More than a million Bitcoin have vanished because owners didn’t plan ahead. Without a crypto inheritance plan, your family could lose access to your assets forever. Here’s how to safeguard them.

Keep reading

As digital assets become a core part of personal wealth, one uncomfortable question lingers: what will happen to your crypto when you’re gone? Unlike traditional assets that can be managed through banks or brokers, cryptocurrencies are bound entirely to whoever holds their private keys. Lose the keys, and the funds are gone. Permanently.

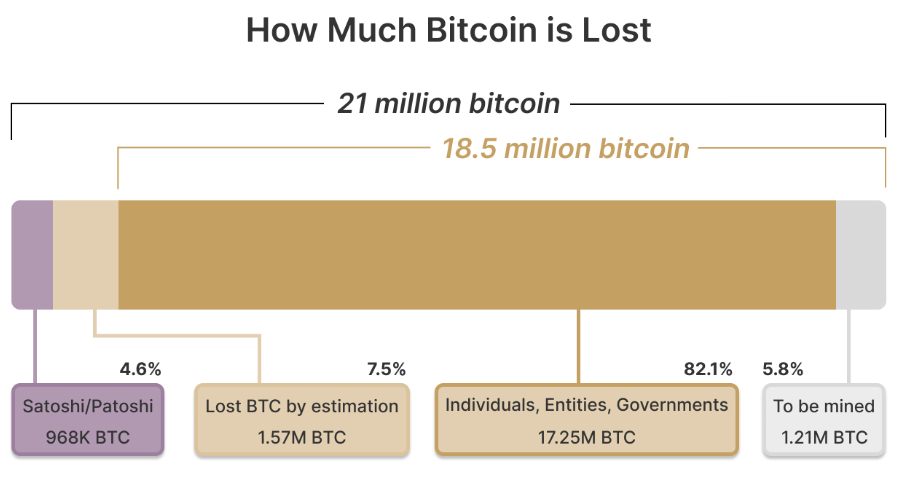

Each year, millions of dollars in Bitcoin, Ether, and other tokens vanish into the digital void when holders pass away without sharing access. It is estimated that around 1.5 million BTC (roughly 7.5% of total supply) may already be lost forever. With digital wealth now part of countless estates, preparing for the inevitable is no longer optional; it’s the responsible thing to do.

Why Planning for Crypto Inheritance Matters

In traditional finance, wealth transfer is handled through wills, trusts, and custodians. But crypto flips that model: you are the bank. Your heirs can’t simply request a password reset or call customer service. Without private keys, wallets, or access instructions, those assets are unrecoverable for all effects and purposes.

A crypto inheritance plan ensures that your digital assets, from Bitcoin and altcoins to NFTs and DeFi holdings, remain both secure and accessible to the people you choose. It bridges two crucial needs: protecting your funds today and ensuring your legacy tomorrow.

Beyond personal security, inheritance planning also reduces emotional and financial stress for your loved ones. By documenting how and where assets can be accessed, you prevent confusion and potential legal disputes.

Building the Foundation of a Crypto Inheritance Plan

Start with Legal Clarity

Consult an attorney familiar with digital assets. A properly structured will or trust should identify your crypto holdings, list beneficiaries, and outline how they can access those funds. Many jurisdictions still lack explicit laws for digital assets, so expert guidance helps ensure compliance and enforceability.

Secure Your Keys… But Don’t Overshare

The biggest challenge in crypto inheritance is private key management. If you die with your keys, your crypto dies with you. However, leaving keys in plain text within a will or document is just as risky. Instead, consider approaches like:

- Multisignature wallets, which require multiple approvals to move funds.

- Shamir’s Secret Sharing, which means splitting your seed phrase into parts distributed among trusted people.

- Encrypted backups or sealed letters stored in secure, offline locations.

Document recovery procedures in plain language so your heirs can follow them even without technical knowledge.

Choose the Right Executor

A traditional executor may not understand how to navigate crypto. You can appoint a tech-literate executor or designate a digital asset custodian to handle that portion of your estate. This ensures smooth execution and reduces the risk of errors or loss.

In a market driven by innovation and constant change, a well-structured inheritance plan offers something rare in crypto, certainty.

New Tools for a Digital Age

The rise of blockchain-based “death protocols” and smart contract automation adds a new layer of possibilities. Some platforms allow transfers to trigger automatically after certain conditions are met (for example, a verifiable death certificate or extended inactivity).

Ethereum and similar chains already support programmable inheritance systems, but these should complement, not replace, legal documents. Technology can help enforce your intentions, but law remains the foundation of inheritance.

Some investors even use “dead man’s switches”, automated systems that transfer funds if the owner doesn’t log in for a set period. While clever, it might be best to pair them with legal documents to prevent accidental activations.

Protecting Privacy While Planning Ahead

While planning for the future, it’s crucial to maintain security in the present. Avoid including wallet addresses, private keys, or passwords in public wills, which become part of the legal record. Instead, store such details in encrypted files or sealed envelopes accessible only to specific individuals.

