Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

LATEST ARTICLEs

As we move into a more digital world with enhanced security systems, so too are hackers and fraudsters. With millions of dollars lost each year at the hands of these ill actors, in this article we take a look at the 5 most common crypto scams and how to spot them. The financial world need not be a scary place, with a few precautions in place you can bank on being able to avoid them.

What is a crypto scam?

A crypto scam is a type of investment fraud revolving around cryptocurrencies. According to a report by Chainalysis, a record-breaking $14 billion of crypto was stolen last year through crypto scams. While there are many different types of crypto scams, of which we'll explore 5 below, the common thread is that crypto is wrongfully taken from a user through fraudulent activities.

The biggest crypto scam of recent times was in late 2020 when people hacked into the Twitter accounts of high profile individuals and claimed that should someone send Bitcoin or Ethereum to an address they will receive twice the value back. These accounts included the likes of Barack Obama, Elon Musk and Joe Biden.

The top 5 most common crypto scams

While there are an infinite amount of crypto scams out there, below we are highlighting the 5 most common ones.

Fake crypto exchanges

These types of exchanges provide a buy/sell platform on which users can trade cryptocurrency, however, once they have deposited the funds they cannot withdraw any money. These funds might still appear on the platform although the money is long gone.

Always read the reviews of a platform, and do your own research before depositing money anywhere.

Ponzi schemes

Ponzi schemes might have started in the late 1800s but they're still here. The scheme works in such a way that each member earns rewards by recruiting new members, whose money is then used to pay off older members. This eventually reaches a saturation point after which it collapses.

Always do your due diligence and ensure that the scheme you're investing in is solid. If it sounds too good to be true, it probably is.

Fake investment schemes

Be wary of an investment opportunity promising to deliver unbelievable gains. This might be in the form of depositing funds on a platform only to lose the money or struggle to withdraw it at a later stage. These are often circulated through well-known publications or on social media with celebrities "endorsing" the products.

Pump and dumps also fall into this category. These schemes are created when a large group of people decide to invest in a coin, only to drive up the prices and cash out at the top. Many people are then left with a worthless coin at the end, having lost their investment.

Imitating a crypto exchange

Similar to the concept of phishing, someone might create a social media account of a big exchange and contact the user "on behalf of the company". This is intended to gain your trust and is either done in an attempt to gain your passwords, or with a message that you owe large amounts in tax which needs to be paid in Bitcoin immediately to avoid imprisonment.

Never follow links in an email, rather access the site from your own browser directly and be sure to check the URL. Successful scams of this nature often have a small typo in the URL which goes unnoticed.

Malware & ransomware

The malware allows scammers to gain access to your computer, either locking you out of files or stealing credit card or crypto address details. With this information, they can drain your accounts in minutes.

Ransomware works slightly differently in that the scammers lock the entire computer and demand a ransom to gain access again. This is often paired with blackmail where the victim, and in some cases organizations, are threatened that if they don't pay sensitive information will be released. A lot of victims in this situation manage to get out of it unharmed.

These might sound very scary, but should you maintain safe online protocols and check URLs before entering your details, they should be entirely avoided.

5 tips on how to avoid crypto scams

These might sound obvious but it never hurts to read them again. Below are 5 tips on how to stay vigilant and avoid crypto scams entirely.

- Be wary of phone calls and emails claiming to be from exchanges and never click the links from them.

- Never give your password, private key or security codes to anyone.

- Never give someone remote access to your device.

- Look out for social media accounts imitating legal firms or exchanges or a prominent person in the industry. Support will never contact you from a social media account.

- And lastly, if it sounds too good to be true - it probably is.

Easily avoided, comfortably secure

We hope this information assists you in keeping your data and money secure online, proper security is always imperative when using payment methods or services on the internet. As technology evolves, so too must our security systems and vigilance. With these tips above you should be well on your way to spotting something that doesn't quite look right, and avoiding crypto scam.

Saving and investing are two key elements to managing one's personal wealth. In this article, we explore the benefits and downfalls of both these tools and give you a broader understanding of the topics.

What Does saving entail?

Saving money is an imperative step in building one's wealth and involves putting money away on a consistent basis, consistency is key. These funds are usually kept in an interest-bearing account, allowing the value to increase passively over the years.

In the United Kingdom, there are different types of ISA (individual savings accounts) that offer tax-free savings options.

In order to save, one must be spending less than they're earning.

What does investing entail?

Investing involves buying an asset with the intention for it to accumulate in value. This typically comes after saving, although the earlier the better. People invest in the likes of stocks, cryptocurrencies, property and even themselves (education, capital for a business) in the hopes of generating returns.

What's the difference between saving and investing?

