Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

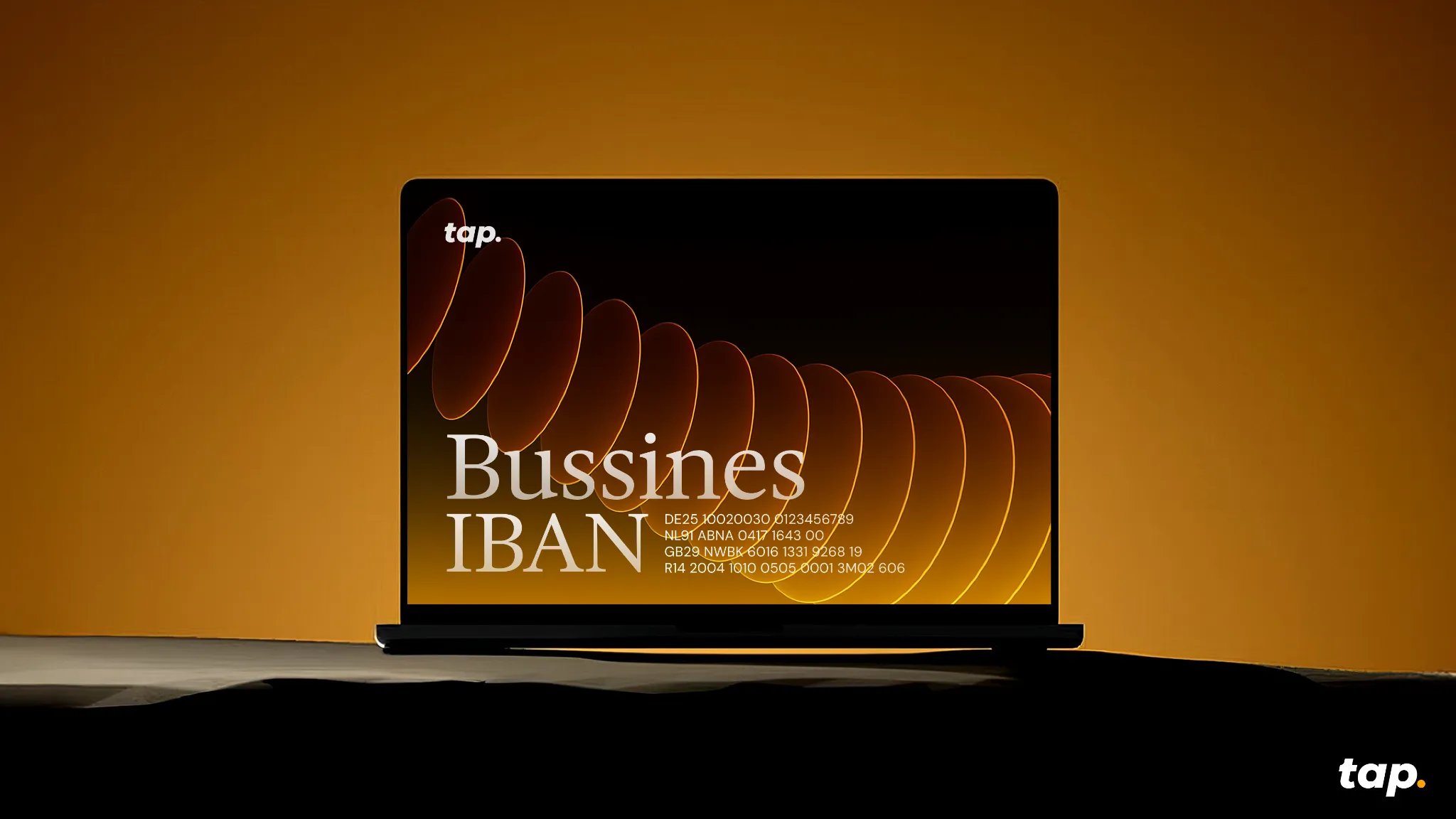

Managing payments across borders remains one of the biggest operational challenges for expanding businesses. While digital transformation has touched nearly every aspect of commerce, international banking is currently lagging behind with separate systems for crypto and traditional currency transactions, creating unnecessary complexity.

Tap solves this problem by offering each business a multi-currency account with a dedicated IBAN that functions as a bridge between these two financial worlds. For businesses handling both crypto and fiat currencies, this means one unified system rather than juggling multiple accounts and conversion processes. This isn't just convenient - it directly impacts your bottom line by reducing transaction fees, speeding up settlements, and simplifying reconciliation.

If you're handling international payments or considering crypto adoption, this could significantly streamline your financial operations. Here's what you need to know.

What is a business IBAN?

An IBAN (International Bank Account Number) serves as your business's financial passport - a standardised identifier recognised across 78+ countries. Unlike traditional account numbers, a Business IBAN follows a structured format that includes country codes, bank identifiers, and your unique account number.

What sets Tap's approach apart is the integration of this established banking standard with crypto functionality. Instead of operating in parallel financial universes, your transactions (whether in euros, dollars, or Bitcoin) flow through a single identifiable channel.

For finance teams, this means the end of reconciliation nightmares. For your customers and partners, it means one consistent payment destination regardless of their preferred currency.