Tools like decentralized identifiers (DIDs) and verifiable credentials can also help manage long-term identity and access rights. These systems allow you to define who can access what, and when, without intermediaries.

Custodial vs. Non-Custodial: Finding the Balance

When structuring inheritance, knowing whether your assets are held in custodial or non-custodial wallets makes all the difference.

Custodial services (like major exchanges) manage private keys on your behalf, which simplifies recovery if your heirs can provide proper documentation. However, it introduces third-party risk. Accounts can be frozen, hacked, or shut down.

Non-custodial wallets, on the other hand, offer maximum control and privacy but demand greater responsibility. If your heirs lose the seed phrase, there’s no backup plan. There’s also the possibility of taking a hybrid approach: keeping long-term holdings in non-custodial storage for security, while using reputable custodians for smaller, more accessible amounts.

Keep It Up to Date

A crypto inheritance plan is not a “set it and forget it” document. Prices change, portfolios evolve, and wallet technologies become obsolete very often. It may be wise to revisit your plan regularly, especially after major life events such as marriage, divorce, or the birth of a child.

It’s also worth keeping track of regulatory updates in your jurisdiction. Laws surrounding digital assets and inheritance are rapidly evolving, and what’s compliant today may not be tomorrow.

Common Inheritance Pitfalls

Even the best intentions can go wrong. Here are the most frequent mistakes to avoid:

- Including seed phrases directly in your will. As we mentioned before, this makes them public and vulnerable.

- Neglecting to educate heirs. Without guidance, even secure plans can fail.

- Relying solely on exchanges. Centralized platforms can fail or freeze funds.

Planning isn’t just about distributing wealth; it’s about ensuring continuity. A clear inheritance strategy preserves your crypto’s value and prevents it from becoming part of the estimated $100 billion in lost digital assets worldwide.

Protecting More Than Just Coins

Preparing a crypto inheritance plan isn’t merely about money; it’s about legacy. For all the talk about decentralization and autonomy, responsibility and forward-thinking remain at the heart of crypto ownership. By taking the time to plan ahead, you safeguard not only your wealth but also your family’s peace of mind.

NEWS AND UPDATES

LATEST ARTICLE

Civic (CVC) is a blockchain-based identity verification platform focused on providing secure, cost-effective identity management solutions. As digital identity verification becomes increasingly important in today’s world, Civic distinguishes itself with its decentralised approach and user-centric control over personal data.

Let's explore how this platform is addressing the challenges of digital identity verification, privacy, and security.

TLDR

- Decentralised identity verification: Civic provides secure personal data verification without storing user information centrally, reducing fraud and identity theft risks.

- User-controlled identity: Users maintain ownership of their personal data, selectively sharing only required information with service providers through the Civic app.

- Multi-layered ecosystem: Utilises the Identity Verification Marketplace and Civic Pass for DeFi access control.

What is the Civic network all about?

Founded in 2015 by Vinny Lingham and Jonathan Smith, Civic launched its Initial Coin Offering (ICO) in June 2017, raising $33 million. The platform enables users to verify their identities on the blockchain while maintaining control over their personal information.

It aims to overcome traditional identity verification drawbacks, such as centralised data storage, repetitive KYC processes, and privacy concerns—and it uses blockchain technology to achieve this. The platform’s infrastructure allows for reusable KYC, minimising the need to repeatedly share personal documents with different service providers, all while reducing verification costs.

In June 2017, Civic conducted its token sale, selling $33 million worth of CVC tokens. Since then, the platform has continued to evolve, introducing Civic Pass in 2021, serving as an identity gateway for DeFi apps, NFT platforms, and DAOs requiring compliance.

At the time of writing, it remains one of the notable blockchain-based identity verification solutions in the cryptocurrency ecosystem.

How does the Civic platform work?

Civic's core architecture revolves around three main components that work together to provide comprehensive identity verification services:

- Identity Verification Marketplace - connects identity requesters with trusted validators to verify user information.

- Civic Pass - provides access control for DeFi applications and other services requiring compliance checks.

It’s worth noting that their product Civic Pay was quietly retired in 2020-2021.

The Identity Verification Marketplace operates on the blockchain, creating a trusted ecosystem where validators (trusted entities that verify identity information) and service providers can interact. When users provide identity information through the Civic app, it's encrypted and stored on their device, not on Civic's servers.

By distributing the verification process across the blockchain and putting users in control of their data, Civic promises to deliver security, privacy, and convenience without compromises. Because users can reuse their verified identity across multiple platforms, this makes it an efficient solution for both individual users and businesses requiring KYC processes.

Civic created CVC to be the utility token across its ecosystem, used for paying for verification services, rewarding validators, and incentivising ecosystem participation.

The advantages of the Civic platform

According to the Civic team, the platform significantly reduces verification costs compared to traditional identity verification methods. It's also capable of completing verifications in minutes rather than days. This makes it a superior solution for businesses looking to streamline their KYC processes while maintaining regulatory compliance.

