November 2025 could be a turning point for crypto. From ETFs to major network upgrades, here are six catalysts that could shape the market.

Keep reading

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

1. Seasonality & Historical Momentum Could Kick In

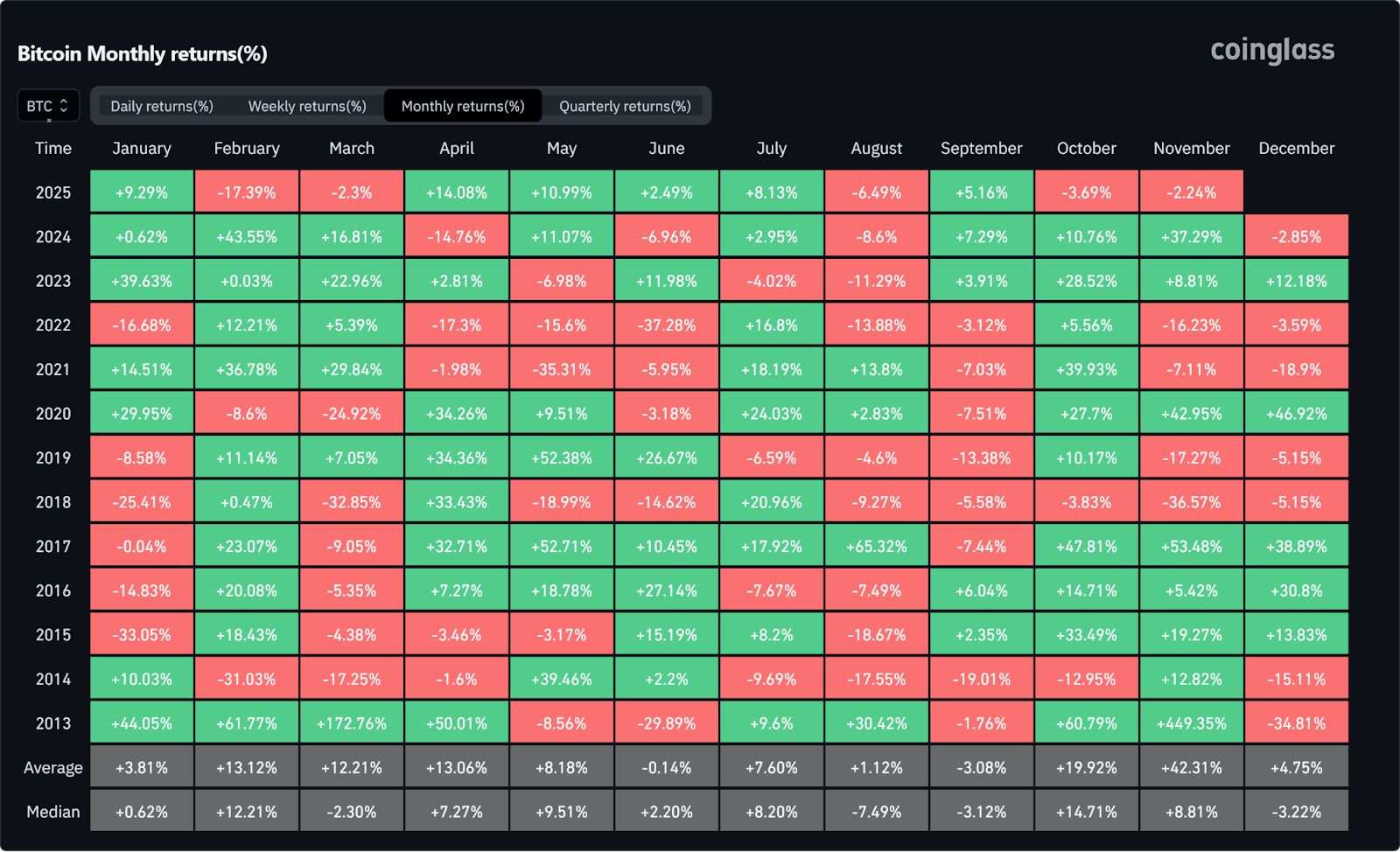

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

4. Altcoins at an Inflection Point

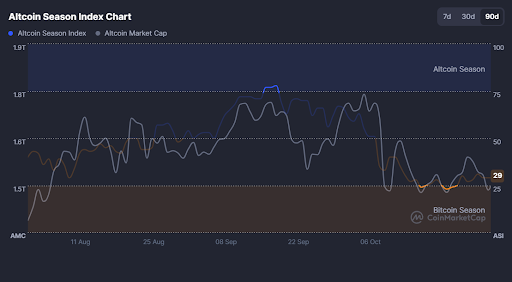

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

NEWS AND UPDATES

LATEST ARTICLE

We're thrilled to share that our fintech company has just celebrated its third anniversary! It's been an incredible journey so far, and we're so grateful for the opportunity to serve our users every day.

When we first launched our platform three years ago, we had a clear mission in mind: to provide an innovative, user-friendly, and accessible way for people to manage their money, trade cryptocurrencies, and access financial services. It was a big goal, and we knew that we had a lot of hard work ahead of us.

But we were determined to succeed. Our small team of passionate and dedicated individuals worked tirelessly, day in and day out, to bring our vision to life. We poured our hearts and souls into this project, and we knew that we were onto something special.

Fast forward three years, and we're proud to say that we've come a long way. We've built a platform that we believe in, and we're constantly striving to improve it. We've listened to feedback from our users, and we've added new features and services that meet their needs. And we've built a community of passionate and engaged users who share our vision for a better way to manage their finance everyday.

One of the things that sets our company apart is our commitment to transparency and user experience. We believe that managing your finances should be easy, intuitive, and stress-free. That's why we've built our platform to be as user-friendly as possible, with clear and straightforward interfaces that make it easy to manage your money and digital assets.

But our success wouldn't be possible without our amazing users. We're so grateful for your continued support, feedback, and encouragement. You've helped us to shape our platform into something truly special, and we're committed to continuing to serve you and improve our platform to meet your needs.

As we celebrate our third anniversary, we're excited to look back on how far we've come and to look forward to all the exciting things that the future holds. We're proud of what we've accomplished, but we know that there's always more work to be done. We're committed to continuing to innovate and improve, and we're grateful to have you along for the ride.

