Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

Want to expand your brand, boost customer loyalty, and unlock new revenue streams - without the cost or complexity of building your own financial infrastructure? White label card solutions do all this (and, you guessed it, more).

These fully customisable payment products, from physical to digital cards, let businesses seamlessly enter the world of embedded finance. In an era where speed, innovation, and customer experience set market leaders apart, offering your own branded payment cards can give you the competitive edge you need.

How do white label card solutions work?

White label card solutions operate through partnerships between businesses and specialised card issuance platforms that handle the technical and regulatory aspects of payment cards.

These solutions typically involve collaboration between the business (program manager), a banking partner (the licensed issuer), and a technology provider that manages the card program infrastructure (in this case, Tap).

The process typically follows these steps:

- A business partners with a white label card provider (Tap)

- The provider handles backend infrastructure, compliance, and processing

- The business applies its branding and determines card features

- Cards are issued to customers under the business's brand

Different types of white label cards serve various business needs:

- Debit cards link to customer accounts and withdraw funds directly

- Credit cards provide revolving credit lines with various repayment options

- Prepaid cards allow customers to load funds in advance for future spending

Modern white label solutions leverage robust APIs for seamless integration with existing business systems, enabling customisation of everything from application processes to transaction notifications and rewards programs.

The strategic advantage of branded cards

When businesses implement branded cards into their service portfolio, they're doing more than just adding a payment option – they're creating an extension of their brand that customers interact with daily.

These white-label card solutions allow companies to maintain complete brand consistency while leveraging sophisticated payment technology that would otherwise require significant investment to develop internally.

Financial service providers aren't the only businesses benefiting from this approach. Companies across sectors – from retail and travel to healthcare and professional services – are discovering how branded cards can transform customer relationships and create new revenue streams.

Key benefits of white label card solutions

Branding and customisation

White label cards serve as powerful brand reinforcement tools through both physical and digital card designs that maintain visual identity. Every transaction becomes a brand interaction, increasing visibility and recognition. Businesses can customise card designs, packaging, and digital experiences to create a cohesive brand ecosystem.

Fast market deployment

Traditional card program development can take years and millions in investment. White label solutions compress this timeline dramatically, allowing businesses to launch card programs in weeks rather than years, accelerating time-to-market and competitive advantage.

Increased revenue streams

Beyond enhancing customer experience, branded cards also create tangible financial benefits. Companies implementing these solutions typically see:

- Revenue from interchange fees

- Increased customer retention and lifetime value

- Higher average transaction values

- Reduced customer acquisition costs through enhanced service offerings

These financial advantages often make branded card programs self-sustaining or even profitable in their own right, transforming what might be considered a cost center into a revenue generator.

Customer loyalty and engagement

Custom rewards programs aligned with specific business offerings create powerful incentives for continued engagement. By connecting card usage with core business services, companies create virtuous cycles that strengthen both payment card usage and primary service engagement.

Data insights and analytics

White label card programs provide comprehensive data insights on customer spending patterns and preferences. These insights allow businesses to refine offerings, personalise marketing, and identify new opportunities based on actual customer behaviour.

Beyond traditional banking: the evolution of card solutions

The fintech revolution has democratised what was once the exclusive domain of traditional banks. Today's white-label card solutions offer businesses unprecedented flexibility and control. These capabilities allow businesses to not just participate in the financial ecosystem but to actively shape it according to their unique value proposition.

White label card security and compliance

Security and regulatory compliance form the foundation of successful white label card programs. Modern solutions incorporate multiple layers of protection:

- Advanced security features: EMV chips, tokenisation, and 3D Secure technology protect transactions from fraudulent activity

- Regulatory compliance: Established providers handle complex requirements including PCI DSS, KYC/AML regulations, and financial licensing

- Custom controls: Businesses can implement specific spending rules, transaction limits, and merchant category restrictions

- Real-time monitoring: Sophisticated fraud detection systems identify unusual patterns and potential threats before they result in losses

Working with experienced white label providers ensures these critical security and compliance components are properly managed while allowing businesses to focus on their core competencies.

Creating seamless customer experiences

Modern consumers expect frictionless experiences across all touchpoints with a brand. Branded cards enable businesses to extend this seamless experience into payment interactions, whether online or in person. By controlling the card experience, companies can ensure consistency at every stage of the customer journey.

This seamless integration becomes particularly valuable when businesses can connect card usage with their core services. For example, a travel company's branded card might offer enhanced rewards for bookings, creating a virtuous cycle that strengthens both card usage and primary service engagement.

Comparison: White label vs. custom-built card solutions

Businesses considering card issuance typically evaluate two approaches:

White label solutions:

- Lower upfront investment

- Faster implementation (weeks/months vs. years)

- Reduced regulatory burden

- Ongoing operational support

- Limited by provider's capabilities

Custom-built solutions:

- Complete control over features

- Potentially lower per-transaction costs at scale

- Greater differentiation potential

- Significant expertise required

- Higher regulatory and compliance burden

For most businesses, white label solutions provide the optimal balance between customisation and practicality, allowing them to focus resources on their core competencies while still delivering compelling financial products.

In terms of timelines, Tap’s streamlined process takes your white label card solution from concept to delivery in just 12 weeks.

How to choose the right white label card provider

Selecting the right partner for your white label card program requires careful evaluation of several factors:

- Customisation depth: How much control will you have over card appearance, features, and user experience?

- Technical integration: Does the provider offer robust APIs and documentation that align with your technical capabilities?

- Compliance expertise: What regulatory requirements will the provider handle, and what remains your responsibility?

- Scalability: Can the solution grow with your business and accommodate increasing transaction volumes?

- Support structure: What level of ongoing assistance is available for both technical and operational issues?

