Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

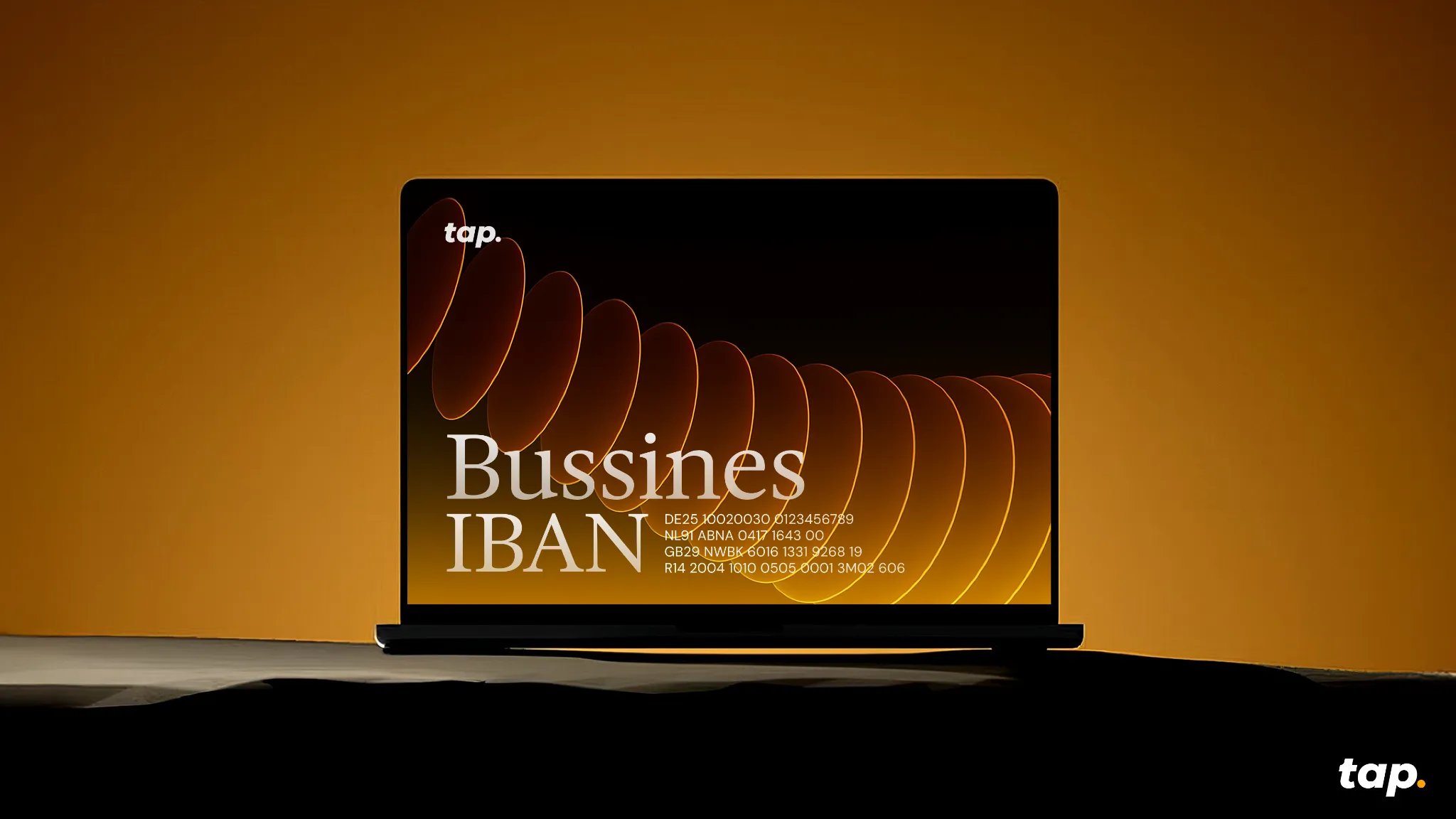

Managing payments across borders remains one of the biggest operational challenges for expanding businesses. While digital transformation has touched nearly every aspect of commerce, international banking is currently lagging behind with separate systems for crypto and traditional currency transactions, creating unnecessary complexity.

