November 2025 could be a turning point for crypto. From ETFs to major network upgrades, here are six catalysts that could shape the market.

Keep reading

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

1. Seasonality & Historical Momentum Could Kick In

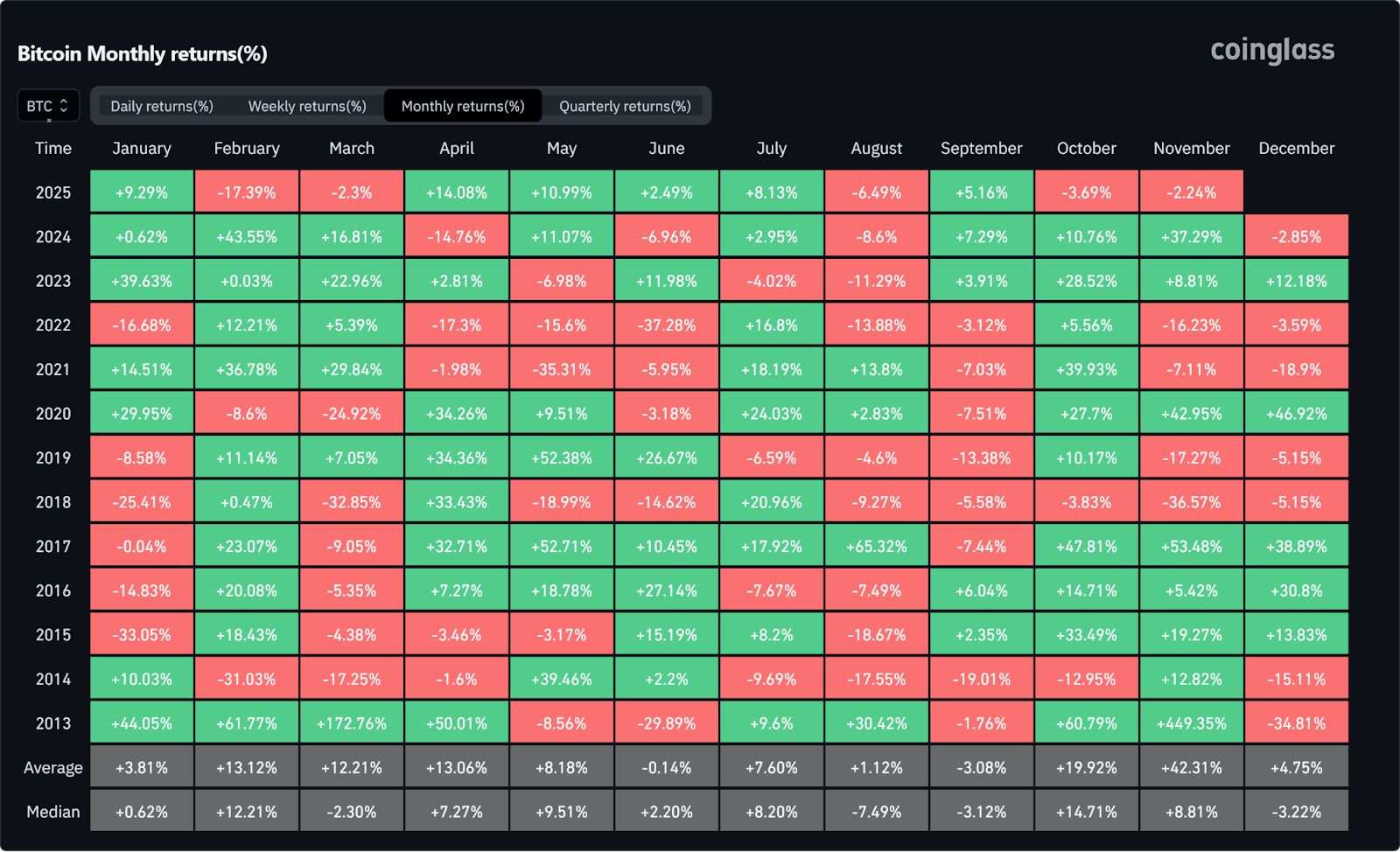

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

4. Altcoins at an Inflection Point

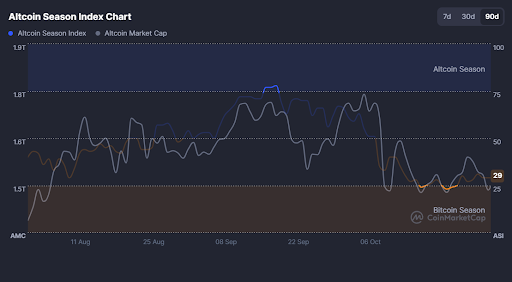

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

NEWS AND UPDATES

LATEST ARTICLE

The stock market is a collective term for stock exchanges around the world. On these exchanges buyers and sellers can trade shares in publicly traded companies, known as stock. Similar to an auction, buyers can name the highest price they're willing to pay, known as the "bid", and sellers can name the lowest price they're willing to accept, known as the "ask". The trade will typically execute somewhere between these two figures.

