Is USDT safe? Explore how Tether works, what backs it, key risks, and why it remains the most-used stablecoin despite regulatory and transparency concerns.

Keep reading

USDT is everywhere in crypto: powering trades, bridging platforms, and acting as a go-to safe haven when markets turn volatile. Backed by Tether, it promises the stability of a dollar with the speed of digital assets. But how secure is that promise?

In this article, we’ll unpack how USDT works, the risks beneath the surface, and why it remains a key player in the crypto economy.

What is USDT and why it matters

Think of USDT (Tether) as the crypto world's attempt to create digital cash that doesn't give you a heart attack every time you check its price. Launched back in 2014 by a company called Tether Limited, USDT was designed to be a "stablecoin" - a cryptocurrency that maintains a steady 1:1 relationship with a certain fiat currency: the US dollar. One USDT should always equal one dollar. Simple, right?.

Well, like most things in crypto, it's a bit more complicated than that.

USDT has become the utility tool of crypto, offering a fast and flexible option to move in and out of positions without cashing out to traditional fiat. It’s the common language of the crypto ecosystem, enabling smooth transfers, seamless trading, and a place to park value when markets swing.

Tether Limited, the company behind USDT, operates globally, with roots in the British Virgin Islands and operations stretching from Hong Kong to the Bahamas. Unlike central banks, Tether isn’t printing dollars, though: it issues tokens, claiming each one is backed 1:1 by assets in reserve.

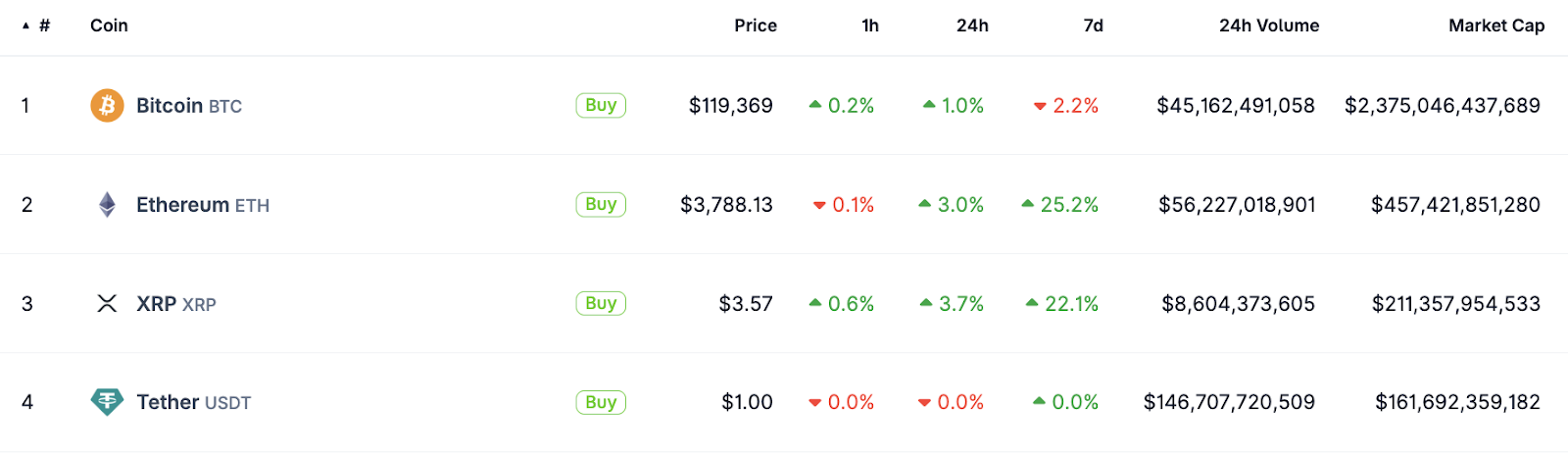

With over $160 billion in circulation as of mid-2025, USDT isn’t just a trading tool, it’s foundational infrastructure for the crypto economy. It’s also the largest stablecoin on the market, based on market cap and 24-hour trading volume.

Top cryptocurrencies by market cap at the time of writing. Source.

Is USDT safe?

The short answer? USDT exists in a grey area between "reasonably safe for what it is" and "proceed with caution."

The slightly longer answer? Here's what you need to know at a glance:

What's working:

- Maintained its dollar peg through multiple market crashes

- Backed by a mix of cash, government securities, and other liquid assets

- Most widely accepted stablecoin across exchanges and platforms

- Regular attestations from accounting firms

What's concerning:

- Limited transparency compared to some competitors

- Regulatory uncertainty and past legal issues

- Concentration risk (too big to fail, too big to save?)

- Not fully backed by cash alone

The reality check: USDT has survived crypto winters, bank runs, and regulatory pressure for nearly a decade. While it's not risk-free (nothing in crypto is), it's proven more resilient than many predicted. For short-term trading and payments, most users find it reliable. For long-term wealth storage? That's where you might want to consider your options more carefully.

How USDT is backed: understanding Tether's reserves

Here’s where things get more complex and where much of the scrutiny around Tether lies.

In simple terms, USDT operates like a digital receipt: you deposit dollars, and in return, you get tokens you can use across the entire crypto ecosystem. But what happens to those dollars? Are they sitting in a vault, or being put to work?

