With a Fed rate cut nearly certain, these three altcoins are positioned to capitalize on the macro shift, here's what makes them stand out.

Keep reading

Heading into the Federal Open Market Committee’s October session, a high-stakes environment is emerging for crypto markets. With the CME Group’s FedWatch Tool showing about a 96 % chance of a 25-basis-point rate cut, the market is eyeing how digital-asset prices might respond.

With macro liquidity on the radar again, these three altcoins stand out as tokens worth tracking under the spotlight of the Fed’s next move.

1. Chainlink (LINK)

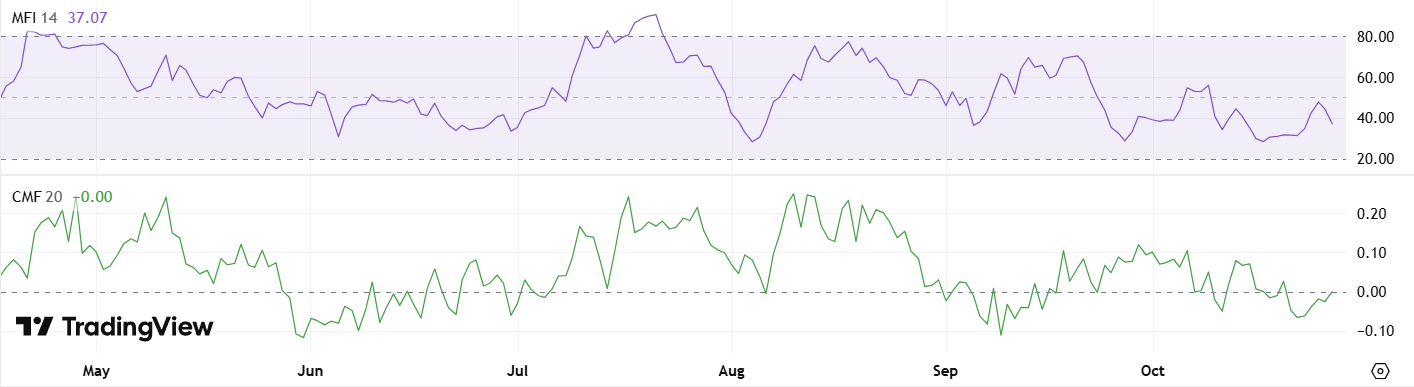

Chainlink has been acting under pressure, trading inside a falling wedge, a pattern which sometimes marks the end of a downtrend. Still, some caution flags remain. Over the past month LINK has been trading downwards, though it’s gained some strength in the last week amid renewed buying interest. The key support around $17.08 remains critical, if LINK closes below that, a drop toward $16 could be triggered.

Conversely, diagnostics like the Money Flow Index (MFI) and Chaikin Money Flow (CMF) are showing signs of life, hinting at growing accumulation from larger holders. Combine this with a potentially dovish Fed decision, and Chainlink could be gearing for something special.

2. Dogecoin (DOGE)

Dogecoin enters the FOMC event with a bit of range-bound suspense. Since October 11, DOGE has been oscillating between $0.17 and $0.20, waiting for a trigger. A clean breakout above $0.21 could open the door to a move back towards $0.27, especially if risk-on sentiment returns.

Volume and whale‐level data add texture to the setup. The Wyckoff volume profile recently flipped from seller control to buyer control, suggesting strategic accumulation may be underway. DOGE may be quieting down before a move, a scenario traders should keep front of mind as the Fed’s decision could stir things.

3. Uniswap (UNI)

Uniswap offers compelling recovery stories entering the FOMC session. The token experienced a sharp drop on October 10, with the RSI falling below 30, classic oversold territory. Since then, UNI has rallied from near $6.20 toward $6.50, supported by strong volume on the breakout. Holding above $6.40 may confirm that buying interest is sustained.

