More than a million Bitcoin have vanished because owners didn’t plan ahead. Without a crypto inheritance plan, your family could lose access to your assets forever. Here’s how to safeguard them.

Keep reading

As digital assets become a core part of personal wealth, one uncomfortable question lingers: what will happen to your crypto when you’re gone? Unlike traditional assets that can be managed through banks or brokers, cryptocurrencies are bound entirely to whoever holds their private keys. Lose the keys, and the funds are gone. Permanently.

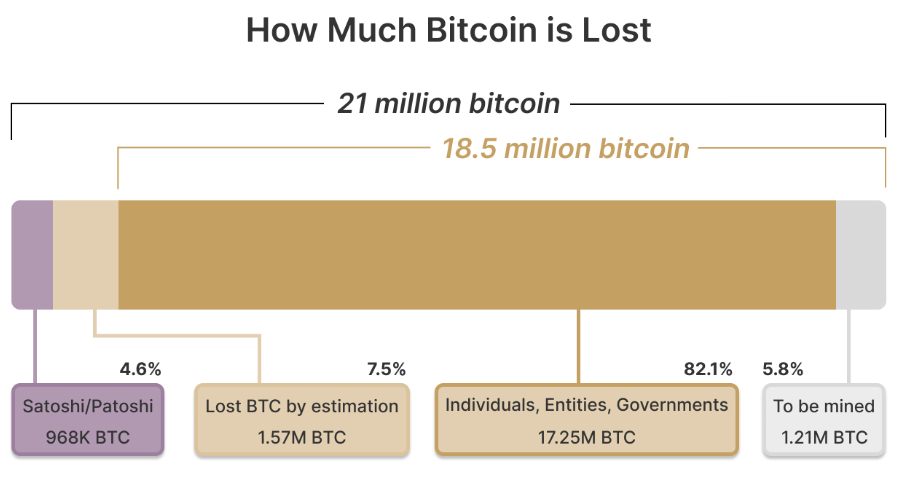

Each year, millions of dollars in Bitcoin, Ether, and other tokens vanish into the digital void when holders pass away without sharing access. It is estimated that around 1.5 million BTC (roughly 7.5% of total supply) may already be lost forever. With digital wealth now part of countless estates, preparing for the inevitable is no longer optional; it’s the responsible thing to do.

Why Planning for Crypto Inheritance Matters

In traditional finance, wealth transfer is handled through wills, trusts, and custodians. But crypto flips that model: you are the bank. Your heirs can’t simply request a password reset or call customer service. Without private keys, wallets, or access instructions, those assets are unrecoverable for all effects and purposes.

A crypto inheritance plan ensures that your digital assets, from Bitcoin and altcoins to NFTs and DeFi holdings, remain both secure and accessible to the people you choose. It bridges two crucial needs: protecting your funds today and ensuring your legacy tomorrow.

Beyond personal security, inheritance planning also reduces emotional and financial stress for your loved ones. By documenting how and where assets can be accessed, you prevent confusion and potential legal disputes.

Building the Foundation of a Crypto Inheritance Plan

Start with Legal Clarity

Consult an attorney familiar with digital assets. A properly structured will or trust should identify your crypto holdings, list beneficiaries, and outline how they can access those funds. Many jurisdictions still lack explicit laws for digital assets, so expert guidance helps ensure compliance and enforceability.

Secure Your Keys… But Don’t Overshare

The biggest challenge in crypto inheritance is private key management. If you die with your keys, your crypto dies with you. However, leaving keys in plain text within a will or document is just as risky. Instead, consider approaches like:

- Multisignature wallets, which require multiple approvals to move funds.

- Shamir’s Secret Sharing, which means splitting your seed phrase into parts distributed among trusted people.

- Encrypted backups or sealed letters stored in secure, offline locations.

Document recovery procedures in plain language so your heirs can follow them even without technical knowledge.

Choose the Right Executor

A traditional executor may not understand how to navigate crypto. You can appoint a tech-literate executor or designate a digital asset custodian to handle that portion of your estate. This ensures smooth execution and reduces the risk of errors or loss.

