Aprender, de forma sencilla

Explora nuestros recursos, guías y artículos sobre todo lo relacionado con el dinero. Gana confianza financiera con contenidos seleccionados por nuestros expertos, tanto si estás empezando como si ya tienes experiencia.

Últimos artículos

¿Recuerdas cuando tus abuelos presumían de una cuenta de ahorro al 2 %? Hoy eso suena a otra época, especialmente cuando en cripto aparecen cifras de APY que harían palidecer a cualquier banquero tradicional. Pero antes de soñar con jubilarte el mes que viene gracias a esos rendimientos tan llamativos, conviene entender qué significa realmente el APY y por qué algunos números parecen sacados de un boleto de lotería.

¿Qué es el APY, en realidad?

Piensa en el APY como el interés compuesto llevado al siguiente nivel. Mientras una cuenta bancaria tradicional apenas se mueve, el APY mide cuánto puede crecer tu saldo en un año cuando los intereses se acumulan sobre intereses. Aquí es donde la idea de “que tu dinero trabaje solo” cobra sentido.

Un pequeño ejercicio de realidad: coloca 1.000 € en un banco con un 5 % de interés simple y al final del año tendrás 1.050 €. Predecible.

Ese mismo importe con un 5 % de APY, compuesto mensualmente, se convertiría en 1.051,16 €.

“Solo un euro más”, podrías pensar. La diferencia aparece con el tiempo. El interés compuesto crea una bola de nieve que no deja de crecer. No son céntimos: es el tipo de efecto que, con el paso del tiempo, marca distancia.

APY vs. APR: la rivalidad que conviene entender

Vale, confesión: incluso gente con experiencia en cripto los mezcla. Aquí tienes la chuleta:

APY (Annual Percentage Yield): lo que puedes ganar cuando prestas o pones a trabajar tus criptomonedas, teniendo en cuenta el interés compuesto.

APR (Annual Percentage Rate): lo que pagas cuando pides prestado, normalmente sin considerar la capitalización.

Piénsalo así: el APY es el que te “trae” rendimiento; el APR es el que te “cuesta” rendimiento.

Para una comparación más detallada, haz clic aquí.

¿Dónde aparece el APY en cripto?

“Cuentas de ahorro” cripto

Algunas plataformas te permiten depositar tokens y ver cómo crecen. Es como poner tus criptomonedas a trabajar en un empleo que sí paga. Tus activos se prestan a traders que los necesitan y tú recibes una parte.

Staking: conviértete en validador de la red

En blockchains con Proof of Stake como Ethereum o Cardano, puedes hacer staking de tus tokens para ayudar a asegurar la red. Es como ser un “vigilante digital” que cobra en cripto: la red se mantiene segura y tú recibes recompensas.

Yield farming: el Lejano Oeste de DeFi

Aquí es donde la cosa se pone interesante… y un poco salvaje. Aportas liquidez a exchanges descentralizados y, a cambio, ganas comisiones de trading más tokens de gobernanza. A veces aparecen APY que parecen números de teléfono, pero suelen bajar rápido. Estos rendimientos tienen fama de aterrizar de golpe.

Protocolos de lending: conviértete en el banco

Plataformas como Aave y Compound te dejan jugar a ser banco. Prestas tus tokens, los prestatarios pagan intereses y tú cobras. El APY sube cuando mucha gente quiere pedir prestado ese activo y baja cuando la demanda se enfría.

¿Por qué los APY en cripto son tan altos?

Mientras un banco te ofrece un 0,5 % (si tienes suerte), en cripto puedes ver cifras como 10 %, 50 % o incluso 1.000 %+. ¿Por qué?

- Los traders pagan primas altas para abrir cortos o ejecutar estrategias complejas de arbitraje. Pura oferta y demanda.

- Los proyectos nuevos suelen “tirar de APY” para atraer liquidez. Es como una promo de lanzamiento, pero con más ceros.

- El riesgo va incluido. En cripto hay más incertidumbre, y los rendimientos reflejan esa montaña rusa.

- Los incentivos en tokens inflan muchas cifras. Parte del APY puede venir en tokens del proyecto, cuyo valor puede subir… o desplomarse.

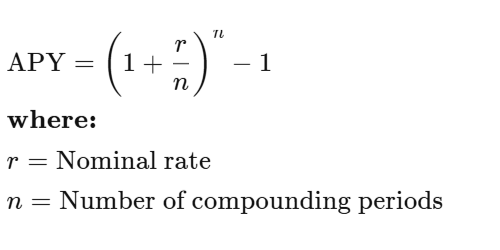

Las matemáticas detrás de la magia

Tranquila, no vamos a convertir esto en una pesadilla de cálculo. La fórmula del APY es bastante simple:

Ejemplo: un 10 % de interés compuesto mensualmente da alrededor de un 10,47 % de APY. ¿Compuesto a diario? Aproximadamente 10,52 %. En cripto, algunos protocolos componen por bloque, casi cada pocos segundos. Tu calculadora podría empezar a sufrir.

La letra pequeña

Antes de dejar tu trabajo y declararte “yield farmer” profesional, toca hablar de lo que no suele salir en las conversaciones con entusiasmo.

Primero, la volatilidad. Puedes ver un APY del 20 %, pero si el token cae un 50 %, el resultado final cambia por completo.

Luego está la pérdida impermanente, que puede morder tus ganancias cuando aportas liquidez y los precios se mueven.

Y ojo con el riesgo de contratos inteligentes. En DeFi, el dinero vive dentro de código, y si algo falla, los fondos pueden evaporarse sin despedida.

