshi = 0.00000001 Bitcoin

- Enables fractional ownership and global accessibility

- Named after Satoshi Nakamoto, Bitcoin’s anonymous creator

- Used for microtransactions, payments, and mining rewards

- Essential for the future of financial inclusion and digital payments

Getting Started: How to Buy and Use Satoshis

You can acquire the exact amount of Satoshis you're looking for through the Tap app, making it easy to begin your journey into the exciting world of Bitcoin.

Etherscan is a free and widely used blockchain explorer that allows anyone to see any transactions made on the Ethereum platform. Not just transactions, blocks, gas fees, wallet addresses, smart contracts, and other on-chain data can be found on the page. Learn more about what Etherscan is and how it works below.

What is Etherscan?

As mentioned above, Etherscan is an Ethereum-based blockchain explorer. Aside from offering a peek into the advantages of blockchain technologies, Etherscan also provides an insightful look at the status of transactions, gas fees, smart contracts and dapp content. Etherscan is the tool that leverages blockchain's transparent nature.

Acting as a search engine and source of blockchain information, one doesn't need an account to access anything. However, users can create an account in order to access extra functionalities associated with their Ethereum portfolio, such as developer tools, enabling notifications for incoming transactions, and creating data feeds. Whether you're investing in a dapp, monitoring a wallet, or depositing funds to a blockchain-based game, all activity can be tracked through this browser-based service.

Why is Etherscan popular?

Etherscan is the most widely used Ethereum blockchain explorer and is highly regarded in the industry due to its seamless experience. While it won't allow you to store or trade ETH, it offers a reliable look into the functioning of the network, blockchain analytics and all Ethereum and Ethereum-based token activity.

Using Etherscan also provides a better understanding of how the blockchain works, providing insights into its operations and potential ability to spot suspicious blockchain activity (like project leaders selling their tokens, or large whale movements that will affect the token's price).

How to use Etherscan

Whether you're wanting to look up a transaction or verify the validity of a smart contract, you can use Etherscan. Below we will guide you through how to look up a transaction.

How To Find A Transaction On Etherscan

Understanding how to track your transactions can be a powerful tool in the world of cryptocurrency, from seeing how many confirmations it has gone through to the amount of gas fees paid.

Each transaction on the blockchain is given a transaction ID (TXID) or transaction hash which identifies the specific transaction (similar to a person's identity number). It looks something like this:

0x3349ea4144aed83291f87b3904b02f8f1e76c3b5bfed0d95a000fafddaed01bc

In order to get the real-time updates on a transaction, you will need to enter this TXID into the space provided on the Etherscan website.

It will then display all the information pertaining to this transaction, as below:

See our breakdown of the terminology below.

Etherscan terminology

Transaction Hash: the TXID associated with your particular transaction.

Status: status of your transaction (in progress, failed, successful)

Block: the number of the block that your transaction was included in (block confirmations indicate the number of blocks that have followed since then).

Timestamp: the date and time that this transaction was executed.

From: the wallet address that the transaction was sent from

To: the wallet address or smart contract receiving the transaction.

Value: the value of the transaction.

Transaction Fee: the gas fees or transaction fees paid.

Gas Price: the cost per unit of gas at the time of the transaction execution (displayed in Ether and Gwei).

How to Find gas prices on Etherscan

When using the Ethereum network you will be required to pay gas fees in order to conduct any activity. Gas fees are assigned to blocks and fluctuate depending on how busy the network is at the time.

Etherscan provides a Gas Tracker which observes the current gas prices and indicates how busy the network is at the time.

In conclusion

Etherscan is a great tool for anyone using Ethereum or any other cryptocurrencies relating to its ecosystem. From confirming transactions to checking gas prices, this tool provides a great oversight of the network, highlighting the transparent benefits of using digital assets.

Bear markets are riddled with panic selling, the act of exiting the market at a low price based on fear. While FOMO tends to apply more to buying when the markets are on the incline, panic selling is more closely associated with bear markets. The Fear and Greed index differentiates between the two using a scale based on market sentiment, allowing anyone to observe the market sentiment before making a trade.