For longer-term watchers, UNI’s former highs at $12.15 in August and $18.71 in December set the stage for what could become a multi-leg recovery if macro conditions cooperate. In a market where liquidity expectations hinge on the Fed, Uniswap's rebound has the potential to accelerate, particularly if altcoin capital begins rotating into DeFi infrastructure.

The Verdict

These tokens aren't just compelling because of their individual fundamentals, it's how those fundamentals intersect with the current macro picture. With markets rebounding and rate cuts looking increasingly likely, crypto stands to gain. Lower rates typically fuel risk appetite, unlock liquidity, and drive capital toward speculative plays, creating tailwinds that can supercharge momentum in well positioned altcoins.

That said, the Fed could also surprise with restraint, and even another “standard” 25-basis-point cut may be viewed as lukewarm. In such scenarios, the dollar may strengthen and risk assets could wobble. Traders and investors should therefore approach the market with discipline, track the macro context, and be prepared for either direction.

NEWS AND UPDATES

LATEST ARTICLE

Whether dissecting crypto or fiat currencies, the foundations remain the same: the currency must serve as a store of value and function as a medium of exchange for goods and services. While both these currency options tick those boxes, cryptocurrencies tend to also be followed by a dark cloud of volatility in the financial sector.

Market volatility is a natural byproduct of a developing market, however, it can also cause many losses if not managed correctly. When the crypto markets go through high levels of market volatility they tend to get discredited with being a viable payment option. After paying withness to the Bitcoin market swings, several individuals recognised this flaw in the digital currency space and created a solution, "the stablecoin".

In this article we establish what is a stablecoin is, how it fits into the financial landscape and explore the pros and cons of these digital currencies.

What Is A Stablecoin?

Stablecoins are digital currencies that harness the benefits of being a decentralized, blockchain-operated currency without volatility. Backed by any currency or commodity, stablecoins are pegged to the value of their underlying asset and managed and secured by their relevant platforms. For instance, Tether is pegged to the US dollar while Tether Gold is pegged to the price of gold and Tether EURt is backed by the Euro.

These currencies operate like any other cryptocurrency, using blockchain technology to maintain and operate the network, but do not fluctuate in value based on supply and demand. Rather the price remains consistent with the asset it is pegged to, providing a better tool for digital payment transactions.

How Do Stablecoins Maintain Their Price?

While we've established that stablecoins are pegged to a commodity and reflect that price, let's cover how exactly that is achieved. Using fiat-backed stablecoins as examples, the companies behind these coins are required to hold a US dollar equivalent for each coin in circulation (or Euro if the stablecoin is pegged to it).

These funds, also referred to as reserves, are either held in bank accounts or can be a combination of cash and short-term U.S. Treasury bonds. Most of the companies issuing stablecoins conduct third-party audits to prove that their reserves are at the correct levels and release this information to assure users that their coins are always worth $1 (or the currency-backed equivalent).

Why Have Stablecoins Become so Popular?

The first stablecoin to enter the market was Tether in 2014, pegged to the US dollar. Tether is currently the third-largest cryptocurrency based on market capitalization, illustrating its vast popularity. The second biggest stablecoin currently on the market is USD Coin, also backed by the US dollar, which sits in the top 5 biggest cryptocurrencies with an equally impressive trade volume. Both these coins have provided valuable talking points within the industry as their market caps and adoption increase and they climb the ranks of the biggest cryptocurrencies.

Due to their resistance towards volatility, stablecoins have increased in popularity and are more widely used for conducting business around the world and executing cross border payments.

The Pros Of Stablecoins

Stablecoins are popular options for both businesses and individuals conducting business across borders. Below we outline the top benefits that stablecoins present to the market:

Digital Currency

The obvious first benefit of stablecoins is that they are maintained by blockchain technology and able to conduct international transactions in a much shorter time frame and for less cost than fiat currencies. The fast settlement times make these currencies an excellent, cross-border medium of exchange. They are also easy to use as they operate from wallets in similar ways to traditional cryptocurrencies.