También existe riesgo de plataforma. Casos como Celsius o FTX demostraron que, a veces, el problema no es el mercado, sino la propia entidad.

Y por último: el “latigazo” del APY. Ese 100 % que viste ayer puede ser 15 % hoy. En cripto, los tipos cambian rápido por demanda, competencia, tokenomics… o simplemente porque el mercado gira.

¿Qué es un “buen” APY?

Conservador. Activos más consolidados y plataformas conocidas: 3 % a 8 %. Para quien prefiere menos sobresaltos.

Moderado. Staking de ciertos altcoins o liquidez: 10 % a 20 %. Emoción contenida.

Alto (YOLO). Proyectos nuevos en DeFi: 50 % a 100 %+… con una posibilidad real de que el riesgo sea igual de alto que el porcentaje.

Si un APY parece demasiado bueno para ser verdad, normalmente viene acompañado de riesgos igual de “creativos”.

Bola de cristal: el futuro del APY en cripto

Aquí cambia el tono. A medida que cripto madura, los APY se están pareciendo menos a boletos de lotería y más a productos financieros de verdad. Entran instituciones, hay más supervisión y el “Lejano Oeste” se va convirtiendo en una ciudad con normas.

Es probable que cripto siga ofreciendo rendimientos más atractivos que la banca tradicional, pero los días de 10.000 % de APY parecen cada vez más un recuerdo.

Conclusión

El APY en cripto es el mismo concepto matemático de siempre, pero con ropa digital y dinámicas distintas. Ya sea staking, lending o yield farming, entender el APY te ayuda a separar oportunidades reales de promesas dudosas.

El APY no es un truco para generar dinero infinito. Es una métrica que puede ayudarte a entender cómo crecen los rendimientos, pero siempre dentro de un entorno con riesgos.

Y vale la pena recordar esto: el mejor APY del mundo no sirve de nada si el proyecto desaparece del mapa. Elige con criterio, diversifica con cabeza y que el interés compuesto te trate bien.

Audius es uno de los proyectos más interesantes del ecosistema Web3. Se trata de una plataforma de streaming musical descentralizada creada para devolver el poder a los artistas. En lugar de depender de discográficas o plataformas centralizadas, Audius conecta directamente a los creadores con sus fans, permitiéndoles publicar, compartir y monetizar su música en sus propios términos. Es una plataforma donde los oyentes pueden escuchar música libremente, mientras que los artistas obtienen recompensas en la criptomoneda nativa de la plataforma, AUDIO.

Fundada en 2018 por Roneil Rumburg y Forrest Browning, Audius ha atraído a millones de usuarios mensuales y a cientos de miles de artistas, con el respaldo de grandes nombres como Katy Perry, Nas, Steve Aoki y Jason Derulo. Su misión es clara: eliminar intermediarios y permitir que los artistas sean verdaderos propietarios de su trabajo y se beneficien directamente de él.

¿Cómo funciona Audius?

A nivel técnico, Audius opera sobre una red descentralizada impulsada por nodos de contenido y nodos de descubrimiento.

Los nodos de contenido alojan y protegen los archivos musicales en nombre de los artistas, mientras que los nodos de descubrimiento los indexan para que los fans puedan encontrar fácilmente las canciones. Este sistema sustituye a los servidores centralizados por una red distribuida, ofreciendo mayor resistencia a la censura y más transparencia.

Los artistas pueden subir música directamente a Audius, decidir cómo compartirla (gratis o de pago) e incluso desbloquear contenido exclusivo para sus fans más fieles. A diferencia de las plataformas tradicionales que pagan únicamente por número de reproducciones, Audius recompensa a los artistas en función del compromiso global: canciones en tendencia, subidas verificadas e interacción con la comunidad.

Aunque Audius se construyó originalmente sobre la blockchain de Ethereum, posteriormente migró su sistema de contenidos a Solana para ofrecer transacciones más rápidas y económicas, manteniendo AUDIO como un token ERC-20. Esta configuración híbrida combina la fiabilidad de Ethereum con la escalabilidad de Solana.

¿Qué hace diferente a Audius?

Audius desafía las normas de la industria musical invirtiendo la estructura de beneficios. En el streaming tradicional, los artistas suelen recibir alrededor del 12 % de los ingresos totales. En Audius, los artistas reciben el 90 % de las recompensas directamente en tokens AUDIO, mientras que el 10 % restante se destina a los operadores de nodos que ayudan a asegurar la red.

Este enfoque crea un modelo más transparente y equitativo, que permite a los artistas conectar directamente con sus oyentes, lanzar contenidos exclusivos o gestionar sus propias comunidades. Además, la plataforma colabora con TikTok, permitiendo enlazar canciones de Audius directamente a vídeos, lo que amplía su exposición en redes sociales convencionales.

Gracias al almacenamiento descentralizado (a través de AudSP, un sistema basado en IPFS), los artistas mantienen el control sobre sus archivos musicales. Esto convierte a Audius en una plataforma resistente a la censura y realmente orientada a los creadores, algo poco habitual en el mundo del streaming.

El token AUDIO

El token AUDIO es el pilar del ecosistema Audius y cumple varias funciones clave:

- Staking y seguridad de la red: los operadores de nodos hacen staking de AUDIO para ejecutar la infraestructura y ganar recompensas.

- Gobernanza: cada token AUDIO otorga un voto en las decisiones del protocolo, dando a la comunidad voz sobre la evolución de la plataforma.

- Acceso a funciones: mantener o hacer staking de AUDIO desbloquea funciones premium, acceso anticipado a nuevas herramientas e insignias para artistas.

