Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

As we explore the world of crypto assets, we take a look at the different types of crypto assets on the market and at the wide range of diversity in the new-age industry. As more people enter the market and start exchanging digital assets, the industry grows and expands to allow new variations.

Below we explore the vast diversity in the industry, from crypto assets used as money to ones that reward users for viewing a website. Each business offers a unique solution, and to navigate this we offer you guidance below.

What Are Crypto Assets?

The terms "crypto asset" and "cryptocurrency" can be used interchangeably. They both refer to a digital asset built using blockchain that can be transferred in a direct peer-to-peer manner. The first crypto asset to launch is Bitcoin, which entered (and created) the scene in 2009. Since then thousands of crypto assets have been created, each one with its own unique use case.

The Different Types Of Crypto Assets

While crypto assets might fall into one or more categories, each has its own set of rules and use cases.

Payment-Focused

These crypto assets can be used to pay for everyday goods and services or as a store of value (in some cases). These include the likes of Bitcoin (BTC), Ethereum (ETH), Litecoin (LTC), Bitcoin Cash (BCH), etc.

Stablecoins

Stablecoins are crypto assets that have their value pegged to a fiat currency or commodity. These crypto assets are designed to bypass the volatility synonymous with the crypto market. These include the likes of Tether (USDT) and USD Coin (USDC).

Privacy Coins

Privacy coins are digital assets that hide details of the transaction, such as the origin, destination and amount. These crypto assets offer untraceable monetary transfers. These include the likes of Monero (XMR) and ZCash (ZEC).

CBDCs

Central Bank Digital Currencies (CBDCs) are crypto assets built and maintained by banks. Used as digital currencies alongside the traditional currency, CBDCs are designed to provide a digital version of the local fiat to which the value is pegged.

Governance Tokens

Common among decentralized finance (DeFi) protocols, governance tokens provide holders with a say in the platform and in future updates.

Utility Tokens

Utility tokens will typically provide a service to the holder on the platform on which it was created. Commonly created using the ERC-20 token standard, utility tokens might represent a subscription on a platform or a use case specific to that ecosystem.

Non-Fungible Tokens

Non-fungible tokens, also known as NFTs, are crypto assets that cannot be used interchangeably and instead hold unique and rare properties. Each NFT represents a singular function that cannot be changed.

How Are Crypto Assets Created And Distributed?

Before crypto assets are created the project's intentions are generally circulated through a white paper. In this white paper, the asset's tokenomics will be outlined which will cover how the asset is created and distributed.

Bitcoin, for example, uses a Proof of Work consensus which means that new coins are entered into circulation through miners solving complex mathematical problems. The network was designed to only ever have 21 million coins created, and new coins are slowly entered into the system each time a miner verifies and adds a new block to the blockchain.

Ethereum on the other hand has no limit to the number of ETH that can be created. The platform is currently moving from a PoW to a Proof of Stake consensus, which alters the way in which transactions are verified, however, new coins still enter circulation through verifying transactions.

XRP minted all its coins prelaunch and slowly release them into the system through a central authority while Tether creates USDT on demand. For each $1 sent, 1 USDT is created, which can later be removed from circulation should it be sold.

The Future Of Crypto Assets

With the ICO Boom in 2017, the DeFi boom in 2020 and the more recent NFT Craze, crypto assets aren't going anywhere. With constant innovation and increasing adoption, crypto assets have become an integral part of the modern day financial landscape.

While mainstream adoption is on the rise, a few wrinkles still need to be ironed out. For one, regulatory bodies around the world are working toward creating legal frameworks in which these crypto assets can exist, while centralized banks are exploring whether CBDCs can co-exist with their physical counterparts. While the world seeks to figure these out, one this is for certain: crypto assets are here, and the industry is becoming bigger by the day.

The financial world is undergoing a significant transformation, largely driven by Millennials and Gen Z. These digital-native generations are embracing cryptocurrencies at an unprecedented rate, challenging traditional financial systems and catalysing a shift toward new forms of digital finance, redefining how we perceive and interact with money.

This movement is not just a fleeting trend but a fundamental change that is redefining how we perceive and interact with money.

