Some crypto companies are fully compliant, fully regulated, and still can't keep their bank accounts. Learn why the financial system is quietly freezing them out.

Keep reading

Why can't a fully compliant, regulated crypto business secure a bank account in 2025?

If you're operating in this space, you already know the answer. You've lived through it. You've submitted the documentation, walked through your AML procedures, and demonstrated your regulatory compliance… only to be rejected. Or worse still, waking up to find your existing account frozen, with no real explanation and no path forward.

This isn't about isolated cases or bad actors being weeded out. It's a pattern of systematic risk aversion that's creating real barriers to growth across the entire sector, and it's throttling one of the most significant financial innovations of our generation.

We're Tap, and we're building the infrastructure that traditional banks refuse to provide.

The Economics Behind the Blockade

Let's examine what's actually driving this exclusion, because it's rarely about the reasons banks cite publicly.

The European Banking Authority has explicitly warned against unwarranted de-risking, noting it causes "severe consequences" and financial exclusion of legitimate customers. Yet the practice continues, driven by two fundamental economic pressures that have nothing to do with your business's actual risk profile.

The compliance cost calculation

Financial crime compliance across EMEA costs organizations approximately $85 billion annually. For traditional banks, the math is simple: serving crypto businesses requires specialized expertise, enhanced monitoring, and ongoing due diligence. As a result, it's cheaper to reject the entire sector than to build the infrastructure needed to serve it properly.

The regulatory capital burden

New EU regulations impose a 1,250% risk weight on unbacked crypto assets such as Bitcoin and Ethereum. This isn't a compliance requirement; it's a capital penalty that makes crypto exposure commercially unviable for traditional institutions, regardless of the actual risk individual clients present.

In the UK, approximately 90% of crypto firm registration applications have been rejected or withdrawn, often citing inadequate AML controls. Whether those assessments are accurate or not, they've created the perfect justification for blanket rejection policies.

The result? Compliant businesses are being treated the same as bad actors; not because of what they've done, but because of the sector they're in.

The Real Cost of Financial Exclusion

Financial exclusion isn’t just an hiccup; it creates tangible operational barriers that ripple through every part of running a crypto business.

Firms that have secured MiCA authorization, built robust compliance programs, and met regulatory requirements can find themselves locked out of basic banking services. Essential fiat on-ramps and off-ramps remain inaccessible, slowing payments, limiting growth, and complicating cash flow management.

Individual cases illustrate the problem vividly as well. Accounts are closed because a business receives a payment from a regulated exchange. Others are dropped with vague references to “commercial decisions,” offering no substantive justification. Founders frequently struggle to separate personal and business finances, as both are considered too risky to serve.

The irony is striking. By refusing service to compliant businesses, traditional banks aren’t mitigating risk; they’re amplifying it. Forced to operate through less regulated channels, these legitimate firms face higher operational and compliance risks, slower transactions, and reduced investor confidence. Over time, this slows innovation, and raises the cost of doing business for firms that are legally and technically sound.

Debanking Beyond Europe: U.S. Crypto Firms Face Their Own Challenges

Limited access to banking services isn’t exclusive to Europe. Leading firms in the U.S. crypto industry have faced numerous challenges regarding the banking blockade. Alex Konanykhin, CEO of Unicoin, described repeated account closures by major banks such as Citi, JPMorgan, and Wells Fargo, noting that access was cut off without explanation. Unicoin’s experience echoes a broader sentiment among crypto executives who argue that traditional financial institutions remain wary of digital asset businesses despite recent policy shifts toward a more pro-innovation stance.

Jesse Powell, co-founder of Kraken, has also spoken out about being dropped by long-time banking partners, calling the practice “financial censorship in disguise.” Caitlin Long, founder of Custodia Bank, recounted how her institution was repeatedly denied services. Gemini founders Tyler Winklevoss and Cameron Winklevoss shared similar frustrations.

These experiences reveal a pattern many in the industry interpret as systemic risk aversion. Even in a market as large and mature as the United States, crypto-focused businesses continue to encounter obstacles in maintaining basic financial infrastructure. The issue became especially acute after the collapse of crypto-friendly banks such as Silvergate, Signature, and Moonstone; institutions that once served as key bridges between fiat and digital assets. Their exit left a gap few traditional players have been willing to fill.