In a market driven by innovation and constant change, a well-structured inheritance plan offers something rare in crypto, certainty.

New Tools for a Digital Age

The rise of blockchain-based “death protocols” and smart contract automation adds a new layer of possibilities. Some platforms allow transfers to trigger automatically after certain conditions are met (for example, a verifiable death certificate or extended inactivity).

Ethereum and similar chains already support programmable inheritance systems, but these should complement, not replace, legal documents. Technology can help enforce your intentions, but law remains the foundation of inheritance.

Some investors even use “dead man’s switches”, automated systems that transfer funds if the owner doesn’t log in for a set period. While clever, it might be best to pair them with legal documents to prevent accidental activations.

Protecting Privacy While Planning Ahead

While planning for the future, it’s crucial to maintain security in the present. Avoid including wallet addresses, private keys, or passwords in public wills, which become part of the legal record. Instead, store such details in encrypted files or sealed envelopes accessible only to specific individuals.

Tools like decentralized identifiers (DIDs) and verifiable credentials can also help manage long-term identity and access rights. These systems allow you to define who can access what, and when, without intermediaries.

Custodial vs. Non-Custodial: Finding the Balance

When structuring inheritance, knowing whether your assets are held in custodial or non-custodial wallets makes all the difference.

Custodial services (like major exchanges) manage private keys on your behalf, which simplifies recovery if your heirs can provide proper documentation. However, it introduces third-party risk. Accounts can be frozen, hacked, or shut down.

Non-custodial wallets, on the other hand, offer maximum control and privacy but demand greater responsibility. If your heirs lose the seed phrase, there’s no backup plan. There’s also the possibility of taking a hybrid approach: keeping long-term holdings in non-custodial storage for security, while using reputable custodians for smaller, more accessible amounts.

Keep It Up to Date

A crypto inheritance plan is not a “set it and forget it” document. Prices change, portfolios evolve, and wallet technologies become obsolete very often. It may be wise to revisit your plan regularly, especially after major life events such as marriage, divorce, or the birth of a child.

It’s also worth keeping track of regulatory updates in your jurisdiction. Laws surrounding digital assets and inheritance are rapidly evolving, and what’s compliant today may not be tomorrow.

Common Inheritance Pitfalls

Even the best intentions can go wrong. Here are the most frequent mistakes to avoid:

- Including seed phrases directly in your will. As we mentioned before, this makes them public and vulnerable.

- Neglecting to educate heirs. Without guidance, even secure plans can fail.

- Relying solely on exchanges. Centralized platforms can fail or freeze funds.

Planning isn’t just about distributing wealth; it’s about ensuring continuity. A clear inheritance strategy preserves your crypto’s value and prevents it from becoming part of the estimated $100 billion in lost digital assets worldwide.

Protecting More Than Just Coins

Preparing a crypto inheritance plan isn’t merely about money; it’s about legacy. For all the talk about decentralization and autonomy, responsibility and forward-thinking remain at the heart of crypto ownership. By taking the time to plan ahead, you safeguard not only your wealth but also your family’s peace of mind.

NEWS AND UPDATES

LATEST ARTICLE

Bitcoin wallets are responsible for not only storing the digital asset but also providing access to the funds and allowing traders to conduct transactions. Whether you're buying Bitcoin for the first time or have been investing in the blockchain-based currency for years, understanding how a Bitcoin wallet works will assist you in developing and improving your trading experience.

In this guide, we're going to assist you in understanding what a Bitcoin wallet is, how they work, and where you can find the best one in the United Kingdom. Because where you store your money has become part of the Tap services that we offer.

What is a Bitcoin Wallet?

A Bitcoin wallet not only stores your digital asset but also facilitates the sending and receiving of BTC. While traditional wallets simply provide a means to store your money, crypto wallets are a more complex product providing more functionality to the user. The digital wallet connects to the blockchain and enables you to conduct transactions, keeps track of your balance, and acts as a "decentralized bank account".

There are different types of Bitcoin wallets with some being referred to as hot wallets while others are cold wallets. Hot wallets are simply cryptocurrency wallets that are connected to the internet, while cold wallets are only connected briefly when conducting trades. Wallets connected to the internet are more vulnerable to hacking, hence cold wallets being a more viable option when storing cryptocurrencies long term.