Zero Volatility

Due to the nature of stablecoins being pegged to a fiat currency or commodity, they typically experience little to no high volatility trading periods resulting in a more reliable currency with the benefits of blockchain technology. Pertinent to increasing its adoption.

Hedge Against Failing Markets

Stablecoins have become increasingly popular for traders to hedge against other cryptocurrencies when markets experience a decline in price. Stablecoins allow traders to quickly liquidate their digital assets and easily reenter the market when the price stabilizes.

The Cons Of Stablecoins

Centralisation

While blockchain technology and cryptocurrencies celebrate the notion of being decentralised, stablecoins do bring in a nature of centralisation, particularly when it comes to the backing of the assets. Ensuring that each coin in circulation is backed by an equal reserve value requires a team that leans the operation more toward a centralized structure.

Transparency

Several stablecoins have been called out publicly for not being transparent with their reserves. Tether, for example, has seen much public outcry concerning whether the company has the correct amount of reserves, leading to fines and regulations imposed by the US government. They have since released a report on the current reserve holdings of the company.

In Conclusion

Many traders have incorporated stablecoins into their portfolios, to have as a hedge against falling crypto markets or falling fiat markets. These digital assets are also used by businesses around the world to conduct payments with the benefits of digital currencies and without the risk of volatility. Through the Tap app, users can now access and purchase USD Coin (USDC) as well as Tether (USDT). The sleek design of the app interface makes it easy for users who want to buy or sell cryptocurrencies with fiat currency through their phones in a click.

When it comes to choosing a stablecoin, consider the projects behind it, the liquidity and the ease of use in terms of wallet compatibility.

If you're looking to earn extra money from anywhere online you've come to the right place. Making money online has certainly become more accessible and easier over the years, and in this blog, we're reviewing several ideas to do so without having to invest.

Whether you're looking to make some money on the side, or as a full-time pursuit, remember that as with most things in life: consistency is key. On this page, you'll find a number of beginner options requiring no particular skillset (only a bank account) for you to look into, relevant everywhere from the United Kingdom to the European Union to Australia. Each method varies in financial contribution, which we've highlighted at the end with a rating of the start-up costs.

Top 5 ways to make money online for beginners

1. Affiliate marketing

Affiliate marketing involves an individual earning money through promoting another business's product. This can be done through your own platform which might range from a blog to a website, social media, email campaigning or simply Google Ads.

All you need is a working internet connection, a bank account and a reliable browser. Each time a friend or family clicks and signs up for the product, you bank a commission.

Many companies these days offer this service, try to find one that you and your network might be interested in and see the opportunities that they present.

Start-up Costs: $

2. Dropshipping

This will require a substantial amount of effort, however, the returns will be that much greater. Dropshipping involves selling a product online that you do not need to keep an inventory of, instead, the company that you are buying the goods from sends them directly to the customer.

You act as the middleman between the manufacturer and the consumer and make money from the margin that you add. The start-up costs will be for your online website and marketing.

Start-up Costs: $$

3. Freelance your skills

You can hire out your skills on sites like Upwork or Fiverr. Users create profiles expressing their skills, anything from writing to graphic design to music creation, and can apply to jobs requiring these skills.

These sites will typically allow employers to connect with employees, and once the work is completed the funds are deposited directly into your account. This is also a great way to start a side hustle in your area of expertise without having to tuck into your savings.

Start-up Costs: zero

4. Explore the world of cryptocurrencies

Engaging with cryptocurrencies has gained significant attention in recent years. Before diving in, it’s important to educate yourself thoroughly to grasp the complexities involved. Our blog section on how to learn about crypto is a great place to begin. The cryptocurrency market is known for its high volatility, which presents both risks and opportunities. Whether you're active daily or only occasionally, understanding the landscape is key. To get started, consider signing up for a reputable and regulated platform like Tap, which can help you manage your funds securely.

Start-up Costs: $$

5. Participate in online surveys

Online surveys are a popular way for beginners to make money online. Companies are always looking for feedback on their products and services, and they are willing to pay for it. There are several websites that offer paid online surveys, such as Swagbucks, Survey Junkie, and Toluna.

