After a volatile October, crypto faces a defining moment. Discover what's fueling both the bullish and bearish cases right now.

Keep reading

After a volatile October that saw one of the sharpest two-day liquidations of the year, the crypto market is trying to regain its footing, but conviction remains divided. Bitcoin has stabilized near key support levels, while altcoins fight against selling pressure. With macro, policy, and on-chain factors all in play, the debate between the bull and bear camps is as alive as ever. Let’s unpack the forces shaping both sides of the ledger.

The Bear Case

When Good News Don’t Move Prices

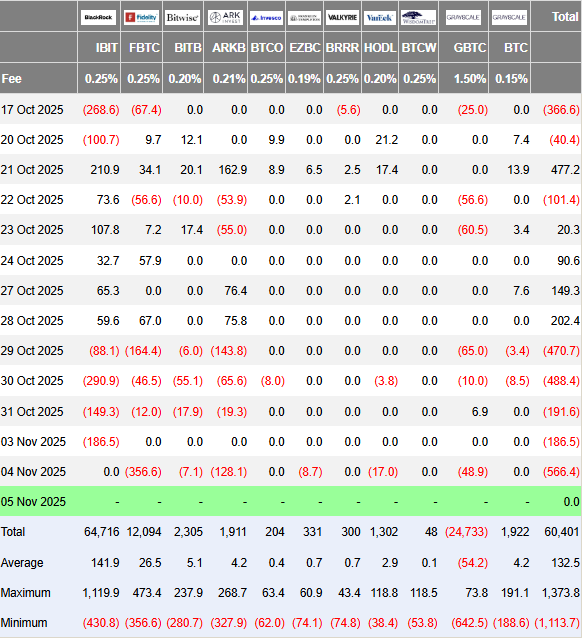

Despite encouraging ETF data and easing rate expectations, crypto failed to rally in late October, a classic warning sign of risk fatigue. According to Farside Investors, U.S. spot Bitcoin ETFs saw outflows of $470 million, $488 million, and $191 million between October 29 and 31, signaling that short-term traders were taking profits or stepping aside after “Uptober” fizzled out.

The AI Narrative

Macro sentiment still casts a long shadow. The tech-heavy equity rally, driven by AI infrastructure and chip stocks, has stirred debate about overvaluation. Nvidia’s brief breach of a $5 trillion valuation in late October triggered flashbacks of the dot-com era. If AI equities begin to deflate, crypto could feel the wealth effect unwind, as liquidity shifts from speculative assets to safer havens.

The 10/10 Crash Aftershock

The October 10 downturn marked one of the largest single-day liquidations in recent memory. Analysts note that this event left traders hunting for “dead entities” and potential hidden losses, injecting caution across the market. Even with recovery underway, scars from that drop remain fresh.

Post-Halving Cycle Timing

Bitcoin’s halving on April 20, 2024 (block 840,000) reset expectations, but it also reignited the age-old question: where are we in the cycle? Historically, the strongest rallies have occurred before or shortly after the halving, not a full year later. Some analysts now argue that the current consolidation could represent a late-cycle phase rather than the start of a new one.

