Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

Solana est une blockchain ultra-performante qui repose sur un mécanisme de consensus unique, lui permettant d’assurer à la fois une grande rapidité d’exécution et un haut niveau de sécurité. Grâce à sa facilité d’utilisation, la plateforme séduit déjà de grandes entreprises. En découvrant ensemble ce qu’est Solana (SOL), nous allons explorer les objectifs du projet, ses réussites, et comprendre pourquoi elle est souvent surnommée la "Ethereum killer".

Depuis la création du Bitcoin en 2009, tout un écosystème crypto s’est développé, atteignant près de 1 200 milliards de dollars de valorisation au moment de la rédaction de cet article. Si le Bitcoin a été imaginé comme un système de paiement mondial visant à résoudre certaines limites du système financier traditionnel, des plateformes comme Ethereum, et désormais Solana, ont vu le jour pour élargir les horizons de la blockchain grâce à des fonctionnalités programmables.

Qu'est-ce que Solana (SOL) ?

Reconnue comme l’un des protocoles les plus dynamiques dans l’univers de la DeFi, Solana est une plateforme destinée aux développeurs souhaitant créer des applications décentralisées (dapps) et des smart contracts, à l’image d’Ethereum. Ce qui différencie Solana, c’est sa vitesse impressionnante et ses frais de transaction particulièrement bas.

Le projet est porté par deux entités principales : la Solana Foundation, une organisation à but non lucratif basée en Suisse qui promeut la plateforme et collabore avec des partenaires internationaux, et Solana Labs, basée à San Francisco, qui pilote le développement technologique du projet.

Solana adopte également une approche innovante pour soutenir un écosystème crypto plus respectueux de l’environnement. En plus du mécanisme de consensus Proof-of-Stake (PoS), la plateforme utilise aussi le Proof-of-History (PoH), un système inventé par l’un de ses fondateurs.

Le PoH révolutionne le fonctionnement des blockchains en permettant à Solana de traiter jusqu’à 65 000 transactions par seconde. À titre de comparaison, Ethereum en traite environ 30 par seconde. Ce mécanisme fonctionne comme une "horloge cryptographique", qui intègre la notion de temps directement dans la structure des données du réseau.

Réputée pour être l'une des blockchains programmables les plus rapides au monde, Solana a su fédérer une communauté solide. On retrouve aujourd’hui des entreprises de secteurs variés, de la finance au voyage, qui utilisent la plateforme, ainsi qu’un vif intérêt pour les tokens SOL, la cryptomonnaie native de l’écosystème.

Les caractéristiques clés de Solana

Solana se démarque dans l’industrie grâce à plusieurs fonctionnalités clés, qui ont contribué à son adoption massive :

Scalabilité

La plateforme est capable de gérer des milliers de transactions par seconde, grâce à des technologies avancées comme le traitement parallèle et les unités de traitement basées sur le mempool.

Smart contracts

Solana prend en charge les smart contracts, offrant aux développeurs la possibilité de créer et faire fonctionner des applications décentralisées.

Consensus Proof of Stake (PoS)

Solana combine le PoS avec le Proof of History (PoH) pour accélérer les transactions, valider rapidement les opérations, et confirmer les blocs en un temps record.

Finance décentralisée (DeFi)

Grâce à des transactions rapides et à faible coût, Solana est devenue une favorite dans la DeFi, facilitant des activités comme le prêt, le trading, ou encore le yield farming.

Qui a créé Solana ?

L’ingénieur logiciel Anatoly Yakovenko est le créateur de Solana. Il a commencé à travailler sur le projet en 2017, soit trois ans avant son lancement officiel, aux côtés de ses anciens collègues Greg Fitzgerald et Eric Williams. Ensemble, avec d’autres experts de la tech, ils ont conçu la plateforme programmable que nous connaissons aujourd’hui.

Anatoly Yakovenko est également à l’origine du protocole Proof of History (PoH), une innovation majeure qui permet d’augmenter la scalabilité et d’améliorer l’utilité de la blockchain. Son expertise a eu un impact considérable sur l’industrie.

En quoi Solana est-elle différente d’Ethereum ?

L’un des principaux objectifs de Solana est d’améliorer certaines limitations techniques d’Ethereum. Elle se distingue notamment par la vitesse de ses transactions, sa capacité de traitement élevée, et des frais bien plus compétitifs. Tout cela fait de Solana un choix privilégié pour ceux qui recherchent efficacité et performance.