To get started, simply sign up for an account, complete your profile, and start taking surveys. You'll earn points or cash for each survey you complete, which can be redeemed for gift cards or PayPal payments. Keep in mind that surveys may have specific demographics, so you may not qualify for every survey. However, with some patience and consistency, you can earn a decent amount of extra income in your spare time.

Start-up Costs: zero

Earn money online from anywhere in the world

Of course, this list is only a small portion of the ways you can make money online, simplified down to the top 5. If you have more time at your disposal you can engage in market surveys, beta testing, becoming a virtual assistant, or even coaching.

The opportunities are endless, with a wide range of start-up costs, time management, returns and the amount of effort required are to be considered. Ensure you do adequate research in order to learn about your next venture before diving in. At the end of the day, anyone can earn money online, the first step is just to get started. Good luck, may you have only lucrative experiences.

5 tips on how to manage your money

Now that you’ve established your income stream/s, here are 5 tips on how to manage the money you’re making. Whether you’re doing this as a side hustle or a full time job, consider implementing the following 5 steps in order to build your finances. .

- Build an Emergency Fund

Just like in personal finance, building an emergency fund is crucial for making money online. This fund will act as a safety net in case you hit a rough patch, and it will allow you to continue your online work without financial stress.

- Create a Budget

Budgeting is another essential aspect of making money online. Creating a budget will help you keep track of your income and expenses, and it will allow you to make informed decisions about where to allocate your resources.

- Focus on Your Niche

To make the process of making money online more enjoyable consider focusing on a specific niche that you are passionate about. Whether it's writing, graphic design, or web development, become an expert in your field and provide value to your clients.

- Network and Build Relationships

Building relationships with other professionals in your industry is a valuable step when making money online. Networking can help you find new clients, build your reputation, and even lead to new business opportunities.

- Stay Consistent and Persistent

Making money online takes time and effort, and it's important to stay consistent and persistent. Set realistic goals for yourself, create a schedule, and stick to it. Remember that success doesn't happen overnight, so don't get discouraged if you don't see results right away.

So, what are you waiting for?

For all those curious about the crypto industry ready to dip their toe in the water, this one is for you. Below we share a warm welcome to the industry with a range of helpful resources covering everything from what cryptocurrency actually is to how to buy and store it. For individuals and businesses alike, let's get into it.

What Is Cryptocurrency?

A great place to start for any people who are crypto-curious, let's cover the basics. Cryptocurrency is essentially digital cash that can be transferred from one person to another without having to rely on an authoritative entity (like a bank or government or financial institution).

This peer to peer cash system is supported by blockchain technology, a technology that facilitates the transactions and essentially acts as a giant public ledger where anyone can view any transactions that have been made on the network.

Through the use of blockchain, a decentralised network (meaning that no one is in charge, rather everyone follows the same protocol) of computers is responsible for verifying and executing transactions. Depending on the network this can be done in a few seconds or up to a few minutes, causing big waves in the traditional financial sector.

If you take away just four points from the above, let it be

- Digital cash

- Peer to peer

- Blockchain technology

- Decentralised

Cryptocurrency gets its name from cryptography currency, as it uses encrypted code (cryptography) to secure and maintain the network.

Each cryptocurrency will have a value, based on what it was last traded for, a market capitalisation, a circulating supply and a ticker symbol. The ticker symbol would be BTC for Bitcoin and ETH for Ethereum.

Let's Take A Look At The Three Biggest Cryptocurrencies

You've definitely heard of Bitcoin, but what about the other top cryptocurrencies? Below we give a very quick breakdown of the other big projects on the scene based on the biggest market caps. When learning about new coins we strongly advise that you do your own research before making any purchases.

Bitcoin (BTC)

A digital cash system that facilitates the quick and cheap cross-border transfer of money.

Ethereum (ETH)

A blockchain platform that allows developers to create their own decentralised applications on top of theirs.