Thank you for being part of our journey. Here's to many more years of growth, success, and innovation!

1inch is a cryptocurrency trading tool for traders, allowing them to quickly find and access competitive prices on decentralized exchanges (DEXs) using its innovative 1INCH token, which provides both utility and governance functionalities to token holders.

What is the 1inch network?

The 1inch network is a decentralized exchange aggregator that assists crypto traders in finding the best prices and lowest fees for their transactions within the DeFi (decentralized finance) sector of the cryptocurrency market.

Decentralized exchanges use self-operating smart contracts to enable trades between buyers and sellers, utilizing a non-custodial infrastructure. This allows for seamless transactions while maintaining the utmost security of funds.

While these exchanges offer heightened security, this does not always lead to heightened liquidity, which can result in what is called slippage. This is where there is a discrepancy between the expected price of a trade and the actual price once executed. The 1inch protocol helps to avoid this problem and other market inefficiencies by joining together trading activity from multiple markets and combining liquidity.

In essence, the DeFi space is notorious for fast-changing prices and transaction fees for crypto assets, and 1inch solves this problem. Instead of traders having to manually resource and compare prices across DEXs, the 1inch network gathers real-time pricing data, including gas fees, from several top exchanges and presents this information to the trader. These exchanges include the likes of 0x, SushiSwap, Uniswap, and Kyber Network.

The network is fueled by the 1INCH token and ERC-20 token that provides governance rights and participation in the network's expansion. The token serves as both a utility token and a governance token on the network allowing holders to vote on key protocol parameters.

Who created the 1inch platform?

1inch was founded by Surjey Kunz and Anton Bukov during the ETHGlobal New York hackathon in May 2019, built on the Ethereum blockchain. The pair had previously entered hackathons together, winning awards along the way.

Prior to this endeavor, Sergej Kunz had a wealth of experience in programming and development. He was a senior developer at Commerce Connector, coded for Herzog agency, directed projects with Mimacom consultancy, and worked in both DevOps and cybersecurity roles at Porsche.