AUDIO tiene una oferta inicial de mil millones de tokens y se utiliza para recompensas de la plataforma, incentivos comunitarios y la seguridad continua de la red. Los holders también pueden ganar AUDIO adicional mediante staking o contribuyendo al crecimiento del ecosistema.

Por qué Audius es importante

Audius es mucho más que una app de música: es una prueba real de cómo la blockchain puede transformar las industrias creativas. En resumen, ofrece:

- Conexión directa entre artistas y fans sin intermediarios

- Reparto de ingresos transparente mediante recompensas on-chain

- Almacenamiento resistente a la censura para música y metadatos

- Escalabilidad cross-chain con interoperabilidad entre Ethereum y Solana

Para los artistas, supone un trato más justo. Para los oyentes, es una forma de apoyar directamente a los creadores y descubrir nuevas comunidades musicales impulsadas por crypto.

Conclusión

Audius reimagina lo que podría ser el streaming musical en la era Web3: un ecosistema justo, abierto y descentralizado donde creatividad y propiedad van de la mano. Une tecnología blockchain y expresión cultural, demostrando que la descentralización no es solo cosa de las finanzas.

Dónde conseguir AUDIO

¿Te interesa el proyecto? Puedes adquirir el token AUDIO en plataformas como Tap.

2025 ha sido un punto de inflexión para la inteligencia artificial. GPT-5 de OpenAI y Claude Sonnet 4.5 de Anthropic han vuelto a elevar el listón, cada uno con el objetivo de integrar un razonamiento más sólido, mayor memoria y más autonomía en un solo sistema coherente.

Ambos están diseñados para abordar programación, investigación, redacción y tareas a escala empresarial, pero sus filosofías de diseño difieren de forma clara. Este análisis compara su rendimiento en razonamiento, programación, matemáticas, eficiencia y coste para ayudarte a decidir dónde brilla cada uno.

Visión general rápida

Claude Sonnet 4.5 se apoya en la familia Claude de Anthropic, ya consolidada. Amplía la memoria entre sesiones, gestiona contextos de hasta un millón de tokens a través de Amazon Bedrock y Vertex AI, e incorpora una gestión inteligente del contexto que evita cortes bruscos. Además, puede operar de forma autónoma durante hasta 30 horas en tareas prolongadas, lo que lo hace ideal para flujos de trabajo continuos.

GPT-5, por su parte, es el modelo insignia de OpenAI tras GPT-4, optimizado para el razonamiento agentic, donde el modelo planifica, ejecuta y coordina herramientas por sí mismo. Su sistema de razonamiento adaptativo decide dinámicamente entre rutas de pensamiento superficial o profundo, permitiendo equilibrar velocidad, coste y profundidad según la tarea. GPT-5 también ofrece variantes especializadas (Mini y Nano) para cargas de trabajo más ligeras.

Razonamiento y análisis

Ambos modelos superan ampliamente a sus versiones de 2024, pero difieren en cómo razonan.

El modo de razonamiento profundo de GPT-5 mejora de forma notable el rendimiento en tareas de lógica compleja, científicas y espaciales. Es capaz de dividir problemas en cadenas de razonamiento, probar subhipótesis y autocorregirse durante el proceso. Sin embargo, cuando este modo se desactiva, la precisión disminuye de forma significativa. Puede ser brillante cuando “piensa a fondo”, pero más variable cuando no lo hace.

Claude Sonnet 4.5, en cambio, mantiene una estabilidad notable incluso sin configuraciones adicionales. Destaca especialmente en lógica financiera, normativa y empresarial, donde la estructura y la coherencia pesan más que los saltos creativos. Para preguntas corporativas o apoyo a la toma de decisiones, esa previsibilidad es una gran ventaja.

Si buscas un razonamiento constante y fiable, Claude lleva la delantera. Si necesitas lógica exploratoria, como pruebas de hipótesis complejas o síntesis entre dominios, la profundidad de GPT-5 no tiene rival.

Matemáticas y resolución de problemas estructurados

Según los benchmarks publicados por Anthropic, Claude Sonnet 4.5 mantiene su racha de consistencia. Ya sea calculando directamente o utilizando herramientas como Python, alcanza una precisión matemática de primer nivel, incluso en entornos restringidos.

GPT-5 también logra una precisión casi perfecta, pero solo cuando el uso de herramientas y la profundidad de razonamiento están activados. Si se deshabilitan, los resultados caen de forma notable. Depende en gran medida de su pipeline de razonamiento para mantenerse preciso.

Veredicto:

- Claude Sonnet 4.5: solucionador matemático fiable desde el primer momento.

- GPT-5: flexible, pero requiere ajustes para rendir al máximo.

Programación e ingeniería de software

En programación, los dos modelos adoptan enfoques distintos.

Claude Sonnet 4.5 ofrece un rendimiento estable sin necesidad de configuraciones especiales. En pruebas similares a HumanEval+ y MBPP+, mantiene una alta precisión en distintas condiciones, lo que lo hace fiable para entornos de producción. Su fortaleza es la consistencia: los resultados rara vez fluctúan, algo crucial a nivel empresarial.

GPT-5, en cambio, alcanza puntuaciones máximas más altas cuando se activa su razonamiento avanzado, especialmente en proyectos grandes o multilenguaje. En tareas de refactorización en JavaScript y Python, superó a Sonnet cuando su modo de alto razonamiento estaba activo, aunque las ejecuciones base sin ese modo mostraron mayor variabilidad.

Para programación agentic, donde la IA interactúa con herramientas externas o terminales, Sonnet 4.5 suele ejecutar con menos comandos fallidos. GPT-5, por su parte, puede encadenar más llamadas a herramientas simultáneamente, lo que lo hace más adecuado para orquestaciones complejas, siempre que esté bien configurado.

