Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

Heading into the Federal Open Market Committee’s October session, a high-stakes environment is emerging for crypto markets. With the CME Group’s FedWatch Tool showing about a 96 % chance of a 25-basis-point rate cut, the market is eyeing how digital-asset prices might respond.

With macro liquidity on the radar again, these three altcoins stand out as tokens worth tracking under the spotlight of the Fed’s next move.

1. Chainlink (LINK)

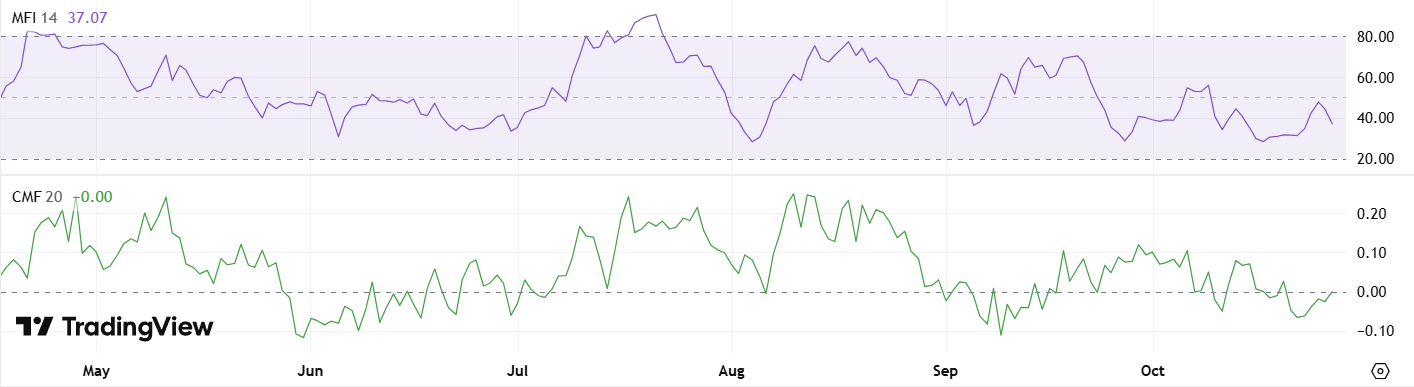

Chainlink has been acting under pressure, trading inside a falling wedge, a pattern which sometimes marks the end of a downtrend. Still, some caution flags remain. Over the past month LINK has been trading downwards, though it’s gained some strength in the last week amid renewed buying interest. The key support around $17.08 remains critical, if LINK closes below that, a drop toward $16 could be triggered.

Conversely, diagnostics like the Money Flow Index (MFI) and Chaikin Money Flow (CMF) are showing signs of life, hinting at growing accumulation from larger holders. Combine this with a potentially dovish Fed decision, and Chainlink could be gearing for something special.

2. Dogecoin (DOGE)

Dogecoin enters the FOMC event with a bit of range-bound suspense. Since October 11, DOGE has been oscillating between $0.17 and $0.20, waiting for a trigger. A clean breakout above $0.21 could open the door to a move back towards $0.27, especially if risk-on sentiment returns.

Volume and whale‐level data add texture to the setup. The Wyckoff volume profile recently flipped from seller control to buyer control, suggesting strategic accumulation may be underway. DOGE may be quieting down before a move, a scenario traders should keep front of mind as the Fed’s decision could stir things.

3. Uniswap (UNI)

Uniswap offers compelling recovery stories entering the FOMC session. The token experienced a sharp drop on October 10, with the RSI falling below 30, classic oversold territory. Since then, UNI has rallied from near $6.20 toward $6.50, supported by strong volume on the breakout. Holding above $6.40 may confirm that buying interest is sustained.

For longer-term watchers, UNI’s former highs at $12.15 in August and $18.71 in December set the stage for what could become a multi-leg recovery if macro conditions cooperate. In a market where liquidity expectations hinge on the Fed, Uniswap's rebound has the potential to accelerate, particularly if altcoin capital begins rotating into DeFi infrastructure.

The Verdict

These tokens aren't just compelling because of their individual fundamentals, it's how those fundamentals intersect with the current macro picture. With markets rebounding and rate cuts looking increasingly likely, crypto stands to gain. Lower rates typically fuel risk appetite, unlock liquidity, and drive capital toward speculative plays, creating tailwinds that can supercharge momentum in well positioned altcoins.

That said, the Fed could also surprise with restraint, and even another “standard” 25-basis-point cut may be viewed as lukewarm. In such scenarios, the dollar may strengthen and risk assets could wobble. Traders and investors should therefore approach the market with discipline, track the macro context, and be prepared for either direction.

2025 has been a defining year for AI. OpenAI’s GPT-5 and Anthropic’s Claude Sonnet 4.5 have raised the bar once again, each one aiming to blend stronger reasoning, longer memory, and more autonomy into one seamless system. Both are built to handle coding, research, writing, and enterprise-scale tasks, yet their design philosophies differ sharply.

