November 2025 could be a turning point for crypto. From ETFs to major network upgrades, here are six catalysts that could shape the market.

Keep reading

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

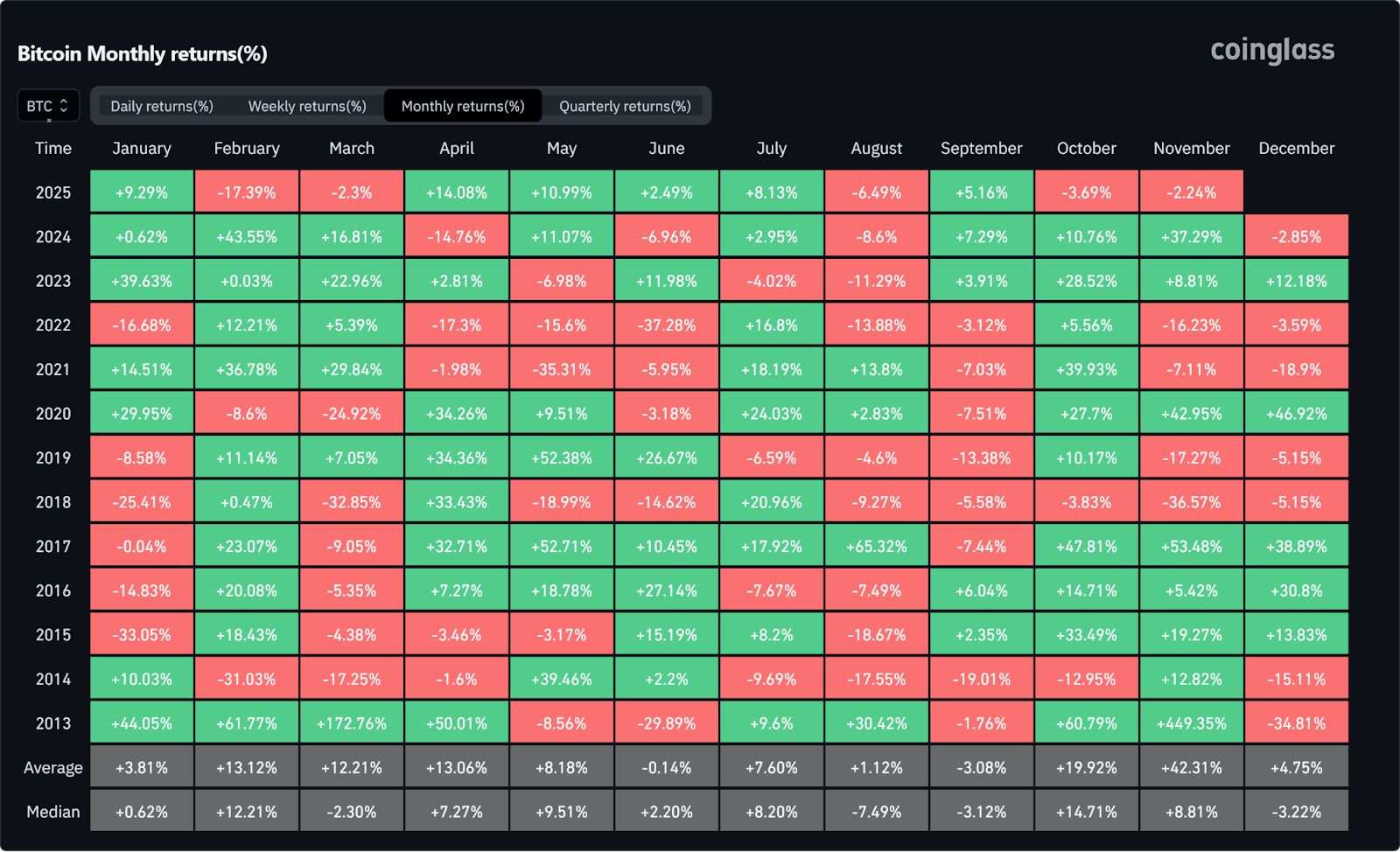

1. Seasonality & Historical Momentum Could Kick In

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

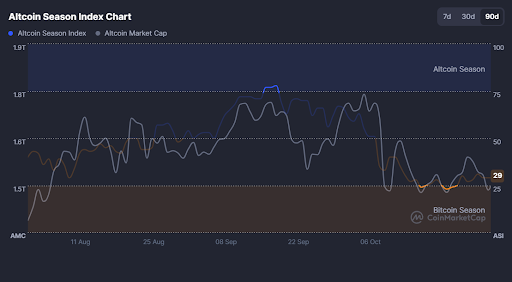

4. Altcoins at an Inflection Point

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

NEWS AND UPDATES

LATEST ARTICLE

Ever wondered how cryptocurrency prices are worked out on exchanges? The answer lies in a powerful tool called an order book. Think of it as a real-time snapshot of what is happening in the crypto market, showing exactly who wants to buy and sell at what prices.