Leading providers differ in their strengths, with some focusing on specific verticals or use cases. The right choice depends on your specific business needs, technical resources, and growth objectives.

Future trends in white label card solutions

The white label card industry continues to evolve rapidly with several emerging trends:

- Digital-first cards: Virtual cards becoming primary with physical cards as optional supplements

- Crypto integration: Adding crypto capabilities to traditional card products

- Buy Now, Pay Later: Incorporating flexible payment options within white label offerings

- AI-enhanced features: Sophisticated spending insights and fraud detection through artificial intelligence

- Embedded finance expansion: Cards becoming entry points to broader financial service ecosystems

For forward-thinking businesses, the question isn't whether to explore branded card offerings – it's how quickly they can be implemented to capture the substantial benefits they provide.

Getting started without the complexity

The technical complexity that once made card issuance prohibitively difficult has been eliminated by modern fintech platforms. Today's white-label solutions handle regulatory compliance, fraud prevention, and technical integration, allowing businesses to focus on what they do best.

By partnering with the right platform, companies can launch branded card programs quickly, creating lasting competitive advantages that will be increasingly difficult for latecomers to overcome.

To learn more about how white label card solutions can influence your specific business, fill in your details here and a specialised account manager will walk it through with you.

In our interconnected global economy, currency symbols are everywhere, whether you're planning international travel, running an e-commerce business, formatting financial documents, or simply trying to understand pricing on a foreign website. Knowing how to recognise and use currency symbols correctly is essential.

The long and the short of it is that currency symbols are shorthand notations that represent different monetary units around the world.

Unlike ISO currency codes (like USD or EUR), these symbols provide a quick visual reference that transcends language barriers. From the familiar dollar sign ($) to the Indian rupee symbol (₹), each symbol tells a story of economic identity and cultural significance.

Understanding currency symbols becomes particularly important when dealing with international transactions, creating multilingual websites, formatting invoices, or developing financial applications. They're not just academic knowledge - they're practical tools for anyone engaged in global commerce or travel.

What is a currency symbol?

A currency symbol is a graphical representation used to illustrate a specific monetary unit. These symbols serve as universal shorthand, allowing people to quickly identify and work with different currencies without needing to spell out the full currency name or remember complex three-letter codes.

For example, the dollar sign ($) immediately signals US dollars, while the euro symbol (€) represents the European Union's currency. The British pound uses (£), and the Japanese yen employs (¥). Each symbol has been carefully designed to be distinctive and memorable.

It's important to distinguish currency symbols from ISO currency codes. While the symbol for US dollars is $, the ISO code is USD. The symbol for euros is €, but the ISO code is EUR. Symbols are visual and compact, while codes are standardised three-letter abbreviations used primarily in financial systems and international banking.

Currency symbol placement rules (before or after the number?)

The placement of currency symbols relative to numbers varies significantly across countries and cultures, following local conventions rather than universal rules.

In most English-speaking countries, the symbol appears before the number: $100, £50, or A$75 for Australian dollars. However, many European countries place the symbol after the number: 100€ in France, or 50₽ in Russia.

Some currencies have unique formatting conventions. In Cape Verde, you might see 20$00, where the dollar sign appears before the decimal portion. Similarly, some Latin American countries write $20.00 or $20,00 depending on their decimal separator conventions.

When working with international documents or websites, always research the local convention for the specific country and currency you're dealing with. This attention to detail demonstrates cultural awareness and professionalism in global business communications.

Complete list of world currency symbols by region

Europe

The Americas

Asia & Pacific

Middle East

Africa

Cryptocurrencies

How to type currency symbols on your keyboard

Windows Shortcuts

- Dollar ($): Shift + 4

- Euro (€): Alt + 0128

- British Pound (£): Alt + 0163

- Japanese Yen (¥): Alt + 0165

- Cent (¢): Alt + 0162

Mac Shortcuts

- Dollar ($): Shift + 4

- Euro (€): Option + Shift + 2

- British Pound (£): Option + 3

- Japanese Yen (¥): Option + Y

- Cent (¢): Option + 4

Additional Methods

For symbols not available through keyboard shortcuts, you can use Unicode codes, copy from character maps, or use online symbol generators. Some fonts may not support all currency symbols, so consider using web-safe fonts like Arial or Times New Roman if your specific font isn’t supportive.

Currency symbols in documents and spreadsheets

Microsoft Word

Navigate to Insert > Symbols to access the complete symbol library. You can also use Alt codes or set up custom keyboard shortcuts for frequently used symbols.

Microsoft Excel

Use Format Cells > Currency to automatically apply currency formatting. Excel recognises most major currency symbols and can format numbers accordingly.

Google Docs

Go to Insert > Special Characters, then search for "currency" to find available symbols. You can also bookmark frequently used symbols for quick access.

Google Sheets

Use Format > Number > Currency to apply currency formatting. Google Sheets automatically detects your location and suggests appropriate currency symbols.

Most traded and recognised currency symbols

The most globally recognised and traded currency symbols include:

- US Dollar ($) - The world's primary reserve currency, used in international trade and forex markets

- Euro (€) - The second most traded currency, representing 19 European Union countries

- British Pound (£) - One of the oldest currencies still in use, significant in global finance

- Japanese Yen (¥ or JP¥) - Major Asian currency and key player in international markets

- Chinese Yuan (¥ or CN¥) - Rapidly growing importance in global trade and reserves

- Indian Rupee (₹) - Representing one of the world's largest economies

Closing summary

Understanding currency symbols is more than academic knowledge - it's a practical skill that enhances your ability to navigate our global economy. Whether you're travelling abroad, conducting international business, or simply trying to understand pricing on a foreign website, knowing how to recognise and properly use currency symbols will have you one step ahead.