The biggest difference between the two is the varying returns you can earn. Saving money in a bank account typically provides returns of 0.5 - 0.8%, while the return potential on cryptocurrencies and stock is much greater.

The other main difference between saving and investing is the risk. So, while earning higher returns on investments might sound much more appealing, the risk is usually greater. Savings accounts carry minimal risk and are usually insured while investment portfolios will rise and fall with the market and are only insured if the investment company fails. Investors should balance the options and establish which risk level they are comfortable with.

In light of these risks, savings are recommended for short term goals while investments cater better to long term financial objectives. This is because long term investments will ride out the ebb and flow of markets and recover even if there is a drop over a certain period. Savings on the other hand are more easily accessible and won't be "interrupted" if the funds are used for an emergency.

However, savings are also susceptible to inflation as the interest rates are seldom higher than the inflation rates. For example, if your bank is offering a 0.6% interest on your savings account and inflation rose 2%, your savings would have actually decreased in value. Investing typically beats inflation.

The similarities between savings and investing

As both tools are excellent at building and creating more wealth, there are bound to be similarities between the two.

The main similarity between the two is that both options are best started now, whether you're in them for the long or short term benefits. This is due to compounding. Compounding is the process where the interest you earn on an investment or savings account is continuously reinvested, increasing the base sum each period.

For example, if you put $1,000 into a compounding savings account and earned 2% interest each year. The next year you will be earning 2% interest on the lump sum plus the interest earned, $1,020. The next year you would earn $1,020.40 ($1,020 interest earned, $20.40). This doesn't sound like too much, but over a ten-year period, you would have amassed $219.20 without having done a thing.

Before you get started

Before getting started on either of these options, ensure that you have a positive cash flow and are debt-free. You'll also need to establish what your risk tolerance is, your short term and long term financial requirements, and when you would like to access the money.

If you don't have one already, you'll want to establish an Emergency Fund that can cover your living expenses for 3 - 6 months. Should you lose your job you can then fall back on this loan and not have to rely on credit cards with high-interest rates.

Experts also recommend setting up a retirement fund, with automated monthly contributions. Once your emergency and retirement funds are established, you can consider a short term savings account or long term investment, or both.

Pros and cons of saving and investing

Below we highlight the pros and cons of both tools:

Saving

Pro: Money is accessible and can easily be withdrawn.

Pro: Exempt from market volatility.

Con: Cannot leverage on market gains (potentially missing out on large compound interest benefits).

Con: Susceptible to inflation.

Investing

Pro: Longer time frames allow for favourable compounding interest.

Pro: Could tap into large market gains.

Con: Exposed to more risk as markets are susceptible to drops.

Con: May incur a penalty if the money is withdrawn too soon.

The bottom line

Both savings and investment options carry their own set of risks and rewards and it's ultimately best for you to speak to a financial adviser who is able to provide you with calculated professional advice.

Disclaimer: This article is intended for communication purposes only, you should not consider any such information, opinions or other material as financial advice. The information herein does not constitute an offer to sell or the solicitation to purchase/invest in any assets and is not to be taken as a recommendation that any particular investment or trading approach is appropriate for any specific person. There is a possibility of risk in investing as investors are exposed to fluctuations in all markets. This communication should be read in conjunction with Tap's Terms and Conditions.

Cryptocurrencies function much like traditional currencies in that they can be transferred digitally and used to pay for goods and services around the globe. However, they also pose several benefits that fiat currencies lack, such as the fact that they operate using a decentralized network and not a bank or government agency (providing greater control to users) and can execute international payments in a fraction of the time and cost.

While many believe cryptocurrencies will eventually replace traditional currencies, there is plenty to be done before we get there. We are sooner more likely to experience cryptocurrencies working alongside traditional currencies than entirely replacing them, a movement that is generating momentum each day.

Before we launch into what the industry needs in order to go mainstream, let's first observe how we reached this pinnacle moment in the history of finance.

How crypto officially got on the map

Bitcoin was created to provide an independent financial system to people that were thrown into serious debt following the global financial crisis. The digital currency was created to provide individuals with the opportunity to control their funds independently from any financial institution.

Since the advent of Bitcoin in 2009, cryptocurrencies have experienced interest from many groups of people, largely outside of mainstream media. In 2017, following a wild bull run, Bitcoin was first thrust into the mainstream media spotlight as it fast became the main topic of conversation across various news channels around the world.

Fast forward three years to the pandemic. Following global market crashes, Bitcoin displayed impressive resistance and built its wealth back more quickly than many other assets and stock markets. This caught the eye of many large corporations, dispelling scepticism and leading one in particular to move their USD reserves into Bitcoin. Following Microstrategy's decision to buy large amounts of BTC, many other large corporations followed suit, with companies like PayPal and Square even incorporating cryptocurrencies into their systems.