Digital Natives Leading the Way

Growing up in the digital age, Millennials (born 1981-1996) and Gen Z (born 1997-2012) are inherently comfortable with technology. This familiarity extends to their financial behaviours, with a noticeable inclination toward adopting innovative solutions like cryptocurrencies and blockchain technology.

According to the Grayscale Investments and Harris Poll Report which studied Americans, 44% agree that “crypto and blockchain technology are the future of finance.” Looking more closely at the demographics, Millenials and Gen Z’s expressed the highest levels of enthusiasm, underscoring the pivotal role younger generations play in driving cryptocurrency adoption.

Desire for Financial Empowerment and Inclusion

Economic challenges such as the 2008 financial crisis and the impacts of the COVID-19 pandemic have shaped these generations' perspectives on traditional finance. There's a growing scepticism toward conventional financial institutions and a desire for greater control over personal finances.

The Grayscale-Harris Poll found that 23% of those surveyed believe that cryptocurrencies are a long-term investment, up from 19% the previous year. The report also found that 41% of participants are currently paying more attention to Bitcoin and other crypto assets because of geopolitical tensions, inflation, and a weakening US dollar (up from 34%).

This sentiment fuels engagement with cryptocurrencies as viable investment assets and tools for financial empowerment.

Influence on Market Dynamics

The collective financial influence of Millennials and Gen Z is significant. Their active participation in cryptocurrency markets contributes to increased liquidity and shapes market trends. Social media platforms like Reddit, Twitter, and TikTok have become pivotal in disseminating information and investment strategies among these generations.

The rise of cryptocurrencies like Dogecoin and Shiba Inu demonstrates how younger investors leverage online communities to impact financial markets2. This phenomenon shows their ability to mobilise and drive market movements, challenging traditional investment paradigms.

Embracing Innovation and Technological Advancement

Cryptocurrencies represent more than just investment opportunities; they embody technological innovation that resonates with Millennials and Gen Z. Blockchain technology and digital assets are areas where these generations are not only users but also contributors.

A 2021 survey by Pew Research Center indicated that 31% of Americans aged 18-29 have invested in, traded, or used cryptocurrency, compared to just 8% of those aged 50-64. This significant disparity highlights the generational embrace of digital assets and the technologies underpinning them.

Impact on Traditional Financial Institutions

The shift toward cryptocurrencies is prompting traditional financial institutions to adapt. Banks, investment firms, and payment platforms are increasingly integrating crypto services to meet the evolving demands of younger clients.

Companies like PayPal and Square have expanded their cryptocurrency offerings, allowing users to buy, hold, and sell cryptocurrencies directly from their platforms. These developments signify the financial industry's recognition of the growing importance of cryptocurrencies.

Challenges and Considerations

While enthusiasm is high, challenges such as regulatory uncertainties, security concerns, and market volatility remain. However, Millennials and Gen Z appear willing to navigate these risks, drawn by the potential rewards and alignment with their values of innovation and financial autonomy.

In summary

Millennials and Gen Z are redefining the financial landscape, with their embrace of cryptocurrencies serving as a catalyst for broader change. This isn't just about alternative investments; it's a shift in how younger generations view financial systems and their place within them. Their drive for autonomy, transparency, and technological integration is pushing traditional institutions to innovate rapidly.

This generational influence extends beyond personal finance, potentially reshaping global economic structures. For industry players, from established banks to fintech startups, adapting to these changing preferences isn't just advantageous—it's essential for long-term viability.

As cryptocurrencies and blockchain technology mature, we're likely to see further transformations in how society interacts with money. Those who can navigate this evolving landscape, balancing innovation with stability, will be well-positioned for the future of finance. It's a complex shift, but one that offers exciting possibilities for a more inclusive and technologically advanced financial ecosystem. The financial world is changing, and it's the young guns who are calling the shots.

Money talks, but some currencies whisper so quietly you need a magnifying glass to hear them. In the grand theatre of global finance, not all currencies are created equal, while some strut around like peacocks (looking at you, Kuwaiti Dinar), others shuffle about with the confidence of a wet paper bag.

The Lebanese Pound (LBP) currently holds the unfortunate distinction of being the world's weakest currency in 2025, with an exchange rate so low that one U.S. dollar equals approximately 89,500 Lebanese pounds. To put this in perspective, you'd need a small suitcase to carry the equivalent of $100 in Lebanese pounds, assuming you could find enough physical notes.

