Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

Are you ready to embrace the future of cashless payments? As Europeans increasingly rely on digital payment methods, the European Union is exploring implementing a safe and effective transition. Enter the digital euro, a potential game-changer in the world of virtual money.

In this article, we'll dive into what the digital euro is all about and how it works. Get ready to discover how this innovative currency could streamline transactions, reduce costs, and empower individuals and businesses throughout the Eurozone. It's high time we unlock the possibilities of the digital euro and embrace the convenience of a cashless future.

What is the digital euro?

The digital euro, at its core, is a virtual currency designed for the Eurozone. It operates entirely digitally, making transactions fast, secure, and innovative. As a digital currency, it exists in electronic form, with no physical counterpart like traditional banknotes or coins.

The European Central Bank (ECB) plays a crucial role in issuing and managing the digital euro, ensuring its legal value and guaranteeing its acceptance alongside physical cash. With the ECB's oversight, the digital euro aims to provide a seamless and convenient payment method for businesses and individuals alike, revolutionising the way we handle money in the digital age.

Is the digital euro a cryptocurrency?

No, the digital euro is not considered a cryptocurrency. While both the digital euro and cryptocurrencies are virtual assets, there are key differences between them.

Cryptocurrencies, like Bitcoin, are typically decentralised and operate independently of central banks or public authorities. They are often issued by private individuals and allow for peer-to-peer transactions without the need for intermediaries like central banks.

In contrast, the digital euro will be issued and regulated by the European Central Bank (ECB), making it a central bank digital currency (CBDC). The digital euro will operate on a centralised system and will be managed and regulated using blockchain technology operated by the central bank.

Why do we need a digital euro?

The digital euro has several key objectives aimed at transforming the financial landscape. Firstly, it seeks to enhance financial integration within the Eurozone by providing a common and easily accessible digital payment solution for all member countries.

Secondly, the digital euro aims to bolster security, offering a safe and trusted digital currency that can mitigate risks associated with traditional payment methods. For users, the digital euro promises convenience by enabling fast and seamless transactions, eliminating the need for physical currency.

Additionally, it has the potential to be cost-effective, reducing transaction fees and providing efficient payment options for both businesses and individuals. The digital euro also allows anyone to use the currency without creating a bank account associated with the central bank.

How will the digital euro work?

The virtual currency operates on an innovative framework, known as blockchain technology, revolutionising the way we transact. To use the digital euro, individuals and businesses will need to create a digital wallet, similar to those used for cryptocurrencies.

However, unlike cryptocurrencies, the digital euro will be issued and regulated by the European Central Bank (ECB), ensuring its stability and legal value. Despite it being a digital currency, it is still regarded as central bank money as it is operated by the central bank. Users won't require a traditional bank account, as the digital euro can be deposited directly at the European Central Bank. This empowers individuals to engage in peer-to-peer transactions without relying on commercial banks as intermediaries.

With blockchain technology as its backbone, the digital euro ensures secure, traceable, and efficient transactions, making it a cutting-edge payment method for the modern era while remaining central bank money.

Advantages of implementing the digital euro

The modern payment tool is designed to empower all private citizens and businesses in the Eurozone. Once approved, the digital euro will revolutionise transactions with its simplicity and immediacy. Here's what it brings:

Streamlined processes

The digitization of payments will make purchases and money transactions simpler and faster.

Cost savings

The digital euro significantly reduces costs associated with payment systems, putting more money back in your pocket.

Environmental benefits

By embracing the digital euro project, we contribute to a drastic reduction in the ecological footprint associated with monetary and payment systems within the financial sector.

Instant support

In times of need, governments can swiftly provide economic aid to citizens, thanks to the digital euro.

Anti-money laundering

With transaction registration, we can effectively combat money laundering and tax evasion.

Financial inclusion

The digital euro ensures everyone, even those without a bank account, can enjoy the simplicity and security of digital payments within the financial system.

Risks associated with the digital euro

While the digital euro brings numerous benefits, it's important to be aware of potential risks. Here are a few considerations:

Privacy

The digital euro complements physical cash, known for its anonymity. While it aids in anti-money laundering, tracking payments could limit citizen privacy to some extent.