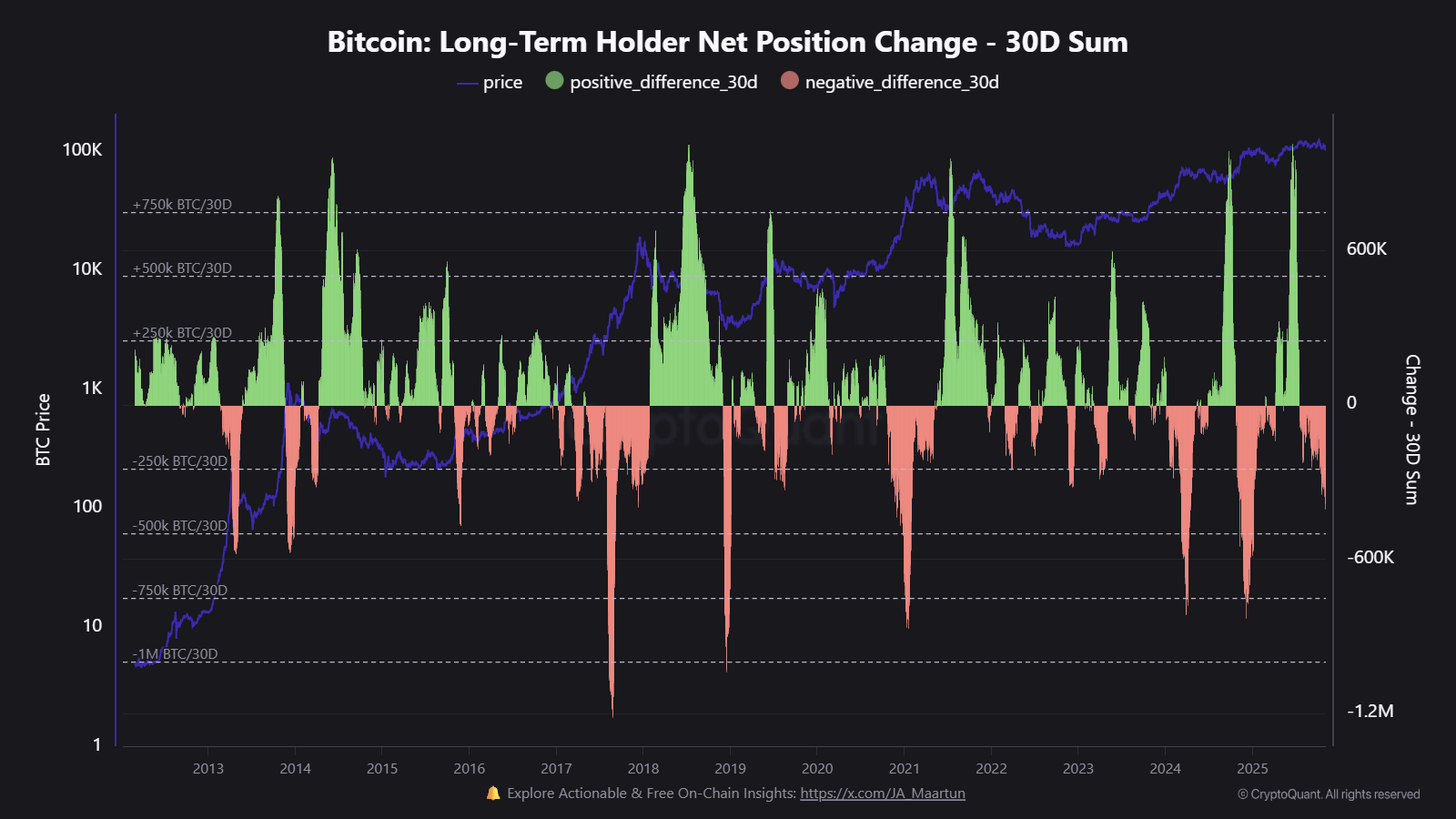

Dormant Wallets Awakening

On-chain data from CryptoQuant shows that long-term holders have increased net distribution since mid-October, with tens of thousands of BTC re-entering circulation. Several Satoshi-era wallets have also moved funds, not necessarily bearish in isolation, but enough to add pressure and short-term supply.

The Bull Case

No Signs of Euphoria

Market positioning remains far from overheated. The Crypto Fear & Greed Index currently sits in the 20s, and has been recently hovering between “Fear” and “Neutral.” That’s a far cry from the exuberant 80s to 90s readings that often precede blow-off tops. In practical terms, this suggests there’s still room for sentiment to improve before the market becomes dangerously crowded.

Liquidity Is Turning

Central banks are easing. The European Central Bank has already paused, the Bank of England has begun cutting, and the U.S. Federal Reserve is expected to follow suit with at least one more rate cut by year-end. According to the CME FedWatch Tool, the odds of a 0.25% cut currently stand above 70%. Historically, easing cycles have correlated strongly with renewed crypto uptrends, as lower yields push investors back into risk assets.

Institutional Adoption Keeps Compounding

Spot ETFs remain the biggest driver of credibility and inflows this year. Despite short-term outflows, global crypto investment products reached $921 million as recently as last week. That steady institutional presence gives crypto markets deeper liquidity and a stronger foundation than in previous cycles, where retail speculation dominated.