In this article, we explain everything you need to know about crypto order books and how they fit into your crypto journey.

Understanding the basics: what is a crypto order book?

A crypto order book is like a dynamic ledger that displays all pending buy and sell orders for a specific cryptocurrency on an exchange. Imagine it as a marketplace where buyers and sellers gather, each stating their desired prices. The order book continuously updates in real-time, keeping a live record of the ever-changing supply and demand dynamics.

How does a crypto order book work?

The order book is divided into two main sections:

- Bid Orders (Buy Side)some text

- Shows prices traders are willing to pay

- Typically displayed in green

- Higher bids appear at the top

- Ask Orders (Sell Side)some text

- Shows prices traders want to sell at

- Usually displayed in red

- Lower asks appear at the bottom

The difference between the highest bid and lowest ask is called the "bid-ask spread". This number is a prime indicator of market liquidity and trading costs.

Different order types

The order book handles several types of orders:

- Market orders: Execute immediately at the best available price

- Limit orders: Set a specific price for execution

- Stop loss: Automatically sell when the price hits a certain level

- Take profit: Lock in gains at predetermined prices

Market depth

The order book also indicates market depth, showing the volume of orders at different price levels. Deep markets with large order volumes typically mean:

- More stable prices

- Easier trading

- Better price execution

How to use an order book

- Watch the spreadsome text

- Tighter spreads indicate better liquidity

- Wider spreads might mean higher trading costs

- Monitor depthsome text

- Look for significant support and resistance levels

- Be cautious of thin order books

- Consider volumesome text

- Higher volumes suggest more active trading

- Lower volumes might indicate increased risk

Why order books matter for crypto trading

Order books have become an integral part of crypto trading because they provide a clear view of real-time supply and demand. This helps traders understand market sentiment, track price changes, and spot potential trends. With this transparency, it’s easier to gauge how the market is moving at any given time.

They also offer a valuable tool for building trading strategies. They help traders find support and resistance levels, identify large orders that might affect prices, and decide when to enter or exit trades.

Common order book patterns to watch out for

- Wall: Large orders at a specific price level that might prevent price movement

- Depth Imbalance: More orders on one side, suggesting potential price direction

- Tight Spread: Indicates high liquidity and active trading

- Wide Spread: Suggests low liquidity and potential volatility

Alternatives to order book trading

While order books dominate centralized exchanges, other trading mechanisms also exist:

- Automated Market Makers (AMMs)some text

- Used by decentralized exchanges

- Rely on mathematical formulas instead of order matching

- Popular in DeFi applications

- Over-the-Counter (OTC)some text

- Direct trading between parties

- Typically used for large volumes

- More private than exchange trading

Final thoughts

Understanding crypto order books is crucial for anyone serious about trading digital assets. They provide valuable insights into market dynamics and help traders make informed decisions. Whether you're a beginner or an experienced trader, mastering order book analysis can significantly improve your trading strategy.

Remember: Order books are just one tool in your trading arsenal. Experienced traders tend to combine order book analysis with other technical and fundamental analysis methods for a more comprehensive trading approach.

The Bahamas, a tropical paradise of crystal-clear waters, pristine beaches, and vibrant culture, offers more than just a vacation destination - it can be your new crypto-friendly home. Whether you're drawn by the laid-back island lifestyle, tax benefits, or the opportunity to wake up to breathtaking ocean views every day, moving to the Bahamas could be your best move yet.

This comprehensive guide is designed to help you navigate the process of relocating to the Bahamas, covering everything from legal requirements to finding your perfect island home. Let's dive into your new Caribbean life.

Table of Contents

Your ultimate guide to moving to the Bahamas 1

Legal Requirements - Visas and Residency Permits 3

Accessing the Healthcare System 6

Fun Facts about the Bahamas

- Population: 415,223

- Total number of islands: 700, with about 30 inhabited

- Capital: Nassau, located on New Providence Island

- Currency: Bahamian Dollar (BSD), pegged 1:1 with the US Dollar *They also use the Sand Dollar, which is the digital version of the Bahamian dollar (B$).

- Official language: English

Understanding the Bahamas

Location and Climate

The Bahamas is an archipelagic state in the Caribbean, consisting of over 700 islands, cays, and islets spread across 100,000 square miles of the Atlantic Ocean. Located just 50 miles off the coast of Florida (a 3-4 hour ferry ride), it's a popular destination for both tourists and expats seeking a tropical lifestyle.

The climate is tropical, with hot and rainy summers (May to October) and mild winters (November to April). Hurricane season typically runs from June to November, so be prepared for potential storms during this period.