Panic selling is not exclusive to the crypto markets, in fact, it can be found across stock markets and financial markets too. People have an ingrained characteristic that allows fear to override logic, often resulting in poor choices, particularly in the investment sector.

Fear is often instigated by the news, particularly in the U.S, China and UK, where FUD spreads like wildfire and share prices can drop in an instant. Take Elon Musk's tweets about Bitcoin and Dogecoin and the media hype surrounding this as a prime example.

To avoid this, traders should create an investment plan that they can adhere to and refer back to when emotions get the better of them. To avoid any pain when it comes to investing in crypto, we suggest you pay close attention to the following pointers.

How To Avoid Panic Selling

If you've found yourself tempted to take unprofitable action, consider the following tips on how to avoid panic selling entirely.

Always Come Back To The Basics

When it comes to making any decisions in the crypto trading space, always come back to the primary objective: cryptocurrency's value proposition. While there weren't too many early investors, many since then have entered the market to tap into the incredible gains that crypto has presented over the recent years.

When in doubt, don't get sucked into price activity and instead return to crypto's value proposition. If you've invested in a cryptocurrency with impressive fundamentals that you believe in, there should be nothing to worry about in the long run. Similar to buying a property in a good area of a city, as long as the suburb remains that way your investment is a solid one.

Consider reading a research paper or two on a cryptocurrency to become familiar with its use case, and use case potential, in order to weed out the more risky assets.

Start By Investing Capital That You Don't Need

You've heard the saying "never invest more than you're willing to lose" but consider this: if you invest $100 that you rely on each month if the market dips you'll want to pull the money out as soon as possible to cut your losses as you need that money to survive.

On the other hand, if you invest money that you don't need that month or in the months to follow, small price changes will carry less emotional weight and have more chance of achieving long term benefits.

Focus On Long Term Results

Anyone invested in the crypto market knows that in a matter of ten years the price of Bitcoin went from a couple of cents to $67,000. While these returns are almost unbelievable, bear in mind that they took a decade to achieve.

Although the markets have since fallen, the long term returns are still impressive and certainly worth tapping into. Every savvy investor will always keep their eye on the long term perspective. As adoption increases with countries around the world incorporating Bitcoin into their financial systems (some even allow citizens to pay their tax in crypto), there is plenty more way to go.

There's no denying that we have all become accustomed to instant gratification, but take a look at the following average annual prices of Bitcoin and observe the value in focussing on the long term:

2015: $500

2016: $900

2017: $15,000

2018: $8,000

2019: $10,000

2020: $9,000

2021: $40,000

Prepare For Pullbacks And Accept The Risks

The crypto market is notorious for being volatile, the best way to tackle this is to accept it. The markets have been known to lose thousands of dollars in a couple of hours. If you want to invest in the best performing asset in history, you need to be prepared for that.

While the Bitcoin price has lost over 85% of its value several times in its existence, it has reclaimed that value every single time. Even the individuals that bought BTC at $20,000 in 2017 regained their value and then some in the bull run of December 2020.

Be prepared to sit through some market dips, but know that it will recover. If you're focused on the long term perspective and have used capital that you don't rely on, pullbacks and market dips should not be damaging factors.

Use A Dollar Cost Averaging Strategy

The DCA strategy involves buying Bitcoin at a certain time of the month as opposed to based on market activity. Buying Bitcoin, or any other cryptocurrency, on certain days of the month will mean that you pay varied prices for the coin.

Say you decide to invest $100 a month in BTC. One month you might get 0.002 BTC while the next month you get 0.003 BTC. Dollar cost averaging levels out the entry price when accumulating the coin and allows you to become less emotionally attached to the market's movements and therefore less likely to panic sell.