Impact on banks

As the digital euro gains popularity, deposits in credit institutions may decrease, potentially affecting loan availability. Credit institutions and payment intermediaries, and even national central banks, may need to revise their business models to adapt to the digital euro ecosystem and safeguard financial stability within the greater financial system.

Traditional euro vs the digital euro

When comparing the digital euro to traditional currency, there are both similarities and differences to consider. In terms of similarities, both the digital euro and physical currency share the fundamental purpose of facilitating transactions and serving as a medium of exchange. While the digital euro operates in the digital realm, central banks physical banknotes and coins continue to play a significant role in everyday transactions alongside the digital euro. It's important to note that both are central bank money.

However, key differences set the digital euro apart. The digital euro offers advantages such as faster transactions, as it eliminates the need for physical exchange and reduces processing times.

Additionally, the digital euro promotes financial inclusion by enabling individuals without a bank account to participate in the digital economy, expanding access to secure and convenient payment methods. The digital euro is not designed to replace the traditional currency, but rather coexist alongside it.

It is, however, poised to shape the future of currency.

The current landscape of CBDCs

While the digital euro is expected to take 5 years to implement, other countries around the world are also in the running to release a central bank digital currency of their own. In fact, approximately 50 central banks around the world are actively researching or experimenting with central bank digital currencies, confirming that the race to embrace digital currencies and central bank money is on.

The Bahamas lead the pack with their Sand Dollar, a digital version of the Bahamian dollar launched in October 2020. The dollar offers users free mobile transactions and a safer option than carrying cash. Other noteworthy initiatives include China with the digital renminbi (e-CNY) already in testing and Sweden’s e-krona, and now, the digital euro project.

This thriving landscape in the financial system signifies the growing acceptance of digital currencies by central banks. As financial inclusion, individual financial stability, streamlined payment systems, and the emergence of private cryptocurrencies take centre stage, the exploration of CBDCs empowers nations and central banks to shape the future of money and unlock new possibilities for a digitally empowered society.

Final thoughts

In conclusion, the digital euro represents a transformative leap toward a cashless future. With its aim of enhancing financial integration, strengthening security, and providing convenient payment options, the digital euro has the potential to revolutionise the way we handle money in the Eurozone.

Operating on blockchain technology and regulated by the European Central Bank, the digital euro offers fast, secure, and efficient transactions, empowering individuals and businesses alike. While the digital euro coexists with physical currency, its advantages, such as faster transactions and increased financial inclusion, make it a promising addition to the financial landscape.

As countries worldwide explore the potential of central bank digital currencies, including the Sand Dollar, the future of digital currencies appears bright, heralding a new era of financial empowerment. Keep an eye out for the digital euro in months to come.

When Satoshi Nakamoto created Bitcoin, he designed it in such a way that should the value increase dramatically, there would still be an inclusive decimal value for the masses. Satoshis could one day be how we buy a cup of coffee anywhere in the world, using the same currency from Britain to Japan.

How Many Satoshis Are in One Bitcoin?

Often shortened to SAT, Satoshi is the smallest unit of Bitcoin, the world’s first and most popular cryptocurrency. Just like the U.S. dollar divides into cents, Bitcoin divides into Satoshis, but on a much finer scale. One Bitcoin equals 100,000,000 Satoshis (0.00000001 BTC).

This structure ensures that Bitcoin remains usable for everyday financial transactions, even as its market value rises. Whether someone is investing a few dollars or buying a cup of coffee, the Bitcoin network allows precise division and ownership down to a single Satoshi, making the digital currency accessible to everyone.

Why Satoshis Matter

Bitcoin’s price often exceeds tens of thousands of U.S. dollars, creating a psychological barrier for newcomers who assume they must buy an entire coin. Satoshis remove that barrier by enabling fractional ownership.

This level of accessibility supports financial inclusion, allowing individuals from all backgrounds (including those in developing markets) to participate in the cryptocurrency economy.

From micropayments to online services, Satoshis make purchasing small products, tipping creators possible, etc. As adoption grows, the ability to transact in Satoshis could become a standard part of personal finance and global economic development.