The stock market exists across the world with stock exchanges situated in New York and Hong Kong, connecting traders through a mutual set of guidelines. Learn more about the role of stockbrokers, portfolio managers, and investors as we take a deep dive into the entire stock market.

What is the stock market?

The stock market can also be referred to as the equities market or share market. As mentioned above, the stock market encompases buyers and sellers of stocks of publically traded companies. Similar to a farmer's market, the stock market forms a base where buyers and sellers can exchange things. Unlike farmer's markets, however, stock markets are heavily regulated and more complex, with prices known to change quickly.

The primary functions that the stock market serves

- The buying of stocks: Both retail investors and institutional investors can purchase shares of companies.

- The selling of stocks: every trade needs a buyer and seller.

- The issuance of stocks: A company raising money may do so by selling a portion of ownership via an initial public offering (IPO). If the company is already public, it can raise money through a secondary public offering. After the individual stocks are issued in either case, it can be bought by or sold to members of the general public.

Trades are typically placed by stockbrokers on behalf of individual investors or portfolio managers.

The primary market is when companies list their shares, while the secondary market is where investors trade these stocks. The secondary market is essentially the stock exchange where stock trading takes place.

It's not just stocks that can be bought and sold on the stock market. Other types of securities, such as exchange-traded funds (ETFs) or REITs, are also traded on the stock market (with some discrepancies in how they're priced and traded).

Around the world, there are 60 major stock exchanges, each varying in size and trading volume. In the United States, for instance, there are 13 different exchanges that make up the stock market, the most popular ones being the New York Stock Exchange and Nasdaq.

How does the stock market work?

The primary function of the stock market is to bring together buyers and sellers so they can trade stocks and other financial instruments. The price is set much like an auction would be.

Bid price

- Buyers determine the bid price. Stockbrokers can bid on the price they're willing to buy a stock for, and the highest price becomes known as the "Best Bid."

Ask price

- Sellers determine the ask price. When an owner of the stock or their stockbroker wants to sell, they place what's called an ask, which is the price that they would like to sell a stock for. The lowest prices become known as the "Best Ask."

The negotiation between the Best Bid and Best Ask is called the “Spread.” The two sides agree to meet somewhere in the middle, and the person who executes the trade gets paid by taking the difference.

As you follow a stock, you’ll notice the share price moves. The stock's price is always changing depending on how many people are buying or selling it and the number of trades that it goes through. As economic, political, and news stories specific to a company affect the movement of markets in general, that company's stock prices can change too as a result. This is known as stock market volatility.

Is trading on stock exchanges risky?

As with any investment pursuit, trading the stock market for both short-term and long-term periods carries a level of risk. Being prepared by knowing that stocks can increase or decrease dramatically at a moment's notice will allow you to prepare for such events in your trading strategy.

In some cases, stock prices can decrease to zero, losing all their value and resulting in a total loss of capital for the investor. While this is an extreme case, making the necessary precautions in one's trading strategy will go a long way.

Is the stock market and stock exchange regulated?

Yes, as the stock market handles trillions of dollars, government organizations around the world have been called in to regulate these markets. In the U.S. for example the SEC (US Securities and Exchange Commission) has been granted the authority by Congress to regulate the stock market because they handle such a large amount of money. Other countries have similar organizations that regulate and enforce different laws.

Regulators are responsible for:

- Safeguarding the investments of the general public

- Promoting a sense of equality and fairness

- Keeping markets running smoothly

Who are the main players in the stock market?

Below are the main players contributing to how the stock market works:

- Retail investors

Buy or sell individual stocks through a brokerage account. When you place an order, it’s sent to exchanges where the trades are executed. - Stockbrokers

“Registered representatives” who have completed professional training and passed a licensing exam and are allowed to buy and sell securities on behalf of investors. Stockbrokers work for brokerages, which can either make their money through markups/markdowns or commissions on trades (known as principals or agents respectively). Fees are often charged by the brokerage to customers that use them to place orders and execute stock trades. - Portfolio managers

Portfolio managers are stockbrokers on a grander scale as they buy and sell stocks through large orders as they manage larger stock portfolios. These might include mutual funds, retirement funds, and pension funds, which contain a bundle of securities (stocks, bonds, etc) that are handled by the portfolio manager. - Investment bankers

Help companies list their shares publicly on exchanges.

