An in-depth look at XRP’s 2025 momentum, as legal clarity, technical strength, and growing institutional interest converge for the first time since 2017.

Keep reading

This week, XRP has been building pressure at $3.30, with three powerful catalysts aligning for the first time since 2017 - setting up what could be the token's most explosive run yet.

TLDR:

- XRP price surged 21% after the SEC Ripple Labs case was officially dismissed

- Technical indicators show buy-side momentum peaking, with Aroon Up hitting 100%

- Nine major asset managers now have pending XRP ETF applications, with 88% market odds for 2025 approval

- CME's XRP futures launched in May have already generated over $1.6 billion in trading volume

Three big forces are hitting XRP at once: legal clarity, strong technical momentum, and rising institutional demand. In the past, this mix has sent prices soaring.

The legal victory that changes everything

The SEC's formal dismissal of its case against Ripple Labs isn't just another regulatory win - it's the removal of XRP's biggest institutional adoption barrier. After nearly five years of uncertainty, corporate treasuries and institutional investors finally have the green light they've been waiting for.

And the timing couldn't be better. Just as regulatory clouds clear, analysts are agreeing that XRP's technical setup is screaming bullish signals that haven't been seen since the 2017 run-up.

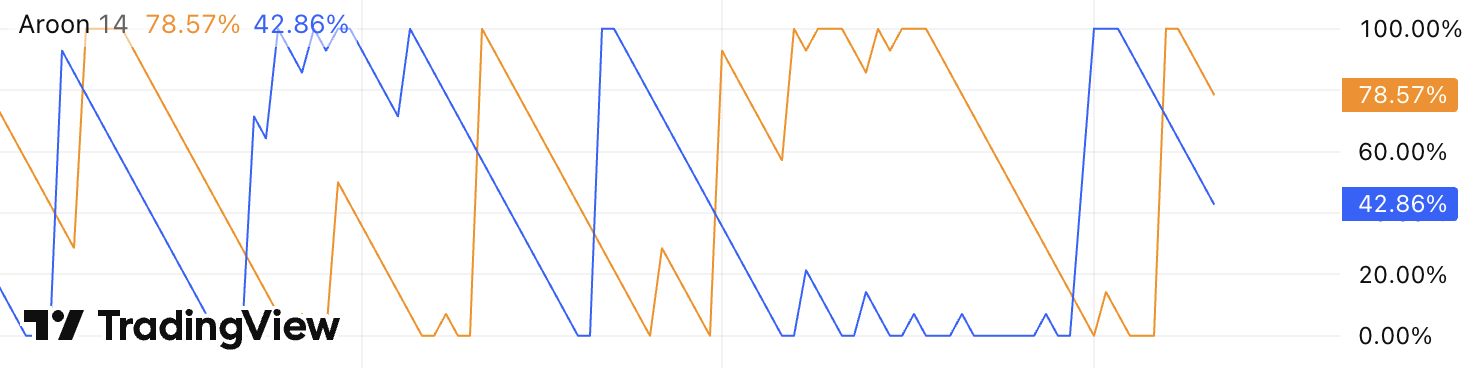

Technical momentum reaches peak levels

XRP's chart tells a compelling story of institutional accumulation disguised as consolidation:

→ For starters, the token has climbed 21% over the past seven days, hitting a recent high of $3.36 (just 8% below its ATH). Momentum indicators suggest this is just the beginning.

→ The Aroon Up line is holding at 100%, showing that buyers are consistently driving XRP to fresh highs. This sustained strength often comes before major moves - especially with the price holding above the key $3.15–$3.16 support area. *To view the current Aroon line, log into Trading View and add the indicator.

→ Market sentiment has shifted decisively bullish, with XRP's weighted sentiment score hitting a two-week high of 1.17. More telling is the token's social dominance, which has climbed to a recent high of 7.95%, meaning XRP is dominating an increasingly larger share of crypto conversations as retail interest reignites.

The institutional infrastructure is already built

While crypto X debates ETF timelines, institutional players have quietly constructed the infrastructure needed for serious XRP adoption. CME Group launched regulated XRP futures in May, providing the hedging tools institutions will need before taking major positions.