Cold wallets can come in the form of physical hardware, like a USB device, or merely a piece of paper (known as a paper wallet). Most wallets come free however hardware wallets you will need to purchase.

How does a Bitcoin wallet work?

As we mentioned earlier, Bitcoin wallets connect to the blockchain of the network. Each wallet is represented by a 26 character alpha-numeric code, known as your public key, which acts as your wallet address allowing anyone to send you Bitcoin and identify you on the blockchain.

Each wallet also comes with a private key, which is essentially the "pin code" to your wallet. This code gives you access to your wallet, allowing you to access and send crypto, and should not be shared with anyone. If someone were to gain access to your private keys, they would have control over your funds.

The Bitcoin blockchain uses the public keys to track Bitcoin transactions, with each wallet representing a BTC balance, and the network receiving updated copies of this. So while Bitcoin wallets don't actually "store" the digital currency, they hold a record of the current balance and previous transactions. As BTC is sent and received, the blockchain records and updates the ownership of each cryptocurrency as well as the wallets' balances.

What types of Bitcoin wallets UK are available?

There are several options available for Bitcoin wallets in the UK which we'll take a look at below. Crypto wallets fall into two categories - hot wallets and cold wallets - and will differ for each cryptocurrency. I.e. you cannot store Bitcoin in an Ethereum wallet, as each connects to a different blockchain. Bitcoin must be stored in a Bitcoin wallet and Ethereum in an Ethereum wallet.

Hot Wallets

Hot wallets are constantly connected to the internet and provide fast access to your Bitcoin portfolio. There are three main types of hot wallets:

- - Desktop wallet, applications on a desktop

- - Mobile wallet, applications on a mobile device

- - Web wallet, applications accessed through a web browser

While these wallets are known to be more vulnerable to hacking, they are the best options for someone looking to day trade.

Cold Wallets

These types of wallets are considered to be more secure as they are not constantly connected to the internet. There are two main types:

- - Hardware wallet, an external device that uses USB or Bluetooth

- - Paper wallet, where public and private keys are printed onto a piece of paper

When looking to make transactions, you will need to connect the cold wallet to a hot wallet. For instance, hardware wallets will come with hot wallet applications for desktop or mobile that, once connected, can facilitate transactions. Paper wallets also require a hot wallet to conduct the transactions.

An example of a hardware wallet is a Ledger Nano S, which allows you to open an account and provides both app and device to assist you in securely storing your crypto. Cold wallets are best suited for long term hodling.

Finding the best Bitcoin wallet UK

Finding the best Bitcoin wallet in the UK needn't be a tiresome task as we have you covered with the Tap app. While the app is conveniently downloaded to mobile devices, traders can carry their cryptocurrency anywhere, with much greater security than other cryptocurrency apps on phones.

While we've redesigned the tech behind traditional mobile wallets, we've also made things easier by allowing you to use a password of your choice. With an easy to navigate interface, and all your balances stored on one page, the Tap app is every trader's dream.

Our Tap wallet allows you to store both crypto and fiat currencies and uses a hybrid of both hot and cold wallet technology to ensure that they are always highly secure, and always available.

Security and convenience are key

If you're searching for a reliable Bitcoin wallet option in the UK, you'll discover it conveniently with the Tap app. Simply download the Tap app, set up an account, complete the KYC verification, and you'll have the opportunity to securely manage your cryptocurrencies with top-notch security features that are available on the market.

You've likely heard a Bitcoin maximalist tell you that crypto is the future and will eventually replace fiat currencies. While that's unlikely to happen overnight or any time soon, we're exploring the question looking at many factors that will contribute to this tech-forward proposition.

While investor interest has certainly infiltrated mainstream culture, cryptocurrencies need to overcome several obstacles before they become a viable replacement. The obstacles include practical application, a willingness from merchants to embrace digital currencies, the market's volatility, and usability. Bearing that in mind, there have still been a number of shifts indicating that crypto adoption is certainly on the cards.

