November 2025 could be a turning point for crypto. From ETFs to major network upgrades, here are six catalysts that could shape the market.

Keep reading

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

1. Seasonality & Historical Momentum Could Kick In

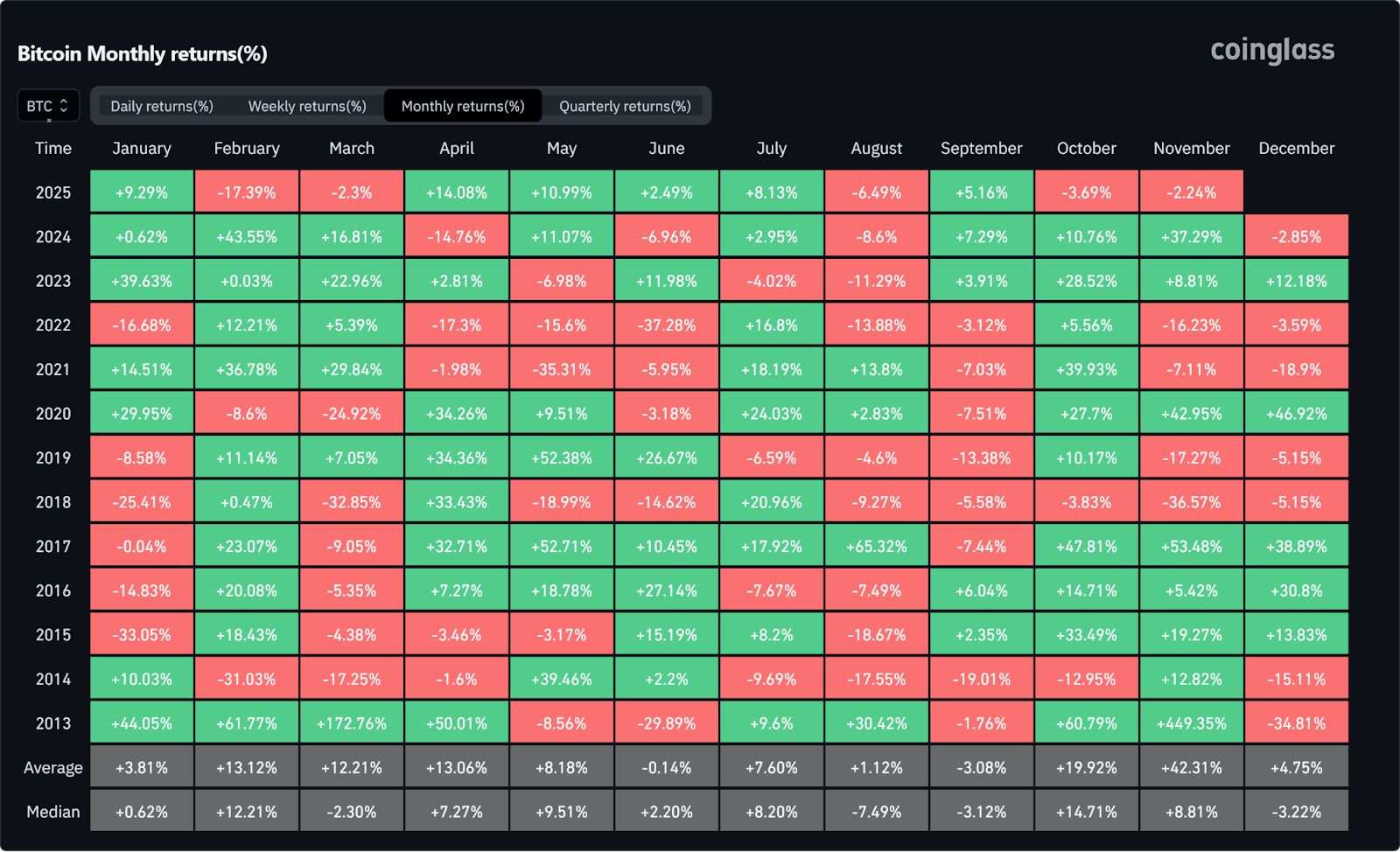

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

4. Altcoins at an Inflection Point

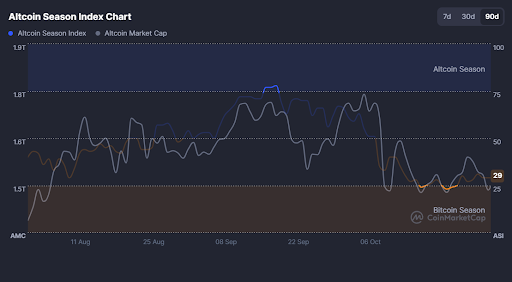

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

NEWS AND UPDATES

LATEST ARTICLE

TON (The Open Network) is a new blockchain system created by the team behind Telegram. Making waves in the industry, the network aims to solve common problems with existing blockchain, notably:

- Scalability: handling more transactions

- Speed: processing transactions faster

- Usability: making it easier for people to use

TON's core component is the TON blockchain, on top of which the TON ecosystem exists. By tackling these issues, TON hopes to make blockchain more practical and widely used. It wants to turn blockchain from just an interesting idea into something that can be used in the real world.

The story behind TON

TON's story began in 2018 when Telegram, the popular messaging app, announced its ambitious blockchain project. Founded by brothers Pavel and Nikolai Durov, TON was envisioned as a fast, secure, and scalable blockchain platform.

The Durovs aimed to create a decentralized network that could handle millions of transactions per second, making it suitable for global adoption. Their vision included adding a new cryptocurrency called Gram to Telegram. This would let Telegram users send money and use blockchain apps right from the messaging app.

Despite facing regulatory hurdles in 2020, which led Telegram to officially step back, the project found new life. The TON community took over development and since then, TON has achieved several milestones, including mainnet launch and growing ecosystem support.

The TON blockchain architecture

TON uses a multi-chain architecture with two main parts: the TON masterchain and workchains. The masterchain, the backbone of the system, handles important tasks like updating protocols, validating transactions, and managing interactions between different chains.