This breakdown explores how the two stack up across performance, reasoning, coding, math, efficiency, and cost, helping users and teams decide where each model truly shines.

A Quick Overview

Claude Sonnet 4.5 builds on Anthropic’s refined Claude family. It extends memory across sessions, handles million-token contexts via Amazon Bedrock and Vertex AI, and features smart context management that prevents sudden cut-offs. It can run autonomously for 30 hours on extended tasks, making it ideal for ongoing workflows.

Meanwhile, GPT-5 is OpenAI’s flagship successor to GPT-4, tuned for agentic reasoning, where the model plans, executes, and coordinates tools on its own. Its adaptive reasoning system dynamically chooses between shallow or deep “thinking” paths, letting users balance speed, cost, and depth per task. GPT-5 also offers specialized variants (Mini, Nano) for lighter workloads.

Reasoning and Analysis

Both models far exceed their 2024 counterparts, but they differ in how they reason.

GPT-5’s deep-reasoning mode significantly boosts performance in multi-step logic, scientific, and spatial tasks. It can break problems into chains, test sub-hypotheses, and self-correct mid-process. However, disabling this mode reduces accuracy sharply, it can be brilliant when “thinking deeply,” but more variable when not.

Claude Sonnet 4.5, by contrast, stays stable even without added configuration. It’s particularly strong in financial, policy, and business logic, where structure and coherence matter more than creative leaps. For enterprise Q&A or decision support, that predictability is valuable.

If you want an AI that reasons steadily, Claude takes the lead. If you need exploratory logic (i.e. complex hypothesis testing or cross-domain synthesis) GPT-5’s deeper path is unmatched.

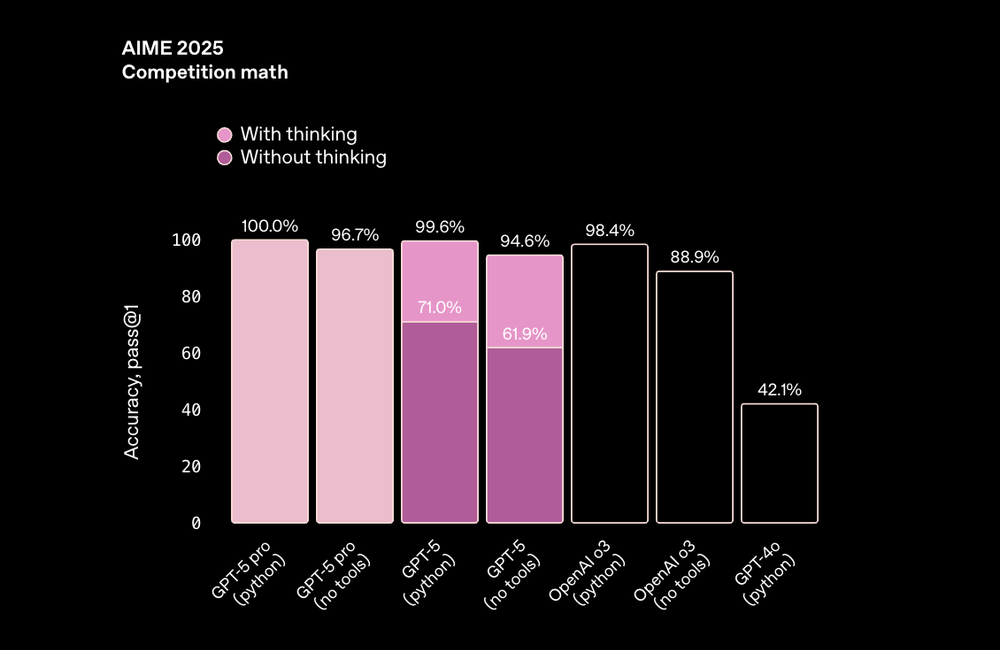

Math and Structured Problem Solving

As seen in the benchmarks provided by Anthropic, Claude Sonnet 4.5 continues its consistency streak. Whether calculating directly or using Python tools, it achieves top-tier math accuracy. This means it handles structured logic even in constrained environments.

GPT-5 also reaches near-perfect accuracy, but only when tool use and reasoning depth are active. Disable them, and results drop noticeably. It relies heavily on its reasoning pipeline to stay sharp.

Verdict:

- Claude Sonnet 4.5: dependable out-of-the-box math solver.

- GPT-5: flexible but needs tuning to perform at its best.