Beyond that, Civic is designed to address major issues facing identity systems today: data breaches and identity theft. This is done by eliminating centralised databases of personal information, ensuring that even if Civic were compromised, users' personal data would remain secure.

It's also highly inclusive. While many identity verification systems require extensive documentation, Civic works to provide solutions for the unbanked and underbanked populations globally, potentially bringing financial services to billions of people.

In 2021, Civic expanded its offerings with enhanced DeFi protection tools and NFT verification services, ensuring that its identity solutions remain relevant in the evolving blockchain ecosystem. The platform continues to develop new use cases for its technology, particularly in combating bot activity and fraud in decentralised applications.

Civic use cases

The Civic network allows individuals and businesses to verify identity information securely and efficiently, whether for account creation, age verification, or compliance with regulatory requirements.

It is one of the first platforms to combine blockchain technology with identity verification to create a user-centric system that puts individuals in control of their personal data while still meeting the verification needs of businesses.

Due to the platform's focus on privacy and security, businesses can implement strong KYC procedures without creating vulnerable centralised databases of user information. This provides them with compliance solutions that protect both the business and its customers.

How to buy CVC

If you’re looking to incorporate CVC into your crypto portfolio, users can effortlessly buy and sell the token on the Tap app (after completing the account registration process). Download the app to get started.

FAQs

How does Civic protect user data?

Civic employs a decentralised identity architecture where users’ personal data is stored locally on their devices, not on central servers. Data is encrypted and hashed, and Civic leverages zero-knowledge proofs in some cases to validate information without exposing the data. Only attestations (proofs of verification) are stored on the blockchain, not the personal data itself. Users maintain control over what information is shared and with whom.

Can you mine CVC tokens?

No, CVC tokens cannot be mined. The total supply of CVC was created during its token generation event in 2017, and no new tokens were issued. As an ERC-20 token on the Ethereum blockchain, CVC transactions are secured by Ethereum’s Proof of Stake mechanism, but CVC is not mined or staked for rewards.

What is the CVC price?

As the market is known to change regularly, please check the Tap app to find the most relevant CVC price.

If you've been exploring the world of cryptocurrency beyond Bitcoin and Ethereum, you've probably heard of Sushi. No, not the Japanese dish – we're talking about a powerful player in the decentralised finance (DeFi) space that's been making waves since its dramatic entrance in 2020.

Sushi, or SushiSwap as the platform is called, burst onto the crypto scene with what many called a "vampire attack" on Uniswap, another popular decentralised exchange (DEX). This bold move involved attracting over a billion dollars of liquidity from its competitor in just a few days.

Today, SushiSwap stands as one of the leading decentralised exchanges in the crypto ecosystem, offering a suite of financial services that go well beyond simple token swapping. With its native SUSHI token, the platform has created an ecosystem that allows users to trade, earn, lend, borrow, and more – all without traditional financial intermediaries.

What makes Sushi truly stand out is how it's putting financial power back into the hands of regular users. By democratising access to sophisticated financial tools that were once only available to privileged institutions, Sushi is helping to create a more open, accessible financial system for everyone.

What is Sushi (SUSHI)?

At its core, Sushi is a DEX and DeFi protocol that allows users to trade cryptocurrencies directly with each other without any middlemen. Unlike centralised exchanges, there's no company controlling your funds or verifying your identity – it's just you, smart contracts, and the blockchain.

Think of SushiSwap as an online marketplace where instead of a company facilitating trades, everything runs on code. It's like if eBay operated without eBay the company – just buyers and sellers interacting through an automated system.

The relationship between SushiSwap and SUSHI is important to understand:

- SushiSwap is the platform – the actual decentralised exchange and suite of DeFi services

- SUSHI is the native token that powers the ecosystem – like owning a piece of the project

The Sushi ecosystem has evolved significantly since its launch, now offering a full menu of DeFi services:

- Token swapping (the basic exchange function)

- Liquidity providing (where users can earn fees)

- Yield farming (earning rewards by supporting the platform)

- Lending and borrowing

- Token launches

- NFT marketplace

- Cross-chain functionality (operating across multiple blockchains)

When compared to other DEXs like Uniswap and PancakeSwap, Sushi stands out for its community-first approach and wide range of features. While Uniswap pioneered the automated market maker model that Sushi uses, Sushi expanded on this foundation by adding more ways for users to participate and earn rewards.

And while PancakeSwap operates primarily on the Binance Smart Chain, Sushi has expanded to multiple blockchains, including Ethereum, Polygon, Avalanche, and more.

The history of Sushi

Sushi's history reads like a crypto soap opera – complete with controversy, drama, and unexpected twists. Grab the popcorn.

It all began in August 2020 when an anonymous developer going by the name "Chef Nomi" created SushiSwap as a fork (essentially a copy with modifications) of Uniswap's code. But Chef Nomi didn't just launch a competitor; they executed what became known as a "vampire attack" – a strategy to drain liquidity from Uniswap by offering better incentives.