How to Convert Satoshis

Because 1 BTC = 100,000,000 SATs, converting between the two is very simple math:

Satoshis = Bitcoin × 100,000,000

Bitcoin = Satoshis ÷ 100,000,000

For instance, if Bitcoin trades at $60,000, then:

- 1 SAT = $0.0006

- 10,000 SATs = $6

- 100,000 SATs = $60

To simplify conversions, users can access Satoshi calculators or adjust display preferences within their cryptocurrency wallet or favorite platform. Many platforms also allow price displays in SATs to improve user experience and accuracy.

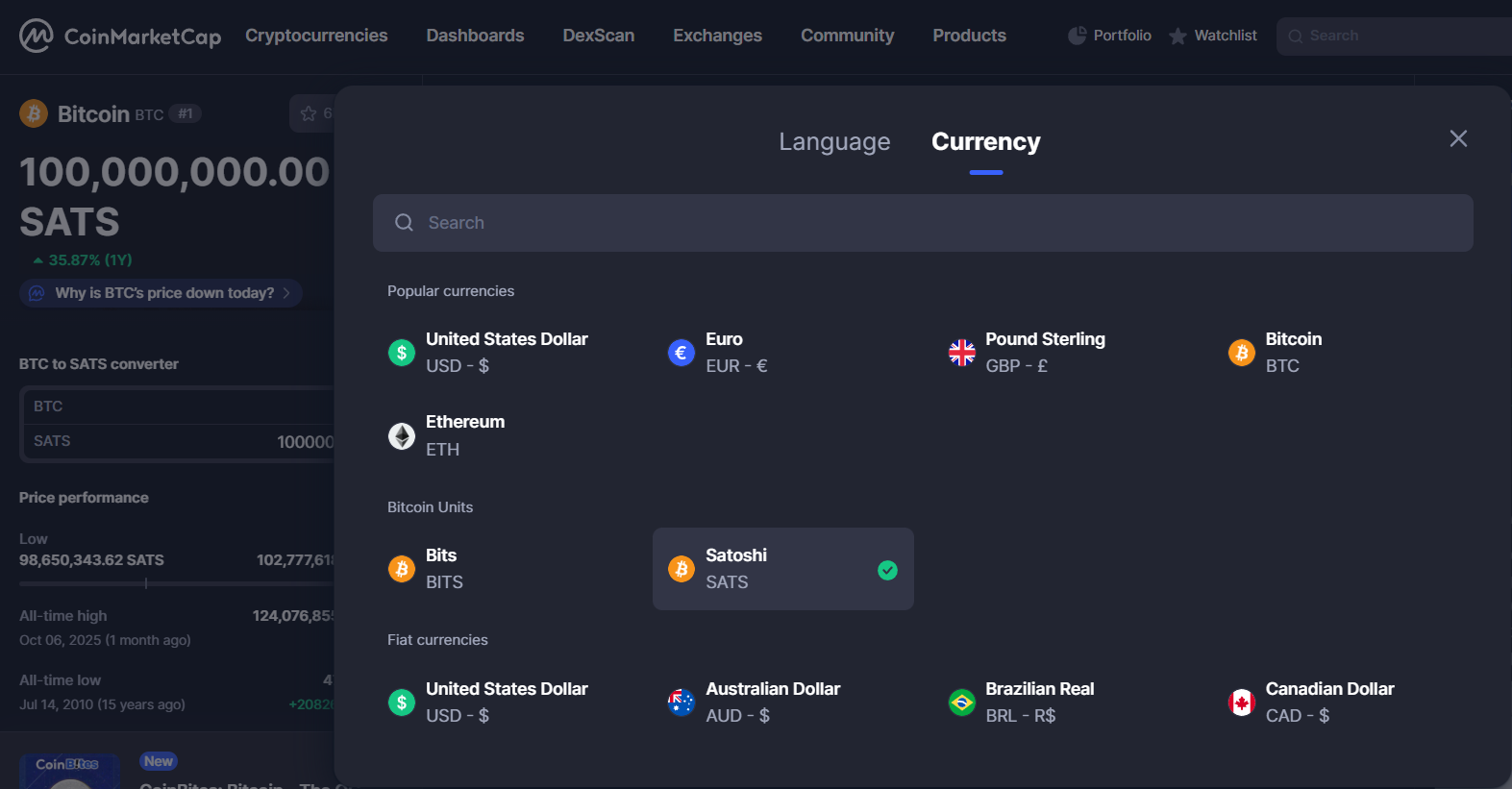

For instance, on CoinMarketCap, you can change the default currency to SATs by selecting the currency drop down option in the top right-hand corner. Select the Satoshi option under Bitcoin units. This will then display all values as Satoshis.

