More than a million Bitcoin have vanished because owners didn’t plan ahead. Without a crypto inheritance plan, your family could lose access to your assets forever. Here’s how to safeguard them.

Keep reading

As digital assets become a core part of personal wealth, one uncomfortable question lingers: what will happen to your crypto when you’re gone? Unlike traditional assets that can be managed through banks or brokers, cryptocurrencies are bound entirely to whoever holds their private keys. Lose the keys, and the funds are gone. Permanently.

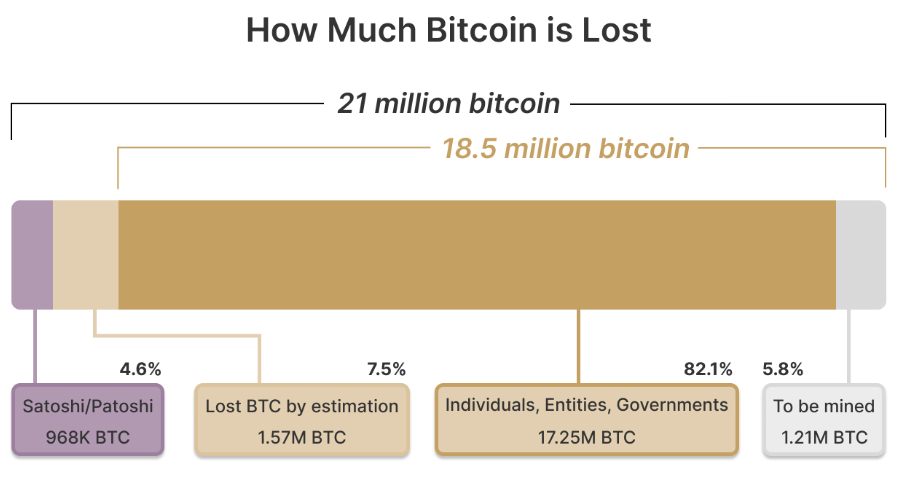

Each year, millions of dollars in Bitcoin, Ether, and other tokens vanish into the digital void when holders pass away without sharing access. It is estimated that around 1.5 million BTC (roughly 7.5% of total supply) may already be lost forever. With digital wealth now part of countless estates, preparing for the inevitable is no longer optional; it’s the responsible thing to do.

Why Planning for Crypto Inheritance Matters

In traditional finance, wealth transfer is handled through wills, trusts, and custodians. But crypto flips that model: you are the bank. Your heirs can’t simply request a password reset or call customer service. Without private keys, wallets, or access instructions, those assets are unrecoverable for all effects and purposes.

A crypto inheritance plan ensures that your digital assets, from Bitcoin and altcoins to NFTs and DeFi holdings, remain both secure and accessible to the people you choose. It bridges two crucial needs: protecting your funds today and ensuring your legacy tomorrow.

Beyond personal security, inheritance planning also reduces emotional and financial stress for your loved ones. By documenting how and where assets can be accessed, you prevent confusion and potential legal disputes.

Building the Foundation of a Crypto Inheritance Plan

Start with Legal Clarity

Consult an attorney familiar with digital assets. A properly structured will or trust should identify your crypto holdings, list beneficiaries, and outline how they can access those funds. Many jurisdictions still lack explicit laws for digital assets, so expert guidance helps ensure compliance and enforceability.

Secure Your Keys… But Don’t Overshare

The biggest challenge in crypto inheritance is private key management. If you die with your keys, your crypto dies with you. However, leaving keys in plain text within a will or document is just as risky. Instead, consider approaches like:

- Multisignature wallets, which require multiple approvals to move funds.

- Shamir’s Secret Sharing, which means splitting your seed phrase into parts distributed among trusted people.

- Encrypted backups or sealed letters stored in secure, offline locations.

Document recovery procedures in plain language so your heirs can follow them even without technical knowledge.

Choose the Right Executor

A traditional executor may not understand how to navigate crypto. You can appoint a tech-literate executor or designate a digital asset custodian to handle that portion of your estate. This ensures smooth execution and reduces the risk of errors or loss.

In a market driven by innovation and constant change, a well-structured inheritance plan offers something rare in crypto, certainty.