Currency weakness isn't just about having a lot of zeros after the decimal point. It reflects a complex web of economic factors, including inflation rates, political stability, monetary policy decisions, and investor confidence. This guide on the world's weakest currencies in 2025, explores the economic stories behind their struggles and what it means for the countries (and the people) who use them.

Top 10 weakest currencies in the world (2025)

Here's the lineup of currencies that make your wallet feel surprisingly heavy when travelling abroad:

Exchange rates are approximate and fluctuate daily. Data compiled from multiple financial sources as of July 2025.

What makes a currency weak?

Before we roll our eyes at long strings of zeros, let’s get clear on what actually drives currency weakness.

Exchange rates show how much of one currency you need to buy another, usually measured against the U.S. dollar. But a low exchange rate isn’t automatically a red flag. Just like shoe sizes, bigger numbers aren’t necessarily worse, they’re just different.

The real reasons a currency weakens?

- Persistent inflation that eats away at value

- Short-term monetary policies that undermine long-term confidence

- Trade imbalances and shrinking foreign reserves

- Political instability that rattles investor trust

When investors lose faith, money moves fast, and exchange rates feel the impact. In short, weak currencies aren’t a punchline, they’re a signal of deeper economic tension.

Country spotlights - case studies behind the weakest currencies

Lebanon | A financial collapse without precedent

Lebanon’s currency crisis is a case study in how not to run an economy. As of mid-2025, the Lebanese pound trades at over 89,500 LBP per USD, making it one of the weakest currencies in the world.

The collapse stemmed from a banking sector that functioned like a state-sponsored Ponzi scheme: banks attracted deposits with sky-high interest rates, only to lend most of those funds to a debt-laden government. When confidence evaporated, the system imploded. Add in the 2019 mass protests and the devastating 2020 Beirut port explosion, and the result was economic freefall.

Today, Lebanese citizens navigate a surreal economy where ATMs limit withdrawals to tiny amounts, and many businesses have shifted to unofficial dollar pricing. A shadow economy thrives alongside the official one, proof that when trust in institutions fails, people find their own workarounds.

Iran | Sanctions, inflation, and isolation

The Iranian rial now trades at over 1,000,000 IRR per USD (yes, that's six zeros). Sanctions have cut Iran off from the global financial system, leaving its oil-rich economy unable to fully monetise its most valuable resource.

It's like owning a garage full of Ferraris with no keys to drive them. In response, Iran has attempted to bypass sanctions with crypto experiments and barter agreements, but none have stabilised the currency.

Inflation routinely exceeds 40%, and as a result Iranians have turned to gold, property, and U.S. dollars to preserve what little value they can. In a country known for its resilience, the rial’s collapse remains a stark reminder of the long-term costs of economic isolation.

Vietnam | Weak by design, not disaster

The Vietnamese dong trades at around 26,000 VND per USD, but that doesn’t signal a crisis, it actually reflects deliberate policy. Vietnam maintains a weaker currency to keep exports competitive, a strategy known as competitive devaluation.

This has helped transform Vietnam into a global manufacturing hub, attracting companies looking to diversify away from China. It's like running a permanent sale on your national output - foreign buyers love the prices, and Vietnamese factories stay busy.

The challenge lies in balance. The government works to avoid the inflation traps that have plagued other countries on this list, proving that not all weak currencies come from failure, some are tools of long-term economic strategy.

Laos | Trapped by debt and dependency

The Laotian kip now trades at around 21,800 LAK per USD, weighed down by inflation above 25% and a debt-to-GDP ratio over 125%. Much of that debt is owed to China, tied to major infrastructure projects that haven’t yet paid off economically.

Laos is a landlocked nation with limited industrial capacity and high import dependence, leaving its currency exposed whenever commodity prices shift. With little monetary wiggle room, the kip’s trajectory reflects deeper economic vulnerabilities.

Sierra Leone | A currency redefined, but still fragile

In 2022, Sierra Leone redenominated its currency, removing three zeros from the leone to simplify transactions. But even the new leone remains weak due to decades of disruption: civil war, the Ebola outbreak, COVID-19, and swings in diamond prices.