With nearly two decades of experience in software development and five years specialized in decentralized finance (DeFi), Anton Bukov has become a seasoned expert, contributing to projects like gDAI.io and NEAR Protocol.

In August 2020, 1inch received $2.8 million in funding from Binance Labs, Galaxy Digital, and several other firms before raising a further $12 million in December from prominent firms including ParaFi Capital and Pantera Capital. A year later, 1inch received $175 million in another funding round led by Amber Group.

How does the 1inch Protocol work?

In its most basic form, 1inch operates in a similar way to prevalent travel booking sites in that the protocol collects and compares crypto prices and transaction fees from several decentralized exchanges. The platform uses three prominent protocols: the aggregation protocol, the liquidity protocol, and the limit order protocol.

The aggregation protocol that factors in gas fees

By utilizing 1inch, traders have the convenience of trading from a single platform while being exposed to the lowest trading fees and best prices across several DEXs. Their Pathfinder product not only finds the top trading routes across several markets but also considers gas fees. The aggregation protocol will automatically factor in the gas fees when establishing the best price routes.

For instance, the complex protocol can break down single trades across multiple DEXs in order to provide the best market price. Finding the most efficient swapping routes might include converting a cryptocurrency to a stablecoin and then finding the best crypto prices across multiple exchanges (factoring in low trading fees) before executing the original trade. 1inch takes care of the complex backend routing processes while the trade effectively executes one trade at the best price.

The liquidity protocol for liquidity providers

The platform's liquidity protocol incorporates a next-generation automated market maker (AMM) that not only provides impressive opportunities for liquidity providers but also protects users from front-running attacks typically associated with liquidity pool trading.

The liquidity protocol allows users to earn passive income from depositing their cryptocurrencies into the relevant liquidity pools and earning LP tokens in return. LP tokens can be staked or exchanged, while the cryptocurrencies in the liquidity pools can be used for transactions made by liquidity providers utilizing the 1inch exchange, a decentralized exchange.

To engage in the liquidity protocol or the 1inch exchange, users simply need to connect their wallet and select the liquidity pool (trading pair) they wish to provide liquidity. Additionally, as the decentralized exchange aggregator does not store any crypto assets on its server, users are never required to pay a withdrawal or deposit fee when using the 1inch exchange services.

The limit order protocol for decentralized exchanges

Considered one of the "most innovative and flexible limit order swap opportunities in DeFi" 1inch’s limit order protocol allows traders to place more advanced, conditioned orders to automatically guarantee their profits at certain prices or avoid losses.

Alongside the flexible limit order functionality, the protocol also offers features such as dynamic pricing, extra RFQ support, and powers various implementations.

What is the 1INCH token?

The 1INCH token is an ERC-20 token that serves as a utility and governance token for the platform. On top of functions like spending, sending, holding, and staking, the 1inch token also provides voting rights to token holders on any proposed updates to the protocol.

How can I buy the 1INCH token?

Users can easily incorporate the 1INCH token into their portfolio through the Tap app's secure platform. The easy method allows anyone with an account to engage in an effortless trading experience using both cryptocurrencies and fiat currency.

Tap into the 1inch ecosystem by opening an account and loading your preferred wallet, then simply execute the trade to buy the 1INCH token. The tokens can then be held in the integrated wallet or used on the 1inch exchange platform or liquidity pools by completing a simple transaction. All you need to do to get started is download the app and create an account.

.svg)

Playing an important role in the adoption of Web3, Enjin provides a platform of software products designed to allow anyone to harness the power of NFTs (non-fungible tokens) through the development, trade, monetization, and marketing of blockchain assets.

The Enjin Coin (ENJ) is the native utility and governance token of the Enjin ecosystem. For gamers, developers and investors alike, ENJ matters because it bridges real-world value with digital goods, offering a means to turn in-game items into tradable assets. In this article you’ll learn what ENJ is, how it works, its key use-cases, how to buy it, its tokenomics, investment considerations and how it stacks up against other gaming tokens.

What Is the Enjin Platform?

The Enjin platform is an ecosystem of interconnected, blockchain-based gaming products designed for individuals, game developers and businesses to create, manage and trade virtual goods such as digital art, games, or virtual marketplaces using the Ethereum blockchain. Enjin aims to provide users with the tools to implement smart digital solutions for blockchain games within the gaming environment.