The workchains are smaller, customizable networks that can run on their own and are used for various purposes. Then there are shard chains which split up work for faster processing. This setup helps TON handle lots of transactions quickly.

The TON ecosystem is anchored by TON Coin (TON), used for gas fees, processing costs, and storage payments. It is also essential for becoming a blockchain validator.

This coin powers various applications and services built on TON, enriching its functionality while smart contracts let people create automated agreements and apps, used for things like online payments or voting systems.

These smart contracts are run by the TON Virtual Machine (TVM), designed to be fast and use less energy than other systems. This makes TON more efficient and easier to use for developers.

Key features of TON

Decentralised

TON isn't run by one company or group, instead, it's controlled by a community of users and developers. This makes it resistant to anyone taking it over or shutting down the network.

Interoperability

TON is able to connect with other blockchain networks and dapps. This allows users to easily move things like money or data between different systems.

Scalability

TON can handle lots of transactions at once. It does this by splitting into smaller interconnected blockchains called "shards." Each shard works on its own, allowing TON to process millions of transactions per second.

Fast transactions

TON is built for speed. It uses a system that's faster and uses less energy than older ones like Bitcoin. This means you can use TON for everyday things like buying coffee or sending money to friends.

The many uses of TON

TON’s versatile architecture lets users build a wide range of services and decentralized applications (dapps). As a community-driven project, its ecosystem is constantly expanding with new services. Here are some key uses:

- Payments and Transfers

TON facilitates quick and secure financial transactions. Its high speed is ideal for peer-to-peer transfers and online purchases, allowing merchants to accept cryptocurrencies seamlessly.

- Gaming

The gaming sector can use TON’s fast transactions and smart contracts to develop decentralized games and in-game economies, offering new opportunities for developers and players. The network hosts the likes of JetTon Games and Hamster Kombat.