In Conclusion

The best crypto investors are able to commit to some degree of emotional detachment, have a strong investment strategy focused on long term gains, and only invest in highly vetted, functional coins. Building a portfolio of coins from strong projects will help to alleviate any market-related uncertainty and allow you to ride out the dips more confidently. If ever you feel tempted to panic sell, revisit this list of factors and resist the urge!

You can also read our article on Emotion Management In Trading for extra insight on how to keep your emotions under control while trading.

So you decided to go deeper into the fundamentals of investing and learn what an APY is. You've come to the right place, let's get you started with this perplexing "APY" term.

What Is APY?

In conventional finance, a savings account frequently offers both a low-interest rate and an annual percentage yield (APY). Let's look at what they are and what they mean.

- The Annual Percentage Yield (APY) is the annual return from the principal and accumulated interest on investments or savings, expressed as a percentage.

- The simple interest rate is the amount earned on the original deposit.

Assume an account at a bank offers a yearly interest rate of 5%. If someone deposits €2,000 into the account, it will be worth €2,100 after a year with the 5% yearly interest rate.

The Difference Between Interest Rate, APY and APR

The APY takes into account the impact of compounding, whereas the interest rate does not. The APY is the projected rate of return earned annually on a deposit after taking compound interest into account.

Compounding interest is the interest that a person accrues from their initial deposit, as well as the interest they earn from their original investment (or in other words, the initial deposit amount plus the interest generated).

The terms APY and APR are frequently used interchangeably, although they represent two different things. These words are sometimes confused due to their close resemblance. However, APY and APR aren't the same things.

The APR (annual percentage rate) is a formula that determines how much interest you'll pay when borrowing money and is the rate of return earned if your funds are invested in an interest-bearing account.

When a person takes out a loan, their lender sets an APR that varies based on the loan. APRs are either fixed or fluctuating depending on the type of loan the user requires. However, the APR is a rather basic interest rate and does not take compounding into account, unlike APY.

How Is APY Calculated?

APY represents your rate of return, also known as the amount of earnings or profit you can make. Of course, your ultimate earnings will vary depending on how long you keep your assets invested while the holding period will influence how much you will earn.

APY measures the rate of the annual return earned on any amount of money or investment after taking into account compounding interest.

The following is the formula for calculating APY:

APY = (1 + p/n)ⁿ − 1

Where:

p = periodic rate of return (or annual APR)

n = number of compounding periods each year

Bear in mind that an APY can be calculated in a variety of ways depending on the provider.

Interest is a fundamental concept in the world of finance and economics. At its simplest, interest can be understood as the fee charged for borrowing money, or the amount earned on invested money. Understanding interest is essential for anyone seeking to manage their finances effectively, whether they are borrowing money, investing their savings, or simply trying to make informed decisions about their financial future.

In this article, we will explore the basics of interest, including how it is calculated, the different types of interest, and how to navigate interest in various financial situations. We will also provide real-life examples and valuable tips to help you make informed decisions about your money.

Types of Interest

There are two primary types of interest: landed money interest and earned interest. Landed money interest refers to the interest paid on borrowed money, while earned interest refers to the interest earned on invested money.

Landed Money Interest

Landed money interest, also known as borrowing interest, is the interest paid by a borrower to a lender in exchange for the use of money. This type of interest is charged on a wide range of financial products, including mortgages, car loans, personal loans, and credit cards.

The interest rate on a loan is typically expressed as a percentage of the amount borrowed, and is determined by a variety of factors, including the borrower's credit score, the term of the loan, and the lender's own risk assessment. The interest rate on a loan can have a significant impact on the overall cost of borrowing, with higher interest rates resulting in higher monthly payments and a greater total cost over the life of the loan.

For example, let's say you take out a $10,000 car loan with an interest rate of 5% per year, to be repaid over a five-year term. Over the course of the loan, you will pay a total of $1,322.74 in interest, in addition to the $10,000 principal amount. If the interest rate were increased to 8%, the total cost of the loan would rise to $1,845.87, a difference of over $500.