How Business IBANs Work

The mechanics behind modern business transactions

A Business IBAN functions as the digital coordinates for your company's financial location in the global banking ecosystem. When properly implemented, it creates a frictionless path for money to flow into and out of your business regardless of currency type or originating country.

Sending and receiving payments

When receiving payments, your Business IBAN acts as a universal identifier that works across different payment systems. Clients simply enter your IBAN (and sometimes BIC code) into their banking platform, eliminating the confusion of different account number formats across countries.

For outgoing payments, the process works in reverse. You provide the recipient's IBAN, specify the amount, and Tap's platform handles the routing complexities behind the scenes. This standardisation prevents the common errors that lead to payment delays and rejection fees.

What separates Tap's system from conventional banking is the integration layer that works with both crypto and traditional currencies. When a client pays in Bitcoin, for example, you can choose to receive it as cryptocurrency or have it automatically converted to your preferred fiat currency before it reaches your account.

Banking networks demystified

Business IBANs interact with several key payment networks:

SEPA (Single Euro Payments Area): Covering 36 European countries, SEPA processes euro-denominated transfers typically within one business day at low fixed costs. Your Business IBAN automatically routes euro payments through this network without requiring a separate setup.

SWIFT (Society for Worldwide Interbank Financial Telecommunication): The backbone of international banking, SWIFT connects over 11,000 financial institutions worldwide.

Real-world transaction example

Consider a UK-based e-commerce business receiving payment from a German customer:

- The customer initiates a €5,000 payment to the merchant's business IBAN

- The transaction enters the SEPA network and arrives in the merchant's Tap account within hours

- The merchant can either keep the funds in euros or convert to GBP at their preferred timing

- If choosing to convert, Tap executes the exchange at market rates with minimal spread

- The funds become available for business operations, supplier payments, or withdrawal

This same process that once required multiple accounts, banking relationships, and days of processing now happens automatically through a single business IBAN. For businesses managing dozens or hundreds of such transactions monthly, the efficiency gains and cost savings compound significantly.

The ability to handle these complex financial pathways through one unified system represents the core value proposition of modern business IBANs - simplicity on the surface, sophisticated routing underneath.

Cross-border advantages that impact your bottom line

The practical benefits of a business IBAN become immediately apparent in cross-border transactions:

- Reduced rejection rates: correctly formatted IBANs virtually eliminate payment failures due to incorrect account details

- Faster settlement times: direct routing through the SEPA network for European transactions

- Lower transaction costs: fewer intermediaries means fewer fees eating into your margins

- Simplified compliance: clearer transaction trails for more straightforward reporting

Bridging crypto and traditional finance

The crypto market now represents a $2 trillion opportunity that many businesses struggle to tap into due to technical and operational barriers. A business account with Tap eliminates these obstacles by providing:

- Seamless conversion between crypto and fiat currencies

- Consolidated financial reporting across all currency types

- Regulatory compliance built into the platform

- Reduced exposure to crypto volatility through instant conversion options

For businesses cautiously exploring crypto acceptance, this hybrid approach offers a low-risk entry point without requiring major infrastructure changes.

Implementation without disruption

Setting up a business account through Tap requires minimal operational changes:

- Fill in the contact form to initiate a callback

- Complete the business account set-up and verification process

- Receive your unique account with IBAN

- Update payment details with clients and suppliers

- Integrate with your existing accounting systems

The entire process typically takes less than 48 hours, with Tap's team handling the technical heavy lifting.

Is a Tap business account right for your growth strategy?

It's worth considering a business account if your company:

- Operates in multiple countries or currencies

- Needs to reduce payment processing costs

- Wants to accept crypto payments without complexity

- Are looking to streamline financial operations

As payment landscapes continue evolving, businesses that implement flexible, future-proof solutions gain a significant competitive advantage in customer experience and operational efficiency.

Explore how a business IBAN could fit into your financial infrastructure by visiting Tap's business solutions page, from where a dedicated account manager can discuss potential savings based on your specific transaction patterns.

The business world won't wait for outdated payment systems to catch up. The question isn't whether you need more efficient payment solutions - it's how quickly you can implement them.

Let’s make your cross-border payments simple. Schedule a chat with our expert team and explore how Tap can work for your business.

The crypto market just pulled off one of its boldest recoveries in recent memory. What began as a violent sell-off on October 10 has given way to a surprisingly strong rebound. In this piece, we’ll dig into “The Great Recovery” of the crypto market, how Bitcoin’s resilience particularly stands out in this comeback, and what to expect next…

The Crash That Shook It All

On October 10, markets were rattled across the board. Bitcoin fell from around $122,000 down to near $109,000 in a matter of hours. Ethereum dropped into the $3,600 to $3,700 range. The sudden collapse triggered massive liquidations, nearly $19 billion across assets, with $16.7B in long positions wiped out.

That kind of forced selling, often magnified by leverage and thin liquidity, created a sharp vacuum. Some call it a “flash crash”; an overreaction to geopolitical news, margin stress, and cascading liquidations.

What’s remarkable, however, is how quickly the market recovered.

