Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

Every move on Ethereum (sending crypto, minting an NFT, using a dapp) comes with a cost. That cost is called gas. It’s not just a fee - it’s the fuel that keeps the network running.

Knowing how gas works means you’re not just using Ethereum, you’re using it smarter. You can time transactions, avoid peak congestion, and cut your costs. Here we explore how it works and how to take control in a simple and easy-to-understand way.

What are Ethereum gas fees?

Let’s start with the basics: gas fees are the cost of using the Ethereum network. Any time you do something - like send ETH or swap tokens - you’re asking the network to do work. That work takes computing power, and gas fees are what you pay to get it done.

These fees serve three critical functions:

- Compensate validators for their work

- Secure the network from spam attacks, and

- Prioritise transactions during busy periods.

When the network buzzes with activity, the fees naturally rise as users compete for limited block space. Picture Ethereum as a busy highway during rush hour. More traffic means higher tolls, but the road remains secure and functional for everyone willing to pay the current rate.

How Ethereum gas fees work

Every gas fee breaks down into a simple formula that establishes your specific transaction cost:

Total fee = (base fee + priority fee) × gas limit

Let’s break it down:

- The base fee is the minimum cost to get your transaction into a block. It goes up when the network is busy and is burned (destroyed) to help reduce ETH supply.

- The priority fee (tip) is an extra amount you add to speed things up (like tipping for faster service).

- The gas limit is how much work your transaction needs. Bigger, more complex actions need a higher limit.

Another important element to understand is that gas prices are measured in Gwei, where 1 Gwei equals 0.000000001 ETH. A typical token swap might use 30,000 gas units. If the current base fee sits at 25 Gwei and you add a 5 Gwei tip, your total cost becomes:

(25 + 5) × 30,000 = 900,000 Gwei = 0.0009 ETH

Let’s say at $2,500 per ETH, that transaction would cost $2.25.

Why Ethereum gas fees fluctuate

Gas fees move with the rhythm of the network. When demand is low, fees drop. When things heat up, they spike.

Big events like new token launches, NFT drops, or market surges can therefore clog the network. More users = more competition for space. That’s when the base fee goes up (remember the formula above: total fee = (base fee + priority fee) × gas limit).

The base fee adjusts with every block (around every 15 seconds). It rises when blocks are more than 50% full and drops when they’re under that threshold.

The type of transaction also matters:

- A simple ETH transfer uses about 21,000 gas units.

- A complex smart contract call: +/-200,000.

- A typical Uniswap swap costs 3–5x more than a basic transfer.

And don’t forget ETH’s price. Even if gas stays steady in Gwei, rising ETH makes each transaction more expensive in dollars.

Quick Tip: Check gas trackers before major transactions. A few minutes of timing can save significant money.

How to check Ethereum gas prices in real time

Active users monitor gas prices like traders watch market charts. There are several tools that provide real-time visibility into the network’s condition.

- Etherscan’s gas tracker (for deep analytics)

Etherscan provides in-depth gas analytics including real-time rates, historical charts, and insights into average and peak fees. It also offers optimisation tips like identifying “safe low‑cost windows” for transactions. - Rabby wallet (for user-friendly alerts)

Rabby’s mobile and browser wallet features built-in gas monitoring, showing current prices and offering “Gas Top Up” functionality. It also supports push notifications (via its GasAccount feature) for favourable conditions. - MetaMask (for fully integrated wallet visibility)

MetaMask displays live gas rates directly in its interface and dashboard. You'll see options like Low, Market, or Aggressive for gas speeds, and it even shows fiat equivalents beside token balances.

Most gas trackers display slow, standard, and fast fee tiers, helping you balance cost and speed.

It’s also worth knowing that slow transactions may take 5-10 minutes but can save you 20-30% on fees, while fast ones aim to process within a couple of minutes, at a premium price.

Gas prices also follow weekly patterns. Fees are usually lower on weekends, when institutional and high-frequency trading slows down. And if you’re not in a rush, consider transacting during early morning hours (2–6 AM EST), often the cheapest window of the day.

Ethereum gas fees before and after the merge

Over the years, Ethereum has gone through major upgrades that changed how gas fees work, though granted not always in the ways people expected.

In 2021, the London Hard Fork introduced EIP-1559, swapping chaotic gas auctions for a more predictable pricing model: a base fee + tip. It made fee estimates more stable, but didn’t necessarily make them cheaper.

Then came The Merge in 2022, shifting Ethereum to proof-of-stake. It cut energy use and made block processing more efficient. But despite common belief, it didn’t slash gas fees overnight.

However, The Merge did lay the groundwork for future upgrades (like sharding and rollups) that will unlock real, lasting fee reductions at scale.

Looking ahead, upgrades like Proto-Danksharding aim to scale Ethereum and bring fees down for good.

How to reduce ETH gas fees

Despite what some might tell you, cutting gas fees isn’t about luck, it’s more about smart choices and good timing. Here are some options:

Use Layer 2s

Networks like Arbitrum, Optimism, and Base offer the biggest savings, sometimes up to 90–95% cheaper than the Ethereum mainnet. For example, a $50 swap on mainnet might cost just $2-$5 on these platforms, with the same level of security. (More on this below).

Simulate before you send

Tools like Tenderly and DeFi Saver let you test complex transactions first, helping you avoid failed attempts that still burn gas.

Pick your moment

As mentioned above, prices drop when the network is quiet. Use gas trackers to spot the best times to transact.

Batch when you can

Some protocols let you combine multiple actions into one transaction, so you pay one base fee instead of several.

Layer 2 solutions that cut gas costs

Layer 2 networks are the future of Ethereum scaling. They can handle thousands of transactions off-chain, then settle them on Ethereum in one go, cutting costs and speeding things up.

- Arbitrum leads in total value locked. It offers fast transactions for just $0.10-$0.50 and supports most major DeFi apps, making it feel like a cheaper version of the mainnet.

- Optimism offers similar savings, with bonus perks like token rewards for developers through its RetroPGF program, driving growth and innovation.

- Base combines low fees with easy fiat onramps. It’s great for beginners moving from exchanges into DeFi.