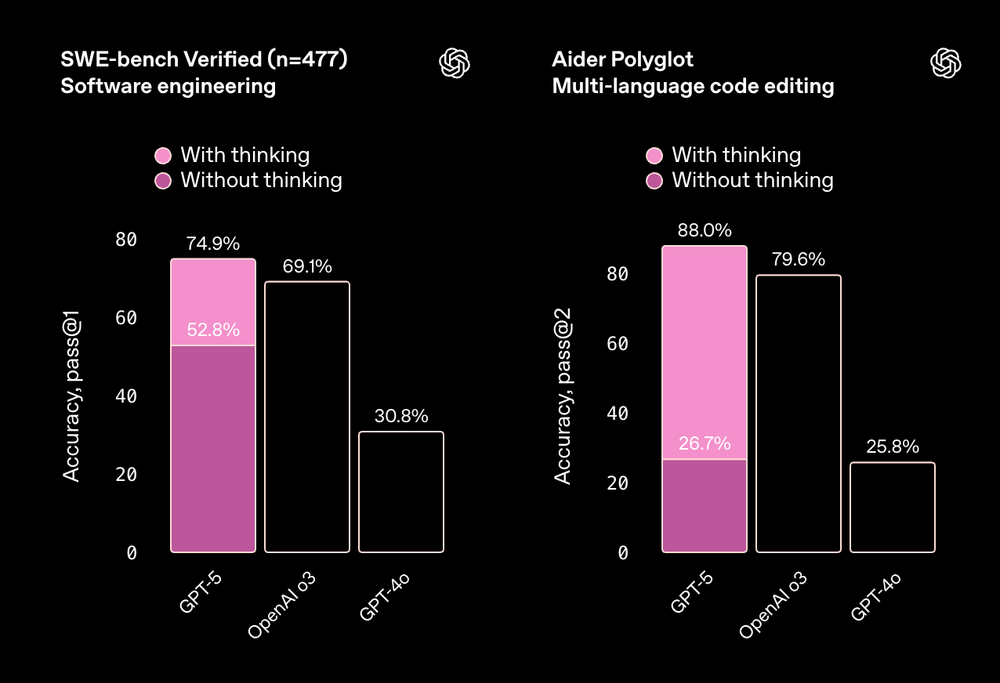

Coding and Software Engineering

When it comes to coding, the two models diverge in style.

Claude Sonnet 4.5 delivers stable performance without special tuning. In tests resembling HumanEval+ and MBPP+, it maintains high accuracy across conditions, making it dependable for production pipelines. Its strength lies in consistency, results rarely fluctuate, which is crucial for enterprise use.

By contrast, GPT-5 achieves higher peak scores when its advanced reasoning is enabled, especially in multi-language or large-project contexts. In JavaScript and Python refactoring tasks, for instance, it outperformed Sonnet when its “high-reasoning” mode was active — though baseline runs without that mode varied more.

For agentic coding, where the AI calls external tools or terminals, Sonnet 4.5 often executes with fewer dropped commands. GPT-5, on the other hand, can chain more tool calls simultaneously, making it better for complex orchestration, provided you configure it carefully.

Verdict:

- Claude Sonnet 4.5: predictable, steady engineering partner.

- GPT-5: versatile powerhouse, but performance hinges on setup.

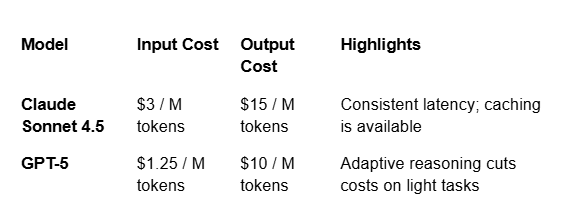

Cost and Efficiency

GPT-5 is clearly cheaper per token, particularly for large inputs. Its adaptive router also saves compute by running simple prompts on lighter paths.

Claude Sonnet 4.5 charges more but maintains predictable latency, a key factor for production environments that value reliability over marginal savings. For very large prompts, its cost rises faster than GPT-5’s, though batch discounts narrow the gap.

TL;DR: GPT-5 wins on price and scalability, whereas Claude wins on timing consistency and stability.

Pricing for Premium Plans

Beyond API access, both OpenAI and Anthropic offer premium subscriptions for individual users, which differ in features and pricing.

ChatGPT Plus, powered by GPT-5, is priced at $20 per month, giving users priority access to GPT-5, faster response times, and early access to new features and memory. OpenAI’s unified ChatGPT experience also includes file uploads, image generation, and custom GPTs.

Claude Pro, meanwhile, costs $20 per month as well and grants access to Claude Sonnet 4.5, offering faster responses, higher rate limits, and longer context windows. While it lacks built-in multimodal tools, Claude focuses on text clarity and structured reasoning, appealing to researchers, analysts, and writers seeking dependability over versatility.

TL;DR: both Plus plans are tied in price; what sets them apart, however, is their offering.

Different Strengths for Different Needs

It’s tempting to crown one “best,” but GPT-5 and Claude Sonnet 4.5 serve different priorities for different users and teams.

- Claude Sonnet 4.5: best for reliability and sustained performance. If you want consistent outputs and clear memory behavior, Claude delivers.