The History Behind the Name

The name “Satoshi” honors Satoshi Nakamoto, the mysterious programmer who invented Bitcoin and published its white paper in 2008.

The term was first proposed in 2010 on the BitcoinTalk forum by a user named Ribuck, who suggested defining a smaller Bitcoin unit for microtransactions. The community endorsed it, and “Satoshi” became the standard reference for Bitcoin’s smallest fraction.

This naming not only pays tribute to Bitcoin’s anonymous creator but also reflects the peer-to-peer and community-driven nature of the blockchain project.

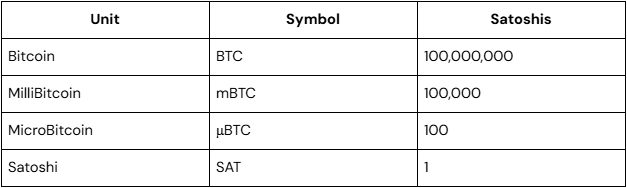

Bitcoin Unit Hierarchy Explained

Bitcoin can be divided into several measurement units, which make it easier to display or calculate different values depending on trade size or market purpose:

Users can choose their preferred unit in most cryptocurrency wallets or mobile apps, which helps reduce confusion when managing balances. This hierarchical structure is part of Bitcoin’s software design, ensuring precision, scalability, and transparency across every financial service or exchange that integrates it.

Real-World Applications of Satoshis

The use of Satoshis extends far beyond calculations. They play a vital role in everyday transactions and digital finance. Examples include:

- Micropayments. Paying for an article, video, or song online using fractions of Bitcoin.

- Remittances. Sending money across borders with minimal fees and no intermediary banks.

- Retail payments. Buying coffee, subscriptions, or services priced in SATs.

- Mining rewards. Bitcoin miners earn Satoshis as rewards for validating blocks on the blockchain.

- Lightning Network transactions. Enables instant, low-cost peer-to-peer payments denominated in milli- or micro-Satoshis.

These use cases show us how cryptocurrency adoption supports faster, cheaper, and more inclusive financial transactions, which helps bridge gaps between traditional fiat money and the digital economy. Satoshis make it easier to represent these small, day-to-day amounts.

Satoshis vs Other Cryptocurrency Units

Other blockchains have their own smallest units. For example, Ethereum uses the Wei, where 1 ETH = 1,000,000,000,000,000,000 Wei (18 decimal places). While Ethereum’s extreme divisibility helps with DeFi and smart contract operations, Bitcoin’s 8-decimal precision balances usability and simplicity. The Satoshi system keeps values easy to calculate, supports market liquidity, and provides enough granularity for future adoption.

This approach makes Bitcoin user-friendly, maintaining accuracy and precision in every financial transaction without overwhelming users with excessive mathematical complexity.

Considerations

Despite its simplicity, using the Satoshi unit can bring some hurdles too:

- Many newcomers are unfamiliar with terms like “Satoshi” or how to interpret BTC in fractional units.

- Since Bitcoin’s price fluctuates, the value of a Satoshi changes constantly, affecting everyday purchasing power.

- Not all wallets and exchanges display Satoshis by default, creating potential confusion for the end user.

- While some companies and fintech platforms already support SAT-based payments, widespread retail exposure is still limited.

Overcoming these hurdles will require better user experience design, educational content, and standardized software development practices across the industry.

The Future of Satoshis

As Bitcoin adoption expands, Satoshis may play an even bigger role in daily finance. With the Lightning Network, users can already transact in milli-satoshis, enabling high-speed, low-cost microtransactions far below one SAT.

In the long term, Bitcoin’s fractional-reserve capabilities and tokenization could make it a backbone for financial services, virtual payments, and cross-border trade. For emerging economies, Satoshis could represent economic empowerment, offering a stable, global currency that anyone around the world can use.

In short, Satoshis are not just a mathematical fraction. They are the mathematical foundation of a global peer-to-peer financial system that continues to evolve.