These networks are able to do what they do by using rollups, a tech that bundles hundreds of transactions into one. Think of it like carpooling: everyone shares the cost of the ride, but still gets where they need to go.

Who receives Ethereum gas fees?

Since The Merge, Ethereum handles gas fees in a smart split between rewards and supply control.

- Validators (who secure the network) earn priority fees - tips from users that reward them for processing transactions. This keeps the network safe and running smoothly.

- Base fees, on the other hand, are burned (permanently removed from circulation). When the network is busy, more ETH is burned, which can reduce supply and make ETH more valuable over time.

Will Ethereum gas fees ever go down?

Ethereum’s roadmap promises big fee cuts, but the biggest changes will take time.

- Proto-Danksharding (EIP-4844) is expected in upcoming upgrades. It will slash Layer 2 costs by 10-100x by creating dedicated space for rollup data. This upgrade is the closest major step toward lower fees.

- Full Danksharding, further down the line, will boost Ethereum’s capacity massively, making tiny, sub-penny transactions on Layer 2 networks a reality without sacrificing security or decentralisation.

- Ethereum’s founder, Vitalik Buterin, envisions the mainnet as a secure settlement layer, while Layer 2s handle most daily transactions quickly and cheaply.

If all goes as planned, popular Layer 2s could offer fees under one cent within 2-3 years, opening the door for micro-transactions and true global use.

Comparison: Ethereum vs other chains

Blockchain networks take different paths when balancing cost, security, and decentralisation, and fees reflect those choices. Let’s take a look at its biggest competitors.

Solana vs Ethereum

Solana offers super low, sub-penny fees and processes around 3,000 transactions per second (far more than Ethereum’s +/-15 TPS). This speed comes from different architectural choices, but with tradeoffs like higher hardware requirements and occasional network outages.

Ethereum, meanwhile, prioritises security and decentralisation, scaling through Layer 2 solutions to keep fees competitive.

Binance Smart Chain vs Ethereum

Binance Smart Chain (BSC) delivers low fees, typically $0.10–$0.50 per transaction, but it sacrifices decentralisation by relying on fewer validators and tighter connections to centralised infrastructure.

Ethereum maintains a more decentralised network while scaling costs through Layer 2s, keeping security front and centre.

Avalanche vs Ethereum

Avalanche strikes a balance with moderate fees ($0.50–$2.00), high throughput, and strong security. However, its ecosystem remains smaller than Ethereum’s rich DeFi landscape, which benefits from Layer 2 scaling and a strong focus on decentralisation.

Final thoughts

Understanding Ethereum gas fees puts you in control, allowing you to save money and utilise the network more efficiently. While fees can fluctuate, smart timing, Layer 2 solutions, and upcoming upgrades promise a future of faster, cheaper transactions.

While Ethereum continues to prioritise security and decentralisation, its gas fee roadmap reflects a careful balance between innovation and accessibility, paving the way for broader adoption and everyday use.

USDT is everywhere in crypto: powering trades, bridging platforms, and acting as a go-to safe haven when markets turn volatile. Backed by Tether, it promises the stability of a dollar with the speed of digital assets. But how secure is that promise?

In this article, we’ll unpack how USDT works, the risks beneath the surface, and why it remains a key player in the crypto economy.

What is USDT and why it matters

Think of USDT (Tether) as the crypto world's attempt to create digital cash that doesn't give you a heart attack every time you check its price. Launched back in 2014 by a company called Tether Limited, USDT was designed to be a "stablecoin" - a cryptocurrency that maintains a steady 1:1 relationship with a certain fiat currency: the US dollar. One USDT should always equal one dollar. Simple, right?.

Well, like most things in crypto, it's a bit more complicated than that.

USDT has become the utility tool of crypto, offering a fast and flexible option to move in and out of positions without cashing out to traditional fiat. It’s the common language of the crypto ecosystem, enabling smooth transfers, seamless trading, and a place to park value when markets swing.

Tether Limited, the company behind USDT, operates globally, with roots in the British Virgin Islands and operations stretching from Hong Kong to the Bahamas. Unlike central banks, Tether isn’t printing dollars, though: it issues tokens, claiming each one is backed 1:1 by assets in reserve.

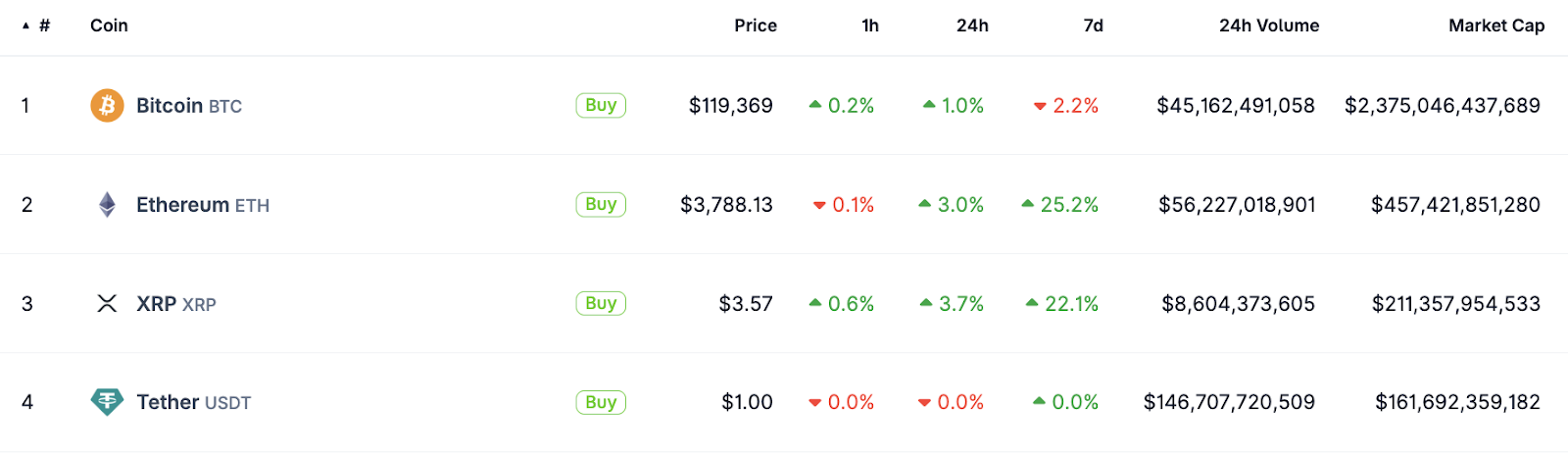

With over $160 billion in circulation as of mid-2025, USDT isn’t just a trading tool, it’s foundational infrastructure for the crypto economy. It’s also the largest stablecoin on the market, based on market cap and 24-hour trading volume.