- GPT-5: best for depth, flexibility, and scalability. When configured properly, it surpasses rivals in creative reasoning, multimodal integration, and adaptive tool use.

Most teams may find the strongest setup is multi-model, using Claude where consistency matters most, and GPT-5 for data-intensive workflows.

Ultimately, these aren’t just chatbots anymore, they’re full-fledged digital collaborators, each with distinct personalities. Claude Sonnet 4.5 is your calm, methodical analyst. GPT-5 is your ambitious polymath. Which one you pick depends less on their individual benchmarks and more on your mission.

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

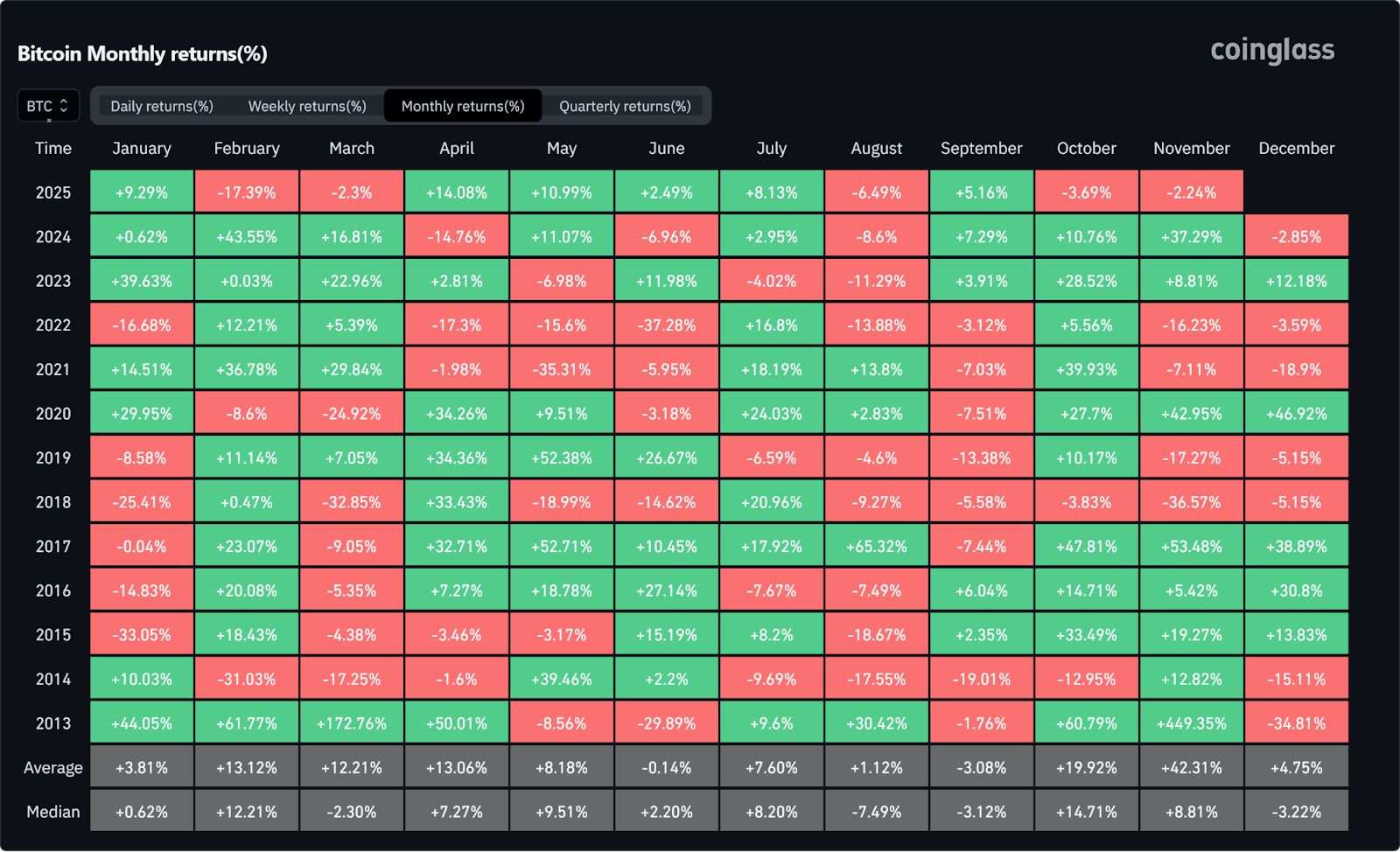

1. Seasonality & Historical Momentum Could Kick In

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

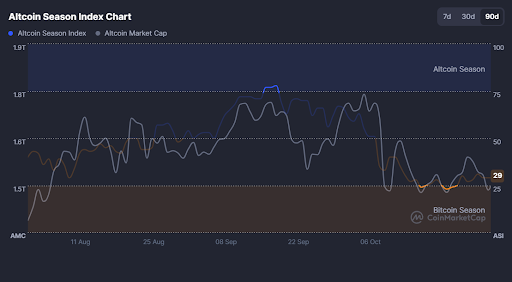

4. Altcoins at an Inflection Point

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

As digital assets become a core part of personal wealth, one uncomfortable question lingers: what will happen to your crypto when you’re gone? Unlike traditional assets that can be managed through banks or brokers, cryptocurrencies are bound entirely to whoever holds their private keys. Lose the keys, and the funds are gone. Permanently.