Why Tap Exists

The crypto industry has reached an inflection point. Regulatory frameworks like MiCA are providing clarity. Institutional adoption is accelerating. The technology is proven and tested. But the fundamental infrastructure gap remains: access to business banking that actually works for digital asset businesses.

This is precisely why we built Tap for Business.

We provide business accounts with dedicated EUR and GBP IBANs specifically designed for crypto companies and businesses that interact with digital assets. This isn't a side offering or an experiment, it's our core focus.

Our approach is straightforward

We built our infrastructure for this sector

Rather than retrofitting traditional banking systems to reluctantly accommodate crypto businesses, we designed our compliance, monitoring, and operational frameworks specifically for digital asset flows. This means we can properly assess and serve businesses that others automatically reject.

We price in the actual risk, not the sector

Blanket rejection policies exist because they're cheap and simple. We take a different approach: evaluating each business based on their actual controls, compliance posture, and operational reality. It costs more, but it's the only way to serve this market properly.

We're committed to sector normalization

Every time a legitimate crypto business is forced to operate without proper banking infrastructure, it reinforces outdated stigmas. By providing professional financial services to compliant businesses, we're helping demonstrate what should be obvious: crypto companies can and should be served by the financial system.

It isn't about taking on risks that others won't. It's about properly evaluating risks that others refuse to understand.

Moving Forward

The industry is maturing. Regulatory clarity is emerging. Institutional adoption is accelerating. But you can't put your business on hold while traditional banks slowly catch up to reality.

That's not sustainable in the long run.

As a firm, you shouldn't have to beg for a bank account. You shouldn't have to downplay your crypto operations just to access basic financial services. And you certainly shouldn't have to accept that systematic exclusion with little to no explanation other than “It’s just how things are."

The crypto sector is building the future of finance. Your banking partner should believe in that future too. If you're ready to work with financial infrastructure built for your business, not in spite of it, here we are.

Talk today with one of our experts to understand how we can help your business access the banking infrastructure you need.

NEWS AND UPDATES

LATEST ARTICLE

We’ve covered what Proof of Work and Proof of Stake is, but what is PaaS?

In this article, we’re making this rather complicated-sounding term easy to understand as we explore where it came from, what it means, and why it’s likely to keep popping up in the crypto realm.

What Is PaaS?

PaaS stands for Platform as a Service and refers to a cloud delivery service that uses third-party cloud service providers. “As a service” indicates that the cloud computing service is provided by a third party, rather than the user having to manage their own hardware and software.

PaaS providers offer a range of services, including operating systems, databases, middleware, and other software development tools. PaaS offerings can be used for both cloud-native and hybrid cloud applications.

PaaS solutions are popular among software developers and businesses looking to migrate their applications to the cloud. They provide an application development platform that can be used to build and deploy applications quickly and easily, without the need for specialized hardware or software.

Some of the key benefits of PaaS include reduced costs, faster deployment, and greater flexibility and scalability. PaaS providers offer a range of services, including operating systems, databases, middleware, and other software development tools. This allows users to develop, run, and manage applications without having to worry about the underlying infrastructure.

The History of PaaS

PaaS first appeared in 2005 as Zimki under the company Fontago. Zimki allowed users to build and deploy web services and applications through its code execution platform.

Billing was determined based on the number of JavaScript operations, the amount of web traffic and the total storage used, providing users with a much clearer cost structure than on other platforms. The platform was eventually shut down in 2008 by its parent company.

That same year the Google App Engine was launched allowing users to create web services and applications using languages like Go, PHP, Node.js, Java and Python.

Today, Google remains the biggest PaaS vendor in the world.

How Does PaaS Work?

Instead of replacing its overall IT infrastructure and running these services in-house, PaaS streamlines access to its key services. This helps to reduce time in deployment as well as minimize startup costs.

PaaS allows users to tap into resources and functions like capacity on demand, data storage, text editing, vision management and testing services despite being in geographically different locations. All while using a pay-per-use model.

PaaS Offers Development Tools

PaaS, or Platform as a Service, is a cloud-based platform that provides users with access to the tools and resources needed to develop and run applications. Instead of replacing its overall IT infrastructure and running these services in-house, PaaS streamlines access to its key services, allowing users to easily tap into resources and functions like capacity on demand, data storage, text editing, vision management, and testing services. This pay-per-use model enables users to access the tools and resources they need without incurring the high costs of building and maintaining their own infrastructure.