Tether (USDT)

A stablecoin, meaning that its value is pegged to a fiat currency, in this case, the US dollar. 1 USDT will always be worth $1. Stable coins are a great way to enter the market as they are less volatile than traditional cryptocurrencies.

How To Store Cryptocurrency

Similar to fiat currencies, cryptocurrencies need to be stored in a wallet. As the currencies are entirely digital, so too must the wallet be. Each cryptocurrency operates off a different network, requiring one wallet for each network.

For instance, you cannot store Bitcoin in an Ethereum wallet as Bitcoin runs off a separate blockchain. Different to fiat wallets, digital wallets are how transactions take place. From your wallet, you will enter the crypto wallet address of the recipient and execute the transaction from there.

To purchase and accumulate cryptocurrency, you will first need a wallet. There are a few different types of wallets, but let's keep it simple for now. On Tap, a fully regulated crypto app, users are automatically given a range of wallets, one for each supported cryptocurrency on the network. This allows users to buy, sell, trade, store and manage many cryptocurrencies from one secure app. Simply head to the Tap website and conveniently download the relevant app from there.

How To Buy Cryptocurrency

Buying cryptocurrency used to be a complicated endeavor however with new products on the market it has become simpler and easier to do. Tap's mobile app is a classic example. Buying crypto Tap has never been so easy all you need to do is to create an account.

You will then be asked to confirm your identity through a process known as KYC (Know Your Customer). This is a common practice required by any entity facilitating the sale of cryptocurrencies. The process is entirely integrated and will require you to submit a picture of an identification document and a selfie of you, easy stuff.

Once your account is created, you can then deposit funds. This can be done through debit card or bank transfer. Simply load your fiat wallet with the currency of your choice for free, using a debit card or a bank transfer as a payment method of your choice.

With a loaded fiat wallet, you are then able to go shopping! Under Assets on the home screen, select Crypto, then find the cryptocurrency you would like to purchase. Simply click Options, then Buy once you are on the cryptocurrency you would like to purchase. The process is as simple and easy as it sounds.

After buying crypto, the funds will be deposited into your wallet in a fraction of a second once the transaction has been confirmed. Not too complicated, was it? Submerge yourself into the world of crypto today with the Tap app, head to your Google Play or Apple app stores to get started straight away.

In this article, we’re guiding you through the intricacies of the e-money licence: what it means, who needs one and of course, how it affects you, the consumer. This new wave of regulation has been put into place to not only safeguard the consumer but also to put measures in place to identify and stop fraudulent activity.

What Is Electronic Money (E-money)?

Before we dive into the licencing requirements, let us first take a look at what electronic money is defined as. Essentially, e-money is a digital version of cash. It maintains a monetary value that can be used to make payments and various transactions, typically over the internet, or through a phone or card.

E-money products are either software-based or hardware-based and are responsible for electronically storing the monetary value. Software-based products are used on computers and tablets and require an internet connection (like PayPal for example) while hardware-based products encompass cards that have a chip card and do not require an online connection (for example, Square).

What Is An E-money Licence?

The e-money licence is a regulatory licence that authorises an electronic money institution (EMI) to conduct business. EMIs represent the digitisation of financial services and are authorized to issue money as well as provide payment cards, e-wallets, and IBAN accounts. While banks may provide a similar service, they require an alternative licence as they are able to provide a greater range of services.

In a nutshell, an EMI is considered as such if it engages in the issuing and redeeming of electronic money (e-money), cash withdrawal, deposit and payment services, remittance services, debit or credit transfers, payment initiation and execution services, and account information services. They may conduct these services only if they have the proper licensing.

How Does It Protect The Consumer?

While regulation and consumer protection are the driving force behind e-money licences, there are also several other reasons as to why the regulatory framework has been put into place. The licence is designed to provide businesses with the opportunity to gain access to the e-money market, to facilitate innovation in secure e-money services, and to build healthy competition in a secure market.