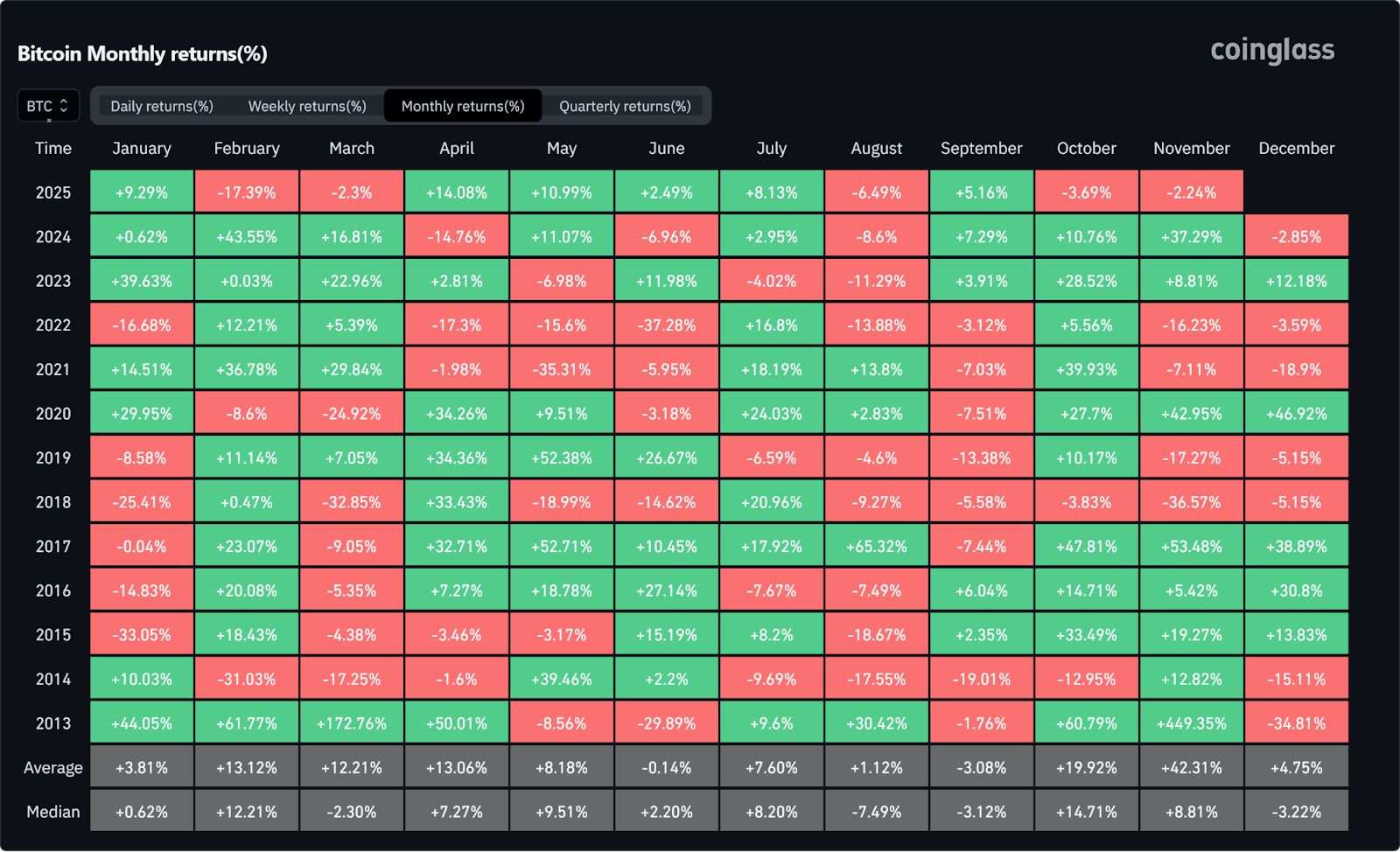

The Seasonal Edge

Seasonality adds another bullish data point. Since 2013, Q4 has consistently been Bitcoin’s strongest quarter on average. With November historically delivering above-average performance, many traders see the current consolidation not as a ceiling, but as a potential setup, particularly if macro data softens and ETF inflows resume.

Improving Global Sentiment

Finally, the U.S.–China trade thaw is a quiet but important catalyst. China has agreed to pause 24% tariffs on U.S. goods, marking the most significant de-escalation yet. For global risk assets, that’s a relief valve, potentially restoring confidence in emerging markets and crypto alike.

Final Verdict

Crypto’s tug-of-war between optimism and caution is far from over. The bull camp points to liquidity, policy progress, and institutional growth as evidence of a maturing ecosystem. The bears, on the other hand, warn that cycle timing, macro fragility, and old-wallet selling could cap any short-term rally.