Cultural Considerations

Bahamian culture is a vibrant mix of African, British, and American influences, reflecting its history and diverse population. The people are known for their friendliness and laid-back "island time" attitude, which can be a significant adjustment for those used to a fast-paced lifestyle.

Religion plays a significant role in Bahamian society, with Christianity being the predominant faith. Respect for local customs and traditions is important, as is an appreciation for the relaxed pace of island life.

Language

English is the official language of the Bahamas, making communication easy for most expats. However, you may encounter Bahamian Creole, a dialect spoken by many locals, especially in more casual settings.

Tax Benefits

The Bahamas is often seen as a tax haven, as there’s no income tax, capital gains tax, inheritance tax, or corporate tax. Additionally, the value-added tax (VAT) on goods and services is relatively low, and essentials like milk and bread are exempt from VAT altogether.

Legal Requirements - Visas and Residency Permits

Before moving to the Bahamas, it's important to know the visa and residency requirements. If you plan to stay long-term, you'll need a long-stay visa, which is issued for specific reasons like work, investment, study, or family reunification.

Alternatively, you can enter the country on a visitor visa and apply for an annual residence permit once you're there.

Work Visas and Permits

Non-Bahamians seeking employment need a work visa and permit. The steps include:

- Your employer must advertise the job locally.

- If no local candidates are found, they submit an application to the Director of Labour.

- Once approved, you'll receive a Labour Certificate (LC), which allows you to apply for a work visa at the Department of Immigration.

Investment-Based Residency

Investors and property owners can qualify for residency by investing BS$500,000 (€454,000) or more in property. You’ll need to show a high net worth and enough income to support yourself without working. Property owners can also get a homeowner’s card, which speeds up immigration for you and your family.

Student Visas

To study in the Bahamas, you’ll need a student visa. This requires proof of admission to a Bahamian school, an acceptance letter, and financial support to cover your stay. A student visa lets you live and work while studying.

Family Reunification

If you're married to a Bahamian citizen, you can apply for a resident spouse permit by submitting a letter to the Director of Immigration with supporting documents. If you've been married for five years or more, you may also be eligible to apply for citizenship.

Always check the official Bahamas Immigration website for the latest info: immigration.gov.bs

Finding a Job

Finding employment in the Bahamas can be challenging for expats, as the government prioritises jobs for Bahamian citizens. However, opportunities do exist, particularly in the following sectors:

- Tourism and hospitality

- Financial services

- Real estate

- Education

- Marine and maritime industries

To search for jobs, you can use online platforms such as:

Networking is crucial in the Bahamas, so consider joining expat groups and professional associations to make connections.

Finding a Place to Stay

The Bahamas offers a range of housing options, from beachfront villas to condos in bustling Nassau. Popular areas for expats include:

- New Providence (Nassau, where 70% of the country’s population live)

- Paradise Island

- Grand Bahama Island

- The Abacos

- Eleuthera

- San Salvador Island

- The Exumas

When looking for a place to live, consider:

- Proximity to work or amenities

- Hurricane resilience of the property

- Access to utilities (some islands have limited infrastructure)

Websites to help with your property search:

Living in Nassau offers a variety of housing options, whether you're in the city centre or a bit further out. A one-bedroom apartment in the heart of the city costs around €1,340 per month, while the same type of apartment outside the centre is slightly higher at €1,510.

For larger spaces, a three-bedroom apartment in the city centre averages €3,420, with similar properties outside the centre going for around €3,510. There are plenty of options, providing flexibility depending on your budget and lifestyle preferences.

Cost of Living

While the Bahamas can be expensive - it’s considered one of the most expensive countries to live in in the Caribbean - costs vary significantly depending on the island and lifestyle. Here's a general idea of monthly costs (excluding rent):

- Single person: $1,717 (€1,545)

- Family of four: $6,125.30 (€5,510)

Some specific costs:

- Basic utilities (electricity, water, garbage) for 85m² apartment: $325 (€290)

- Internet (60 Mbps or more): $105 (€94)

- Mobile phone monthly plan with calls and 10gb+ data: $70 (€63)

- Gym membership: $113 (€101)

The cost of living in Nassau, excluding rent, is approximately 3.5% lower than that in New York City, while rent prices are 41.5% lower. Note that imported goods can be quite expensive due to high import duties.

Setting up a Bank Account

To open a bank account in the Bahamas, you'll typically need:

- Valid passport

- Proof of residency (lease agreement or utility bill)

- Reference letter from your current bank

- Proof of income or funds

Major banks in the Bahamas include:

- Bank of The Bahamas

- Commonwealth Bank

- Scotiabank

- Fidelity Bank

Many expats maintain offshore accounts in addition to their local Bahamian accounts. But be aware of tax implications and reporting requirements for your home country.