Scalabilité

Les responsables du projet estiment que Solana pourrait à terme gérer jusqu’à 700 000 transactions par seconde, mais actuellement, elle atteint déjà environ 65 000 TPS, bien au-delà des 30 TPS d’Ethereum.

Solana est l’une des rares solutions de couche 1 à pouvoir prendre en charge des milliers de transactions par seconde sans avoir recours à des solutions off-chain ou de seconde couche.

Coût

La structure du réseau Solana permet de proposer des frais de transaction ultra-compétitifs, tournant autour de 0,000125 $ par transaction. En comparaison, Ethereum facture environ 0,0005 $ par opération au moment de la rédaction.

Qu’est-ce que le SOL ?

SOL est la cryptomonnaie native de la plateforme Solana, alimentant la scalabilité et la structure économique du réseau. Ce token utilitaire est utilisé pour payer les frais de transaction et pour sécuriser le réseau via le staking.

SOL repose sur le mécanisme de preuve d’enjeu (PoS), où les participants du réseau sécurisent la blockchain en stakant leurs tokens. Son prix est influencé par divers facteurs classiques tels que les évolutions du projet, la dynamique du marché, ou l’activité sur les plateformes d’échange, mais aussi par des éléments spécifiques comme le taux d’inflation du token, les montants brûlés et l’expansion de l’écosystème Solana.

Comment acheter du SOL ?

Si vous envisagez d’ajouter Solana à votre portefeuille crypto, l’application Tap est là pour ça. Elle vous permet d’acheter, vendre, échanger et stocker du SOL en toute simplicité. Que ce soit avec des cryptos ou de la monnaie fiduciaire, vous pouvez facilement accéder à ce marché en pleine croissance et rejoindre la révolution blockchain portée par Solana.

Pour en savoir plus sur la façon d’échanger du Solana, consultez les ressources disponibles sur le blog de Tap.

Le slippage peut faire toute la différence dans vos résultats de trading. Il représente l’écart entre le prix que vous pensiez payer et le prix réel au moment de l’exécution d’un ordre. Voici tout ce que vous devez savoir pour comprendre ce phénomène, gérer le risque et l’éviter autant que possible.

C’est quoi le slippage en crypto ?

Le slippage se produit lorsqu’un ordre d’achat ou de vente est exécuté à un prix différent de celui initialement affiché, en raison de mouvements du marché entre le moment où l’ordre est passé et celui où il est exécuté.

Pourquoi le slippage se produit-il ?

Deux grands facteurs sont à l’origine du slippage : la volatilité et la liquidité.

- Volatilité : Les marchés crypto sont connus pour leurs mouvements de prix rapides. Cela signifie que le prix peut changer entre le moment où vous validez un ordre et son exécution.

- Liquidité : Si une crypto est peu échangée, l’écart entre l’offre et la demande est plus large, ce qui peut entraîner un prix d’exécution bien moins avantageux. Cela arrive souvent sur les altcoins peu liquides, et encore plus fréquemment sur les DEX (échanges décentralisés).

Slippage positif vs. slippage négatif

- Slippage positif : L’ordre est exécuté à un prix plus avantageux que prévu. Par exemple, vous achetez moins cher ou vous vendez plus cher.

- Slippage négatif : L’ordre est exécuté à un prix moins favorable. Cela peut sérieusement impacter votre rentabilité si cela se répète souvent.

Peut-on éviter le slippage ?

On ne peut pas l’éliminer totalement, mais voici quelques techniques pour le limiter :

1. Utiliser des ordres limités

Contrairement aux ordres au marché, les ordres limités vous permettent de fixer un prix maximum (ou minimum) pour l’achat ou la vente. L’ordre ne sera exécuté que si ce prix est atteint.

2. Définir un taux de slippage

Certains échanges permettent de fixer une tolérance de slippage (ex. 0,1 % à 5 %). Cela empêche l’ordre de passer si le prix varie trop. Attention toutefois à ne pas fixer un seuil trop bas, sinon l’ordre pourrait ne jamais être exécuté.

3. Comprendre la volatilité d’un token

Plus vous en savez, mieux vous tradez. Renseignez-vous sur les mouvements passés du token, et sur la volatilité de la plateforme utilisée. Cela vous aidera à prendre des décisions plus éclairées.