- Decentralized Finance (DeFi)

TON’s scalability and security support DeFi applications like lending platforms and decentralized exchanges, handling large volumes of transactions effectively.

- Content Distribution

TON enables the creation of decentralized content platforms for video streaming and file sharing, ensuring fast and secure content delivery.

- Social Media and Messaging

With integration into Telegram, TON supports decentralized social media and messaging apps, providing enhanced security and a variety of mini-apps and services.

Conclusion

TON (The Open Network) is a major step forward in blockchain technology, solving problems like slow speeds and limited scalability. Started by Telegram’s founders, TON has grown into a community-driven platform with a smart design and many uses. It aims to make blockchain practical and widely used in everyday life.

Much like traditional ATMs, Bitcoin ATMs are specialized ATMs that allow users to buy or sell Bitcoin using cash, bank transfers or debit cards. These machines provide a convenient way to exchange traditional currency for cryptocurrency, or vice versa. In this article, we’re doing a deep dive on everything you need to know about using Bitcoin ATMs, including how to find one.

The benefits of using a Bitcoin ATM

There are a number of reasons one might look to use a Bitcoin ATM instead of an exchange or wallet app.

- Accessibility & Convenience

Easily buy and sell Bitcoin without complex online processes.

Located in high-traffic areas, easy to access.

- Instant transactions

No waiting for bank transfers or exchange processing.

- No bank account needed

Accessible to unbanked or underbanked individuals.

Provides a reliable option where traditional banking is unavailable.

Security concerns when using a Bitcoin ATM

Bitcoin ATMs offer a quick, accessible way to enter the cryptocurrency market, especially for those seeking more privacy or lacking traditional banking options. However, there are also downsides one should be aware of:

- Fraud and theft risks

ATMs can be targets for criminals. Always be aware of your surroundings and use ATMs in well-lit, public areas.

- Secure your Bitcoin wallet

Ensure that your Bitcoin wallet is ironclad, using strong passwords with two-factor authentication. Also, ensure that if using an exchange wallet that the platform is reliable and regulated.

- Tips for safe Bitcoin ATM transactions

- Verify all transaction details before confirming

- Don’t share sensitive information with anyone

- Don't accept help from strangers

- Keep your receipt

- Monitor your wallet for discrepancies

By staying alert and following these precautions, you can safely use Bitcoin ATMs while minimizing security risks.

Fees associated with using a Bitcoin ATM

Bitcoin ATM fees typically consist of transaction fees (usually a percentage) and network fees for Bitcoin transfers. These rates can vary significantly between ATMs and operators, so it's best to use online comparison tools to find the best deals.

To minimize costs, consider using ATMs with lower fees, even if they're less convenient. And note that conducting larger transactions can reduce the impact of flat fees, while alternative methods might be more cost-effective for smaller amounts.

Keep in mind that Bitcoin ATM fees are generally higher than those on online exchanges, so always check the fee structure before transacting to avoid unexpected costs.

How to find a Bitcoin ATM near me

Finding a Bitcoin ATM near you is easier than you might think, with various online tools and local resources at your disposal. Whether you prefer using Google, mobile apps, or exploring your local area, there are multiple ways to find a Bitcoin ATM near you.

- Online directories and maps

• Use websites like Coin ATM Radar or Bitcoin.com ATM Map

• Enter your location to find nearby ATMs

• Filter results by buy/sell options and supported cryptocurrencies

- Mobile apps

• Download apps like Bitcoin ATM Map or CoinATMRadar

• Enable location services for real-time nearby ATM info

• Get directions and ATM details on-the-go

- Local businesses and retail locations

• Check convenience stores, gas stations, and shopping malls

• Ask cryptocurrency-friendly businesses for recommendations

• Look for Bitcoin ATM signage in high-traffic areas

Remember to verify the ATM's legitimacy and compare fees before you use one. Not all Bitcoin ATMs are created equal, do your research.