Key Takeaways

- 1 Satoshi = 0.00000001 Bitcoin

- Enables fractional ownership and global accessibility

- Named after Satoshi Nakamoto, Bitcoin’s anonymous creator

- Used for microtransactions, payments, and mining rewards

- Essential for the future of financial inclusion and digital payments

Getting Started: How to Buy and Use Satoshis

You can acquire the exact amount of Satoshis you're looking for through the Tap app, making it easy to begin your journey into the exciting world of Bitcoin.

L’ENS, c’est quoi exactement ?

L’Ethereum Name Service (ENS) est un système de nommage décentralisé conçu pour rendre les interactions sur Ethereum plus intuitives. Il permet aux utilisateurs de remplacer les longues adresses alphanumériques par des noms lisibles comme monnom.eth, facilitant ainsi les envois et réceptions de fonds.

Imaginez : au lieu de copier-coller une adresse complexe, il suffit d’écrire lea.eth pour envoyer des cryptos à cette personne. L’ENS fonctionne un peu comme le DNS sur internet, mais pour les adresses Ethereum.

Comment ça fonctionne ?

ENS repose sur deux composants principaux :

Le registre ENS

C’est ici que sont enregistrés tous les noms .eth. Lorsqu’un utilisateur enregistre un nom via une interface comme le ENS Manager, celui-ci est ajouté au registre et devient sa propriété.

Le résolveur ENS

C’est un smart contract qui associe un nom ENS à une adresse Ethereum. Il joue le rôle de traducteur : lorsqu’on saisit monnom.eth, le résolveur retrouve l’adresse Ethereum correspondante et permet l’envoi de fonds.

Les utilisateurs peuvent également ajouter des données supplémentaires, comme un lien IPFS ou un hash Swarm, ce qui permet d’associer des contenus décentralisés à leur domaine ENS.

Qui a créé l’ENS ?

L’ENS a été imaginé en 2016 par Nick Johnson, un ancien ingénieur de Google ayant rejoint la Fondation Ethereum. Le système a officiellement vu le jour en mai 2017 sous la forme d’un service autonome sur la blockchain Ethereum. Depuis, il est devenu un outil central dans l’écosystème Ethereum.

À quoi sert l’ENS dans la pratique ?

L'ENS facilite la vie des utilisateurs en simplifiant les paiements, les interactions avec les dapps et l’accès à du contenu décentralisé. Voici quelques cas concrets :

- Envoyer des cryptos à une adresse lisible (

tonpseudo.eth) au lieu d’une suite de chiffres et de lettres. - Héberger un site Web décentralisé via un lien IPFS rattaché à un nom ENS.

- Créer des sous-domaines (

nft.tonnom.eth,pro.tonnom.eth) pour organiser ses services Web3.

Le token ENS, à quoi sert-il ?

En 2021, ENS a lancé son propre token de gouvernance, le ENS, permettant à sa communauté de participer aux décisions. Il ne sert pas à payer l’enregistrement de noms, qui se fait en ETH, mais uniquement à voter sur les propositions.

Voici un aperçu des prix (en ETH) pour enregistrer un domaine ENS .eth :

- 5 $/an pour un nom de 5 caractères ou plus

- 160 $/an pour un nom de 4 caractères

- 640 $/an pour un nom de 3 caractères

Ces tarifs reflètent la rareté des noms plus courts.

Qu’est-ce que l’ENS DAO ?

L’ENS DAO est une organisation autonome décentralisée qui gère l’évolution du protocole. Les détenteurs du token ENS peuvent :

- Proposer et voter des mises à jour ou des changements de politique

- Influencer les décisions stratégiques du projet

- Participer à la gouvernance d’un projet Web3 phare

Et la Fondation ENS ?

La Fondation ENS est une structure à but non lucratif chargée de soutenir l’adoption et le développement du projet. Elle organise des événements communautaires, distribue des subventions aux développeurs, et accompagne la croissance de l’écosystème en parallèle de l’ENS DAO.

Comment acheter des tokens ENS ?

Vous pouvez acheter, vendre et stocker des tokens ENS directement dans l’app Tap :

- Échangez vos cryptos ou devises contre des ENS

- Achetez du ENS avec votre carte Visa ou Mastercard

- Stockez vos ENS dans un portefeuille sécurisé intégré

L’app Tap offre une expérience fluide pour gérer vos actifs numériques, que ce soit pour explorer l’univers ENS ou d’autres projets Web3.