Comment calculer le slippage ?

Le slippage peut être exprimé en valeur absolue (en euros ou dollars) ou en pourcentage.

- Montant du slippage : Prix réel - Prix attendu

- Pourcentage : (Montant du slippage ÷ Différence entre prix attendu et prix limite) × 100

Exemple : Vous voulez acheter du Bitcoin à 50 000 $, avec un ordre limite à 50 500 $. Finalement, l’ordre est exécuté à 50 250 $.

- Slippage = 250 $

- Pourcentage = (250 ÷ 500) × 100 = 50 %

Dans cet exemple, votre slippage est de 250 $ ou 50 %.

Vous voulez en savoir plus sur les crypto-monnaies et le trading ? Consultez tous nos autres articles éducatifs ici.

Ce qui a commencé comme une blague est rapidement devenu un phénomène mondial, avec une capitalisation qui le place parmi les 10 plus grandes cryptomonnaies. Explorons ensemble l’origine du Dogecoin, les raisons de son succès, et en quoi il se distingue de Bitcoin.

Pionnier du mouvement des mèmes, Dogecoin s’est imposé comme un leader improbable dans l’univers crypto, notamment grâce à son prix attractif. Des investisseurs aux simples internautes, beaucoup ont suivi la hype autour de cette cryptomonnaie pas comme les autres.

Fun fact : il y a actuellement plus de DOGE en circulation que de tokens Ethereum et Litecoin réunis.

Qui a créé le Dogecoin ?

Dogecoin a été lancé en 2013 par deux développeurs, Billy Markus et Jackson Palmer, qui souhaitaient parodier le Bitcoin en créant une cryptomonnaie basée sur le célèbre mème du chien Shiba Inu. Ce qui n’était qu’un clin d'œil humoristique est devenu un acteur de poids dans l’écosystème crypto.

C’est quoi, Dogecoin ?

Dogecoin est une cryptomonnaie peer-to-peer conçue pour faciliter les paiements. Issue d’un hard fork du réseau Litecoin, elle fonctionne avec sa propre blockchain et n’a pas de limite d’émission : il existe déjà plus de 131 milliards de DOGE en circulation.

Si elle est utilisée comme moyen de paiement, Dogecoin est surtout populaire en tant que système de pourboires sur les réseaux sociaux, notamment Twitter et Reddit.

Pourquoi Dogecoin a-t-il explosé ?

L’une des raisons majeures de la montée en flèche du Dogecoin : Elon Musk. Le patron de Tesla et SpaceX, surnommé le "Dogefather", a largement contribué à faire grimper le cours du DOGE à coups de tweets devenus viraux.

Utilisant la même technologie de minage que Litecoin (Scrypt), Dogecoin est apprécié par les traders pour sa rapidité et sa simplicité.

Comment fonctionne Dogecoin ?

Dogecoin s’appuie sur la technologie blockchain pour garantir des transactions transparentes et sécurisées. Grâce à son algorithme de consensus Proof-of-Work, chaque bloc est validé toutes les minutes — bien plus rapide que Bitcoin.

Pour commencer, il suffit de créer un portefeuille DOGE, dans lequel vous pouvez recevoir, envoyer ou simplement conserver vos DOGE.

La Dogecoin Foundation

En 2014, une fondation à but non lucratif a été créée pour structurer le développement du projet. Après quelques années de silence, elle a été relancée en 2021 avec un nouveau comité comprenant, entre autres, Vitalik Buterin (fondateur d’Ethereum) et Jared Birchall (associé d’Elon Musk).

La fondation se réunit mensuellement pour discuter des avancées du projet. Markus, cofondateur, supervise la communauté, Keller s’occupe des aspects techniques, Buterin agit en tant que conseiller blockchain et Birchall couvre les volets financiers et juridiques.

Une communauté soudée

Depuis ses débuts, Dogecoin a fédéré une communauté engagée. Elle a notamment financé des événements insolites comme l’envoi de l’équipe jamaïcaine de bobsleigh aux Jeux olympiques de 2014 ou encore le sponsoring d’un pilote NASCAR.