New Tools for a Digital Age

The rise of blockchain-based “death protocols” and smart contract automation adds a new layer of possibilities. Some platforms allow transfers to trigger automatically after certain conditions are met (for example, a verifiable death certificate or extended inactivity).

Ethereum and similar chains already support programmable inheritance systems, but these should complement, not replace, legal documents. Technology can help enforce your intentions, but law remains the foundation of inheritance.

Some investors even use “dead man’s switches”, automated systems that transfer funds if the owner doesn’t log in for a set period. While clever, it might be best to pair them with legal documents to prevent accidental activations.

Protecting Privacy While Planning Ahead

While planning for the future, it’s crucial to maintain security in the present. Avoid including wallet addresses, private keys, or passwords in public wills, which become part of the legal record. Instead, store such details in encrypted files or sealed envelopes accessible only to specific individuals.

Tools like decentralized identifiers (DIDs) and verifiable credentials can also help manage long-term identity and access rights. These systems allow you to define who can access what, and when, without intermediaries.

Custodial vs. Non-Custodial: Finding the Balance

When structuring inheritance, knowing whether your assets are held in custodial or non-custodial wallets makes all the difference.

Custodial services (like major exchanges) manage private keys on your behalf, which simplifies recovery if your heirs can provide proper documentation. However, it introduces third-party risk. Accounts can be frozen, hacked, or shut down.

Non-custodial wallets, on the other hand, offer maximum control and privacy but demand greater responsibility. If your heirs lose the seed phrase, there’s no backup plan. There’s also the possibility of taking a hybrid approach: keeping long-term holdings in non-custodial storage for security, while using reputable custodians for smaller, more accessible amounts.

Keep It Up to Date

A crypto inheritance plan is not a “set it and forget it” document. Prices change, portfolios evolve, and wallet technologies become obsolete very often. It may be wise to revisit your plan regularly, especially after major life events such as marriage, divorce, or the birth of a child.

It’s also worth keeping track of regulatory updates in your jurisdiction. Laws surrounding digital assets and inheritance are rapidly evolving, and what’s compliant today may not be tomorrow.

Common Inheritance Pitfalls

Even the best intentions can go wrong. Here are the most frequent mistakes to avoid:

- Including seed phrases directly in your will. As we mentioned before, this makes them public and vulnerable.

- Neglecting to educate heirs. Without guidance, even secure plans can fail.

- Relying solely on exchanges. Centralized platforms can fail or freeze funds.

Planning isn’t just about distributing wealth; it’s about ensuring continuity. A clear inheritance strategy preserves your crypto’s value and prevents it from becoming part of the estimated $100 billion in lost digital assets worldwide.

Protecting More Than Just Coins

Preparing a crypto inheritance plan isn’t merely about money; it’s about legacy. For all the talk about decentralization and autonomy, responsibility and forward-thinking remain at the heart of crypto ownership. By taking the time to plan ahead, you safeguard not only your wealth but also your family’s peace of mind.

NEWS AND UPDATES

LATEST ARTICLE

Vi har goda nyheter – Auto Top-Up för kortet är äntligen här, och det kommer göra din vardag så mycket enklare.

Glöm stressen vid kassan när saldot är för lågt. Den här nya funktionen fyller automatiskt på ditt kort när balansen sjunker – helt på dina villkor.

Ni bad om det – vi lyssnade. Tack vare er feedback har vi byggt Auto Top-Up för att ta bort onödig stress från din vardag. Kortet är alltid redo – så du kan fokusera på viktigare saker (som att välja vad du ska äta till lunch 🍜).

Och här är det bästa av allt: du kan nu använda dina krypto till att betala direkt. Välj vilken kryptotillgång du vill, fyll på kortet – och börja spendera. Så enkelt är det.

Inga fler “Oj, saldot är slut!” 😬

Vi har alla varit där – man ska betala något viktigt, men kortet har för lite pengar. Auto Top-Up ser till att du alltid har pengar på kortet, utan att du ens behöver tänka på det.