Tap solves this problem by offering each business a multi-currency account with a dedicated IBAN that functions as a bridge between these two financial worlds. For businesses handling both crypto and fiat currencies, this means one unified system rather than juggling multiple accounts and conversion processes. This isn't just convenient - it directly impacts your bottom line by reducing transaction fees, speeding up settlements, and simplifying reconciliation.

If you're handling international payments or considering crypto adoption, this could significantly streamline your financial operations. Here's what you need to know.

What is a business IBAN?

An IBAN (International Bank Account Number) serves as your business's financial passport - a standardised identifier recognised across 78+ countries. Unlike traditional account numbers, a Business IBAN follows a structured format that includes country codes, bank identifiers, and your unique account number.

What sets Tap's approach apart is the integration of this established banking standard with crypto functionality. Instead of operating in parallel financial universes, your transactions (whether in euros, dollars, or Bitcoin) flow through a single identifiable channel.

For finance teams, this means the end of reconciliation nightmares. For your customers and partners, it means one consistent payment destination regardless of their preferred currency.

How Business IBANs Work

The mechanics behind modern business transactions

A Business IBAN functions as the digital coordinates for your company's financial location in the global banking ecosystem. When properly implemented, it creates a frictionless path for money to flow into and out of your business regardless of currency type or originating country.

Sending and receiving payments

When receiving payments, your Business IBAN acts as a universal identifier that works across different payment systems. Clients simply enter your IBAN (and sometimes BIC code) into their banking platform, eliminating the confusion of different account number formats across countries.

For outgoing payments, the process works in reverse. You provide the recipient's IBAN, specify the amount, and Tap's platform handles the routing complexities behind the scenes. This standardisation prevents the common errors that lead to payment delays and rejection fees.

What separates Tap's system from conventional banking is the integration layer that works with both crypto and traditional currencies. When a client pays in Bitcoin, for example, you can choose to receive it as cryptocurrency or have it automatically converted to your preferred fiat currency before it reaches your account.

Banking networks demystified

Business IBANs interact with several key payment networks:

SEPA (Single Euro Payments Area): Covering 36 European countries, SEPA processes euro-denominated transfers typically within one business day at low fixed costs. Your Business IBAN automatically routes euro payments through this network without requiring a separate setup.

SWIFT (Society for Worldwide Interbank Financial Telecommunication): The backbone of international banking, SWIFT connects over 11,000 financial institutions worldwide.

Real-world transaction example

Consider a UK-based e-commerce business receiving payment from a German customer:

- The customer initiates a €5,000 payment to the merchant's business IBAN

- The transaction enters the SEPA network and arrives in the merchant's Tap account within hours

- The merchant can either keep the funds in euros or convert to GBP at their preferred timing

- If choosing to convert, Tap executes the exchange at market rates with minimal spread

- The funds become available for business operations, supplier payments, or withdrawal

This same process that once required multiple accounts, banking relationships, and days of processing now happens automatically through a single business IBAN. For businesses managing dozens or hundreds of such transactions monthly, the efficiency gains and cost savings compound significantly.

The ability to handle these complex financial pathways through one unified system represents the core value proposition of modern business IBANs - simplicity on the surface, sophisticated routing underneath.

Cross-border advantages that impact your bottom line

The practical benefits of a business IBAN become immediately apparent in cross-border transactions:

- Reduced rejection rates: correctly formatted IBANs virtually eliminate payment failures due to incorrect account details

- Faster settlement times: direct routing through the SEPA network for European transactions

- Lower transaction costs: fewer intermediaries means fewer fees eating into your margins

- Simplified compliance: clearer transaction trails for more straightforward reporting

Bridging crypto and traditional finance

The crypto market now represents a $2 trillion opportunity that many businesses struggle to tap into due to technical and operational barriers. A business account with Tap eliminates these obstacles by providing:

- Seamless conversion between crypto and fiat currencies

- Consolidated financial reporting across all currency types

- Regulatory compliance built into the platform

- Reduced exposure to crypto volatility through instant conversion options

For businesses cautiously exploring crypto acceptance, this hybrid approach offers a low-risk entry point without requiring major infrastructure changes.