Earned Interest

Earned interest, also known as investment interest, is the interest earned on invested money. This type of interest is paid to investors by banks, governments, and other financial institutions in exchange for the use of their money.

The interest rate on investments can vary widely depending on the type of investment, the term of the investment, and the risk associated with the investment. For example, savings accounts and certificates of deposit (CDs) typically offer lower interest rates but are considered low-risk investments, while stocks and other securities can offer higher potential returns but are also considered higher risk.

For example, let's say you invest $10,000 in a CD with an interest rate of 2% per year for a five-year term. At the end of the term, you will have earned a total of $1,047.13 in interest, in addition to the $10,000 principal amount. If you had instead invested the same $10,000 in the stock market and earned an average annual return of 8%, your investment would have grown to $14,693.28 over the same five-year period.

Calculating Interest

The calculation of interest depends on a variety of factors, including the amount of the loan or investment, the interest rate, and the length of the loan or investment term. In general, the formula for calculating interest is as follows:

Interest = Principal x Rate x Time

Where:

- Principal is the amount borrowed or invested

- Rate is the interest rate expressed as a decimal

- Time is the length of the loan or investment term, expressed in years

For example, let's say you invest $5,000 in a savings account with an interest rate of 2% per year, to be held for three years. Using the formula above, we can calculate the interest earned as follows:

Interest = $5,000 x 0.02 x 3Interest = $300

In this case, you would earn $300 in interest over the three-year term, in addition to the $5,000 principal amount.

Tips for Navigating Interest

Navigating interest can be challenging, particularly for those new to the world of finance. Here are some valuable tips to help you make informed decisions about interest in various financial situations:

- Understand the terms of your loan or investment: Before taking out a loan or investing your money, make sure you understand the terms of the agreement, including the interest rate, term length, and any associated fees or penalties.

- Shop around for the best interest rates: When taking out a loan or investing your money, be sure to shop around for the best interest rates. Compare offers from multiple lenders or financial institutions to ensure you are getting the best deal.

- Consider the impact of compounding interest: When investing your money, consider the impact of compounding interest. Compounding interest is interest that is earned on both the principal amount and any accumulated interest, resulting in exponential growth over time.

- Avoid overexposure: Be careful not to overexpose yourself to any one type of investment or loan. Diversify your portfolio and consider spreading your investments across a range of asset classes to minimize risk.

- Take advantage of tax benefits: Some types of interest, such as mortgage interest and student loan interest, may be tax-deductible. Be sure to take advantage of any available tax benefits when borrowing or investing.

Real-Life Examples

Let's look at some real-life examples of interest in action:

- Car loan: You take out a $20,000 car loan with an interest rate of 4% per year, to be repaid over a five-year term. Over the course of the loan, you will pay a total of $2,164.17 in interest, in addition to the $20,000 principal amount.

- Savings account: You deposit $10,000 in a savings account with an interest rate of 1% per year, to be held for three years. Over the three-year term, you will earn a total of $308.18 in interest, in addition to the $10,000 principal amount.

- Mortgage: You take out a $300,000 mortgage with an interest rate of 3.5% per year, to be repaid over a 30-year term. Over the course of the mortgage, you will pay a total of $184,968.79 in interest, in addition to the $300,000 principal amount.

In Conclusion:

Interest is a fundamental concept in the world of finance and economics, and understanding how it works is essential for anyone seeking to manage their finances effectively.

Whether you are borrowing money, investing your savings, or simply trying to make informed decisions about your financial future, understanding interest can help you make better decisions and maximize your potential returns. By considering the tips and real-life examples presented in this article, you can navigate interest with confidence and make informed decisions about your money.

A common misconception for people outside of the crypto community is that cryptocurrencies are used for illicit and fraudulent activities. While a decade ago, cryptocurrencies were largely associated with the dark web and drug trafficking, these days the modern crypto landscape is much more regulated.

In fact, most countries these days have integrated rules and regulations pertaining to the use of cryptocurrencies, from conducting business with crypto to outlining the tax requirements.