Ställ in det en gång – sen kan du slappna av

Aktivera Auto Top-Up en gång, så sköter det sig själv. Du slipper ladda kortet manuellt varje gång saldot sjunker.

Dina pengar, dina regler 💸

Vill du använda fiat? Krypto? Båda? Du bestämmer själv vilken valuta som används vid varje påfyllning.

Alltid redo att betala

Oavsett om du handlar i butik, online eller reser – med Auto Top-Up är ditt kort alltid redo att användas.

Hur funkar det? ✨

Med Auto Top-Up har du full kontroll. Du bestämmer:

- Vilket saldo som ska trigga en automatisk påfyllning.

- Hur mycket som ska fyllas på varje gång.

- Vilken valuta som ska användas – fiat eller krypto.

Tänk dig att du ska betala något viktigt och upptäcker att saldot är för lågt – irriterande, eller hur? Med Auto Top-Up händer inte det längre. Ställ in din gräns och Tap fyller automatiskt på ditt kort innan du ens märker att det behövs – helt enligt dina inställningar.

Så här kommer du igång

- Logga in i din Tap-app

- Gå till kortinställningar

- Aktivera Auto Top-Up och välj dina preferenser

- Klart! Ditt kort är alltid redo

Byggt för sinnesro 😌

Oavsett om du är på resa, shoppar eller betalar vardagsutgifter – med Auto Top-Up slipper du oroa dig för att kortet inte räcker till. Kortet håller sig laddat, så du slipper tänka på det.

Börja använda Auto Top-Up redan idag

Se till att din Tap-app är uppdaterad, gå till kortfliken och aktivera Auto Top-Up där.

Har du frågor? Vårt supportteam finns här för att hjälpa dig komma igång!

Civic (CVC) är en blockchain-baserad plattform för identitetsverifiering som fokuserar på att erbjuda säkra och kostnadseffektiva lösningar för hantering av digital identitet. I takt med att behovet av tillförlitlig identitetsverifiering växer, särskiljer sig Civic genom sin decentraliserade struktur och användarcentrerade kontroll av personlig data.

Låt oss utforska hur Civic tacklar utmaningarna inom digital identitet, integritet och säkerhet.

Kort sammanfattning (TLDR)

- Decentraliserad verifiering: Civic erbjuder säkra identitetsverifieringar utan att lagra data centralt, vilket minskar risken för bedrägerier och identitetsstölder.

- Användarens kontroll: Du äger din data och väljer själv vad du vill dela – och med vem – via Civic-appen.

- Ekosystem: Använder Identity Verification Marketplace och Civic Pass för att möjliggöra åtkomstkontroll, särskilt inom DeFi.

Vad är Civic-nätverket?

Civic grundades 2015 av Vinny Lingham och Jonathan Smith och genomförde en tokenförsäljning 2017 där man tog in 33 miljoner dollar. Målet var att modernisera identitetsverifiering med hjälp av blockchain – där du inte längre behöver skicka dina ID-dokument till olika tjänster gång på gång.

Istället bygger plattformen på återanvändningsbara verifieringar (reusable KYC), vilket minskar både risk och kostnad för användare och företag.

Civic Pass, som lanserades 2021, fungerar som en identitetsnyckel för DeFi-tjänster, NFT-plattformar och DAO:er som kräver efterlevnad. Plattformen fortsätter att vara en av de mer framträdande lösningarna för digital ID-verifiering i blockchainvärlden.

Hur fungerar Civic?

Plattformen bygger på tre huvudkomponenter:

- Identity Verification Marketplace – Kopplar ihop verifieringstjänster med betrodda validerare.

- Civic Pass – Erbjuder åtkomstkontroll för DeFi och andra tjänster med krav på identitetsverifiering.

All information lagras lokalt på användarens enhet – aldrig centralt hos Civic – och verifieras via blockchain. Genom att kombinera decentralisering och datakontroll erbjuder Civic både säkerhet och smidighet.

CVC-token används inom ekosystemet för att betala för verifieringstjänster och belöna validerare.

Fördelar med Civic

Enligt Civic-teamet kan verifieringsprocesser genomföras snabbare och billigare än traditionella metoder. Dessutom elimineras centrala databasrisker, vilket minskar hotet om dataintrång och identitetsstölder.