Prior to setting up your bank account in the Bahamas (and after), the Tap app offers a seamless money solution. The app lets you handle both fiat and crypto in one place, offering an easy way to load funds onto your Tap card and pay for goods and services wherever you are.

Whether you’re making everyday purchases or covering bills back home, Tap simplifies the process by allowing you to use your preferred currency effortlessly.

Getting Around the Bahamas

Transportation in the Bahamas varies depending on the island:

- In Nassau and Freeport, public buses (locally called "jitneys") are available and inexpensive. Note that they are less frequent on Sundays and public holidays.

- Taxis are widely available but can be costly for longer trips.

- Car rentals are an option on larger islands, note that they drive on the left side of the road.

- Inter-island travel is typically by small plane or ferry.

For inter-island transportation, check out:

Accessing the Healthcare System

The Bahamas has public and private healthcare facilities, with one of the most successful healthcare systems in the Caribbean (for locals). While emergency care is available to everyone, expats are generally expected to have private health insurance.

- Private clinics and hospitals offer higher quality care but at a higher cost.

- For serious medical conditions, many expats choose to travel to Florida for treatment.

Consider international health insurance plans that cover medical evacuation for peace of mind.

Learn the Language

English is widely spoken throughout the Bahamas, so language barriers are minimal for most expats. However, learning some Bahamian slang can help you connect with locals:

- "Sip sip" - gossip

- "Sky juice" - a local cocktail made with gin, coconut water, condensed milk, and sometimes nutmeg

- "Conchy joe" - a white Bahamian

Conclusion

Moving to the Bahamas offers a unique opportunity to embrace island living while still enjoying modern amenities. From the turquoise waters to the friendly locals, life in the Bahamas can be a dream come true for many.

Remember to respect local customs, prepare for the tropical climate, and embrace the relaxed pace of life. Whether you're retirement planning, seeking a career change, or just want to wake up to paradise every day, the Bahamas welcomes you to write your own island story.

Pack your sunscreen, Tap card, your sense of adventure, and maybe a good book for those lazy beach days – your Bahamian journey awaits.

Dubai is a city of dazzling skyscrapers, luxury shopping, and vibrant culture, blending modernity with tradition in a unique desert setting. Whether you're drawn by its booming job market, captivating architecture, or tax-friendly environment, moving to Dubai offers an exciting adventure.

This ultimate guide is designed to provide you with everything you need to know to make your relocation smooth and successful. From navigating the real estate market to understanding local customs, we’ve got you covered every step of the way.

Your Ultimate Guide to Moving to Dubai 1

Legal Requirements - visas, residency permits 2

Accessing the healthcare system 6

Fun facts about Dubai

- Dubai population: 3.638 million

- Total foreigners: 2.72 million (75%)

- Currency: United Arab Emirates Dirham (AED), also called Dirhams (symbolised as Dhs)

- Capital: Dubai, the city, is the largest city within the Emirate of Dubai

- Official languages: Arabic, although English very common

Understanding Dubai

Location and Climate

Dubai sits on the southeastern coast of the Arabian Peninsula, right along the sparkling Arabian Gulf. The city's modern skyscrapers and luxurious lifestyle stand in sharp contrast to the traditional desert backdrop, offering a fascinating mix of old-world charm and contemporary flair.

Expect extreme temperatures, with scorching heat - temperatures can soar up to 54°C (129°F) during the summer (May - September) - and much cooler nights, winter nights typically drop to between 10°C and 16°C (50°F to 61°F).

Cultural Considerations

Dubai is a melting pot of cultures, with people from all over the world calling it home. This diversity makes it a vibrant city, but it also means understanding and respecting local customs is important.

The laws and cultural norms in Dubai and the UAE are deeply rooted in Islamic tradition, with customs and etiquette that might differ from what you’re accustomed to. To stay respectful and avoid any issues, dress modestly in public, avoid being intoxicated or disruptive, and keep displays of affection like hugging or kissing to a minimum.

It wouldn’t hurt to dive deeper into the traditional Arabian values to get a better understanding of the local way of life before you touch down.

Language

Arabic is the official language, but you'll find that English is widely spoken and understood, especially in business and social settings. This makes settling in easier for newcomers and helps you navigate daily life without too much hassle. See more on this later.

Legal Requirements - visas, residency permits

Before relocating to Dubai, ensure your paperwork is in order. Your passport should be valid for at least six months from your entry date and make sure to have any necessary documents, like marriage licenses or diplomas, certified before you go.

If you’re from the US, UK, Canada, or most European countries, you can get a 30-day visa on arrival, and reapply for a work visa once you’ve found a job. Alternatively, you can sort out your residency permit beforehand by finding a job and getting the employer to apply on your behalf.