Users who provided liquidity to Uniswap could stake their LP (liquidity provider) tokens on SushiSwap to earn SUSHI rewards. Then, in a coordinated event called "The Migration," over $1 billion in crypto assets moved from Uniswap to SushiSwap virtually overnight. The crypto community was stunned by the aggressive yet innovative approach.

But the drama was just beginning. Shortly after the successful migration, Chef Nomi suddenly converted a large amount of SUSHI tokens (worth about $14 million at the time) into Ethereum and withdrew it. The community viewed this as an "exit scam," and the price of SUSHI plummeted.

In a surprising turn of events, Sam Bankman-Fried, then-CEO of FTX (a major crypto exchange at the time), stepped in to take control of the project. Days later, Chef Nomi returned all the funds and apologised to the community.

Control of the project was then transferred to a multi-signature wallet controlled by several trusted community members, transitioning SushiSwap to true community governance. Since then, the protocol has seen steady development and expansion, including:

- Launch of Kashi lending platform (March 2021)

- Introduction of BentoBox, a yield-generating vault (Q1 2021)

- Expansion to multiple blockchains beyond Ethereum

- Release of Miso launchpad for new tokens

- Development of Shoyu, an NFT marketplace

Despite its tumultuous beginnings, Sushi managed to establish itself as a serious contender in the DeFi space through continuous innovation and a strong community focus.

How does SushiSwap work?

SushiSwap operates on a model called an automated market maker (AMM), which is fundamentally different from traditional exchanges. Here's how it works in simple terms:

Instead of matching buyers with sellers (the way stock exchanges work), SushiSwap uses liquidity pools – essentially big pots of cryptocurrencies that users can trade against. Imagine a vending machine that's always ready to exchange one token for another, rather than waiting to find someone who wants the opposite side of your trade.

These pools are created and maintained by liquidity providers – regular users who deposit pairs of tokens (like ETH and USDT) into the pools. In return for providing this liquidity, they earn fees from trades that happen in their pool.

When you want to swap tokens on SushiSwap, here's what happens:

- You select the tokens you want to exchange (for example, ETH for USDT)

- Smart contracts calculate the exchange rate based on the ratio of tokens in the relevant liquidity pool

- The more of one token you want, the more expensive it gets (this is called "slippage")

- A small fee (0.3% of the trade) is taken and distributed to liquidity providers

- The tokens are exchanged directly in your wallet

The beauty of this system is that it's all handled by smart contracts – self-executing code on the blockchain. There's no company processing your trade or holding your funds; it's all automated and trustless.

Of this 0.3% fee, 0.25% goes directly to liquidity providers in the pool, while the remaining 0.05% is converted to SUSHI tokens and distributed to SUSHI stakers. This creates a sustainable revenue model where active users earn from the platform's success.

Key features of the Sushi ecosystem

Sushi has evolved from a simple token exchange into a comprehensive DeFi ecosystem. Let's explore the main ingredients in Sushi's expanding menu:

SushiSwap DEX: The heart of the ecosystem is the decentralised exchange where users can swap virtually any ERC-20 token (and tokens on other supported blockchains). With competitive rates and deep liquidity across many trading pairs, it's the foundation of the Sushi experience.

Kashi: This lending and margin trading platform allows users to borrow assets against their crypto collateral. What makes Kashi unique is its isolated risk markets – meaning a problem in one lending market won't affect others, making it potentially safer than some competitors.

BentoBox: Think of this as a smart crypto savings account. BentoBox is a token vault that generates yield on deposited assets while they're waiting to be used in other Sushi products. It's like your money earning interest while sitting in your wallet, ready to use.

Onsen: This liquidity mining program incentivises users to provide liquidity for specific token pairs by offering additional SUSHI rewards. It's named after Japanese hot springs – places where people gather and relax, much like how Onsen gathers liquidity for the platform.

Miso: A launchpad for new tokens, Miso helps projects conduct token sales with various auction types. It's like Kickstarter for new crypto projects, helping them raise funds and distribute tokens fairly.

Shoyu: Sushi's NFT marketplace allows for the creation, buying, and selling of digital collectables. While newer than some competitors, it aims to offer lower fees and better integration with the rest of the Sushi ecosystem.

Cross-chain deployment: Unlike many DeFi protocols that only exist on Ethereum, Sushi has expanded to numerous blockchains including Polygon, Avalanche, Binance Smart Chain, Fantom, and more. This multi-chain approach helps users avoid Ethereum's sometimes high transaction fees while still accessing Sushi's services.

This diverse ecosystem makes Sushi a one-stop shop for many DeFi activities, allowing users to move seamlessly between trading, earning, lending, and more.

SUSHI tokenomics

The SUSHI token is the special sauce that brings the whole Sushi ecosystem together. Let's break down how it works:

Total supply: SUSHI has no maximum supply cap. New tokens are minted at a rate of 100 SUSHI per Ethereum block (roughly every 12 seconds), though this emission rate has been adjusted through governance votes over time.