The results speak volumes: CME's XRP futures have already surpassed $1.6 billion in trading volume, signalling genuine institutional demand beyond retail speculation. These aren't just paper trades; they represent real institutional capital positioning for XRP's next move.

Nine major asset managers now have pending XRP ETF applications, including heavyweights like Grayscale, ProShares, and 21Shares. Polymarket traders are pricing in 88% odds for SEC approval by year-end, creating a feedback loop where institutional preparation drives retail anticipation.

Why this time is different

Previous XRP rallies were driven primarily by retail speculation and partnership announcements. But today's setup combines retail enthusiasm with genuine institutional infrastructure and regulatory clarity: a trifecta that hasn't existed since XRP's 2017-2018 surge.

The numbers back this up. Institutional trading volumes have spiked 208% to $12.40 billion following the SEC dismissal, while derivatives open interest climbed 15% to $5.90 billion.

Large-order flows are consistently defending the $3.15 support level, suggesting institutional accumulation even during short-term volatility.

What traders are watching

Analysts are saying that technical analysis points to immediate resistance at $3.39-$3.40, with sustained bullish momentum (bolstered by institutional flows and ETF positioning) raising the odds of a breakout, particularly if the Aroon Up indicator remains high.

According to market insiders, a successful move higher could fuel a run toward the $3.50-$3.75 range, with a longer-term target of $3.66+ for a cycle high retest.

Key levels to monitor:

- Support: $3.15-$3.16 (proven institutional buying zone)

- Resistance: $3.39-$3.40 (breakout confirmation level)

- Bull target: $3.66+ (cycle high retest)

Legal clarity, a technical breakout, and rising institutional demand are all hitting XRP at once - a rare mix of fundamentals and market momentum. For holders who’ve endured years of regulatory uncertainty, some are interpreting this as a potential breakout scenario.

NEWS AND UPDATES

LATEST ARTICLE

In March 2022, Onyx Protocol (formerly Chain) rebranded its token from CHN to XCN and saw widespread success. The shared, multi-asset, cryptographic ledger has seen considerable market attention and increased in value by almost 50% in the first few months post-launch.

Then, after implementing upgrades that included the likes of Chain Decentralised Autonomous Organisation (DAO), the beta release of the Onyx Cloud product, XCN staking, as well as listing on several crypto exchanges, Onyxcoin (XCN) reached its a new all-time high price. An honorable feat for the Onyx ecosystem considering that the greater crypto market was in a decline.

What Is Onyx protocol?

Onyx is a cloud blockchain infrastructure that allows companies to create and provide improved financial service solutions through their unique closed-ended blockchain network. This gives them the opportunity to upgrade to blockchain technology without carrying the risks linked to bigger public networks. The platform then allows them to issue, store and transfer digital assets on the company's private independent networks through several Chain ecosystem products.

According to the platform's whitepaper, the Chain protocol defines that it "allows participants to issue and control assets programmatically using digital signatures and custom rules."

Designed to improve on the current downfalls within the financial settlements industry, the Onyx protocol offers improved solutions for everything from transfer fees to transparency to settlement delays, as well as security issues and the reversibility of transactions.

Other Onyx ecosystem products include a standard and premium option of both an RPC/API (Remote Procedure Call API) product and a ledger-as-a-service option known as Sequence.

The standard RCP/API provides users access to various services within the Onyx Cloud that allows them to develop products on public blockchains. The premium access options provide added solutions and the opportunity to build on private networks. This option charges an annual fixed amount charged in XCN.

Sequence provides users access to Onyx's cloud blockchain accounting service where they can manage balances in a tokenized format. Again, there is a standard option or a premium access option with added benefits, payable in XCN.

The protocol also offers users end-to-end solutions covering the “design, development, compliance, sale and utilization” of NFTs through its Sequence NFT product.

The Onyx Decentralized Autonomous Organization (DAO) runs the whole Chain Protocol, which is governed by XCN token holders. To participate in the Onyx DAO and governance of the Chain, XCN holders must stake their tokens.

Who created Onyx protocol?

The Onyx blockchain network was founded in 2014 by the venture capitalist Adam Ludwin with the backing of several other venture capital firms, providing a solution to modern financial systems. The developers launched Chain Core after raising over $40 million through funding and strategic partnerships from the likes of Nasdaq, Orange, Capital One, and Citigroup.