Top cryptocurrencies by market cap at the time of writing. Source.

Is USDT safe?

The short answer? USDT exists in a grey area between "reasonably safe for what it is" and "proceed with caution."

The slightly longer answer? Here's what you need to know at a glance:

What's working:

- Maintained its dollar peg through multiple market crashes

- Backed by a mix of cash, government securities, and other liquid assets

- Most widely accepted stablecoin across exchanges and platforms

- Regular attestations from accounting firms

What's concerning:

- Limited transparency compared to some competitors

- Regulatory uncertainty and past legal issues

- Concentration risk (too big to fail, too big to save?)

- Not fully backed by cash alone

The reality check: USDT has survived crypto winters, bank runs, and regulatory pressure for nearly a decade. While it's not risk-free (nothing in crypto is), it's proven more resilient than many predicted. For short-term trading and payments, most users find it reliable. For long-term wealth storage? That's where you might want to consider your options more carefully.

How USDT is backed: understanding Tether's reserves

Here’s where things get more complex and where much of the scrutiny around Tether lies.

In simple terms, USDT operates like a digital receipt: you deposit dollars, and in return, you get tokens you can use across the entire crypto ecosystem. But what happens to those dollars? Are they sitting in a vault, or being put to work?

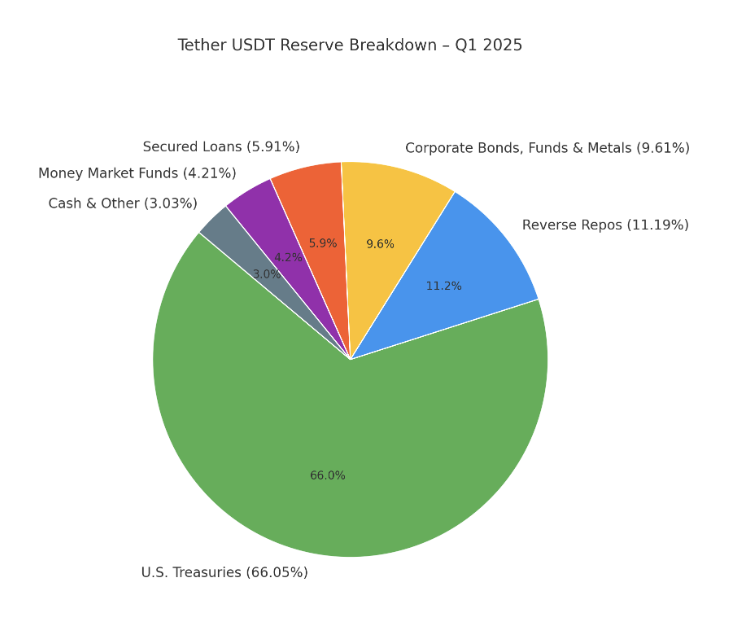

Tether has long opted for the investment route. Instead of holding pure cash, it backs USDT with a diversified portfolio of assets. According to its Q1 2025 attestation from BDO, Tether’s reserves looked roughly like this:

The shift toward U.S. Treasuries and away from riskier assets marked a significant improvement in its reserve quality. While not fully audited, Tether does publish quarterly attestations from BDO, providing some visibility into how reserves are managed. It’s not a full audit, but it’s a step forward from the opaque reporting of earlier years.

That being said, past controversies still shape how Tether is perceived. In 2019, Tether admitted that USDT was not fully backed by cash at all times and revealed it had lent $850 million to Bitfinex, its sister company. This led to a high-profile settlement with the New York Attorney General in 2021, requiring Tether to improve transparency and cease operations in New York.

Again, to put it in simple terms: imagine your bank quietly loaning out customer deposits to a related company without clearly telling you. Not necessarily illegal, but definitely a breach of trust for users expecting a 1:1 backed stablecoin.

Regulatory scrutiny & legal risks

If USDT were a person, it would probably have a thick file folder in regulatory offices around the world. Sure, being the largest stablecoin makes you a big target, but Tether has also found itself in the crosshairs of regulators who are still figuring out how to handle the crypto revolution.

In the United States, Tether operates in something of a regulatory twilight zone. The company has faced pressure from agencies like the Commodity Futures Trading Commission (CFTC), which fined Tether $41 million in 2021 for making false statements about being fully backed by US dollars.

The European Union is taking a more structured approach with its Markets in Crypto-Assets (MiCA) regulation, which will require stablecoins to be backed by highly liquid assets. This could actually work in Tether's favour, as they've already been moving in that direction.

Emerging markets present their own challenges. Some countries have embraced USDT as a hedge against local currency instability, while others have banned it outright, not far from a global game of regulatory whack-a-mole.

For users, the regulatory risks are real but indirect. If major jurisdictions crack down hard on Tether, it could affect the token's liquidity and usability. However, a complete overnight shutdown seems unlikely given USDT's deep integration into the crypto ecosystem.

The bigger risk might be increased compliance requirements that could make using USDT more cumbersome, similar to how traditional banking has become more regulated over time.

How safe is USDT for holding assets?

This is where we need to have an honest conversation about what "safe" means in crypto land.

For short-term use (days to weeks):

USDT works pretty well. If you're trading crypto or need to park funds briefly between investments, it's like using a decent hotel - not your forever home, but comfortable enough for a short stay.

The peg has held remarkably well through various market conditions, and liquidity is excellent across most major platforms.

For medium-term holdings (months):

Here's where things get a bit more nuanced. USDT has survived multiple "stress tests", including the Terra Luna collapse, FTX implosion, and various banking sector scares. However, you're essentially trusting that Tether's reserve management continues to work smoothly and that no major regulatory bombshell disrupts operations.