E-money licences are obtained to safeguard a consumer’s funds should the EMI become insolvent. This operates in an entirely different manner to a banking licence. Under the proper regulation, EMI’s can choose to do either of the following options to safeguard consumer funds (funds provided by customers in exchange for the issuance of e-money):

- deposit the funds into a segregated client’s funds account with an authorised credit institution, or

- acquire insurance that will cover the risks associated with the client’s funds.

This ensures that the consumer is always protected against loss of funds, and will be compensated accordingly should the situation present itself. It is imperative that consumers only choose EMIs with the correct e-money licences.

How Much Money Is Protected With The E-Money Licence?

According to the FCA regulations, the EMI is responsible for establishing the appropriate organisational arrangements to ensure that the safeguarded funds are at all times protected.

As mentioned above, this can be done by either storing the deposited customer funds in a separate account (different from the institution’s working capital and other funds) or by ensuring that they are covered by an appropriate insurance policy or comparable guarantee.

While licenced banks work in conjunction with the Financial Services Compensation Scheme (FSCS) and only insure users up to £85,000, EMIs are required to protect 100% of the consumers’ funds.

According to the licence, EMIs are required to safeguard all funds deposited on the platform and not just a portion as per the licence required by the banks.

While EMIs take several other precautions to protect consumer funds, the e-money licence ensures that the most fundamental legal requirements are met, granting the company the right to legally operate.

Cryptocurrencies derive their value from supply and demand, with the buyers and sellers playing an enormous role in the market's liquidity, and ultimately, success. This rings true for stocks, commodities and forex markets too, essentially any asset markets with trading volumes.

Anyone participating in these markets will have been a maker or a taker at some stage, most likely, both. In this article, we're breaking down the concept of makers vs takers, exploring their vital role in the market and large quantities of these result in stronger exchanges.

Liquidity Explained

Before we dive in, let's first cover an important concept: liquidity. Assets can sometimes be described as liquid or illiquid, this simply refers to how easily the asset can sell. Gold is a prime example of a liquid asset as anyone could easily trade it for cash without any hassle, while a glass statue of your neighbour's cat would be an illiquid asset as the chances of anyone wanting to own it are slim (except for the neighbour, maybe).

Building on this, market liquidity indicates how liquid a market is. A liquid market means that the asset is in high demand, traders are actively looking to acquire the asset, while also having a high supply, meaning that traders are actively looking to offload the asset. An illiquid market then means that there is low supply and demand, making it difficult to buy or sell the asset for a fair price.

In a liquid market where there are many traders looking to buy and sell an asset, the sell order (ask price) tends to be in the same region as the buy order (buy price). Typically, the lowest sell order will be the same as the highest buy order, creating a tight buy-ask spread.

Now that we've covered liquidity, it's time for makers vs takers.

What Is The Difference Between Market Makers And Market Takers?

As mentioned above, any successful exchange requires a fair amount of makers and takers. Let's explore the difference between the two below.

Market Makers

Exchanges typically use an order book to conduct trades. The order book will store offers to buy and sell as they come in, and execute the trades when the criteria are met, i.e. someone could create an offer that says when Bitcoin reaches $40,000, buy 4. When the BTC price reaches $40,000, the order book with automatically execute this trade.

In this case, the person creating this buy order is known as a maker. They are essentially "making" the market by announcing their intentions ahead of time via the order book. While many retail investors are makers, the field is typically made up of big traders and high-frequency trading institutions.

A market maker is a liquidity provider.

Market Takers

Market takers are then liquidity "takers", removing liquidity from the market. Takers create market orders that indicate to the exchange that the trader wants to buy or sell at the current market price. The exchange will then automatically execute the trade using a maker's offer.

A taker is a trader filling someone else's order. Market makers create offers for the order book, making it easier for users to buy and sell, while market takers exercise this liquidity by buying the asset.

What Are Maker-Taker Fees?