Implementation without disruption

Setting up a business account through Tap requires minimal operational changes:

- Fill in the contact form to initiate a callback

- Complete the business account set-up and verification process

- Receive your unique account with IBAN

- Update payment details with clients and suppliers

- Integrate with your existing accounting systems

The entire process typically takes less than 48 hours, with Tap's team handling the technical heavy lifting.

Is a Tap business account right for your growth strategy?

It's worth considering a business account if your company:

- Operates in multiple countries or currencies

- Needs to reduce payment processing costs

- Wants to accept crypto payments without complexity

- Are looking to streamline financial operations

As payment landscapes continue evolving, businesses that implement flexible, future-proof solutions gain a significant competitive advantage in customer experience and operational efficiency.

Explore how a business IBAN could fit into your financial infrastructure by visiting Tap's business solutions page, from where a dedicated account manager can discuss potential savings based on your specific transaction patterns.

The business world won't wait for outdated payment systems to catch up. The question isn't whether you need more efficient payment solutions - it's how quickly you can implement them.

Let’s make your cross-border payments simple. Schedule a chat with our expert team and explore how Tap can work for your business.

Le slippage peut faire toute la différence dans vos résultats de trading. Il représente l’écart entre le prix que vous pensiez payer et le prix réel au moment de l’exécution d’un ordre. Voici tout ce que vous devez savoir pour comprendre ce phénomène, gérer le risque et l’éviter autant que possible.

C’est quoi le slippage en crypto ?

Le slippage se produit lorsqu’un ordre d’achat ou de vente est exécuté à un prix différent de celui initialement affiché, en raison de mouvements du marché entre le moment où l’ordre est passé et celui où il est exécuté.

Pourquoi le slippage se produit-il ?

Deux grands facteurs sont à l’origine du slippage : la volatilité et la liquidité.

- Volatilité : Les marchés crypto sont connus pour leurs mouvements de prix rapides. Cela signifie que le prix peut changer entre le moment où vous validez un ordre et son exécution.

- Liquidité : Si une crypto est peu échangée, l’écart entre l’offre et la demande est plus large, ce qui peut entraîner un prix d’exécution bien moins avantageux. Cela arrive souvent sur les altcoins peu liquides, et encore plus fréquemment sur les DEX (échanges décentralisés).

Slippage positif vs. slippage négatif

- Slippage positif : L’ordre est exécuté à un prix plus avantageux que prévu. Par exemple, vous achetez moins cher ou vous vendez plus cher.

- Slippage négatif : L’ordre est exécuté à un prix moins favorable. Cela peut sérieusement impacter votre rentabilité si cela se répète souvent.

Peut-on éviter le slippage ?

On ne peut pas l’éliminer totalement, mais voici quelques techniques pour le limiter :

1. Utiliser des ordres limités

Contrairement aux ordres au marché, les ordres limités vous permettent de fixer un prix maximum (ou minimum) pour l’achat ou la vente. L’ordre ne sera exécuté que si ce prix est atteint.

2. Définir un taux de slippage

Certains échanges permettent de fixer une tolérance de slippage (ex. 0,1 % à 5 %). Cela empêche l’ordre de passer si le prix varie trop. Attention toutefois à ne pas fixer un seuil trop bas, sinon l’ordre pourrait ne jamais être exécuté.

3. Comprendre la volatilité d’un token

Plus vous en savez, mieux vous tradez. Renseignez-vous sur les mouvements passés du token, et sur la volatilité de la plateforme utilisée. Cela vous aidera à prendre des décisions plus éclairées.

Comment calculer le slippage ?

Le slippage peut être exprimé en valeur absolue (en euros ou dollars) ou en pourcentage.

- Montant du slippage : Prix réel - Prix attendu

- Pourcentage : (Montant du slippage ÷ Différence entre prix attendu et prix limite) × 100

Exemple : Vous voulez acheter du Bitcoin à 50 000 $, avec un ordre limite à 50 500 $. Finalement, l’ordre est exécuté à 50 250 $.

- Slippage = 250 $

- Pourcentage = (250 ÷ 500) × 100 = 50 %

Dans cet exemple, votre slippage est de 250 $ ou 50 %.