Outre Elon Musk, Mark Cuban — propriétaire des Dallas Mavericks — est un fervent défenseur du Dogecoin. Son équipe NBA accepte d’ailleurs les paiements en DOGE pour les billets et produits dérivés depuis 2021.

Dogecoin vs Bitcoin

Même si les deux utilisent un système de minage similaire (Proof-of-Work), Dogecoin se démarque :

- Temps de transaction : 1 minute pour Dogecoin contre 10 minutes pour Bitcoin.

- Politique monétaire : Bitcoin est limité à 21 millions de coins, Dogecoin est inflationniste avec une offre illimitée.

- Utilisation : Bitcoin est souvent vu comme une réserve de valeur, tandis que DOGE est plus utilisé pour les paiements quotidiens.

Dogecoin est soutenu par une communauté très active, notamment sur Twitter et Reddit, ce qui contribue à maintenir sa notoriété.

Comment acheter du Dogecoin ?

En moins d’un an, DOGE est passé d’un mème internet à un actif crypto incontournable, enregistrant une hausse de 5 000 % et entrant dans le top 10 des cryptomonnaies.

Si vous souhaitez ajouter du Dogecoin à votre portefeuille, l’application Tap vous permet désormais d’en acheter facilement. Achetez, vendez ou stockez vos DOGE depuis votre portefeuille crypto ou en utilisant une carte bancaire ou un virement classique.

En 2021, un phénomène crypto inattendu a fait fureur : les cryptomonnaies à thème canin, avec en tête de file Shiba Inu, qui a réussi à voler la vedette. Initialement considéré comme un simple "meme token", ce réseau a rapidement révélé des ambitions bien plus vastes que ce que l'on aurait pu imaginer.

Origines et Concept

Shiba Inu tire son nom et son inspiration du même mème internet qui a donné naissance à Dogecoin : un adorable chien Shiba Inu. Créé en 2020 comme une alternative décentralisée à Dogecoin, le projet repose sur le réseau Ethereum. La cryptomonnaie SHIB, basée sur le standard ERC-20, n'est qu'une partie d'un écosystème beaucoup plus riche.

Un Écosystème Innovant

Au-delà d'une simple monnaie numérique, Shiba Inu propose plusieurs fonctionnalités originales :

- ShibaSwap : Une plateforme d'échange décentralisée

- Tokens complémentaires :

- LEASH : Un token permettant de fournir de la liquidité

- BONE : Un token de gouvernance offrant des droits de vote

- Shiboshi Game : Un jeu NFT

- Shiba Artist Incubator : Un incubateur pour les artistes NFT

Une Ascension Fulgurante

L'histoire de Shiba Inu est pour le moins spectaculaire. En novembre 2021, la cryptomonnaie a connu une croissance hallucinante de plus de 60 000 000% depuis le début de l'année. Son ajout sur Coinbase a provoqué une hausse de 40% en seulement deux jours.

Le Mystère Derrière le Projet

Comme souvent dans le monde des cryptomonnaies, le créateur de Shiba Inu reste anonyme. Connu sous le pseudonyme de Ryoshi, il a lancé le projet avec une émission totale de 1 quadrillion de tokens. Un élément fascinant de son histoire : 50% des tokens ont été verrouillés sur Uniswap, tandis que les 500 trilliards restants ont été envoyés à Vitalik Buterin, le fondateur d'Ethereum.

Buterin a alors pris une décision surprenante : il a brûlé 90% de sa part et a fait don des 10% restants à un fonds de secours Covid en Inde, ce qui a eu un impact significatif sur le marché.

Une Communauté Passionnée

Fortement relayé sur les réseaux sociaux et dans les médias, Shiba Inu s'est rapidement imposé comme bien plus qu'un simple "meme token". La communauté, influencée par des personnalités comme Elon Musk, a joué un rôle crucial dans sa popularisation.

Bien que Musk ait mentionné SHIB sur Twitter, il a précisé ne pas en posséder lui-même.

À Retenir

Shiba Inu représente plus qu'une simple cryptomonnaie. C'est un projet ambitieux qui illustre parfaitement l'innovation et la créativité de l'écosystème des cryptomonnaies, où l'humour et la technologie se rencontrent de manière inattendue.

Are you ready to embrace the future of cashless payments? As Europeans increasingly rely on digital payment methods, the European Union is exploring implementing a safe and effective transition. Enter the digital euro, a potential game-changer in the world of virtual money.