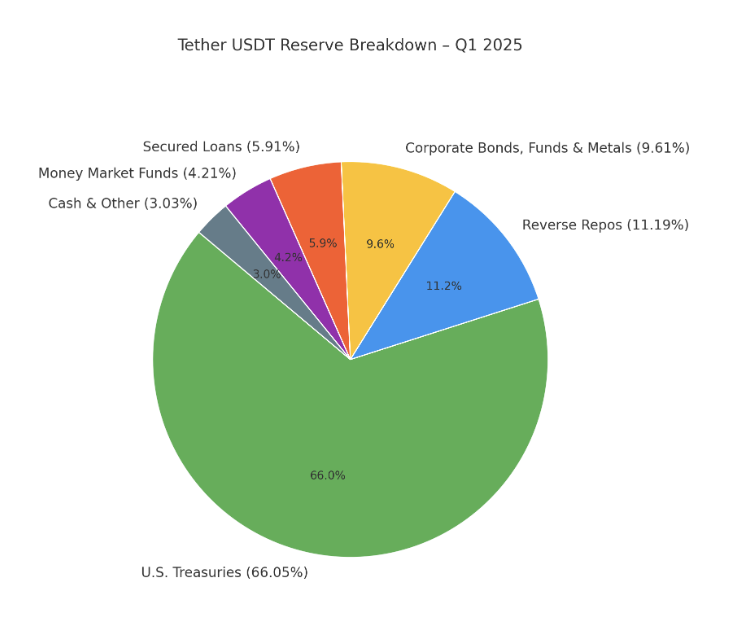

Tether has long opted for the investment route. Instead of holding pure cash, it backs USDT with a diversified portfolio of assets. According to its Q1 2025 attestation from BDO, Tether’s reserves looked roughly like this:

The shift toward U.S. Treasuries and away from riskier assets marked a significant improvement in its reserve quality. While not fully audited, Tether does publish quarterly attestations from BDO, providing some visibility into how reserves are managed. It’s not a full audit, but it’s a step forward from the opaque reporting of earlier years.

That being said, past controversies still shape how Tether is perceived. In 2019, Tether admitted that USDT was not fully backed by cash at all times and revealed it had lent $850 million to Bitfinex, its sister company. This led to a high-profile settlement with the New York Attorney General in 2021, requiring Tether to improve transparency and cease operations in New York.

Again, to put it in simple terms: imagine your bank quietly loaning out customer deposits to a related company without clearly telling you. Not necessarily illegal, but definitely a breach of trust for users expecting a 1:1 backed stablecoin.

Regulatory scrutiny & legal risks

If USDT were a person, it would probably have a thick file folder in regulatory offices around the world. Sure, being the largest stablecoin makes you a big target, but Tether has also found itself in the crosshairs of regulators who are still figuring out how to handle the crypto revolution.

In the United States, Tether operates in something of a regulatory twilight zone. The company has faced pressure from agencies like the Commodity Futures Trading Commission (CFTC), which fined Tether $41 million in 2021 for making false statements about being fully backed by US dollars.

The European Union is taking a more structured approach with its Markets in Crypto-Assets (MiCA) regulation, which will require stablecoins to be backed by highly liquid assets. This could actually work in Tether's favour, as they've already been moving in that direction.

Emerging markets present their own challenges. Some countries have embraced USDT as a hedge against local currency instability, while others have banned it outright, not far from a global game of regulatory whack-a-mole.

For users, the regulatory risks are real but indirect. If major jurisdictions crack down hard on Tether, it could affect the token's liquidity and usability. However, a complete overnight shutdown seems unlikely given USDT's deep integration into the crypto ecosystem.

The bigger risk might be increased compliance requirements that could make using USDT more cumbersome, similar to how traditional banking has become more regulated over time.

How safe is USDT for holding assets?

This is where we need to have an honest conversation about what "safe" means in crypto land.

For short-term use (days to weeks):

USDT works pretty well. If you're trading crypto or need to park funds briefly between investments, it's like using a decent hotel - not your forever home, but comfortable enough for a short stay.

The peg has held remarkably well through various market conditions, and liquidity is excellent across most major platforms.

For medium-term holdings (months):

Here's where things get a bit more nuanced. USDT has survived multiple "stress tests", including the Terra Luna collapse, FTX implosion, and various banking sector scares. However, you're essentially trusting that Tether's reserve management continues to work smoothly and that no major regulatory bombshell disrupts operations.

For long-term wealth storage (years):

This is where many experts start raising eyebrows. Holding large amounts in any stablecoin for extended periods comes with risks that compound over time. You're exposed to regulatory changes, potential company mismanagement, and the general "unknown unknowns" that come with relatively new financial instruments.

Essentially, USDT is like keeping money in a foreign bank account. It might work great for a while, but you're subject to the laws, regulations, and business practices of entities outside your home jurisdiction.

The key insight from the crypto community is diversification. Even USDT supporters rarely recommend putting all your eggs in the Tether basket.

Security best practices when using USDT

Using USDT safely isn't just about trusting Tether - it's also about protecting yourself from the various ways things can go wrong in the crypto world.

Platform risk management: Remember, USDT is only as safe as the platform you're using it on. The token itself might be fine, but if you're holding it on a sketchy exchange that gets hacked or goes bankrupt, you could lose everything. Stick to regulated platforms only.

Diversification strategies: Many crypto users often split their stablecoin holdings across multiple tokens and platforms. Think of it as not putting all your digital eggs in one digital basket. As an example, some might hold 40% USDT, 40% USDC, and 20% in other stablecoins or traditional assets.

For crypto beginners: Start small, learn the ropes, and, if you wish, gradually increase your holdings as you become more comfortable. Use well-established exchanges for your first purchases, enable two-factor authentication on everything, etc. Treat your crypto security like you would your online banking, that's essentially what it is.

USDT vs other stablecoins

The stablecoin world isn't a one-horse race, and understanding the alternatives helps put USDT's safety in perspective.

USDT vs USDC

USDT dominates in usage and global liquidity. It's the most widely accepted stablecoin across exchanges, DeFi platforms, and payment rails. But it has faced criticism over the years for a lack of full audits and historical opacity around reserves.