In a market where volatility is the norm and headlines change daily, it’s no surprise that many investors are shifting their focus from high-risk speculation to long-term financial security. Safe, long-term investments aren’t about playing it small, they’re about playing it smart.

At their core, these investments aim to preserve your capital, deliver steady returns, and minimise emotional decision-making. But let’s be clear: “Safe” doesn’t mean zero risk, it means lower, more predictable risk. “Long-term” means holding your investments for at least five years, giving them time to recover from short-term dips and benefit from compounding growth.

Why does this approach work? Because it builds resilience. You protect your wealth against inflation, diversify across stable asset classes, and avoid the panic of market timing. Over time, this strategy tends to outperform more reactive investing, especially when paired with regular contributions and a clear understanding of your financial goals.

In 2025, safe investing doesn’t just mean sticking to traditional government bonds (though those still have their place). It also includes high-quality dividend stocks, inflation-linked securities, ETFs focused on defensive sectors, and increasingly, professionally managed portfolios via robo-advisors that prioritise low-risk, long-term growth.

If you’re looking to grow your wealth without riding the emotional rollercoaster, here are several strategies tried and tested by the most cautious of investors. Because smart investing isn’t about guessing right, it’s about building a plan that works, even when the market doesn’t.

What makes an investment 'safe' for the long term?

When we talk about safe investments, we're looking for specific characteristics that have proven reliable over decades. Capital preservation comes first, meaning that your initial investment should be protected from significant loss. This doesn't mean guaranteed returns, but it does mean the probability of major losses is low.

- Predictable returns matter more than spectacular ones.

An investment that consistently delivers 6% annually is often better than one that swings between 20% gains and 15% losses. Consistency allows you to plan, budget, and sleep well at night.

- Inflation protection is non-negotiable for long-term wealth building.

An investment earning 3% when inflation runs at 4% is actually losing you money. Many investors seek out options that beat inflation or adjust returns to keep pace with rising prices.

- The risk-reward relationship remains fundamental to all investing.

Generally, safer investments offer lower potential returns, but they also offer something valuable: predictability. This trade-off becomes particularly attractive when you consider the psychological cost of volatile investments and the mathematical power of consistent compounding.

- Diversification isn't just a safety net, it's a requirement.

Spreading investments across different asset classes, sectors, and even countries reduces the impact of any single investment's poor performance. It's the closest thing to a free lunch in investing.

Top safe long-term investment options (2025 edition)

Based on the principles listed above and options favoured by the investors focused on long-term time-frames, here are several options one could consider:

U.S. Treasury Securities & TIPS

Treasury securities represent the gold standard of safe investing, backed by the full faith and credit of the U.S. government, offering different time horizons through bills, notes, and bonds.

Treasury Inflation-Protected Securities (TIPS), on the other hand, adjust their principal value based on inflation rates, addressing the main concern with traditional bonds for long-term holders.

The primary risk here is opportunity cost rather than loss of principal, sacrificing potential growth for safety and predictability.

High-Yield Savings Accounts & CDs

FDIC insurance makes these the safest options available, protecting deposits up to £250,000 per account, with high-yield savings offering competitive rates and full liquidity while CDs lock in higher rates for specific periods.

These suit investors building emergency funds or holding money for near-term goals, though the main limitation is the return potential that may barely beat inflation. The only real risk is opportunity cost, as you're guaranteed not to lose principal but may miss out on higher returns from other investments.

Investment-Grade Bonds & Bond Funds

Corporate and municipal bonds rated BBB or higher offer a step up in yield from government securities while maintaining relatively low risk, with bond funds and ETFs providing instant diversification across hundreds of individual bonds.

These appeal to investors seeking higher income than government bonds can provide, though they carry credit risk (potential issuer default) and interest rate risk (bond values fall when rates rise).

Investment-grade ratings significantly reduce default probability, making short-to-intermediate term bonds (1-7 years) particularly suitable for conservative portfolios due to lower interest rate sensitivity.

Dividend-Paying Stocks

High-quality companies with long dividend histories offer the potential for both regular income and capital appreciation, with Dividend Aristocrats (S&P 500 companies that have increased dividends for 25+ years) representing the most reliable payers.

These stocks provide dividend growth over time, offering natural inflation protection that bonds can't match, though they suit investors comfortable with moderate price volatility.

The main risks include potential dividend cuts during economic downturns and stock price fluctuations, though quality dividend stocks typically show less volatility than growth stocks and recover more quickly from market downturns.

Index Funds & ETFs (e.g., S&P 500)

Broad market index funds provide exposure to hundreds or thousands of companies with minimal fees and no active management risk, with the S&P 500 delivering average annual returns of approximately 10% over long periods.

These funds work well for investors seeking market returns without stock selection complexity, using dollar-cost averaging to reduce timing risk and smooth out market volatility.

The main risk is market volatility with significant year-to-year variation, though this approach has historically outperformed most actively managed funds over time due to its simplicity and low costs.

Target-Date Retirement Funds

These funds automatically adjust their asset allocation based on your target retirement date, becoming more conservative as you approach retirement while holding a diversified mix of stock and bond funds.

They suit investors who prefer a hands-off approach to portfolio management, with the fund company handling rebalancing and asset allocation changes.

The trade-off is less control over specific investments and potentially higher fees than building your own portfolio, though the convenience and professional management often justify the additional cost for many investors.

Real Estate (Direct & REITs)

Real estate provides tangible assets that often appreciate over time while generating rental income, with Real Estate Investment Trusts (REITs) offering real estate exposure without property ownership responsibilities while trading like stocks and paying substantial dividends.

REITs provide diversification benefits as real estate often performs differently than stocks and bonds, particularly during inflationary periods, while offering stock-like liquidity.