El Salvador Legalises Bitcoin

In June 2021, the president of the small Central American country, Nayib Bukele, announced that Bitcoin would officially be accepted as legal tender. The president also announced plans to create a Bitcoin City with the intention of becoming "the financial centre of the world.".

Rolling out a number of services to support this concept, including a national wallet named Chivo, the endeavour cost a large amount of taxpayers' money, and not all were happy about this.

On the other hand, Bukele was praised for being a revolutionary in the tech field, and a pioneer in the movement to shift from fiat to crypto. It's worth noting that there were mixed reactions on both sides of the crypto fence, some favouring the movement while others expressed concern over it being too premature.

New York Mayor Accepts Salary In Crypto

In a move to make New York City the crypto capital of the world, the current mayor, Eric Adams, has stuck to his word and accepted his salary in crypto. As part of his campaign, the politician promised to accept his first three paychecks in cryptocurrency and received his first instalment in a combination of Bitcoin and Ethereum in January.

Adams has also been vocal about his support for the NYC Coin, a digital currency that would take on similar functions as the Miami Coin released in 2021. Adams confirmed in a statement:

"New York is the centre of the world, and we want it to be the centre of cryptocurrency and other financial innovations. Being on the forefront of such innovation will help us create jobs, improve our economy, and continue to be a magnet for talent from all over the globe."

Rise In CBDCs

Venezuela is another country to adopt a pro-crypto attitude albeit born from less savoury conditions. Following a bout of hyperinflation, many turned to cryptocurrency as an alternative store of value, and as an income source as mining in the area with such low electricity prices was very lucrative.

This eventually led to the country creating its own digital currency, the Petro, released in 2018. Cryptocurrencies released by the government in this nature are referred to as central bank digital currencies, CBDCs.

The Bahamas and Nigeria also recently released their pilot central bank digital currencies to test the functionality and national responsiveness of the people. The "Sand Dollar" in The Bahamas is believed to be born from a combination of centralized banks being destroyed by hurricanes and accessibility to money across the various islands.

Nigeria confirmed that the move was in line with needing a more digital approach to finances as the country has a considerably young population (in 2020, 43% of the population was aged 0 - 14 years).

A number of other countries have also announced plans to "explore" CBDcs, with China also currently rolling out a pilot program in several cities across the country. Decentralized digital currencies play an advantageous role over fiat currencies in countries affected by corruption and with largely remote areas.

The Future Of Crypto

The future looks bright for the integration of cryptocurrencies into our traditional financial space. While it's unlikely that crypto will entirely replace fiat currencies (anytime soon or ever) it is likely that they can work alongside each other. With the rise in CBDCs around the world and the increase in mainstream crypto integration, the world has certainly taken notice of the vast benefits of using cryptocurrencies and the innovation in the space.

Tap remains ahead of the curve with its mobile app allowing users to pay for everything using cryptocurrencies from their portfolios. Simply select which cryptocurrency you would like to use and Tap will liquidate it for the local currency of the relevant account and send the required amount of fiat funds without any hassle for you. Simple and efficient, Tap is paving the way for the future.

Investing is not as easy as the internet makes it seem, with every profit comes plenty of research behind it. Not to mention all the strategies. Similar to trading, investing can at times be time-consuming and demanding. While investing, whether in the stock market or cryptocurrencies or any other asset classes, is beneficial in so many aspects, it can also come with some trial and error. In this article, we take a look at the time-tested dollar-cost averaging and explain why this is considered to be a low-risk strategy.

What is DCA?

DCA is an abbreviation for dollar-cost averaging. You may be wondering what DCA is? To put it simply, DCA is an investment strategy that sees people investing gradually over time rather than dropping a lump sum of money into assets.

Let's say an investor has a total of $10,000 to invest monthly, lump-sum investing would see them entering all that money into an asset market while DCA would have them investing $500 each week or month. Not only does DCA provide your leeway to pay your bills while still investing, but it also protects you from excess loss. While lump-sum investing does have its perks, it also has the potential for big losses.