Veredicto:

- Claude Sonnet 4.5: socio de ingeniería predecible y constante.

- GPT-5: potencia versátil, pero su rendimiento depende de la configuración.

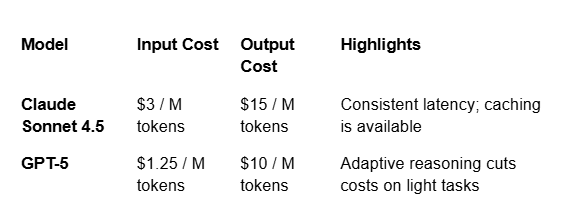

Coste y eficiencia

GPT-5 es claramente más económico por token, especialmente en entradas grandes. Su enrutador adaptativo también ahorra recursos al ejecutar prompts simples por rutas más ligeras.

Claude Sonnet 4.5 es más caro, pero ofrece una latencia predecible, un factor clave en entornos de producción que priorizan la fiabilidad frente a ahorros marginales. En prompts muy largos, su coste aumenta más rápido que el de GPT-5, aunque los descuentos por lotes reducen esa diferencia.

TL;DR: GPT-5 gana en precio y escalabilidad, mientras que Claude destaca por consistencia y estabilidad en tiempos de respuesta.

Precios de los planes premium

Más allá del acceso por API, tanto OpenAI como Anthropic ofrecen suscripciones premium para usuarios individuales.

ChatGPT Plus, impulsado por GPT-5, cuesta 20 dólares al mes e incluye acceso prioritario a GPT-5, respuestas más rápidas y acceso anticipado a nuevas funciones y memoria. La experiencia unificada de ChatGPT también incorpora subida de archivos, generación de imágenes y GPTs personalizados.

Claude Pro, por su parte, también cuesta 20 dólares al mes y da acceso a Claude Sonnet 4.5, con respuestas más rápidas, mayores límites de uso y ventanas de contexto más largas. Aunque carece de herramientas multimodales integradas, se centra en claridad textual y razonamiento estructurado, lo que resulta atractivo para investigadores, analistas y escritores que priorizan la fiabilidad.

TL;DR: ambos planes Plus tienen el mismo precio; lo que los diferencia es la propuesta de valor.

Fortalezas distintas para necesidades distintas

Es tentador declarar un “ganador”, pero GPT-5 y Claude Sonnet 4.5 responden a prioridades diferentes según el usuario o el equipo.

- Claude Sonnet 4.5: ideal para fiabilidad y rendimiento sostenido. Si buscas resultados consistentes y una gestión clara de la memoria, Claude cumple.

- GPT-5: ideal para profundidad, flexibilidad y escalabilidad. Bien configurado, supera a sus competidores en razonamiento creativo, integración multimodal y uso adaptativo de herramientas.

Muchos equipos descubren que la mejor estrategia es multimodelo: usar Claude donde la consistencia es clave y GPT-5 para flujos de trabajo intensivos en datos.

En última instancia, ya no hablamos solo de chatbots, sino de colaboradores digitales completos, cada uno con su propia personalidad. Claude Sonnet 4.5 es el analista tranquilo y metódico. GPT-5 es el polígrafo ambicioso. La elección depende menos de los benchmarks individuales y más de tu objetivo final.

A medida que te familiarizas con la industria de las criptomonedas, irás incorporando nuevas expresiones a tu vocabulario. Una de ellas es HODL. Aunque no es un término utilizado en las finanzas tradicionales, veremos por qué HODL se ha convertido en una parte tan valorada del ecosistema cripto. En este artículo exploramos el origen de este famoso término, qué significa y por qué todo trader de criptomonedas debería entender este concepto.

¿Qué significa HODL?

HODL se refiere a mantener una criptomoneda específica durante un largo periodo de tiempo con el objetivo de beneficiarse de la subida de su precio. En años recientes, parte de la comunidad cripto ha convertido el término en el acrónimo “Hold On for Dear Life” (aguanta con todas tus fuerzas), aunque esto no forma parte de su origen real.

HODL se ha vuelto sinónimo de no vender una criptomoneda durante un mercado bajista o en periodos de alta volatilidad. El término ha sido ampliamente adoptado por la comunidad cripto y se utiliza en contenidos de todo tipo y en todas las plataformas.

¿De dónde viene HODL?

HODL apareció por primera vez en un foro de BitcoinTalk en 2013, cuando un usuario llamado GameKyuubi escribió mal la palabra “hold”. En estado de ebriedad, publicó el siguiente mensaje:

“I type d that tyitle twice because I knew it was wrong the first time. Still wrong. w/e,” escribió GameKyuubi sobre el ahora famoso error ortográfico de “holding”. “WHY AM I HODLING? I'LL TELL YOU WHY,” continuó. “It's because I'm a bad trader and I KNOW I'M A BAD TRADER. Yeah you good traders can spot the highs and the lows pit pat piffy wing wong wang just like that and make a millino bucks sure no problem bro.”

En 2013, el precio de Bitcoin atravesó un periodo de gran volatilidad, subiendo de 130 dólares en abril a 950 dólares en diciembre. El usuario animaba a otros inversores de Bitcoin a no vender y, en su lugar, “hodlear”.

En menos de una hora, el término se convirtió en un meme ampliamente difundido y, más de una década después, sigue utilizándose.