Who makes up the stock market ecosystem?

To better understand how the stock market works you will need to understand the varying components that make up the primary market. Investors buying and selling stock make up the biggest component of the stock market, however, there are plenty of middlemen acting between those buyers and sellers earning money by providing services to them. Below are some examples:

- The stock exchanges charge a small transaction fee and listing fee to the companies that offer their shares on the exchange.

- Agents are the middlemen connecting the buyers with sellers. For connecting each side of the transaction they take a commission.

- Principals are broker-dealer firms that manage a portfolio of shares they're willing to sell. Broker-dealers usually earn a profit by adding a markup to stocks they sell and charge investors less than the full value when buying stock. For example, have you ever noticed how much more car dealerships will sell cars for versus what they offered to pay you for your old one? Brokerages do something similar with stocks.

- Retail investors are people who invest for themselves, and not as part of their job, are retail investors. These individuals manage their own stocks (or other assets) through personal accounts with brokerages.

- Custodians. Brokerage firms use custodians to physically hold stocks, which is seen as less of a risk in terms of loss, theft, or damage. For doing so they charge a fee.

What is the history of the stock market?

The original concept of the stock market is the opportunity for a company to divide its ownership, known as equity, and sell it to investors. This practice dates back hundreds of years to the 1600s where European explorers would raise money for their ventures by selling shares in the company.

Investors would then get a cut of the explorer's missions, whether it be bringing back foreign spices or animal hides. The Dutch East India Company was a pioneer in this movement, selling shares in exchange for future profits on Amsterdam's stock exchange.

A century later and the first modern stock exchange was launched in London. Due to a high amount of fraud and minimal information on the company available to the public, the London Stock Exchange was created in 1773 which provided a consistent and fair platform on which to trade stocks.

Across the pond in 1790 the first stock exchange was formed in Philidelphia, followed shortly after by the New York Stock Exchange. Fast forward to modern days and the NYSE now provides both digital trading and a physical trading floor on Wall Street, the latter of which is a National Historic Landmark.

Nasdaq (National Association of Securities Dealers Automated Quotations) launched in 1971 as the world's first electronic market. The electronic stock exchange is a popular option for tech companies looking to list their shares and a crosstown rival to the NYSE. From a trading perspective, where the shares are listed makes little to no difference to the investor.

In conclusion: what is the stock market?

The stock market is a collective term for stock exchanges around the world that facilitate the trade of stocks and other financial instruments.

The world we are living in is constantly evolving, finding new ways to embrace technology and the impact it can have on our future. From struggling to get a man on the moon to billionaires casually flying up into space, we have come a long way from what was once only dreams.

One thing that has been on peoples' minds for a while is our integration into a more VR-compatible world. If you have seen the movie "Ready Player One" then you know what we are talking about. Although augmented reality and VR is not as inclusive as it could be yet, it offers an escape from our realities via the internet.

Buying a VR headset and visiting Japan would be much cheaper than plane tickets, accommodation, and money for food. This once-off price for VR has provided a new dream for many of us, and there are a few companies taking advantage of this demand in the market.

The Metaverse Explained

Although Metaverse is closely tied to Facebook, now called Meta, the term was first coined in the 1992 novel Snow Crash by author Neal Stephenson. The novel followed a dystopic future where people spend most of their time in a virtual reality metaverse. Why Facebook would base their project on a dystopian novel is a question we can't answer. Facebook isn't even the first company to embrace a "VR universe", we have seen game providers such as Epic Games host VR concerts on their platforms, such as the Travis Scott performance.

We have also seen games like Second Life become increasingly popular as social contact has become limited in past years due to the pandemic, providing a relatively safe virtual world for people to interact. While these platforms have come close, nothing compares to what the Metaverse has in store.

"Meta" relates to the Greek origin for the word beyond, while "Verse" is associated with the word universe, meaning beyond universe. The core concept of this idea is to create a virtual reality world, giving us access to everything in our world and beyond. From buying to selling to gaming, to human interactions, and more. There is no limit to how far the Metaverse can go.

The Metaverse could provide a way for humans to experience more at a reduced price and easier access, whether that be school education or leisure activities. In its basic form, the Metaverse is a way for people to integrate into a virtual world and perform complex interactions.