In this article, we'll dive into what the digital euro is all about and how it works. Get ready to discover how this innovative currency could streamline transactions, reduce costs, and empower individuals and businesses throughout the Eurozone. It's high time we unlock the possibilities of the digital euro and embrace the convenience of a cashless future.

What is the digital euro?

The digital euro, at its core, is a virtual currency designed for the Eurozone. It operates entirely digitally, making transactions fast, secure, and innovative. As a digital currency, it exists in electronic form, with no physical counterpart like traditional banknotes or coins.

The European Central Bank (ECB) plays a crucial role in issuing and managing the digital euro, ensuring its legal value and guaranteeing its acceptance alongside physical cash. With the ECB's oversight, the digital euro aims to provide a seamless and convenient payment method for businesses and individuals alike, revolutionising the way we handle money in the digital age.

Is the digital euro a cryptocurrency?

No, the digital euro is not considered a cryptocurrency. While both the digital euro and cryptocurrencies are virtual assets, there are key differences between them.

Cryptocurrencies, like Bitcoin, are typically decentralised and operate independently of central banks or public authorities. They are often issued by private individuals and allow for peer-to-peer transactions without the need for intermediaries like central banks.

In contrast, the digital euro will be issued and regulated by the European Central Bank (ECB), making it a central bank digital currency (CBDC). The digital euro will operate on a centralised system and will be managed and regulated using blockchain technology operated by the central bank.

Why do we need a digital euro?

The digital euro has several key objectives aimed at transforming the financial landscape. Firstly, it seeks to enhance financial integration within the Eurozone by providing a common and easily accessible digital payment solution for all member countries.

Secondly, the digital euro aims to bolster security, offering a safe and trusted digital currency that can mitigate risks associated with traditional payment methods. For users, the digital euro promises convenience by enabling fast and seamless transactions, eliminating the need for physical currency.

Additionally, it has the potential to be cost-effective, reducing transaction fees and providing efficient payment options for both businesses and individuals. The digital euro also allows anyone to use the currency without creating a bank account associated with the central bank.

How will the digital euro work?

The virtual currency operates on an innovative framework, known as blockchain technology, revolutionising the way we transact. To use the digital euro, individuals and businesses will need to create a digital wallet, similar to those used for cryptocurrencies.

However, unlike cryptocurrencies, the digital euro will be issued and regulated by the European Central Bank (ECB), ensuring its stability and legal value. Despite it being a digital currency, it is still regarded as central bank money as it is operated by the central bank. Users won't require a traditional bank account, as the digital euro can be deposited directly at the European Central Bank. This empowers individuals to engage in peer-to-peer transactions without relying on commercial banks as intermediaries.

With blockchain technology as its backbone, the digital euro ensures secure, traceable, and efficient transactions, making it a cutting-edge payment method for the modern era while remaining central bank money.

Advantages of implementing the digital euro

The modern payment tool is designed to empower all private citizens and businesses in the Eurozone. Once approved, the digital euro will revolutionise transactions with its simplicity and immediacy. Here's what it brings:

Streamlined processes

The digitization of payments will make purchases and money transactions simpler and faster.

Cost savings

The digital euro significantly reduces costs associated with payment systems, putting more money back in your pocket.

Environmental benefits

By embracing the digital euro project, we contribute to a drastic reduction in the ecological footprint associated with monetary and payment systems within the financial sector.

Instant support

In times of need, governments can swiftly provide economic aid to citizens, thanks to the digital euro.

Anti-money laundering

With transaction registration, we can effectively combat money laundering and tax evasion.

Financial inclusion

The digital euro ensures everyone, even those without a bank account, can enjoy the simplicity and security of digital payments within the financial system.

Risks associated with the digital euro

While the digital euro brings numerous benefits, it's important to be aware of potential risks. Here are a few considerations:

Privacy

The digital euro complements physical cash, known for its anonymity. While it aids in anti-money laundering, tracking payments could limit citizen privacy to some extent.

Impact on banks

As the digital euro gains popularity, deposits in credit institutions may decrease, potentially affecting loan availability. Credit institutions and payment intermediaries, and even national central banks, may need to revise their business models to adapt to the digital euro ecosystem and safeguard financial stability within the greater financial system.

