November 2025 could be a turning point for crypto. From ETFs to major network upgrades, here are six catalysts that could shape the market.

Keep reading

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

1. Seasonality & Historical Momentum Could Kick In

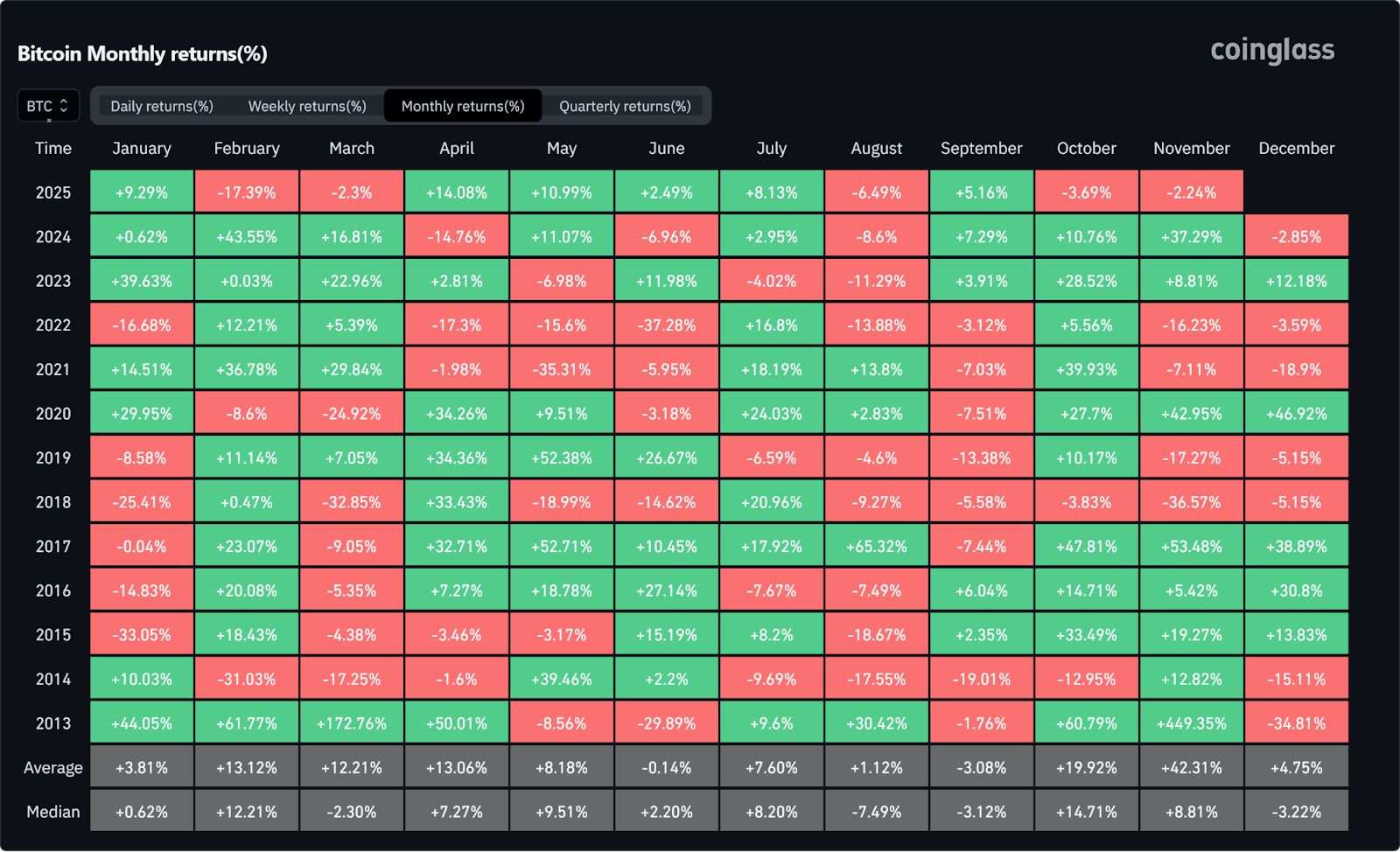

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

4. Altcoins at an Inflection Point

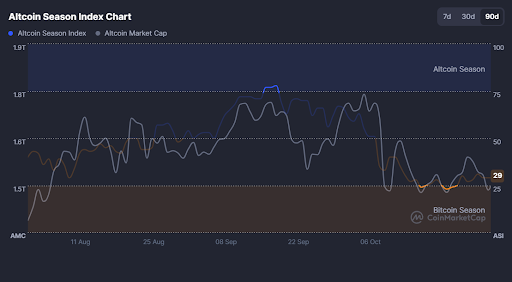

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

NEWS AND UPDATES

LATEST ARTICLE

ISO/IEC 27001

TAP manages confidential information on a daily basis and recognizes the importance of protecting this information from the risk of data leakage, loss or theft. Thus, it has adequately implemented the leading international and certifiable Standard for information security managementISO/IEC 27001 (IT Information Management System).

ISO/IEC 27001, sets out the requirements for defining, implementing, monitoring and improving an information security management system (ISMS) and it involves people, processes and IT systems implementing a risk management process. It offers a systematic and well-structured approach that protects the confidentiality of TAP’s stored information, ensures the integrity of the company data, and improves the availability of its IT systems.

Tap’s ISO/IEC 270001 certificate of implementation has international readability and validity and ensures the verification of compliance with relevant laws and regulations.

At European level, the GDPR (the General Data Protection Regulation 2016/679 on data protection and privacy in the European Union and the European Economic Area), encourages the use of certification systems such as ISO/IEC 27001, as this standard describes the requirements that an organization must meet in order to manage its information security comprehensively and effectively. By adopting ISO/IEC 27001, Tap can demonstrate that actively manages its data security in accordance with international best practices.

100m insurance Bitgo

Tap’s partnership with BitGo, a top qualified digital assets custodian, ensures the highest-level of security for Tap’s customers.