What To Expect

While Facebook, or Meta, has not definitively laid out their plans for the Metaverse and all the more intricate details, there are some things we can expect. So using some creative freedom, basic expectations, and what has been confirmed, these are 5 things you can expect from the Metaverse:

Virtual reality: The most obvious feature we can expect from the Metaverse is that it will be based in a virtual reality world, or universe, accessible through VR-compatible devices.

Workspaces: Another feature to expect is a workspace, whether it be to motivate people, or board rooms designed for teams to have talks, we are sure the Metaverse is making space for work.

Events: We have already seen other platforms host virtual events, this is surely something we will see popping up in the Metaverse. Expect concerts, conferences, and more.

Games: There has already been some confirmation of VR games entering the Metaverse, we may not be sure what games yet, but it would be a waste not to include a community already interested in VR gaming.

Retail purchasing: The Metaverse is geared up and ready to take on retail, whether that be allowing people to buy things through the Metaverse for delivery, or to use on the Metaverse. We can expect VR clothing and merch to be a big feature.

This is just the basics, we believe, with so much more to still be conceptualized and confirmed. The Metaverse, while exciting, holds more praise in its potential than its progress as of yet. Hopefully we will see more fun additions, maybe some VR Disney Worlds or skiing trips down Mount Everest, who knows?

Things You Might Still Be Wondering About The Metaverse

Now that you know the basics of what a Metaverse is and what to expect from the Facebook Metaverse let delve into some other topics. These are the most frequently asked questions associated with the Metaverse:

Is Metaverse just VR?

Not necessarily, we have seen Metaverse-adjacent projects run their virtual worlds without the use of VR or VR headsets. In short, the Metaverse offered by Facebook is being launched as a Virtual Reality world, but that doesn't mean all will be.

Do you need Occulas for Metaverse?

The device of choice, or choices, has not been announced as of yet. We expect the Facebook Metaverse to offer more than one option point for accessibility.

Is Roblox a Metaverse?

At its core basics, yes, it is a virtual world with a variety of interaction options such as retail, socializing, and gaming.

Who owns the Metaverse?

No one person owns the Metaverse, there are multiple companies working to launch their versions of a Metaverse. There is currently no patent on the term or concept yet, although we may see features patented in the future.

Is Decentraland a Metaverse?

At its core basics, yes, it is a virtual world with a variety of interaction options such as retail, socializing, and gaming.

Why is the Metaverse good?

We have highlighted some points, but let's break them down again. It is generally cheaper for some experiences, it is accessible to the world, it's another way for the world to connect, and it's an advancement of technology. There is more, but these are the main focal points.

In Conclusion

The Metaverse, whether that be Facebooks' version or another, is a very exciting thing. There are so many possibilities, and ways it can better the world. Virtual protests anyone can join, recovery programs or groups, being able to go to your favorite artist's concert without flying thousands of miles, and more.

The possibilities truly are endless, and we are privileged to be able to be a part of the building's progress. A virtual world, or universe, may have some risks associated with it, but we also see plenty of potential for good. The positives and negatives of the Metaverse are going to vary, from platform to platform, depending on what the company has in store.

While the Facebook Metaverse may be the most mainstream at the moment, there are and will be better Metaverses such as the Microsoft one rising soon enough. So stay tuned as the Metaverse is brought to reality.

Tether (USDT) consistently ranks among the top cryptocurrencies by market cap and regularly posts the highest daily trading volume in the entire crypto market. It's become an essential tool for traders worldwide.

While critics point to crypto's volatility as a weakness, stablecoins like Tether offer a different value proposition: the speed and accessibility of digital currency with the stability of the US dollar.

What Is Tether (USDT)?

Tether (USDT) is a widely used stablecoin, a type of cryptocurrency designed to maintain a fixed value by being pegged to a fiat currency, in this case the United States dollar. Unlike Bitcoin, whose price fluctuates based on supply and market demand, USDT is meant to stay close to $1 USD, providing stability in otherwise volatile markets.

Originally launched in 2014 under the name Realcoin, Tether was rebranded and built to act as a bridge between fiat money and digital assets. It enables traders, exchanges, and users to move value quickly, reliably, and with less exposure to cryptocurrency volatility.

Because of its stability and liquidity, USDT is often used as a “parking spot” in crypto trading, when the market is unstable, investors might convert volatile tokens into USDT to preserve value without leaving the crypto ecosystem entirely.

As of 2025, Tether is consistently ranked among the top 3 cryptocurrencies by market capitalization, and its daily trading volume often surpasses that of other major tokens.

In this article, we’ll dig into how USDT works, why people use it, the risks and controversies, and how to buy and use it responsibly.

Who Created Tether?