For long-term wealth storage (years):

This is where many experts start raising eyebrows. Holding large amounts in any stablecoin for extended periods comes with risks that compound over time. You're exposed to regulatory changes, potential company mismanagement, and the general "unknown unknowns" that come with relatively new financial instruments.

Essentially, USDT is like keeping money in a foreign bank account. It might work great for a while, but you're subject to the laws, regulations, and business practices of entities outside your home jurisdiction.

The key insight from the crypto community is diversification. Even USDT supporters rarely recommend putting all your eggs in the Tether basket.

Security best practices when using USDT

Using USDT safely isn't just about trusting Tether - it's also about protecting yourself from the various ways things can go wrong in the crypto world.

Platform risk management: Remember, USDT is only as safe as the platform you're using it on. The token itself might be fine, but if you're holding it on a sketchy exchange that gets hacked or goes bankrupt, you could lose everything. Stick to regulated platforms only.

Diversification strategies: Many crypto users often split their stablecoin holdings across multiple tokens and platforms. Think of it as not putting all your digital eggs in one digital basket. As an example, some might hold 40% USDT, 40% USDC, and 20% in other stablecoins or traditional assets.

For crypto beginners: Start small, learn the ropes, and, if you wish, gradually increase your holdings as you become more comfortable. Use well-established exchanges for your first purchases, enable two-factor authentication on everything, etc. Treat your crypto security like you would your online banking, that's essentially what it is.

USDT vs other stablecoins

The stablecoin world isn't a one-horse race, and understanding the alternatives helps put USDT's safety in perspective.

USDT vs USDC

USDT dominates in usage and global liquidity. It's the most widely accepted stablecoin across exchanges, DeFi platforms, and payment rails. But it has faced criticism over the years for a lack of full audits and historical opacity around reserves.

USD Coin (USDC), issued by Circle, takes a different approach. It’s often seen as the “regulated” stablecoin, with monthly attestations and a conservative reserve mix (primarily cash and short-term U.S. Treasuries).

- USDT is ideal for fast-moving markets and broad platform compatibility.

- USDC appeals to those who prioritise transparency and regulatory oversight.

USDT vs DAI

DAI takes a completely different route. Issued by MakerDAO, it’s a decentralised stablecoin backed by overcollateralised crypto assets like ETH, not fiat. There’s no single company behind it, just smart contracts and community governance.

While DAI offers full on-chain transparency and avoids centralised custodians, it also comes with higher complexity and potential risks tied to smart contract bugs or extreme market conditions.

- USDT provides speed and simplicity, backed by a traditional corporate structure.

- DAI offers a decentralised alternative, ideal for DeFi-native users.

USDT vs BUSD

BUSD, once a major player backed by Binance and Paxos, was phased out in 2024 due to regulatory pressure. It serves as a reminder that centralised stablecoins depend on both market forces and compliance frameworks, and can be wound down unexpectedly.

While USDT remains standing, BUSD’s sunset reinforces the importance of evaluating who’s behind the stablecoin and how stable their operations really are.

What happens if Tether fails?

Let's play out a hypothetical scenario: what if USDT actually collapsed?

Given USDT's role as the primary trading pair and liquidity source for much of the crypto market, a Tether failure would be like removing a major highway from a city's transportation network. The immediate effects would likely include:

Market chaos: Traders scrambling to exit USDT positions would create massive selling pressure across crypto markets. We're talking about potentially the largest fire sale in crypto history, as billions of dollars worth of USDT holders try to convert to other assets simultaneously.

Liquidity crisis: Many smaller cryptocurrencies rely heavily on USDT trading pairs. Without this liquidity, some tokens might become effectively untradeable, at least temporarily.

Contagion effects: Other stablecoins might face runs as confidence in the entire sector erodes. Even well-managed stablecoins could struggle if everyone tries to redeem at once.

The silver lining: The crypto ecosystem has become more resilient over time. Alternative stablecoins like USDC have grown substantially, providing some redundancy. Additionally, the market has survived previous "extinction-level events" and adapted.

Conclusion: Is USDT worth the risk?

USDT isn’t perfect, but it’s proven its place in the crypto ecosystem. With high liquidity and global acceptance, it’s a practical choice for trading, payments, and short-term value storage.

However, concerns around transparency and regulatory clarity mean it’s not ideal for long-term holding or users who prioritise full visibility. But like any financial tool, its value depends on how you use it.

The smart approach is to understand the trade-offs, diversify across stablecoins, and align your choices with your goals and risk tolerance. As the space evolves, USDT remains useful, but it’s just one part of a broader digital finance strategy.

.webp)

So you've probably heard about ChatGPT by now - it's that AI assistant that seems to pop up in every conversation about productivity and technology. And honestly? It lives up to the hype.

Think of it as having a really smart friend who's available whenever you need them, whether you're stuck on a work project, trying to craft the perfect email, or just curious about something random at 11 PM.

But here's what I wish someone had told me when I first started using it: not all ChatGPT plans are created equal. The differences between the free version and the paid tiers can be pretty dramatic, we're talking about the difference between having a helpful but sometimes busy friend versus having a dedicated assistant who's always ready to dive deep into whatever you need.

Whether you're trying to stretch every dollar as a student or you're ready to invest in serious productivity tools, understanding these pricing tiers will help you make the right choice for your situation. Let’s dive in.

ChatGPT pricing plans explained (2025)

Let's break down what each plan offers and what you're actually paying for:

ChatGPT Free Plan

Cost: $0

Features:

- Access to GPT-4o mini

- Limited GPT-4o access

- Standard voice mode

- File uploads

- Image generation

- Web browsing

- Advanced data analysis

Who it's for: Perfect for curious newcomers who want to explore AI without commitment. Think of it as your test drive - you'll get a taste of what ChatGPT can do, but with some speed bumps along the way.

ChatGPT Plus Plan

Cost: $20 per month

Features:

- Higher capacity than ChatGPT free — users can send 80 messages

- Priority access to GPT-4o

- Faster response times

- Advanced voice mode

- Early access to new features

- Custom GPTs

Who it's for: This is the sweet spot for most individual users. If you're a freelancer, student, or professional who relies on AI regularly, this plan transforms ChatGPT from a helpful tool into an indispensable work companion.