Tap’s first line of defense against theft, loss or damage of private keys includes software, hardware, physical security measures and top quality Know Your Customer (KYC) and Anti-Money Laundering (AML) policies and procedures. By carrying a $100 million coverage insurance as an additional layer of protection from Bit Go, Tap integrates a significant hedge against loss.

Licensed & Regulated

Tap is a legitimate Distributed Ledger Technology (DLT) provider as it is fully authorized by the Gibraltar Financial Services Commission (GFSC), with license number 25532.

This authorization ensures that Tap meets all the required standards to provide efficiently and securely its services and has proper regard to the DLT associated risks in order to protect its customers.

In general, Tap is fully complied with all applicable regulatory, legal and contractual rules and the company’s policies and procedures are frequently reviewed and updated in order to align with the regulative framework. Tap checks on a daily for compliance breaches, ensures that its staff is properly familiar with the KYC and AML/CTF global standards and guarantees the effectiveness and adequacy of its procedures, internal controls and systems.

(In addition, TAP’s provided prepaid card is issued by Transact Payments Limited, which is regulated by the Financial Services Commission Gibraltar, under the Financial Services (Banking)Act 1992.)

When faced with something new or unfamiliar, especially when dealing with money, people often tend to automatically put it into a box. Unfortunately, Bitcoin is no exception. Since its rise in value since its initial launch in 2009, many have been skeptical of how and why it could do so. In this informative article, we explore the common misconception that Bitcoin is a Ponzi Scheme.

What Is A Ponzi Scheme?

First, let's take a look at what a Ponzi Scheme actually is. Ponzi Schemes are fraudulent investment scams which promise high rates of return with minimal risk. This is orchestrated by a "portfolio manager" taking an investment (payment) from a new recruit and using those funds to pay off earlier investors, taking a portion of the funds for themselves.