As mentioned above Tether was initially called Realcoin when it was launched in 2014 and was created by Bitcoin investor Brock Pierce, entrepreneur Reeve Collins and software developer, Craig Sellars. It later changed its name to USTether, eventually settling on USDT.

All three co-founders have profound experience within the crypto industry, each co-founding and actively involved in several cryptocurrency and blockchain projects.

The business has also created a number of other stablecoins solving the volatility problem across numerous markets, notably a Euro-pegged Tether coin (EURT), a Chinese Yuan-pegged Tether coin (CNHT), and a gold-pegged Tether coin (XAUT).

How Does USDT Work?

Reserve Backing & Peg Mechanism

To maintain its peg (i.e. USDT = 1 USD), Tether claims each USDT in circulation is backed by reserves. These reserves include cash, cash equivalents, repos, commercial paper, U.S. Treasury bills, and other short-term assets.

In recent attestations, Tether reports that about 81.5% of its reserves are in cash and U.S. Treasuries, with smaller portions in other assets.

When demand for USDT increases, Tether issues (mints) new tokens; when demand falls, tokens can be destroyed (burned) to reduce supply. This dynamic supply adjustment helps keep the exchange rate close to 1 USD.

Blockchain Infrastructure & Multi-Chain Support

Tether does not have its own dedicated blockchain. Instead, USDT operates as a token on various blockchains, including Ethereum (ERC-20), TRON (TRC-20), Solana, Algorand, EOS, and more. This multi-chain deployment enhances accessibility and interoperability.

Transactions are handled by the underlying networks: you need to send USDT on the same chain type, or bridges/wrapping mechanisms if moving across chains. Mistakes sending USDT on mismatched chains can lead to permanent loss.

Minting, Burning & Peg Maintenance

Tether monitors supply vs demand. If too many redemptions occur, USDT supply contracts; if demand surges, new tokens are minted. The reserve assets are used to maintain liquidity for redemptions and guarantee that each USDT has backing.

To preserve the peg, Tether also relies on arbitrage: if USDT drifts slightly above $1, there’s an incentive to redeem or sell, and if it dips below, it encourages buyers. Combined with market forces and reserve backing, this helps anchor the price.

Why Do People Use USDT?

- Users often convert volatile crypto into USDT during turbulent markets to protect value without exiting the digital asset ecosystem.

- USDT is accepted in a vast array of exchanges and trading pairs, making it a preferred medium of exchange.

- Because it behaves like USD but lives on the blockchain, USDT can move quickly across borders without traditional banking friction.

- Many decentralized finance platforms use USDT as a base asset for lending, yield farming, and stable lending markets.

- In regions with unstable local currencies, USDT often provides a stable alternative for savings, payments, or transfers.

Is USDT Safe? Risks & Concerns

While USDT offers utility, it also attracts scrutiny and criticism.

Centralization & Counterparty Risk

Tether Limited acts as the central issuer. That means users must trust that the company actually holds sufficient reserves and will honor redemptions. This centralized model contrasts with fully decentralized cryptocurrencies.

Transparency & Reserve Audits

Tether publishes regular attestation reports, but has yet to provide a full independent audit by a Big Four firm in many periods.

In 2025, Tether announced it is in talks with a Big Four accounting firm to pursue a full audit.

Historical controversies include a fine by the New York Attorney General in 2021 over misrepresentation about reserve backing.

Regulatory & Legal Uncertainty

Stablecoins face evolving regulatory environments globally. Some jurisdictions may impose stricter rules, reserve requirements, or classification of USDT as a regulated instrument.

Reserve Composition & Liquidity Risk

Though cash and Treasury bills dominate reported reserves, some portion may be in less liquid assets. In times of mass redemptions, liquidity risk may strain backing.

Price Deviations & Peg Risk

While USDT is generally stable, in extreme market stress, the peg might deviate briefly. Arbitrage, reserve liquidity, and market confidence are key to restoring balance.

How to Buy, Sell & Use USDT

Buying USDT

You can acquire USDT on most major cryptocurrency exchanges (e.g. Binance, Coinbase, Kraken). Many platforms allow purchase via fiat currencies (bank transfer, card) or by trading other crypto for USDT.

In the Tap app, you can buy USDT and have it stored in your wallet, making it easier to manage alongside your other assets.

Storing USDT

Store USDT in wallets that support the relevant chain (ERC-20, TRC-20, etc.). Hardware wallets like Ledger or Trezor support ERC-20 USDT (via Ethereum).

Converting USDT to Fiat

On many exchanges, you can sell USDT for fiat (USD, GBP, EUR) and withdraw to your bank.