Currently, the most realistic view lies somewhere in between these two extremes. After October's flash crash sent shockwaves through the market, a period of recalibration has taken hold. Whenever the next significant high arrives, the current environment may be best described not as peak fear or euphoria, but as consolidation.

NEWS AND UPDATES

LATEST ARTICLE

The global financial crash in 2007 was the catalyst for the creation of Bitcoin. Designed to provide a decentralized way in which people can manage their own money, digital currencies slowly infiltrated the greater financial markets.

Almost a decade later, crypto adoption is at its highest and for the first time challenging traditional financial institutions and their product range. So, which is better? Let's explore the pros and cons of each category.

Blockchain technology has seen an incredible increase in interest in the last few years. While it provides a universal backbone relevant to almost any industry, it has also brought the world cryptocurrencies, NFTs, decentralized finance (DeFi) and other digital assets.

Tackling existing centralized monetary challenges, blockchain technology and digital currencies are two of the greatest inventions of the 21st century.

Digital currency versus banking

Cryptocurrencies are decentralized digital currencies that can be used to exchange goods and services as well as a store of value. They're typically acquired through crypto exchanges and kept in secure crypto wallets. These virtual currencies are autonomous, operate in a secure manner with little human interaction, and are increasingly considered the future of finance.

The predominant financial systems in the world are currently banks. They provide financial services to those that meet their requirements, including loans, savings, and other financial services.

However, unlike cryptocurrencies, they have several problems core to them being centralized and susceptible to biases. They're also slower than cryptos, and some of them charge exorbitant interest rates on loans as well as routine purchases.

The pros and cons of the Banking system vs digital currencies

There has been little development in the banking sector in the last several decades, so while the products are useful there has been very little innovation in the space. Below we outline the current challenges that the traditional systems face when compared to the advantages of a digital currency.

Financial Inclusivity

Banks are notorious for requiring lengthy paperwork and in-depth background checks. They are also known to provide different products and limits to different groups of people, including payment durations, soft loans, limits, etc.

When creating the digital currency Bitcoin, Satoshi Nakamoto wanted to counteract this financial inclusivity pertaining to fiat currencies and the greater financial system and instead provide a financial product available to all. Cryptocurrencies, therefore, do not require any paperwork or identification to operate or open a digital wallet.

While buying digital assets on an exchange will require personal information, they do not require any background checks or credit scores. Unlike in the traditional financial system, engaging in crypto markets is also not exclusive to location, allowing anyone from any corner of the globe to immediately access the digital payment systems.

Accessibility

Banking institutions operate within certain hours and are closed on weekends, meaning that transactions can sometimes take days to clear. They will also typically require an in-person authentication for very large transactions, and affect the remittance markets in the global financial system.

Cryptocurrencies on the other hand operate 24/7 (even on public holidays) as they are maintained by members all around the world. Cryptocurrencies provide zero downtime with unlimited amounts and do not require third-party authentication before making transactions. One digital currency can send value to the other side of the world in minutes, requiring no in-person authentication.

Security

The banking industry, particularly online systems, are susceptible to being hacked, alongside fraudulent activities and money embezzlement. While this is not always the direct fault of the central bank or financial institutions, it has become a common problem as ill actors have learned how to navigate the security systems and trick the owners of these accounts.

Through the use of blockchain technology, transactions cannot be intercepted or reversed, and are handled in a peer-to-peer nature ensuring that they do not go through a third party for authentication and require minimal human interference.

Fees and Transaction Times

During transaction periods, banks often add on extra costs and taxes. When sending and receiving money, banks frequently charge very high transaction fees and taxes, especially when conducting international remittances. These transactions also take a long time to clear due to their sluggish procedures, especially for large amounts of cash.

Cryptocurrencies provide an excellent solution to the remittance markets as they provide fast and cheap transactions. Blockchain technology ensures that they clear in several minutes (depending on the cryptocurrency and the network’s congestion at the time) and that they are sent directly to the recipient’s wallet (as opposed to waiting for the receiving bank to clear the transaction).

Diversification

Traditional banking services generally lack significant diversification options due to their competitive pricing structures. However, cryptocurrencies enable users to engage with multiple products simultaneously, which can provide opportunities for leveraging various networks and creating portfolios with reduced risk concentration.

Smart Contracts

Another advantage that blockchain currently holds over traditional banking systems is the use of smart contracts. Smart contracts are digital agreements that automatically execute once predetermined criteria have been met. Leveraging smart contracts in the financial services industry offers a seamless and entirely decentralized approach to modern banking.