USD Coin (USDC), issued by Circle, takes a different approach. It’s often seen as the “regulated” stablecoin, with monthly attestations and a conservative reserve mix (primarily cash and short-term U.S. Treasuries).

- USDT is ideal for fast-moving markets and broad platform compatibility.

- USDC appeals to those who prioritise transparency and regulatory oversight.

USDT vs DAI

DAI takes a completely different route. Issued by MakerDAO, it’s a decentralised stablecoin backed by overcollateralised crypto assets like ETH, not fiat. There’s no single company behind it, just smart contracts and community governance.

While DAI offers full on-chain transparency and avoids centralised custodians, it also comes with higher complexity and potential risks tied to smart contract bugs or extreme market conditions.

- USDT provides speed and simplicity, backed by a traditional corporate structure.

- DAI offers a decentralised alternative, ideal for DeFi-native users.

USDT vs BUSD

BUSD, once a major player backed by Binance and Paxos, was phased out in 2024 due to regulatory pressure. It serves as a reminder that centralised stablecoins depend on both market forces and compliance frameworks, and can be wound down unexpectedly.

While USDT remains standing, BUSD’s sunset reinforces the importance of evaluating who’s behind the stablecoin and how stable their operations really are.

What happens if Tether fails?

Let's play out a hypothetical scenario: what if USDT actually collapsed?

Given USDT's role as the primary trading pair and liquidity source for much of the crypto market, a Tether failure would be like removing a major highway from a city's transportation network. The immediate effects would likely include:

Market chaos: Traders scrambling to exit USDT positions would create massive selling pressure across crypto markets. We're talking about potentially the largest fire sale in crypto history, as billions of dollars worth of USDT holders try to convert to other assets simultaneously.

Liquidity crisis: Many smaller cryptocurrencies rely heavily on USDT trading pairs. Without this liquidity, some tokens might become effectively untradeable, at least temporarily.

Contagion effects: Other stablecoins might face runs as confidence in the entire sector erodes. Even well-managed stablecoins could struggle if everyone tries to redeem at once.

The silver lining: The crypto ecosystem has become more resilient over time. Alternative stablecoins like USDC have grown substantially, providing some redundancy. Additionally, the market has survived previous "extinction-level events" and adapted.

Conclusion: Is USDT worth the risk?

USDT isn’t perfect, but it’s proven its place in the crypto ecosystem. With high liquidity and global acceptance, it’s a practical choice for trading, payments, and short-term value storage.

However, concerns around transparency and regulatory clarity mean it’s not ideal for long-term holding or users who prioritise full visibility. But like any financial tool, its value depends on how you use it.

The smart approach is to understand the trade-offs, diversify across stablecoins, and align your choices with your goals and risk tolerance. As the space evolves, USDT remains useful, but it’s just one part of a broader digital finance strategy.

NEWS AND UPDATES

LATEST ARTICLE

Polkastarter represents one of the leading decentralised launchpad platforms in the blockchain ecosystem, focused on empowering early-stage crypto projects to raise funds and launch tokens. First launched in December 2020, it has established itself as a prominent player in the Initial DEX Offering (IDO) space, providing a secure and efficient environment for project launches.

The platform has facilitated the launch of over 100 projects, demonstrating its significant impact on the crypto funding landscape. Polkastarter also features a dedicated marketing team, including video production and design, providing support beyond just the technical infrastructure.

TLDR

Multi-chain launchpad: Polkastarter is a decentralised platform that enables crypto projects to conduct token sales and fundraising campaigns across multiple blockchain networks.

Fixed-price swaps: The platform's main offering is its fixed-swap smart contract, which allows projects to easily launch liquidity pools that execute orders at a fixed price, rather than using traditional AMM models.

Cross-chain support: Polkastarter currently supports Ethereum, BNB Chain, Polygon, Celo, and Avalanche, providing flexibility for projects across different ecosystems.

Native token (POLS): POLS serves as the platform's utility token, providing access to IDO participation, governance rights, and various platform benefits.

What is Polkastarter (POLS)?

Polkastarter is a decentralised launchpad platform designed to democratise access to early-stage crypto investments through Initial DEX Offerings (IDOs). The platform serves as a bridge between innovative blockchain projects seeking funding and investors looking for early access to promising tokens.

The platform's core innovation lies in its fixed-swap mechanism, which provides predictable pricing for token sales rather than the variable pricing models used by automated market makers. This approach offers greater transparency and certainty for both projects and investors during token launch events.

Beyond the launchpad functionality, Polkastarter runs an internal incubation and advisory program, bringing together experience and lessons learned from 100+ project launches to nurture and grow Web3 projects, helping to ensure that projects launched on the platform receive proper guidance and support.

The platform takes security seriously by carefully reviewing each project before allowing it to launch. This screening process helps ensure that only legitimate, high-quality projects reach investors, protecting users from scams and poorly developed tokens.

Who created Polkastarter?

Polkastarter was founded in 2020 by Daniel Stockhaus, Tiago Martins, and Miguel Leite. The founding team brought together diverse expertise in business development, technology, and product management to address the growing need for reliable fundraising infrastructure in the decentralised finance space.

Daniel Stockhaus serves as CEO and Co-founder, leading the platform's strategic direction and business development efforts. Under his leadership, the platform has grown from a startup concept to one of the most recognised launchpad platforms in the crypto industry.

The founding team recognised the challenges faced by early-stage crypto projects in accessing capital and the difficulties investors encountered in finding legitimate investment opportunities. Their solution was to create a platform that could serve both sides of this equation while maintaining high standards for security and project quality.

How does Polkastarter work?