How to use a Bitcoin ATM for buying/selling crypto

Once you’ve DYOR and found a reliable Bitcoin ATM, using it is straightforward. To buy or sell cryptocurrency, start by selecting your transaction type on the machine's interface.

You'll typically need to verify your identity by scanning an ID or entering a phone number, depending on the amount you’d like to buy or sell and your local regulations. Next, enter your wallet address or scan its QR code.

For buying, insert cash and for selling, send Bitcoin to the provided address. Once the transaction is processed, you'll receive a confirmation and receipt. Keep this safe until the Bitcoin has been deposited into your wallet.

As with any crypto transaction, always double-check all details before finalizing your transaction.

An easier alternative: Tap into the future

Why hunt for Bitcoin ATMs when you can have an all in one crypto app in your pocket? The Tap app revolutionizes how you can buy and sell cryptocurrencies. No more searching for ATMs or carrying cash - simply open the app and trade a wide range of digital assets instantly.

With high-grade security and the freedom to transact anywhere, anytime, Tap offers unparalleled convenience. Enjoy lower fees, a sleek interface, and portfolio management in one secure location (your phone).

Whether you're a crypto novice or a seasoned trader, Tap delivers a seamless experience that traditional ATMs can't match. Ready to upgrade your crypto game? Tap into the future of digital asset trading.

The crypto market has entered a phase that veterans often call the "boring zone." It's a time when:

- Bitcoin's price seems stuck, fluctuating between $50,000 and $70,000 for months.

- Altcoins are in an even deeper slumber, with many down 50-80% from their peaks.

- Trading volumes on major exchanges have plummeted, dropping 30% from the last bull market's heights.

Sound familiar? It should. This lull is a recurring theme in the crypto market cycle, and historically, it's often the calm before the storm. It’s also a common attribute after a recent Bitcoin halving.

Let's look at what happened after previous Bitcoin halvings:

- 2012 Halving: 92 days until new all-time high

- 2016 Halving: 291 days until new all-time high

- 2020 Halving: 216 days until new all-time high

For perspective, 28 July 2024 marks 100 days from the most recent halving, with 25 February 2025 marking the 300-day mark.

The power of patient investing

Investing in cryptocurrencies over longer time horizons can be likened to early-stage venture investing, where patience could potentially lead to significant returns. While past performance doesn't guarantee future results, historical examples like Ethereum and Solana demonstrate this potential.

Ethereum, launching at less than $1 in 2014, and Solana, starting below $1 in 2020, have since seen their values grow to over $3,000 and $140 respectively as of early 2024.

In the crypto space, what’s known as the HODL approach, emphasises the power of time and compound growth, similar to that of traditional asset classes. The idea is straightforward: if you've taken a position in a project you believe has strong fundamentals, maintaining that position through periods of high volatility could potentially lead to significant gains.

To illustrate this point further, in 2010, Bitcoin was worth less than $0.01. By April 2024, it had reached around $70,000. An investor who bought $100 worth of Bitcoin in 2010 and held it until 2024 would have seen their investment grow to millions of dollars.

Strategies for surviving (and thriving) in the "boring zone"

During quiet periods in crypto dive deeper into blockchain fundamentals, research promising projects, instead of anxiously checking prices or reacting to every piece of news, use this time productively.

Alternatively, for those with capital to invest, dollar-cost averaging (DCA) could be something to consider. A Vanguard study found that DCA outperformed lump-sum investing in 68% of cases during market downturns, highlighting its potential effectiveness in notoriously volatile markets.

Know with certainty that this "boring zone" is often temporary. Based on previous cycles, we might see a new Bitcoin all-time high in 30 to 150 days, and once Bitcoin breaks its previous record, top altcoin projects have historically seen gains of 200% to 1,000%.

By staying patient and disciplined during quiet periods, you can be prepared for potential opportunities that may arise as the crypto market evolves. Remember, while historical patterns offer insights, they don't guarantee future results, but these historical patterns are worth considering as you plan your strategy.