Traditional euro vs the digital euro

When comparing the digital euro to traditional currency, there are both similarities and differences to consider. In terms of similarities, both the digital euro and physical currency share the fundamental purpose of facilitating transactions and serving as a medium of exchange. While the digital euro operates in the digital realm, central banks physical banknotes and coins continue to play a significant role in everyday transactions alongside the digital euro. It's important to note that both are central bank money.

However, key differences set the digital euro apart. The digital euro offers advantages such as faster transactions, as it eliminates the need for physical exchange and reduces processing times.

Additionally, the digital euro promotes financial inclusion by enabling individuals without a bank account to participate in the digital economy, expanding access to secure and convenient payment methods. The digital euro is not designed to replace the traditional currency, but rather coexist alongside it.

It is, however, poised to shape the future of currency.

The current landscape of CBDCs

While the digital euro is expected to take 5 years to implement, other countries around the world are also in the running to release a central bank digital currency of their own. In fact, approximately 50 central banks around the world are actively researching or experimenting with central bank digital currencies, confirming that the race to embrace digital currencies and central bank money is on.

The Bahamas lead the pack with their Sand Dollar, a digital version of the Bahamian dollar launched in October 2020. The dollar offers users free mobile transactions and a safer option than carrying cash. Other noteworthy initiatives include China with the digital renminbi (e-CNY) already in testing and Sweden’s e-krona, and now, the digital euro project.

This thriving landscape in the financial system signifies the growing acceptance of digital currencies by central banks. As financial inclusion, individual financial stability, streamlined payment systems, and the emergence of private cryptocurrencies take centre stage, the exploration of CBDCs empowers nations and central banks to shape the future of money and unlock new possibilities for a digitally empowered society.

Final thoughts

In conclusion, the digital euro represents a transformative leap toward a cashless future. With its aim of enhancing financial integration, strengthening security, and providing convenient payment options, the digital euro has the potential to revolutionise the way we handle money in the Eurozone.

Operating on blockchain technology and regulated by the European Central Bank, the digital euro offers fast, secure, and efficient transactions, empowering individuals and businesses alike. While the digital euro coexists with physical currency, its advantages, such as faster transactions and increased financial inclusion, make it a promising addition to the financial landscape.

As countries worldwide explore the potential of central bank digital currencies, including the Sand Dollar, the future of digital currencies appears bright, heralding a new era of financial empowerment. Keep an eye out for the digital euro in months to come.

When Satoshi Nakamoto created Bitcoin, he designed it in such a way that should the value increase dramatically, there would still be an inclusive decimal value for the masses. Satoshis could one day be how we buy a cup of coffee anywhere in the world, using the same currency from Britain to Japan.

How Many Satoshis Are in One Bitcoin?

Often shortened to SAT, Satoshi is the smallest unit of Bitcoin, the world’s first and most popular cryptocurrency. Just like the U.S. dollar divides into cents, Bitcoin divides into Satoshis, but on a much finer scale. One Bitcoin equals 100,000,000 Satoshis (0.00000001 BTC).

This structure ensures that Bitcoin remains usable for everyday financial transactions, even as its market value rises. Whether someone is investing a few dollars or buying a cup of coffee, the Bitcoin network allows precise division and ownership down to a single Satoshi, making the digital currency accessible to everyone.

Why Satoshis Matter

Bitcoin’s price often exceeds tens of thousands of U.S. dollars, creating a psychological barrier for newcomers who assume they must buy an entire coin. Satoshis remove that barrier by enabling fractional ownership.

This level of accessibility supports financial inclusion, allowing individuals from all backgrounds (including those in developing markets) to participate in the cryptocurrency economy.

From micropayments to online services, Satoshis make purchasing small products, tipping creators possible, etc. As adoption grows, the ability to transact in Satoshis could become a standard part of personal finance and global economic development.

How to Convert Satoshis

Because 1 BTC = 100,000,000 SATs, converting between the two is very simple math:

Satoshis = Bitcoin × 100,000,000

Bitcoin = Satoshis ÷ 100,000,000

For instance, if Bitcoin trades at $60,000, then:

- 1 SAT = $0.0006

- 10,000 SATs = $6

- 100,000 SATs = $60

To simplify conversions, users can access Satoshi calculators or adjust display preferences within their cryptocurrency wallet or favorite platform. Many platforms also allow price displays in SATs to improve user experience and accuracy.