Which is Better: The central bank or digital assets?

Comparing central banks and digital assets reveals intriguing aspects of both systems. Banking systems have become an integral part of modern society, underpinning economies and facilitating everyday financial transactions. They offer stability, regulatory frameworks, and familiarity to the masses.

On the other hand, cryptocurrencies introduce a realm of innovation. Their decentralized nature challenges traditional financial paradigms, enabling secure and direct peer-to-peer transactions. Additionally, cryptocurrencies empower novel applications such as smart contracts, decentralized finance (DeFi), and tokenization of assets.

Selecting one over the other isn't straightforward due to their contrasting strengths. Central banks provide stability and a well-established foundation, while digital assets spark possibilities for disruption and financial inclusivity.

Presently, these financial systems coexist synergistically. The banking system maintains its role as a bedrock for economic operations, while digital assets complement by offering alternative avenues for value exchange and financial exploration. As both systems continue to evolve, it's likely that their interaction will shape the financial landscape in intricate and unexpected ways.

Why not use both? Tap offers the perfect solution to merging the best of both worlds through an innovative alt-banking mobile app. Through the app, users can load both fiat and cryptocurrencies into their unique, secure digital wallets and use both interchangeably to pay bills, send money to friends, and even earn interest. Get the best of both worlds by enjoying the benefits of both the traditional banking systems and cryptocurrencies.

Why not harness the strengths of both paradigms? Embracing this dual approach, Tap presents a groundbreaking solution that seamlessly blends the attributes of both money accounts and digital assets within an innovative mobile application. Tap empowers users to effortlessly load fiat currencies alongside cryptocurrencies into their individualized, secure digital wallets.

This fusion enables users to fluidly alternate between these assets for various purposes, such as settling bills, conducting peer-to-peer transactions, and even capitalizing on interest-earning opportunities. By embracing this convergence, you can truly enjoy the advantages offered by both traditional finance and the dynamic potential of cryptocurrencies.

When referring to the yield on an investment, this indicates the earnings generated over a certain period of time. It is generally presented in percentage form and includes the interest or dividends relevant to the initial investment.

While returns are calculated using the difference in value at two specific points in time, the yield will calculate the total (net) value earned over a period of time. This provides an invaluable tool in helping you understand the potential value of an investment.

Basic yield is calculated as the net realised return divided by the initial investment amount. For example, if an investor bought $100 worth of Bitcoin which grew to $2,000 in the next year, then the formula would look like this:

$1,900 / $100 = 19

-> which translates to 1900%.

There are several different formulas based on the type of yield you wish to calculate. These include:

- Yield on Stocks

- Yield on Bonds

- Yield to Maturity

- Yield to Worst

- Yield to Call

A high yield isn’t necessarily a good thing. Should the market’s decline or the company pays out high dividends the yield will still reflect as high. Always do your own research when considering an investment, or trust a financial advisor.

You might have come across the term p.a. in traditional investment cycles, but how does it relate to crypto? In this article, we’re breaking down what p.a. means, how to get in on it and how it relates to the crypto industry.

What does P.A. mean?

P.a. is an investment term that stands for per annum. This refers to the interest an investor can gain over a year's period and provides insight into the yields that the investment will generate. This is calculated on a simple basis and not compound.

You might see digital wallet platforms offering reward rates of 8% p.a. Or 14% p.a., this tells the potential investor that the platform will provide 8% of the initial investment, over a 12 month period.

PA can also stand for price action, a popular term used on crypto Twitter. In this piece we're focusing on the annual interest rates version.

How can users make money with crypto assets?

There are several ways in with industry participants can earn cryptocurrency. Below we outline the most widely used, and safest options. Be sure to check each option with the relevant blockchain network as these will differ from network to network.

Crypto Mining

Crypto mining can be a lucrative means of generating a passive income, however, the costs might run high depending on where you live and what cryptocurrency you are mining. Each network has its own way of minting new coins, which require different hardware and electricity means.

Bitcoin, for instance, is a Proof of Work network that requires miners to use large amounts of energy as they race to finish a complex cryptographic puzzle. The first to complete this is rewarded with mining the next block and receiving the associated payoffs.

Bitcoin requires a large amount of electricity, not practical in areas with high electricity costs, and either a graphics processing unit (GPU) or an application-specific integrated circuit (ASIC), which can also be costly.