The new recruit will only be paid once they have recruited more new people, whose funds will be used to pay off their investment. As long as new people are entering the system, the earlier investors are seemingly making profits. This all falls apart when the pool of potential investors becomes saturated and no new investors are entering the system.

The business concept was first mentioned in literature in the 1800s but was officially coined in the 1920s after a person by the name of Charles Ponzi. Ponzi schemes pose as financial services and are illegal in the UK and most other countries and are punishable in the same light as anti-money laundering.

Why Bitcoin Is Not A Ponzi Scheme

As Bitcoin is an entirely decentralised asset and operates using the transparency of blockchain technology, Bitcoin cannot be a Ponzi Scheme. Due to the nature of blockchain, anyone at any time can verify all transactions made on the Bitcoin network, dissimilar to a Ponzi Scheme where "investments" are shrouded in secrecy.

Ponzi Schemes need to obfuscate transactions from both investors and regulators in order for the scam to work, which is the exact opposite of how blockchain functions. These issues alone prove that Bitcoin cannot be a Ponzi Scheme.

Instead, Bitcoin is open to anyone and following one purchase the investor can own and hold the original cryptocurrency. As a digital currency, Bitcoin is stored in digital wallets which are accessible to anyone, without the need for lengthy paperwork. Most exchanges offer users access to a Bitcoin wallet, which can easily be accessed directly on the platform.

Bitcoin Volatility Confirms It Is Not A Ponzi Scheme

Not often seen in a positive light, Bitcoin's market volatility puts the final nail in the coffin when considering whether Bitcoin is a Ponzi Scheme. See, in Ponzi Schemes investors receive suspiciously consistent returns, which is just not plausible when it comes to trading Bitcoin.

Day traders have been known to witness high price swings over short periods of time, sometimes losing or accumulating a large amount in mere hours. This is entirely unrealistic when it comes to the functioning of a Ponzi Scheme.

Instead, Bitcoin's price history has shown that substantial growth is generally witnessed in four year periods. This is in line with the Bitcoin halving event, an automated change to the miner's rewards which manages the number of new coins entering circulation. After every 210,000 blocks are added to the network's blockchain, the halving event is initiated, and the rewards are automatically halved. History has shown that roughly 12 - 18 months later Bitcoin has seen substantial gains. The next halving to take place will be in 2024.

How To Avoid Ponzi Schemes In The Crypto Realm

While Bitcoin and other cryptocurrencies are not Ponzi Schemes themselves, that doesn't mean that Ponzi Schemes cannot use Bitcoin to lure in potential investors. Beware of any investment "firms" looking to invest in crypto for you, particularly if they're claiming to provide inflated rates of returns.

Instead, invest in crypto yourself through a reputable platform like Tap and take matters into your own hands. Buying cryptocurrency is simple, you can do so with a credit card or bank transfer, and then the funds are stored in the digital wallets allocated to you specifically. From the mobile app you have full control over your funds, able to sell or buy at a moment's notice. The platform also utilises integrated technology which scans multiple exchanges and order books around the world to find you the best price in real time.

Stay clear of Ponzi Schemes and other investment scams, and utilise the financially-inclusive world of crypto investments yourself.

USD Coin is a prominent stablecoin in the cryptocurrency market. Providing a plethora of use cases to both crypto and traditional investors, financial services and traders, USD Coin sits among the top 10 biggest cryptocurrencies by market capitalisation.

In this article, we explore this celebrated stablecoin and all it has to offer in terms of being a traditional investment opportunity, savings relief and digital value settlement service.

USD Coin is relatively new to the market, launching in September 2018. The stablecoin is pegged to the US dollar, meaning that its value will always reflect the price of the dollar on a 1:1 ratio.

This is established by keeping an equivalent amount of the circulating supply in a reserve account, i.e. for every 1 USDC in circulation, $1 needs to be held in reserve. The reserve is a mixture of cash and short-term U.S. Treasury bonds.