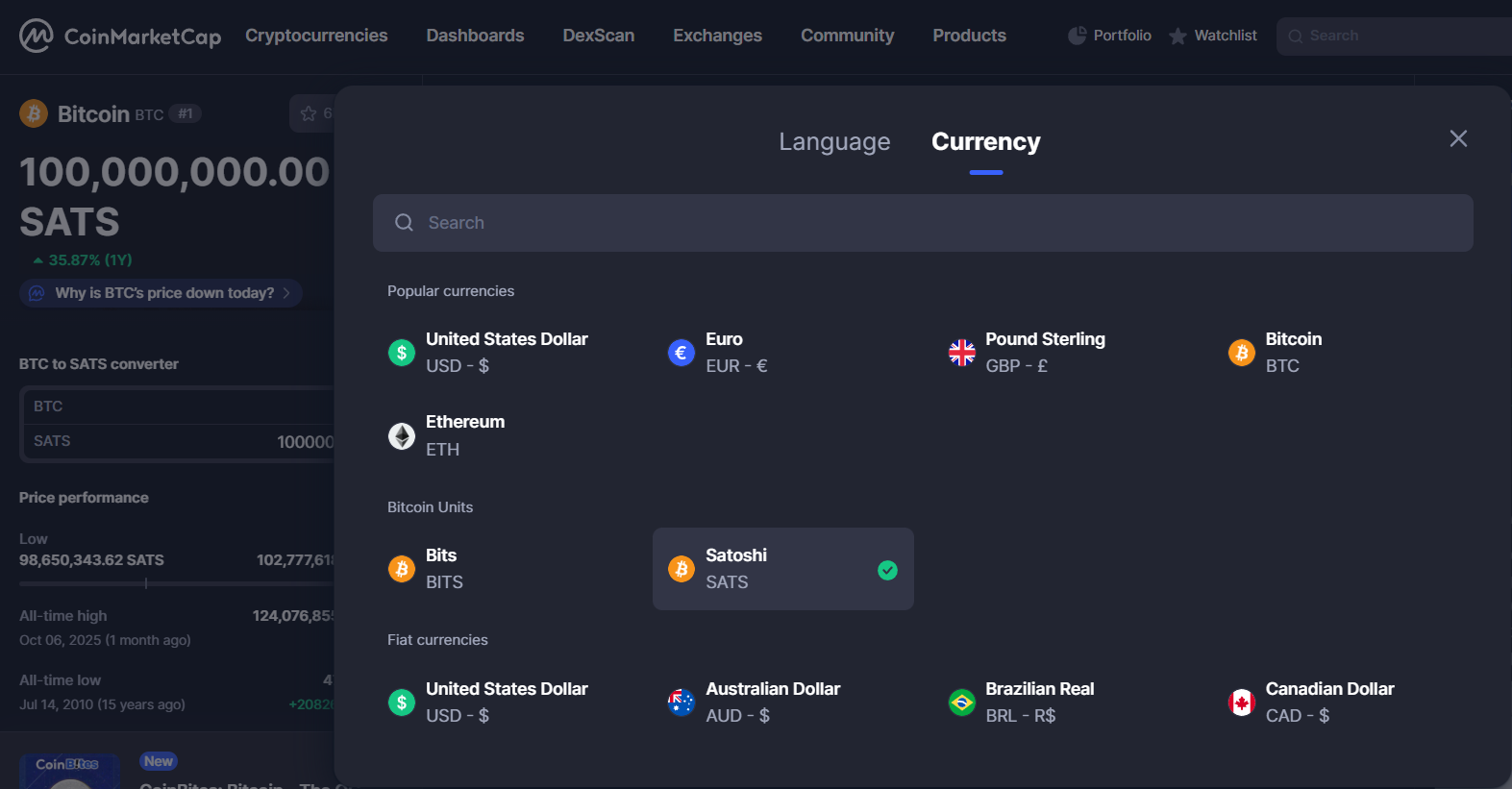

For instance, on CoinMarketCap, you can change the default currency to SATs by selecting the currency drop down option in the top right-hand corner. Select the Satoshi option under Bitcoin units. This will then display all values as Satoshis.

The History Behind the Name

The name “Satoshi” honors Satoshi Nakamoto, the mysterious programmer who invented Bitcoin and published its white paper in 2008.