You might have heard of maker-taker fees before, this makes up a considerable amount of how exchanges generate an income (after all, exchanges are businesses that need to make money). When an exchange matches a maker and a taker, they will take a small fee for the efforts on their part. This fee will differ from exchange to exchange, and will also be dependent on how big of a trade it is.

As makers are providing liquidity to the exchange (an enticing attribute for any trading platform) they will pay lower fees compared to a trader taking away from the platform's liquidity. Always be sure to check the fee structure and pricing on a platform before engaging in any trading activity, these will be outlined in the platform's trading policy.

How Do Trading Companies Make Money?

Cryptocurrency and blockchain technology was designed to provide a decentralized financial system that bypasses government control. However, to alleviate regulatory concerns, exchanges were established to provide a reliable and convenient means of operating within the crypto markets. These exchanges provide a secure way in which users can buy, sell and trade cryptocurrencies, and in return make money through the activities of its customers as it is a business after all.

While maker and taker fees make up a large portion of how a platform generates an income, the business also generates income through deposit and withdrawal fees, commissions made on trades and listing fees. These typically make up the cost of production and running the business.

In Conclusion

Market makers contribute to the market's liquidity by creating orders looking to be filled, while market takers fill these orders. Makers are typically rewarded for bringing liquidity to a platform with low maker fees, while takers pay higher fees when they make use of this liquidity, easily buying and selling the asset.

Level up your crypto trading with the right tools. Whether you’re brand new to the industry or a seasoned trader, you can never know enough about the industry, the crypto market or what to expect. Crypto trading is a unique and exciting endeavour, and we’re here to make sure you always have your best foot forward.

It’s not always easy to know where to start

Being a beginner at anything in life is hard, and the crypto industry is no exception. It’s common for newbies to be inundated with content and it’s not easy to know what’s worth your attention and time and what isn’t. On top of that, there is also a lot of misinformation out there, with publications or platforms selling services through content directed to that purpose.

Through our Crypto Basics platform, you can learn the fundamentals of the crypto industry. We’ve curated the topics to ensure that you get a broad understanding while still covering topics that are relevant to your learning curve. Entering the crypto market should be fun and stimulating, so we’ve geared our Crypto Basics platform as well as all our content toward that.

Start Learning Right From Our Crypto Basics Learning Portal

Tap crypto basics 101

In our online learning portal, you will have access to plenty of blogs to assist you in gathering all the knowledge you need to know. We’ll start you off with an introduction to the three top cryptocurrencies, explaining what they are, how they came about, and what functions they offer. After the crash course on Bitcoin, Ethereum and Litecoin you’ll have a good idea of what cryptocurrencies are and how they differentiate themselves. You’ll then be introduced to altcoins, a common term used to refer to any cryptocurrency that isn’t Bitcoin.

From there you can gain an understanding of how cryptocurrency transactions work and what goes on behind the scenes to facilitate these digital transactions. We’ll also give you an introduction to how mining works, a term used to describe the process of new coins entering the system (also used to verify and process transactions).

How Do Bitcoin And Altcoin Transactions Work?

What is Bitcoin Mining and How Does it Work?

How Long Will It Take To Mine All The Bitcoins?

In the explanation on Ethereum or across the industry in general, you will likely come across terms like “smart contracts”, “dapps” and “DeFi”. We’ve got you covered with simple explanations on each of these, delivering a comprehensive overview to help you navigate news pieces or forum discussions with confidence.

From there you can explore industry terms like “what is KYC?” as well as take a look at things like market caps and bull versus bear markets. These terms you will hear a lot of in the industry, and these blogs provide you with the terminology to breeze through.

What is A Bull Or Bear Market?

Tap into your own potential

This is a good introduction to our Learning Portal, however, there is so much more on offer. As we constantly update the portal be sure to check in when you’re ready for your next dose of crypto knowledge, or better yet bookmark the link so that you constantly are in the know. We regularly update the section with new and insightful material, so be sure to check-in. You’re never too experienced to upgrade your crypto knowledge, so use Tap as your tool kit to further expand your crypto knowledge and navigate the markets with ease.