Plattformen är även inkluderande – lösningar finns för personer som inte har tillgång till traditionella finansiella tjänster, vilket kan bidra till ökad ekonomisk tillgänglighet globalt.

Sedan 2021 har Civic utvecklat verktyg för DeFi-säkerhet och NFT-verifiering, och fortsätter att hitta nya användningsområden inom decentraliserade applikationer.

Användningsområden

Civic används för säker och effektiv identitetsverifiering, oavsett om det gäller kontoskapande, åldersverifiering eller efterlevnad av regelverk. Företag kan implementera starka KYC-rutiner utan att behöva hantera känslig information i sårbara databaser.

Vad är CVC?

CVC är den inbyggda tokenen i Civic-ekosystemet. Den används för:

- Att betala transaktionsavgifter och verifieringstjänster

- Belöningar till validerare

- Incitament inom nätverket

CVC är en ERC-20-token med en fast total tillgång och kan inte brytas.

Hur köper jag CVC?

Du kan enkelt köpa, sälja och lagra CVC i Tap-appen. Allt du behöver göra är att registrera ett konto och komma igång direkt.

%201.webp)

Ever wondered how companies launch those shiny credit cards with their logos on them? Let's dive into the world of card programs and break down everything you need to know to launch one successfully.

What's a card program, anyway?

Think of a card program as your business's very own payment ecosystem. It's like having your own mini-bank, but without the vault, technical infrastructure and security guards. Companies use card programs to offer payment solutions to their customers or employees, whether a store credit card, a corporate expense card, or even a digital wallet.

As you’ve probably figured, the financial world is quickly moving away from cash, and card payments are becoming the norm. In fact, they're now as essential to business as having a product, website or social media presence.

Why should your business launch a card program?

Launching a card program isn't just about joining the cool kids' club – it's about creating real business value and heightened exposure. Here's what you can achieve:

Keep your customers coming back

Remember those loyalty cards from your favourite coffee shop? Card programs take that concept to the next level. When customers have your card in their wallet, they're more likely to choose your business over competitors. Plus, every time they pull out that card, they (and everyone else around) see your brand.

Show me the money!

Card programs open up exciting new revenue streams. You can earn from:

- Interest charges (if applicable)

- Transaction fees from merchants

- Annual membership fees

- Premium features and services

- Insights and information on spending habits

Know your customers better

Want to know what your customers really want? Their spending patterns tell the story. Card programs give you valuable insights into customer behaviour, helping you make smarter business decisions.

Understanding the card program ecosystem

Let's break down the key players in this game:

The dream team

Picture a football team where everyone has a crucial role:

- Card networks (like Visa and Mastercard) are the referees, setting the rules

- Card issuers (like Tap) are the coaches, making sure everything runs smoothly

- Processors (overseen by Tap) are the players, handling all the transactions on the field

Open vs. closed loop: what's the difference?

Open-loop and closed-loop cards differ in where they can be used and who processes the transactions. Let’s break this down:

Open-loop cards:

These cards are branded with major payment networks like Visa, Mastercard, or American Express, and are accepted almost anywhere the network is supported, both domestically and internationally.

Examples: Traditional debit or credit cards, prepaid cards branded by major networks.

Pros: Wide acceptance and flexibility.

Cons: May come with fees for international use or transactions.

Closed-loop cards:

Cards issued by a specific retailer or service provider for exclusive use within their ecosystem. These cards are limited to the issuing brand or select partners.

Examples: Store gift cards (like Starbucks or Amazon), fuel cards for specific gas stations.

Pros: Often come with brand-specific rewards or discounts.

Cons: Limited to specific merchants; less flexibility.

Challenges that may arise

Let's be honest – launching a card program isn't all smooth sailing. Here are the hurdles you'll need to jump:

The regulatory maze

Remember trying to read those terms and conditions? Well, card program regulations are even more complex. You'll need to navigate through compliance requirements that would make your head spin.

Security

Fraud is like that uninvited guest at a party – it shows up when you least expect it. You'll need robust security measures to protect your program and your customers.