The term was first proposed in 2010 on the BitcoinTalk forum by a user named Ribuck, who suggested defining a smaller Bitcoin unit for microtransactions. The community endorsed it, and “Satoshi” became the standard reference for Bitcoin’s smallest fraction.

This naming not only pays tribute to Bitcoin’s anonymous creator but also reflects the peer-to-peer and community-driven nature of the blockchain project.

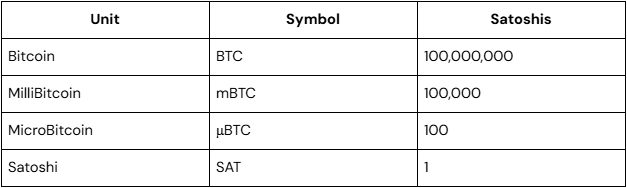

Bitcoin Unit Hierarchy Explained

Bitcoin can be divided into several measurement units, which make it easier to display or calculate different values depending on trade size or market purpose:

Users can choose their preferred unit in most cryptocurrency wallets or mobile apps, which helps reduce confusion when managing balances. This hierarchical structure is part of Bitcoin’s software design, ensuring precision, scalability, and transparency across every financial service or exchange that integrates it.

Real-World Applications of Satoshis

The use of Satoshis extends far beyond calculations. They play a vital role in everyday transactions and digital finance. Examples include:

- Micropayments. Paying for an article, video, or song online using fractions of Bitcoin.

- Remittances. Sending money across borders with minimal fees and no intermediary banks.

- Retail payments. Buying coffee, subscriptions, or services priced in SATs.

- Mining rewards. Bitcoin miners earn Satoshis as rewards for validating blocks on the blockchain.

- Lightning Network transactions. Enables instant, low-cost peer-to-peer payments denominated in milli- or micro-Satoshis.

These use cases show us how cryptocurrency adoption supports faster, cheaper, and more inclusive financial transactions, which helps bridge gaps between traditional fiat money and the digital economy. Satoshis make it easier to represent these small, day-to-day amounts.

Satoshis vs Other Cryptocurrency Units

Other blockchains have their own smallest units. For example, Ethereum uses the Wei, where 1 ETH = 1,000,000,000,000,000,000 Wei (18 decimal places). While Ethereum’s extreme divisibility helps with DeFi and smart contract operations, Bitcoin’s 8-decimal precision balances usability and simplicity. The Satoshi system keeps values easy to calculate, supports market liquidity, and provides enough granularity for future adoption.

This approach makes Bitcoin user-friendly, maintaining accuracy and precision in every financial transaction without overwhelming users with excessive mathematical complexity.

Considerations

Despite its simplicity, using the Satoshi unit can bring some hurdles too:

- Many newcomers are unfamiliar with terms like “Satoshi” or how to interpret BTC in fractional units.

- Since Bitcoin’s price fluctuates, the value of a Satoshi changes constantly, affecting everyday purchasing power.

- Not all wallets and exchanges display Satoshis by default, creating potential confusion for the end user.

- While some companies and fintech platforms already support SAT-based payments, widespread retail exposure is still limited.

Overcoming these hurdles will require better user experience design, educational content, and standardized software development practices across the industry.

The Future of Satoshis

As Bitcoin adoption expands, Satoshis may play an even bigger role in daily finance. With the Lightning Network, users can already transact in milli-satoshis, enabling high-speed, low-cost microtransactions far below one SAT.

In the long term, Bitcoin’s fractional-reserve capabilities and tokenization could make it a backbone for financial services, virtual payments, and cross-border trade. For emerging economies, Satoshis could represent economic empowerment, offering a stable, global currency that anyone around the world can use.

In short, Satoshis are not just a mathematical fraction. They are the mathematical foundation of a global peer-to-peer financial system that continues to evolve.

Key Takeaways

- 1 Satoshi = 0.00000001 Bitcoin

- Enables fractional ownership and global accessibility

- Named after Satoshi Nakamoto, Bitcoin’s anonymous creator

- Used for microtransactions, payments, and mining rewards

- Essential for the future of financial inclusion and digital payments

Getting Started: How to Buy and Use Satoshis

You can acquire the exact amount of Satoshis you're looking for through the Tap app, making it easy to begin your journey into the exciting world of Bitcoin.