What Is The Point Of The USD Coin?

Built on top of the Ethereum network, USDC is a tokenised version of the US dollar that can operate over the internet and public blockchains. It is designed to provide a stable digital currency in an industry prone to volatility.

Setting itself apart in an increasingly saturated stablecoin market, USD Coin has received wide interest due to it providing a strong layer of transparency. The platform maintains strict protocols to ensure that the reserves are always at the correct levels, ensuring holders that they can withdraw 1 USDC for $1 at any given time, by way of enlisting a major accounting firm.

All USD holdings are required to be reported regularly by USDC issuers, which are in turn published by Grant Thornton LLP (as witnessed in the news). Unlike Bitcoin, while the company uses the decentralized network of Ethereum to function, it has a centralized agency controlling it.

Who Created USD Coin?

The coin was created by the Centre Consortium, a foundation consisting of the peer-to-peer payment service company, Circle and cryptocurrency exchange, Coinbase. Circle and Coinbase were the first commercial industry users of the stablecoin.

In 2020, Circle and Coinbase announced an upgrade to the USDC protocol and smart contracts. These upgrades were implemented to increase the cryptocurrency's usability for everyday payments, commerce and peer-to-peer transactions.

Both companies are well-funded and have achieved regulatory compliance, confirming the cryptocurrency's stability and international transparency appeal.

How Does USD Coin Work?

USD Coins are created through a process of minting. Users send USD to the USDC issuer's bank account, which then uses the USDC smart contract to create the equivalent amount of USDC. The digital currencies are then delivered to the user, with the fiat payment held in reserve.

Should the user wish to liquidate their USDC, they can send a request to the USDC issuer who then sends a request to the USDC smart contract to take a certain amount of USDC out of circulation. The issuer then sends the equivalent amount of USD (minus fees) to the user's bank account, taken from the reserve.

USD Coins can be traded through exchanges for other cryptocurrencies, or sent to crypto wallets around the world (provided that they support ERC-20 tokens). The coins are also often used to hedge against cryptocurrencies going through turbulent or crashing market periods.

What Is USDC?

USDC is a fiat-collateralised ERC-20 token hosted on the Ethereum blockchain platform. The stablecoin has an unlimited total supply with currently just under 37 billion USDC in circulation.

The coin provides an easy means of transferring funds internationally at a fraction of the cost and time that sending the traditional fiat would take. It has also proven to be a popular innovation in the DeFi (decentralized finance) space.

How Can I Buy USDC?

If you're looking to add USDC to your crypto portfolio you can do so conveniently through the Tap app. In a recent upgrade, the Tap app has added support for a number of prominent cryptocurrencies, including USDC.

Users can simply exchange one of the supported cryptocurrencies for USDC, or purchase USDC using fiat money. These can then be stored in the unique wallets integrated into your Tap account.

The study of token economics is known as tokenomics. It covers all elements of a cryptocurrency's creation, management, and sometimes removal from a blockchain network. The term "tokenomics" is formed by pairing up the two words "token" and "economics" and is largely used within the crypto ecosystem to project the potential of a cryptocurrency. Tokenomics, simply put, is how token value is determined and what affects its value.

Tokenomics and cryptocurrencies

Tokenomics and cryptocurrencies are closely connected. Tokenomics refers to the set of rules and principles that govern how cryptocurrencies work. It includes important aspects like how many tokens exist, how they are distributed, and what they can be used for. These rules are crucial for designing and managing cryptocurrencies effectively.

Tokenomics plays a significant role in determining the value of cryptocurrencies. It influences how people perceive and evaluate a cryptocurrency's worth. Factors such as token scarcity (limited supply), the usefulness of tokens in various applications, and the level of demand for them can impact the price and acceptance of a cryptocurrency.