Through the platform's software development kits (SDKs) and APIs, users can build digital assets as well as seamlessly integrate them into their games and applications.

Under the Enjin umbrella is the Enjin Network, a community gaming platform that allows users to create websites, chat, and host virtual stores. Over the course of a decade, the Enjin platform has accumulated over 20 million users.

The ecosystem binds together gaming communities, game-asset markets and blockchain infrastructure. For example, a developer might create a limited edition in-game sword, mint it using ENJ as backing, list it on the marketplace, players trade it, and the underlying ENJ can be melted or reused. For developers, Enjin provides monetisation tools. For gamers, it provides ownership and portability of digital items.

Powering the ecosystem is the Enjin Coin (ENJ), a token used to back the value of NFTs and other assets minted on the platform. When an asset is minted it locks ENJ tokens into a smart contract and effectively removes the tokens from circulation.

It’s also worth noting that Witek Radomski, Enjin's co-founder and the brainchild behind the ERC-1155 Ethereum token standard, wrote the code for the first non-fungible token (NFT). By utilizing its cutting-edge technology, Enjin is revolutionizing the future of gaming and digital assets.

Who Created Enjin?

Enjin was originally founded in 2009 as a gaming community platform by Maxim Blagov and Witek Radomski. Blagov took on the responsibility of being CEO and in charge of the platform's creative direction while Radomski took on the role of CTO, leading the technical development of the platform's products.

Following Radomski's interest in Bitcoin in 2012, the platform explored incorporating blockchain technology into its business model and embraced the world of tokenized digital assets.

Radomski went on to write the ERC-1155 token standard in June 2018, a token standard used for minting both fungible, semi-fungible and non-fungible tokens using the Ethereum network. This token standard is a critical building block in the platform’s design.

In 2017, the Enjin platform launched an initial coin offering (ICO), raising $18.9 million through ENJ token sales. A year later the project went live and in September 2019, the Enjin Marketplace was launched.

How Does Enjin Work?

The primary goal of the Enjin network is to facilitate the management and storage of virtual goods for games, anything from in-game currencies to unique in-game items. So, how does Enjin work? The process of creating and destroying these tokens involves five steps:

- Purchase

Developers purchase Enjin Coin. - Minting

In-game items are designed and effectively minted with the appropriate amount of ENJ locked into a smart contract. - Utilization

Players use these tokens within the game. - Trading

Players trade the tokens between fellow players or on the internal or external marketplace. - Melting

Players sell the tokens for Enjin Coin, referred to as melting. The token is destroyed and Enjin Coin is released from the smart contract.

SDKs (software development kits) come into play here, with kits designed to fulfill certain functions, such as facilitating a payment platform or being wallet-focused. These kits are designed to minimize costs and simplify the process of creating these virtual goods. APIs (application programming interfaces) work alongside the SDKs to integrate these virtual goods (digital assets) into the game.

The Enjin platform utilizes JumpNet which is integrated with other products in the ecosystem, such as the Marketplace, Enjin Beam, and the Enjin Wallet to allow for gas-free transactions for ENJ and NFTs.

The Enjin ecosystem encompasses the Enjin smart wallet that allows players to store and trade their in-game items with ease. The Enjin wallet is designed to connect all the features, from managing inventory to conducting transactions and selling these tokenized digital assets for ENJ.

What is the Enjin Coin (ENJ)?

As we mentioned previously, Enjin Coin (ENJ) is the native token of the Enjin ecosystem. Built on the Ethereum blockchain and compatible with multiple gaming platforms, the Enjin Coin is an ERC-20 token that allows the in-game items created on the platform to be traded with real-world value. The ENJ token has a maximum supply of 1 billion coins.

The token also allows developers to mint these digital goods. The process requires the users to lock Enjin Coin (ENJ) into a smart contract that automatically assigns value to the in-game item. Players that later use these items can use them in the game, trade them or sell them for ENJ, equivalent to the original minting cost. Once sold, the item is destroyed (known as melting) and the ENJ that was locked in the smart contract is released to the seller.

How Can I Buy the Enjin Coin?