Token utility: The SUSHI token serves several important functions:

- Governance: SUSHI holders can vote on proposals to change the protocol

- Fee sharing: When staked, SUSHI entitles holders to a portion of all trading fees

- Liquidity mining rewards: Users can earn SUSHI by providing liquidity

- Platform access: Some features may require SUSHI holdings or staking

Governance rights: Holding SUSHI means having a say in the future of the platform. Token holders can propose and vote on changes ranging from technical upgrades to treasury management and new feature development.

xSUSHI mechanism: When users stake their SUSHI tokens, they receive xSUSHI in return. This represents their share of the staking pool, which constantly grows as trading fees are added to it. When users unstake, they get their original SUSHI plus their portion of accumulated fees – making it a passive income opportunity.

Staking rewards: The current APY (Annual Percentage Yield) for staking SUSHI varies depending on platform volume and the number of stakers, but it has historically offered attractive returns compared to traditional finance.

Market performance: As with many cryptocurrencies, SUSHI has experienced significant price volatility since its launch. After reaching all-time highs during the 2021 bull market, the token has settled into a more stable trading range.

The tokenomics of SUSHI are designed to align the interests of users, liquidity providers, and token holders – when the platform succeeds, SUSHI holders benefit through increased value and fee sharing.

How to buy and sell SUSHI

Looking to get your hands on some SUSHI tokens? Here's how you can do it through the Tap app:

How to buy SUSHI on the Tap App:

- Download the Tap app from your device's app store

- Create an account and complete the required verification

- Fund your account using a supported payment method (bank transfer, card, etc.)

- Navigate to the crypto section and search for SUSHI

- Enter the amount you want to buy

- Review the transaction details and confirm your purchase

- Your SUSHI tokens will appear in your Tap wallet

How to sell SUSHI on the Tap App:

- Navigate to your SUSHI wallet in the app

- Select the Sell option

- Enter the amount you want to sell, and what currency you would like in return (crypto or fiat)

- Review and confirm the transaction details

- Your desired currency will appear in the relevant Tap wallet

Conclusion

Sushi has come a long way from its controversial beginnings to establish itself as a cornerstone of the DeFi ecosystem. What started as a fork of Uniswap has evolved into a comprehensive financial platform that offers trading, earning, lending, and more – all without traditional financial intermediaries.

By addressing one of the biggest pain points in DeFi – high Ethereum gas fees – through multi-chain deployment, Sushi makes decentralised finance more accessible to everyday users.

As with any cryptocurrency project, Sushi faces challenges and competition, but its innovative features, passionate community, and continuous development make it a project worth watching in the years to come.

In the same way that Bitcoin revolutionised the financial landscape, stablecoins are here to revolutionise international payments. And they’re ready to go.

We know that in the high-stakes world of global commerce, every second and every cent counts. Now there is a financial technology that can slice through the bureaucratic red tape of international payments, eliminating weeks of waiting and thousands in unnecessary fees.

Welcome to the stablecoin revolution – a game-changing innovation that's quietly rewriting the rules of global business transactions.

The hidden cost of traditional payments

Traditional international payments can often feel like navigating a labyrinth blindfolded. Banks and financial intermediaries create a complex web of fees, delays, and opacity that can transform what should be a straightforward transaction into a costly, time-consuming nightmare.

Multinational corporations have long accepted these inefficiencies as an unavoidable cost of doing business – until now.

Enter stablecoins

Stablecoins represent more than just a technological upgrade; they're a strategic weapon for forward-thinking businesses. Unlike volatile cryptocurrencies, these digital currencies are anchored to stable assets like the Euro or U.S. dollar, providing a rock-solid foundation for international transactions.

Breaking down the benefits:

- Transforming cost structures

Stablecoins don't just reduce costs – they fundamentally reimagine them. By eliminating intermediaries, businesses can slash transaction fees by up to 80%. For a mid-sized multinational, this could mean millions of dollars saved annually, redirected towards innovation, expansion, or talent acquisition.

- Lightning fast transactions

Where traditional bank transfers crawl, stablecoins sprint. A transaction that once took 3-5 business days can now be completed in minutes. Offering a serious competitive advantage - imagine closing an international deal before your competitors have even processed their paperwork.

- Predictability in an unpredictable world

Currency volatility has long been the bane of international business. Stablecoins provide a predictable, consistent value that allows financial planners to create robust, long-term strategies without constantly hedging against exchange rate fluctuations.

The transparency revolution

Blockchain ensures that both sides of the transactions are fully in the know, at all times. Every single transaction is recorded on a distributed ledger, creating an immutable audit trail.

For compliance officers and financial controllers, this means real-time tracking, instant verification, and dramatically reduced risk of fraud.

Offering a new paradigm of business expansion

Offering a passport to global business dealings, small and medium enterprises can now compete on an international stage without the traditional barriers of complex banking relationships or prohibitive transaction costs.