Using USDT for Payments or Transfers

Some platforms accept USDT as payment. You can also transfer USDT peer-to-peer across wallets quickly and globally, with network transaction fees (gas) depending on the chain used.

USDT Reserve Composition & Transparency

Tether provides quarterly transparency reports detailing reserve breakdowns, but falls short of full independent audits historically.

As of recent attestations, ~81.5% of reserves are held in cash & U.S. Treasuries, while smaller portions are in other assets.

Tether held over $127 billion in U.S. Treasuries as of Q2 2025.

Reserve composition evolves over time; Tether has reduced reliance on commercial paper and shifted toward safer instruments.

While attestations improve transparency, critics assert a full, external audit would bolster confidence.

USDT vs Other Stablecoins

While USDT remains dominant, several alternatives exist:

- USDC: Known for stricter auditing and regulatory compliance

- DAI: Decentralized, over-collateralized stablecoin

USDT held around 62–63% of the stablecoin market share as of 2025. It maintains dominance due to liquidity, widespread adoption, and support across exchanges and DeFi. However, users might opt for alternatives for perceived transparency or regulatory comfort.

Investment Considerations

USDT is not designed as a growth asset; its value is meant to remain stable. Its role is more of a utility token: liquidity provider, trading medium, and stability anchor.

That said, you can earn yield on USDT via lending platforms, DeFi protocols, or savings accounts, though returns may be modest and come with risk.

Consider that holding large amounts of USDT long-term yields little upside, and inflation or counterparty risk may erode value.

Always balance USDT exposure within a diversified strategy, rather than viewing it as an investment vehicle.

Conclusion

Tether (USDT) plays a critical role as the most widely used stablecoin in crypto, offering a digital dollar alternative that combines stability with blockchain utility. While its popularity and liquidity make it indispensable in trading and DeFi, it operates under risks tied to transparency, centralization, and regulatory shifts.

If using USDT, treat it as a tool for stability and liquidity, not speculative growth. Used wisely, USDT helps you move between crypto and fiat more fluidly, manage volatility, and access global financial systems with fewer intermediaries.

Stocks are essentially shares in a company that the company sells to shareholders in order to raise money. Shareholders are then entitled to dividends if the company succeeds, and might also receive voting rights when the company makes big decisions (depending on the company).

What are stocks?

Stocks play an important role in the global economy, assisting both companies (in raising capital) and individuals (in potentially earning returns). Traders can buy and sell stocks through stock trades facilitated by various stock exchanges. The stock price is determined by supply and demand, largely influenced by the company's success and media representation.

These "units of ownership" are sold through exchanges, like Nasdaq or the London Stock Exchange, under the guidance of regulatory bodies, such as the Securities and Exchange Commission (SEC) in the United States. These regulatory bodies set specific regulations on how companies can distribute and manage their stocks.

What are the different types of stocks?

There are two types of stocks, common stocks and preferred stocks, as outlined below.

Common Stock

Shareholders of common stock typically have voting rights, where each shareholder has one vote per share. This might grant them access to attending annual general meetings and being able to vote on corporate issues like electing people to the board, stock splits, or general company strategy.

Preferred Stock

For investors more interested in stability and receiving regular payments rather than voting on corporate issues, preferred stocks are often the security of choice. Preferred stock are shares that provide dividends but without the voting rights. Like bonds, there are a number of features that make them attractive investments. For example, many companies include clauses allowing them to repurchase shares at an agreed-upon price.

Stock vs bond

Although both stocks and bonds signify an investment, they vary in how they operate. With bonds, you're essentially lending money to the government or a company and collecting interest as a return while with stocks you're buying part-ownership of a company. Another key difference is that bondholders usually have more protection than stockholders do.

In contrast to stocks, bonds are not normally traded on an exchange, but rather over the counter (the investor has to deal straight with the issuing company, government, or other entity).

Stocks vs futures and options

Futures and Options contrast stocks in that they are derivatives; their value is reliant on other assets like commodities, shares, currencies, and so on. They are contracts established off the volatility of underlying assets instead of ownership of the asset itself.

Stocks vs cryptocurrencies

While stocks provide a unit of ownership in a company, cryptocurrencies are digital assets that operate on their own network. Cryptocurrencies are decentralised, meaning that no one entity is in charge, while stocks are shares in companies that are heavily centralised and held accountable for their price movements. Both the stock price and the price of cryptocurrencies are determined by supply and demand.

Another key difference is that stocks are regulated while, at present, cryptocurrencies are not.

Where did stock trading originate?