We’ve designed our card program to handle these niggles, so that you can bypass the challenges and reap the rewards. With a carefully curated experience, we take care of the setup, programming and hardware so that you can focus on the benefits and users.

Closing thoughts

Launching a card program is like building a house – it takes careful planning, the right tools, and expert help. But when done right, it can become a powerful engine for business growth.

Contact us to get started on building a card program tailored to your company. After all, the future of payments is digital, and there's never been a better time to get started.

Currency volatility is a challenge that businesses operating across borders can’t afford to ignore. Exchange rate fluctuations can erode profits, increase costs, and create financial uncertainty, making it difficult for companies to plan effectively.

For businesses that deal with international transactions, traditional solutions like foreign exchange (forex) hedging can be expensive and complicated. Thankfully now, there's a smarter, more efficient alternative—stablecoins.

Stablecoins offer businesses a way to bypass the unpredictability of currency fluctuations by providing a digital asset pegged to stable currencies like the US dollar. The black and white of it is that they make cross-border payments faster, cheaper, and more reliable.

In this article, we’ll explore why stablecoins are an ideal solution for tackling currency volatility in global financial management.

The challenges of currency volatility in global finance

Global businesses are constantly exposed to currency risks, for a range of reasons, including:

- Geopolitical events – Trade wars, conflicts, or political instability can impact currency values.

- Inflation and interest rate changes – Central bank policies can cause sudden shifts in exchange rates.

- Market speculation – Traders and investors can drive rapid price swings.

For businesses, currency volatility can lead to higher transaction costs, as moving money internationally becomes more expensive. It can also result in unpredictable revenue, making it difficult for companies operating in multiple countries to manage pricing. Additionally, if a currency depreciates suddenly, businesses may face financial losses as profits shrink overnight.

Many businesses use forex hedging strategies (such as forward contracts and options) to manage risk, but these methods are often costly, complex, and require expert knowledge. A simpler, more efficient solution is needed—and that’s where stablecoins come in.

Why stablecoins are the perfect hedge for businesses

Stablecoins offer a practical way for businesses to protect themselves against currency volatility. Unlike traditional cryptocurrencies (which are often highly volatile), stablecoins are pegged to a fiat currency providing a reliable and steady value.

Key benefits for businesses:

- Price stability – With stablecoins, businesses don’t have to worry about sudden exchange rate swings affecting their revenue or costs.

- Fast, low-cost transactions – International payments using stablecoins settle in minutes, not days, with significantly lower fees than traditional banking systems.

- No dependence on banks – Unlike wire transfers, stablecoin payments don’t require intermediaries, reducing delays and extra costs.

- Transparent and secure transactions – Built on blockchain technology, stablecoins ensure auditable, tamper-proof payments, adding an extra layer of security.

For businesses engaging in global trade, payroll, treasury management, or e-commerce, stablecoins offer a modern financial tool to streamline operations and avoid currency-related risks.

Choosing the right stablecoin for your business needs

Not all stablecoins are created equal. Businesses need to choose the right one based on factors like trust, regulation, and network efficiency.

Top stablecoins to consider:

💰 USDT (Tether) – The most widely used stablecoin, but with some concerns around transparency.

💰 USDC (USD Coin) – Fully backed by regulated financial institutions, making it a trusted option.

💰 DAI – A decentralized stablecoin, offering stability without relying on a central issuer.

💰 EUROC (Euro Coin) – A fully backed euro-denominated stablecoin issued by Circle, providing a stable digital alternative for euro transactions.

Key considerations:

- Regulatory compliance – Ensure the stablecoin follows financial regulations in your operating regions.

- Blockchain network – Some stablecoins operate on multiple blockchains (Ethereum, Tron, Solana). Choosing the right network affects transaction speed and fees.

- Liquidity and acceptance – Businesses should opt for stablecoins with high liquidity and broad industry adoption.

Choosing the right stablecoin is essential for seamless global transactions while ensuring stability and security.

The future of stablecoins in global finance

Stablecoins are no longer just a niche tool—they are gaining mainstream acceptance among businesses, financial institutions, and regulators.

Growing adoption – Companies like PayPal and Visa are integrating stablecoins into their payment systems.