This is an economy that's faced shock after shock, and recovery is slow. The mining sector, especially diamonds, still dominates, leaving the leone vulnerable to commodity price drops.

Healthcare challenges and limited infrastructure add even more pressure, reducing productivity and increasing fiscal strain. The leone’s weakness tells the story of a country rebuilding piece by piece, with its currency reflecting both the past and the uphill path ahead.

Why some countries choose to keep their currency weak

Believe it or not, some countries actually prefer their currencies to be weaker - and for good economic reasons. It's counterintuitive, like preferring to drive in the slow lane, but the strategy can be remarkably effective.

Export competitiveness represents the primary motivation. A weaker currency makes domestic products cheaper for foreign buyers, essentially providing a permanent discount. German cars might be excellent, but if Vietnamese motorcycles cost 70% less due to currency differences, guess which ones developing countries will buy?

Countries like China famously maintained an artificially weak currency for decades, helping fuel their manufacturing boom. The strategy worked so well that other countries accused them of "currency manipulation" - the economic equivalent of being too good at a game and getting accused of cheating.

However, this approach carries significant risks. Import costs rise dramatically, making everything from oil to smartphones more expensive for domestic consumers

Long-term currency weakness can also trigger capital flight, where wealthy citisens move their money abroad. When your own citisens don't trust your currency, convincing foreigners becomes considerably more challenging.

Does a weak currency mean a weak economy?

We’ve established that a weak currency doesn't automatically signal economic disaster,sometimes it's just a reflection of different economic structures and historical circumstances.

Indonesia and Vietnam serve as the best examples of countries with numerically weak currencies but relatively strong economies. Both nations have achieved consistent growth, reduced poverty, and built increasingly diversified economies despite their currencies requiring calculators to count properly.

The key lies in purchasing power parity - what matters isn't how many zeros follow your currency symbol, but what those zeros can actually buy. A Vietnamese worker earning 10 million dong monthly isn't necessarily poor if that amount provides a comfortable living standard within the Vietnamese economy.

The real measure of economic health involves factors like employment rates, productivity growth, infrastructure development, and living standards. A country with a weak currency but growing wages, improving infrastructure, and expanding opportunities may be economically healthier than a nation with a strong currency but declining industries and rising unemployment.

What are the consequences of a weak currency?

In essence, a weak currency makes daily life more expensive, with rising prices on imports like food, fuel, and electronics. Added into the mix, Inflation erodes savings, and capital flight accelerates as people move their money into more stable currencies.

Over time, foreign currencies may replace the local one in everyday use, limiting government control. Internationally, weak currencies hurt credit ratings and investor confidence, reinforcing instability.

Final thoughts

Currency weakness is more than just numbers, it’s a signal. We’ve learnt above that it can both expose deep economic flaws or reflect deliberate strategies for growth. Lebanon and Iran highlight how instability and isolation can erode value fast, while Vietnam shows how weakness can fuel exports and development.

These disparities then shape the country’s trade, capital flows, and financial stability worldwide, causing a wider ripple effect. In a global economy, no currency moves alone; each affects the rest. And behind every weak currency are real people navigating inflation, opportunity, or uncertainty.

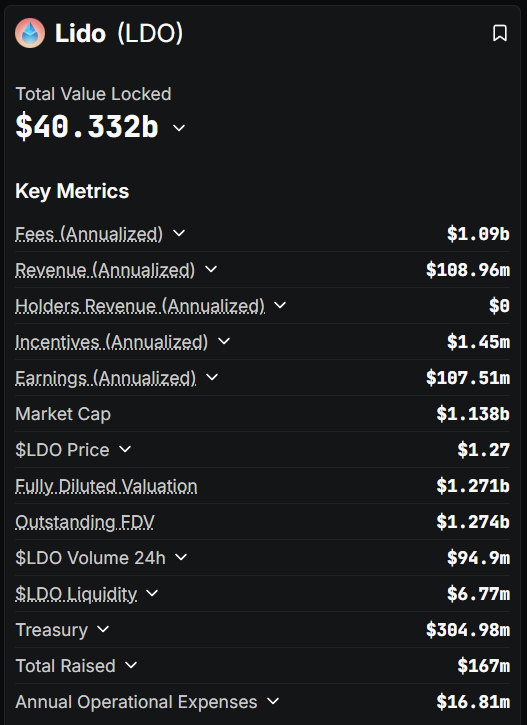

If you’re interested in staking Ethereum, you came to the right place. The largest liquid staking protocol in the crypto ecosystem, trusted by thousands of ETH holders who want rewards without losing liquidity, has a name: Lido DAO.