Crypto Vanishes All the Time

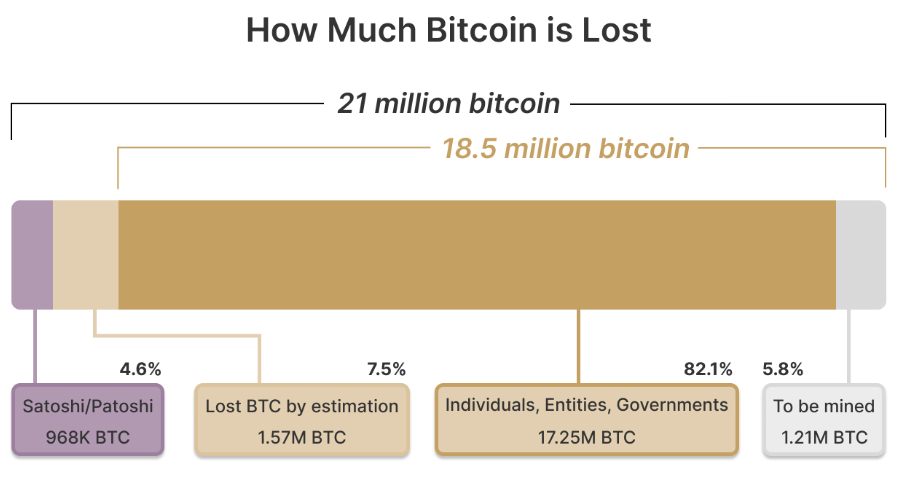

Each year, millions of dollars in Bitcoin, Ether, and other tokens vanish into the digital void when holders pass away without sharing access. It is estimated that around 1.5 million BTC (roughly 7.5% of total supply) may already be lost forever. With digital wealth now part of countless estates, preparing for the inevitable is no longer optional; it’s the responsible thing to do.

Why Planning for Crypto Inheritance Matters

In traditional finance, wealth transfer is handled through wills, trusts, and custodians. But crypto flips that model: you are the bank. Your heirs can’t simply request a password reset or call customer service. Without private keys, wallets, or access instructions, those assets are unrecoverable for all effects and purposes.

A crypto inheritance plan ensures that your digital assets, from Bitcoin and altcoins to NFTs and DeFi holdings, remain both secure and accessible to the people you choose. It bridges two crucial needs: protecting your funds today and ensuring your legacy tomorrow.

Beyond personal security, inheritance planning also reduces emotional and financial stress for your loved ones. By documenting how and where assets can be accessed, you prevent confusion and potential legal disputes.

Building the Foundation of a Crypto Inheritance Plan

Start with Legal Clarity

Consult an attorney familiar with digital assets. A properly structured will or trust should identify your crypto holdings, list beneficiaries, and outline how they can access those funds. Many jurisdictions still lack explicit laws for digital assets, so expert guidance helps ensure compliance and enforceability.

Secure Your Keys… But Don’t Overshare

The biggest challenge in crypto inheritance is private key management. If you die with your keys, your crypto dies with you. However, leaving keys in plain text within a will or document is just as risky. Instead, consider approaches like:

- Multisignature wallets, which require multiple approvals to move funds.

- Shamir’s Secret Sharing, which means splitting your seed phrase into parts distributed among trusted people.

- Encrypted backups or sealed letters stored in secure, offline locations.

Document recovery procedures in plain language so your heirs can follow them even without technical knowledge.

Choose the Right Executor

A traditional executor may not understand how to navigate crypto. You can appoint a tech-literate executor or designate a digital asset custodian to handle that portion of your estate. This ensures smooth execution and reduces the risk of errors or loss.

In a market driven by innovation and constant change, a well-structured inheritance plan offers something rare in crypto, certainty.

New Tools for a Digital Age

The rise of blockchain-based “death protocols” and smart contract automation adds a new layer of possibilities. Some platforms allow transfers to trigger automatically after certain conditions are met (for example, a verifiable death certificate or extended inactivity).

Ethereum and similar chains already support programmable inheritance systems, but these should complement, not replace, legal documents. Technology can help enforce your intentions, but law remains the foundation of inheritance.

Some investors even use “dead man’s switches”, automated systems that transfer funds if the owner doesn’t log in for a set period. While clever, it might be best to pair them with legal documents to prevent accidental activations.