In 2018 the platform was sold to Lightyear Corp., a division within the Stellar Development Foundation, but as of 2021, the company is now operating as a privately held corporation with new offices, shareholders, and a new board of directors.

How does the Onyx protocol work?

Onyx allows for multiple, independent blockchain networks to exist and work together, even if they're operated by different firms. Using the principle of least authority keeps control over assets separate from control over ledger synchronization so that everyone stays safe.

The Onyx cloud protocol allows any network participant to define and issue assets by creating their own "issuance programs." After they've been issued, units of an asset are kept in custody by "control programs," which are written in a flexible and Turing-complete programming language that may be used to create sophisticated smart contracts for blockchain networks.

A group of "block signers" secure each network. The system is protected against forks as long as a majority of the block signers follow the protocol. To make things more efficient, the protocol delegates block creation to a single "block generator." Any node on the network can validate blocks and submit transactions too.

The Onyx Core software is an enterprise solution that uses the Onyx Protocol. An open-source developer edition of Onyx Core is available for download, and Chain operates a freely accessible testnet to manage the Chain blockchain network.

What are XCN tokens?

XCN is the native token to the Onyx ecosystem and acts as both a utility token and a governance token. Holders are allowed to vote on community programs and protocol improvement plans through the Onyx DAO. The cryptocurrency also provides discounts on premium plans, a payment method for Onyx Cloud and Sequence fees, and node deployment.

Alongside the rebranding of CHN to XCN, Chain also launched its new Onyx Token smart contract on the Ethereum blockchain. Holders of CHN were given XCN tokens at a 1:1,000 ratio. Onyxcoin (XCN) has a maximum supply of 48.4 billion.

The Onyxcoin (XCN) has a total and maximum supply of 48,470,523,779 coins, with approximately 23,576,983,951 (44%) currently in circulation (at the time of writing). During the launch phase, 15 billion tokens were allocated to the foundation and ten billion to the DAO, with monthly distributions of 200 million and 100 million coins, respectively.

How can I buy the XCN token?

For those looking to incorporate Chain into their crypto portfolios, things just got a lot easier. The Tap app has recently added XCN to the list of supported currencies, allowing anyone with a Tap account to easily and conveniently access the Chain market.

Users can buy /sell XCN by using balances in either their crypto or fiat wallets or can buy the cryptocurrency with traditional payment options like bank transfers. Through the integrated wallets on the platform, users can also store and manage their XCN holdings easily and conveniently.

The post-pandemic working world is a different place entirely. These days, many people have given up their nine to five jobs to work from home, joining the gig economy where projects are more short-term and schedules are flexible. After all, all one needs is a reliable internet connection and a space to work.

These temporary projects allow for more freedom when it comes to creative license, time constraints and living a life best suited to the individual. And they just got a whole lot easier thanks to the electronic cash system that is Bitcoin (and other crypto assets).

The Gig Economy Meets Blockchain

There are plenty of upsides to working in the gig economy, most notably that you can pick your own hours. As you are in control of your schedule you can choose your vacation times, you’re your own boss, and you get to choose what jobs you take on.

In the UK alone the gig economy between 2016 and 2019 doubled in size, equating to a staggering 4.7 million workers. Meanwhile, in the European Union, the number of freelancers rose by 24% between 2008 and 2015, from 7.7 million to 9.6 million people.

The U.S. Bureau of Labor Statistics reported that 36% of all employees in the United States are part of the gig economy, approximately 57 million people. Unfortunately of these 57 million, 58% reported that they have not been paid for work that has been completed.

This problem could be solved through the use of blockchain and smart contracts. Smart contracts are digital agreements that automatically execute once the criteria have been met. Say you agree to complete a project within a certain time frame, once the project is completed and submitted, the payment is released. No need to request or accept payment, the funds are cleared and deposited directly into the relevant account.

Another positive to merging the gig economy with blockchain technology is the use of cryptocurrencies.

4 Reasons Why Getting Paid In Crypto Just Makes Sense

While smart contracts would need to be made in order for them to smoothen out the wrinkles of unpaid jobs, cryptocurrencies are available right now. The benefits of crypto transactions when it comes to working remotely just make sense.