.webp)

Le phénomène memecoin, kesako

Dans l'univers coloré et souvent chaotique des cryptos, il existe un coin particulier dominé par ce qu'on appelle les "memecoins". Contrairement aux cryptos classiques qui se prennent au sérieux avec leur technologie sophistiquée, les memecoins jouent une tout autre partition. Pas de grands discours sur la révolution financière ici - ces cryptos surfent plutôt sur la vague du fun et de la culture web.

Malgré leur côté amusant, les memecoins sont souvent au cœur de manipulations de marché et d'autres arnaques, ce qui en fait de véritables montagnes russes. Leur volatilité est extrême, et les risques sont bien réels.

Alors, qu'est-ce qui attire tant de monde vers ces blagues numériques ? C'est simple : certains memecoins ont parfois offert des rendements astronomiques aux plus téméraires. Mais dans cette galaxie de memecoins, comment distinguer les vraies pépites des arnaques ? Voici quelques repères essentiels.

Qu'est-ce qui rend les memecoins si populaires ?

Les memecoins, comme le célèbre Dogecoin ou Shiba Inu, démarrent souvent comme des blagues. Ils sont davantage associés au divertissement qu'à l'utilité, et gagnent en popularité grâce à la force de leur communauté, aux réseaux sociaux et parfois aux soutiens de célébrités.

Contrairement aux cryptomonnaies traditionnelles comme Bitcoin ou Ethereum, les memecoins ne reposent généralement pas sur une technologie complexe ou des cas d'usage spécifiques. Leur objectif n'est pas de résoudre de grands défis technologiques mais plutôt de capturer l'esprit d'Internet sous forme de jetons. Leur valeur est donc principalement portée par l'enthousiasme collectif, le buzz en ligne et l'excitation de participer à un mouvement viral.

Les revers de la popularité

Récemment, les memecoins font beaucoup parler d'eux, suscitant une vague d'enthousiasme — et malheureusement, une recrudescence des arnaques. Pour naviguer dans ce secteur particulier du marché crypto, il faut avoir l'œil affûté. Avant de se lancer dans un memecoin, il est crucial d'examiner le projet, l'équipe qui le développe, sa feuille de route et sa transparence globale.

Les bons réflexes pour éviter les arnaques

Au-delà des blagues et du buzz

Si l'attrait initial d'un memecoin vient souvent de son humour, sa pérennité nécessite plus de substance. Recherchez des memecoins qui offrent une véritable utilité et un rôle dans un écosystème plus large — ce sont des signes d'un projet qui potentiellement peut durer.

La transparence avant tout

Méfiance quand tout est flou! Méfiez-vous des memecoins entourés de mystère, où les informations sur l'équipe et leurs mises à jour sont rares. Un projet de memecoin fiable communique ouvertement sur ses avancées et sur les personnes qui le dirigent.

La sécurité, c'est du sérieux

Les memecoins attirant souvent l'attention des pirates informatiques, une sécurité robuste est indispensable. Un memecoin crédible aura fait l'objet d'audits de sécurité rigoureux. L'absence de mesures de sécurité solides est un signal d'alarme.

Une communauté qui assure

Une communauté dynamique et active est cruciale pour le succès d'un memecoin. Les projets portés par leurs communautés ont tendance à avoir un avenir plus prometteur, s'épanouissant grâce au soutien collectif de leurs membres.

Conclusion

Les memecoins représentent un phénomène unique dans l'univers des cryptomonnaies, mêlant l'humour d'Internet au monde des actifs numériques. Qu'on en rie ou qu'on les prenne au sérieux, ils sont devenus une partie fascinante de l'histoire des cryptos. Entre les succès éclair et les arnaques bien ficelées, difficile parfois de s'y retrouver.

Cependant, les caractéristiques mêmes qui rendent les memecoins attractifs — leur nature virale et l'engouement communautaire — en font aussi un terrain propice aux bulles spéculatives et aux déboires financiers. Ce marché peu ou pas régulé et souvent imprévisible attire à la fois les opportunités et les arnaqueurs.