Vous voulez en savoir plus sur les crypto-monnaies et le trading ? Consultez tous nos autres articles éducatifs ici.

.png)

Que vous soyez fidèle à votre écran d’ordinateur ou adepte du smartphone, vous vous êtes sûrement déjà demandé comment insérer le symbole de la livre sterling (£) dans un document, un email ou un message. Ne cherchez plus — ce guide pratique vous montre comment taper rapidement le symbole £ sur Mac, PC ou mobile.

💡 Et si vous devez envoyer des livres sterling à l’étranger, Tap vous permet de transférer des fonds facilement avec des frais réduits et un excellent taux de change. Envoyez, dépensez ou échangez des GBP ou EUR depuis l’app, partout dans le monde — et gratuitement entre utilisateurs Tap.

D’où vient le symbole de la livre sterling ?

La livre sterling (GBP), symbolisée par £, possède une histoire riche de plus de 1 200 ans. À l’origine, elle représentait un poids d’argent dans l’Angleterre anglo-saxonne. Elle est devenue monnaie officielle en 1694 sous le règne de Guillaume III.

Avec l’expansion de l’Empire britannique, la livre a gagné une importance mondiale. Même après des événements majeurs comme les guerres, la dévaluation de 1967 ou encore le Brexit, elle reste une devise clé de l’économie mondiale.

Selon la Banque d’Angleterre, le symbole £ vient de la lettre L, initiale du mot latin libra, qui signifiait « une livre de monnaie ». L’ajout de la barre horizontale (le trait du £) remonte au moins à 1660, sur un ancien chèque conservé par la banque.

📌 En anglais, le symbole £ est toujours placé avant le montant : par exemple, £10 signifie dix livres. Petite anecdote : en 1970, un billet de £20 représentant William Shakespeare a été émis — une tradition est née, celle d’honorer des figures emblématiques sur les billets et pièces.

Comment insérer le symbole £ dans un document ?

Maintenant que vous connaissez son origine, voyons comment taper le symbole £ selon l’appareil que vous utilisez.

Sur Mac

Le raccourci le plus rapide est :Option (ou Alt sur certains claviers) + 3

Cette combinaison fonctionne sur les claviers européens. Si vous avez un clavier américain, vous devrez peut-être ajuster votre configuration régionale pour activer les symboles monétaires européens.

Sur Windows

Sur la plupart des claviers Windows, utilisez simplement :Alt + 0163 (en utilisant le pavé numérique)

Ou, si vous avez un clavier britannique :Maj + 3 vous donnera directement le symbole £, souvent visible juste au-dessus du chiffre.

💡 Vous pouvez aussi copier-coller ce symbole directement ici : £

Sur smartphone (iOS ou Android)

Sur votre clavier mobile, appuyez sur le bouton ?123 ou symbole, puis cherchez le £ dans les options.

Si vous ne le voyez pas immédiatement :

- Maintenez le doigt appuyé sur le symbole $ (dollar)

- D’autres symboles monétaires apparaîtront, dont £

Sans clavier ? Aucun souci

Si vous utilisez Microsoft Word ou Google Docs, vous pouvez insérer le symbole sans taper quoi que ce soit.

Voici comment faire :

- Dans Word, cliquez sur Insertion > Symbole > recherchez £

- Dans Google Docs, allez dans Insertion > Caractères spéciaux > puis sélectionnez la catégorie Monnaie

Cliquez sur le symbole £ pour l’insérer dans votre texte.

Et voilà !

Vous savez désormais comment insérer le symbole £ facilement, que vous soyez sur ordinateur ou sur téléphone. Que ce soit pour un mail professionnel, une facture ou un post sur les réseaux, vous êtes prêt·e à taper £ en toute simplicité

.

Vous connaissez peut-être déjà l’achat et la vente de cryptomonnaies, mais avez-vous déjà entendu parler des airdrops ? Ces distributions gratuites de tokens sont en réalité des stratégies marketing visant à faire connaître un projet blockchain. Elles permettent de toucher une large audience et de créer de l’engagement. Explorons ensemble comment fonctionnent les airdrops et ce qu’ils peuvent réellement apporter.

Qu’est-ce qu’un airdrop crypto ?