The Great Recovery: Scope and Speed

Within days, many major cryptocurrencies recouped large parts of their losses. Bitcoin climbed back above $115,000, and Ethereum surged more than 8%, reclaiming the $4,100 level and beyond. Altcoins like Cardano and Dogecoin led some of the strongest rebounds.

One narrative gaining traction is that this crash was not a structural breakdown but a “relief rally”, a market reset after overleveraged participants were squeezed out of positions. Analysts highlight that sell pressure has eased, sentiment is stabilizing, and capital is re-entering the market, all signs that the broader uptrend may still be intact.

“What we just saw was a massive emotional reset,” Head of Partnerships at Arctic Digital Justin d’Anethan said.

“I would have another, more positive take: seeing 10B worth of liquidation happen in a flash and pushing BTC prices down 15%+ in less than 24hrs to then see BTC recoup 10% to 110K is a testament to how far we've come and how massive and important BTC has become,” he posted on 𝕏.

Moreover, an important datapoint stands out. Exchange inflows to BTC have shrunk, signaling that fewer holders are moving coins to exchanges for sale. This signals that fewer investors are transferring their Bitcoin from personal wallets to exchanges, which is a common precursor to selling. In layman terms, coins are being held rather than prepared for trade.

Bitcoin’s Backbone: Resilience Under Pressure

Bitcoin’s ability to rebound after extreme volatility has long been one of its defining traits. Friday’s drop admittedly sent shockwaves through the market, triggering billions in liquidations and exposing the fragility of leveraged trading.

Yet, as history has shown, such sharp pullbacks are far from new for the world’s largest cryptocurrency. In its short history, Bitcoin has endured dozens of drawdowns exceeding 10% in a single day (from the infamous “COVID crash” of 2020 to the FTX collapse in 2022) only to recover and set new highs months later.

This latest event, while painful, highlights a maturing market structure. Since the approval of spot Bitcoin ETFs in early 2024, institutional involvement has deepened, creating greater liquidity buffers and stronger institutional confidence. Even as billions in leveraged positions were wiped out, Bitcoin has held firm around the $110,000 zone, a level that has since acted as psychological support.

What to Watch Next

The key question now is whether this rebound marks a short-term relief rally or the start of a renewed uptrend. Analysts are closely watching derivatives funding rates, on-chain flows, and ETF inflows for clues. A sustained increase in ETF demand could provide a steady bid under the market, offsetting the effects of future liquidation cascades. Meanwhile, Bitcoin’s ability to hold above $110,000 (an area of heavy trading volume) may serve as confirmation that investor confidence remains intact.

As the market digests the events of October 10, one lesson stands out. Bitcoin’s recovery isn’t just a matter of luck, it’s a reflection of underlying market structure that can absorb shocks. It is built on a growing base of long-term holders, institutional adoption, and a financial system increasingly intertwined with digital assets. Corrections, however dramatic, are not signs of weakness; they are reminders of a maturing market that is striding towards equilibrium.

Bottom Line

The crash on October 10 was brutal, there’s no denying that. It was one of the deepest and fastest in recent memory. But the recovery has been equally sharp. Rather than exposing faults, the rebound has underscored the market’s adaptability and Bitcoin’s central role.

The market consensus is seemingly leaning towards a reset; not a reversal. The shakeout purged excess leverage, and the comeback underlined demand. If Bitcoin can maintain that strength, and the broader market keeps its footing in the coming days, this could mark a turning point rather than a cave-in.

.webp)

Unless you’ve been living under a rock, you’ve probably heard about ChatGPT… this almighty, em dash-loving AI assistant that seems to pop up in every conversation nowadays regarding productivity and technology.

It truly is everywhere, and honestly, it lives up to the hype.

Think of it as a chatty, super-smart friend you can tap into anytime, whether you’re fine-tuning an email, researching, or tackling coding questions late at night.

But one thing many newcomers don’t quickly realize: not all ChatGPT plans are created equal. The differences between the free version and paid tiers can be striking, from a helpful but occasionally busy assistant to a premium version that's always ready to go deep on your tasks. With multiple plans, variable costs, and constant updates, it’s not always clear which version offers the best value for one's specific needs.

Whether you're watching your budget or ready to upgrade your productivity, knowing which plan aligns with your needs will help you make the best choice. So, let’s dive in.

ChatGPT Pricing Plans Explained

Let’s break down what each subscription tier offers and what you're actually paying for:

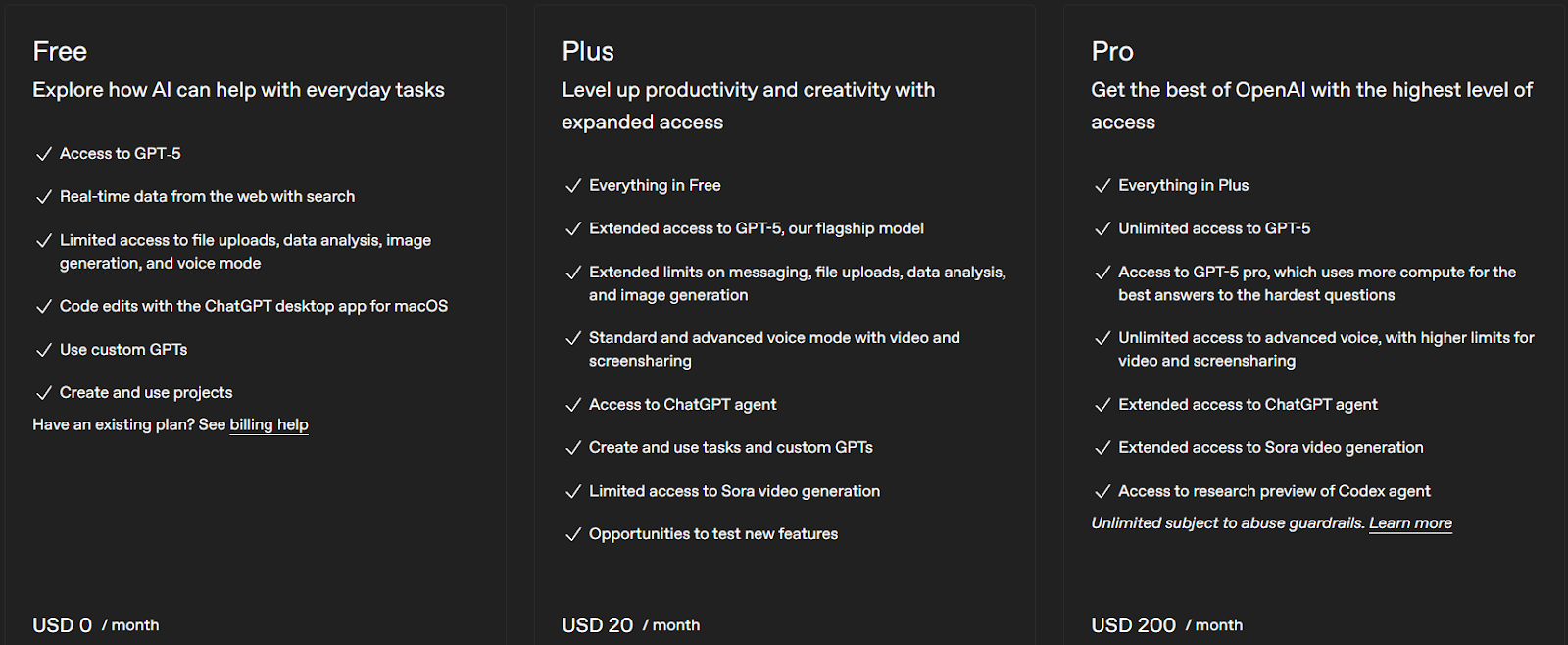

ChatGPT Free Plan

- Access to GPT-5 (automatic fast/reasoning mode) with standard performance.

- Features: voice mode, file uploads, image generation, web browsing, basic analysis.

- Best for: New users exploring ChatGPT’s capabilities without commitment. Offers solid functionality for casual use, though access and speed can be limited during high demand.

ChatGPT Plus ($20/month)

- Priority access to GPT-5 with faster responses.

- Advanced voice mode, early feature access, GPT-4o, custom GPTs.

- Best for: Individuals like freelancers or students needing reliable performance and enhanced features.

ChatGPT Pro ($200/month)

- Unlimited GPT-5 access in "Pro" mode offering deeper, more complex reasoning.

- Premium compute power and research-grade performance.

- Best for: Power users; researchers, engineers, and professionals requiring high-level reasoning and uninterrupted access.