PaaS technology offers a range of benefits for both developers and businesses, including the ability to easily integrate databases, manage infrastructure, and access data centers. This can provide a range of advantages, such as improved performance, enhanced security, and increased scalability.

PaaS technology providers also offer a range of services and support to their customers, including integration platforms and infrastructure management services. This can help businesses to quickly and easily integrate their applications with other systems and platforms, allowing them to take advantage of the benefits of PaaS without having to worry about the underlying infrastructure.

PaaS vs IaaS vs SaaS

PaaS, IaaS, and SaaS are all different models of cloud computing. PaaS, or Platform as a Service, provides access to the tools and resources needed to develop and run applications, while IaaS, or Infrastructure as a Service, offers access to the underlying infrastructure, including storage, networking, and computing power. SaaS, or Software as a Service, provides access to software applications over the internet.

These models differ in terms of what areas are handled on-site and which are handled by a third-party provider. For example, with PaaS, the infrastructure and operating system are managed by the provider, while the customer focuses on developing and deploying their own applications. With IaaS, the provider manages the infrastructure, while the customer is responsible for the operating system and applications. With SaaS, the provider manages everything, including the infrastructure, operating system, and applications.

Examples of companies that offer PaaS services include Amazon Web Services and the IBM Cloud, while IaaS providers include AWS, Microsoft Azure, and Google Cloud. Dropbox, Salesforce, and Google Apps are examples of SaaS providers.

These models offer advantages to businesses and developers looking to enter the cloud computing space. For example, PaaS offers the ability to focus on app development without worrying about the underlying infrastructure, while IaaS and SaaS provide access to cloud resources and the ability to quickly deploy and scale applications. These models can also be used to build communications platforms and other mobile applications, providing access to the necessary infrastructure and resources.

PaaS Provider In Blockchain

The use of PaaS technology, or Platform as a Service, within the blockchain industry is becoming increasingly popular. While blockchain platforms themselves are not typically structured in a PaaS way, the concept of BPaaS, or Blockchain Platform as a Service, offers businesses and enterprises the opportunity to focus on the development of software and other services for customers.

BPaaS provides numerous advantages for companies looking to enter the blockchain space. It allows businesses to leverage the power of cloud-based infrastructure and resources to develop and deploy applications without the need to manage their own hardware and software.

PaaS providers like Amazon Managed Blockchain and the IBM Blockchain Platform are leading the way in offering BPaaS solutions to businesses. These platforms offer a range of tools and resources for application development, including integrated development environments (IDEs), code libraries, and APIs. This allows developers to focus on building and deploying their own blockchain-based applications without worrying about the underlying infrastructure.

Overall, the use of PaaS in the blockchain industry offers numerous benefits, including reduced production costs, streamlined deployment, and the ability to easily integrate specific AI capabilities into applications. This makes it an attractive option for businesses looking to enter the blockchain space.

Crypto lending might be the hot new product in the cryptocurrency space, but before you dive in be sure to first understand what it entails. The concept grew great traction with the rise of the decentralized finance (DeFi) movement, with platforms offering users high yields for borrowing crypto assets.

Let’s get started with what crypto lending is, and then explore how the product works.

What is crypto lending?

Crypto lending is a traditional banking service curated to the crypto world. With the DeFi space remains largely unregulated, many crypto exchanges and other platforms have started offering these services, with added security.

Crypto lending involves a user lending crypto assets to a platform in return for interest, which allows other users to then borrow said crypto assets, paying interest on the amount borrowed. The platform will then take a small percentage of the interest paid.

Depending on the platform and other factors, crypto lending platforms may be centralized or decentralized and offer exceptionally high-interest rates, with annual percentage yields (APYs) of 15% or more. With the interest rates being higher than traditional bank accounts, lenders gain access to much greater yields, increasing their returns.

Another advantage to crypto lending is that users are still exposed to price gains in the market. Meaning that if you deposit your Bitcoin when it's worth $20,000 and the price rises in value to $50,000, you are still able to realize these returns and earn interest for the duration of the loan.

Note that interest rates might fluctuate with market conditions on some platforms, increasing when the prices increase and decreasing when markets are down.

How does crypto lending work?

Cryptocurrency lending platforms function as middlemen connecting lenders to borrowers. Lenders deposit their digital currency into high-interest lending accounts, and borrowers utilize the lending platform to acquire loans. These systems then lend money utilizing the crypto that investors have provided them.