Protecting Privacy While Planning Ahead

While planning for the future, it’s crucial to maintain security in the present. Avoid including wallet addresses, private keys, or passwords in public wills, which become part of the legal record. Instead, store such details in encrypted files or sealed envelopes accessible only to specific individuals.

Tools like decentralized identifiers (DIDs) and verifiable credentials can also help manage long-term identity and access rights. These systems allow you to define who can access what, and when, without intermediaries.

Custodial vs. Non-Custodial: Finding the Balance

When structuring inheritance, knowing whether your assets are held in custodial or non-custodial wallets makes all the difference.

Custodial services (like major exchanges) manage private keys on your behalf, which simplifies recovery if your heirs can provide proper documentation. However, it introduces third-party risk. Accounts can be frozen, hacked, or shut down.

Non-custodial wallets, on the other hand, offer maximum control and privacy but demand greater responsibility. If your heirs lose the seed phrase, there’s no backup plan. There’s also the possibility of taking a hybrid approach: keeping long-term holdings in non-custodial storage for security, while using reputable custodians for smaller, more accessible amounts.

Keep It Up to Date

A crypto inheritance plan is not a “set it and forget it” document. Prices change, portfolios evolve, and wallet technologies become obsolete very often. It may be wise to revisit your plan regularly, especially after major life events such as marriage, divorce, or the birth of a child.

It’s also worth keeping track of regulatory updates in your jurisdiction. Laws surrounding digital assets and inheritance are rapidly evolving, and what’s compliant today may not be tomorrow.

Common Inheritance Pitfalls

Even the best intentions can go wrong. Here are the most frequent mistakes to avoid:

- Including seed phrases directly in your will. As we mentioned before, this makes them public and vulnerable.

- Neglecting to educate heirs. Without guidance, even secure plans can fail.

- Relying solely on exchanges. Centralized platforms can fail or freeze funds.

Planning isn’t just about distributing wealth; it’s about ensuring continuity. A clear inheritance strategy preserves your crypto’s value and prevents it from becoming part of the estimated $100 billion in lost digital assets worldwide.

Protecting More Than Just Coins

Preparing a crypto inheritance plan isn’t merely about money; it’s about legacy. For all the talk about decentralization and autonomy, responsibility and forward-thinking remain at the heart of crypto ownership. By taking the time to plan ahead, you safeguard not only your wealth but also your family’s peace of mind.

After a volatile October that saw one of the sharpest two-day liquidations of the year, the crypto market is trying to regain its footing, but conviction remains divided. Bitcoin has stabilized near key support levels, while altcoins fight against selling pressure. With macro, policy, and on-chain factors all in play, the debate between the bull and bear camps is as alive as ever. Let’s unpack the forces shaping both sides of the ledger.

The Bear Case

When Good News Don’t Move Prices

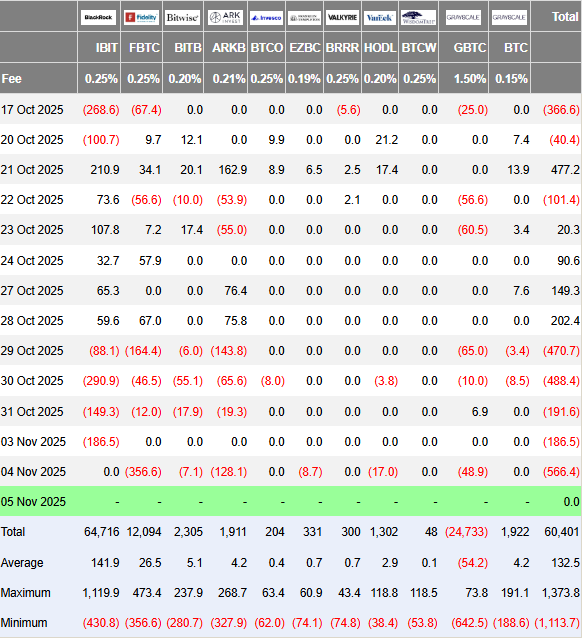

Despite encouraging ETF data and easing rate expectations, crypto failed to rally in late October, a classic warning sign of risk fatigue. According to Farside Investors, U.S. spot Bitcoin ETFs saw outflows of $470 million, $488 million, and $191 million between October 29 and 31, signaling that short-term traders were taking profits or stepping aside after “Uptober” fizzled out.

The AI Narrative

Macro sentiment still casts a long shadow. The tech-heavy equity rally, driven by AI infrastructure and chip stocks, has stirred debate about overvaluation. Nvidia’s brief breach of a $5 trillion valuation in late October triggered flashbacks of the dot-com era. If AI equities begin to deflate, crypto could feel the wealth effect unwind, as liquidity shifts from speculative assets to safer havens.