Pour les curieux et les passionnés, naviguer dans cet univers demande de rester informé, vigilant et perspicace. Comprendre ce qui différencie un véritable memecoin d'une arnaque est crucial. Il ne s'agit pas uniquement du buzz initial ou de l'humour, mais de bien d'autres éléments comme de la valeur sous-jacente, des mesures de sécurité, de la transparence et de l'engagement communautaire qui soutiennent la pérennité du projet.

While the crypto industry continues to grow at a breathtaking pace, one problem continues to run wild. That problem is the fact that blockchains are not interoperable, meaning that they can only exist in their individual nature. Polkadot set out to change this, creating a network that aims to connect multiple blockchains in one simple solution. As a direct competitor to Ethereum, the blockchain network has a different structural approach.

What Is Polkadot (DOT)?

Polkadot is a blockchain network created by one of the Ethereum founders. Through the use of intricate architecture, the platform aims to connect multiple networks through their relay chain and parachain system (more on this below).

Similar to Ethereum, developers can create their own decentralized apps (dapps) and smart contracts on the network. Referred to as a sharding multichain network, Polkadot aims to provide a platform on which developers can build multiple blockchain networks off a common standard. Traders can then trade a range of products built on the network, similar to how ERC-20 tokens are traded.

Who Created Polkadot?

Founded in 2016, Polkadot was created by one of the Ethereum co-founders, Gavin Wood, alongside Peter Czaban and Robert Habermeier. Woods notably created the Ethereum language Solidity, which allows developers to create dapps on the Ethereum network.

Wood is also the founder of Parity Technologies and the president of Web3 Foundation. Web3 Foundation is a Swiss foundation that was designed to facilitate a user-friendly, open-source decentralized web. The company's approach to crypto is one of its kind and sets it above any other competitor.

How Does Polkadot Work?

As mentioned above, Polkadot utilizes a relay chain and parachain system. Each parachain is a blockchain in itself, however, they all rely on the relay chain to facilitate transactions. These blockchains work in a "parallel" manner (hence the name) and can each hold their own tokens and individual use cases. The relay chain provides blockchain support to the parachains on the network.

Finalizing the transactions and being responsible for maintaining network security, the relay chain is able to facilitate 1,000 transactions per second (TPS). Utilizing a hybrid consensus mechanism, the enterprise network has created proof-of-stake (PoS) and a nominated-proof-of-stake (NPoS) model.

Through this variation, anyone can stake DOT in a particular smart contract and perform network roles such as being a :

- Validators (validate data in parachain blocks, vote on network changes)

- Nominators (select validators by delegating their staked DOT to them)

- Collators (nodes with full histories of each parachain, that transfer this information into blocks for the relay chain)

- Fishermen (responsible for monitoring the network and reporting bad behaviour to the validators)

These four roles allow Polkadot to have a highly sophisticated user-driven governance system as each role contributes to maintaining and securing the network while eradicating bad behaviour.

The network is working on a third blockchain functionality known as a bridge. Bridges will allow blockchains on the Polkadot network to interact with "outside" blockchains, essentially allowing tokens to be swapped directly without needing to go through an exchange.

Through this intensive structuring, Polkadot aims to solve two problems that the blockchain network is currently plagued with scalability and governance.

What Is DOT?

DOT is the native cryptocurrency to the Polkadot network and is used as a governance and utility token, allowing users to vote on proposed upgrades and used for gas fees. It plays an integral role in maintaining and operating the network. As a digital currency, it can also be used to execute cross-border transactions.

The platform was launched in 2020 and has already established itself in the top 10 biggest cryptocurrencies.

Does Polkadot Have A Max Supply Cap?

To answer the question "what is the total supply of Polkadot" the answer is that there isn't one. The network opted to leave the total number of DOT infinite. At the time of writing the circulating supply was just short of 1 billion coins.

What Is The Difference Between Polkadot And Ethereum?

A common question in the crypto community, not just because they share similar use cases but also because the two networks share a founder. Both networks provide a platform on which developers can create their own blockchains, and following the launch of Ethereum 2.0., will both be using a PoS consensus.

Structurally the Polkadot platform differs in that it makes use of parachains and a relay chain. This is a unique feat in the blockchain industry. Through this structure, the network aims to improve on several of Ethereum's functionalities and deliver a trifactor of governance, scalability and interoperability to the blockchain industry, without compromising security.

How Can I Buy Polkadot?