This wave of institutional investment not only increased the value of the markets but also helped to build confidence for retail investors to invest in such "risky" assets. This also played a large role in major corporations embarking on serious research and development of both blockchain technology and cryptocurrencies.

What crypto needs

Commonly used as an investment tool, cryptocurrencies were designed to facilitate faster and more economical transactions. Operating on a peer-to-peer basis, cryptocurrencies essentially cut out the middleman (and its fees) and make digital cash more readily available.

As with most things in life, there are two significant camps for and against the mainstream use of cryptocurrencies. Those for the widespread adoption believe the spike in interest will continue on its upward trajectory, believing that very little could hinder its growth. Those against the growth argue that fluctuating market prices and uncertainty around the practical application will hinder its mainstream adoption.

What cryptocurrencies likely need before any mainstream adoption is a well planned regulatory framework that can appease both the innovative technology and the merchants and consumers using it. Regulations are a necessary component to anything becoming mainstream, and the ones surrounding cryptocurrencies are vague at best. While many nations are working on creating and implementing these, there is still a gaping hole in the industry.

Based on conversations taking place in the banking and fintech worlds, it is highly likely that in the coming years more traditional companies will expand to offer crypto-enabled financial services. As interest and access continue to grow, companies will need to follow suit if they wish to stay in the game. Large payment processing companies like Visa and Mastercard are already looking to provide crypto services, a key indicator as to where the market is headed.

What are the advantages of Bitcoin over existing currencies?

Bitcoin, and other cryptocurrencies, pose several advantages over fiat currencies. The biggest attribute to cryptocurrencies is that they are decentralized, meaning that they are not controlled by governments or banks, rather they are issued by the network and managed by the individual holding them. Instead of a government deciding to print more money thereby increasing inflation, cryptocurrencies are inflationary and instead created using a mining system that is controlled by various mechanisms.

Using blockchain technology, the digital cash systems provide an immutable and transparent ledger that records all the transactions and ownership, ensuring that funds are handled properly and with the correct measures. Cryptocurrencies also pose a much faster and cheaper means of sending money across borders, a huge advantage for businesses operating on a global level (i.e. sending funds from the U.S. to the United Kingdom).

The biggest advantage to crypto is that it is financially inclusive. Anyone around the world can partake in the payment system with no paperwork, previous financial statements or tedious processes required, it simply requires an internet connection.

What are the disadvantages of Bitcoin compared with existing currencies?

Currently, the disadvantages of cryptocurrencies are that they are not freely accepted around the world (yet). While the adoption levels are rising there is still a gap in how and where users can spend their cryptocurrencies. Another disadvantage is the market's volatility, posing potential inconsistencies between the price when making a payment and once the payment is received.

El Salvador leads the pack

In late 2021 El Salvador became the first country to initiate Bitcoin as a legal tender alongside the US dollar. The decision has accumulated many mixed reviews, with some hailing the president a revolutionary and others concerned he will crash the country's already fragile economy. Should his plan work out we're likely to see this happen again.

In conclusion: Crypto is on an upward trajectory

With all things considered, cryptocurrencies and blockchain technology are here to stay. While cryptocurrencies might be a significant distance from becoming mainstream, they are far too integrated into our society and financial landscape to all but disappear. All things considered, the money is too great, the technology too innovative and the thought of financial inclusion too promising for any of it to go away.

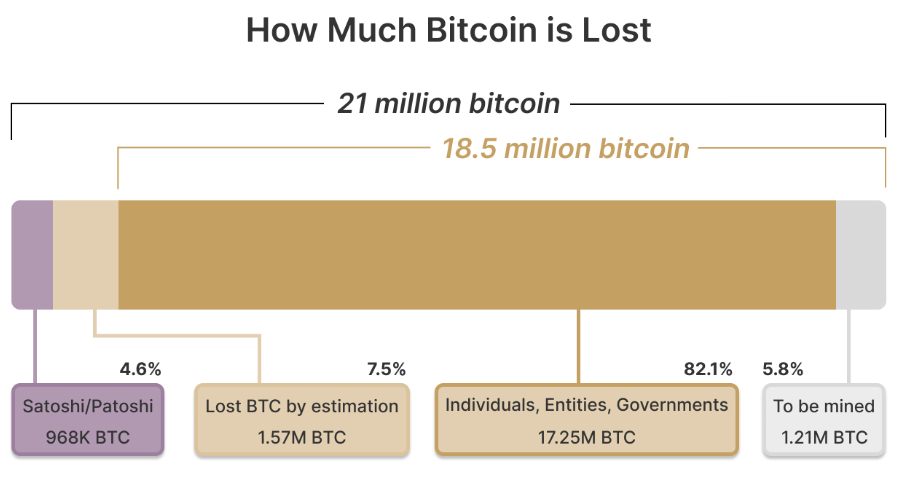

As digital assets become a core part of personal wealth, one uncomfortable question lingers: what will happen to your crypto when you’re gone? Unlike traditional assets that can be managed through banks or brokers, cryptocurrencies are bound entirely to whoever holds their private keys. Lose the keys, and the funds are gone. Permanently.