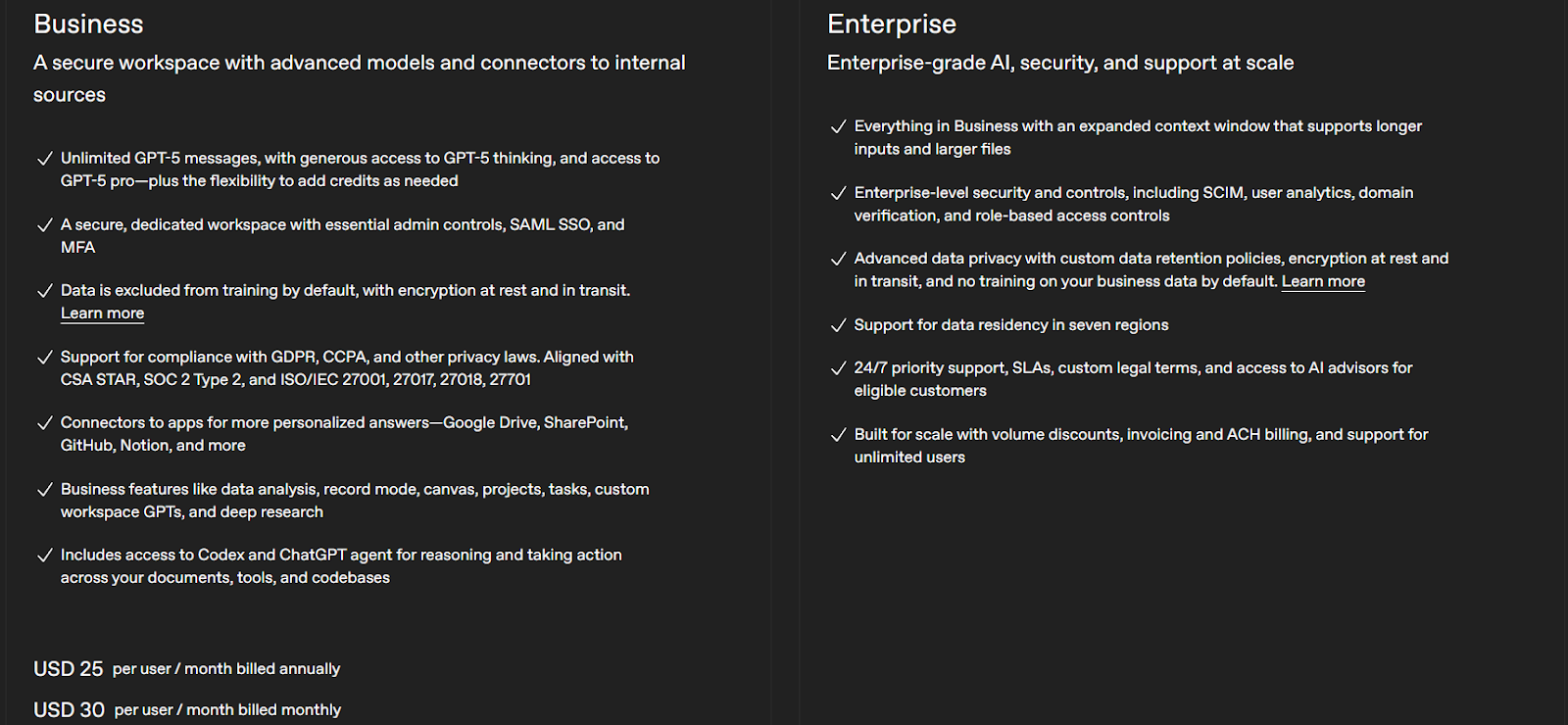

ChatGPT Team ($25–30 per user/month)

- All Plus features plus team-focused tools.

- Collaboration workspace, admin controls, privacy (OpenAI won’t train on your data), shared GPTs.

- Best for: Small teams or startups that value collaboration with enhanced security.

ChatGPT Enterprise (Custom pricing)

- Advanced security, enterprise-grade privacy, integrations (e.g., Google Drive, SharePoint), and dedicated support.

- Best for: Large organisations embedding AI into their core infrastructure with full admin and compliance controls.

Which ChatGPT Plan Is Right for You?

Choosing the right plan is like picking a mobile phone tariff. You want features that fit your needs without overpaying:

- Students: Start with Free; upgrade to Plus if peak usage becomes a drag.

- Freelancers / Pros: Plus is your professional toolkit; it’s reliable, responsive, and worth every dollar.

- Developers / Tech Users: Plus covers light work; Pro fits deep coding or complex data tasks.

- Small Teams / Startups: Team plan adds collaboration and privacy; it’s critical for joint projects.

- Large Enterprises: Enterprise plan solidifies AI as a business workflow pillar.

ChatGPT Hidden Costs & Limitations to Know

Even beyond the listed prices, here are some caveats to keep in mind:

- API Usage: If you use ChatGPT APIs, you'll pay extra per token. For example, GPT-4o mini input tokens cost significantly less than full models.

- Message Limits & Throttling: Paid plans have generous but not infinite usage. Pro handles higher loads; Free can be restrictive.

- Feature Rollouts: Some features debut first to higher plans. Free users may get them later, like being in general admission while Plus users enjoy VIP access.

- Storage Limits: File sizes and frequency may be capped, depending on the plan.

Cost-Saving Tips

- Annual billing: Check for annual pricing discounts, especially on Team plans. Savings of 15–20% are common.

- Track usage: Keep an eye on how many messages or uploads you consume. Some plans never reveal that data clearly.

- Bundle savings: If your organization qualifies, inquire about nonprofit discounts. OpenAI sometimes offers 20–50% off Business or Enterprise plans.

ChatGPT Alternatives: Is There a Better Deal?

ChatGPT isn’t the only tool in town. Here’s a quick look at the competition:

- Claude AI (Anthropic): great at deep reasoning and handling longer contexts

- Perplexity AI: excels in web search, complete with cited sources

- DeepSeek: lower cost, decent performance for budget-conscious users

- Google Gemini: seamless if you already heavily use Google’s ecosystem

Each platform brings its own strengths. ChatGPT remains very versatile, but depending on your needs, one of these may outperform it.

Final Thoughts: Is ChatGPT Worth the Price in 2025?

The value comes down to your personal use. The Free plan is surprisingly capable for casual use. For most professionals, the $20 Plus plan soon pays for itself. For teams and businesses, Team or Enterprise plans consolidate productivity, compliance, and privacy in one package.

The good news is you're not stuck with one choice forever. Experiment with free versions of ChatGPT, Claude, or Perplexity, and upgrade when the fit and features match your workflow. Try them all out. Get crazy with those chats!

We're still figuring out this whole AI conundrum, but one thing's clear, these tools are becoming as essential as e-mail or Google Drive. The question is not whether you'll use AI, it's whether you’ll find a way to make it fit your current needs… knowing you can always level up later.

Slippage is a natural part of trading that happens when there’s a difference between the price you expect to pay for an asset and the price you actually get. It’s common across all markets, from crypto to forex, stocks, and commodities, and it reflects the gap between your order request and the execution price.