The 10/10 Crash Aftershock

The October 10 downturn marked one of the largest single-day liquidations in recent memory. Analysts note that this event left traders hunting for “dead entities” and potential hidden losses, injecting caution across the market. Even with recovery underway, scars from that drop remain fresh.

Post-Halving Cycle Timing

Bitcoin’s halving on April 20, 2024 (block 840,000) reset expectations, but it also reignited the age-old question: where are we in the cycle? Historically, the strongest rallies have occurred before or shortly after the halving, not a full year later. Some analysts now argue that the current consolidation could represent a late-cycle phase rather than the start of a new one.

Dormant Wallets Awakening

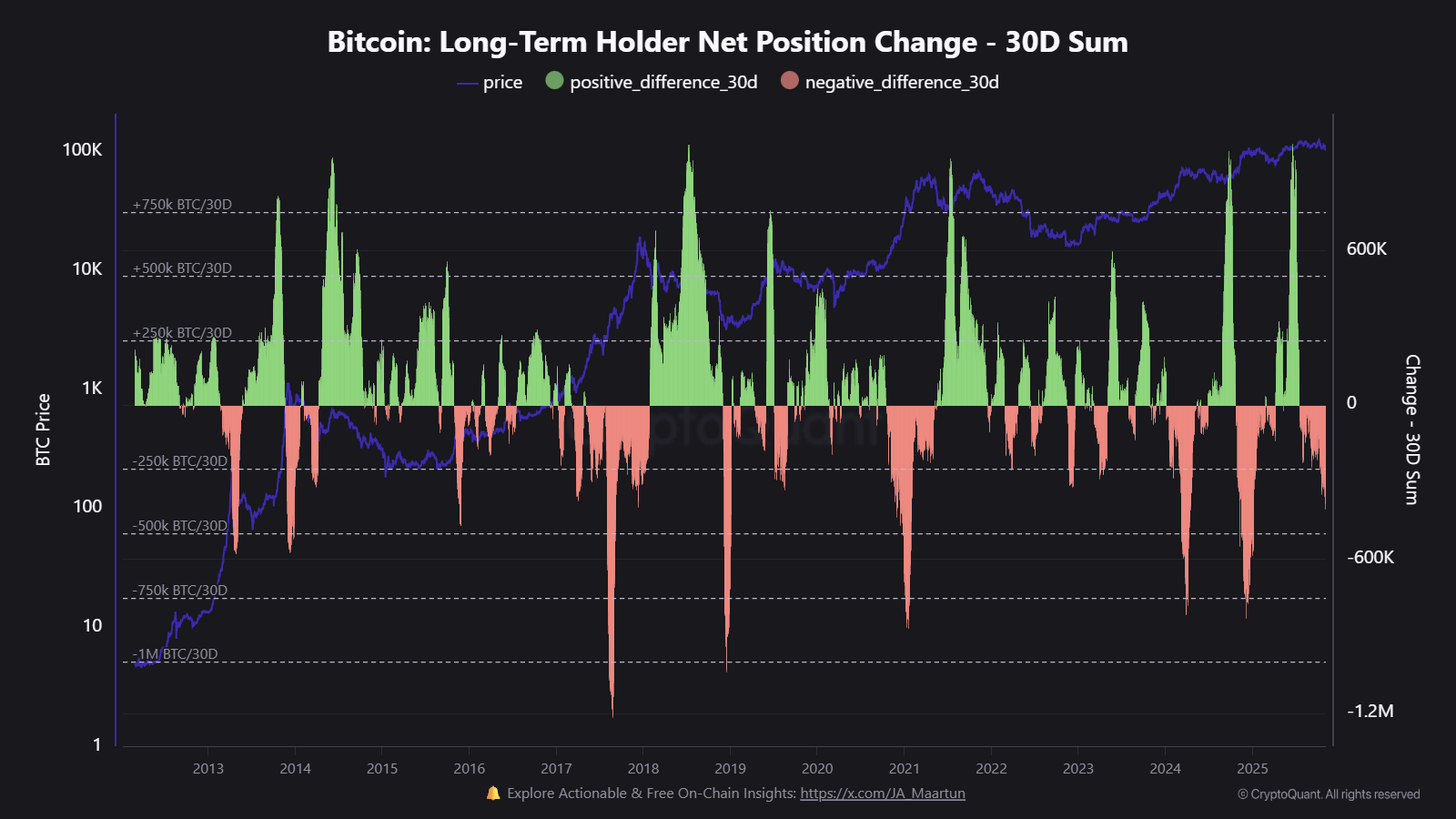

On-chain data from CryptoQuant shows that long-term holders have increased net distribution since mid-October, with tens of thousands of BTC re-entering circulation. Several Satoshi-era wallets have also moved funds, not necessarily bearish in isolation, but enough to add pressure and short-term supply.