ChatGPT Team Plan

Cost: $30/seat/mo monthly or $25/seat/mo annually

Features:

- Everything in Plus

- Available for 2 or more users

- Workspace collaboration tools

- OpenAI won't train on your workspace's data

- Admin controls and usage insights

- Custom workspace GPTs

Who it's for: Small to medium teams who need to collaborate on AI projects while maintaining some privacy controls. It's like having a shared digital workspace where everyone can contribute.

ChatGPT Pro Plan

Cost: $200 a month per user

Features:

- Unlimited access to GPT-4o

- Advanced reasoning capabilities

- Research-grade performance

- Premium compute resources

- All previous plan features

Who it's for: This is for the AI power users: researchers, developers, and professionals who need unrestricted access to the most advanced capabilities. It's a significant investment, but for those who live and breathe AI, it can be worth every penny.

ChatGPT Enterprise Plan

Cost: Around $60 per user per month with a minimum of 150 users and a 12-month contract

Features:

- Enterprise-grade privacy and data analysis capabilities

- Connectors to internal sources for more personalised answers (Google Drive, SharePoint, GitHub, Dropbox, and more)

- Custom deployment options

- Advanced security controls

- Dedicated support

- Custom usage limits

Who it's for: Large organizations that need enterprise-level security, compliance, and integration capabilities. This plan isn't just about using AI, it's really about making AI part of your business infrastructure.

Which ChatGPT plan is right for you?

Choosing the right plan feels a bit like picking the perfect phone plan - you want enough features without paying for things you'll never use. Here's how to think about it:

For students

Recommendation: Start with Free, upgrade to Plus if needed (students often have unpredictable usage patterns). The free plan lets you handle research, writing assistance, and study help without breaking the bank. If you find yourself hitting limits regularly during busy academic periods, the Plus plan's reliability makes it worth the investment.

For freelancers and individual professionals

Recommendation: ChatGPT Plus ($20/month). This is your professional toolkit. Whether you're a content creator, consultant, or entrepreneur, the Plus plan gives you consistent access to advanced features that can significantly boost your productivity. Think of it as investing in a skilled assistant who never takes sick days.

For developers and technical users

Recommendation: ChatGPT Plus or Pro (depending on intensity). If you're coding occasionally, Plus handles most development tasks beautifully. But if you're building AI applications or need extensive code generation, the Pro plan's unlimited access prevents frustrating interruptions during deep work sessions.

For small teams and startups

Recommendation: ChatGPT Team ($25-30/user/month) The collaboration features and data privacy controls make this worthwhile for teams of 2-10 people. You're not just paying for individual access, you're investing in team productivity and maintaining professional data standards.

For large enterprises

Recommendation: ChatGPT Enterprise (custom pricing). When you need AI integrated into your business processes with enterprise-grade security, this becomes a strategic investment rather than just a productivity tool. The custom pricing reflects the complex needs of large organisations.

ChatGPT hidden costs and limitations to know

Before you commit to any plan, let's talk about the fine print - because nobody likes surprise costs.

API usage beyond regular plans

If you're building applications that use ChatGPT's API, you'll encounter separate pricing based on token usage.

API pricing alone (GPT-4: $0.012/prompt tokens, $0.024/completion tokens) doesn't tell the whole story as actual costs often double when you factor in servers, optimisation, and hidden infrastructure needs.

Message limits and throttling

Even paid plans have limits. The free plan caps your usage significantly, while Plus gives you more headroom but isn't unlimited. If you're a heavy user, you might hit these walls sooner than expected.

Feature access restrictions

Some advanced features roll out to higher-tier plans first. Free users often wait months for features that Plus subscribers get immediately. It's like being in the general admission section while others enjoy VIP access.

Storage and file handling

While most plans include file uploads, there are size limits and processing restrictions that might affect your workflow if you regularly work with large documents or datasets.

ChatGPT alternatives: is there a better deal?

Let's be honest – ChatGPT isn't the only sheriff in town anymore. Here's how the competition stacks up:

Claude AI (Anthropic)

Pricing: Free tier + $20/month Pro Strengths: Excellent for analysis and reasoning, longer context windows Best for: Users who need thoughtful, nuanced responses and can work with longer documents.

Perplexity AI

Pricing: Free + $20/month Pro Strengths: Web search integration, cited sources Best for: Research-focused users who need current information with source verification.

DeepSeek

Pricing: Free and paid version, with the paid model consisting of an individual plan with a $20-$50 monthly fee and a team plan that comes with custom pricing Strengths: Competitive performance at lower costs Best for: Budget-conscious users who want good performance without premium pricing

Google Gemini

Pricing: Free tier + Google One AI Premium ($20/month) Strengths: Deep Google ecosystem integration Best for: Users heavily invested in Google's productivity suite

The truth is, each AI has its personality and strengths. ChatGPT excels at versatility and ease of use, but depending on your specific needs, one of these alternatives might be a better fit for your workflow and budget.

Final thoughts: is ChatGPT worth the price in 2025?

The bottom line of ChatGPT pricing boils down to how much you’re actually going to use it.

If you're just dabbling occasionally, the free plan is surprisingly decent. For most working professionals, the $20 Plus plan pays for itself quickly (think of it as buying back an hour of your week). And for teams or businesses? The higher-tier plans make sense when AI becomes a core part of how you operate.

The good news is you're not stuck with one choice forever. Try the free versions of ChatGPT, Claude, and Perplexity to see which one clicks with how you work. Then upgrade the one that feels most natural.

We're still figuring out this whole AI thing, but one thing's clear: these tools are becoming as essential as email or Google Drive. The question isn't whether you'll use AI - it's finding the right fit for where you are now, knowing you can always level up later.

Private label cards are branded payment solutions that enable businesses to offer customized rewards, incentives, and financing options to their customers and employees. These cards serve as powerful tools for driving customer loyalty, improving cash flow management, and gaining valuable spending insights. In this article, we'll guide you through the concept of private label cards, their key benefits for businesses, and delve into how they work.

What are private label cards?

Private label cards are branded payment cards issued by businesses to their customers or employees, allowing them to make purchases or access funds within a specific ecosystem or network. Unlike traditional debit or credit cards issued by a bank, private label cards are a product tailored to the branding and specific needs of the issuing company.