1) Cryptocurrency transactions are fast and cheap

While the thought of using Bitcoin payments might sound scary, they are in fact incredibly simple to send, receive and withdraw. With the use of blockchain technology and the Bitcoin network, international transactions can be completed in minutes with considerably fewer fees. Not just Bitcoin, all digital currencies for that matter.

All you need to do is pick a cryptocurrency, share your wallet address and wait for the crypto transaction to clear. Through the Tap mobile app you can then use the funds to pay bills or sell them for fiat currencies and send them to your personal Tap account to spend as you please or directly to your bank account.

2Anyone can make crypto payments

While opening a bank account is typically a very tedious task, opening a crypto account is very easy. Anyone anywhere in the world can easily create an account, add funds, and start transacting. As the network is entirely digital, employees and employers based anywhere in the world can tap into this and effortlessly make crypto payments.

3) You can work from anywhere

On that note, cryptocurrencies give you the freedom to work anywhere in the world as there are no constraints on receiving payments allowing you to sell your skills in the global market. There has also been an increase in jobs looking for freelancers that are willing to accept Bitcoin, goodbye central banks and hello digital assets

4)Low transaction fees make small jobs worth it

If you've ever been hesitant about accepting small jobs, this is the one for you. When small jobs pay less, the payments might frequently be entirely overwhelmed by the transaction fees associated with receiving your payment for the job.

That is not the case when it comes to some cryptocurrencies, with Litecoin for example charging merely $0.02 per transaction.

How To Get Paid In Cryptocurrencies

If you’ve decided to take the plunge, you can either request that your employer pays in crypto, or specifically look for crypto-paying jobs (more on this below). The next step is to set up an account from where you can receive said crypto.

The Tap mobile app will tick all the boxes, and opening an account is incredibly simple. First, you will need to download the app and then register. You’ll be asked to fill in some personal information and then verify your identity with a government-issued identity document. This is all very normal and is required by law.

Once you are verified, head to the home page, select the Crypto wallet and choose a cryptocurrency you would like to receive / the cryptocurrency you will be paid in. Then select Receive and send the wallet address to your employer/contractor. You will get a notification when the funds arrive in your account.

If you’re looking for jobs that specifically pay in crypto, look to Purse.io, Ethlance and Coinality. These are part of the gig economy and pay in cryptocurrencies. Good luck out there, it will 100% be worth it!

Att få betalt i kryptovalutor har öppnat upp den globala gig-ekonomin som aldrig förr. Du behöver inte längre bo i samma land – eller ens på samma kontinent – som din uppdragsgivare. Kryptojobb är inte bara mer tillgängliga, de har också blivit allt mer accepterade.

I den här guiden visar vi var du kan hitta jobb som specifikt betalar i kryptovaluta. Men först – varför är det här så attraktivt?

Fördelar med att få betalt med blockkedjeteknik

Den snabbt växande blockkedjebranschen integrerar nu kryptovalutor i traditionella arbetsmarknader. Oavsett om du jobbar frilans eller söker en fast tjänst kan du numera få din lön i krypto.

Kryptovalutor gör internationella utbetalningar både snabbare och billigare. Tack vare den decentraliserade tekniken sker betalningarna på bara några minuter, med minimala transaktionsavgifter – oavsett vart i världen du befinner dig. Det här gör det särskilt smidigt för frilansare att ta på sig kortare uppdrag utan att avgifterna äter upp hela inkomsten.

Men kanske den största fördelen är friheten – du kan arbeta för vem som helst, var som helst. Det här har blivit extra relevant sedan distansarbete blivit normen för många yrkesgrupper efter pandemin.

Kort sagt: oavsett din erfarenhet eller expertis, finns det med största sannolikhet ett företag där ute som vill anlita dig.

Så hittar du jobb som betalar i krypto

Här är några plattformar där du kan hitta kryptobetalda uppdrag:

LaborX

LaborX är en jobbsajt som kopplar samman arbetsgivare och frilansare. Plattformen stödjer ett brett spektrum av kryptovalutor som betalning, och erbjuder allt från tillfälliga gig till heltidsjobb inom exempelvis dataanalys, marknadsföring och utveckling.

Bakom LaborX står ett blockchainföretag som även erbjuder HR-lösningar – vilket bidrar till en professionell och pålitlig upplevelse.