HODL como estrategia de trading

En la inversión en criptomonedas, la volatilidad de precios es una constante. Sin embargo, el concepto de HODL ofrece una forma estratégica de afrontar estas fluctuaciones. HODL implica mantener tus inversiones durante un periodo prolongado, independientemente de los movimientos de precio a corto plazo. A pesar de las subidas y bajadas del mercado, esta estrategia puede aportar estabilidad y generar beneficios a largo plazo. Permite a los inversores navegar la volatilidad con paciencia y confianza en el crecimiento futuro.

Este enfoque ha sido adoptado por una gran parte de la comunidad de Bitcoin y del ecosistema cripto en general como una forma de generar ganancias. Para los maximalistas de Bitcoin, HODL es casi un estilo de vida. Muchos utilizan esta estrategia para evitar decisiones que erosionen beneficios, como reaccionar al FUD (miedo, incertidumbre y duda) o al FOMO (miedo a quedarse fuera), conceptos que veremos a continuación.

¿Cuándo es el mejor momento para hacer HODL?

De forma similar al proverbio chino “El mejor momento para plantar un árbol fue hace 20 años. El segundo mejor momento es ahora”, el mejor momento para hacer HODL es ahora. Como estrategia de inversión, comprar y mantener un activo suele considerarse rentable a largo plazo, ya que su valor tiende a crecer con el tiempo.

HODL es también una creencia ideológica en el potencial a largo plazo de la tecnología blockchain, las criptomonedas y las comunidades que se han formado en torno a ellas. Algunos traders del mercado bursátil han adoptado esta mentalidad, aunque el término HODL sigue utilizándose principalmente en el contexto cripto.

Otros términos cripto importantes que debes conocer

A medida que amplíes tu vocabulario cripto, es probable que te encuentres con los siguientes términos:

BTFD (buy the f*ing dip)

Término coloquial usado frecuentemente en Twitter. BTFD anima a los traders a comprar cuando los precios están bajos, con la intención de obtener beneficios cuando se recuperan.

FUD (fear, uncertainty, doubt)

Como se mencionó anteriormente, FUD se refiere a la difusión de información negativa o engañosa que suele incentivar a los traders a vender.

FOMO (fear of missing out)

Creadores de contenido o medios tradicionales pueden utilizar el FOMO para incitar a la compra de una criptomoneda, apelando al miedo de perderse grandes ganancias o “la próxima gran oportunidad”.

Lambo

Abreviatura de Lamborghini. Hace referencia a que el precio de un activo suba tanto que el usuario pueda venderlo y comprar este coche de lujo. “When Lambo?” es una frase común para preguntar cuándo el precio alcanzará ese nivel.

To The Moon

Se utiliza para describir precios que alcanzan niveles extraordinariamente altos, como si fueran rumbo a la luna.

Whale

Una ballena cripto es una persona u organización que posee una gran cantidad de una criptomoneda específica, generalmente alrededor del 10% de su suministro total.

Reflexión final

HODL hace referencia a una estrategia de comprar y mantener que nació a partir de un error tipográfico en un foro de BitcoinTalk en 2013. El concepto sigue siendo relevante más de una década después, con muchos traders y maximalistas que continúan utilizándolo. El objetivo del HODL es beneficiarse de grandes subidas de precio y reducir el impacto de los mercados volátiles.

Nunca es tarde para aprender sobre el nuevo sistema de pagos financieros. Bitcoin se ha vuelto cada vez más popular con el paso de los años y, a medida que las tasas de adopción siguen creciendo, ahora es el momento perfecto para familiarizarse con la primera y mayor criptomoneda del mundo.

¿Qué es Bitcoin?

Bitcoin es un sistema de pagos peer-to-peer que funciona a través de internet y no mediante una autoridad centralizada como ocurre con las monedas tradicionales. Esta moneda digital elimina intermediarios y permite a los usuarios enviar dinero directamente entre sí, reduciendo comisiones elevadas, procesos largos y tiempos de espera para que los fondos se confirmen.

En lugar de estar gestionado por un banco, un gobierno o una institución financiera, Bitcoin funciona gracias a una red de ordenadores repartidos por todo el mundo que siguen un mismo protocolo para garantizar el correcto funcionamiento del sistema. La tecnología blockchain es la base de Bitcoin y asegura que todas las transacciones se procesen de forma eficiente, transparente e inmutable.

Bitcoin es un sistema de pago seguro, descentralizado y sin fronteras, y una forma de moneda digital que opera las 24 horas del día, los 7 días de la semana.

Bitcoin suele compararse con el oro, ya que ambos activos han demostrado ser inversiones sólidas a lo largo del tiempo. Aunque la regulación en torno a las criptomonedas sigue desarrollándose, Bitcoin continúa siendo un sistema de pago ampliamente adoptado y utilizado.

¿Cuáles son los beneficios de Bitcoin?

- Descentralizado: la red está completamente libre de control centralizado, incluyendo la posibilidad de bloquear transacciones, congelar cuentas o exigir trámites complejos.

- Accesible: cualquier persona, en cualquier lugar, puede utilizar el sistema de pagos de Bitcoin siempre que tenga conexión a internet. Es una plataforma totalmente inclusiva.

- Transparente: aunque la red se considera “pseudónima”, todas las transacciones se registran en un ledger público en tiempo real, creando un ecosistema completamente transparente.

- Liquidez: Bitcoin puede intercambiarse en cientos de plataformas en todo el mundo, lo que garantiza una alta liquidez constante.

¿Cómo funciona Bitcoin?

Gracias a la tecnología blockchain, la red de ordenadores puede facilitar transacciones de activos digitales de un usuario a otro sin necesidad de intermediarios. Veámoslo paso a paso.