These cards differ from traditional cards in several ways. Firstly, they are not tied to a specific financial institution but rather to the company's brand and loyalty program. Secondly, they often offer unique rewards and incentives tailored to the business's products or services. Additionally, private label cards provide businesses with valuable customer data and insights, enabling targeted marketing efforts and personalized experiences.

Private label cards and fintechs

In recent years, fintech platforms have revolutionized the issuance and management of private label cards. These technology-driven companies act as program managers, handling the end-to-end process of card issuance, transaction processing, and compliance adherence.

By partnering with fintech platforms like Tap, businesses can efficiently launch and manage their private label card programs, leveraging advanced technologies, scalability, and industry expertise without the need for extensive in-house resources.

How private label cards benefit businesses

Private label cards empower businesses to strengthen customer relationships, optimize financial operations, and gain a competitive edge through tailored rewards, data-driven insights, and robust security measures. Let’s explore some of these concepts below:

Drive business

Private label cards offer businesses a range of benefits that can drive customer loyalty, enhance brand recognition, and streamline operations. By offering customizable rewards and loyalty programs tailored to their products or services, businesses can incentivize customers to make repeat purchases while simultaneously collecting data on customer preferences, fostering long-term relationships and brand advocacy.

Cash flow management

Private label cards provide businesses with a valuable tool for cash flow management. By encouraging customers to use their branded cards, companies can receive payments more quickly, improving their working capital and financial flexibility.

Collect data and analytics

One of the key advantages of private label cards is the wealth of data and analytics they provide. Businesses can gain insights into customer spending patterns, preferences, and behaviours, enabling data-driven decision-making and targeted marketing strategies.

Security benefits

Additionally, private label card programs prioritize security and fraud prevention measures. Fintech platforms offering these solutions employ advanced technologies and protocols to safeguard customer information and transactions, providing businesses and their customers with peace of mind.

The differences between private label and co-branded cards

Private label cards are issued by a single retailer or business, bearing their branding and tailored rewards program. Co-branded cards, however, involve a partnership between a merchant and a major card network (Visa, Mastercard), carrying dual branding.

In general, private label cards offer more customization and control for the merchant but may have limited acceptance outside their network. They can also drive stronger loyalty but require more resources to manage.

Co-branded cards, on the other hand, have wider acceptance but less flexibility in terms of rewards/benefits. As they leverage an existing card network's infrastructure, they offer less differentiation.

The choice depends on the merchant's goals; private label are beneficial for deeper customization and loyalty while co-branded cards off wider acceptance and shared resources with a card network partner.

How private label cards work

Private label cards are issued through a collaborative process involving businesses and fintech platforms. Businesses define the card program's features, branding, and reward structure, while fintech platforms handle the technical and operational aspects. As program managers, fintech companies then oversee card issuance, transaction processing, and data management, leveraging their expertise and scalable technologies.

The importance of compliance and adherence to regulatory requirements cannot be underestimated or overlooked when looking at the issuance of private label cards. Fintech platforms need to ensure that card programs comply with industry standards, data privacy laws, and anti-fraud measures, providing businesses with a secure and reliable payment solution.

Regular audits and risk assessments are conducted to maintain compliance and mitigate potential risks. Businesses must always do their research before engaging in private label card issuance with a fintech platform.

Examples of use cases

Private label cards can offer a range of use cases across various industries. See several examples below:

Retail and e-commerce

In the retail and e-commerce sectors, they serve as powerful loyalty tools, incentivizing customers with tailored rewards and exclusive offers. Businesses can leverage these cards to drive repeat purchases and foster brand loyalty. An example would be the Amazon Store Card.

Corporate expense management

Corporate organizations utilize private label cards for streamlined expense management, enabling employees to make authorized purchases while providing detailed spending data for analysis and budgeting purposes.

These cards also facilitate employee incentive and recognition programs, rewarding high-performers with customized benefits and privileges. An example of this would be a company card issued to employees to use for company expenses.

Specific purposes

Additionally, private label cards can be issued as prepaid cards for specific purposes, such as payroll disbursements, gift cards, or restricted-use cards for controlled spending. This versatility allows businesses to tailor card programs to their unique needs, ensuring efficient fund management and targeted usage.

An example of this could be a corporate-branded preloaded gift card for promotional purposes allowing holders to buy something in-store using the card.

How to create a private label card for your business

With Tap, you can seamlessly integrate private label card programs into your operations. Tap streamlines the entire card issuance and management process, allowing companies to leverage off their advanced technologies and industry expertise.

By partnering with Tap, you gain access to a scalable and flexible solution, enabling you to launch and adapt card programs efficiently, tailored to your company’s specific needs. Tap's platform offers robust features, real-time analytics, and end-to-end support, empowering every businesses to deliver tailored payment experiences while ensuring compliance and security.

With Tap, you have the power to not only launch and adapt your card programs efficiently but also to customise the fees charged to your users. Our approach is entirely flexible, allowing you to set charges that align with your clientele's needs. Our platform offers unparalleled freedom, allowing you to tailor your card programs precisely to your company's needs and goals.

Conclusion

In summary, private label cards empower businesses with a versatile payment solution that promotes customer loyalty, optimizes operations, and delivers valuable data insights. Whether for retail, corporate, or specific use cases, private label cards offer a competitive edge through tailored rewards, data-driven strategies, and enhanced customer experiences - paving the way for business growth.

Please contact xxx for further information on setting up your private label card.

There is no denying that innovation in the technology sector has amplified the fast-paced world of finance, instigating constant transformation from brands that want to stay ahead. As with any fast-paced industry, many trends emerge as companies fight to remain relevant. One such trend we will be exploring is the increase in white-label cards and the companies facilitating the issuing of them.

The process of issuing white-label cards has emerged as a powerful solution in the fintech space, offering customized payment experiences that cater to the unique needs of both businesses and customers. In this article, we will delve into the world of white-label cards, exploring its benefits, applications, and why it has become such a popular choice for financial institutions and fintech companies.