Un airdrop crypto, c’est lorsqu’un projet distribue gratuitement ses tokens natifs à des utilisateurs — souvent pour attirer l’attention, élargir sa communauté ou encourager l’adoption. En clair : de la crypto gratuite, parfois en échange d’une petite action (suivre un compte, s’inscrire à une newsletter), parfois sans rien faire du tout.

Les tokens sont transférés dans les portefeuilles des utilisateurs existants ou potentiels. Cette technique a explosé lors du boom des ICOs en 2017, et reste encore largement utilisée. Même si ces tokens sont donnés gratuitement, leur valeur peut augmenter avec le temps — ce qui les rend parfois très intéressants pour les détenteurs.

C’est aussi une méthode pour augmenter le nombre de portefeuilles actifs (un bon indicateur pour les nouveaux projets) et favoriser la décentralisation en élargissant la détention des tokens.

Comment fonctionne un airdrop crypto ?

Les airdrops sont souvent planifiés dans la feuille de route d’un projet et se déclenchent après avoir atteint certains objectifs. Les modalités varient, mais en général, de petites quantités de tokens (souvent sur Ethereum ou une autre blockchain compatible avec les smart contracts) sont envoyées à plusieurs portefeuilles.

Certains airdrops sont entièrement gratuits, d’autres demandent de remplir quelques conditions : s’abonner à un canal Telegram, relayer un post sur X, ou simplement détenir un certain nombre de tokens.

Un airdrop bien pensé génère souvent du bouche-à-oreille autour du projet avant même sa cotation sur un exchange.

Quelle est la différence entre un ICO et un airdrop ?

Même s’ils sont tous deux liés au lancement de nouveaux projets crypto, la différence est claire :

- Un ICO (Initial Coin Offering) demande aux participants d’acheter des tokens, généralement pour lever des fonds.

- Un airdrop, lui, consiste à distribuer gratuitement des tokens, sans engagement financier.

Les ICO sont donc des moyens de financement, tandis que les airdrops sont des outils marketing.

Quels sont les différents types d’airdrops ?

Il existe plusieurs formes d’airdrops. Voici les plus courants :

Airdrops exclusifs

Réservés aux utilisateurs précoces ou aux membres actifs de la communauté, ces airdrops récompensent la fidélité. Exemple célèbre : Uniswap, qui a distribué 400 UNI à chaque portefeuille ayant interagi avec la plateforme avant une certaine date. Ces tokens de gouvernance donnaient un droit de vote sur les décisions du projet.

Airdrops “bounty”

Ces airdrops exigent une participation active : suivre des comptes, partager des contenus, inviter des amis, etc. Le projet peut demander une preuve d’engagement avant de distribuer les tokens.

Airdrops pour détenteurs (holders)

Ici, seuls les portefeuilles détenant déjà des tokens du projet sont récompensés. Le projet effectue une capture d’écran (snapshot) des soldes à un moment donné, et distribue des tokens aux portefeuilles éligibles.

Certains projets utilisent aussi des airdrops pour attirer des utilisateurs d’autres blockchains. En 2016, par exemple, Stellar (XLM) a distribué 3 milliards de XLM aux détenteurs de Bitcoin, dans l’idée d’élargir sa base d’utilisateurs.

Les risques liés aux airdrops

Comme souvent dans l’univers crypto, tout n’est pas toujours rose. Les airdrops attirent aussi des acteurs malveillants.

Exemples de scams courants :

- Vous recevez des tokens inconnus dans votre portefeuille. En les bougeant, votre portefeuille est vidé.

- Un faux projet vous incite à connecter votre wallet à une plateforme frauduleuse. Résultat : vos données privées sont récupérées.

⚠️ Un airdrop légitime ne vous demandera jamais de payer quoi que ce soit, ni de fournir votre seed phrase ou clé privée. Restez toujours vigilant et faites vos propres recherches (DYOR).

Autre point à surveiller :

Un airdrop massif peut fausser la perception de la popularité d’un projet. Si un token est envoyé à des milliers de wallets mais n’est quasiment jamais échangé, attention au miroir aux alouettes. Assurez-vous que le volume de trading réel correspond au nombre d’utilisateurs actifs.