By investing only what you are willing to lose, you are at no risk of financially crippling yourself. DCA ensures you do not lose all your money on an investment, whereas one wrong trade in lump sum trading can greatly set you back. DCA is a great way for newbies to test the markets and trust in an investment before moving forward, seasoned traders are also a fan of DCA as it allows them to diversify their funds in a more structured way.

The point of DCA is to avoid market watching and big losses, DCA is the practice of routinely investing smaller amounts, timed over regular intervals, regardless of price. This typically allows the investor to buy an asset at an average cost of a long period of time.

Why and how to use DCA

The how is easily answered, as already stated prior, it is as simple as allocating a set amount aside each month with the plan to invest. You invest your set amount a month routinely, regardless of the price, growing your total shares. But the real question is why? Why is this strategy so popular and why is it so highly recommended? Let's get into it.

The benefits right from the get-go are clear, you hold less risk of losing everything at once. As the traders' tale goes, only put in what you are willing to lose. Lump-sum investments do not take this approach with caution, putting it all on the line, or a large portion at least.

DCA means that you are continuously putting in small amounts that do not greatly limit your day-to-day life while still growing the value of your portfolio. DCA is a longer-term investment strategy. It also eliminates some of the risks involved with investing.

With DCA, the markets don't matter, you are buying your assets at whatever price they are at and reaping the profits when the price climbs. But also, by purchasing every week rather than all at once, you have the option and ability to buy in on the volatile markets getting better prices per share than someone who puts it all in at once.

This strategy also helps you manage emotional investing, forcing you to hold onto your investment despite FUD being spread, ensuring you don't sell low or buy high.

The DCA conclusion

While there are many investment strategies out there, this is a favoured strategy by many investors, that is not to say it is the only or best strategy, just one to consider. There are many perks that come with DCA, and that's what we wanted to highlight in this piece for you today. DCA provides a sense of commitment that is hard to find, ensuring you secure your space in the market without any added risks. There will always be risks involved with investing, but the DCA strategy finds some ways to minimise those risks in comparison.

Any crypto trader or investor will know the rigorous, albeit essential, process of completing KYC practices before being able to buy or sell Bitcoin and other cryptocurrencies. In this article, we're debunking the myths and highlighting the reality of why these Know Your Customer processes are necessary, and how it fits in with AML (anti-money laundering) laws.

As cryptocurrency exchanges continue to solidify their position in the greater financial landscape, the need for strict and regulatory practices has increased. Due to the nature of cryptocurrency transactions being pseudonymous, the need to weed out illicit activities is imperative.

With little regulation in place, the market remains vulnerable to all kinds of criminal activity, from terrorist financing to ransomware attacks. While regulators were scrambling to change this, a whole new industry within the crypto space evolved. From the even more decentralised nature of DeFi to entirely unregulated NFT dealings, both financial regulatory bodies and institutional investors have joined forces to create more structured frameworks to fight blockchain crime. The results have proven to be successful.

With fast-changing landscapes and increasing innovation, regulating the crypto markets comes with a need to match the pace. Considering that the current financial regulatory frameworks were created based on fundamentally different economic principles, regulatory bodies have their hands full when it comes to building and implementing regulations that can support, while not extinguishing, this financial services revolution. Not to mention the laws required from an insurance standpoint.

What Is AML In Crypto?

Anti-money laundering encompasses a range of regulations, procedures and laws to stop criminals from disguising illegally obtained funds as legitimate income. These measures were not implemented into big exchanges in the early stages of the crypto timeline, but are rather now making their way into platforms' due diligence processes as per tighter regulations. These generally involve traders confirming their identity before being able to conduct any payments when buying digital assets or executing any crypto transactions.

As noted in the banking and crypto industries, when individuals or businesses attempt to conceal unlawful earnings this is typically done in three stages: placement, layering, and integration. The placement layer involves the money being deposited on the crypto exchange.

The layering stage is when the illegitimate funds are mixed with legal funds making it challenging for authorities to keep tabs on them. In the final stage, the laundered money is "cleaned" and returned to the beneficiary. This is how criminals circulate illicit income and manage to launder money undetected.

In the decentralised world of cryptocurrencies keeping tabs on such activities has its own set of challenges. Hence why AML measures and controls are vital to the industry's operations as well as reputation.