Imagina que Amal quiere enviar 1 BTC a George. Para ello, inicia la transacción desde su wallet de Bitcoin introduciendo la dirección de wallet de George y el importe. Bitcoin se almacena en wallets digitales que cuentan con dos códigos importantes: la dirección de wallet (clave pública) y la clave privada, que solo el propietario debe conocer (similar al PIN de un cajero).

Una vez iniciada la transacción, esta entra en un pool de transacciones pendientes en la red. A partir de ahí, los miners la “recogen” y compiten entre sí para ser los primeros en resolver un complejo problema criptográfico. El primero en lograrlo valida la transacción.

Los fondos salen de la wallet de Amal y se depositan en la wallet de George. Esto queda registrado en la blockchain, un ledger digital transparente compartido por toda la red, que incluye fecha, hora, direcciones de wallet e importe dentro de un bloque, almacenado en orden cronológico. A continuación, se actualiza el balance de cada wallet.

Normalmente, las wallets requieren 3 confirmaciones antes de que los fondos puedan gastarse. Esto significa que deben añadirse tres nuevos bloques a la blockchain, y cada bloque representa una confirmación.

¿Qué le da valor a Bitcoin?

El valor de Bitcoin se determina por la oferta y la demanda, fluctuando cuando la oferta disminuye y la demanda aumenta. Desde su creación, su código establece que solo existirán 21 millones de BTC. Al limitar el suministro total, la moneda es naturalmente deflacionaria, lo contrario de las monedas fiat.

Debido al notable aumento de su valor a lo largo de los años, muchos inversores consideran Bitcoin una sólida reserva de valor. Esto, junto con su disponibilidad constante y alta liquidez, lo convierte en una inversión a largo plazo muy atractiva, conocida en el sector como “hodling”.

¿Para qué se utiliza Bitcoin?

Con la funcionalidad fluida del efectivo, su disponibilidad permanente y la posibilidad de transferirse a cualquier parte del mundo en cuestión de minutos, Bitcoin es un excelente medio de intercambio.

Cualquiera puede usar Bitcoin para pagar bienes y servicios (muchos comercios en todo el mundo ya aceptan la criptomoneda) o como reserva de valor. Siempre que una persona tenga conexión a internet, puede enviar y recibir Bitcoin.

¿De dónde viene Bitcoin?

Anunciado por primera vez el 31 de octubre de 2008 y lanzado oficialmente a principios de enero de 2009, Bitcoin fue creado por una entidad anónima conocida como Satoshi Nakamoto, pionera de la revolución crypto.

En el whitepaper del proyecto, se explica que Bitcoin nació como respuesta a la crisis financiera global. La idea era crear una moneda libre del control de gobiernos y bancos, permitiendo a las personas tener pleno control sobre sus fondos y ser totalmente responsables de ellos.

Alrededor de 2010, Satoshi Nakamoto desapareció y hasta hoy no se ha logrado confirmar su identidad. Muchos creen que no era una sola persona, sino un grupo.

Desde la aparición de Bitcoin, se han creado miles de nuevas criptomonedas. A cualquier nueva moneda se la denominó altcoin (alternative coin), término que se mantiene hasta hoy. Existen más de 12.000 criptomonedas, cada una con su propio caso de uso. Por ejemplo, Ethereum se creó para que los desarrolladores pudieran construir aplicaciones descentralizadas, mientras que otras como Litecoin nacieron para mejorar el sistema de pagos de Bitcoin.

¿Cómo invertir en Bitcoin?

Comprar Bitcoin es mucho más sencillo de lo que la mayoría imagina. Lo podras encontar facilmente en plataformas como Tap.

En un mundo en el que cada proyecto crypto afirma ser “revolucionario”, Ethereum es de los pocos que realmente lo demuestra, cambiando cómo entendemos internet, las finanzas y la propiedad digital.

Concebido por Vitalik Buterin en 2013 y lanzado en 2015, Ethereum amplió las posibilidades de la tecnología blockchain más allá de las simples transacciones de moneda, introduciendo un mundo en el que las aplicaciones pueden ejecutarse exactamente como fueron programadas, sin censura ni interferencias de terceros.

Si Bitcoin nos introdujo al dinero digital, Ethereum nos trajo el dinero programable (y mucho más, por cierto). Puede que lo hayas oído describirse como “el ordenador del mundo”, porque permite a los desarrolladores crear y desplegar aplicaciones descentralizadas (dapps) capaces de transformar industrias como las finanzas, el arte, los videojuegos o la gobernanza.

En esta guía completa, veremos qué hace especial a Ethereum, cómo funciona por dentro y por qué sigue estando en el centro de la revolución blockchain. Tanto si estás empezando desde cero como si quieres profundizar, explicaremos desde los smart contracts y los NFTs hasta el paso a Ethereum 2.0, The Merge y lo que podría traer el futuro para esta tecnología.

¿Qué es Ethereum? Explicado de forma sencilla

Piensa en Ethereum como una plataforma global y open-source para aplicaciones descentralizadas. Mientras que Bitcoin está diseñado principalmente como dinero digital, Ethereum se construyó como una plataforma de desarrollo: una base sobre la que los desarrolladores pueden crear nuevas aplicaciones que ninguna entidad controla por completo.

La forma más fácil de entender Ethereum es compararlo con el sistema operativo de tu móvil. Igual que iOS o Android proporcionan una plataforma para crear apps, Ethereum ofrece una plataforma para desarrollar dapps. Estas aplicaciones funcionan en una red de miles de ordenadores por todo el mundo, en lugar de ejecutarse en servidores centralizados propiedad de empresas como Google o Amazon.