Let's Talk About Getting Your Crypto to Work While You Sleep

Remember when your grandparents bragged about their 2% savings account? Those days feel like ancient history now that crypto APY percentages are floating around that would make a traditional banker faint. But hold up, before you start dreaming about retiring next month on those sweet, sweet yields, let's dive into what APY actually means and why some of these numbers look like lottery tickets.

What the Is APY, Anyway?

Think of APY as compound interest on steroids. While your bank's savings account sits there earning dust, APY measures how much your money can actually grow in a year when interest keeps building on top of interest. The faucet of passive income is now open.

Here's a reality check: Park $1,000 in your bank at 5% simple interest, and you'll have a whopping $1,050 after a year. Yawn, boring… But that same money with 5% APY compounded monthly? You're looking at $1,051.16.

"Big deal, that's only a dollar!" you might say. But here's where it gets interesting. Over time, that compounding effect turns into a money snowball rolling down a mountain. The difference between simple interest and compound interest isn't just pennies; it's the difference between walking and taking a rocket ship.

APY vs. APR: The Sibling Rivalry You Need to Understand

Okay, confession time…even seasoned crypto folks mix these up. Here's your cheat sheet:

APY (Annual Percentage Yield): What you earn when you lend out your crypto. The higher, the better for your wallet.

APR (Annual Percentage Rate): What you pay when you borrow crypto. Lower is your friend here.

Think of it this way: APY is the cool cousin who brings you money, while APR is the one who always asks to borrow twenty bucks.

For a more detailed comparison, click here.

Where Does APY Show Up in Crypto?

- Crypto "Savings Accounts"

Some platforms let you deposit your tokens and watch them multiply. It's like putting your crypto to work at a job that actually pays decent wages. Your coins get lent out to traders who need them, and you get a cut of the action.

- Staking: Become a Network Validator

With Proof-of-Stake blockchains like Ethereum or Cardano, you can "stake" your tokens to help secure the network. Think of it as being a digital security guard who gets paid in crypto. The network stays safe, and you earn rewards. Win-win.

- Yield Farming: The Wild West of DeFi

This is where things get interesting, and a bit crazy. You provide liquidity to decentralized exchanges, and in return, you earn trading fees plus shiny new governance tokens. Early yield farmers sometimes see APYs that look like phone numbers, but don't get too excited; those rates have a habit of crashing back to earth.

- Lending Protocols: Become the Bank

Platforms like Aave and Compound let you play banker. You lend your tokens, borrowers pay interest, and you collect the proceeds. APY goes up when everyone wants to borrow your particular flavor of crypto, and down when the demand cools off.

Why Are Crypto APYs So High?

While your bank offers you a measly 0.5%, crypto platforms are throwing around eye-watering numbers like 10%, 50%, or even 1,000%+. Here's why:

Crypto traders will pay premium rates to short a token or execute complex arbitrage strategies. Supply and demand at its finest.

Hype for new projects also plays a role. Fresh projects often throw ridiculous APYs at users to attract liquidity. It's like a grand opening sale, but with more zeros.

Risk gets factored in. Let's be real, crypto can get risky at times. Higher returns compensate for the white-knuckle ride.

Finally, token Incentives can play a role too. Many of those eye-popping APYs come partially from project tokens that could moon... or crater. It's the crypto Russian roulette.

The Math Behind the Magic

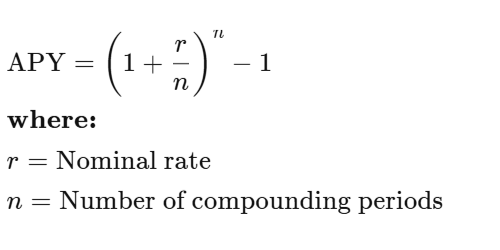

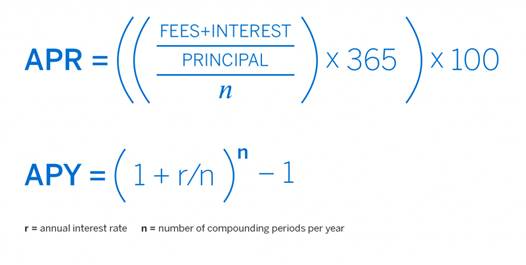

Don't worry, we're not about to turn this into a calculus nightmare. The APY formula is actually pretty straightforward:

Example: 10% interest compounded monthly gives you about 10.47% APY. Compound it daily? You're looking at 10.52%. In crypto, some protocols compound every block, which is like compounding every few seconds. Your calculator might start smoking.