Jobs4Bitcoins

Jobs4Bitcoins är ett aktivt Reddit-forum där användare lägger upp jobberbjudanden eller presenterar sina tjänster. Trots namnet handlar det inte bara om Bitcoin – flera kryptovalutor används som betalning.

Plattformen är öppen och otroligt mångsidig, men kom ihåg att det inte finns någon granskning av arbetsgivare eller kandidater, så agera med försiktighet.

Blocklancer

Blocklancer fokuserar på Ethereum och är en marknadsplats där du kan hitta allt från innehållsskapande till blockchainprojekt. Om du föredrar en annan valuta än ETH kan du enkelt växla via appar som Tap.

Plattformen innehåller även ett system för att hantera tvister, vilket kan vara en trygghet för både uppdragsgivare och frilansare.

Bitfortip

Vill du inte ge dig in i traditionella uppdrag? Bitfortip låter användare få dricks i krypto för att ge bra idéer eller svar på frågor. Du kan bli belönad i Bitcoin, Bitcoin Cash, NANO eller Tezos.

PompCryptoJobs

En professionell och strukturerad plattform för dig som letar efter heltidsjobb inom kryptobranschen. Här hittar du roller som skribent, produktdesigner, utvecklare, analytiker – listan är lång.

Plattformen används av några av de största företagen i branschen och fokuserar uteslutande på roller som betalar i krypto.

Så får du betalt i krypto

Behöver du ett konto för att ta emot betalningar i Bitcoin eller andra kryptovalutor? Tap erbjuder konton där du enkelt kan ta emot både fiat- och kryptovalutor.

När du har öppnat ett konto får du tillgång till flera kryptoplånböcker och dedikerade IBAN-konton. Dela bara din plånboksadress med din uppdragsgivare – pengarna är inne inom några minuter, beroende på nätverket.

Med Tap-kortet kan du dessutom använda dina medel direkt i butik eller online, oavsett om du spenderar i fiat eller krypto. Smidigt, flexibelt och gränslöst.

.png)

BitDAO is building a decentralized token economy open to everybody. Managed by BIT token holders and one of the largest decentralized autonomous organizations (DAOs), BitDAO is committed to growing the DeFi ecosystem through partner projects and a decentralized economy.

What Is BitDAO?

BitDAO aims to create an accessible tokenized economy that provides support, such as research and development, liquidity bootstrapping and funding, to a wide range of partner projects across the DeFi, DAO, NFT and gaming space. Through co-development offers and token swaps, BitDAO aims to attract developer talent and build a sustainable treasury of top crypto coins.

BitDAO's ultimate goal is to create products that will not only improve BitDAO's efficiency and effectiveness, but also other DAOs. The core product comprises a series of both on-chain and off-chain governance solutions and products; with the latter, DAO treasury management would be able to deploy and monitor assets in order to earn yield.

Moreover, BitDAO plans on providing grants to different teams within the crypto industry for research or development purposes, all of which are voted on by members and given for the public good of cryptocurrency communities worldwide.

Through its DAO structure, the company does not rely on a traditional hierarchy to operate, instead, it is run by a group of token holders that contribute to the platform's development. Token holders are then rewarded in BIT tokens for participating.

Changes to the BitDAO protocol are proposed to the BIT token holders who then have the power to vote on whether these changes are implemented or rejected. While the platform's vision has been outlined, where it ends up will be decided on by governance suggestions and forum participation.

To sum it up, the people who hold BitDAO's tokens, investors, and members of its community will help shape BitDAO's vision which includes dedicating both financial and human resources to support DeFi's development.

What is the BitDAO Treasury?

Controlled by BIT token holders, the BitDAO Treasury is responsible for allocating funds as per decisions made by BIT token holders. The BitDAO Treasury also undertakes token swaps with emerging and existing projects with the intention to support them and incentivize the project's contribution to their success.

The BitDAO Treasury allocation was 30% of the projects initial 10 billion BIT total supply. Monthly contributions from Bybit and varying contributions from DeFi partners, determined by smart contracts, also contribute to the DAO treasury management solutions.

Who created the BitDAO platform?

In a unique move, the BitDAO platform has no founders. While being supported by big names such as Bybit, Peter Thiel, Pantera, Founders Fund and more, the project is entirely run by contributors holding BIT tokens. Bybit is recorded as being an early contributor and is believed to have contributed over $1 billion in funding to the initiative.