We get it, the waiting game is hard

Holding onto your crypto during boring market times can be tougher than you'd think. When prices aren't moving much, it's easy to get antsy or start doubting your choices. But keeping a cool head and being rational is key to long-term success.

First off, remember why you got into crypto in the first place. Was it the tech? The potential? Keep that big picture in mind. It helps to set realistic expectations too - crypto's known for its ups and downs, so flat periods are normal.

Try to limit how often you check prices. Constantly peeking at your portfolio can drive you nuts during slow times. Instead, focus on other parts of your life or dive deeper into learning about blockchain.

Connecting with other crypto fans can help too. Chat about ideas, not just prices. And don't forget to celebrate small wins - even if the market's quiet, projects are still developing and growing.

Stay patient, stay curious, and remember: in crypto, today's boredom could be tomorrow's excitement.

Chances are you've come across the terms "on-chain" and "off-chain," but what exactly do they mean? Our article dives into the differences between on-chain and off-chain cryptocurrency transactions, helping you grasp these fundamental concepts. Let's delve into their definitions, importance, and critical differences.

Brief explanation of how blockchain technology works

Before we dive in, let's quickly cover the basics of blockchain technology. Blockchain, the underlying technology of cryptocurrencies, operates as a decentralised ledger that records transactions across a network of computers. Each cryptocurrency uses its own blockchain, storing the relevant information pertaining to the transactions that take place on the network.

When a transaction occurs, it's verified by network participants, added to a block, and then added to the chain. This process of data storage ensures transparency, as each transaction is publicly recorded once validated and cannot be altered retroactively.

Additionally, the decentralised nature of blockchain enhances security by eliminating the need for a central authority to oversee transactions.

For a more detailed explanation, please see our What is Blockchain article.

Difference between on-chain and off-chain transactions

In a nutshell, on-chain transactions occur directly on the blockchain network, where transaction data is recorded and confirmed by network parties. In contrast, off-chain transactions happen outside the blockchain network, typically facilitated by centralised intermediaries.

On-chain transactions rely on blockchain technology for verification and record-keeping, ensuring transparency and security. These are conducted through Proof of Work (used by Bitcoin) or Proof of Stake (used by Ethereum) consensus mechanisms, ensuring trustless transactions. While secure, they often face scalability issues.

Off-chain transactions, on the other hand, involve private databases or alternative payment channels to facilitate transactions faster and with lower fees. These are typically conducted on Layer-2 solutions, a secondary blockchain network that alleviates the strain on the main chain by managing a portion of its functionalities. This is used to increase scalability and efficiency.

While on-chain transactions are inherently decentralised and immutable, off-chain transactions may offer greater scalability and privacy, albeit with some trade-offs in terms of trust and security.

Transaction speed and fees

When it comes to transaction speeds, it's worth noting that these typically vary between on-chain and off-chain transactions. On-chain transactions, directly processed on the blockchain, can be slower due to network congestion and verification processes.

In contrast, off-chain transactions, facilitated outside the main blockchain, often offer faster processing times, especially in payment channels or layer 2 solutions.

However, on-chain transactions typically incur higher fees due to network congestion and the computational resources required for verification. Off-chain transactions, leveraging centralised intermediaries or sidechains, may have lower fees but could compromise decentralisation and security.

The trade-off between speed and fees depends on the specific use case and desired level of decentralisation a user desires.

Security considerations to consider

On-chain transactions, being directly processed on the blockchain, benefit from inherent decentralisation and immutability, enhancing security. However, they are susceptible to network attacks and vulnerabilities in smart contracts.

Off-chain transactions, while offering scalability and speed, often rely on trusted intermediaries, raising concerns about centralization and potential breaches. Despite this, off-chain solutions implement security measures such as encryption and multi-signature authentication to mitigate risks.