The main risks include interest rate sensitivity (REITs often decline when rates rise) and economic cycles that affect property values, though diversified REIT funds spread these risks across different property types and regions.

Robo-Advisors for Conservative Portfolios

Algorithm-based investment platforms create diversified portfolios based on your risk tolerance and goals, with automatic rebalancing and tax-loss harvesting, typically emphasising bonds and dividend stocks for conservative allocations.

These platforms suit investors who want professional portfolio management without traditional financial advisor costs, as algorithms handle technical portfolio construction and maintenance while removing emotion from investment decisions.

The main limitations include less customisation than self-directed investing and ongoing management fees, though these are typically modest compared to traditional advisory services.

Annuities (For Retirement-Focused Investors)

Fixed annuities provide guaranteed income for life or specific periods, eliminating longevity risk in retirement, with immediate annuities beginning payments right away while deferred annuities accumulate value first.

They appeal to retirees who prioritise income certainty over growth potential, essentially serving as insurance against outliving your money. The main downsides include limited liquidity, potentially high fees, and inflation risk with fixed payments, while variable annuities add complexity and market risk that can defeat the purpose of guaranteed income.

Comparing investment options by safety, return & liquidity

If you’re curious about how to approach crypto while keeping risk in check, you’re not alone. As more people fold digital assets into their traditional portfolios, it helps to understand the basics of portfolio management and how crypto markets move.

Much like with stocks or bonds, having a sense of different investment approaches and how they align with your own goals, style, and long-term plan can make all the difference.

With that in mind, here are five key concepts worth knowing when it comes to navigating the crypto market and managing risk (no technical analysis necessary). If you're already in the know, feel free to skip to the next part!

Understanding the basics of cryptocurrency investment

Cryptocurrency is a form of digital asset that exists on decentralised networks, secured by blockchain technology. Unlike traditional money, it isn’t issued or controlled by a single entity, which creates both opportunities and challenges for anyone exploring the space.

It’s helpful to distinguish between investing and trading. Trading typically involves frequent buying and selling to take advantage of short-term price movements, while investing usually focuses on holding digital assets over a longer period to capture potential growth. Understanding these approaches is essential when developing your own strategy.

Bitcoin continues to serve as the benchmark asset for the crypto market. Its widespread adoption, liquidity, and historical performance make it a reference point for comparing other digital currencies. That said, all cryptocurrencies carry unique risks and opportunities, from volatility and regulatory changes to innovations in blockchain technology.

Before buying any crypto, it’s important to do your own research. Explore the technology behind each asset, consider market trends, and assess your comfort with risk. Learning the fundamentals first provides a stronger foundation for navigating the market with confidence.

Top 5 tools for your crypto investment strategy

Here are five key things to keep in mind as you explore digital currencies. They can help you learn different crypto investment approaches and prevent common mistakes along the way.

Understanding liquidity

In crypto, liquidity is one of the most important concepts to understand. Simply put, liquidity measures how easily an asset can be turned into cash without losing much value. For traders, it’s about how quickly and reliably they can buy or sell at a fair price.

Bitcoin is a good example — it consistently has some of the highest liquidity in the market. In a volatile space like crypto, being able to enter or exit positions quickly can make a big difference. That depends on supply and demand: buyers willing to pay a fair price and sellers ready to trade.

A common way to gauge liquidity is by looking at trading volume (how much of a coin is being bought and sold) along with the level of interest from market participants.

Embrace volatility

The crypto market is well known for its sharp ups and downs. While volatility can create opportunities to profit when prices swing, it also brings risks, especially for long-term investors.

Over time, cryptocurrencies have matured, yet speculation and shifting market sentiment still drive sudden moves. Big swings are part of the risk, while smaller day-to-day fluctuations remain a constant trend across the market.

A good guide is to understand your own risk tolerance before jumping in. Keeping up with exchange activity, news, blockchain updates, and historical price data can help you spot patterns and stay informed about where the market might be heading.

The fundamental rule: only invest what you can afford

Possibly the most important crypto investment strategy: the golden rule of investing is never to invest more than you're willing to lose. If losing all of your crypto would put you in financial trouble, that’s a sign your allocation might be too high for your current money situation.

A practical guide is to think about your income, expenses, and overall financial picture when weighing risk. Some people also choose to talk with a professional financial advisor for extra clarity.

You’ll often see commentators mention small, single-digit allocations for beginners and higher allocations for more active participants. But there’s no one-size-fits-all approach; it really depends on your personal circumstances. These are just general examples for learning purposes, not personalised advice.

Profit-taking strategies

Some people in the crypto industry take a more systematic approach to profit-taking (but, again, there’s no single strategy that works for everyone).

When it comes to ownership of digital assets, investors often debate whether to cash out or hold through the swings. Some companies and individuals stick to the classic ‘hodl’ approach, while others sell portions of their gains and move into stablecoins, sometimes re-entering if prices drop.

This method can help secure profits while staying connected to the market, but predicting short-term economic trends and timing swings consistently remains one of the biggest challenges in crypto.

Diversification Revelation

The traditional wisdom of "don't put all your eggs in one basket" applies strongly to crypto portfolios and investment approaches. Building a thoughtful portfolio typically involves incorporating different types of coins and crypto projects, always after conducting thorough research.

Some market participants create diversity by exploring various established digital currencies alongside DeFi projects, coins associated with emerging technologies, or NFT-related tokens. Diversification allows crypto explorers to potentially balance lower-risk and higher-risk assets, though all crypto investments carry substantial risk.

Timing the market vs time in the market

One of the biggest challenges in crypto is timing price movements. Even experienced traders struggle to consistently predict when to buy low or sell high. The fast pace of the market, combined with global economic news and shifting industry trends, makes short-term timing extremely difficult.