Ethereum's Leading Liquid Staking Protocol

How does it work?

Lido DAO is a decentralized autonomous organization that provides a liquid staking solution on the Ethereum 2.0 blockchain as well as other Proof of Stake (PoS) platforms like Solana (SOL), Polygon (MATIC), Polkadot (DOT), and Kusama (KSM).

Instead of locking up funds, users stake ETH and receive stETH tokens in return, which represent their staked ETH plus accrued rewards. This allows users to continue trading, lending, or using their tokens across DeFi while still benefiting from staking yields. Since launching in 2020, Lido DAO has grown to manage more than $40.33B in Total Value Locked (TVL), with staking rewards currently averaging an annual percentage rate (APR) of 2.71%. The protocol is governed by holders of the LDO token, ensuring community-driven decision-making.

Where did it come from?

Lido DAO was co-founded by Kasper Rasmussen and Jordan Fish, also known as CryptoCobain. Behind the Lido DAO are a number of individuals and organizations that are well-regarded within the DeFi space. Since its inception in December 2020, shortly after ETH 2.0's release, the platform has been overseen by the Lido DAO, with several key members including Semantic VC, Chorus, ParaFi Capital, P2P Capital, Libertus Capital, Terra, StakeFish, Bitscale Capital, StakingFacilities, and KR1. Several of the highly esteemed angel investors include Stani Kulechov of Aave, Banteg of Yearn, Will Harborne of Deversifi, Julien Bouteloup from Stake Capital, and Kain Warwick from Synthetix.

Since then, Lido DAO has gained an impressive reputation for its liquid staking capabilities, and now boasts over $13 billion in staked assets. Its core focus is on Ethereum, yet its horizons are expanding to other blockchain networks including Terra and Solana, both of which launched staking capabilities in 2021, as well as several other layer 1 PoS blockchains.

Liquid Staking Made Simple

Lido DAO simplifies staking into a three-step process: deposit ETH, receive stETH, and start earning rewards automatically. When a user deposits ETH, the protocol delegates funds to a decentralized network of professional node operators. There are over 800 node operators worldwide, who manage validation securely and efficiently.

The stETH tokens received are liquid ERC-20 assets whose value increases over time as rewards accumulate. With one-click staking through Lido DAO’s interface, users can skip the hassle of running their own validator while enjoying a 98.2% validator performance.

How validator rewards are earned from staked assets

So, in order to stake ETH, become a validator and earn rewards for validating payments on the Ethereum platform, users are required to stake a minimum of 32 ETH tokens. What if I don’t have 32 ETH? You may ask. To bypass this minimum requirement and still earn rewards, Lido DAO allows users to stake a fraction of this amount and earn a proportionate amount of block rewards.

Users will then deposit ETH into the Lido smart contract and receive the same number of stETH. These tokens are minted once the funds have been received and are burned when the users withdraw their original ETH. The staked funds will then be distributed to the validators on the Lido network and deposited into the Ethereum Beacon Chain from where they will be secured in a smart contract.

The Lido DAO will then assign, onboard, support and enter the validators' addresses to the smart contract registry before being given a set of keys for the validation. All ETH that users have deposited on the Lido platform will be split into groups of 32 ETH among the active Lido node operators who will use this public validation key to validate transactions. The block rewards will then be shared proportionately.

Notably, this distribution process of sharing staked assets eliminates single-point-of-failure risks common among single-validator staking.

Your Liquid Staking Asset

At the center of Lido DAO’s system is stETH, the tokenized representation of staked ETH. stETH trades on major exchanges, offering deep liquidity and integration with several DeFi protocols. Staking rewards are earned automatically, so users never need to claim manually.

Users can stake any amount of ETH to the Beacon Chain without having to deal with lock-up requirements or withdrawal delays. This way Ethereum holders can enjoy both liquidity and yield simultaneously. For providing this staked ETH service, a 10% fee is collected by Lido for each process.