Taking the notion of decentralization to a new level, the project has no teams, leaders or companies behind its operations. All changes are proposed by individuals within the community and then voted on by BIT token holders.

How do the BitDAO core protocols work?

BitDAO is governed and administered by the holders of BIT tokens. It works on the DAO mechanism, a common governance structure within the crypto space. The DAO framework gives BIT token holders power over BitDAO decisions and actions through a system of voting on proposals.

The platform supports the following measures, which will only be executed if the proposal receives a positive vote through the DAO system.

- Financing or milestone development grants for development teams and R&D centers who create BitDAO solutions or assist partnered existing and emerging projects.

- Upgrades to BitDAO's fundamental protocols, notably governance and treasury management.

- Token swaps for current and new initiatives.

- The Treasury will deploy funds based on various tactics.

- Grants will be made available for blockchain technology projects, educational programs, as well as other services related to blockchain.

- Support in the way of cash flow through existing assets will be provided to partner initiatives.

There are three ways to get involved with BitDAO: contributing to the project, becoming a partner, or holding the tokens. Contributors and partners can be any DeFi or CeFi project looking to build the BitDAO ecosystem while token holders are considered to "own" the platform as they have the power to recommend and vote on BitDAO's growth strategies as well as the allocation of BitDAO's treasury resources.

Non-token holders are defined as community members and can have their say through the forum and social media channels. Here they can pitch their ideas, which BIT token holders can then choose to embrace.

What is the BIT token?

The BIT token is the native token of the BitDAO ecosystem. The governance token allows for off-chain vote aggregation and delegated voting and provides the opportunity for switching to on-chain governance in the future. The BIT token can best be compared to the COMP token in the Compound Finance ecosystem.

There is a maximum supply of 10,000,000,000 BIT tokens, with the BitDAO Treasury allocation accounting for 30% of these. Token holders technically possess these treasury tokens based on their share of BIT. I.e. if someone holds 10% of the total BIT supply, they have ownership of 10% of the Treasury's 30% supply, equating to an additional 1%.

How BIT token holders can leverage Tap

You can now easily incorporate BitDAO (BIT) into your crypto portfolio by using the Tap app. The Tap app has recently added BIT to the list of supported crypto tokens, allowing anyone to conveniently and securely access the BitDAO market and safely store their BIT tokens.

Users can buy BitDAO (BIT) with fiat currency or engage in token swaps with other supported cryptocurrencies on the platform, or they can use traditional payment methods like bank transfers. The integrated wallets on the platform also make it easy for users to store and manage their BIT cryptocurrency.

We are delighted to announce the listing and support of BitDao (BIT) on Tap !

BIT is now available for trading on the Tap mobile app. You can now Buy, Sell, Trade or hold BIT for any of the other asset supported on the platform without any pair boundaries. Tap is pair agnostic, meaning you can trade any asset for any other asset without having to worries if a "trading pair" is available.

We believe supporting BIT will provide value to our users. We are looking forward to continue supporting new crypto projects with the aim of providing access to financial power and freedom for all.

BitDAO is building a decentralized token economy open to everybody. Managed by BIT token holders and one of the largest decentralized autonomous organizations (DAOs), BitDAO is committed to growing the DeFi ecosystem through partner projects and a decentralized economy.

BitDAO is governed and administered by the holders of BIT tokens. It works on the DAO mechanism, a common governance structure within the crypto space. The DAO framework gives BIT token holders power over BitDAO decisions and actions through a system of voting on proposals.

Get to know more about BitDao (BIT) in our dedicated article here.

You’ve probably heard whispers about the "whales" swimming in the crypto seas. But these aren’t your typical marine mammals – they’re the ultra-wealthy folks and organizations holding massive amounts of digital currency.

What Exactly is a Crypto Whale?

So, what makes someone a crypto whale? There’s no hard-and-fast rule, but it generally comes down to owning a huge chunk of a coin’s total supply. We’re talking over 10% of the available coins for a particular cryptocurrency. That’s an ocean-sized wallet!

Take Bitcoin, for example. In May 2022, just four wallets controlled over 3% of all Bitcoin in existence. The top 100 wallets? They collectively held over 15%. Now that’s some serious whale power!