Ultimately, the choice between on-chain and off-chain transactions depends on balancing security considerations with scalability and efficiency requirements in the context of specific use cases.

On-chain and off-chain transactions in terms of cryptocurrency wallets

When it comes to understanding how crypto wallets work for on-chain and off-chain transactions, it's essential to grasp their role in storing and facilitating cryptocurrency transactions. For on-chain transactions, wallets interact directly with the blockchain, securely managing digital assets on the network, while off-chain transactions may require specialised wallets that enable interactions outside the main blockchain, offering features like payment channels or compatibility with layer 2 solutions.

Choosing the right wallet depends on factors like security, compatibility, and functionality for each transaction type.

Conclusion

In summary, it's crucial to understand the key differences between on-chain and off-chain transactions when engaging with the crypto ecosystem.

While on-chain transactions offer decentralisation and immutability, these can be slower and costlier. Off-chain transactions, on the other hand, provide speed and scalability but may compromise security.

Choosing the right method depends on balancing factors like security, cost, and speed. Thus, it's essential to consider these aspects to optimise cryptocurrency transactions and ensure they meet specific needs in the ever-evolving blockchain landscape.

.webp)

RFID (radio frequency identification) credit cards are payment cards that use radio frequency technology for contactless payments. While the technology has been around since 1973, these cards have only recently gained increasing popularity, with many major credit card issuers offering RFID-enabled cards as the default option. The rise of RFID credit cards has been driven by consumer demand for faster, more convenient payment experiences.

You can spot RFID credit cards easily by the unique logo on the card, resembling a Wi-Fi symbol. This icon indicates that the card has RFID technology that allows contactless, tap-and-go payments. Seeing this logo, consumers can swiftly identify RFID-enabled cards, distinguishing them from traditional magnetic stripe cards.

How RFID credit cards work

RFID technology in credit cards is designed to allow for quick, convenient contactless payments. So, when buying an item you simply need to tap or wave your RFID-enabled card near a payment terminal, which initiates the card's embedded RFID chip to communicate with the reader using radio frequency signals.

This wireless communication allows the reader to securely access the necessary payment information, such as the card number and expiration date, without physically swiping or inserting the card. Exchanging this data over a short distance facilitates fast, frictionless transactions for consumers.

Compared to traditional card insertion or swiping techniques, this wireless payment method significantly streamlines the checkout process.

Security features of RFID cards

RFID credit cards offer strong security to prevent fraud and theft. They use advanced encryption protocols to protect payment data, ensuring it stays safe during transactions, so even if the signal is intercepted, the information remains unreadable to unauthorised parties.

Additionally, many RFID credit cards feature built-in anti-skimming technology to prevent card information from being illegally accessed or cloned. These security measures provide customers with peace of mind when making contactless payments.

RFID credit cards vs traditional magnetic stripe cards

RFID credit cards offer significant advantages over traditional magnetic stripe cards. With contactless payment capabilities, RFID cards provide a more secure and convenient payment experience. The wireless, encrypted communication between the RFID chip and the reader helps prevent fraud, as card data is less exposed compared to magnetic stripe cards that require physical swiping. Additionally, RFID transactions are faster and more seamless, reducing checkout times for consumers.

As RFID technology continues to mature and become more widely adopted, it's expected that RFID credit cards will become the new standard. Consumers are increasingly demanding the speed and convenience of contactless payments, and merchants are rapidly upgrading their infrastructure to accept RFID transactions. The migration towards RFID credit cards is a clear industry trend that is likely to accelerate in the coming years.

RFID credit cards and contactless payment methods

RFID credit cards are just one type of contactless payment method, which also includes mobile wallets and wearable devices. While these all leverage wireless technology for faster, more convenient transactions, RFID credit cards offer a uniquely familiar payment experience for consumers.

Compared to mobile or wearable contactless options, RFID credit cards provide the same familiar feel as traditional cards, with the added benefit of quicker, more secure transactions. However, mobile wallets and wearables offer additional functionality, like the ability to store multiple payment cards digitally.