The first recorded instance of stock-like instruments being used was by the Romans as a way to involve their citizens in public works. Businesses contracted by the state would sell an instrument similar to a share to raise money for different ventures. This method was called 'lease holding.'

The 1600s gave rise to the East India Company (EIC), which is considered by many the first joint-stock company in history. The EIC increased its notoriety by trading various commodities in the Indian Ocean region. Today, we see the limited liability company (LLC) as a watered-down version of the joint-stock company.

How does the stock market work?

The 'stock market’ is an umbrella term that refers to the various exchanges where stocks in public companies are bought, sold, and traded.

The stock market is composed of similar yet different investment opportunities that allow investors to buy and sell stocks, these are called "stock exchanges." The best-known exchanges in the United States are the New York Stock Exchange (NYSE), Nasdaq, Better Alternative Trading System (BATS), and the Chicago Board Options Exchange (CBOE).

Together, these organisations form what we call the U.S. stock market. Other financial instruments like commodities, bonds, derivatives, and currencies are also traded on the stock market.

An example: the New York Stock Exchange

The New York Stock Exchange (NYSE) is the largest equity exchange in the world, and it has a long and rich history. Established in 1792, it was originally known as the "Buttonwood Agreement" between 24 stockbrokers who gathered at 68 Wall Street to sign an agreement that called for the trading of securities in an organised manner.

Since then, the NYSE has become a global leader in financial markets, with more than 2,400 companies listed and nearly $26.2 trillion in market capitalization. The exchange has an average daily trade volume of $123 billion.

Investing in common stock or preferred stock on the NYSE can be done through a broker or online stock trading platform. When trading on the NYSE, investors have access to a wide range of products and services, including stocks, bonds, mutual funds and ETFs (exchange-traded funds).

Investors can also take advantage of the numerous benefits that come with trading on the NYSE, such as access to real-time information and the ability to buy and sell quickly. The trading platform is regulated by the U.S. Securities and Exchange Commission (SEC).

How to navigate stock market volatility

Stock market volatility, characterised by rapid and unpredictable changes in stock prices, is influenced by economic indicators, geopolitical events, and investor sentiment. To manage this volatility, investors can diversify their portfolios, set clear investment goals, and maintain a long-term perspective.

Regular portfolio reviews and seeking guidance from financial advisors can also help when it comes to making informed decisions during volatile periods. Investors who stay informed about market trends and use strategic approaches can navigate market fluctuations more effectively, which better positions them for long-term success in stock investing.

The importance of diversification when investing

Diversification is key when investing, and the stock market is no exception. The "don't put all your eggs in one basket" approach offers benefits like risk reduction and the potential for higher returns. Strategies for diversification include investing across different sectors, industries, and asset classes.

By spreading investments, investors can manage risk effectively, ensuring their portfolio isn't overly exposed to any single asset or market sector. This helps cushion against market downturns and enhances the overall stability of the investment portfolio.

Terminology associated with the stock market

- Broker: A broker is someone who buys and sells assets on behalf of another person, charging a commission for their services.

- Stockholders equity: The value of a company's stock can be better understood by this metric, which is the company's assets remaining after all bills are covered (liabilities).

- Stock splits: Conducting a stock split is one way that companies make their stocks more accessible to investors. Although it won't change the market capitalisation or value of shares, it will increase the number available.

- Short selling: If an investor wants to bet on a stock's price going down, they can take a "short" position. To do this, they must borrow the stock from either a broker or a financial institution.

- Blue-chip stocks: Companies that are large and have a lot of capital typically fall into the blue-chip category. They usually trade on famous stock exchanges, like the NYSE or Nasdaq.

- Pink sheet stocks: 'Penny' or 'pink-sheet' stocks are those that trade below the $5 threshold and are typically OTC (over the counter). These can be high risk.

- Buying on margin: Buying on margin is using borrowed money to buy stocks, bonds, or other investments in the hopes of making big returns and paying off the loan.

- Market order: When placing an order for a trade, the investor needs to pick from several types of orders. A market order is executed at whatever the next price is, which can be risky if there's a big gap between what buyers and sellers are offering.

- Limit order: A limit order is an order to buy or sell a security at a specified price, with a maximum amount decided on before executing the trade.

- Stop order: A stop order, also referred to as a stop-loss order, is an order placed with a broker to buy or sell once the stock reaches a predetermined price.

In conclusion

Shares, or stock, are units of fractional ownership in a company that investors buy to gain capital appreciation and tap into a company's earnings if the company's stock pays dividends. Companies, through listing their stock on an exchange, can raise capital to further develop the business.

Stock is traded on an exchange, and the stock prices are determined by supply and demand.