The industry is also required to complete stringent KYC (Know Your Customer), AML (anti-money laundering), and anti-fraud procedures when working with crypto, leaving little to no room for criminal activity or criminal networks involved.

Understanding the intricate world of crypto compliance: avoiding serious and organized crime

Staying compliant with cryptocurrency regulations is vital for all companies in the industry, as failure to do so can result in hefty fines and loss of business. Established businesses take KYC/KYB/AML processes very seriously in order to protect their reputation and minimize risk.

Leading market players are not the only ones that must adhere to these tight regulations. Every platform that enables crypto transactions in most crypto-friendly nations is required to follow such protocols. These entail thorough KYC/AML procedures and establishing the identity of its clients.

The company is required to comply with local requirements if it wants to operate legally. Another reason why using a regulated platform to manage your cryptocurrency is always the best option.

At the same time, B2B clients have entirely different expectations. KYB serves to evaluate every potential partner thoroughly, working out many details and investigating the company's directors.

A few compliance tips for businesses:

- Ensure your staff and partners have a basic understanding of crypto security measures.

- Make sure your policies are always up to date and submitted on time.

- Ensure monitoring procedures are up to date and operating optimally.

- Review your past progress and adapt your plans as needed.

Crypto vs fiat currency: law enforcement investigations

According to a study, less than 1% of illicit funds used in financial crimes in 2019 were carried out using digital assets (even less in 2020). Considering how cryptocurrency operates, this number may surprise you. What's more surprising is that most of these crimes were related to scams; less than money laundering, drug trafficking, terrorist financing, and any other major major criminal use of cryptocurrency.

Money laundering statistics currently attribute $1.6 billion worth of cryptocurrencies being involved in financial crimes, compared to the estimated $1.6 trillion laundered through cash annually.

Responsible crypto enterprises and crypto financial institutions are frequently eager to cooperate with authorities and aid in the fight against financial crimes and criminal activity. Tether's chief technological officer was quick to respond when a token swap platform was hacked, immediately taking action on a $33 million USDT transaction related to the incident. A few weeks later, the assets' owners were reimbursed.

Blockchain surveillance firms, such as Chainalysis and Elliptic, employ specialized software for the following purposes. They collaborate with it to gather blockchain data and examine it for possible illegal behavior. This plays a vital role in helping law enforcement trace digital currency transactions related to the Dark Web and stop illicit funds flowing straight into the wrong hands.

Does crypto hinder law enforcement investigations?

Contrary to popular belief, cryptocurrency transactions are not anonymous. In fact, many cybercriminals have been caught because their identities were eventually traced. For example, the Justice Department was able to track down 63.7 BTC paid by Colonial Pipeline Company to hackers after its computer systems were disabled and caused fuel shortages and a gas price surge across the East Coast. This criminal use of cryptocurrency was quickly investigated and prosecuted.

As blockchain technology uses cryptography to secure its transactions, there is another misconception, and that is that crypto transactions are anonymous, when in reality they are pseudonymous. This means that all transactions on the blockchain are visible, however, they are not tied to identities. So, should you know someone's wallet address you can see their transaction history. This provides law enforcement access to transaction history and the chance to conduct on-chain forensics.

The good news is that law enforcement is getting better at tracking down illicit funds each year. And the cryptocurrency sector is only eager to assist.

Final Thoughts

The recent rapid growth of global regulations has helped foster the growth of the cryptocurrency industry. Digital currencies are actually traceable and don't account for a large majority of financial crimes, despite what many people believe.

Responsible crypto platforms take measures to prevent illegal activities, protect users from fraud and other risks, and encourage them to stay financially responsible. This includes cooperating with law enforcement, as well as offering training and rewards to users.

While cryptocurrencies have played a small role in being used to fund illicit activities, it pales in comparison to the large number of fiat currencies used annually in fraudulent and illegal activities. That's not to say you should stop using fiat currencies, and the same applies for crypto.