The platform controls its net interest margins by establishing the interest rates for both lending and borrowing.

Rates on platforms differ from cryptocurrency to cryptocurrency, some platforms might offer higher interest rates to lenders willing to commit to a certain time frame. There is no standard interest rate for cryptocurrencies, as each platform has its own set of rules.

Centralized crypto lending means putting your money in the hands of a corporation or other entity to manage and make the process easier. Accounts are created for borrowers and lenders, and loans may be requested by applicants.

Lenders and borrowers may connect their cryptocurrency wallets to a decentralized crypto lending protocol, which uses smart contracts to automate the lender-borrower relationship. Smart contracts are automated digital agreements that execute once certain criteria is met.

The advantages of crypto lending

There are several benefits to crypto lending when comparing it to a regular bank account.

Borrowers have access to these financial services without having to pass a credit check, making it more financially inclusive than traditional banking services. They are also exposed to lower interest rates than regular banking loans.

Lenders that give loans in the form of cryptocurrencies can make a lot more money from their crypto assets than savings accounts. It may also be a more adaptable choice to crypto staking, which requires users to lock up their cryptocurrency and submit it to a blockchain security method. Depending on the platform, lending usually gives users access to their funds.

The downside to crypto lending

The agreement with crypto loan companies is generally made on individual terms by institution borrowers. As interest rates vary across platforms and cryptocurrencies, each company is different.

There have been several cases where lending platforms have been hit by severe liquidity crisis, notably Celsius, Voyager Digital, and BlockFi. Glenn Huybrecht, COO of Cake DeFi, said, “Some lending providers have been very generous with low collateral requirements, which then puts them in hot water when one of their customer's defaults.”

Due to the ongoing regulation battles, these crypto services are also not backed by government safety nets, like the traditional banks are. However, some platforms do hold insurance and the necessary regulatory accreditations so be sure to seek one that has all of the above.

Closing thoughts

Crypto lending platforms differ greatly from one another so be sure to check each platform, their interest rates for all the various currencies supported, and if there are any lock-up periods or fees payable.

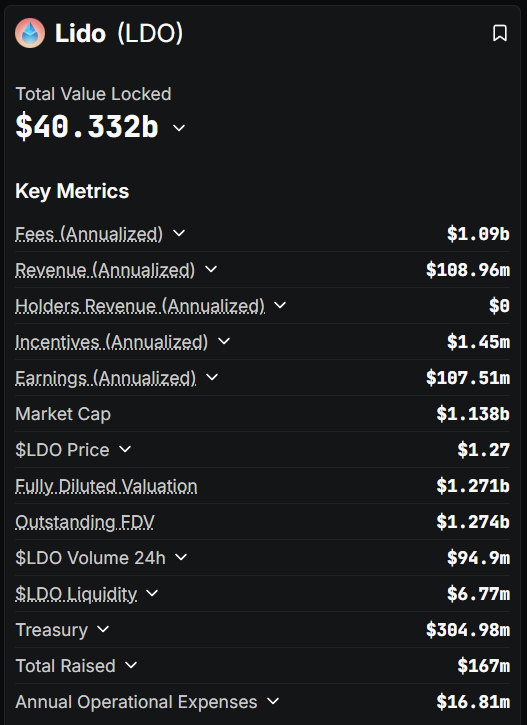

If you’re interested in staking Ethereum, you came to the right place. The largest liquid staking protocol in the crypto ecosystem, trusted by thousands of ETH holders who want rewards without losing liquidity, has a name: Lido DAO.

Ethereum's Leading Liquid Staking Protocol

How does it work?

Lido DAO is a decentralized autonomous organization that provides a liquid staking solution on the Ethereum 2.0 blockchain as well as other Proof of Stake (PoS) platforms like Solana (SOL), Polygon (MATIC), Polkadot (DOT), and Kusama (KSM).

Instead of locking up funds, users stake ETH and receive stETH tokens in return, which represent their staked ETH plus accrued rewards. This allows users to continue trading, lending, or using their tokens across DeFi while still benefiting from staking yields. Since launching in 2020, Lido DAO has grown to manage more than $40.33B in Total Value Locked (TVL), with staking rewards currently averaging an annual percentage rate (APR) of 2.71%. The protocol is governed by holders of the LDO token, ensuring community-driven decision-making.