Launchpad mechanism

To participate in token launches, users need to hold POLS tokens, with different amounts unlocking various access levels. The more POLS you hold, the better your chances of getting into popular launches and the more you can invest.

Projects set fixed prices for their tokens rather than using changing market prices. This means investors know exactly what they're paying and how many tokens they'll get before they invest.

Multi-chain infrastructure

Polkastarter works across several different blockchains, so projects can pick the one that best fits their needs. Some chains have lower fees, others are faster, and some have different user communities.

Project curation and support

As mentioned above, before any project can launch on Polkastarter, it goes through a thorough review process. The team checks the technology, verifies who's behind the project, and evaluates whether the business makes sense.

Projects also get help with marketing, strategy advice, and technical support to give them the best chance of success both during their launch and afterwards.

What Is POLS?

POLS is the native utility token of the Polkastarter ecosystem, serving a range of functions within the ecosystem:

- Tier access: Users must hold and stake POLS tokens to access different participation tiers in IDO launches, with higher holdings providing better benefits and guaranteed allocations.

- Governance rights: POLS holders can participate in platform governance decisions, voting on proposals that affect the platform's future development and policies.

- Staking rewards: Token holders can stake their POLS to earn rewards while maintaining their tier status for IDO participation.

- Platform fees: POLS can be used to pay for various platform services and may provide discounts on transaction fees.

How can I buy and sell POLS?

POLS tokens are available on Tap, allowing verified users to easily buy, sell, and trade the token. Before investing in POLS, we encourage you to consider how useful the token is on the Polkastarter platform and how much the launchpad space is growing. The token’s value depends largely on the platform’s success and how widely IDO fundraising is adopted.

Managing payments across borders remains one of the biggest operational challenges for expanding businesses. While digital transformation has touched nearly every aspect of commerce, international banking is currently lagging behind with separate systems for crypto and traditional currency transactions, creating unnecessary complexity.

Tap solves this problem by offering each business a multi-currency account with a dedicated IBAN that functions as a bridge between these two financial worlds. For businesses handling both crypto and fiat currencies, this means one unified system rather than juggling multiple accounts and conversion processes. This isn't just convenient - it directly impacts your bottom line by reducing transaction fees, speeding up settlements, and simplifying reconciliation.

If you're handling international payments or considering crypto adoption, this could significantly streamline your financial operations. Here's what you need to know.

What is a business IBAN?

An IBAN (International Bank Account Number) serves as your business's financial passport - a standardised identifier recognised across 78+ countries. Unlike traditional account numbers, a Business IBAN follows a structured format that includes country codes, bank identifiers, and your unique account number.

What sets Tap's approach apart is the integration of this established banking standard with crypto functionality. Instead of operating in parallel financial universes, your transactions (whether in euros, dollars, or Bitcoin) flow through a single identifiable channel.

For finance teams, this means the end of reconciliation nightmares. For your customers and partners, it means one consistent payment destination regardless of their preferred currency.

How Business IBANs Work

The mechanics behind modern business transactions

A Business IBAN functions as the digital coordinates for your company's financial location in the global banking ecosystem. When properly implemented, it creates a frictionless path for money to flow into and out of your business regardless of currency type or originating country.

Sending and receiving payments

When receiving payments, your Business IBAN acts as a universal identifier that works across different payment systems. Clients simply enter your IBAN (and sometimes BIC code) into their banking platform, eliminating the confusion of different account number formats across countries.

For outgoing payments, the process works in reverse. You provide the recipient's IBAN, specify the amount, and Tap's platform handles the routing complexities behind the scenes. This standardisation prevents the common errors that lead to payment delays and rejection fees.

What separates Tap's system from conventional banking is the integration layer that works with both crypto and traditional currencies. When a client pays in Bitcoin, for example, you can choose to receive it as cryptocurrency or have it automatically converted to your preferred fiat currency before it reaches your account.

Banking networks demystified

Business IBANs interact with several key payment networks:

SEPA (Single Euro Payments Area): Covering 36 European countries, SEPA processes euro-denominated transfers typically within one business day at low fixed costs. Your Business IBAN automatically routes euro payments through this network without requiring a separate setup.

SWIFT (Society for Worldwide Interbank Financial Telecommunication): The backbone of international banking, SWIFT connects over 11,000 financial institutions worldwide.

Real-world transaction example

Consider a UK-based e-commerce business receiving payment from a German customer:

- The customer initiates a €5,000 payment to the merchant's business IBAN

- The transaction enters the SEPA network and arrives in the merchant's Tap account within hours

- The merchant can either keep the funds in euros or convert to GBP at their preferred timing

- If choosing to convert, Tap executes the exchange at market rates with minimal spread

- The funds become available for business operations, supplier payments, or withdrawal

This same process that once required multiple accounts, banking relationships, and days of processing now happens automatically through a single business IBAN. For businesses managing dozens or hundreds of such transactions monthly, the efficiency gains and cost savings compound significantly.

The ability to handle these complex financial pathways through one unified system represents the core value proposition of modern business IBANs - simplicity on the surface, sophisticated routing underneath.

Cross-border advantages that impact your bottom line

The practical benefits of a business IBAN become immediately apparent in cross-border transactions:

- Reduced rejection rates: correctly formatted IBANs virtually eliminate payment failures due to incorrect account details

- Faster settlement times: direct routing through the SEPA network for European transactions

- Lower transaction costs: fewer intermediaries means fewer fees eating into your margins

- Simplified compliance: clearer transaction trails for more straightforward reporting

Bridging crypto and traditional finance

The crypto market now represents a $2 trillion opportunity that many businesses struggle to tap into due to technical and operational barriers. A business account with Tap eliminates these obstacles by providing:

- Seamless conversion between crypto and fiat currencies

- Consolidated financial reporting across all currency types

- Regulatory compliance built into the platform

- Reduced exposure to crypto volatility through instant conversion options

For businesses cautiously exploring crypto acceptance, this hybrid approach offers a low-risk entry point without requiring major infrastructure changes.