Anyone can tap into the Enjin ecosystem by acquiring ENJ tokens through the Tap mobile app. Simply create an account and complete the verification process in order to gain access to your unique Enjin wallet, from where you can buy, trade and sell Enjin Coin.

Fully licensed and regulated, Tap provides a secure and convenient means of managing your funds, allowing users to manage and store both crypto and fiat currencies in one location. With a wide range of supported currencies and services, Tap is revolutionizing the financial space.

Take advantage of the power of Enjin Coin on the Tap app - the ultimate platform to buy, sell or hold ENJ. With seamless integration and an intuitive interface, trading Enjin tokens has never been easier. Stay up-to-date with the latest market trends and keep your portfolio on track by monitoring the Enjin Coin price in real-time.

Bottom Line

Enjin Coin (ENJ) is more than just another cryptocurrency; it's the utility token powering a complete blockchain gaming ecosystem. It allows game studios to create, manage, and monetize digital assets, gives gamers true ownership and the ability to trade those assets, and offers investors exposure to where gaming, NFTs, and Web3 infrastructure converge.

That said, adoption rates, competition, and regulatory developments all play a role in ENJ’s future. If blockchain gaming, asset tokenization, and virtual economies interest you, ENJ presents a compelling option. Just make sure to do your research, evaluate the projects actually using it, and align any investment with your own goals and risk tolerance.

We are delighted to announce the listing and support of Ankr (ANKR) on Tap!

ANKR is now available for trading on the Tap mobile app. You can now Buy, Sell, Trade or hold ANKR for any of the other asset supported on the platform without any pair boundaries. Tap is pair agnostic, meaning you can trade any asset for any other asset without having to worries if a "trading pair" is available.

We believe supporting ANKR will provide value to our users. We are looking forward to continue supporting new crypto projects with the aim of providing access to financial power and freedom for all.

Ankr is playing an integral role in the adoption of Web3, providing growth and development opportunities for network stakers, app developers, and other participants in the DeFi space.

Ankr is a decentralized Web3 infrastructure provider that facilitates the swift and effortless connection between developers, dapps, stakers, and blockchains. With Ankr's APIs & RPCs you can quickly build blockchain-based applications with confidence, stake on Ankr Earn as well as access custom solutions for any blockchain enterprise needs.

ANKR is Ankr's native cryptocurrency fueling the platform and is used as a payment method within the ecosystem.

Get to know more about Ankr (ANKR) in our dedicated article here.

Ankr is playing an integral role in the adoption of Web3, providing growth and development opportunities for network stakers, app developers, and other participants in the DeFi space.

Ankr is leading the way in making it easier for users to interact with multiple blockchains. Streamlined and simple, Ankr simplifies complex tasks so that you can access multi-blockchain technologies quickly and securely.

What is Ankr (ANKR)?

Ankr is a decentralized Web3 infrastructure provider that facilitates the swift and effortless connection between developers, dapps, stakers, and blockchains. With Ankr's APIs & RPCs you can quickly build blockchain-based applications with confidence, stake on Ankr Earn as well as access custom solutions for any blockchain enterprise needs.

Ankr simplifies the process of setting up and participating in Proof of Stake (PoS) blockchains. It provides various tools and services to help users deploy nodes, stake their PoS tokens, and access decentralized finance (DeFi) applications. The Ankr platform was first launched as a Distributed Cloud Computing Network that leverages idle computing resources. This allowed users to access cloud computing services without relying on a single provider's infrastructure.

Ankr provides a variety of features and tools, such as node hosting, staking pools, analytics, and automated notifications. These services work together to make participating in Web3 easier by providing simple solutions.

The node creation process is supported across multiple blockchains and in return for the services provided, node operators pay a monthly fee to Ankr.

ANKR is Ankr's native cryptocurrency fueling the platform and is used as a payment method within the ecosystem.

Who created the Ankr platform?

Ankr was founded in 2017 by Chandler Song, Ryan Fang and Stanley Wu and officially launched in 2019. Song and Fang were former college roommates while Song worked under Wu, a computer engineer at Amazon Web services, while interning. Together the three founders created Ankr, with a mission to build the most decentralized and scalable Web3 infrastructure possible. Song is currently serving as CEO, Fang as COO, and Wu as CTO.