That’s why many observers point to the benefits of “time in the market” rather than trying to “time the market.” Long-term strategies and consistent investing approaches often give participants a better chance of riding out volatility. A common case study is Bitcoin: while short-term traders sometimes caught profits during sudden spikes, many long-term holders benefited from simply staying invested through multiple cycles.

The key takeaway is balance. Knowledge, patience, and discipline often matter more than chasing the perfect entry or exit. Securing your assets, preventing avoidable risks, diversifying across different companies and projects, and doing thorough research before buying are all part of building resilience.

Markets will always fluctuate, but staying informed and engaged gives you the tools to adapt.

Trade with confidence

Another important element to consider when investing in cryptocurrencies is where to keep them. Ensure that you store your cryptocurrencies in a safe location, preferably on a regulated platform that holds insurance.

Looking ahead in 2025

As the crypto market continues to mature, some digital assets have demonstrated resilience over multiple market cycles. Market participants often view periods of lower prices as potential accumulation opportunities, though past performance doesn't guarantee future results.

These 5 crypto investing strategy concepts can serve as educational foundations for understanding the space. Remember that cryptocurrency markets remain highly volatile and speculative, and it's important to do your own research and consider consulting with qualified financial professionals before making investment decisions.

Despite radically reshaping the world’s financial landscape, the first ever cryptocurrency has limitations when interacting with newer blockchains. For example, Ethereum. Wrapped Bitcoin (WBTC) solves this limitation by allowing Bitcoin to function on the Ethereum network, enabling access to decentralized finance (DeFi) services.

WBTC is an ERC-20 token that represents Bitcoin 1:1 on the Ethereum blockchain, combining Bitcoin’s value with Ethereum’s smart contract power, and opening new opportunities for BTC holders in decentralized finance (DeFi). Unlike Bitcoin variants aiming to improve its technology, WBTC extends Bitcoin's utility without replacing it.

Join us in this deep dive on how WBTC works, its benefits, risks, and how it connects Bitcoin to the broader DeFi ecosystem.

Unlocking Bitcoin’s Power on Ethereum

Launched in January 2019, approximately 10 years after Bitcoin's initial release, WBTC was created as a collaborative effort between BitGo, Kyber Network, and Ren (formerly Republic Protocol), along with other major players in the DeFi space including MakerDAO, Dharma, and Set Protocol.

As an ERC-20 token, WBTC adheres to Ethereum's token standard, making it compatible with the entire Ethereum ecosystem, including its smart contracts, decentralized applications, and wallets.

In structure, WBTC bears similarities to stablecoins like USDC or USDT, which are backed by reserve assets. However, while stablecoins aim to maintain a stable value (usually pegged to a fiat currency like the US dollar), WBTC's value fluctuates with Bitcoin's market price.

Each WBTC token is backed by an equivalent amount of Bitcoin (BTC) held in reserve by a custodian, maintaining a strict 1:1 ratio, meaning 1 WBTC is always equivalent to 1 BTC in value.

Wrapped Bitcoin is now under the control of a Decentralized Autonomous Organization (DAO) called the WBTC DAO. This organization oversees the protocol, ensuring the integrity of the wrapping process and maintaining transparency in the system. Unlike Bitcoin's fully decentralized nature, WBTC relies on certain trusted entities to maintain the backing of the tokens, which creates an interesting balance between utility and trustworthiness.

WBTC belongs to a broader category of financial instruments known as "wrapped tokens." These are cryptocurrencies that are enclosed or "wrapped" in a digital vault and represented as another token on a different blockchain. While WBTC represents Bitcoin on Ethereum, there are other wrapped tokens in the cryptocurrency space, including Wrapped Ether (WETH) which, somewhat paradoxically, is a wrapped version of Ethereum's native token on its own blockchain that conforms more strictly to the ERC-20 standard.

Why Does Wrapped Bitcoin Exist?

Wrapped Bitcoin (WBTC) was created to bridge the gap between Bitcoin and newer blockchain platforms like Ethereum.

1. Bitcoin's limited smart contract functionality

Bitcoin prioritizes security over programmability, making it unsuitable for complex decentralized apps. In contrast, Ethereum supports smart contracts that power a wide range of automated financial services.

2. Access to DeFi for Bitcoin holders

Ethereum's DeFi ecosystem offers lending, trading, and yield farming, but Bitcoin holders couldn't participate without converting their BTC. WBTC solves this, letting them use Bitcoin's value within Ethereum-based applications.

3. Unlocking Bitcoin's liquidity

Bitcoin's vast market capitalization holds significant untapped liquidity. WBTC brings this capital into Ethereum's DeFi network, benefiting both Bitcoin holders and the broader ecosystem.

4. Faster, more flexible Bitcoin transactions

While Bitcoin transactions can be slow and costly, WBTC uses Ethereum's network for quicker, cheaper trades-ideal for active traders and DeFi users.

In short, WBTC enhances Bitcoin's utility without altering its core protocol, connecting it to the evolving world of decentralized finance.

How Does Wrapped Bitcoin Work? The Nuts and Bolts

Wrapped Bitcoin (WBTC) bridges Bitcoin and Ethereum through a secure, transparent process involving key participants and smart contracts.

1. Wrapping and unwrapping process:

Wrapping (BTC → WBTC): Users send Bitcoin to a custodian, who secures it and mints an equivalent amount of WBTC on Ethereum, sending it to the user's Ethereum wallet.

Unwrapping (WBTC → BTC): Users burn WBTC, prompting the custodian to release the equivalent Bitcoin back to their Bitcoin wallet.

This 1:1 pegging ensures WBTC is fully backed by Bitcoin reserves.