Implementation without disruption

Setting up a business account through Tap requires minimal operational changes:

- Fill in the contact form to initiate a callback

- Complete the business account set-up and verification process

- Receive your unique account with IBAN

- Update payment details with clients and suppliers

- Integrate with your existing accounting systems

The entire process typically takes less than 48 hours, with Tap's team handling the technical heavy lifting.

Is a Tap business account right for your growth strategy?

It's worth considering a business account if your company:

- Operates in multiple countries or currencies

- Needs to reduce payment processing costs

- Wants to accept crypto payments without complexity

- Are looking to streamline financial operations

As payment landscapes continue evolving, businesses that implement flexible, future-proof solutions gain a significant competitive advantage in customer experience and operational efficiency.

Explore how a business IBAN could fit into your financial infrastructure by visiting Tap's business solutions page, from where a dedicated account manager can discuss potential savings based on your specific transaction patterns.

The business world won't wait for outdated payment systems to catch up. The question isn't whether you need more efficient payment solutions - it's how quickly you can implement them.

Anyone who’s been here long enough can tell you that the crypto space has long been dominated by headlines about dramatic price swings, viral meme coins, and speculative trading frenzies. While these stories grab public attention, they overshadow a far more significant development: the steady construction of digital infrastructure that's quietly reshaping how we think about money, ownership, and global coordination.

This infrastructure (comprising protocols, networks, and platforms) represents the foundational layer upon which the future digital economy will be built. Understanding its importance requires looking beyond the noise of market speculation to examine the technological bedrock that makes decentralised applications, global finance, and new forms of digital cooperation possible.

Some will argue that the journey from surface-level crypto awareness to deep appreciation of its infrastructure parallels the early internet's evolution. Just as few people in the 1990s understood TCP/IP protocols while browsing the web, today's crypto users often interact with sophisticated infrastructure without recognising its complexity or potential. So, let’s go there.

Understanding crypto infrastructure

Crypto infrastructure encompasses the foundational systems that enable decentralised networks to function. At its core, this includes Layer 1 blockchains like Bitcoin and Ethereum, which serve as base settlement layers. Layer 2 solutions build on top of these foundations, provide faster transactions and reduced costs while still maintaining the security of the underlying chain.

Stay with me; beyond the blockchain layers themselves, crypto infrastructure encompasses decentralised storage networks, oracle systems that connect blockchains to real-world data, cross-chain bridges, and smart contract platforms that enable programmable money and automated agreements.

Here, the comparison to internet infrastructure development resurfaces. Just as the internet required foundational protocols like TCP/IP for data transmission and HTTP for web browsing, crypto requires its own stack of interoperable protocols. Ethereum's introduction of smart contracts in 2015 paralleled the web's evolution from static pages to dynamic applications, enabling what we now call Web3.

This infrastructure exhibits composability, allowing different protocols and applications to interact seamlessly, thereby creating network effects where each new component enhances the utility of existing ones.

For example, a decentralised exchange can integrate with a lending protocol, which connects to an insurance platform, all running on shared infrastructure and speaking the same digital language.

The role of infrastructure in real-world use cases

Let's take a look at perhaps the most mature application of crypto infrastructure: Decentralised finance (DeFi). Platforms like Uniswap have processed hundreds of billions in trading volume without traditional intermediaries, while lending protocols enable global credit markets operating 24/7 without geographic restrictions. Let the record state that these are not theoretical experiments: they're functioning financial systems serving millions of users.

Non-fungible tokens (NFTs), despite their heavy association with speculative art markets, demonstrate infrastructure capabilities for digital ownership and provenance. The underlying technology enables everything from supply chain tracking to digital identity verification, with applications extending far beyond collectables.

Looking at another example, Decentralised Autonomous Organisations (DAOs) showcase how crypto infrastructure can enable new forms of governance and coordination. Organisations like MakerDAO govern multi-billion-dollar protocols through token-based voting, while smaller DAOs coordinate everything from research funding to community management without traditional corporate structures.

Global remittances showcase the infrastructure's practical impact. Traditional international transfers often take days and attract significant fees, especially for users in developing nations. However, crypto infrastructure enables near-instant, low-cost transfers that bypass legacy banking systems, providing financial inclusion for underserved populations.

Looking further, storage networks like Filecoin and IPFS show us how crypto principles apply beyond finance. These systems create decentralised alternatives to centralised cloud storage, with cryptoeconomic incentives ensuring data persistence and availability without relying on corporate guarantees.

Finally (for now), oracle networks like Chainlink bridge the gap between blockchain systems and external data, enabling smart contracts to respond to real-world events. This infrastructure component is essential for applications ranging from crop insurance to prediction markets.

Why infrastructure trumps hype

Unfortunately, hype cycles are inevitable in emerging technologies. Let’s look at the internet again, which experienced multiple boom-bust cycles, from the dot-com bubble to social media speculation, yet the underlying infrastructure continued evolving throughout these times.

Crypto follows a similar pattern: speculative excess grabs headlines, but fundamental infrastructure development goes on regardless of market sentiment.

→ Layer 1 blockchain innovation continues advancing despite price volatility.

→ Ethereum's transition to proof-of-stake reduced energy consumption by over 99% while maintaining security.

→ New consensus mechanisms and scaling solutions emerge regularly, addressing earlier limitations through technological iteration rather than marketing promises.

Take Layer 2 scaling solutions for instance, these have matured significantly, with platforms like Arbitrum and Polygon processing thousands of transactions per second at fraction-of-a-penny costs without making front page news. These developments solve practical problems that enable broader adoption, creating value through utility rather than speculation.