DeFi Integration Opportunities

For advanced users, stETH unlocks a wide range of yield optimization strategies. Lending platforms like AAVE accept stETH as collateral, while liquidity pools on CURVE and UNISWAP offer additional yield opportunities. Leveraged staking strategies also allow users to compound rewards further.

Proven Security

Security and safety are central to Lido DAO's success. Since the beginning, the protocol has undergone a dramatic array of independent audits, conducted by top-tier firms including Statemind, Certora, Hexens, Oxorio, MixBytes, and Ackee Blockchain.

Importantly, Lido DAO has never suffered a major protocol-wide hack. The protocol takes advantage of open-source code, multisig governance, and safeguards like GateSeal for emergency pauses, deposit security modules, and DAO oversight to anticipate and mitigate emerging threats. These layers of defense, combined with a multi-validator, geographically distributed network, reduce single points of failure.

What is Lido DAO token (LDO)?

Governance of the Lido DAO is powered by the LDO token, which grants voting rights to its holders. With a market capitalization of $1.14B and an all time high (ATH) price of $2.38 USD, LDO plays a central role in shaping the protocol’s future. Token holders vote on proposals, influence fee structures, and participate in selecting node operators. The governance community is highly active, with regular proposals and ongoing discussions that ensure the protocol evolves in a decentralized and transparent way.

How to buy Lido LDO?

Staking with Lido DAO is meant to be as accessible as possible. There are no minimum deposit requirements; end users can stake any amount of ETH. You can connect an Ethereum wallet, confirm the transaction, and receive stETH instantly.

If you're looking to expand your digital currencies portfolio, LDO tokens can be a potential addition. The Tap app provides an easy and secure way for anyone with an account to add these tokens to their portfolios in no time, making it one of the most effortless trading experiences around.

You can utilize the Tap app to access the Lido ecosystem by purchasing LDO tokens with either crypto or fiat currencies. End users can then choose to store their LDO tokens securely in the integrated crypto wallet or transfer them to the Lido platform and engage in the platform's earning potential. All you need to do to get started is download the app and create an account in minutes.

Despite radically reshaping the world’s financial landscape, the first ever cryptocurrency has limitations when interacting with newer blockchains. For example, Ethereum. Wrapped Bitcoin (WBTC) solves this limitation by allowing Bitcoin to function on the Ethereum network, enabling access to decentralized finance (DeFi) services.

WBTC is an ERC-20 token that represents Bitcoin 1:1 on the Ethereum blockchain, combining Bitcoin’s value with Ethereum’s smart contract power, and opening new opportunities for BTC holders in decentralized finance (DeFi). Unlike Bitcoin variants aiming to improve its technology, WBTC extends Bitcoin's utility without replacing it.

Join us in this deep dive on how WBTC works, its benefits, risks, and how it connects Bitcoin to the broader DeFi ecosystem.

Unlocking Bitcoin’s Power on Ethereum

Launched in January 2019, approximately 10 years after Bitcoin's initial release, WBTC was created as a collaborative effort between BitGo, Kyber Network, and Ren (formerly Republic Protocol), along with other major players in the DeFi space including MakerDAO, Dharma, and Set Protocol.

As an ERC-20 token, WBTC adheres to Ethereum's token standard, making it compatible with the entire Ethereum ecosystem, including its smart contracts, decentralized applications, and wallets.

In structure, WBTC bears similarities to stablecoins like USDC or USDT, which are backed by reserve assets. However, while stablecoins aim to maintain a stable value (usually pegged to a fiat currency like the US dollar), WBTC's value fluctuates with Bitcoin's market price.

Each WBTC token is backed by an equivalent amount of Bitcoin (BTC) held in reserve by a custodian, maintaining a strict 1:1 ratio, meaning 1 WBTC is always equivalent to 1 BTC in value.

Wrapped Bitcoin is now under the control of a Decentralized Autonomous Organization (DAO) called the WBTC DAO. This organization oversees the protocol, ensuring the integrity of the wrapping process and maintaining transparency in the system. Unlike Bitcoin's fully decentralized nature, WBTC relies on certain trusted entities to maintain the backing of the tokens, which creates an interesting balance between utility and trustworthiness.