Well-designed tokenomics can foster trust and adoption, and increase the overall value of a digital currency. Conversely, poorly designed tokenomics can hinder adoption and limit the perceived value of a cryptocurrency when traded for fiat currencies or other cryptocurrencies. Therefore, creating a solid and thoughtful tokenomics model is essential for the success and widespread acceptance of cryptocurrencies.

An example of tokenomics: Bitcoin

Bitcoin operates on a specific set of tokenomics. It has a maximum supply of 21 million coins that will ever enter circulation, ensuring scarcity and value appreciation over time. Ethereum, for example, has an unlimited amount of coins. The issuance of new Bitcoins through mining creates incentives for network security while halving events reduces the rate of new supply.

Additionally, Bitcoin's decentralised nature and widespread adoption contribute to its value, with market demand and utility driving its price in the open market. These tokenomics elements make Bitcoin a deflationary digital asset with a unique economic model within the cryptocurrency ecosystem.

Why is tokenomics important?

Tokenomics is especially important in the crypto space due to the lack of regulation. Since there are no laws governing cryptocurrencies, tokenomics provide an opportunity for cryptocurrencies to be evaluated according to their real-life merit, not just how they are traded on exchanges.

What are the benefits of tokenomics?

Tokenomics offers several benefits within the cryptocurrency ecosystem. Firstly, it establishes clear rules and incentives, ensuring a fair and transparent economic system for participants. Tokenomics can incentivise desirable behaviour, such as staking or contributing to network security, promoting overall network growth and sustainability.

Additionally, tokenomics enables the creation of utility and value for tokens, providing variable economic benefits to holders. It allows for the development of decentralised applications (dapps) and the creation of vibrant ecosystems around cryptocurrencies. Similarly, tokenomics facilitates liquidity and trading opportunities, enabling users to buy, sell, and exchange tokens in various markets.

Overall, tokenomics fosters innovation, incentivizes participation, and contributes to the overall growth and success of the cryptocurrency ecosystem.

What are the negatives of tokenomics?

While tokenomics has numerous advantages, there are some downsides to consider. One downside is the potential for market volatility, as token prices can be subject to rapid fluctuations influenced by various factors, including market speculation and investor sentiment.

Additionally, inadequate or poorly designed tokenomics models may result in economic inefficiencies, lack of token utility, or even vulnerability to manipulation. It's important to note that tokenomics may not guarantee long-term value stability, and investors should carefully assess the risks associated with specific tokens and projects before engaging in the cryptocurrency market.

The different tokenomics terms explained

Asset valuation

The process of determining the value of a coin or token. This is especially useful for users who want to purchase new coins or tokens. If they can estimate how much a coin or token will be worth in the future, it might be easier to decide whether or not its price is worth tapping into. Coin and token valuation is also important for traders who have made a significant purchase of a coin or token, and want to assess if its price is likely going up or down.

Inflation

In the context of tokenomics, inflation refers to the increase in the token supply over time, resulting in a decrease in the token's purchasing power and value. Inflation can impact the economic stability of a cryptocurrency ecosystem, and its management is crucial to maintain the desired balance between supply, demand, and overall token value.

Deflation

In tokenomics, deflation refers to the decrease in the token supply, leading to a potential increase in the token's purchasing power and value over time. Deflationary tokenomics can promote scarcity, create incentives for holding tokens, and potentially drive price appreciation within the cryptocurrency ecosystem.

Supply and demand elasticity

If a coin has high supply-and-demand elasticity, its price will likely be more affected by changes in demand relative to its supply. This means that if demand for a particular coin rises, the coin will experience more positive price action ($$) than if demand for the same coin fell.

Supply and demand elasticity = (% change in quantity supplied) / (% change in quantity demanded).

Community rewards

When a coin or token has a substantial community surrounding it, it can play a role in contributing to improving the asset’s fundamentals. This is an example of market-based governance that has the potential to lead to a rise in the coin or token's value as it is considered an indicator of trust in the network.