2. Key participants:

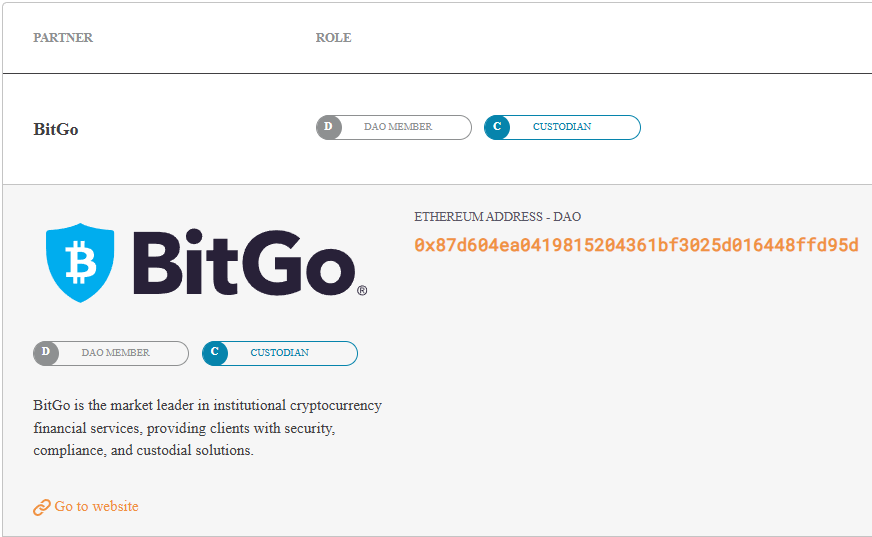

Custodians (e.g., BitGo): Hold and safeguard the Bitcoin backing WBTC.

Merchants: Authorized to request minting or burning of WBTC.

Users: Individuals or entities using WBTC in Ethereum's DeFi ecosystem.

WBTC DAO Members: Stakeholders who govern protocol decisions.

3. Transparency and verification:

Proof of reserves: Publicly verifiable Bitcoin addresses back every WBTC in circulation.

On-chain verification: Minting and burning are recorded on both blockchains.

Regular attestations: Independent checks confirm reserve accuracy.

4. Technical implementation:

WBTC is built as an ERC-20 token, Ethereum’s standard for fungible tokens. All ERC-20 tokens follow the same set of rules, which makes them interchangeable, easy to trade, and instantly compatible with most Ethereum wallets and DeFi apps.

This makes WBTC easily transferable, compatible with wallets, and usable in DeFi apps like lending platforms, decentralized exchanges, and yield farming protocols. It gives Bitcoin the same programmability and utility as Ethereum-native assets.

Showdown: Wrapped Bitcoin (WBTC) vs. Bitcoin (BTC)

Although WBTC and BTC share the same value, their use cases differ. Bitcoin is designed for security, immutability, and censorship resistance. WBTC, on the other hand, thrives in Ethereum’s ecosystem where smart contracts enable lending, borrowing, and trading.

For storing wealth long-term, Bitcoin remains the go-to. For generating yield or accessing DeFi, WBTC is the practical choice. Different uses for different needs.

How Wrapped Bitcoin Boosts Your Crypto

1. DeFi accessibility:

WBTC lets users leverage Bitcoin in DeFi platforms for:

Lending & borrowing: Use WBTC as collateral on platforms like Aave or Compound to earn interest or borrow assets.

Yield farming: Provide WBTC liquidity for rewards, often surpassing Bitcoin's passive holding returns.

Liquidity provision: Earn trading fees by adding WBTC to pools on exchanges like Uniswap.

Synthetic assets: Mint assets pegged to traditional markets using WBTC as collateral.

2. Enhanced liquidity:

WBTC boosts capital efficiency across Ethereum by:

Expanding DeFi liquidity: Unlocking Bitcoin's market value to strengthen liquidity pools.

Reducing slippage: Deeper markets enable smoother trades.

Providing stable collateral: Bitcoin-backed assets offer trusted options for DeFi protocols.

3. Transaction advantages:

Compared to Bitcoin, WBTC transactions on Ethereum benefit from:

Faster confirmations: Ethereum's ~12-second block times outpace Bitcoin's 10-minute average.

Predictable fees: Ethereum's fee structure can be more cost-effective in certain conditions.

Smart contract integration: WBTC supports complex transactions Bitcoin's network can't handle.

4. Broader utility:

Beyond DeFi, WBTC enhances user options by:

Accessing smart contracts: Participate in advanced applications without selling Bitcoin.

Composability: Use WBTC across multiple protocols simultaneously.

Simplified management: Store WBTC alongside other Ethereum assets in common wallets.

Gaming & NFTs: Spend WBTC in blockchain games or NFT marketplaces.

While WBTC offers significant opportunities, it comes with trade-offs regarding decentralization and security, as covered in the next section.

Navigating Wrapped Bitcoin: Risks and Challenges

Custodial risks

While WBTC brings Bitcoin into DeFi, it introduces centralization as well. WBTC depends on BitGo as the sole custodian to hold the backing Bitcoin, creating a central point of failure. Users must trust these custodians to safeguard funds, process redemptions, and comply with regulations that could freeze assets or restrict conversions.

BitGo, DAO member and sole custodian. Source.

Smart contract risks

WBTC relies on Ethereum smart contracts, which, despite audits, can still have vulnerabilities or coding flaws. It's also affected by Ethereum network issues like congestion, high gas fees, and risks from interacting with DeFi platforms.

Price and market risks

WBTC tracks Bitcoin's price and shares its volatility. In turbulent markets, it may trade slightly above or below Bitcoin's value. Large conversions can strain liquidity, making big trades harder without impacting price.