Ultimately, both RFID credit cards and other contactless payment methods are driving the shift towards a more seamless, frictionless payment landscape. Consumers now have more choice than ever when it comes to fast, convenient ways to make purchases.

Benefits of using RFID credit cards for payments

Using RFID credit cards offers numerous benefits for both consumers and merchants. The tap-and-go convenience of RFID payments streamlines the checkout process, reducing transaction times compared to traditional swiping or inserting cards. This increased speed and efficiency can be especially advantageous in fast-paced environments like quick-service restaurants or transit systems.

Moreover, the enhanced security features of RFID cards, such as encrypted data transmission and anti-skimming technology, help protect against fraud. Businesses that accept RFID payments report reduced incidences of chargebacks and improved customer trust.

Overall, the combination of convenience and security makes RFID credit cards an attractive payment option for consumers and merchants alike.

Closing thoughts

In conclusion, RFID credit cards are revolutionising the payment landscape by offering a more convenient, secure, and streamlined payment experience for both consumers and merchants. As the adoption of this technology continues to grow, RFID credit cards are poised to become the new standard in the credit card industry.

If you're new to the world of cryptocurrency, you might have heard the term "spot trading" thrown around. Don't worry if it sounds confusing – we're here to break it down for you in simple terms.

What is spot trading?

Spot trading is one of the most basic and common ways to buy and sell cryptocurrencies. The word "spot" refers to the fact that these trades happen immediately, or "on the spot." When you do a spot trade, you're buying or selling a cryptocurrency at its current market price.

Think of it like buying groceries at a supermarket. You see the price of an apple, decide if you want to buy it, and if you do, you pay for it right away and take it home. That's essentially what spot trading is in the crypto and financial world.

How spot trading works

Here's a step-by-step breakdown of how spot trading typically works:

- Choose a cryptocurrency exchange: This is like picking your supermarket.

- Create an account and verify your identity: Most reputable platforms require this to prevent fraud.

- Deposit funds: You'll need to transfer money (usually traditional currency like euros) into your exchange account.

- Select the cryptocurrency you want to trade: Let's say you want to buy Bitcoin, check its value.

- Place an order: Enter the amount of Bitcoin you would like to buy and confirm the trade.

- Receive your cryptocurrency: The Bitcoin you bought will appear in your exchange wallet.

That's it! You've just completed a spot trade.

Advantages of spot trading

Spot trading offers several advantages, particularly for beginners. Its primary benefit is simplicity – the process is straightforward and easy to grasp, making it an ideal starting point for those new to the industry.

Another key advantage is immediate ownership, when you make a spot trade, you receive your cryptocurrency right away, giving you instant control over your digital assets. Spot trading also tends to have lower fees compared to some other trading methods.

Lastly, spot trading provides excellent price transparency. You always know exactly what price you're paying for your cryptocurrency, which can help you make more informed decisions about when to buy or sell.

Things to keep in mind

While spot trading is relatively simple, there are a few important points to remember:

- Volatility

Cryptocurrency prices can change rapidly, this could equate to both profit or loss, so always check.

- Fees

Always check the exchange's fee structure, and carefully review it before executing a transaction. Even small fees can add up over time.

- Security

Keep your account secure with strong passwords and two-factor authentication.

- Don't invest more than you can afford to lose

Cryptocurrency markets can be unpredictable so always stick to this golden rule.

Spot trading vs. other types of trading

You might hear about other types of crypto trading, like futures or margin trading, but be aware that these are more complex and often riskier. Spot trading is generally considered the safest and most straightforward option for traders.

Remember, the crypto market never sleeps – it's open 24/7. This means you can spot trade anytime, but it also means prices can change at any moment.

Conclusion

Spot trading is your entry point into the world of cryptocurrency trading. It's simple, immediate, and gives you full control over your crypto assets. As with any investment, make sure to do your research and understand the risks involved.