If you wish to get involved with mining cryptocrrencies be sure to do adequate research on what will be required and what income this could generate before investing any money.

Crypto Staking

Crypto staking is an alternative minting solution for Proof of Stake networks, such as Cardano and soon-to-be Ethereum. Crypto staking requires users putting their funds in a smart contract usually for a predetermined lock up period to confirm transactions on the network. This will typically require a minimum amount, so as to ensure that individuals hold a “stake” in the network and will act on good intentions.

When crypto traders stake the minimum balance, a node will deposit these funds into a staking pool on the network, similar to a deposit. The bigger the stake, the higher the chances of that user, now referred to as a node, being chosen to verify transactions. When the node is chosen to confirm transactions, they will create a new block and receive a reward for adding it to the blockchain.

Reward rates are specific to each blockchain network so be sure to check the details relevant to platform on which you wish to stake. As a security mechanism, the staked coin in the network is typically taken away if the node acts with ill intent.

Passive Income

There are a number of crypto initiatives that allow users to earn passive income through their crypto assets. These work in a similar way to holding funds in a wallet, however, these wallets will likely be on a cryptocurrency exchange or DeFi wallet and the user will typically not be able to access the funds for a certain period of time.

Over the duration the user will earn interest as stipulated in the initial agreement. Note that p.a. Values are subject to change with market fluctuations, rising when prices rise and falling when an asset’s price takes a dip. This typically works in the same way as a savings account.

Its worth noting that the onus lies on the traders to pay taxes on any income generated. It is important to check the crypto specific tax laws in your region.

Disclaimer: This article is intended for communication purposes only, you should not consider any such information, opinions, or other material as financial advice.

There are plenty of reports of investors making huge gains in the crypto market over the years, however, there are plenty more ones on people who have lost money. While investing is designed to increase your personal wealth, many investors are often intimidated by the digital currency market due to its volatility and age. In this piece, we're going to run you through the various ways of making money from cryptocurrencies without making a single trade.

After the economies around the world were deeply affected by the Covid-19 pandemic, now is as good a time as any to regain control over your funds and use passive income opportunities as a tool to do so. Tap into the innovation available in the crypto space to pay off your mortgage, bond or leverage your pension and forget about fluctuating market prices.

Passive income 101

The least risky way in which to build your personal wealth is through passive income. Passive income involves generating money from investments that don't require any intervention. This includes activities such as earning dividends from stocks, automated sales through a business, monthly or annual rental from properties, etc.

Another avenue of passive income is earning interest on money in the bank. In this case, the bank will pay you a predetermined percentage of the funds stored in that account. Thankfully, the crypto space has caught up and currently has a number of programs that are offering crypto holders the same benefits, albeit with far greater interest rates. While the regulation surrounding these programs is still being structured, many reliable and trustworthy platforms are offering programs worth taking advantage of.

How to earn passive income with crypto

Below we explore several smart ways in which you can earn a passive income with crypto, all designed to grow your capital. These options are outside of the decentralized finance (DeFi) space so as to avoid any potential problems or scams, rather stick to reliable platforms and networks as outlined below.

Staking

As the crypto space has evolved, many platforms have shifted from the original Proof of Work consensus mechanism to a Proof of Stake one. PoW involves miners competing to solve a complex cryptographic puzzle in order to validate transactions on the network and earn the block reward.

PoS models are less energy-intensive and instead require validators on the network to stake a certain amount of the native cryptocurrency in order to validate the transactions and earn the reward. Anyone can get involved thanks to the likes of PoS platforms like Cardano, Polkadot, and Ethereum 2.0.

Stakers can delegate crypto to a validator and earn a portion of the payouts when the validator completes the process. Requiring very little technical knowledge and minimal capital (each platform is different), staking provides an easy opportunity for a cryptocurrency holder to earn passive income.

Stakes can also opt to be a validator, which requires a considerable amount of effort and technical information. With two options available when it comes to staking, one can either opt to be a validator or delegate coins to a validator. The former will require more capital and attention but yield higher returns, while the latter provides lower returns but ensures that the validators do all the work.

Mining

On the other side of the coin, there is mining. Mining is native to PoW networks and involves confirming transactions for a reward. Networks vary in terms of what computer resources one might need, although cheap electricity is essential as these machines typically require large amounts of power.

The world of mining has progressed in leaps and bounds since the early days of using CPUs to mine Bitcoin. Should one want to explore this path, we advise you do extensive research on the cost implications beforehand.