Bitcoin isn’t the only one with its share of whales. Dogecoin, the beloved meme coin, had a pretty wild concentration too. In 2022, just 15 addresses held nearly 52% of its total supply. Even Vitalik Buterin, the mastermind behind Ethereum, is considered an Ether whale thanks to his massive stake in the coin he created.

How Whales Make Waves

With that kind of buying power, whales can really make waves in the crypto marketplace. If a whale decides to sell off a giant chunk of their holdings, it creates a tidal wave of downward pressure on prices due to the sheer volume and lack of liquidity. Other crypto enthusiasts are always on the lookout for signs of an impending "whale dump," closely monitoring exchange inflows to spot potential dangers.

Here’s the twist, though – whales keeping their coins locked away actually reduces trading liquidity in the market since there are fewer coins actively circulating. Their massive idle fortunes are like icebergs weighing down the crypto ocean.

Tracking Whale Movements

Not every whale transaction is a sell-off. These giants could simply be migrating to new wallets, switching exchanges, or making monster-sized purchases. But you can bet experienced crypto folks keep a keen eye on those huge whale wallets, carefully tracking any ripples they make to navigate the ever-shifting tides of the market.

Whale Alert is a popular service that tracks these large transactions and reports them, often on Twitter. Whenever a whale makes a big move, it’s usually publicized quickly, giving everyone a heads-up on potential market changes.

Below is an example from Twitter from Whale Alert:

The Human Side of Whales

Behind these massive holdings are real people and organizations. Some whales are early adopters who bought into Bitcoin or other cryptocurrencies when they were cheap. Others are companies that have invested heavily in the belief that cryptocurrencies will continue to grow in value. For instance, Ethereum’s founder, Vitalik Buterin, is the biggest Ethereum whale because he holds a significant amount of the cryptocurrency he created.

How whales affect crypto's price

Price volatility can be increased by whales, particularly when they move a significant amount of one cryptocurrency in one go. For example, when an owner tries to sell their BTC for fiat currency, the lack of liquidity and enormous transaction size create downward pressure on Bitcoin's price. When whales sell, other investors become extremely vigilant, looking for hints of whether the whale is "dumping" their crypto (and whether they should do the same).

The exchange inflow mean, also known as the average amount of a certain cryptocurrency deposited into exchanges, is one of the most common indicators crypto investors look for. If the mean transaction volume rises above 2.0, it implies that whales are likely to start dumping if there are a large number of them using the exchange. This can be viewed by regular crypto traders as a time to act before losing any potential profit.

How whales effect liquidity

When it comes to learning about whales and liquidity, one must remember that while whales are generally considered neutral elements in the industry, when a large number of whales hold a particular cryptocurrency, instead of using it, this reduces the liquidity in the market due to there being fewer coins available.

What crypto whales mean to investors

In terms of the relationship between whales and investors, one must remember that there are various situations in which a person may transfer their cryptocurrency holdings. It's worth mentioning that moving one's assets doesn't always indicate that you're selling them; they might be switching wallets or exchanges, or making a major purchase.

Occasionally, whales may sell portions of their holdings in discrete transactions over a longer period to avoid drawing attention to themselves or generating market anomalies that send the price up or down unpredictably. This is why investors keep an eye on known whale addresses to check for the number of transactions and value. This is not necessarily a task that newbie investors need to actively be involved with, however, understanding the terms and how whale accounts can affect the market is recommended.

Why Whales Matter

Whether you love them or hate them, whales are a formidable force in the crypto world, shaping its dynamics in profound ways. These giants, whether they’re creators, collectors, or traders, have a tremendous impact across the digital waters. When they make a move, it can trigger monumental swells that ripple through the entire market.

By understanding whale activity, anyone involved in cryptocurrency can better navigate these choppy waters. Staying informed about whale movements helps both newbies and seasoned traders make smarter decisions and stay afloat in this ever-changing space. Keep an eye on these behemoths; their actions can significantly influence your crypto journey.

While tracking whale activity can offer valuable insights into the cryptocurrency market, it's important to complement this knowledge with expert advice. Consulting with a financial advisor can help you navigate the complexities of investing and ensure your strategies align with your personal financial goals and risk tolerance.