Infrastructure ensures long-term utility by focusing on fundamental capabilities rather than short-term price appreciation. A robust smart contract platform retains value whether tokens cost $10 or $10,000, because its utility derives from enabling new applications and business models, not from speculative trading.

Public blockchains: root access for everyone

Now, for public blockchains. These provide something unprecedented in digital systems: root access for ordinary users. In traditional computing, root access gives complete control over a system, typically reserved for administrators. Public blockchains extend analogous privileges to anyone with an internet connection, enabling direct interaction with global financial infrastructure without permission from intermediaries.

This represents a fundamental shift in digital sovereignty. Users can hold assets, execute contracts, and participate in governance without relying on banks, corporations, or governments to maintain accounts or process transactions. The infrastructure operates according to transparent rules encoded in software rather than opaque policies subject to change.

Shared governance emerges naturally from this design, as protocol changes require community consensus, enabling systems to evolve through democratic participation rather than top-down corporate decision-making. Now, token holders can vote on upgrades, fee structures, and resource allocation, participating in economic governance at a scale previously impossible.

On top of this, interoperability benefits from shared standards and open protocols. This allows applications built on public infrastructure to integrate seamlessly, creating network effects that strengthen the entire ecosystem. Or a wallet application that works across multiple platforms, a lending protocol that can source liquidity from various exchanges, and identity systems that can port credentials between services.

This also means that censorship resistance can become a practical reality rather than a theoretical ideal. Transactions can now execute according to protocol rules rather than institutional policies, providing financial access to users regardless of political status, geographic location, or social standing. This infrastructure has proven particularly valuable for individuals in countries with capital controls or political instability.

Limitations and criticisms

We cannot celebrate the highs without addressing the lows. Firstly, scalability remains a significant challenge for blockchain infrastructure. Bitcoin processes roughly seven transactions per second, while Ethereum handles about fifteen, far below Visa's theoretical capacity of 65,000 transactions per second.

Of course, this comparison oversimplifies the trade-offs involved, as Layer 2 solutions and alternative consensus mechanisms continue improving throughput while maintaining decentralisation and security properties.

Another media-preferred limitation is energy consumption, particularly for proof-of-work systems like Bitcoin. What the media don’t reveal is that the narrative of excessive energy use often ignores several factors: Bitcoin mining increasingly uses renewable energy sources, proof-of-stake systems like Ethereum consume negligible energy, and the current financial system's energy footprint includes bank branches, data centers, and cash transportation networks rarely counted in comparisons.

Looking at governance, challenges can arise from the tension between decentralisation and coordination. Protocol forks like Bitcoin Cash and Ethereum Classic demonstrate how communities sometimes split over technical or philosophical disagreements. While these events can be disruptive, they also illustrate the system's ability to accommodate different visions rather than forcing consensus.

The Bank for International Settlements (BIS) has raised concerns about trust, scalability, and institutional integration in crypto systems. Their perspective highlights important considerations: public blockchains require users to trust cryptography and consensus mechanisms rather than institutional guarantees, scalability improvements often involve trade-offs in decentralisation, and integration with existing financial infrastructure remains complex.

However, many criticisms reflect misunderstandings about ongoing development. "Crypto is too slow" ignores Layer 2 innovations that achieve traditional payment system speeds while maintaining blockchain security guarantees. "Bitcoin uses too much energy" doesn't account for proof-of-stake alternatives or renewable energy adoption in mining operations.

Enter a new paradigm: the crypto economy

The crypto economy fundamentally shifts how digital systems create value. Traditional platforms extract wealth through data collection while users provide free content and attention. Crypto infrastructure flips this model: users own platform stakes, earn tokens for contributions, and participate in governance decisions.

This infrastructure operates without geographic boundaries. A Nigerian developer receives payment from a Swedish client through the same system enabling a Singapore DAO to fund global research. Smart contracts automate complex relationships: insurance pays out based on weather data, funds rebalance algorithmically, and revenue is distributed to thousands of contributors simultaneously.

The notion that "crypto will eat the digital economy" reflects the infrastructure's potential to reorganise systems around user ownership rather than platform extraction. This is proven by the fast rate at which decentralised alternatives are appearing, institutional blockchain adoption, and government exploration of digital currencies built on similar technologies.

Concluding thoughts

While speculation captures headlines, crypto infrastructure represents a quiet revolution in digital coordination and value transfer. Like the internet's lasting value came from enabling new applications rather than domain name speculation, crypto's impact will stem from infrastructure capabilities, not token prices.

This new infrastructure reshapes how we think about ownership, governance, and economic coordination in digital systems. It provides early examples of how future digital economies might grant users greater control and participation in the systems they use.

As this infrastructure matures, its influence will extend into areas we're only beginning to imagine. The quiet revolution of crypto infrastructure may ultimately prove more transformative than any speculative bubble, creating lasting change in how societies coordinate and create value in an increasingly digital world.

Welcome to Tap’s weekly crypto market recap.

Here are the biggest stories from last week (8 - 14 July).

💥 Bitcoin breaks new ATH

Bitcoin officially hit above $122,000 marking its first record since May and pushing total 2025 gains to around +20% YTD. The rally was driven by heavy inflows into U.S. spot ETFs, over $218m into BTC and $211m into ETH in a single day, while nearly all top 100 coins turned green.

📌 Trump Media files for “Crypto Blue‑Chip ETF”

Trump Media & Technology Group has submitted an S‑1 to the SEC for a new “Crypto Blue Chip ETF” focused primarily on BTC (70%), ETH (15%), SOL (8%), XRP (5%), and CRO (2%), marking its third crypto ETF push this year.