Despite the technological sophistication, the most significant breakthrough of stablecoins is fundamentally human. They restore trust in a financial system that has become increasingly opaque and complex. By providing clear, instantaneous, and secure transactions, stablecoins are rebuilding the most critical currency in business: confidence.

Getting started with stablecoins in business

How stablecoins actually work

Before the “how”, let’s explore the “what”. At their core, stablecoins are digital tokens that operate on blockchain networks but maintain a stable value by being pegged to traditional assets. Unlike Bitcoin or Ethereum, which can fluctuate wildly in price, stablecoins aim to maintain a consistent value, typically 1:1 with a fiat currency like the Euro or US dollar.

The stability is maintained through one of three primary mechanisms:

- Fiat-collateralized: Backed by reserves of traditional currency held by a custodian

- Crypto-collateralized: Backed by other cryptocurrencies with excess collateral to account for volatility

- Algorithmic: Use smart contracts to automatically expand or contract the supply based on demand

For business purposes, fiat-collateralized stablecoins offer the most straightforward and trusted solution, essentially functioning as a digital version of the backing currency with blockchain-powered benefits.

Popular stablecoins for business transactions

Several stablecoins have emerged as leaders in the business space:

US dollar-backed stablecoins:

- USDC (USD Coin), USDT (Tether), USDP (Pax Dollar)

Euro-backed stablecoins:

- EUROC (Euro Coin), EURS (Stasis Euro), agEUR (Angle Euro)

Crypto-backed stablecoins:

- DAI (DAI), FRAX (Frax), USDD (USDD)

Multi-currency backed stablecoins:

- XSGD (Xfers Singapore Dollar), CAUD (TrueAUD), NZDS (New Zealand Dollar Stablecoin)

For most business applications, USDC and USDT offer the most immediate utility due to their widespread acceptance and established compliance frameworks. Be sure to research the ones you are interested in before diving in.

Getting started with the Tap App

The Tap app provides one of the most streamlined onboarding experiences for businesses looking to leverage stablecoins. Get in touch with us here, and an account manager will make contact and discuss how stablecoins can assist with your business needs.

We’ll run you through the entire process – from concept to implementation – explaining everything along the way and ensuring all your questions are answered.

Looking forward

As blockchain technology continues to mature, stablecoins are poised to become more than an alternative – they'll become the standard. Forward-thinking businesses aren't just adopting this technology; they're positioning themselves at the forefront of a global financial transformation.

.webp)

On Friday, 7 March 2025, the White House held its first-ever Crypto Summit, marking a major turning point in how the U.S. government views the crypto industry. The event gathered top industry leaders, policymakers, and key players to discuss the future of digital assets in the U.S.

In this article, we explore what people expected from the summit, what actually happened, and how it’s already shaping the crypto market.

What was anticipated

Before the summit, the crypto community was cautiously optimistic. The Trump administration had already shown interest in digital assets—especially after President Trump appeared at Bitcoin 2024, which got mixed reactions from the market.

Many investors and industry leaders were hoping the summit would bring clearer rules, encourage innovation, and fix past regulatory issues.

Hype grew even more after the announcement of an executive order to create a Strategic Bitcoin Reserve, raising expectations that Bitcoin might soon play a bigger role in the U.S. economy. Spurring a 12% increase across the crypto market, Bitcoin’s price rose above $92,000 in anticipation of the meeting.

Summit proceedings

The summit featured prominent figures such as Michael Saylor (of Strategy), Brian Armstrong (of Coinbase), and Brad Garlinghouse (of Ripple), reflecting the administration's commitment to engaging with key industry stakeholders.

One of the most significant highlights of the gathering was President Trump signing an executive order to create a U.S. Strategic Bitcoin Reserve. The plan is to boost the country’s economic strength by holding Bitcoin seized through asset forfeitures. Described as a “virtual Fort Knox” for digital gold, managed by the Treasury.

Data from Arkham Intelligence reveals that the U.S. government presently owns 198,109 Bitcoin worth $17.5 billion based on current market values.

The executive order also requires federal departments to review their cryptocurrency holdings and find ways to acquire more Bitcoin through “budget-neutral” strategies without burdening taxpayers.

There was also talk about creating a Digital Asset Stockpile, which would include other cryptocurrencies like XRP, Solana (SOL), and Cardano (ADA), to boost the credibility of these digital assets.

Strategic Bitcoin Reserve vs Digital Asset Stockpile

The U.S. government’s approach to digital assets involves two distinct initiatives: the Strategic Bitcoin Reserve and the Digital Asset Stockpile.

The Strategic Bitcoin Reserve aims to hold Bitcoin long-term, using confiscated Bitcoin rather than new government purchases, which has sparked controversy due to Bitcoin's volatility and its decentralised nature, which some argue conflicts with government control.

Critics also worry that the reserve’s reliance on confiscated assets may lead to politically motivated holdings, rather than a clear strategic plan.