Lending

A method favoured by long term investors looking to earn interest on their already accumulated crypto assets, lending involves borrowing the funds to a platform in return for interest. These funds are typically locked away for a certain period of time in exchange for interest payments later on.

Peer-to-peer (P2P) lending platforms usually have a fixed or variable interest rate and will handle the logistics of the borrower and lender. These types of services are often found on platforms that offer margin trading.

Make money without engaging in any trades, with no betting on the outcome of the market. Passive income from cryptocurrencies can be done simply by storing your already accumulated digital currencies in an income-generating account. Experiences on various platforms will vary, however, in most cases the customer will deposit their funds into a specific account and earn interest in the same currency. Check the platform's publication for guidance if you need any assistance.

There's a time-old debate over whether hodling or trading leads to better profits when it comes to buying into the cryptocurrency market. While both are great options, in the article below we look at the pros and cons of each option and weigh them up.

What is trading?

Trading refers to the buying and selling of financial instruments, assets, or commodities in financial markets with the aim of making a profit. Trading requires continuous monitoring of the charts and frequent study, whether in the crypto or stock market. Crypto trading involves buying and selling crypto at various intervals, whether minutes, hours, days, weeks, months, and years. Despite the greater risks involved, the potential for big percentage returns attracts individuals to trading.

If you want to trade crypto assets, it's essential to have a basic knowledge of the industry and how events in the news may influence Bitcoin's price. Remember to set stop losses and take profits so that you can protect your trade.

The pros of trading

- Potentially sizable profits

Crypto is known to be a volatile market and it's not uncommon to see price movements of 30% or above when crypto trading. With some strong analytical skills, one can observe, analyze and trade these waves and yield sizable profits.

- You're in control

Some people make a living trading part-time or full-time, particularly day trading. Day trading is where you enter and exit positions typically within a 24-hour period. Either way, you are in control of your own hours and workload, allowing you to take a break after you've met or exceeded your daily or weekly earnings targets.

The cons of trading

- Need to know trading fundamentals and technical analysis

Before you begin trading, you need to learn how to do fundamental and technical analysis of charts. This process requires dedicated effort and time investment.

- Need to be able to manage emotions

The prices of cryptocurrencies can change rapidly, making this a more risky proposition than long-term holding. You must be prepared to sell a losing cryptocurrency when it's plunging or decide to hodl for it to recover. Anything might happen in this fast-paced market, so you must make wise decisions without getting emotional.

What is hodling?

The term first came about in 2013 from a misspelled work in a BitcoinTalk Forum. The inebriated trader made the now infamous typo, and the word stuck. Almost a decade later, the term "hodl" remains a permanent fixture in the crypto ecosystem. Some have since branded it as "Hold On for Dear Life".

The term refers to holding a particular cryptocurrency for long periods of time, ignoring market volatility and knuckling through a bear market. As a passive strategy designed for long-term time frames, hodling requires a trader to simply buy a cryptocurrency and hold it in a secure place for months or even years until it reaches your price target.

You can buy Bitcoin or your favorite cryptocurrency at regular intervals if you're planning to HODL. This term is associated with buying a small amount of Bitcoins weekly or monthly. For example, let's say you have $1,000 to buy over time.

In this case, you might purchase $30 in Bitcoin each week or $50 worth every month. By staggering your buys like this rather than putting it all at once, you minimize the likelihood of price fluctuations having as much impact on the price per coin. This strategy prefers to buy Bitcoin over trade Bitcoin.

The upside to hodling

- Minimal effort

Hodling requires initial research into the cryptocurrency you wish to buy in (very important ans crucial to do your own research). From there establish your budget and strategy.

- Minimal stress

The crypto market is known for its significant swings in value. Thankfully with hodling there is no need to time the market for entry and exit positions or watch the chart all of the time.

- Minimal trading fees

Save money on trading fees by conducting on a few transactions, versus the many you will need to do when day trading. Some countries won't even charge tax on your crypto gains after a certain period of time (but be sure to check this in your area).

The downside of hodling

- Need patience

As hodling is a long-term strategy approach it requires patience and mental endurance. If you decide to use the Hodling strategy you'll need to manage emotions during tough market fluctuations and might need to wait years before being able to cash in on any ROI (return on investment).

- Funds are locked in

Because this is a long-term strategy, your funds would be inaccessible for an extended period of time. This might result in foregone opportunities to invest elsewhere in the crypto space or any other market.