Understanding white-label cards

White-label cards, also known as private-label credit cards, involve the practice of businesses providing other businesses with the opportunity to offer customized credit or debit cards to their customers. Trusted financial institutions or fintech companies issue these cards on behalf of the businesses, while still reflecting the company's branding.

This approach allows businesses to incorporate their logo and branding on the private label credit card, granting the business ownership and control over the card's identity, all without the burden of creating or designing it from scratch.

By partnering with an established financial institution or fintech company, businesses can save time, effort, and resources by leveraging ready-to-use payment solutions instead of going through the costly and complex process of obtaining licenses from companies like Mastercard or Visa.

The shift toward customized payment solutions

Traditional banking systems have often been perceived as slow in adopting new systems and embracing innovation. As the demand for personalized payment experiences continues to grow, businesses are leveraging the opportunity to keep up with the evolving needs of customers seeking customized payment solutions and private-label credit cards.

Consumers today seek customized solutions that align with their preferences and reflect the brands they trust. This shift in consumer behavior has paved the way for white-label cards and in turn, card issuers, which offers businesses the ability to tailor payment solutions and private-label credit cards to their customers' needs.

Third-party establishments are now offering streamlined payment solutions to these businesses, allowing them to leverage this new technology without needing to complete extensive and costly onboarding processes. Instead, the card issuing companies undergo this process and once accredited are able to provide full-service payment options to their clients.

With co-branded private-label credit cards, customers can unlock a multitude of rewards, bonus points, and exclusive discounts that can be utilized across various services, retailers, and online shopping platforms. By offering these enticing benefits, businesses are able to enhance the overall purchasing experience for their customers, cultivating loyalty and satisfaction.

Private-label credit cards can also come in the form of virtual cards, allowing users to make online payments or use services like Apple Pay with their unique account that essentially acts as a bank account.

The advantages and benefits of private label credit cards

The advantages of businesses utilizing the services of white-label card issuers are numerous, benefiting not only businesses but individuals too.

For businesses

Firstly, white-label card programs offer a cost-effective alternative to building an in-house card program. By partnering with established providers, businesses can save on upfront costs, development time, and ongoing maintenance expenses.

White-label card programs also offer flexibility and scalability, making them suitable for businesses of all sizes. Whether you're a startup looking to launch a branded payment card quickly or an established business seeking to enhance your payment offerings, the processing of white-label cards can be tailored to meet your unique requirements.

From a branding perspective, white-label card programs provide businesses with heightened visibility and customer loyalty. By issuing branded payment cards, businesses can strengthen their brand identity and foster a deeper connection with their customers. Customizable card designs, exclusive rewards programs, and personalized customer experiences all contribute to building customer loyalty and market competitiveness.

For consumers

For individuals, white-label cards bring convenience and security. These cards can be seamlessly integrated into existing payment ecosystems, enabling individuals to make secure transactions while enjoying the benefits and perks offered by the businesses they frequent.

Whether it's earning loyalty points, accessing exclusive discounts, or tracking expenses, white-label cards empower individuals with a seamless and tailored payment experience.

Addressing security and regulatory concerns

As with any financial solution, security and regulatory compliance are paramount. Financial institutions and fintech companies offering white-label card programs implement robust security measures to safeguard cardholder data and prevent fraudulent activities.

Compliance with industry regulations, such as PCI DSS (Payment Card Industry Data Security Standard), ensures that customer data is handled securely. Additionally, data privacy and protection measures are put in place to give cardholders peace of mind when using white-label cards.

Examples of brands that have launched a private label card

Below are two examples of prominent brands that have embraced the white-label card trend in its early stages.

Square

In 2019, Square, a prominent payment processing company, partnered with Marqeta's white-label card processing platform to introduce the Square Card, a business debit card designed specifically for Square's sellers. This strategic move allowed Square's business customers to gain immediate access to funds, reducing their reliance on traditional banking services.

By leveraging Marqeta's solution, Square not only expanded its product portfolio but also strengthened its relationships with its existing customer base.

Shopify

Another notable fintech player, Stripe, offers businesses APIs to issue their own credit cards, debit cards, and prepaid cards. Shopify, a renowned e-commerce platform, utilized Stripe's card issuing services to create the Shopify Balance Card, designed to help businesses start, grow and run their operations.

This card enables over 1 million of Shopify’s merchants to access their earnings instantly through a smart money management tool. The response to the launch was immediate and overwhelmingly positive, as over 100,000 small businesses in the United States embraced Shopify Balance accounts within the first four months.

Through the implementation of Stripe's white-label solution, Shopify added significant value to its merchants, setting itself apart from other e-commerce platforms.

Benefits reported in the case studies

Companies that have implemented the processes to issue white-label cards have reported several potential benefits, including:

Speed to market

Utilizing a white-label solution enables companies to launch card programs more swiftly. These solutions handle critical aspects such as regulatory compliance, technology development, card design, and manufacturing, which can be time-consuming and costly to manage in-house.

Cost reduction

White-label solutions generally require less investment than building a card-issuing infrastructure from scratch. Consequently, companies can save costs associated with development, maintenance, and compliance.

Enhanced customer engagement and retention

By offering a branded payment solution, companies can build stronger customer loyalty. Customers appreciate the convenience and exclusive perks that come with these cards, leading to higher engagement and retention rates.

Creation of new revenue streams

Companies can generate additional revenue streams by offering supplementary services through the card, such as cash-back rewards, premium subscriptions, or lending services.

What businesses should consider before implementing

Implementing a white-label card program requires careful planning and consideration. While the benefits listed above have been reported by companies that have implemented these strategies, these outcomes are not guaranteed. Businesses need to collaborate closely with their chosen white-label card issuer to ensure a smooth implementation process.

This involves outlining the desired features and functionalities, integrating with existing payment infrastructure and systems, and training staff to manage the program effectively. Technical requirements, such as API integrations and data synchronization, should be addressed to ensure a seamless user experience.

Future trends and innovations in white-label card programs

Looking ahead, the future of issuing white-label cards holds great promise, driven by several key factors:

Market demand

The ever-evolving demand for financial services presents a significant opportunity. Regardless of their size or industry, businesses are increasingly seeking to expand their service offerings with payment and financial solutions.

This trend aims to cultivate customer loyalty and explore new revenue streams. As a result, the demand for issuing white-label cards is expected to continue its upward trajectory.