However, as mentioned above, these measures need to be carefully implemented so as not to kill the nature of why people are attracted to cryptocurrencies in the first place (being free from third parties or central authorities). The regulations need to respect the decentralised nature of cryptocurrencies while still providing the opportunity for policing should illicit activities be happening, and then needs to be built into the business model of the company providing the crypto services.

The Crypto AML Red Flags

While there are plenty of anonymous means of transacting your crypto, such as privacy-focused cryptocurrencies, there are still several aspects that traditional cryptocurrencies possess that trigger red flags when it comes to AML.

The estimated amount of money laundered in 2021 is $800 billion - $2 trillion, with roughly 50% of money laundering going undetected. According to a Basel System Report, 62% of compliance officers in business crime say that this type of criminal activity is becoming more difficult to spot. With this in mind, here are the top AML red flags that are present across the board:

Obscured identity of transaction makers

Unclear transaction size

Obscured geographic location

Unofficial profiles of parties involved

Lack of information on the source of funds

Withdrawing funds from a wallet with no transaction history

Consecutive high-value transactions

How AML Protocols Are Implemented At Crypto Exchanges

As crypto exchanges work toward integrating cryptocurrencies into the mainstream financial landscape, they are required to work hand in hand with regulatory bodies. These actions vary around the world, with many countries opting to embrace different methods of imposing AML practices.

Here is a look at how 5 countries imposed varying rules:

The U.S.

Governed by the Financial Transactions and Reports Analysis Centre (FINTRAC) and Financial Crimes Enforcement Network (FinCEN) the country has strict regulations when it comes to AML and KYC regulations. It continues to work on the legal framework.

South Korea

Following an investigation with crypto exchange Bithumb revealing that $1.45 billion worth of funds were illegally moved through the platform, the country is working on imposing more defined AML and KYC rules.

Singapore

Taking a rare approach to crypto regulation, the financial hub of Asia and a key player in the development of the blockchain and crypto industries, Singapore is choosing to educate people on the technology rather than impose stringent policies.

Canada

The country recently imposed regulations under the guidance of the FINTRAC unit that mandates the same KYC requirements as traditional financial institutions.

Thailand

The Thai regulatory bodies have implemented regulations to keep foreign investors out of their local markets by upgrading their KYC regulations with in-person verification and microchips in their ID cards.

Today, most modern nations have implemented rules that demand businesses to use sophisticated technologies to prevent crypto from being utilised to finance unlawful activities and protect their investors.

Cryptocurrency compliance is an industry that has its own set of rules. Every year, businesses must demonstrate greater levels of security and minimise risks in order to stay compliant. KYC/KYB/AML processes are taken very seriously by reputable cryptocurrency firms. They might be subject to huge penalties if they fail to comply with this requirement.

In Conclusion: AML Is Here To Stay

While these new financial transparency measures might go against the very nature of cryptocurrencies, it is important to ensure the security of crypto users, and for the overall adoption of the industry. They also play an imperative role if crypto wants to live alongside fiat currencies in the global financial landscape.

The introduction of new global regulations contributes to the growth of the cryptocurrency industry. Despite a widespread misconception, digital currencies are traceable and do not account for most financial crimes.

Reputable cryptocurrency platforms collaborate with law enforcement to assist in the prevention of illegal activities. They also safeguard their users from fraud and other potential risks.

If you’re thinking about incorporating crypto into your business or looking to better understand how digital currencies are infiltrating the business world, you’ll find everything you need to know on the topic below. Looking at the benefits these digital currencies can provide, as well as the downsides, we are effectively dissecting the concept of cryptocurrency in a traditional business model.

Each day we move into a more digital space, be it from the way we communicate to the way we pay for goods, there is no denying that the direction we’re headed in is digitally dominated. The evolution of money is taking a similar stride, from gold coins to banknotes to electronic transfers, and now, digital currencies.

Since the advent of Bitcoin, the world’s first cryptocurrency, over a decade ago, the world has embraced the new age payment system (even if it was one sector at a time). From early investors and developers to huge corporations, crypto has and continues to, infiltrate the financial sector. The recent Bitcoin futures ETF approval provides a classic example.