A major political/media player launching a multi-asset crypto fund signals growing mainstream and institutional acceptance, and sparks fresh conflict-of-interest questions. We’ll keep you updated.

🌍 Pakistan launches CBDC pilot & virtual‑asset regulation

The State Bank of Pakistan has initiated a pilot for a central bank digital currency and is finalising virtual-asset laws, with Binance CEO CZ advising government efforts. With inflation at just 3.2% and rising foreign reserves (~$14.5b), Pakistan is embracing fintech ahead of emerging-market peers like India.

🛫 Emirates Airline to accept crypto payments

Dubai’s Emirates signed a preliminary partnership with Crypto.com to enable crypto payments starting in 2026, deepening the Gulf’s commitment to crypto-friendly infrastructure.

*Not to take away from the adoption excitement, but you can book Emirates flights with your Tap card, using whichever crypto you like.

🏛️ U.S. declares next week “Crypto Week”

House Republicans have designated 14-18 July as “Crypto Week,” aiming for votes on GENIUS (stablecoin oversight), CLARITY (jurisdiction clarity), and Anti‑CBDC bills. The idea is that these bills could reshape how U.S. defines crypto regulation and limit federal CBDC initiatives under Trump-aligned priorities.

Stay tuned for next week’s instalment, delivered on Monday mornings.

We’re excited to share that XTP trading is officially back online in the Tap app!

Following the successful integration of ProBit, a trusted exchange that continues to support XTP, users can now trade seamlessly within the app once again. This marks an important step in restoring access and strengthening the trading experience for our community

We know that waiting isn’t always easy, and we want to sincerely thank you for your patience and continued support throughout this transition. Your trust drives everything we do.

As always, we’re working behind the scenes to bring you more ways to access and use XTP, stay tuned for what’s next.

The Tap team.

Building a solid investment portfolio isn't just about chasing hot stocks - it's about playing smart. In today's hasty financial world, knowing how to structure your investments and plan your strategies accordingly can make or break your financial goals. So let's dive into the essentials to help you level up your portfolio game.

What is an investment portfolio?

An investment portfolio is essentially your collection of financial assets - think stocks, bonds, ETFs, real estate, and other investments all working together toward your financial goals. It's not just a random assortment of investments you've picked up along the way; it's a carefully crafted strategy designed to balance risk and reward.

The magic happens through diversification. By spreading your money across different assets that react differently to market ups and downs, you're giving yourself a better shot at riding out the lows and capitalising on the highs. Think of it as crafting a playlist: you want a mix that works together, not one song on repeat.

Experts suggest that your portfolio should align with three key elements: your tolerance for risk, your expected returns, and your personal financial objectives. When these pieces fit together properly, your portfolio becomes a powerful tool for building wealth over time rather than just a collection of random investments hoping for the best.

Why building the right portfolio matters

The difference between a well-structured portfolio and a haphazard collection of investments can literally make or break your financial future. Poor portfolio construction often leads to unnecessary losses during market downturns, missed opportunities during growth periods, and sleepless nights worrying about your financial security.

On the flip side, a thoughtfully built portfolio acts as your financial foundation - steady enough to weather storms while positioned to capture growth when markets are favourable. It's about creating a strategy that matches your personal goals and risk tolerance, not following the latest investment trend or copying what worked for someone else.

Success in investing starts with a framework tailored to you - your goals, risk tolerance, income needs, and even your personal values. It's not about the fanciest strategy; it's about one you understand and can stick to through market ups and downs.

How to build an investment portfolio

Step 1: Define your investment goals and time horizon

Before you buy your first stock or bond, you need to get crystal clear on what you're investing for. Are you building toward retirement in 30 years? Saving for a house down payment in five years? Planning for your kids' education? Each goal requires a different investment approach.

Your time horizon is crucial here. Long-term goals (10+ years) can handle more volatility because you have time to ride out market cycles. Short-term goals (under 5 years) need more conservative approaches since you can't afford to lose money right when you need it.

Here's how time influences your strategy: if you're 25 and investing for retirement, you can afford to be more aggressive with growth-focused investments. But if you're 55 and need that money in 10 years, you'll want a more balanced approach with some stability mixed in.

Connect your goal-setting to your risk profile. Aggressive growth goals require accepting higher volatility, while conservative income goals call for steadier, lower-risk investments. Many investors aim to align their goals, timeline, and risk tolerance to create a more coherent strategy.

Step 2: Understand your risk tolerance

Risk tolerance isn't just about how much money you can afford to lose - it's about how much volatility you can stomach without making emotional decisions that hurt your long-term success. Some investors sleep soundly while their portfolio swings 20% up or down; others lose sleep over 5% movements.

Ask yourself: How would you feel if your portfolio dropped 25% in a year? Would you panic and sell everything, or would you see it as a buying opportunity? Your honest answer reveals more about your risk tolerance than any questionnaire.

Conservative investors typically prefer stability over growth potential. They're comfortable with lower returns in exchange for predictable outcomes and fewer sleepless nights. Aggressive investors, on the other hand, are willing to accept significant ups and downs for the potential of higher long-term returns.

Consider using this simple scale: if market volatility makes you constantly check your account and lose sleep, you're probably a conservative investor. If you can ignore short-term swings and focus on long-term trends, you might be more aggressive. Most people fall somewhere in between - and that's perfectly fine.

Step 3: Choose your asset allocation

According to several studies, asset allocation has been shown to explain the majority of return variability in a portfolio.. This is where you decide how to split your money between different asset classes based on your goals and risk tolerance.