WBTC belongs to a broader category of financial instruments known as "wrapped tokens." These are cryptocurrencies that are enclosed or "wrapped" in a digital vault and represented as another token on a different blockchain. While WBTC represents Bitcoin on Ethereum, there are other wrapped tokens in the cryptocurrency space, including Wrapped Ether (WETH) which, somewhat paradoxically, is a wrapped version of Ethereum's native token on its own blockchain that conforms more strictly to the ERC-20 standard.

Why Does Wrapped Bitcoin Exist?

Wrapped Bitcoin (WBTC) was created to bridge the gap between Bitcoin and newer blockchain platforms like Ethereum.

1. Bitcoin's limited smart contract functionality

Bitcoin prioritizes security over programmability, making it unsuitable for complex decentralized apps. In contrast, Ethereum supports smart contracts that power a wide range of automated financial services.

2. Access to DeFi for Bitcoin holders

Ethereum's DeFi ecosystem offers lending, trading, and yield farming, but Bitcoin holders couldn't participate without converting their BTC. WBTC solves this, letting them use Bitcoin's value within Ethereum-based applications.

3. Unlocking Bitcoin's liquidity

Bitcoin's vast market capitalization holds significant untapped liquidity. WBTC brings this capital into Ethereum's DeFi network, benefiting both Bitcoin holders and the broader ecosystem.

4. Faster, more flexible Bitcoin transactions

While Bitcoin transactions can be slow and costly, WBTC uses Ethereum's network for quicker, cheaper trades-ideal for active traders and DeFi users.

In short, WBTC enhances Bitcoin's utility without altering its core protocol, connecting it to the evolving world of decentralized finance.

How Does Wrapped Bitcoin Work? The Nuts and Bolts

Wrapped Bitcoin (WBTC) bridges Bitcoin and Ethereum through a secure, transparent process involving key participants and smart contracts.

1. Wrapping and unwrapping process:

Wrapping (BTC → WBTC): Users send Bitcoin to a custodian, who secures it and mints an equivalent amount of WBTC on Ethereum, sending it to the user's Ethereum wallet.

Unwrapping (WBTC → BTC): Users burn WBTC, prompting the custodian to release the equivalent Bitcoin back to their Bitcoin wallet.

This 1:1 pegging ensures WBTC is fully backed by Bitcoin reserves.

2. Key participants:

Custodians (e.g., BitGo): Hold and safeguard the Bitcoin backing WBTC.

Merchants: Authorized to request minting or burning of WBTC.

Users: Individuals or entities using WBTC in Ethereum's DeFi ecosystem.

WBTC DAO Members: Stakeholders who govern protocol decisions.

3. Transparency and verification:

Proof of reserves: Publicly verifiable Bitcoin addresses back every WBTC in circulation.

On-chain verification: Minting and burning are recorded on both blockchains.

Regular attestations: Independent checks confirm reserve accuracy.

4. Technical implementation:

WBTC is built as an ERC-20 token, Ethereum’s standard for fungible tokens. All ERC-20 tokens follow the same set of rules, which makes them interchangeable, easy to trade, and instantly compatible with most Ethereum wallets and DeFi apps.

This makes WBTC easily transferable, compatible with wallets, and usable in DeFi apps like lending platforms, decentralized exchanges, and yield farming protocols. It gives Bitcoin the same programmability and utility as Ethereum-native assets.

Showdown: Wrapped Bitcoin (WBTC) vs. Bitcoin (BTC)

Although WBTC and BTC share the same value, their use cases differ. Bitcoin is designed for security, immutability, and censorship resistance. WBTC, on the other hand, thrives in Ethereum’s ecosystem where smart contracts enable lending, borrowing, and trading.

For storing wealth long-term, Bitcoin remains the go-to. For generating yield or accessing DeFi, WBTC is the practical choice. Different uses for different needs.

How Wrapped Bitcoin Boosts Your Crypto

1. DeFi accessibility:

WBTC lets users leverage Bitcoin in DeFi platforms for:

Lending & borrowing: Use WBTC as collateral on platforms like Aave or Compound to earn interest or borrow assets.

Yield farming: Provide WBTC liquidity for rewards, often surpassing Bitcoin's passive holding returns.