However, this can be avoided by leaving your funds in a crypto interest account. Tap provides users access to yield-generating wallets that allow you to enjoy both the long-term price gains as well as the returns.

In Conclusion: hodling vs trading

If you're a novice cryptocurrency investor, proceed with caution. There is no right or wrong answer to which of these strategies is "superior" and you could always combine both methods to match your portfolio depending of your risk appetite. Always keep in mind that before making any decisions, always do your homework, research about the asset you wish to purchase and about diversifying your portfolio to reduce risk regardless of the strategy you pick.

As we move into a more digital world with enhanced security systems, so too are hackers and fraudsters. With millions of dollars lost each year at the hands of these ill actors, in this article we take a look at the 5 most common crypto scams and how to spot them. The financial world need not be a scary place, with a few precautions in place you can bank on being able to avoid them.

What is a crypto scam?

A crypto scam is a type of investment fraud revolving around cryptocurrencies. According to a report by Chainalysis, a record-breaking $14 billion of crypto was stolen last year through crypto scams. While there are many different types of crypto scams, of which we'll explore 5 below, the common thread is that crypto is wrongfully taken from a user through fraudulent activities.

The biggest crypto scam of recent times was in late 2020 when people hacked into the Twitter accounts of high profile individuals and claimed that should someone send Bitcoin or Ethereum to an address they will receive twice the value back. These accounts included the likes of Barack Obama, Elon Musk and Joe Biden.

The top 5 most common crypto scams

While there are an infinite amount of crypto scams out there, below we are highlighting the 5 most common ones.

Fake crypto exchanges

These types of exchanges provide a buy/sell platform on which users can trade cryptocurrency, however, once they have deposited the funds they cannot withdraw any money. These funds might still appear on the platform although the money is long gone.

Always read the reviews of a platform, and do your own research before depositing money anywhere.

Ponzi schemes

Ponzi schemes might have started in the late 1800s but they're still here. The scheme works in such a way that each member earns rewards by recruiting new members, whose money is then used to pay off older members. This eventually reaches a saturation point after which it collapses.

Always do your due diligence and ensure that the scheme you're investing in is solid. If it sounds too good to be true, it probably is.

Fake investment schemes

Be wary of an investment opportunity promising to deliver unbelievable gains. This might be in the form of depositing funds on a platform only to lose the money or struggle to withdraw it at a later stage. These are often circulated through well-known publications or on social media with celebrities "endorsing" the products.

Pump and dumps also fall into this category. These schemes are created when a large group of people decide to invest in a coin, only to drive up the prices and cash out at the top. Many people are then left with a worthless coin at the end, having lost their investment.

Imitating a crypto exchange

Similar to the concept of phishing, someone might create a social media account of a big exchange and contact the user "on behalf of the company". This is intended to gain your trust and is either done in an attempt to gain your passwords, or with a message that you owe large amounts in tax which needs to be paid in Bitcoin immediately to avoid imprisonment.

Never follow links in an email, rather access the site from your own browser directly and be sure to check the URL. Successful scams of this nature often have a small typo in the URL which goes unnoticed.

Malware & ransomware

The malware allows scammers to gain access to your computer, either locking you out of files or stealing credit card or crypto address details. With this information, they can drain your accounts in minutes.

Ransomware works slightly differently in that the scammers lock the entire computer and demand a ransom to gain access again. This is often paired with blackmail where the victim, and in some cases organizations, are threatened that if they don't pay sensitive information will be released. A lot of victims in this situation manage to get out of it unharmed.

These might sound very scary, but should you maintain safe online protocols and check URLs before entering your details, they should be entirely avoided.

5 tips on how to avoid crypto scams

These might sound obvious but it never hurts to read them again. Below are 5 tips on how to stay vigilant and avoid crypto scams entirely.

- Be wary of phone calls and emails claiming to be from exchanges and never click the links from them.

- Never give your password, private key or security codes to anyone.

- Never give someone remote access to your device.

- Look out for social media accounts imitating legal firms or exchanges or a prominent person in the industry. Support will never contact you from a social media account.

- And lastly, if it sounds too good to be true - it probably is.

Easily avoided, comfortably secure

We hope this information assists you in keeping your data and money secure online, proper security is always imperative when using payment methods or services on the internet. As technology evolves, so too must our security systems and vigilance. With these tips above you should be well on your way to spotting something that doesn't quite look right, and avoiding crypto scam.