Operational challenges

Managing WBTC involves both Bitcoin and Ethereum blockchains, which can be complex for newcomers. High Ethereum gas fees and slow WBTC-to-Bitcoin conversions (especially for large transactions) are additional hurdles.

Alternatives with less trust required

Some users prefer fully decentralized options like native Bitcoin, though it lacks smart contract functionality. Other wrapped Bitcoin solutions use different technologies to reduce reliance on custodians.

Wrapping Up WBTC

WBTC represents a shift in the cryptocurrency space, bridging the gap between Bitcoin's unparalleled network security and store-of-value properties with Ethereum's programmability and vibrant DeFi landscape. Since its launch in 2019, WBTC has grown from a novel concept to a cornerstone of cross-chain interoperability, enabling countless new use cases for Bitcoin holders.

For users, WBTC allows exposure to Bitcoin while engaging with decentralized finance (DeFi) on Ethereum and other platforms, enabling participation in both without choosing between them. While for DeFi, Bitcoin's liquidity has fostered growth, stability and asset diversity. WBTC has also paved the way for other wrapped assets, making the crypto ecosystem more interconnected and efficient.

As blockchain technology evolves, solutions like WBTC will address limitations while retaining core utility. Its success shows how cryptocurrency innovation can build upon existing strengths without replacing them.

Other Wrapped Bitcoin alternatives

While WBTC is the most widely used Bitcoin representation on Ethereum, several alternatives have emerged, each with different approaches to the bridge between Bitcoin and other blockchains:

- renBTC

- tBTC

- sBTC (Synthetic BTC)

- HBTC

- pBTC

How Can I Buy Wrapped Bitcoin (WBTC)?

If you’re looking to bring Bitcoin into the world of Ethereum, Wrapped Bitcoin (WBTC) is the gateway you might be looking for. Through the Tap app, users can easily add WBTC to their portfolios, opening up access to Ethereum’s thriving DeFi ecosystem. Getting started is simple: just download the app, create an account, and start trading WBTC in minutes.

You know that feeling when the Fed announces a rate cut and suddenly everyone's talking about how "bullish" it is for crypto? Many people just nod along, but honestly have no clue why cheaper borrowing costs would make Bitcoin go up. Let's dig deep into this topic and share what the data shows – whether you're totally new to this stuff or already trading like a pro.

Let's Start Simple: What Are Interest Rates Anyway?

Okay, let's assume you're not an economics major here. Interest rates are basically the price of money. When you borrow money, you pay interest. When you save money, you (hopefully) earn interest. The big kahuna is the rate set by central banks like the Federal Reserve – this is the rate that affects pretty much everything else in the economy.

Here's the deal: when rates are high, borrowing money sucks because it's expensive. People spend less, businesses hold off on big investments, and suddenly that savings account looks pretty attractive. When rates are low, it's the opposite – borrowing is cheap, so people and businesses start spending and investing more aggressively.

A rate cut is just the central bank saying "Hey, we want people to spend more money and take more risks." And guess what falls into that "risky investment" bucket? Yep, crypto.

The Crypto Connection (Or: Why Bitcoin Doesn't Care About Your Savings Account)

Here's something that becomes clear when you think about it: Bitcoin doesn't pay you anything to hold it. Neither does Ethereum, Solana, or pretty much any other crypto sitting in your wallet. They're not like bonds or savings accounts that give you a steady income.

When interest rates are near zero, this isn't a big deal. But imagine government bonds are paying 5% with zero risk. Suddenly, holding volatile crypto that might crash 50% overnight doesn't look so smart, right?

So the math is pretty straightforward:

- High rates = "Why gamble on crypto when you can get guaranteed returns?"

- Low rates = "These bonds pay nothing, maybe Bitcoin looks interesting..."

This is probably the biggest reason why rate cuts get crypto people excited. When safe investments pay peanuts, risky assets start looking a lot more appealing.

How Rate Cuts Actually Push Money Into Crypto

Alright, let's get into the nitty-gritty of how this actually works. It's not just about psychology – there are real mechanisms at play here. Beyond simple psychology, several concrete mechanisms drive capital toward cryptocurrency markets when central banks ease monetary policy.

When central banks cut rates, they typically inject additional liquidity into the financial system. This expanded money supply creates excess capital that seeks higher returns, with crypto markets often benefiting from these flows.

Lower interest rates fundamentally alter investment opportunity costs. This is finance speak for "what am I giving up?" If I can only earn 0.5% in a savings account, the opportunity cost of holding Bitcoin (which pays nothing) is pretty low. But if savings accounts pay 5%, then holding Bitcoin means I'm giving up a lot of guaranteed income.

Here's something interesting: when the U.S. cuts rates, it often makes the dollar less attractive to international investors. A weaker dollar historically has been good for Bitcoin, especially since many people see it as "digital gold", a way to protect against currency debasement.

Accommodative monetary policy encourages risk-taking across markets. Traders can borrow more to make bigger bets, capital flows more easily toward crypto startups, and regular folks start FOMOing into altcoins. It's like the whole market gets a shot of adrenaline.

The COVID Case Study (AKA When Everything Went Bananas)

Want to see this in action? Look at what happened during COVID. In March 2020, everything crashed: stocks, crypto, you name it. Central banks freaked out and slashed rates to basically zero while printing money like it was going out of style.

At first, Bitcoin crashed along with everything else (down to around $3,200). But once all that stimulus money started flowing through the system, crypto went absolutely bonkers. Bitcoin went from that March low to nearly $70,000 by late 2021. That's more than a 20x return in less than two years!

Now, rate cuts alone didn't cause that rally, there was a lot going on, including institutional adoption, the whole "inflation hedge" narrative, and pure FOMO. But the massive liquidity injection definitely set the stage.