Where did it come from?

Lido DAO was co-founded by Kasper Rasmussen and Jordan Fish, also known as CryptoCobain. Behind the Lido DAO are a number of individuals and organizations that are well-regarded within the DeFi space. Since its inception in December 2020, shortly after ETH 2.0's release, the platform has been overseen by the Lido DAO, with several key members including Semantic VC, Chorus, ParaFi Capital, P2P Capital, Libertus Capital, Terra, StakeFish, Bitscale Capital, StakingFacilities, and KR1. Several of the highly esteemed angel investors include Stani Kulechov of Aave, Banteg of Yearn, Will Harborne of Deversifi, Julien Bouteloup from Stake Capital, and Kain Warwick from Synthetix.

Since then, Lido DAO has gained an impressive reputation for its liquid staking capabilities, and now boasts over $13 billion in staked assets. Its core focus is on Ethereum, yet its horizons are expanding to other blockchain networks including Terra and Solana, both of which launched staking capabilities in 2021, as well as several other layer 1 PoS blockchains.

Liquid Staking Made Simple

Lido DAO simplifies staking into a three-step process: deposit ETH, receive stETH, and start earning rewards automatically. When a user deposits ETH, the protocol delegates funds to a decentralized network of professional node operators. There are over 800 node operators worldwide, who manage validation securely and efficiently.

The stETH tokens received are liquid ERC-20 assets whose value increases over time as rewards accumulate. With one-click staking through Lido DAO’s interface, users can skip the hassle of running their own validator while enjoying a 98.2% validator performance.

How validator rewards are earned from staked assets

So, in order to stake ETH, become a validator and earn rewards for validating payments on the Ethereum platform, users are required to stake a minimum of 32 ETH tokens. What if I don’t have 32 ETH? You may ask. To bypass this minimum requirement and still earn rewards, Lido DAO allows users to stake a fraction of this amount and earn a proportionate amount of block rewards.

Users will then deposit ETH into the Lido smart contract and receive the same number of stETH. These tokens are minted once the funds have been received and are burned when the users withdraw their original ETH. The staked funds will then be distributed to the validators on the Lido network and deposited into the Ethereum Beacon Chain from where they will be secured in a smart contract.

The Lido DAO will then assign, onboard, support and enter the validators' addresses to the smart contract registry before being given a set of keys for the validation. All ETH that users have deposited on the Lido platform will be split into groups of 32 ETH among the active Lido node operators who will use this public validation key to validate transactions. The block rewards will then be shared proportionately.

Notably, this distribution process of sharing staked assets eliminates single-point-of-failure risks common among single-validator staking.

Your Liquid Staking Asset

At the center of Lido DAO’s system is stETH, the tokenized representation of staked ETH. stETH trades on major exchanges, offering deep liquidity and integration with several DeFi protocols. Staking rewards are earned automatically, so users never need to claim manually.

Users can stake any amount of ETH to the Beacon Chain without having to deal with lock-up requirements or withdrawal delays. This way Ethereum holders can enjoy both liquidity and yield simultaneously. For providing this staked ETH service, a 10% fee is collected by Lido for each process.

DeFi Integration Opportunities

For advanced users, stETH unlocks a wide range of yield optimization strategies. Lending platforms like AAVE accept stETH as collateral, while liquidity pools on CURVE and UNISWAP offer additional yield opportunities. Leveraged staking strategies also allow users to compound rewards further.

Proven Security

Security and safety are central to Lido DAO's success. Since the beginning, the protocol has undergone a dramatic array of independent audits, conducted by top-tier firms including Statemind, Certora, Hexens, Oxorio, MixBytes, and Ackee Blockchain.

Importantly, Lido DAO has never suffered a major protocol-wide hack. The protocol takes advantage of open-source code, multisig governance, and safeguards like GateSeal for emergency pauses, deposit security modules, and DAO oversight to anticipate and mitigate emerging threats. These layers of defense, combined with a multi-validator, geographically distributed network, reduce single points of failure.

What is Lido DAO token (LDO)?

Governance of the Lido DAO is powered by the LDO token, which grants voting rights to its holders. With a market capitalization of $1.14B and an all time high (ATH) price of $2.38 USD, LDO plays a central role in shaping the protocol’s future. Token holders vote on proposals, influence fee structures, and participate in selecting node operators. The governance community is highly active, with regular proposals and ongoing discussions that ensure the protocol evolves in a decentralized and transparent way.