Institutional backing – Banks and investment firms are exploring stablecoin use for settlements and asset management.

Regulation on the rise – Governments are working on stablecoin frameworks, aiming to balance innovation with security.

Emerging financial products – Stablecoin-based loans, savings accounts, and remittance services are expanding the financial ecosystem.

As stablecoins evolve, their role in global financial management will only grow, making them a key tool for businesses worldwide.

Conclusion

Currency volatility remains a major challenge for businesses operating globally, as traditional hedging strategies are often expensive and inefficient, leaving companies searching for a better way to manage financial risk.

As outlined above, stablecoins offer a simple, effective, and low-cost solution to tackling currency fluctuations. By providing price stability, fast transactions, and reduced banking dependency, stablecoins empower businesses to operate seamlessly across borders.

For companies looking to future-proof their global financial operations, stablecoins are an answer worth considering. Now is the time to explore how they can be integrated into your business strategy: and we’re here to help.

Onyxcoin (XCN), tidigare känt som Chain (CHN), representerar ett stort steg framåt inom blockchaininfrastruktur. Sedan omprofileringen i mars 2022 har projektet blivit ett ledande alternativ för företag som vill bygga finansiella tjänster på privata blockchain-nätverk. Men vad är det som gör XCN så intressant? Låt oss dyka in.

Vad är XCN?

XCN är kryptovalutan bakom Onyx Protocol – ett flexibelt blockchainnätverk som är utvecklat för att förbättra finansiella avvecklingar. Det används både som nyckel för att få tillgång till tjänster och som styrningsverktyg inom det decentraliserade ekosystemet.

Onyx Protocol möjliggör att separata nätverk kommunicerar smidigt genom gemensamma standarder. Det är både säkert och flexibelt tack vare ett system där tillgångskontroll separeras från registersynkronisering. Nätverket förlitar sig på ett utvalt antal ”block signers” för att säkerställa integritet och en enda ”block generator” för effektiv blockskapande.

Allt detta styrs via Onyx DAO på Ethereum, där XCN används för styrning, premiumtjänster och uppgraderingar av nätverket.

Projektet startades 2014 och har stöttats av investerare som Nasdaq och Citigroup. Det har sedan dess utvecklats till en avancerad och självständig blockchainlösning.

Viktiga egenskaper:

- Molnbaserad blockchain-infrastruktur för företag

- Anpassningsbara verktyg för tillgångsskapande

- Smart contracts via "control programs"

- DAO-styrning för användarinflytande

- Tjänstnivåer: standard och premium

Marknadsanalys: Tekniskt och fundamentalt

Tokenomics

Det finns totalt 48,47 miljarder XCN, varav cirka 65 % redan är i cirkulation. Av detta är 15 miljarder reserverade för stiftelsen och 10 miljarder för DAO:n, med en månadsvis tilldelning om 200 miljoner XCN för att hålla utbudet under kontroll.

Teknisk arkitektur

- Parallella blockchain-nätverk

- Strikt åtkomstkontroll för tillgångar

- Validering via betrodda noder

- Effektiv blockproduktion

Volym, volatilitet och marknadssentiment

Handelsvolym

XCN:s handelsvolymer kan säga mycket om marknadsintresset. Höga eller stabila volymer tyder ofta på stark aktivitet, medan hastiga upp- eller nedgångar kan spegla spekulation eller nyheter.

Prisvolatilitet

XCN:s pris har växlat mellan stabilitet och snabba rörelser. Volatilitet lockar vissa investerare men kan avskräcka andra. Rörelserna påverkas ofta av makroekonomiska faktorer och branschens övergripande humör.

Sentiment

Via sociala medier, forum och nyhetsrapportering kan man få en bild av marknadens attityd. Positiva nyheter om projektets utveckling har genererat optimistiskt sentiment, medan osäkerhet kan trycka ner stämningen.