Understanding how slippage works helps investors manage expectations, avoid unnecessary losses, and choose smarter trading strategies. In this guide, we’ll explore what causes slippage, how to calculate it, and how to minimize its impact in real trading scenarios.

What Is Slippage In Trading?

Slippage is when an investor opens a trade but between creating the trade and executing the trade; the price changes due to price movements in the greater market. This can often be a costly problem in the financial sector and particularly when trading digital currencies on crypto exchanges.

How Does Slippage Occur?

The two main causes of slippage are volatility and liquidity, outlined in more information below.

Volatility is when the price changes rapidly, as is common in cryptocurrency markets, and as a result the price changes between the time of creating the buy or sell order and the time of execution.

Liquidity concerns on the other hand are when the coin you are trading is not traded very often and the range between the lowest ask and the highest bid is wide. This can cause sudden and dramatic price changes, resulting in slippage. Fewer people trading an asset results in fewer asking prices, resulting in less favourable prices.

This is common among altcoins with low volume and liquidity. While slippage can occur in forex and stock markets too, it is much more prevalent in crypto markets, particularly on decentralized exchanges (DEXs).

There are two types of slippages:

Positive Slippage

Positive slippage is when a trader creates a buy order and the executed price is lower than the price initially expected. This will result in the trader getting a better rate. The same is true for a sell order that experiences a higher price point at trade execution, resulting in more favourable value for the trader. Positive slippage banks profits.

Negative Slippage

Negative slippage is when the trader loses out on the trade, with the price of the buy order higher than expected at the time of execution. The opposite is true for sell orders, meaning that the execution price is lower at the time of execution, similarly resulting in losses for the trader..

How To Calculate Slippage

Slippage can be calculated in two ways, either in dollar amount or percentage. Although to work out the percentage, you will first need the dollar amount. This is calculated by subtracting the price you expected to pay from the price you actually paid. This amount will indicate if you incurred a positive or negative slippage.

Most exchanges express this amount in percentages. This is calculated by dividing the dollar amount of slippage by the difference between the price you expected to get and the limit price. Then multiply that by 100.

Slippage Example in Practice

Imagine you plan to buy 1 BTC for $50,000, but by the time your market order executes, the price has risen to $50,250. You’ve experienced negative slippage of $250.

Now imagine you place a limit order at $50,000, and the order executes at $49,900, that’s positive slippage, meaning you paid less than expected.

To calculate slippage:

Slippage amount = Executed Price − Expected Price

Slippage percentage = (Slippage ÷ Expected Price Difference) × 100

For example, if your expected buy was £50,000 and you paid £50,250, slippage = £250 (0.5%).

This simple math helps traders evaluate execution quality and whether slippage is within acceptable limits.

Slippage Across Different Markets

Crypto Markets:

Crypto markets operate 24/7 and can swing several percent in seconds. On decentralised exchanges (DEXs) like Uniswap, prices depend on liquidity pools; so if liquidity is low, large trades can move the price dramatically. Tokens with small trading volumes, like new altcoins, are particularly prone to high slippage.

Forex Markets:

In the foreign exchange market, slippage often occurs during news releases (e.g., interest rate decisions). Liquidity is usually high, but during volatile moments, even major pairs like GBP/USD can slip several pips.

Stock Markets:

Stock slippage tends to appear at market open or close, when volatility spikes. During major events (earnings reports, Fed meetings) even large-cap shares can gap before orders fill.

Across all asset classes, slippage is most noticeable during low liquidity or high volatility, two conditions traders should always monitor.

How To Avoid Slippage

While one can't eradicate slippage entirely, there are several measures one can take to better manage slippage, as regularly falling victim to negative slippages can result in losing a lot of money.

Create limit orders:

Instead of creating market orders, traders can instead create limit orders as these types of trades don't settle for unfavourable prices. Market orders are designed to execute a trade service as quickly as possible at the current available price.

Set a slippage percentage:

Traders can create a slippage percentage that eliminates trades happening outside of the predetermined range. This can range from 0.1% to 5%, however, if the slippage percentage is too low this could lead to the trade not being executed and the trader missing out on large drops/jumps.

Understand the coin's volatility:

When in doubt, get educated. Learn about the coin's volatility as well as the volatility on the trading platform you are using. Understanding more about previous patterns can assist in making more informed decisions on when to open and close a position, and avoiding negative slippages.

Bottom Line

Slippage is inevitable but manageable. Whether you’re trading crypto, forex, or equities, some gap between expected and actual execution is normal. The goal isn’t to eliminate slippage, but to understand it, anticipate it, and minimize unnecessary exposure.

By combining timing awareness and education, traders can protect profits and execute more confidently, even in fast-moving markets.

.png)

Whether you’re part of the big screen team or prefer to use your smartphone, if you’re looking for a way to add the British pound symbol (£) to your documents, emails, or messages, we have your back. In this guide, we'll walk you through the simple steps to quickly insert the GBP symbol on your device: whether it is MacOS, Windows PC, or smartphone.

What Is the British Pound Symbol (£)?

The British pound symbol (£) represents the pound sterling, the official currency of the United Kingdom. Its three-letter ISO code is GBP (Great British Pound), but some people mistakenly write “GPB.” Remember, it’s always GBP.