How to buy Lido LDO?

Staking with Lido DAO is meant to be as accessible as possible. There are no minimum deposit requirements; end users can stake any amount of ETH. You can connect an Ethereum wallet, confirm the transaction, and receive stETH instantly.

If you're looking to expand your digital currencies portfolio, LDO tokens can be a potential addition. The Tap app provides an easy and secure way for anyone with an account to add these tokens to their portfolios in no time, making it one of the most effortless trading experiences around.

You can utilize the Tap app to access the Lido ecosystem by purchasing LDO tokens with either crypto or fiat currencies. End users can then choose to store their LDO tokens securely in the integrated crypto wallet or transfer them to the Lido platform and engage in the platform's earning potential. All you need to do to get started is download the app and create an account in minutes.

We are delighted to announce the listing and support of Ankr (ANKR) on Tap!

ANKR is now available for trading on the Tap mobile app. You can now Buy, Sell, Trade or hold ANKR for any of the other asset supported on the platform without any pair boundaries. Tap is pair agnostic, meaning you can trade any asset for any other asset without having to worries if a "trading pair" is available.

We believe supporting ANKR will provide value to our users. We are looking forward to continue supporting new crypto projects with the aim of providing access to financial power and freedom for all.

Ankr is playing an integral role in the adoption of Web3, providing growth and development opportunities for network stakers, app developers, and other participants in the DeFi space.

Ankr is a decentralized Web3 infrastructure provider that facilitates the swift and effortless connection between developers, dapps, stakers, and blockchains. With Ankr's APIs & RPCs you can quickly build blockchain-based applications with confidence, stake on Ankr Earn as well as access custom solutions for any blockchain enterprise needs.

ANKR is Ankr's native cryptocurrency fueling the platform and is used as a payment method within the ecosystem.

Get to know more about Ankr (ANKR) in our dedicated article here.

.svg)

Playing an important role in the adoption of Web3, Enjin provides a platform of software products designed to allow anyone to harness the power of NFTs (non-fungible tokens) through the development, trade, monetization, and marketing of blockchain assets.

What is the Enjin platform?

The Enjin platform is an ecosystem of interconnected, blockchain-based gaming products designed for individuals, game developers and businesses to create, manage and trade virtual goods such as digital art, games, or virtual marketplaces using the Ethereum blockchain. Enjin aims to provide users with the tools to implement smart digital solutions for blockchain games within the gaming environment.

Through the platform's software development kits (SDKs) and APIs, users can build digital assets as well as seamlessly integrate them into their games and applications.

Under the Enjin umbrella is the Enjin Network, a community gaming platform that allows users to create websites, chat, and host virtual stores. Over the course of a decade, the Enjin platform has accumulated over 20 million users.

Powering the ecosystem is the Enjin Coin (ENJ), a token used to back the value of NFTs and other assets minted on the platform. When an asset is minted it locks ENJ tokens into a smart contract and effectively removes the tokens from circulation.

It’s also worth noting that Witek Radomski, Enjin's co-founder and the brainchild behind the ERC-1155 Ethereum token standard, wrote the code for the first non-fungible token (NFT). By utilizing its cutting-edge technology, Enjin is revolutionizing the future of gaming and digital assets.

Who created Enjin?

Enjin was originally founded in 2009 as a gaming community platform by Maxim Blagov and Witek Radomski. Blagov took on the responsibility of being CEO and in charge of the platform's creative direction while Radomski took on the role of CTO, leading the technical development of the platform's products.

Following Radomski's interest in Bitcoin in 2012, the platform explored incorporating blockchain technology into its business model and embraced the world of tokenized digital assets.

Radomski went on to write the ERC-1155 token standard in June 2018, a token standard used for minting both fungible, semi-fungible and non-fungible tokens using the Ethereum network. This token standard is a critical building block in the platform’s design.

In 2017, the Enjin platform launched an initial coin offering (ICO), raising $18.9 million through ENJ token sales. A year later the project went live and in September 2019, the Enjin Marketplace was launched.

How does Enjin work?

The primary goal of the Enjin network is to facilitate the management and storage of virtual goods for games, anything from in-game currencies to unique in-game items. So, how does Enjin work? The process of creating and destroying these tokens involves five steps, as outlined below.