Crypto In Business

Since the global pandemic, Bitcoin (and the cryptocurrency industry) has edged itself into both the mainstream media as well as the corporate world. Following global market crashes, Bitcoin rose from the ashes and soared to reach unprecedented highs months later.

Many corporations looked to shift their company reserves from the devaluing US dollar to Bitcoin, instigating a massive wave of institutional involvement. Many big companies, everyone from PayPal to Wholefoods, started accepting (or facilitating the trade of) Bitcoin, and gradually crypto became less of a taboo in the Financial sector.

By the end of 2020, it is estimated that around 2,300 businesses in the United States had started accepting cryptocurrencies, alongside the 17,000 Bitcoin ATMs available across the country. As more businesses create teams to focus on the benefits of implementing cryptocurrency in their business, we’ve outlined the pros and cons of adopting the revolutionary technology.

The Pros Of Crypto In Business

For those not yet familiar with the benefits of crypto, or perhaps what it could do for companies (especially virtual and e-commerce ones), find the advantages that cryptocurrency can bring below:

• Removes The Middleman

The intent behind cryptocurrency creation was to establish a peer-to-peer payment system that circumvents the need for intermediary banks and financial establishments. This direct transactional approach results in diminished fees, quicker processing times, and a reduction in the often protracted paperwork and administrative formalities. Instead of relying on centralized entities, this payment system relies on a distributed network and a transparent, unchangeable ledger for its operational functionality.

• Fast, Secure Settlements

The network can facilitate international transactions in under an hour, for a fraction of the cost that fiat transactions cost. Using encrypted means of facilitating transactions, cryptocurrency networks are much more secure than any traditional bank.

• Increased User Engagement And Conversion Rates

The more payment options a company offers, the bigger the net of potential customers and conversion rates. The same is true for a wider range of currencies. By providing more options for customers to choose from, the wider the net of potential profit grows.

• Growth Potential

Change often leads to growth, particularly in saturated, highly competitive markets. Adopting and supporting crypto in business practices puts the company at the forefront of emerging technology, a space many will want to be as the world gets more digital.

• Lower Transaction Fees

Payment networks are notorious for charging high fees when receiving transactions, however, Bitcoin and other cryptocurrencies typically charge a much lower percentage. Tap has recently opened a channel for companies to conduct crypto business activities, and charges as low as 1.00% fees on transactions for business accounts.

The Cons Of Crypto In Business

Of course, there is always a downside to everything. Below we look at some of the risks associated with incorporating cryptocurrencies in business.

• Volatility

Cryptocurrencies have become synonymous with volatility, as the markets move to match supply and demand. Each market has been known to go through stages of increased price movement, however, analysts remain certain that while short term volatility is imminent, long term growth is on the cards.

• Consider Your Target Market

Not everyone has jumped on the crypto bandwagon so it is best to assess whether your clientele would be interested in such an option. If your business is catered to a predominantly older demographic then perhaps incorporating crypto as a payment option is not the best move.

• Security Is Your Responsibility

In the past, many people have lost their crypto portfolios due to lost private keys or hacks. With cryptocurrency, the onus lies on the holder to maintain adequate security measures in order to ensure the safety of the funds. Thankfully, Tap’s business section bypasses with cold storage of your cryptocurrencies assets and state of the art security.

Conclusion

After evaluating the advantages and disadvantages of incorporating cryptocurrency into your business, take a moment to determine if this decision aligns with your company's strategic direction. If you're considering integrating this modern payment system into your business operations, consider Tap as your solution to handle your requirements and provide the necessary infrastructure for the implementation of cryptocurrencies in your business.

Cryptocurrency and blockchain technology are not the easiest topics to understand, especially with fast and ever-growing industries forming beneath them. Even if you have a grasp on the core details, there is still a lot of external factors that come into play. While Bitcoin and other cryptocurrencies hold undeniable value, external factors still hold considerable influence and can affect the financial value of these assets.