Ethereum se describe a menudo como un “ordenador mundial” porque es, en esencia, un enorme sistema de computación distribuida que pertenece a todo el mundo y a nadie al mismo tiempo. A diferencia de los ordenadores tradicionales controlados por personas o empresas, este “ordenador mundial” ejecuta programas (llamados smart contracts) exactamente como fueron escritos, sin posibilidad de censura, caídas del sistema o interferencias de terceros.

Como “blockchain de segunda generación”, Ethereum tomó la innovación de Bitcoin (un registro descentralizado) y le añadió programabilidad. Ese avance abrió un universo de posibilidades más allá de la simple transferencia de valor, permitiendo instrumentos financieros complejos, registros de propiedad digital e incluso organizaciones autónomas dentro de blockchain.

Cómo funciona Ethereum

En su base, Ethereum se apoya en la misma tecnología blockchain que impulsa Bitcoin. Una blockchain es una cadena de bloques, y cada bloque contiene un registro de transacciones. Lo que la hace especial es que este registro lo mantienen miles de ordenadores (nodes) en todo el mundo, no una autoridad central como un banco.

¿Qué son los smart contracts?

Donde Ethereum realmente brilla es en los smart contracts. Piensa en ellos como acuerdos digitales que se ejecutan automáticamente cuando se cumplen condiciones predefinidas, como una máquina expendedora que te da un refresco cuando introduces el importe exacto. Estos contratos son:

Se autoejecutan: funcionan automáticamente cuando se cumplen las condiciones

Inmutables: una vez desplegados, no se pueden modificar

Transparentes: cualquiera puede verificar el código del contrato

Trustless: no necesitas confiar en un tercero; el código es la garantía

¿Qué es Ether (ETH)?

Ether (ETH) es la criptomoneda nativa de la red Ethereum. Cumple dos funciones principales:

Como moneda digital que se puede enviar al instante a cualquier persona, en cualquier lugar

Como “combustible” para ejecutar smart contracts y transacciones en la red

¿Qué son las gas fees?

Esto nos lleva a las gas fees. Igual que un coche necesita combustible, las operaciones en Ethereum necesitan “gas” para ejecutarse. Las gas fees son pequeñas cantidades de ETH (medidas en “gwei”, una subunidad de ETH) que se pagan a los participantes de la red que aportan potencia de cálculo para validar transacciones. Estas comisiones ayudan a mantener la red segura y evitan el spam o programas que se ejecuten indefinidamente y saturen el sistema.

Cuando la red está muy ocupada, el precio del gas sube porque hay espacio limitado en cada bloque, lo que puede encarecer las transacciones de Ethereum en momentos de alta demanda.

¿Qué son los estándares de token?

Ethereum revolucionó el ecosistema de las criptomonedas con sus estándares de token. Son marcos que definen cómo se comportan los activos digitales en la red.

Los estándares de token de Ethereum son como planos de arquitectura: ofrecen un diseño consistente que los desarrolladores pueden seguir para asegurar que cada “estructura” (token) encaje sin fricciones en la “ciudad” (el ecosistema Ethereum).

Los 3 principales estándares de token de Ethereum

ERC-20: estableció la plantilla para tokens fungibles (intercambiables), facilitando crear nuevos tokens sin construir una blockchain nueva (aunque la adopción depende del diseño y la demanda). Este estándar impulsa miles de tokens, incluidas stablecoins como USDC y la mayoría de tokens de DeFi.

ERC-721: fue el primer estándar que definió los NFTs en Ethereum, aunque hoy existen otros estándares relacionados con NFTs, como ERC-2981 para royalties. Hizo posible la revolución del arte digital e impulsó colecciones como CryptoPunks y Bored Ape Yacht Club.

ERC-1155: introducido por Enjin, es ideal para juegos y aplicaciones de metaverso donde se necesitan tanto tokens fungibles como NFTs y coleccionables únicos.

Estos estándares transformaron crypto al crear una interoperabilidad masiva: de repente, los tokens construidos en Ethereum funcionaban al instante con cientos de wallets y exchanges. Esta funcionalidad “plug-and-play” aceleró de forma drástica la innovación y la adopción.

La influencia de estos estándares es tan grande que incluso blockchains competidoras implementan compatibilidad con ellos, convirtiéndolos prácticamente en el lenguaje universal de los activos digitales.

El ecosistema de Ethereum

El verdadero poder de Ethereum está en su ecosistema, que no deja de crecer:

Aplicaciones descentralizadas (dapps)

Son aplicaciones construidas en Ethereum que conectan usuarios y proveedores directamente, sin que ninguna organización intermediaria controle el servicio. Ejemplos conocidos:

Uniswap: un exchange descentralizado para hacer trading de tokens

Aave: una plataforma de préstamos y borrowing

OpenSea: un marketplace de activos digitales

DeFi (finanzas descentralizadas)

Quizá el impacto más transformador de Ethereum ha sido en las finanzas. Las aplicaciones DeFi replican servicios financieros tradicionales como lending, borrowing y trading, pero sin bancos ni brokers.

En su lugar, usan smart contracts para crear protocolos que funcionan exactamente como fueron programados. Para abril de 2025, el total value locked en protocolos DeFi ha crecido hasta decenas de miles de millones de dólares, lo que demuestra una adopción significativa.

NFTs (Non-Fungible Tokens)

Los NFTs representan activos digitales únicos, desde arte hasta música o bienes inmuebles virtuales. A diferencia de las criptomonedas, donde cada unidad es idéntica, cada NFT tiene propiedades distintas que lo hacen irrepetible.

Esta tecnología ha transformado el arte digital al permitir propiedad verificable y escasez digital, impulsando nuevas formas de creación y oportunidades de ingresos para artistas.