Pump and dump schemes

A pump and dump scheme is a manipulative practice within tokenomics where a group artificially inflates the price of a token through coordinated buying, creating a "pump." This creates a false sense of value and attracts unsuspecting users. Once the price reaches a peak, the group sells off their holdings, causing a rapid price decline, or "dump," leaving other users at a loss. Pump and dump schemes are considered fraudulent and can lead to significant financial losses for those involved.

In conclusion

Tokenomics plays a vital role in the cryptocurrency ecosystem by establishing rules, incentives, and economic principles for cryptocurrencies. It influences the value and acceptance of cryptocurrencies by determining factors such as scarcity, utility, and demand.

Well-designed tokenomics can foster trust, adoption, and increase the overall value of cryptocurrencies. However, it's important to be aware of potential downsides, such as market volatility and poorly designed tokenomics models. Understanding tokenomics helps participants evaluate the real-life merit of cryptocurrencies and make informed decisions.

The financial landscape well and truly changed after Bitcoin was released in 2009. The new digital cash system took the financial power away from banks and government entities and put it back into the hands of the people. While Bitcoin has become a household name over the last decade, the creator still remains a mystery. Let's take a deeper dive into one of the biggest mysteries of the modern world.

The Bitcoin solution

Before we plunge into the mysteries of the anonymous entity behind this century's greatest invention, let us first highlight the revolutionary product that is Bitcoin. The electronic payment system was first introduced to the world in late 2008 by a certain Satoshi Nakamoto.

The character seemingly came from the abyss and presented to the world a solution to the global financial crisis that caused widespread disruption. This solution was in the form of a digital currency and used blockchain technology to facilitate, maintain and operate the network.

Nakamoto did not invent blockchain technology, instead, he improved on several issues like the double-spending problem. The technology was originally created to facilitate file sharing although was hindered by that issue. Today, blockchain technology has a wide range of use cases and is being implemented in industries around the world, far beyond just the crypto and financial fields.

Bitcoin remains the biggest cryptocurrency to this day, with over 17,500 alternative cryptocurrencies and counting. At the time of writing the industry is worth just over $2.2 trillion, although it reached highs of $2.968 trillion in November 2021. No asset in the history of the world has gone on to achieve such success in such a short space of time.

What we know about Satoshi Nakamoto

While we know the name Satoshi Nakamoto, it remains to be known who is behind the pseudonym. This person or entity released the Bitcoin whitepaper in October 2008 to a group of cryptographers and shortly afterwards created the BitcoinTalk forum and Bitcoin.org website.

Two months later, the first block on the Bitcoin network was mined, known as the Genesis block, with the caption "The Times 03/Jan/2009 Chancellor on brink of second bailout for banks." It was mined that same day.

Stephan Thomas, a BitcoinTalk Forum member, mapped out when Nakamoto posted on forums to get an indication of what time zone he might live in. The results showed that he was least active during 6h00 to 11h00 GMT, suggesting that should he sleep at night (not a given for developers) that would place him in a time zone somewhere between GMT -5 to GMT -7, somewhere in the Americas.

During 2010, Nakamoto was an active member of the Bitcoin community. He worked on building Bitcoin's protocol and often collaborated and communicated with other developers. Then, towards the end of the year, he strangely handed over the keys and codes to another active developer, Gavin Andresen, and transferred the domains he had created to other members of the community. By the end of the year, he seemed to have cut ties with the project.

Before all but vanishing, the last trace of communication we know of from Satoshi Nakamoto was a message to Mike Hearn, another developer, on 23 April 2011, that read: "I've moved on to other things. It's in good hands with Gavin and everyone." And just as abruptly as Bitcoin had entered the world, Nakamoto left it.

Who could be behind the anonymous entity?