Getting a visa allows you to open a bank account, secure loans (personal or car), access visa-free travel to several countries, enroll your children in private or government schools, get a driver’s license, and access government health services and insurance.

For long-term stays, there are three main visa options: the Green Visa, Standard Visa and Golden Visa. There is also the option to study there, which you’ll need a student visa for.

- Green Visa

The UAE’s Green Visa is a five-year residence visa that allows holders to self-sponsor, removing the need for a UAE national or employer to provide sponsorship.

Requirements:

- Freelancers and Self-Employedsome text

- Freelance/self-employment permit from the Ministry of Human Resources and Emiratisation

- Bachelor’s degree or specialized diploma

- Proof of annual income of at least AED 360,000 for the past two years, or financial solvency for your duration of stay.

- Skilled Employeessome text

- Valid employment contract

- Classification in the first, second, or third occupational level

- Minimum of a bachelor’s degree or equivalent

- Salary of at least AED 15,000 per month

- Standard Work Visa

Your employer is responsible for this application, and will need to apply for a residency visa through the General Directorate of Residency and Foreigners Affairs (GDRFAD) Dubai. Available for employees in the private and government sectors and free zone.

- Golden Visa

The UAE’s Golden visa is a long-term residence visa designed for foreign talents, offering the following benefits:

- Entry visa: A six-month entry visa with multiple entries to proceed with residence issuance.

- Long-term residence: Renewable visa valid for 5 or 10 years.

- No sponsor needed: Allows holders to live without needing a local sponsor.

- Extended stay: Permits holders to stay outside the UAE beyond the usual six-month period.

- Family sponsorship: Enables sponsorship of family members, including spouses and children of any age, and unlimited domestic helpers.

- Continuity: Family members can remain in the UAE until their permit expires if the primary visa holder passes away.

- Student Visa

Students need a student visa, which are typically valid for one year and renewable annually. To apply, provide a passport, recent photos, an acceptance letter from a UAE educational institution, and a tenancy agreement if applicable. A security check and medical tests for tuberculosis, HIV, and hepatitis may also be required.

As all this information is subject to change, be sure to check the finer details before taking the leap. Find more info here.

Finding a job

Finding a job in Dubai can be an exciting opportunity due to its tax-free income and diverse job market. To get started, you can explore popular online job boards such as Bayt, Buzzon, Dubizzle, Naukrigulf, and Gulf Talent.

Alternatively, consider partnering with a reputable recruitment agency known for connecting job seekers with Dubai employers (be sure to check the reviews!). If possible, it’s advisable to secure a position before arriving.

Job seekers can also use English-speaking sites like UAE Recruitment Agency, Caterer Global, GoToGulf, and Gulflancer.

Be aware that the work week typically runs from Sunday to Thursday, with Friday and Saturday as the weekend, and working hours are reduced during Ramadan.

Finding a place to stay

Finding a place to live in Dubai can be a bit of a task, but it’s manageable with some prep. Many jobs come with housing perks or allowances, but if you’re renting, don’t be surprised if you’re asked to fork over six months to a year’s rent upfront. You’ll find both furnished and unfurnished options, so pick what suits you best.

If you’re eyeing swanky areas like Jumeirah or Dubai Marina, be prepared for higher rents and fierce competition. For something a bit easier on the wallet, try The Lakes, The Meadows, or The Springs. And if you don’t mind a longer drive, the suburbs along Sheikh Zayed Road have plenty of choices too.

In Dubai, renting a one-bedroom apartment in the city center averages around €2,000 per month, while outside the city center it’s more affordable at approximately €1,250. For a three-bedroom apartment, expect to pay about €3,750 in the city center and €2,600 outside of it.

Here’s a quick rundown of what renting an apartment will entail:

- Make an offer: Agree on the rent and terms.

- Pay a deposit: Usually one month’s rent, plus a copy of your passport and visa.

- Sign the lease: Review and sign the tenancy contract.

- Register your lease: Use Ejari to register your lease online or via an agent.

You’ll need:

- Original lease contract

- Landlord’s title deed

- Passport copies (yours and the landlord’s)

- Emirates ID

Also, remember to apply for utilities with DEWA and get a move-in permit if needed. If you’re using an agent, make sure they’re registered with Dubai’s Real Estate Regulatory Agency (RERA).

Cost of Living

The good news is that living in Dubai is considerably more affordable than living in cities like New York. Here’s a quick look at some common costs:

- Basic utilities (electricity, heating, cooling, water, garbage) for a 915 sq ft apartment: 732.78 AED (€180)

- Mobile phone monthly plan (calls and 10gb+ data): 197.80 AED (€50)

- Internet (60 mbps or more, unlimited data): 365.99 AED (€90)

- Fitness club monthly fee: 316.49 AED (€78)

Estimated monthly costs without rent:

- Single Person: 4,020.9 AED (€990)

- Family of Four: 14,036.8 AED (€3,500)

Overall, Dubai is about 40.8% cheaper than New York without considering rent, and rent in Dubai is approximately 49.9% lower.