DAOs (Decentralised Autonomous Organisations)

Las DAOs son organizaciones nativas de internet, propiedad y gestión colectiva por sus miembros. Operan según reglas codificadas en smart contracts: los miembros votan decisiones y el resultado se ejecuta automáticamente mediante código. Desde clubs de inversión hasta fundaciones benéficas, las DAOs están reimaginando cómo nos organizamos y colaboramos.

Ethereum 2.0 y The Merge

En 2022, Ethereum vivió su actualización más importante desde su lanzamiento al pasar de Proof of Work (PoW) a Proof of Stake (PoS) con un evento conocido como “The Merge”. Esta transición abordó varios retos clave:

Impacto medioambiental

El Ethereum original (como Bitcoin) usaba Proof of Work, que requiere gran potencia de cálculo y consumo energético. El cambio a Proof of Stake redujo el consumo de energía de Ethereum aproximadamente un 99,95%, resolviendo una de las críticas más fuertes a la tecnología blockchain.

Escalabilidad

La popularidad de Ethereum generó congestión de red y gas fees altas. El paso a PoS sentó las bases para futuras soluciones de escalado, incluyendo sharding (dividir la red en segmentos paralelos para aumentar drásticamente la capacidad de transacciones).

Oportunidades de staking

Con el nuevo sistema, los usuarios pueden hacer staking de su ETH (bloquearlo como colateral) para ayudar a asegurar la red y ganar recompensas, normalmente alrededor del 3–5% anual. Esto permite a los holders de ETH generar ingresos pasivos mientras contribuyen a la seguridad de la red.

Ethereum frente a otras blockchains

Ethereum vs Bitcoin

- Bitcoin: principalmente reserva de valor y medio de intercambio

- Ethereum: plataforma para construir aplicaciones y ejecutar smart contracts

“Ethereum killers”

- Solana: ofrece mayor velocidad de transacción y menores costes

- Cardano: se centra en investigación académica y verificación formal

- Polkadot: creado por un cofundador de Ethereum para permitir interoperabilidad entre cadenas

- Avalanche: prioriza alto rendimiento y finalización rápida

Estas ventajas pueden implicar compromisos en aspectos como descentralización, madurez del ecosistema o facilidad de uso.

Ventajas de Ethereum

- Ventaja del pionero y enorme comunidad de desarrolladores

- Alta seguridad gracias a una red grande y distribuida

- Ecosistema más amplio de aplicaciones y herramientas

- Fuertes efectos de red y reconocimiento de marca

Riesgos y consideraciones

Ethereum ofrece posibilidades muy interesantes, pero también es importante conocer los riesgos:

Volatilidad de precio

ETH, como la mayoría de criptomonedas, tiene fuertes oscilaciones. Desde 2015 ha vivido caídas del 90% y subidas de 1000% o más.

Riesgos de seguridad

Aunque el protocolo base de Ethereum ha demostrado ser seguro, los smart contracts pueden contener errores o vulnerabilidades. Algunos hacks conocidos han provocado pérdidas de cientos de millones a lo largo de los años.

Incertidumbre regulatoria

Gobiernos de todo el mundo siguen definiendo cómo regular crypto y DeFi. Cambios regulatorios pueden afectar ciertas aplicaciones o casos de uso.

Retos técnicos

A pesar de las mejoras, Ethereum aún debe seguir avanzando en escalabilidad, mantener descentralización y ofrecer una experiencia de usuario más fluida.

El futuro de Ethereum

El roadmap de Ethereum sigue evolucionando, con varias líneas clave:

Soluciones de escalado: se espera que sharding aumente de forma significativa la capacidad al dividir la red en segmentos paralelos, con potencial para miles de transacciones por segundo.

Crecimiento de Layer 2: soluciones como Optimism, Arbitrum y Polygon siguen ganando tracción, con comisiones menores y transacciones más rápidas, manteniendo seguridad al liquidar en la main chain de Ethereum.

Adopción por parte de la industria: grandes compañías de finanzas y entretenimiento exploran Ethereum para casos como seguimiento de supply chain o distribución de royalties. Se espera que la adopción empresarial acelere con mejoras de escalabilidad.

Integración con Web3: la visión de Web3, un internet más descentralizado donde los usuarios controlan sus datos e identidades digitales, se construye en gran parte sobre Ethereum, lo que podría cambiar cómo interactuamos con servicios online.

Cómo comprar Ethereum (ETH)

Si quieres involucrarte en el ecosistema Ethereum y tener el activo que impulsa la red, necesitarás comprar ETH en plataformas de confianza como Tap, y después configurar una wallet de Ethereum si así lo deseas.

Reflexión final: por qué Ethereum importa

Ethereum representa uno de los experimentos tecnológicos más ambiciosos de nuestro tiempo: un intento de reconstruir las bases de cómo transaccionamos, colaboramos y creamos en internet. Al eliminar intermediarios y permitir interacciones peer-to-peer directas, Ethereum desafía estructuras tradicionales y abre nuevas posibilidades de coordinación humana.

Que Ethereum acabe cumpliendo su visión de convertirse en la capa de liquidación de un internet descentralizado dependerá de cómo resuelva los retos de escalabilidad, usabilidad y regulación. Pero su impacto ya es innegable: ha dado lugar a industrias enteras, desde DeFi hasta NFTs, e inspiró a una generación de desarrolladores a replantearse lo que es posible con la tecnología blockchain.

Lo más interesante de Ethereum quizá sea que aún estamos en los primeros capítulos de su historia. Como el internet de los años 90, podemos ver su potencial, pero todavía no imaginamos todas las formas en que transformará el mundo en las próximas décadas.