Where Did the British Pound Symbol Come From?

The British pound sterling, symbol £, boasts a rich history dating back over 1,200 years. It began as a weight of silver in Anglo-Saxon England and became the official currency in 1694 under William III.

With the growth of the British Empire, it gained global prominence. Despite challenges such as wartime disruptions and the 1967 devaluation, it remained strong. The pound left the gold standard in 1971. Through shifts like Brexit, it endures as a significant global currency, shaped by the UK’s economic journey and historical impact on finance and trade.

According to the Bank of England, the sign originates from the letter L, which is the first letter of the Latin word for libra, meaning a pound of money. Although the exact time when the horizontal line was added is uncertain, it can be traced back to a 1660 cheque in the Bank of England's collection.

Fun fact: in 1970 a new £20 banknote featuring William Shakespeare was issued by the Bank of England, sparking the tradition of including characters that have shaped the United Kingdom on coins and notes.

Simple Ways to Insert the £ Symbol into a Document

Now that we're familiar with the British pound symbol, let's delve into how to type it on both MacOS and Windows keyboards, as well as a smartphone.

For Mac Users

If you're using a Mac, the quickest way is to use a keyboard shortcut. Simply hold down the Option (⌥) key and simultaneously press the number 3.

For Windows Users

On a Windows PC or laptop, you can use different methods:

- Hold down the Shift key and press the number 3 (UK keyboard).

- On US keyboards, press Alt + 0163 using the numeric keypad.

- Alternatively, use the Windows Character Map to copy and paste the symbol.

To make things even easier, some keyboards have the £ sign printed above the number 3 key, providing a visual reminder. Just keep in mind that American keyboards may not include the British pound symbol.

If you prefer a simpler method, you can always copy and paste the pound symbol from here: £

For Smartphone Users

Now, let's move on to inserting the £ sign on your mobile device, whether it's an iOS or Android.

Using your smartphone or tablet, simply switch to the numbers and symbols keyboard on your device, and you'll find the £ symbol as one of the character options. In case you can't locate it, try long-pressing the dollar sign ($) to access more currency symbols.

Keyboard-Free? No Problem

What if you don't have access to a keyboard? Don't worry! There's a way to insert the British pound symbol in popular word processors without typing.

If you're using applications like Microsoft Word or Google Docs, follow these steps:

- In Microsoft Word, go to the "Insert" tab at the top and select "Symbol." In Google Docs, choose "Special Characters" from the drop-down menu.

- Look for the pound sign (£) in the list of characters. In Google Docs, you may need to select "Symbol" first and then navigate to the "Currency" category.

- Click on the £ symbol to insert it into your document.

Proper Usage and Formatting Rules

Knowing how to type the symbol is only half the story. You should also use it correctly. Here are the basics:

- Unlike the United States dollar ($), the British pound symbol (£) always comes before the amount, with no space. Correct: £50.

- Avoid placing it after the number (50£) or with a space (£ 50).

- In professional and international contexts, use the code GBP instead of the symbol (for example: GBP 50).

- Reserve the £ symbol for everyday contexts like receipts, emails, or casual writing.

These formatting rules ensure consistency with standards set by financial institutions like the Bank of England among others.

Conclusion

That’s all there is to it! Now you know how to effortlessly type the British pound symbol (£) on your MacOS computer, Windows PC, or mobile device. Not only that. You’ve also learned its historical background, proper usage rules, and formatting standards.

Feel free to use these methods whenever you need to add this important currency symbol to your content, whether for documents, messages, or financial transactions.

If you need to send pounds overseas, Tap has got you covered with low fees and excellent exchange rates. Send funds from anywhere to anywhere, and for free between Tap users. Simply load either GBP or Euro onto the app and seamlessly send, spend or exchange your funds wherever you are.

Want to earn free cryptocurrency without spending a cent? That’s the promise of airdrop crypto: a blockchain project distributes tokens directly to users as part of a marketing strategy. These airdrops are designed to grow awareness, attract community members, and decentralize token ownership. For end users, it can mean free coins that sometimes turn into thousands of dollars. So, win-win.

Join us, and you’ll learn exactly what a crypto airdrop is, how it works, how much you can earn, and the safest ways to participate. Whether you’re new to tokenization or already active in DeFi channels, airdrops can be a powerful way to expand your portfolio.

Airdropping Facts

- Airdrops in crypto mean free token distribution from a project website or official channel.

- Some airdrops have paid out up to $10,000+ depending on project success.

- Most require simple tasks like following socials, joining a community, or holding a wallet balance.

- Earlier participation means higher probability of receiving valuable tokens.

- Airdrops may be taxable depending on your jurisdiction.

What’s an Airdrop in Crypto?

A crypto airdrop is when a project gives out its native coins for free as a marketing tool to generate hype, grow its network and gain wider adoption, essentially providing free money. On occasion, the coins require small tasks such as following social media pages, and other times they are entirely free of engagements.

These coins are then transferred to current or potential users' wallets for free in the hopes of drawing in more business. Airdrops rose to fame in the ICO boom of 2017 and are still used today. While handed out for free, airdrops can increase in value over time, becoming potentially lucrative to the receivers.