When it comes to trading cryptocurrencies, having an understanding of the market can prove incredibly useful, while having an understanding of crypto fundamental analysis can prove to be invaluable for traders, investors, and those curious about sentiment. In order to understand why crypto fundamental analysis is so important, we need to understand what it is.

What is fundamental analysis?

Fundamental analysis can be understood as methods to evaluate the core metrics and proposition of an asset, in this case the world of digital money, cryptocurrencies. Fundamental analysis is more than looking at the price of a cryptocurrency, but rather delving deeper into the external factors that could impact the product, such as macro and micro factors.

Fundamental analysis is about looking at all the available data of a financial asset. This can include countries' sentiment towards the currency, how many people are using the digital cash every day, or even the team behind the project.

The process of fundamental analysis can be started by taking a wider outlook before narrowing it down and focusing on smaller details. You would start by evaluating the projects' market cap and how healthy the ecosystem is in terms of daily buy-in or sales data. You could then look at the projects' marketing approach, the team, and what the public has to say about the token, for an example of strategy.

To put it simply, looking at what the media is saying about Bitcoin would be an in-depth outlook, whereas just looking at the price would be considered more of a broad approach, all these factors work together to create fundamental analysis.

There are three metric areas of analysis that investors generally look at, so let's take a deeper look at those fundamentals.

Fundamental analysis metrics

These are a few of the most common metrics investors look out for, although there are definitely more things to keep in mind. At the basics of fundamental analysis, it is just doing your own research and seeing if a project aligns with what you are looking for, whether that be long-term or short-term.

The three main metrics that people evaluate are on-chain metrics, project metrics, and financial metrics. There are some things within those metrics to be considered:

On-chain Metrics

- Transaction Count

- Active Addresses

- Fees

- Hash Rate

Financial Metrics

- Market Cap

- Liquidity

- Token Supply

Project Metrics

- Whitepaper

- Tokenomics

- Competitors

- Team

These metrics will help you vet projects you potentially want to invest in or trade. Let's take a look at an example from each one. Starting with project metrics, looking at the team behind a project often shows whether they have the experience or commitment to see a project through to success. When it comes to financial metrics, understanding the token supply and the potential it has on the market cap in the future can be greatly rewarding.

Finally, for on-chain metrics, finding out how many active addresses there are within that blockchain can pinpoint whether this chain has a flourishing and healthy ecosystem for buyers and sellers. All points should be taken into consideration to verify your fundamental analysis.

Crypto fundamental analysis Q+A

After covering what fundamental analysis is, how it affects cryptocurrency investing, and what metrics to consider, let's look at some of the frequently asked questions. These are the most commonly asked questions when it comes to cryptocurrency fundamental analysis.

Is there fundamental analysis in crypto?

Yes, as outlined by this article. Fundamental analysis in crypto is very similar to that of more traditional financial assets, just with a few different metrics in place.

How do you analyse crypto?

As already stated, there are three main metrics investors and traders look at: projects metrics, financial metrics, and on-chain metrics. There are more metrics to be considered, but these have been proven to be the most helpful.

What fundamentals affect Bitcoin?

Bitcoin doesn't have much of a focus on project metrics, as it lacks a team and tokenomics for the future. The metrics relating to market cap, token supply, transaction count, active addresses, and fees are still very much important to look at.

Is fundamental or technical analysis better?

That depends on what your goal is, without going into too much detail about technical analysis, most prefer it for short-term reasoning whereas fundamental analysis can be used for short-term and long-term reasoning, although it is much better for the long term.

Does fundamental analysis work?

Yes, it most certainly does when done properly. It's basically just in-depth research of a project to see whether it has the potential to succeed or fail.

Crypto fundamental analysis conclusion

And now you know. These are the basics of fundamental analysis when it comes to cryptocurrency, as vague as they may seem, these are the markers to consider when vetting a project you want to put funds into. Sadly we can not help you vet every project you come across, but we hope this guide will assist you in more confidently doing the analysis yourself.

Every project is different, from its founding date to the project economics, but the above information should help you get a rough idea of whether it is a project you are interested in. In crypto, it always comes down to "DYOR", or do your own research, and crypto fundamental analysis is no different. Good luck and happy fundamental analysing.