Technological advancements

Fintech advancements, such as the widespread use of APIs and enhanced security measures, are simplifying the adoption of issuing white-label cards for businesses. As technology continues to progress, platforms issuing white-label cards are poised to become even more efficient, flexible, and secure, providing a seamless experience for both businesses and customers.

Developments in financial institutions' regulations

The regulatory landscape in the financial services sector is undergoing significant changes. Regulatory bodies worldwide are displaying a willingness to embrace fintech innovation, with some jurisdictions creating "fintech sandboxes" that facilitate controlled testing of new financial products. Should this trend persist, it could streamline the process for businesses to launch the issuing of white-label card programs.

The future of companies issuing white-label cards faces challenges primarily from increasing competition in the market. With more companies entering the space, businesses may experience pricing pressures and difficulties in standing out from the competition. To succeed, businesses need to differentiate themselves through innovation, personalized experiences, and strong partnerships.

They must also navigate regulatory uncertainties, address cybersecurity risks, and employ strategies to seize opportunities and overcome challenges in this dynamic sector. Continuous monitoring, agile decision-making, and a proactive approach are essential for businesses operating in the white-label card-issuing industry.

Tap’s white-label card solution

Tap’s business portfolio offers a streamlined card-issuing service to businesses of all kinds. Fully accredited, Tap is able to offer its partnering companies Mastercard-powered private cards for a fraction of the cost and time it would take if done directly with the financial services company.

In 2023, Tap provided Bitfinex, the longest-running and most liquid major crypto exchange, with a white-label prepaid card solution. By providing the behind-the-scenes financial infrastructure, the established exchange provided its clients with a unique payment solution and created a new revenue stream for the business.

With the necessary card-issuing license and already-established in-house processing system in place, businesses can quickly create their own white-label cards through Tap’s fiat and cryptocurrency-to-fiat funded card programs and other innovative services.

Conclusion

White-label card issuing is revolutionizing the payment landscape, with its rise signifying a powerful solution in the fintech space, delivering customized payment experiences that cater to the unique needs of businesses and customers.

As technology continues to drive innovation, white-label card programs offer speed to market, cost reduction, enhanced customer engagement, and the creation of new revenue streams. However, businesses should carefully consider implementation factors and address potential challenges, such as regulatory compliance and cybersecurity risks.

The future of private-label credit card issuing appears promising, driven by market demand, technological advancements, and regulatory developments. To capitalize on this trend, businesses must differentiate themselves in a competitive landscape and adapt to evolving market dynamics.

Tap's white-label card solution exemplifies the potential of such programs, providing businesses with streamlined card-issuing services and opening new opportunities for revenue growth. As the industry continues to evolve, white-label card issuing will play a vital role in shaping the future of finance, enabling seamless and tailored payment experiences for businesses and individuals alike.

%201.webp)

Ever wondered how companies launch those shiny credit cards with their logos on them? Let's dive into the world of card programs and break down everything you need to know to launch one successfully.

What's a card program, anyway?

Think of a card program as your business's very own payment ecosystem. It's like having your own mini-bank, but without the vault, technical infrastructure and security guards. Companies use card programs to offer payment solutions to their customers or employees, whether a store credit card, a corporate expense card, or even a digital wallet.

As you’ve probably figured, the financial world is quickly moving away from cash, and card payments are becoming the norm. In fact, they're now as essential to business as having a product, website or social media presence.

Why should your business launch a card program?

Launching a card program isn't just about joining the cool kids' club – it's about creating real business value and heightened exposure. Here's what you can achieve:

Keep your customers coming back

Remember those loyalty cards from your favourite coffee shop? Card programs take that concept to the next level. When customers have your card in their wallet, they're more likely to choose your business over competitors. Plus, every time they pull out that card, they (and everyone else around) see your brand.

Show me the money!

Card programs open up exciting new revenue streams. You can earn from:

- Interest charges (if applicable)

- Transaction fees from merchants

- Annual membership fees

- Premium features and services

- Insights and information on spending habits

Know your customers better

Want to know what your customers really want? Their spending patterns tell the story. Card programs give you valuable insights into customer behaviour, helping you make smarter business decisions.

Understanding the card program ecosystem

Let's break down the key players in this game:

The dream team

Picture a football team where everyone has a crucial role:

- Card networks (like Visa and Mastercard) are the referees, setting the rules

- Card issuers (like Tap) are the coaches, making sure everything runs smoothly

- Processors (overseen by Tap) are the players, handling all the transactions on the field

Open vs. closed loop: what's the difference?

Open-loop and closed-loop cards differ in where they can be used and who processes the transactions. Let’s break this down:

Open-loop cards:

These cards are branded with major payment networks like Visa, Mastercard, or American Express, and are accepted almost anywhere the network is supported, both domestically and internationally.

Examples: Traditional debit or credit cards, prepaid cards branded by major networks.

Pros: Wide acceptance and flexibility.

Cons: May come with fees for international use or transactions.

Closed-loop cards:

Cards issued by a specific retailer or service provider for exclusive use within their ecosystem. These cards are limited to the issuing brand or select partners.

Examples: Store gift cards (like Starbucks or Amazon), fuel cards for specific gas stations.

Pros: Often come with brand-specific rewards or discounts.

Cons: Limited to specific merchants; less flexibility.

Challenges that may arise

Let's be honest – launching a card program isn't all smooth sailing. Here are the hurdles you'll need to jump:

The regulatory maze

Remember trying to read those terms and conditions? Well, card program regulations are even more complex. You'll need to navigate through compliance requirements that would make your head spin.

Security

Fraud is like that uninvited guest at a party – it shows up when you least expect it. You'll need robust security measures to protect your program and your customers.

We’ve designed our card program to handle these niggles, so that you can bypass the challenges and reap the rewards. With a carefully curated experience, we take care of the setup, programming and hardware so that you can focus on the benefits and users.

Closing thoughts

Launching a card program is like building a house – it takes careful planning, the right tools, and expert help. But when done right, it can become a powerful engine for business growth.

Contact us to get started on building a card program tailored to your company. After all, the future of payments is digital, and there's never been a better time to get started.

.webp)

.webp)