Through distributing coins, projects increase their number of holders (a positive metric for up and coming projects) as well as increase their decentralisation (due to increased token ownership).

How Much Can You Earn from Crypto Airdrops?

The earning potential of crypto airdrops can be surprising. Some are small, worth a few dollars, while others have changed lives. For example, in 2020, Uniswap rewarded active users with 400 UNI tokens, valued at over $1,200 at the time. In 2021, the dYdX airdrop delivered more than $10,000 to certain traders.

The value of an airdrop depends on several factors:

- The project’s success and adoption

- The timing of token distribution vs. market demand

- The level of task requirements and how early you joined

While not guaranteed, dedicated participants who consistently engage with projects and their computing platforms can build a portfolio worth thousands over time.

How Crypto Airdrops Work

At its core, a crypto airdrop is a blockchain-based marketing strategy. It is typically outlined in a project's roadmap and will commence once certain criteria have been met. While airdrops can range from project to project, they typically involve small amounts of cryptocurrencies, often built on Ethereum or other smart chain, being distributed to several wallets.

These coins are usually distributed for free, however, on occasion users will need to perform small tasks related to marketing, like engaging on social media, or hold a certain number of coins in their wallet. A successful airdrop will see its recipients promoting the project and generating hype before being listed on an exchange.

Regarding the actual distribution, a project allocates a portion of its token supply to distribute freely to wallets. This distribution can happen automatically (via snapshot of holders) or manually (users claim via the project website).

Projects airdrop tokens for three main reasons:

- Marketing & awareness: generate buzz through socials and web content.

- Decentralization: increase the number of holders across the community.

- Rewarding users: thanking early adopters or incentivizing loyalty.

Most airdrops happen on Ethereum, but they can also use other blockchains, and increasingly involve both fungible and non-fungible tokens.

What’s The Difference Between An ICO And An Airdrop?

While both are related to new digital currency projects, the major difference between the two is that airdrops are when tokens are distributed for free while ICOs require participants to purchase the project's tokens with an outlined purchase price. ICOs are a source of crowdfunding while airdrops are marketing strategies.

Types of Crypto Airdrops

There are several kinds of airdrops, each with unique requirements and earning potential:

- Standard Airdrops: Free tokens distributed just for registering a wallet address.

- Holder Airdrops: Tokens sent to users who already hold the project’s coin. Stellar once dropped 3B XLM to Bitcoin holders.

- Bounty/Task Airdrops: Require marketing-related engagement like retweeting, joining a Telegram channel, or tagging friends. The project might ask to see proof before distributing the coins.

- Exclusive Airdrops: Sent to a select group, often early adopters or whitelisted wallets.

- Retroactive Airdrops: Rewards for using a project before a certain date. Uniswap is a classic example of this, distributing 400 UNI to each wallet that had engaged in the platform before a certain date. The governance token allowed holders to vote on the project’s future developments.

Typically, retroactive and exclusive airdrops offer the highest payouts because they reward active community involvement.

The Downsides to Airdrops

There are malicious actors out there who take advantage and have created airdrop scams. These scams might involve a "project" airdropping tokens into a wallet but when the holder attempts to move these tokens their wallet is drained.

Another example of an airdrop scam is a project enticing you to sign up for the airdrop by connecting your wallet only to take your wallet details and gain access to your account. These are typically conducted through websites and fake Twitter and Telegram accounts that look very similar to the real deal but are actually phishing scams.

It's important to do your own research when engaging in an airdrop, and know that a project will never require you to send funds in order to "unlock" tokens or require you to provide a seed phrase or private key.

Another downside to airdrops is that projects can create an incorrect impression of growth. If thousands of coins are distributed to thousands of wallets this might cause the project to look busier and more adopted than it actually is. When judging a project by this metric, make sure that it has an active trading volume that reflects the number of wallet holders. You don’t want to see plenty of holders with minimal activity.

Red Flags

Not every airdrop is safe. Be on the lookout for these red flags:

- Fake websites and phishing scams imitating real projects.

- Tokens that drain wallets when moved.

- Requests for private keys or seed phrases (always a scam).

How to Get Started with Crypto Airdrops

Getting started is easier than most beginners think. Here’s what you’ll need:

- Set up a wallet compatible with ERC-20 and other popular standards.

- Follow aggregator sites like Airdrop Alert or CoinMarketCap’s airdrop page for upcoming opportunities.

- Join project communities on Discord, Telegram, or Twitter to stay informed about announcements.

- Create social media accounts dedicated to airdrops: useful for bounty requirements.

- Keep your wallet safe and updated: never share private keys.

Want to be ready for the next big crypto airdrop? While some airdrops reward users simply for interacting with a new protocol, many of the most succulent opportunities are reserved for those who hold a specific token. For example, past airdrops have targeted Bitcoin (BTC) and Ethereum (ETH) holders to bootstrap new projects on their respective blockchains.

So, do you need BTC or ETH or SOL maybe? Look no further and get them on Tap! Tap offers a seamless all-in-one platform where you can easily on-ramp from fiat to crypto and get the coins you need, without extra steps. Find the exact cryptocurrency you need to qualify and grab your airdrop before anyone else!

.webp)

.webp)