Used across all markets, the spread is the difference between the buy (offer) and sell (bid) prices of an asset. Spreads provide an additional opportunity to traders to make money through buying and selling assets.

The spread of an asset will depend on the current demand or an asset and the market’s volatility and is presented in either a percentage or value form. Assets with markets displaying higher levels of demand will typically have smaller spreads and usually higher price points.

As an example, when you look at an order book for Bitcoin you will usually see prices reflected in green and red reflecting the offer prices and bid prices. The spread will then be indicated above the most recent trades. As another example, consider foreign exchange counters where the buy and sell prices are different, this difference is known as the spread. Market makers use spreads to generate money from transactions completed at market prices.

Let's put this in context: George buys 100 shares for a £2 ask price in “ABC” a publicly listed company. George pays £200 in return for 100 shares. If he decides to sell the shares back at the same price he bought them for, he would sell the 100 shares for the bid price at £1.95 and would receive £1.95 each instead of £2. This would mean he gets a return of £195 and loses £5, which would be paid to the market maker.

Sitting among the 30 biggest cryptocurrencies by market cap, Stellar is focused on bridging the gap between the business of blockchain and the traditional financial institutions. The platform provides a means for users to send assets and money through the blockchain, utilising a decentralised network of authenticators.

Redefining the financial landscape, Steller presents a digital transformation on the traditional services users have become accustomed to. Merging innovation with a practical application, the network is able to help users around the world, as well as financial industries, achieve a more streamlined service. Let's explore what Stellar is.

What is Stellar (XLM)?

Before we dive into the "what", let's first stipulate that one stellar is known as a lumen and uses the ticker XLM. Stellar launched in July 2014 and soon afterwards changed its strategy to be more focused on integrating blockchain technology into financial institutions.

The concept behind Stellar is to provide a space in which users can transfer everything from traditional crypto and fiat currencies to tokens representing new and existing assets, increasing their transaction performance by using lumens.

Similar to the Ripple XRP network, Stellar is designed to cater to both payment providers and financial institutions, building a bridge between the blockchain and traditional financial sector. Developing on the Ripple concept, Stellar has also positioned itself as an exchange as its ledger has an inbuilt order book that keeps track of all the assets on the network.

Who Created Stellar?

The founders of Stellar are Jed McCaleb and Joyce Kim, both previously employees at Ripple. McCaleb, who founded and was acting CTO of Ripple, and lawyer Joyce Kim, decided to create Stellar after they left the Ripple team in 2013 following a disagreement on the direction that Ripple was taking. McCaleb is also credited with creating the first successful Bitcoin exchange, Mt Gox.

McCaleb described Stellar's aim as giving people a means of moving their fiat into crypto and more seamlessly conducting international payments. The network provides cross border transactions with low transaction fees and fast executions. With leading technology and innovative problem solving, the network has made a healthy impression on both institutions and investors alike.

How Does Stellar Work?

Stellar is a hard fork off of the Ripple network with several similarities in design and functionality, however, the platform set itself apart by building in several key features. The platform is secured through the Stellar Consensus Protocol which revolves around these core business concepts: decentralised control, flexible trust, low latency, and asymptotic security.

The biggest upgrade launch came in 2015 when the platform replaced its consensus mechanism with a concept called federated Byzantine agreement. This required nodes to vote on transactions until quorums are reached. Anyone is able to join the consensus, and there are measures in place to inhibit bad actors operating with ill intent on the network.

The software behind the platform is called Stellar Core and can be altered to adhere to the needs of the operation using it. The nodes making up the network can be created to function as either Watchers, Archivers, Basic Validators or Full Validators. For example, watchers can only submit transactions while Full Validators can vote on which transactions are valid and maintain a ledger of all node activity.

Another element to the network is the Stellar Anchors. These gateways are responsible for accepting deposits of currencies and assets and issuing depictions of these on Stellar.

What Is XLM?

Known as lumens, XLM is the native cryptocurrency to the Stellar platform. XLM acts as an intermediary currency for transactions taking place on the network. With cost-effective experience priorities, every transaction on the Stellar network costs 0.00001 XLM, a fraction of a dollar (at the time of writing).

When the platform launched in 2014, 100 billion lumens were minted, programmed to increase by 1% annually until the total supply reached 105 billion. Five years later the Stellar uses voted to end this process.

That same year, in 2019, the Stellar Development Foundation (a non-profit organisation) reduced its share of XLM in order to regulate the Stellar economy. This brought the total supply down to 50 billion. At the time of writing, roughly 49% of this total supply is in circulation.