In contrast, the Digital Asset Stockpile, managed by the Treasury, will hold other cryptocurrencies like Ethereum, XRP, Solana, and Cardano. Unlike the Bitcoin reserve, the stockpile may allow for more flexibility, including potential sales of its assets.

While the Bitcoin reserve aims to solidify Bitcoin’s place as a strategic asset, the inclusion of other cryptocurrencies in the stockpile raises questions about the government’s broader digital asset strategy. Many aspects still remain unclear.

Market reactions over the outcome

The market's reaction to the summit was mixed. At first, Bitcoin's price surged on optimism. But when it became clear that the Strategic Bitcoin Reserve would rely on existing government holdings instead of new purchases, sentiment shifted. The executive order signed on Thursday confirmed that the reserve would only include Bitcoin the government already holds—mostly from asset forfeitures in criminal and civil cases. Many had expected fresh Bitcoin buys for the fund. While that seems unlikely in the short term, the door has been left open.

This led to a significant price correction, with Bitcoin's value dropping to around $85,000 before stabilising at approximately $88,000, marking a decline of over 3% within 24 hours. Within days, the price dropped to below $80,000.

In addition, Bitcoin ETFs saw significant outflows, with $370 million pulled out as investors reconsidered the impact of the government’s strategy. The wider cryptocurrency market mirrored this volatility, reflecting the complex dynamics between government policy announcements and investor sentiment.

Navigating the future of cryptocurrency regulation

The White House Crypto Summit was a landmark event in how the U.S. government engages with the crypto industry. While the creation of the Strategic Bitcoin Reserve shows a move toward officially recognising digital assets, the market’s reaction made it clear that investors want clearer, more practical policies. The U.S. is at a pivotal moment in shaping the future of digital finance.

The White House Crypto Summit signalled a shift toward embracing crypto, but the real challenge lies ahead—crafting policies that fuel innovation while keeping markets steady. With the right approach, the U.S. could very well lead the global financial revolution, unlocking the full potential of digital assets and setting the stage for a future where opportunity and stability go hand in hand.

%201.webp)

Ever wondered how companies launch those shiny credit cards with their logos on them? Let's dive into the world of card programs and break down everything you need to know to launch one successfully.

What's a card program, anyway?

Think of a card program as your business's very own payment ecosystem. It's like having your own mini-bank, but without the vault, technical infrastructure and security guards. Companies use card programs to offer payment solutions to their customers or employees, whether a store credit card, a corporate expense card, or even a digital wallet.

As you’ve probably figured, the financial world is quickly moving away from cash, and card payments are becoming the norm. In fact, they're now as essential to business as having a product, website or social media presence.

Why should your business launch a card program?

Launching a card program isn't just about joining the cool kids' club – it's about creating real business value and heightened exposure. Here's what you can achieve:

Keep your customers coming back

Remember those loyalty cards from your favourite coffee shop? Card programs take that concept to the next level. When customers have your card in their wallet, they're more likely to choose your business over competitors. Plus, every time they pull out that card, they (and everyone else around) see your brand.

Show me the money!

Card programs open up exciting new revenue streams. You can earn from:

- Interest charges (if applicable)

- Transaction fees from merchants

- Annual membership fees

- Premium features and services

- Insights and information on spending habits

Know your customers better

Want to know what your customers really want? Their spending patterns tell the story. Card programs give you valuable insights into customer behaviour, helping you make smarter business decisions.

Understanding the card program ecosystem

Let's break down the key players in this game:

The dream team

Picture a football team where everyone has a crucial role:

- Card networks (like Visa and Mastercard) are the referees, setting the rules

- Card issuers (like Tap) are the coaches, making sure everything runs smoothly

- Processors (overseen by Tap) are the players, handling all the transactions on the field

Open vs. closed loop: what's the difference?

Open-loop and closed-loop cards differ in where they can be used and who processes the transactions. Let’s break this down:

Open-loop cards:

These cards are branded with major payment networks like Visa, Mastercard, or American Express, and are accepted almost anywhere the network is supported, both domestically and internationally.

Examples: Traditional debit or credit cards, prepaid cards branded by major networks.

Pros: Wide acceptance and flexibility.

Cons: May come with fees for international use or transactions.

Closed-loop cards:

Cards issued by a specific retailer or service provider for exclusive use within their ecosystem. These cards are limited to the issuing brand or select partners.

Examples: Store gift cards (like Starbucks or Amazon), fuel cards for specific gas stations.

Pros: Often come with brand-specific rewards or discounts.

Cons: Limited to specific merchants; less flexibility.

Challenges that may arise

Let's be honest – launching a card program isn't all smooth sailing. Here are the hurdles you'll need to jump:

The regulatory maze

Remember trying to read those terms and conditions? Well, card program regulations are even more complex. You'll need to navigate through compliance requirements that would make your head spin.

Security

Fraud is like that uninvited guest at a party – it shows up when you least expect it. You'll need robust security measures to protect your program and your customers.

We’ve designed our card program to handle these niggles, so that you can bypass the challenges and reap the rewards. With a carefully curated experience, we take care of the setup, programming and hardware so that you can focus on the benefits and users.