The Fine Print

Before you quit your day job and become a full-time yield farmer, let's talk about the risks that nobody likes to mention at crypto parties. First up is volatility. Sure, your APY might be 20%, but if your token's price drops 50%, you're still in the red. Math is cruel like that. Then there's impermanent loss, which sounds harmless but can eat into your gains faster than you can say "automated market maker" when you're providing liquidity and token prices start dancing around.

Don't forget about smart contract risk, either. DeFi protocols are basically computer programs holding billions of dollars, and if they break, funds can disappear into the digital ether without so much as a goodbye note. Platform risk is equally sobering. Remember Celsius? FTX? Sometimes the platforms themselves go belly-up, taking user funds with them like the Titanic.

Last but not least, there’s APY whiplash. That jaw-dropping 100% APY you bookmarked yesterday? It might be 15% today because crypto moves fast. Rates fluctuate based on demand, new competition, token economics, and sometimes just because the crypto gods felt like shaking things up.

What's a "Good" APY?

- Conservative. Sticking to blue-chip assets and reputable platforms for 3-8% APY. For the faint of heart.

- Moderate. Staking some altcoins or providing liquidity for 10-20% APY. There’s some excitement, but not heart-attack levels.

- High (YOLO). Chasing new DeFi projects for 50-100%+ APY. It’s worth keeping in mind there’s a non-zero chance your tokens might become expensive digital art.

Remember, if an APY looks too good to be true, it's probably attached to risks that would make a hedge fund manager nervous.

Crystal Ball Time: The Future of APY in Crypto

Here's where things get interesting. As crypto grows up, APYs are starting to act less like lottery tickets and more like actual financial products. Big institutions are getting into staking, regulators are paying attention, and the wild west is slowly becoming a proper town with actual roads.

It’s likely crypto will keep offering better yields than traditional finance. It's just that the 10,000% APY days are likely becoming a fond memory.

The Bottom Line

APY in crypto is the same mathematical concept your finance professor taught you, just dressed up in digital clothing and offering significantly better rates. Whether you're staking, lending, or yield farming, understanding APY helps you separate the wheat from the chaff and the legitimate opportunities from dubious schemes.

APY isn't a cheat code to infinite money. It's a tool that, when used wisely, can help your crypto actually work for you instead of just sitting in your wallet looking pretty. But like everything in crypto, it comes with risks that deserve respect and careful consideration.

It’s worth remembering the best APY in the world is worthless if the underlying project disappears into the digital sunset. Choose wisely, diversify smartly, and may your compounds be ever in your favor.

Picture this: You're scrolling through DeFi platforms, and suddenly you see two different projects. One screams "12% APR!" while another boasts "12% APY!" Your brain probably thinks, "Same, right?"

Wrong. Very wrong.

When it comes to comparing interest rates, APR and APY might look like twins… but they’re not. Far from it. The difference between them can determine whether you grow your savings or overpay on a loan. In this guide, we’ll break down what APR and APY really mean, how they work in banking, lending, and crypto, and how understanding them can help you make smarter financial decisions.

Key Takeaways

- APR (Annual Percentage Rate) shows the yearly cost of borrowing, including interest and certain fees.

- APY (Annual Percentage Yield) reflects your total yearly return, factoring in compounding.

- For borrowers, lower APR = lower total cost. For savers, higher APY = higher returns.

- In crypto and DeFi, compounding frequency can turn modest APRs into much higher APYs.

APY vs APR: The Essential Difference

At a glance, APR tells you how much interest you’ll pay (or earn) over a year, without compounding. APY, on the other hand, includes compounding, the process where interest earns more interest over time.

When comparing financial products, whether a credit card, savings account, or staking pool, this distinction matters. For borrowers, APR reveals the true cost of debt, while for investors, APY highlights the power of compound growth.