While many people have been suspected of being Satoshi Nakamoto, there is yet to be enough evidence to convince everyone else. Over the years, many journalists have tried to lift the veil, and again, to no avail. For over a decade, the world has been left wondering who is behind the anonymous name, and why would they not come forward?

The biggest contenders for the mystery person have been Hal Finney, Nick Szabo, and Dave Kleiman, who have all denied this. One man, Craig Wright, has come forward to claim to be Satoshi Nakamoto, however, the industry remains unconvinced (along with a judge in a recent legal battle that played out in a British court).

Hal Finney

Hal Finney is a computer scientist who had previously tried to create a digital cash system. Finney is noted as being one of the earliest people interested in Bitcoin, with the first transaction taking place between Satoshi Nakamoto's wallet and Finney's.

Finney also lived in the same town as Dorian Satoshi Nakamoto, a Japanese man who was hunted by the media when they assumed they had found the "real" identity. Finney passed away in August 2014.

Nick Szabo

Nick Szabo is credited with having tried to create a digital cash system prior to Bitcoin's launch, releasing BitGold in 1998. He also coined the name "smart contracts". The cryptographer and computer scientist was listed as the most likely person to be Satoshi Nakamoto following a study done in 2014 by a group of students and researchers at Aston University who conducted a thorough linguistics analysis on all previous communication.

Dave Kleiman

Dave Kleiman was a computer forensics expert whose name has come up plenty of times, largely thanks to Craig Wright. Kleiman's estate sued Wright over claims that they had invented Bitcoin together and had access to a large, shared amount of BTC. He died broke and in squalor in 2013.

Craig Wright

The Australian computer scientist and businessman has gone to great lengths to claim to be Satoshi Nakamoto, however, has provided little to no evidence. These claims have been unequivocally disregarded by the Bitcoin community.

The mystery remains unsolved

Perhaps the biggest irony of all, is that the technology is entirely trustless and operates with the work of thousands of nodes who don't know each other. All we know is that whoever it was/they are, they revolutionised the world as we know it and have left us with some sort of extraordinary.

Cryptocurrencies have gained a reputation for being largely volatile investments. While stocks too can have their moments (what with Peloton stocks dropping 20% every other day) the crypto market carries the brunt of it.

Thankfully, stablecoins have come to the rescue. While still functioning as digital currencies powered by blockchain technology, stablecoins are pegged to external assets such as fiat currencies or gold, thereby eradicating (most of) their volatility.

A Short History Of Stablecoins

After the advent of Bitcoin in 2009, it was only a few years later that a stable digital asset entered the market. Stablecoins came into existence in 2014 when a Hong-Kong based company named Tether Limited released a coin of the same name. The Tether coins' value was pegged to the US dollar, meaning that 1 USDT would always be worth $1.

In order to guarantee this value, the company held the dollar equivalent in bank accounts. Skip past the controversy surrounding their reserves and lack of financial analysis, and there are now plenty of other stablecoin options on the market.

Seeing the infinite benefits of digital currency transactions and blockchain technology, like speed, transparency and low fees, many companies around the world have created their own version of the stablecoin, mostly improving on the previous release. These coins have proven to be invaluable with businesses and retail merchants around the world.

Today, the two biggest stablecoins on the market are Tether (USDT) and USD Coin (USDC). One can argue whether these are "safe haven" assets, but one cannot deny that these tokens hold most of the advantages that digital currencies hold while considerably diminishing the unpredictable market swings.

In our attempt to better understand the concept, let's take a look at the two biggest stablecoins.

Tether (USDT) vs USD Coin (USDC)

Below we explore the two multi-billion-dollar market cap stablecoins, while they both provide the same service in terms of a digital currency, the companies behind them operate quite differently.

What Is Tether (USDT)?

As mentioned above, Tether is the first stablecoin to enter the market. Launched in 2014, the network was initially built on the Ethereum blockchain but is now compatible with a number of other networks.