Setting up a bank account

After receiving your visa, you’ll need to get your Emirates ID through the Federal Authority for Identity, Citizenship, Customs and Ports Security website. It’s not just for the bank; it's a legal requirement for everyone in the UAE to carry it.

Once you’ve got this, opening a bank account is relatively straightforward. For this you'll need to provide:

- A copy of your passport with the residence visa

- A copy of your Emirates ID card

- A salary certificate or a letter from your employer or sponsor confirming this

Setting up a bank account might take some time, so you will need other ways to handle your money initially. That’s where services like Tap can come in handy.

With the Tap app, you can manage all your currencies in one place (fiat and crypto), load funds as you need onto your Tap card, and pay for goods and services with a single Tap. The app also allows you to pay bills back home effortlessly, using your preferred currency. Learn more here.

Please note that once you have received your residency permit you are no longer allowed to use the Tap app in the UAE as we do not cover that jurisdiction.

Getting around Dubai

Dubai's transport system is just as sleek and efficient as the city itself. The Dubai Metro, with its state-of-the-art setup, is a budget-friendly way to get around. A single ticket costs around 7 AED (about €1.7), and a monthly pass for unlimited rides is around 300 AED (about €74).

If you prefer a more personalised touch, taxis are readily available, starting at 12 AED (€3) with a rate of around 4.83 AED (€1.2) per mile.

Thinking of driving? Dubai’s roads are well-kept, though traffic can get intense. Gas is reasonably priced at 11.35 AED (€2.8) per gallon, making car ownership appealing. A new Volkswagen Golf or something similar will set you back about 124,000 AED (€30,500). Renting a car is also an option, offering a taste for driving without the long-term commitment.

Accessing the healthcare system

The UAE’s healthcare system is pretty extensive, with both government-funded and private options available.

In Dubai, you can get free or affordable care at public hospitals if you have a health card from the Department of Health and Medical Services. Employers are required to provide health insurance for their staff, and if you’re sponsoring family members, you’ll need to cover them too.

If you’re handling your own sponsorship, you’ll need to sort out your own insurance coverage.

Learn the language

If you want to really get involved, you can learn some basics. Arabic is the official language in Dubai and the UAE, but you'll hear English spoken by many residents. Due to the influx of international visitors, languages like Hindi, Chinese, and Urdu are also common.

If you’re keen to pick up some Arabic, there are plenty of free online resources like Duolingo and Madinah Arabic. Local universities and schools in Dubai also offer language classes if you prefer a more hands-on approach.

Conclusion

So there you have it. From navigating the visa maze to mastering the art of Metro-hopping, you're now equipped with the essentials for your desert adventure.

Remember, Dubai is a city where ancient traditions dance with futuristic dreams, so whether you're chasing career heights in a skyscraper or perfecting your Arabic in a local café, embrace the journey. Pack your sunscreen, your sense of wonder, and maybe a phrase book – your Dubai story awaits.

When making purchases with your debit card, you’re typically asked to provide a security code, also known as a CVV or CVV2 code. This 3-digit (or sometimes 4-digit) number is an important security feature that helps protect your card from unauthorised use. Understanding what this code is, where to find it, and why it's crucial to keep it safe can help prevent financial fraud and give you greater control over your accounts. In this article, we dive into the details.

What is the security code used for?

The debit card security code serves a critical purpose in verifying your identity and protecting against fraudulent activity. When you provide the code during a transaction, it confirms that you physically possess the card, rather than just having access to the card number alone.

This helps prevent criminals from making unauthorised purchases, especially for online, phone, or mail-order transactions where the physical card is not present. By requiring the security code, merchants and financial institutions can have an additional safeguard against fraud, giving you greater confidence that your hard-earned money stays secure.

Why are debit card security codes important?

The bottom line is that debit card security codes play a vital role in safeguarding your financial information and protecting your hard-earned money. This security code acts as an additional layer of security beyond just your card number and expiration date and without it, criminals would have a much easier time making unauthorised purchases or accessing your accounts.

Where can I find my debit card security code?

The debit card security code is typically found in one of two places on your card:

On most standard debit cards, the 3-digit code is printed on the back of the card, often in the signature strip or just to the right of it.

Some debit cards may have a 4-digit security code that is printed on the front of the card, usually in the top right corner.

How debit card security codes work with contactless payments

While debit cards with security codes are primarily used for in-person, online, and over-the-phone transactions, the code also plays a role in contactless or "tap-to-pay" payments.