Korttidsprognoser (1–3 år)

Möjligt positivt scenario

Drivkrafter:

- Företagsanpassning (partnerskap, adoption)

- Teknologiska förbättringar (transaktionstider, avgifter)

- Ökat institutionellt intresse

Prognos: $0.005 – $0.015 beroende på utveckling och marknadens respons

Möjligt negativt scenario

Risker:

- Regulatorisk osäkerhet

- Konkurrens från liknande projekt

Prognos: $0.001 – $0.0017

Långsiktsprognoser (3–5 år)

Möjligt positivt scenario

Drivkrafter:

- Utbredd användning av Onyx-teknik

- Ekosystemets tillväxt

- Kryptomarknadens generella expansion

Prognos: $0.02 – $0.08 beroende på tillväxt och innovation

Möjligt negativt scenario

Risker:

- Lång nedgång i kryptomarknaden

- Överlägsen konkurrens

Prognos: $0.0005 – $0.0015

Slutsats

Onyxcoin (XCN) har potential att växa genom ökad användning och teknisk utveckling, men står också inför utmaningar som kan påverka dess framtid. Prognoserna varierar kraftigt beroende på marknadens riktning, teknologins framsteg och investerarnas förtroende.

Som alltid när det gäller digitala tillgångar, är det klokt att läsa på ordentligt, följa utvecklingen nära och reflektera över sin egen risktolerans. Håll koll på XCN direkt i Tap-appen för senaste uppdateringar och prisrörelser.

%20_.webp)

Vad är Onyxcoin (XCN)?

Onyxcoin är den inhemska tokenen för Onyx Protocol, en molnbaserad blockchain-infrastruktur som gör det möjligt för företag att skapa privata blockchain-nätverk för finansiella tjänster. Till skillnad från offentliga blockkedjor erbjuder Onyx en sluten och säker miljö för att utfärda, lagra och överföra digitala tillgångar, vilket minimerar risker som säkerhetsintrång och transaktionsförseningar.

Onyx Protocol är utformat för att ansluta oberoende nätverk under gemensamma standarder, vilket säkerställer smidig interoperabilitet. Genom att separera kontrollen över tillgångar från synkroniseringen av huvudboken levererar det både säkerhet och flexibilitet till användarna.

Användningsområden för XCN

XCN fungerar både som en nyttotoken och en styrningstoken inom Onyx-ekosystemet. Det används för att betala för premiumtjänster, finansiera nätverksuppgraderingar och ger innehavare möjlighet att påverka protokollets framtida utveckling genom deltagande i Onyx DAO, en decentraliserad autonom organisation på Ethereum.

Företag kan använda Onyx Protocol för att skapa anpassade "utfärdandeprogram" för tillgångsskapande, som hanteras av "kontrollprogram" som möjliggör skapandet av avancerade smarta kontrakt. Nätverkets säkerhet upprätthålls av en federation av "blocksignerare" för att förhindra förgreningar, medan en enda "blockgenerator" säkerställer effektiv blockskapande.

Framtidsutsikter för XCN

Prognoser för XCN varierar beroende på marknadsscenarier. I ett positivt scenario, med ökad företagsadoption och teknologiska framsteg, kan XCN:s pris öka betydligt över de kommande åren. I ett mindre gynnsamt scenario, med ökad konkurrens och regulatoriska utmaningar, kan priset förbli stabilt eller minska.

Det är viktigt att notera att kryptovalutamarknaden är mycket volatil, och priserna kan påverkas av en mängd faktorer, inklusive teknologiska framsteg, marknadssentiment och globala ekonomiska förhållanden.

Vanliga frågor om Onyxcoin (XCN)

Är Onyxcoin (XCN) relaterat till JP Morgan?

Nej, Onyxcoin är ett oberoende projekt och har ingen koppling till JP Morgan eller dess tidigare blockchain-enhet, som nu är känd som Kinexys.

Hur kan jag köpa och använda XCN?

XCN kan köpas på flera större kryptovalutabörser. För att delta i styrningen av Onyx Protocol eller använda premiumtjänster, kan innehavare satsa sina tokens genom den officiella plattformen.With Tap

Vad är den maximala tillgången på XCN?

Den maximala tillgången på XCN är 48,4 miljarder tokens, med cirka 65% för närvarande i cirkulation.

För att hålla dig uppdaterad om XCN:s prisrörelser och nyheter kan du följa dess sida inom Tap-appen.