Note that the Ethereum-based USDT cannot be traded as a TRON-based token, coins need to stick to their respective blockchain networks as this is how the transactions are processed.

It wasn't long before USDT was listed on the top exchanges, and included in dozens of trading pairs.

Tether Limited have since released a Euro-based stablecoin as well as Tether crypto coin pegged to the price of gold. The downside to Tether falls on the company's reputation surrounding transparency and reserve funds.

There have been several court cases where individuals and regulatory bodies have called for transparency surrounding the funds held in reserves. Tether has since provided access to this information but is yet to go through a third party audit. Regardless, Tether holds the third biggest market cap (at the time of writing).

What Is USDC (USD Coin)?

USD Coin is a stablecoin created by the Centre Consortium, an organisation made up of crypto trading platform Coinbase and Circle, a peer to peer payment platform. It launched in 2018 as an ERC-20 token and has since climbed the ranks to be in the top 5 biggest cryptocurrencies based on market cap. USD Coin is available on the Ethereum blockchain, as well as Solana, Polygon, Algorand and Binance Smart Chain networks.

The significant bonus that USDC holds over its biggest competitor, USDT, is that the coin is regularly audited by a third-party institution. These audits are made public, allowing any user to verify the authenticity of their USDC value each month. Since launching USDC, Coinbase has removed USDT from its platform.

USDT vs USDC: Head-to-Head Comparison

Adoption

With over a decade in circulation, USDT has achieved far greater adoption worldwide. It remains the dominant stablecoin in trading pairs and global liquidity, particularly in emerging markets. Winner: USDT

Transparency

Tether has historically struggled with transparency, though it now publishes quarterly attestations. By contrast, USDC provides monthly reports with independent verification, giving it the edge for investors who value oversight and regulatory clarity. Winner: USDC

Regulatory Compliance

Circle and Coinbase designed USDC with U.S. and international regulations in mind. USDC reserves are kept in regulated banks and Treasuries, and Circle is registered as a money transmitter in multiple jurisdictions. Tether claims compliance but lacks comparable transparency. Winner: USDC

Price Stability

Both USDT and USDC are pegged 1:1 to the U.S. dollar. While they occasionally experience small deviations, both have shown resilience and quickly return to their peg. Winner: Tie

Redemption Process

Redeeming USDT directly requires a minimum of 100,000 USDT plus fees, which makes it impractical for small investors. USDC allows redemptions starting at just $100, giving it an accessibility advantage. Winner: USDC

Incidents

Both stablecoins have faced brief de-pegging events. USDT dipped below $0.95 during market stress in 2022, while USDC fell to around $0.87 during the Silicon Valley Bank crisis. In both cases, prices stabilized quickly. Winner: Tie

Longevity

Tether has been around since 2014, giving it a proven track record and first-mover advantage. Winner: USDT

Which Stablecoin Should You Choose?

Due to the fact that these respective companies are holding the dollar-equivalent value in reserves, these two digital currencies are considered to be centralized, while the rest of the cryptocurrency market holds a decentralized nature. As the demand for digital currencies increases, it is likely that these two stablecoins will only continue to grow.

When looking for a stablecoin, these are two most recognised options. Choosing between USDT and USDC depends on what you value most as an investor or user.

- If you need deep liquidity, global adoption, and access across more blockchains, USDT remains the go-to option. Its size and reach are unmatched, making it the default stablecoin for many traders.

- If you prioritize regulatory compliance, transparency, and a lower barrier for redemptions, USDC is the safer bet. It continues to build trust among institutions and investors who want accountability.

Ultimately, both stablecoins play vital roles in today’s crypto ecosystem. Some traders even use a combination of USDT and USDC to balance adoption with transparency, hedging against risks specific to either coin.

Users can both buy and sell USDT and USDC directly through the Tap app. Simply create your account, complete the KYC process and deposit funds into your digital wallet. Manage your entire crypto (and fiat) portfolio from one convenient, secure location.