The main asset classes include:

- Equities: Stocks and ETFs offer growth potential but come with higher volatility

- Fixed income: Government and corporate bonds provide stability and steady income

- Real assets: Real estate and commodities help hedge against inflation

- Cash & equivalents: Keep this for liquidity and as a safety net

- Alternative investments: Private equity, hedge funds, and digital assets add diversification

Strategic allocation sets your long-term targets (like 70% stocks, 30% bonds), while tactical allocation allows for short-term adjustments based on market conditions. Most successful investors stick primarily to their strategic allocation.

Here are three examples of diversification in portfolios:

- Cautious: 40% stocks, 50% bonds, 10% cash - prioritises stability

- Balanced: 60% stocks, 30% bonds, 10% alternatives - moderate growth with some protection

- Adventurous: 80% stocks, 15% alternatives, 5% cash - maximum growth potential

Remember, there's no universally "right" allocation - only what's right for your specific situation and goals. Please contact a financial advisor for portfolio recommendations specific to you.

Step 4: Diversify within asset classes

Once you've set your overall asset allocation, it's time to diversify within each category. This means spreading your risk across different sectors, regions, company sizes, and investment styles rather than putting all your money into similar investments.

For your stock allocation, consider diversifying across:

- Sectors: Don't overload on tech or any single industry

- Geography: Mix domestic and international markets

- Market cap: Blend large, mid, and small-cap companies

- Investment styles: Combine growth and value approaches

Bond diversification works similarly. Mix different types of bonds like corporate bonds for yield, government bonds for safety, and varying maturities from short-term to long-term. Municipal bonds can add tax advantages for higher-income investors.

Geographic diversification helps reduce the impact of local economic problems. If the U.S. market struggles, international investments might still perform well. Sector allocation prevents you from getting crushed if one industry hits hard times - remember how concentrated tech portfolios suffered in 2022.

The goal isn't to own everything, but to avoid having your entire portfolio's success dependent on any single factor. This approach helps smooth out returns over time and reduces the chance of catastrophic losses.

Step 5: Pick your investments (stocks, funds, ETFs, etc.)

Now comes the tactical phase: choosing specific investments within your allocation framework. You've got several options, each with distinct advantages and drawbacks.

Individual stocks give you complete control and the potential for outsized returns, but they require significant research and carry higher risk. Unless you're prepared to thoroughly analyse companies and monitor your holdings regularly, individual stocks probably shouldn't dominate your portfolio.

Mutual funds offer professional management and instant diversification. Active funds try to beat the market through stock picking and timing, while passive funds simply track market indexes. The trade-off? Active funds charge higher fees and rarely beat their benchmarks long-term.

ETFs combine the best of both worlds: broad diversification like mutual funds with the flexibility to trade like stocks. They typically have lower fees than mutual funds and offer exposure to virtually any market segment you can imagine.

Pay attention to fees - they compound over time and can significantly impact your returns. A fund charging 1.5% annually will cost you much more over decades than one charging 0.1%. Low-cost index funds and ETFs are often favoured by long-term investors for their diversification and lower fees.

Step 6: Consider tax implications and account types

Taxes can seriously eat into your investment returns if you're not strategic about account types and asset location. The key is understanding which investments to hold in which accounts.

Tax-deferred accounts let your investments grow without annual tax consequences, but you'll pay taxes when you withdraw. On the other hand, for some accounts you pay tax upfront and enjoy tax-free growth down the line. Be sure to fully understand the tax implications before investing.

Taxable accounts offer flexibility since you can access your money anytime, but you'll owe taxes on dividends and capital gains each year. The trick is putting the right investments in the right accounts.

Some investors choose to place tax-inefficient assets in tax-deferred accounts to potentially reduce tax drag.

Asset location strategy can add significant value over time.

Step 7: Monitor and rebalance your portfolio regularly

Your portfolio isn't a 'set-it-and-forget-it' deal - it needs regular check-ins to stay aligned with your goals. Market movements will naturally shift your allocation over time, and your personal situation will evolve too.

Rebalancing means adjusting your holdings back to your target allocation. If stocks have performed well and now represent 80% of your portfolio instead of your target 70%, you'd sell some stocks and buy more bonds to get back on track.

You can rebalance on a schedule (annually or quarterly) or when your allocation drifts beyond certain thresholds (like 5% away from targets). Both approaches work - consistency matters more than the exact method.

Some investors use tax-loss harvesting to offset gains and manage capital gains taxes, though results depend on individual tax situations.

Remember, the goal isn't perfect timing or constant tweaking. It's maintaining discipline and keeping your portfolio working toward your long-term objectives rather than getting caught up in short-term market noise.

Common mistakes to avoid when building a portfolio

Even experienced investors fall into these traps, but knowing what to watch for can keep you on track.

Emotional decision-making tops the list. Market swings can spark impulsive choices, but sticking to your strategy is what separates successful investors from the crowd. Discipline beats panic every time. When markets crash, successful investors either stay the course or see buying opportunities.

Insufficient diversification is another classic mistake. Putting all your money into familiar assets or one sector might feel safe, but it leaves you exposed to unnecessary risks. Spread it out across different asset classes, sectors, and geographies to protect yourself.

Overconfidence bias catches many investors who've had recent success. Just because you've had wins in the past doesn't mean you've cracked the market code. Markets change constantly - stay humble, adaptable, and stick to proven principles rather than assuming you can consistently beat the market.

Don't forget about fees and taxes either. High-cost investments and tax-inefficient strategies can quietly drain your returns over time, making a huge difference in your long-term wealth building.

The bottom line

Portfolio management is a journey, not a one-time task. By focusing on the essentials, staying disciplined, and avoiding common pitfalls, you can build a portfolio that works toward your goals and lets you sleep easily at night. Remember, the best portfolio is one you understand and can stick with through all market conditions - that consistency will serve you far better than any complex strategy you can't maintain.