Following several successful rounds of funding, the team has amassed tens of millions of dollars from big blockchain investors such as Pantera Capital and NEO Global Capital (NGC) as well as several funding rounds. The first token presale raised $15.9 million followed by another token sale which raised $18.7 million in just six days. Once opened to the general public, the platform raised a further $2.75 million.

How does the Ankr Protocol work?

It is important to note that Ankr is not a blockchain. Instead, it provides specialized tools which are beneficial for builders, stakers, and businesses alike. Its main features can be broken down into these four categories below:

Node infrastructure services

With Ankr's decentralized infrastructure, DeFi platforms, NFT projects, blockchain games and dapps of all kind can receive faster access to blockchains at a more scalable and cost-efficient rate. Hosted by numerous high-performing nodes across the world simultaneously serving requests, these applications are guaranteed optimal performance.

However, setting up a blockchain node requires technical know-how, time, and effort, skills not everyone possesses. Ankr provides a service where it can launch one which can be accessed remotely. This provides the opportunity for users of all skill levels to participate in the validation process on a Proof of Stake blockchain. Additionally, the platform overlooks the performance of the node to ensure that users' funds staked are not punished due to any downtime or dishonesty.

Instant API and RCP access for developers

Developers who are launching smart contracts and dapps to a blockchain are required to use designated APIs (Application Programming Interfaces). This process typically involves running a node alongside these and spending time synchronizing it to the data on the blockchain.

To solve this issue, Ankr provides instant API services and RPC (Remote Procedure Call) access to developers. This allows for uninterrupted access to blockchains without having to worry about vying traffic. It also provides access to the whole chain's data, supplying the dapp with all the information it might require and an overall better user experience.

Custom Blockchain Enterprise Tools

For enterprises in need of custom-made, streamlined solutions for handling multiple blockchain networks, Ankr provides a Web3 Infrastructure-as-a-Service model. Accessible through an easy-to-use monitoring platform, businesses can utilize the platform's API and RPC services making their operations more efficient and cost-effective.

Liquid staking

Ankr provides staking capabilities across multiple chains, offering reward-earning tokens to represent these staked funds. The tokens can then be used to trade or for various DeFi activities such as lending, yield farming, liquidity mining, etc. This allows users to maximize their earning potential while still engaging in staking activities.

For example, instead of staking the minimum required amount of 32 ETH on Ethereum 2.0, users can stake 0.5 ETH through the Ankr protocol, with these funds automatically being routed to the pools with the highest yield. In return, users will receive aETHb or aETHc tokens, which provide a liquid way in which users can access their staked tokens.

What is the ANKR token

ANKR is an ERC-20 and BEP-20 token that operates across both the Ethereum and BNB Smart Chain networks. The utility token has a number of functions, as outlined below, and a maximum supply of 10,000,000,000.

ANKR is primarily a form of payment on the platform but also offers staking functionalities and governance rights.

How can I buy the Ankr token?

Tap's mobile app makes it effortless for users to acquire ANKR and store it in the integrated wallet with assurance. Not only can you benefit from a convenient place to acquire and store your ANKR token, but also withdraw coins immediately for use on the linked DeFi platform. Tap provides you with not just an easy way to trade digital assets, but also a reliable space where your assets holdings can remain securely stored over extended periods of time.

Unlock the potential of a range of verified cryptocurrencies and fiat wallets by downloading the Tap mobile app.

Convex Finance has been dubbed a "DeFi 2.0 protocol," and is part of the ever-growing subset of second-generation decentralized finance (DeFi) protocols that offer yield farming services to users. Deeply ingrained in the DeFi space, Convex empowers Curve Finance users to further benefit from earning and optimizing yields.

What is Convex Finance (CVX)?

Convex Finance is a revolutionary DeFi platform that offers enhanced staking rewards and works on top of the Curve Finance network, a decentralized exchange (DEX) liquidity pool designed for the swapping of stablecoins. By focusing on stablecoins, the Curve exchange platform is able to bypass volatility typically associated with the cryptocurrency industry, as well as offer lower trading fees and less slippage.

Curve Finance functions using its native CRV tokens which are earned when users deposit crypto assets into its liquidity pools. Both protocols, Curve and Convex, are built on the Ethereum blockchain. Convex acts as a yield optimizer for both Curve CRV token holders and Curve liquidity providers on the network.