Closing thoughts

Launching a card program is like building a house – it takes careful planning, the right tools, and expert help. But when done right, it can become a powerful engine for business growth.

Contact us to get started on building a card program tailored to your company. After all, the future of payments is digital, and there's never been a better time to get started.

Currency volatility is a challenge that businesses operating across borders can’t afford to ignore. Exchange rate fluctuations can erode profits, increase costs, and create financial uncertainty, making it difficult for companies to plan effectively.

For businesses that deal with international transactions, traditional solutions like foreign exchange (forex) hedging can be expensive and complicated. Thankfully now, there's a smarter, more efficient alternative—stablecoins.

Stablecoins offer businesses a way to bypass the unpredictability of currency fluctuations by providing a digital asset pegged to stable currencies like the US dollar. The black and white of it is that they make cross-border payments faster, cheaper, and more reliable.

In this article, we’ll explore why stablecoins are an ideal solution for tackling currency volatility in global financial management.

The challenges of currency volatility in global finance

Global businesses are constantly exposed to currency risks, for a range of reasons, including:

- Geopolitical events – Trade wars, conflicts, or political instability can impact currency values.

- Inflation and interest rate changes – Central bank policies can cause sudden shifts in exchange rates.

- Market speculation – Traders and investors can drive rapid price swings.

For businesses, currency volatility can lead to higher transaction costs, as moving money internationally becomes more expensive. It can also result in unpredictable revenue, making it difficult for companies operating in multiple countries to manage pricing. Additionally, if a currency depreciates suddenly, businesses may face financial losses as profits shrink overnight.

Many businesses use forex hedging strategies (such as forward contracts and options) to manage risk, but these methods are often costly, complex, and require expert knowledge. A simpler, more efficient solution is needed—and that’s where stablecoins come in.

Why stablecoins are the perfect hedge for businesses

Stablecoins offer a practical way for businesses to protect themselves against currency volatility. Unlike traditional cryptocurrencies (which are often highly volatile), stablecoins are pegged to a fiat currency providing a reliable and steady value.

Key benefits for businesses:

- Price stability – With stablecoins, businesses don’t have to worry about sudden exchange rate swings affecting their revenue or costs.

- Fast, low-cost transactions – International payments using stablecoins settle in minutes, not days, with significantly lower fees than traditional banking systems.

- No dependence on banks – Unlike wire transfers, stablecoin payments don’t require intermediaries, reducing delays and extra costs.

- Transparent and secure transactions – Built on blockchain technology, stablecoins ensure auditable, tamper-proof payments, adding an extra layer of security.

For businesses engaging in global trade, payroll, treasury management, or e-commerce, stablecoins offer a modern financial tool to streamline operations and avoid currency-related risks.

Choosing the right stablecoin for your business needs

Not all stablecoins are created equal. Businesses need to choose the right one based on factors like trust, regulation, and network efficiency.

Top stablecoins to consider:

💰 USDT (Tether) – The most widely used stablecoin, but with some concerns around transparency.

💰 USDC (USD Coin) – Fully backed by regulated financial institutions, making it a trusted option.

💰 DAI – A decentralized stablecoin, offering stability without relying on a central issuer.

💰 EUROC (Euro Coin) – A fully backed euro-denominated stablecoin issued by Circle, providing a stable digital alternative for euro transactions.

Key considerations:

- Regulatory compliance – Ensure the stablecoin follows financial regulations in your operating regions.

- Blockchain network – Some stablecoins operate on multiple blockchains (Ethereum, Tron, Solana). Choosing the right network affects transaction speed and fees.

- Liquidity and acceptance – Businesses should opt for stablecoins with high liquidity and broad industry adoption.

Choosing the right stablecoin is essential for seamless global transactions while ensuring stability and security.

The future of stablecoins in global finance

Stablecoins are no longer just a niche tool—they are gaining mainstream acceptance among businesses, financial institutions, and regulators.

Growing adoption – Companies like PayPal and Visa are integrating stablecoins into their payment systems.

Institutional backing – Banks and investment firms are exploring stablecoin use for settlements and asset management.

Regulation on the rise – Governments are working on stablecoin frameworks, aiming to balance innovation with security.

Emerging financial products – Stablecoin-based loans, savings accounts, and remittance services are expanding the financial ecosystem.

As stablecoins evolve, their role in global financial management will only grow, making them a key tool for businesses worldwide.

Conclusion

Currency volatility remains a major challenge for businesses operating globally, as traditional hedging strategies are often expensive and inefficient, leaving companies searching for a better way to manage financial risk.

As outlined above, stablecoins offer a simple, effective, and low-cost solution to tackling currency fluctuations. By providing price stability, fast transactions, and reduced banking dependency, stablecoins empower businesses to operate seamlessly across borders.

For companies looking to future-proof their global financial operations, stablecoins are an answer worth considering. Now is the time to explore how they can be integrated into your business strategy: and we’re here to help.