When you hold your debit card up to a contactless payment terminal, the 3- or 4-digit security code is digitally transmitted along with your card information. This allows the payment system to verify your identity and approve the transaction, just as it would for a contact-based payment that requires manually entering the security code.

The security code therefore provides an extra layer of protection, even for quick tap-and-go purchases.

CVV vs OTP

The key difference between a debit card's CVV (card verification value) code and an OTP (one-time password) lies in how they function to verify transactions. A CVV is a static 3 or 4-digit code printed on your physical debit card, which you manually enter to confirm your identity.

In contrast, an OTP is a dynamically generated code, typically sent to your mobile device via SMS from the bank or an authentication app, that changes with each new transaction. While both add an extra security layer, OTPs provide stronger protection, as they cannot be reused like a static CVV.

Combining the use of your debit card's CVV code and a one-time password (OTP) provides the strongest protection against financial fraud.

CVV vs PIN

Your debit card's PIN (Personal Identification Number) is different from the CVV (card verification value) code.

The PIN is used to verify in-person transactions when you use the physical card, like at a store checkout or ATM.

The CVV code is used instead for remote purchases, like online or over the phone, where the physical card isn't present.

Closing thoughts

In summary, the debit card security code, also found on a credit card, is an essential safeguard against fraud and unauthorised transactions. By understanding what this code is, where to find it, and how it protects your finances, you can take control of your financial security and enjoy greater peace of mind when using your debit card in the wild or online.

Crypto recovery scams involve fraudsters claiming they can recover lost or stolen cryptocurrency for a fee. These scammers prey on individuals who have lost access to their digital assets.

As cryptocurrencies grow in popularity, these deceptive schemes are also becoming more and more prevalent. Being able to identify and avoid such scams is crucial. Not only will it help to safeguard your current investments but will also prevent further financial losses. In this article we’re going to guide you through identifying these scams, and what to do from there.

Signs of a crypto recovery scam

Spotting a crypto recovery scam can be easier if you know the telltale signs:

- Be wary of unsolicited offers to recover your lost or stolen crypto, as legitimate services don't operate that way.

- Scammers often demand exorbitant upfront fees before providing any services, while legitimate ones typically charge after a successful recovery.

- Unrealistic promises of guaranteed recovery should also raise suspicion, as legitimate services are upfront about risks and limitations.

Another red flag is a lack of transparency about their methods and processes. Scammers tend to be vague, while legitimate services are open about their approach.

Finally, watch out for high-pressure tactics like creating a false sense of urgency. Scammers may use these to rush you into a decision, whereas legitimate services allow you to make an informed choice. Acknowledging and staying vigilant about these signs can protect you from falling victim to crypto recovery scams.

How scammers typically operate a crypto recovery scam

In a cunning ploy, scammers impersonate representatives from reputable companies, reaching out to unsuspecting individuals with the promise of recovering funds lost in previous scams. These impostors may even possess specific details about the victims, such as the amount of money they had lost, further lending credibility to their claims.

Once they gain the trust of their targets, the scammers instruct the victims to promptly send Bitcoin or other cryptocurrencies to a wallet address controlled by the scammers themselves. In some cases, the scammers may suggest that the victims create accounts on cryptocurrency exchanges that allow multiple owners for a single wallet, such as Atomic Wallet. In other instances, the scammers may have already set up these accounts themselves and merely grant the victims access, ensuring complete control over the funds.

To further facilitate the transfer of funds, some victims are coaxed into downloading remote access software like AnyDesk, under the pretense of receiving assistance with setting up bank or exchange accounts. This tactic grants the scammers direct access to the victims' devices, providing yet another avenue for diverting funds to their chosen destinations.

How to protect yourself

To protect yourself from crypto recovery scams, it's essential to do thorough research on any company or service before engaging with it. Be sure to scrutinize their credentials, reviews, and track record, and if something sounds too good to be true, it usually is.

As mentioned above, always be highly sceptical of unsolicited offers or claims, as these are often tactics used by scammers. Instead, do your own homework and find a service that aligns with your needs and sense of comfort.

Never share your private keys or seed phrases with anyone, as this grants them complete access to your funds. Instead, consider using reputable and trusted crypto recovery services, such as CryptoRecovery.com or CoinRecovered.com, which have established reputations and transparent processes.

While this might sound like scary business, rest assured that by exercising due diligence, maintaining a healthy dose of scepticism, and safeguarding your private information, you can significantly reduce the risk of falling victim to these deceptive schemes.

Reporting crypto recovery scams

If you suspect you have been contacted by a crypto recovery scam service or found one online, report it to the appropriate authorities as well as the Tap team immediately. Many countries have dedicated cybercrime units or financial fraud hotlines where you can file a complaint. Additionally, by alerting Tap we can escalate the report and inform other crypto holders before they potentially fall prey to these scammers.