Convex offers a simple user experience alongside extra advantages such as low-performance fees and zero withdrawal fees, which allows liquidity providers and CRV stakers to earn higher returns. Convex Finance CVX tokens are the platform's native token and are ERC-20-based utility tokens with additional governance incentives.

The Convex Finance protocol offers two ways in which users can optimize their yields: staking and providing liquidity.

- Staking: users can stake CRV tokens on Convex (instead of staking on Curve directly) to receive additional rewards (CVX and a portion of the protocol's earnings). CVX can also be staked on the Convex platform, and in return, users earn a share of Curve liquidity providers' CRV earnings.

- Liquidity providers: as a reward for providing liquidity on the Curve platform, liquidity providers earn Curve LP tokens. These tokens can be staked on the Convex platform in return for CRV tokens and additional rewards. The more CRV tokens that are staked, the higher the reward distribution.

CVX token holders can earn governance rights by locking their tokens on the platform for a specific amount of time.

Who created the Convex Finance platform?

Convex Finance was launched in May 2021 by a pseudonymous founder, C2tp. Little is known about this person or group but it is assumed that they came from a software development background. Despite anonymous founders generally being a red flag for risky investments, Convex has defied this norm and is considered to be one of the most influential and important protocols in the DeFi industry.

In its first month, Convex Finance recorded $68 million in total value locked (TVL), reaching its peak in January 2022 of $21 billion. TVL refers to the sum of all the crypto assets deposited in a DeFi protocol at any given.

Soon after launching, the Convex platform was whitelisted on the Curve platform. Due to a large number of CRV tokens being deposited on Convex, Curve granted Convex permission to participate in Curve's governance.

How does Convex Finance work?

The Convex Finance protocol provides users access to liquidity and earning trading fees through Curve's established stablecoin pools. In order to do so, users need to deposit Curve tokens into Curve's liquidity pools and then stake them on Convex. Acting as an intermediary, Convex then auto-harvests these tokens and reimburses liquidity providers with the gained rewards.

CRV tokens and curve liquidity providers

These rewards can be distributed as either CRV or other tokens such as LDO or SNX. Liquidity providers can also increase their returns by further compounding their earned CVX tokens through the staking mechanism. Both CRV stakers and Curve’s liquidity providers are entitled to Convex liquidity mining rewards.

Convex Finance CVX tokens were designed to simplify staking on Curve's platform with an added fee-earning nature. When a user deposits CRV into Convex, the platform converts these tokens into veCRV (vote escrowed CRV) and credits the depositor with cvxCRV on a 1:1 ratio. Users can then exchange the cvxCRV tokens for CRV using the Curve liquidity pool and earn higher yields by locking up more CRV.

When users have deposited a certain amount of CRV tokens into the Convex protocol they receive wrapped cvxCRV tokens. These tokens can be staked for CVX tokens and are entitled to CRV rewards earned through the protocol. These rewards include receiving a part of the CVX token airdrop and a 10% share of the CRV harvested by the vaults.

By providing users the opportunity to earn staking rewards and trading fees without having to lock in CRV, Convex offers a secondary source of income for tokens users already own through Curve. This is the core reason for Convex's success and growth.

What are CVX tokens?

Convex Finance CVX tokens are ERC-20-based tokens with both utility and governance functionality. The token is used to receive a share of Convex platform fees and reward CRV stakers.

The token has a maximum supply of 100 million, with 50% of the tokens assigned to rewarding Curve liquidity providers. 25% of the remaining tokens are allocated to liquidity mining distributions over the next four years while 9.7% are held in the platform's treasury.

How can I buy the Convex Finance CVX token?

Tap grants its users the freedom to trade securely while retaining their cryptocurrencies in its integrated wallet or the choice of withdrawing them for use on DeFi platforms. Tap offers a secure space to not only trade digital assets but to store them long term too.

Unlock the power of Tap's mobile app by creating an account and completing your account verification steps. You'll then enjoy access to a wide array of vetted crypto markets and fiat currencies, from where you can buy or sell Convex Finance CVX tokens in a click. All that stands between you and get started with Tap is getting the app today.