The Bull Case

No Signs of Euphoria

Market positioning remains far from overheated. The Crypto Fear & Greed Index currently sits in the 20s, and has been recently hovering between “Fear” and “Neutral.” That’s a far cry from the exuberant 80s to 90s readings that often precede blow-off tops. In practical terms, this suggests there’s still room for sentiment to improve before the market becomes dangerously crowded.

Liquidity Is Turning

Central banks are easing. The European Central Bank has already paused, the Bank of England has begun cutting, and the U.S. Federal Reserve is expected to follow suit with at least one more rate cut by year-end. According to the CME FedWatch Tool, the odds of a 0.25% cut currently stand above 70%. Historically, easing cycles have correlated strongly with renewed crypto uptrends, as lower yields push investors back into risk assets.

Institutional Adoption Keeps Compounding

Spot ETFs remain the biggest driver of credibility and inflows this year. Despite short-term outflows, global crypto investment products reached $921 million as recently as last week. That steady institutional presence gives crypto markets deeper liquidity and a stronger foundation than in previous cycles, where retail speculation dominated.

The Seasonal Edge

Seasonality adds another bullish data point. Since 2013, Q4 has consistently been Bitcoin’s strongest quarter on average. With November historically delivering above-average performance, many traders see the current consolidation not as a ceiling, but as a potential setup, particularly if macro data softens and ETF inflows resume.

Improving Global Sentiment

Finally, the U.S.–China trade thaw is a quiet but important catalyst. China has agreed to pause 24% tariffs on U.S. goods, marking the most significant de-escalation yet. For global risk assets, that’s a relief valve, potentially restoring confidence in emerging markets and crypto alike.

Final Verdict

Crypto’s tug-of-war between optimism and caution is far from over. The bull camp points to liquidity, policy progress, and institutional growth as evidence of a maturing ecosystem. The bears, on the other hand, warn that cycle timing, macro fragility, and old-wallet selling could cap any short-term rally.

Currently, the most realistic view lies somewhere in between these two extremes. After October's flash crash sent shockwaves through the market, a period of recalibration has taken hold. Whenever the next significant high arrives, the current environment may be best described not as peak fear or euphoria, but as consolidation.

Something's shifting in crypto, and it's not just the charts. After weeks of sideways action and uncertainty, major developments out of the United States could be the catalyst that many were hoping for.

The timing couldn't be more interesting. Retail appetite is quietly building, whales are accumulating aggressively (especially in XRP), and macro conditions are starting to tilt back in crypto's favor. Individually, each of these catalysts matters. Combined, they set the stage for the kind of conditions that have historically preceded major shifts. Here's what you need to know, and why the next few weeks might be more important than most people realize.

1. U.S. Tariff Dividend

One of the biggest stories to watch is the “tariff dividend” President Donald Trump announced, a direct payment that could reach around $2,000 per person. The idea is that funds collected from higher import tariffs could be redistributed to citizens, effectively a form of economic stimulus. This could inject billions into consumer wallets, creating new liquidity across markets.

If history is any guide, such payouts can ripple into crypto. During the 2020 stimulus-era, Bitcoin saw a sharp uptick as retail investors channeled part of their checks into digital assets. The same pattern could repeat if a new wave of disposable income reaches American households, especially with crypto platforms now far more accessible than they were five years ago.

2. U.S. Government Shutdown Ending

Another factor lifting sentiment is the prospect of the U.S. government reopening. Political gridlock has weighed on markets, but signs of resolution have already sparked rallies across equities and digital assets alike. The relief comes as investors regain confidence that key economic functions will resume smoothly.

The last comparable event came in 2019, when a record-long U.S. shutdown ended after 35 days. Shortly afterward, Bitcoin began a sustained recovery, climbing from roughly $3,500 in late January 2019 to over $13,000 by mid-year. While correlation doesn’t imply causation, renewed fiscal clarity and market confidence often coincide with higher risk-appetite, the environment where crypto tends to thrive.

3. Pending ETF Approvals: Keep an Eye on XRP

Finally, the next big trigger could come from the regulatory side. Several new spot crypto ETF applications are nearing decision windows, with assets like XRP and Solana drawing heavy attention. The success of Bitcoin and Ethereum ETFs has already shown how much institutional demand can reshape liquidity and credibility in the space.

In particular, XRP could be one of the biggest winners. According to recent on-chain data, whales have accumulated more than $560 million worth of XRP in the past few weeks, a sign of growing confidence ahead of potential ETF approval. Broader adoption through regulated investment vehicles could finally unlock fresh capital inflows for alternative crypto assets beyond Bitcoin and Ethereum.

Bottom Line

Nothing is set in stone in crypto. But when liquidity, regulatory progress, and accumulation all start pointing in the same direction? That's when things get very interesting.

We're heading into the final stretch of 2025 with more aligned positive factors than we've seen in months. So, for anyone involved in crypto, whether you're trading daily or holding, now's the time to stay plugged in.