TL;DR. APR is about cost, APY is about growth. Knowing which one applies helps you choose between competing offers with confidence.

What Is APR (Annual Percentage Rate)?

APR represents the yearly interest rate charged to borrow money, or the rate you earn before compounding if you lend it. It includes interest and certain fees, helping you understand the total cost of credit.

APR is widely used in credit cards, personal loans, mortgages, and auto financing. For example, if your credit card has an 18% APR, you’ll pay 18% interest on any carried balance. Fixed-rate loans maintain the same APR, while variable-rate loans fluctuate with market conditions and Federal Reserve changes.

Example: Borrow $10,000 at 10% APR for one year. You’ll owe $1,000 in interest. Simple and transparent, without compounding surprises.

What Is APY (Annual Percentage Yield)?

APY measures how much your money grows over a year, including compounding. It reflects how often your interest is added to your balance (daily, monthly, or annually) which then generates more interest.

This is the standard metric for savings accounts, money market accounts, and certificates of deposit (CDs). Banks and digital financial platforms often advertise APY because it paints a more complete picture of earning potential.

Example: Deposit $10,000 in an account with a 5% APY, compounded monthly. After one year, your balance grows to $10,511, slightly higher than a flat 5% APR return.

The more frequent the compounding, the greater the growth, especially important in DeFi protocols that compound every few minutes.

APR vs APY in Different Financial Products

Credit Cards and Loans (APR)

When borrowing, APR helps you understand the true borrowing cost. For instance, if a mortgage advertises a 6.5% APR, that includes both the interest and certain closing costs.

Car loans, student loans, and credit cards use APR to keep comparisons straightforward across lenders. The key? Lower APR = less expensive borrowing.

Savings and Investment Accounts (APY Focus)

If your goal is wealth building, APY is your guide. A high-yield savings account with 4.5% APY grows faster than one with 4% because compounding quietly amplifies returns.

For certificates of deposit (CDs) or fixed deposits, APY helps you compare the real impact of compounding frequency.

Cryptocurrency and DeFi (Both APR and APY)

In crypto lending, staking, or yield farming, both metrics appear and can be easily confused.

- APR shows base rewards (without compounding).

- APY assumes you’re constantly reinvesting.

Example: A DeFi pool may show 100% APR, but with daily compounding, it becomes 171% APY. The key is understanding how often you can claim rewards and whether gas fees make compounding worthwhile.

How to Calculate APR vs APY

To compare offers correctly, you can calculate one from the other:

Example: 12% APR compounded monthly

APY = (1 + 0.12/12)^12 - 1 = 12.68%

Compounding more frequently increases APY slightly each time.

Which Should You Focus On?

- If you’re borrowing, prioritize APR. It reflects the total cost of debt.

- If you’re saving or investing, look at APY. It shows how compounding boosts earnings.

- In crypto, check both. APR tells you the base reward, APY reveals potential if you reinvest.

When comparing offers, always read the fine print; frequency, fees, and conditions can shift the real value dramatically.

Common Misconceptions and Pro Tips

Myth: “APY is always better.”

Reality: Only if compounding happens, or if you reinvest earnings.

Myth: “APR ignores compounding, so it’s useless.”

Reality: APR helps borrowers compare costs clearly.

Pro Tip: Use online APR-to-APY calculators for quick comparisons. They’re free and eliminate guesswork.

The Bottom Line

APR and APY aren't just different ways of saying the same thing, they represent two different approaches to measuring returns.

When you see APR, you're looking at simple interest calculated over a year. When you see APY, you're seeing what happens when earnings get reinvested and compound over time. Both are valid measurements, just showing different scenarios.

This distinction becomes more noticeable with higher interest rates. A 50% APR becomes closer to 65% when compounded daily. The higher the base rate, the bigger the difference between these two numbers becomes.

Understanding which one you're looking at helps you compare options accurately. APR gives you the base rate, while APY shows the potential with compounding factored in.

Once you get the hang of spotting the difference, those financial offers suddenly make a lot more sense. No more squinting at numbers wondering why similar-sounding deals seem to work out so differently. It's like finally understanding why some recipe measurements are in cups and others in ounces - same concept, different scales, and knowing which is which makes all the difference.