- Purchase

Developers purchase Enjin Coin. - Minting

In-game items are designed and effectively minted with the appropriate amount of ENJ locked into a smart contract. - Utilization

Players use these tokens within the game. - Trading

Players trade the tokens between fellow players or on the internal or external marketplace. - Melting

Players sell the tokens for Enjin Coin, referred to as melting. The token is destroyed and Enjin Coin is released from the smart contract.

SDKs (software development kits) come into play here, with kits designed to fulfill certain functions, such as facilitating a payment platform or being wallet-focused. These kits are designed to minimize costs and simplify the process of creating these virtual goods. APIs (application programming interfaces) work alongside the SDKs to integrate these virtual goods (digital assets) into the game.

The Enjin platform utilizes JumpNet which is integrated with other products in the ecosystem, such as the Marketplace, Enjin Beam, and the Enjin Wallet to allow for gas-free transactions for ENJ and NFTs.

The Enjin ecosystem encompasses the Enjin smart wallet that allows players to store and trade their in-game items with ease. The Enjin wallet is designed to connect all the features, from managing inventory to conducting transactions and selling these tokenized digital assets for ENJ.

What is the Enjin Coin (ENJ)?

Enjin Coin (ENJ) is the native token of the Enjin ecosystem. Built on the Ethereum blockchain and compatible with multiple gaming platforms, the Enjin Coin is an ERC-20 token that allows the in-game items created on the platform to be traded with real-world value. The ENJ token has a maximum supply of 1 billion coins.

The token also allows developers to mint these digital goods. The process requires the users to lock Enjin Coin (ENJ) into a smart contract that automatically assigns value to the in-game item. Players that later use these items can use them in the game, trade them or sell them for ENJ, equivalent to the original minting cost. Once sold, the item is destroyed (known as melting) and the ENJ that was locked in the smart contract is released to the seller.

How can I buy Enjin Coin?

Anyone can tap into the Enjin ecosystem by acquiring ENJ tokens through the Tap mobile app. Simply create an account and complete the verification process in order to gain access to your unique Enjin wallet, from where you can buy, trade and sell Enjin Coin.

Fully licensed and regulated, Tap provides a secure and convenient means of managing your funds, allowing users to manage and store both crypto and fiat currencies in one location. With a wide range of supported currencies and services, Tap is revolutionizing the financial space.

Take advantage of the power of Enjin Coin on the Tap app - the ultimate platform to buy, sell or hold ENJ. With seamless integration and an intuitive interface, trading Enjin tokens has never been easier. Stay up-to-date with the latest market trends and keep your portfolio on track by monitoring the Enjin Coin price in real-time.

We're thrilled to share that our fintech company has just celebrated its third anniversary! It's been an incredible journey so far, and we're so grateful for the opportunity to serve our users every day.

When we first launched our platform three years ago, we had a clear mission in mind: to provide an innovative, user-friendly, and accessible way for people to manage their money, trade cryptocurrencies, and access financial services. It was a big goal, and we knew that we had a lot of hard work ahead of us.

But we were determined to succeed. Our small team of passionate and dedicated individuals worked tirelessly, day in and day out, to bring our vision to life. We poured our hearts and souls into this project, and we knew that we were onto something special.

Fast forward three years, and we're proud to say that we've come a long way. We've built a platform that we believe in, and we're constantly striving to improve it. We've listened to feedback from our users, and we've added new features and services that meet their needs. And we've built a community of passionate and engaged users who share our vision for a better way to manage their finance everyday.

One of the things that sets our company apart is our commitment to transparency and user experience. We believe that managing your finances should be easy, intuitive, and stress-free. That's why we've built our platform to be as user-friendly as possible, with clear and straightforward interfaces that make it easy to manage your money and digital assets.

But our success wouldn't be possible without our amazing users. We're so grateful for your continued support, feedback, and encouragement. You've helped us to shape our platform into something truly special, and we're committed to continuing to serve you and improve our platform to meet your needs.

As we celebrate our third anniversary, we're excited to look back on how far we've come and to look forward to all the exciting things that the future holds. We're proud of what we've accomplished, but we know that there's always more work to be done. We're committed to continuing to innovate and improve, and we're grateful to have you along for the ride.

Thank you for being part of our journey. Here's to many more years of growth, success, and innovation!