If you're looking to incorporate Polkadot (DOT) in your cryptocurrency portfolio, look no further than Tap Global. A recent addition to the exchange's portfolio, users can buy, sell, trade and store DOT directly through the professional app. Whether looking to trade DOT for its technology and smart contract capabilities, or to tap into a new market, Tap allows traders to diversify their cryptocurrency portfolio in one secure location.

In this article, we’re exploring the most recent addition to the list of supported cryptocurrencies on the Tap App, one of the highly esteemed top 20 cryptocurrencies based on market cap, Algorand (ALGO).

What is Algorand (ALGO)?

Algorand is a decentralized blockchain platform that supports the development of a wide range of dapps (decentralized applications). The platform has been used to create dapps across industries like real estate, copyright, microfinance and more. Launching the same month as its ICO, the Algorand mainnet officially went live in June 2019.

The Pure-Proof-of-Stake (PPoS) network was created to improve efficiency and transaction times within the crypto space, as well as reduce transaction costs. With no mining (due to the PPoS consensus), Algorand represents a more sustainable and energy-reserving contribution to the space.

A unique aspect of the platform is that as new ALGO enter circulation with the creation of each new block, the newly minted coins are distributed to everyone who holds a certain amount of ALGO in their wallets.

While the project is relatively new, it has received the backing of big names and has seen impressive company interest. In June 2021, Arrington Capital bet $100 million on the platform after launching a fund supporting initiatives building on Algorand, while fintech infrastructure provider Six Clovers launched a cross-border payment system on the platform.

The platform was also selected to host the Marshall Islands CBDC.

Who created Algorand?

The blockchain platform was created by Silvio Micali, a highly regarded contributor to the crypto space and recipient of the 2012 Turing Award. The MIT computer science professor was recognised for his fundamental contributions to “the theory and practice of secure two-party computation, electronic cash, cryptocurrencies and blockchain protocols.”

The Algorand whitepaper was co-authored by Stony Brook University professor Jing Chen.

When first conceptualised in 2017, Micali wanted to create a platform that not only provided digital transactions but also tracked assets like titles and property. The platform also allows for the creation of smart contracts (decentralized digital agreements) and tokens.

How does Algorand work?

The Algorand platform is divided into two layers: layer 1, responsible for ensuring the network’s security and compatibility, and layer 2, responsible for more complex developments.

Layer 1 supports asset creation, smart contracts, and atomic swaps between assets while layer 2 is reserved for more compound smart contracts and dApp development. These two layers allow the network to process transactions more efficiently, with simple transactions taking place on layer 1, while more complex smart contracts are executed off-chain.

Through the pure proof of work consensus, the two-phase block production is conducted through a propose and vote system where users who stake ALGO are randomly selected to validate and approve each block as it is created. Stakers only need to hold 1 ALGO in order to generate a participation key necessary to become a Participation Node.

These nodes are coordinated by Relay Nodes which are not actively involved in the verification process but are responsible for facilitating communication among the Participation Nodes.

The more of the native cryptocurrency a user holds, the more likely they are to be selected. This consensus ensures that the platform is secure, decentralized and able to process transactions in seconds as opposed to minutes (as on other networks).

Algorand is able to process over 1,000 transactions per second (TPS) and validate transactions in less than five seconds.

What is ALGO?

ALGO is the native token to the Algorand platform. As the newly minted coins are distributed to all users holding ALGO (whether on an exchange or in a non-custodial wallet) and not just the nodes verifying transactions, holders of the token are able to earn a 7.5% annual percentage yield (APY).

A total of 10 billion tokens were minted, with roughly 6.8 billion in circulation at the time of writing. These tokens are gradually entered into circulation through predetermined distribution channels. The token distribution for ALGO is as follows:

- 3.0 billion. To be injected into circulation over the first 5 years, at first via auction.

- 1.75 billion. Allocated to participation rewards.

- 2.5 billion. Allocated to relay node runners.

- 2.5 billion. Allocated to the Singapore-based Algorand Foundation & Algorand, Inc.

- 0.25 billion. Allocated to end-user grants.

How Can I Buy ALGO?

If you’re interested in accumulating this leading blockchain token, you can do so effortlessly through the Tap app. As part of a new string of supported tokens, Tap users will now be able to buy, sell, trade and store the cryptocurrency that everyone is talking about.