Fast forward to now, and we're starting to see rate cuts again. The Fed just cut rates for the first time in years, and everyone's wondering if we're about to see another crypto supercycle. Spoiler alert: it's complicated.

Why It's Not Always That Simple (The Plot Thickens)

The relationship between monetary policy and cryptocurrency prices isn't as straightforward as it seems. Rate cuts don't guarantee crypto rallies, and several factors can throw a wrench in this supposedly reliable connection.

Take timing, for instance. Monetary policy doesn't work like flipping a switch. The Fed cuts rates today, but that doesn't mean money suddenly floods into Bitcoin tomorrow. These effects take months to work through the financial system, creating frustrating delays between policy changes and actual market movements.

Then there's the whole expectations game. If everyone and their mother already expects a rate cut, the actual announcement might barely move markets. It's already baked into prices, as traders say. But when cuts come by surprise? That's when things get interesting, and volatile.

Inflation makes everything messier. Central banks get nervous about cutting rates when prices are already rising. And if they do cut while inflation is running hot, investors start worrying about the economy overheating. This is why smart money watches real interest rates, the actual rate minus inflation, which sometimes tells a completely different story than the headline numbers.

The Advanced Stuff (For Market Nerds)

Okay, this is where things get really interesting. If you're already trading and want to understand what moves the big money, here are the deeper dynamics that separate amateur hour from professional-grade analysis.

Real rates matter more than anything else. When rates sit at 2% but inflation runs at 4%, cash holders are losing 2% annually in purchasing power. That’s the kind of environment where Bitcoin’s ‘hard money’ narrative tends to resonate, and where institutional investors have historically shown greater interest.

The yield curve tells stories that headline rates can't. This relationship between short and long-term rates reveals market psychology. When short rates exceed long rates, the dreaded inverted curve, recession fears dominate. Rate cuts during these periods often fall flat because fear trumps greed, and nobody wants to touch risky assets regardless of how cheap money becomes.

But here's what separates the pros from everyone else: they know it's never just about rates. Credit spreads show how much extra yield risky borrowers pay compared to safe government debt. Dollar funding conditions reveal whether international markets can actually access all that cheap liquidity. And bank lending standards determine if that Fed money ever makes it past Wall Street desks into the real economy. The Fed can slash rates to zero, but if banks won't lend and credit markets freeze up, crypto won't see a dime of that stimulus.

The Dark Side (Because Nothing's Ever Perfect)

Let's be honest here, painting rate cuts as some magic crypto catalyst without acknowledging the risks would be doing everyone a disservice. Easy money creates bubbles, and when those bubbles burst, crypto typically gets damaged first and hardest.

The inflation trap is real and brutal. When rate cuts work too well and prices start spiraling upward, central banks panic and slam the brakes with aggressive rate hikes. That policy whiplash absolutely crushes speculative assets, with crypto leading the carnage every single time.

Then there's the liquidity trap – monetary policy's most frustrating failure mode. Sometimes rate cuts simply don't work. Banks refuse to lend, consumers won't borrow, and all that cheap money sits trapped in the financial system instead of flowing into markets. Japan learned this lesson painfully over decades of ineffective stimulus.

Here's an uncomfortable truth: despite all the "digital gold" rhetoric, crypto still dances to the stock market's tune most days. When rate cuts happen during genuine recessions and equities crater, Bitcoin rarely stays immune. The correlation breaks down only during very specific market conditions, not during broad-based selloffs.

Finally, there's the regulatory sword hanging over everything. Crypto rallies have this annoying habit of attracting government attention, especially when retail investors pile in and inevitably lose their shirts. That regulatory risk never disappears, it just sits there waiting for the next bubble to pop.

Strategic Approaches at Different Levels

The beauty of understanding rate cut dynamics is that you can apply this knowledge regardless of where you are in your trading journey. Here's how to think about it based on your experience level.

Starting out? Keep things dead simple. Track Fed meetings, watch inflation numbers, and brace for wild swings around major announcements. Don't get lost in the weeds trying to predict every twist and turn. Just remember that cheaper money generally makes crypto more attractive, even if the timing stays unpredictable.

Getting more serious about this game? Time to expand the toolkit. Real interest rates become your new best friend, along with the dollar index (DXY) and whatever the Fed chair actually says about future moves. Pay close attention to how crypto moves when stocks hiccup, that correlation hasn't disappeared just because Bitcoin hit some arbitrary price target.

Going full macro nerd? Now we're talking. Layer in yield curve analysis, credit spreads, and options flow data. The goal shifts from reacting to news toward positioning ahead of surprises. This means using derivatives to hedge positions and managing risk like the professionals do. At this level, it's less about being right and more about surviving when you're wrong.

The Bottom Line

So why are interest rate cuts good for crypto? Because they make safe assets less attractive, flood the system with liquidity, weaken fiat currencies, and make everyone a little more willing to take risks. For Bitcoin, that often strengthens its narrative as a store of value. For altcoins, it can fuel speculative rallies and bring more funding to interesting projects.

But here's the key insight: context is everything. Rate cuts during an economic expansion can be rocket fuel for crypto. Rate cuts during a deep recession might just keep things from getting worse. The difference comes down to liquidity conditions, market sentiment, and whether people actually believe the central bank's strategy will work.

For newcomers, the headline is simple enough: lower rates usually help crypto. For everyone else, remember that it's not just about the rate cut itself, it's about how that cut fits into the bigger macroeconomic puzzle.

The most successful traders don't just look at rate cuts in isolation. They consider the whole picture: inflation, employment, credit conditions, dollar strength, and market positioning. Because at the end of the day, markets are about human psychology as much as they are about monetary policy.

And honestly? That's what makes this whole game so fascinating, and frustrating at the same time.

.webp)

.webp)