Liquidity provision: Earn trading fees by adding WBTC to pools on exchanges like Uniswap.

Synthetic assets: Mint assets pegged to traditional markets using WBTC as collateral.

2. Enhanced liquidity:

WBTC boosts capital efficiency across Ethereum by:

Expanding DeFi liquidity: Unlocking Bitcoin's market value to strengthen liquidity pools.

Reducing slippage: Deeper markets enable smoother trades.

Providing stable collateral: Bitcoin-backed assets offer trusted options for DeFi protocols.

3. Transaction advantages:

Compared to Bitcoin, WBTC transactions on Ethereum benefit from:

Faster confirmations: Ethereum's ~12-second block times outpace Bitcoin's 10-minute average.

Predictable fees: Ethereum's fee structure can be more cost-effective in certain conditions.

Smart contract integration: WBTC supports complex transactions Bitcoin's network can't handle.

4. Broader utility:

Beyond DeFi, WBTC enhances user options by:

Accessing smart contracts: Participate in advanced applications without selling Bitcoin.

Composability: Use WBTC across multiple protocols simultaneously.

Simplified management: Store WBTC alongside other Ethereum assets in common wallets.

Gaming & NFTs: Spend WBTC in blockchain games or NFT marketplaces.

While WBTC offers significant opportunities, it comes with trade-offs regarding decentralization and security, as covered in the next section.

Navigating Wrapped Bitcoin: Risks and Challenges

Custodial risks

While WBTC brings Bitcoin into DeFi, it introduces centralization as well. WBTC depends on BitGo as the sole custodian to hold the backing Bitcoin, creating a central point of failure. Users must trust these custodians to safeguard funds, process redemptions, and comply with regulations that could freeze assets or restrict conversions.

BitGo, DAO member and sole custodian. Source.

Smart contract risks

WBTC relies on Ethereum smart contracts, which, despite audits, can still have vulnerabilities or coding flaws. It's also affected by Ethereum network issues like congestion, high gas fees, and risks from interacting with DeFi platforms.

Price and market risks

WBTC tracks Bitcoin's price and shares its volatility. In turbulent markets, it may trade slightly above or below Bitcoin's value. Large conversions can strain liquidity, making big trades harder without impacting price.

Operational challenges

Managing WBTC involves both Bitcoin and Ethereum blockchains, which can be complex for newcomers. High Ethereum gas fees and slow WBTC-to-Bitcoin conversions (especially for large transactions) are additional hurdles.

Alternatives with less trust required

Some users prefer fully decentralized options like native Bitcoin, though it lacks smart contract functionality. Other wrapped Bitcoin solutions use different technologies to reduce reliance on custodians.

Wrapping Up WBTC

WBTC represents a shift in the cryptocurrency space, bridging the gap between Bitcoin's unparalleled network security and store-of-value properties with Ethereum's programmability and vibrant DeFi landscape. Since its launch in 2019, WBTC has grown from a novel concept to a cornerstone of cross-chain interoperability, enabling countless new use cases for Bitcoin holders.

For users, WBTC allows exposure to Bitcoin while engaging with decentralized finance (DeFi) on Ethereum and other platforms, enabling participation in both without choosing between them. While for DeFi, Bitcoin's liquidity has fostered growth, stability and asset diversity. WBTC has also paved the way for other wrapped assets, making the crypto ecosystem more interconnected and efficient.

As blockchain technology evolves, solutions like WBTC will address limitations while retaining core utility. Its success shows how cryptocurrency innovation can build upon existing strengths without replacing them.

Other Wrapped Bitcoin alternatives

While WBTC is the most widely used Bitcoin representation on Ethereum, several alternatives have emerged, each with different approaches to the bridge between Bitcoin and other blockchains:

- renBTC

- tBTC

- sBTC (Synthetic BTC)

- HBTC

- pBTC

How Can I Buy Wrapped Bitcoin (WBTC)?

If you’re looking to bring Bitcoin into the world of Ethereum, Wrapped Bitcoin (WBTC) is the gateway you might be looking for. Through the Tap app, users can easily add WBTC to their portfolios, opening up access to Ethereum’s thriving DeFi ecosystem. Getting started is simple: just download the app, create an account, and start trading WBTC in minutes.