Always remember that raising awareness is crucial in combating these scams. Share your experience on forums, social media, or with your network to warn others. By doing so, you can help prevent more people from falling victim and contribute to the collective effort against crypto-related frauds.

Key takeaways from this article

Key signs of a crypto recovery scam include unsolicited offers, demands for exorbitant upfront fees, lack of transparency about methods, unrealistic promises of guaranteed recovery, and high-pressure tactics. Exercise extreme caution and conduct thorough due diligence before engaging with any service claiming to recover lost or stolen cryptocurrency.

Additionally, spreading awareness is crucial to combating these scams. Share information about the telltale signs and your experiences with Tap, the appropriate authorities, your network and online communities. By raising awareness, you can help others avoid falling victim to these deceptive schemes and contribute to the collective effort against crypto-related fraud.

For more information, here are the top 5 crypto scams people fall victim to.

No matter your travel budget, navigating ATM fees is worth your time when travelling around Europe. In this article, we’re giving you a run-through of the common charges you may face, from withdrawal and balance inquiry fees to currency conversion costs, and how to easily navigate them.

Why do ATMs charge fees?

Wondering why ATMs charge those pesky fees? The truth is, there's a cost involved for the banks behind those convenient cash machines. They have to stock the cash, maintain the equipment, and liaise with your home bank to reconcile the transactions. Those ATM fees you see? That's how banks recoup those operational expenses, with a little profit margin added in for good measure.

Common ATM fees in Europe

When using ATMs in Europe, you'll likely encounter several common fees that can mount up fast. While less common in the UK, in countries like Germany, ATM fees can quickly add up to €4. Let’s take a look at what kinds of fees one might encounter.

Bear in mind that the amount you'll have to pay at a European ATM depends on two main factors:

- Your home bank's fees: they may charge a withdrawal fee, typically a few euros to several dollars, every time you use an ATM abroad.

- The ATM's own fees: the bank that owns the ATM you're using may also levy its own withdrawal fee, on top of what your home bank charges.

These charges will vary depending on your bank, so be sure to check before leaving. While most banks list their ATM use charges in their terms, with some offering limited free withdrawals, others charge a flat fee per transaction, especially for out-of-network or international ATM use, so be mindful of potential fees when accessing your money abroad.

In addition to withdrawal fees, you may also encounter balance inquiry fees just for checking your account balance, as well as conversion or foreign transaction fees when using a card issued outside of the Eurozone.

Factors affecting ATM fees

The fees you'll encounter at European ATMs can vary quite a bit depending on several key factors. First, the location of the ATM makes a big difference - if it's part of your home bank's network, you'll likely pay lower (or even no) withdrawal fees. But use an out-of-network machine, and those charges can start to add up quickly.

The type of card you're using also plays a role. Debit cards generally incur fewer fees than credit cards when used for ATM withdrawals. And your home bank's specific policies on international ATM use can further impact the costs you face.

Keeping these variables in mind as you access cash abroad will help you sidestep unnecessary fees and make your travel budget stretch further.

Tips for minimising ATM fees in Europe

When navigating the ATM landscape in Europe, there are a few savvy strategies you can employ to steer clear of those ATM fees:

- Seek out a bank account that offers fee-free withdrawals - some digital-only banks provide a certain number of complimentary ATM transactions each month.

- Stick to ATMs owned and operated by banks, rather than independent machines often found in convenience stores, as those are more likely to come with added charges.

- Be strategic with your cash withdrawals - if your account allows for free branch ATM use, plan ahead and make larger, less frequent withdrawals to minimise fees. Conversely, if you have a limited number of free monthly transactions, opt for larger sums to get more mileage from those.

- Finally, minimise cash usage altogether by relying on your debit card for payments wherever possible, reserving cash for small, cash-only establishments like markets.

By employing these tactics, you can keep more of your hard-earned money in your pocket while exploring Europe.

The Tap Solution

Tap provides users within the European zone with a free prepaid crypto and fiat card that can be used anywhere in the world. Powered by Mastercard, the card links directly to the funds in the holder’s Tap app, allowing them to easily manage their money and constantly be in the know.

With all options providing free card deposits and free in store purchases, the premium options offer impressive fees when it comes to exchanging and trading funds. When it comes to monthly ATM withdrawals, the Essential account allows free withdrawals up to €500, higher tiers offer up to €1,000, while the Prestige level provides unlimited free withdrawals before incurring charges.

Get more information about the available options when it comes to your Tap card here.

Conclusion

In summary, being aware of European ATM fees - including withdrawal charges, balance inquiries, and currency conversion costs - is key to managing your travel budget. Research your bank's policies, locate in-network ATMs, and strategise cash withdrawals before your trip. With some smart planning, you can sidestep unnecessary fees and make the most of your time exploring Europe.