Each year, millions of dollars in Bitcoin, Ether, and other tokens vanish into the digital void when holders pass away without sharing access. It is estimated that around 1.5 million BTC (roughly 7.5% of total supply) may already be lost forever. With digital wealth now part of countless estates, preparing for the inevitable is no longer optional; it’s the responsible thing to do.

Why Planning for Crypto Inheritance Matters

In traditional finance, wealth transfer is handled through wills, trusts, and custodians. But crypto flips that model: you are the bank. Your heirs can’t simply request a password reset or call customer service. Without private keys, wallets, or access instructions, those assets are unrecoverable for all effects and purposes.

A crypto inheritance plan ensures that your digital assets, from Bitcoin and altcoins to NFTs and DeFi holdings, remain both secure and accessible to the people you choose. It bridges two crucial needs: protecting your funds today and ensuring your legacy tomorrow.

Beyond personal security, inheritance planning also reduces emotional and financial stress for your loved ones. By documenting how and where assets can be accessed, you prevent confusion and potential legal disputes.

Building the Foundation of a Crypto Inheritance Plan

Start with Legal Clarity

Consult an attorney familiar with digital assets. A properly structured will or trust should identify your crypto holdings, list beneficiaries, and outline how they can access those funds. Many jurisdictions still lack explicit laws for digital assets, so expert guidance helps ensure compliance and enforceability.

Secure Your Keys… But Don’t Overshare

The biggest challenge in crypto inheritance is private key management. If you die with your keys, your crypto dies with you. However, leaving keys in plain text within a will or document is just as risky. Instead, consider approaches like:

- Multisignature wallets, which require multiple approvals to move funds.

- Shamir’s Secret Sharing, which means splitting your seed phrase into parts distributed among trusted people.

- Encrypted backups or sealed letters stored in secure, offline locations.

Document recovery procedures in plain language so your heirs can follow them even without technical knowledge.

Choose the Right Executor

A traditional executor may not understand how to navigate crypto. You can appoint a tech-literate executor or designate a digital asset custodian to handle that portion of your estate. This ensures smooth execution and reduces the risk of errors or loss.

In a market driven by innovation and constant change, a well-structured inheritance plan offers something rare in crypto, certainty.

New Tools for a Digital Age

The rise of blockchain-based “death protocols” and smart contract automation adds a new layer of possibilities. Some platforms allow transfers to trigger automatically after certain conditions are met (for example, a verifiable death certificate or extended inactivity).

Ethereum and similar chains already support programmable inheritance systems, but these should complement, not replace, legal documents. Technology can help enforce your intentions, but law remains the foundation of inheritance.

Some investors even use “dead man’s switches”, automated systems that transfer funds if the owner doesn’t log in for a set period. While clever, it might be best to pair them with legal documents to prevent accidental activations.

Protecting Privacy While Planning Ahead

While planning for the future, it’s crucial to maintain security in the present. Avoid including wallet addresses, private keys, or passwords in public wills, which become part of the legal record. Instead, store such details in encrypted files or sealed envelopes accessible only to specific individuals.

Tools like decentralized identifiers (DIDs) and verifiable credentials can also help manage long-term identity and access rights. These systems allow you to define who can access what, and when, without intermediaries.

Custodial vs. Non-Custodial: Finding the Balance

When structuring inheritance, knowing whether your assets are held in custodial or non-custodial wallets makes all the difference.

Custodial services (like major exchanges) manage private keys on your behalf, which simplifies recovery if your heirs can provide proper documentation. However, it introduces third-party risk. Accounts can be frozen, hacked, or shut down.

Non-custodial wallets, on the other hand, offer maximum control and privacy but demand greater responsibility. If your heirs lose the seed phrase, there’s no backup plan. There’s also the possibility of taking a hybrid approach: keeping long-term holdings in non-custodial storage for security, while using reputable custodians for smaller, more accessible amounts.

Keep It Up to Date

A crypto inheritance plan is not a “set it and forget it” document. Prices change, portfolios evolve, and wallet technologies become obsolete very often. It may be wise to revisit your plan regularly, especially after major life events such as marriage, divorce, or the birth of a child.

It’s also worth keeping track of regulatory updates in your jurisdiction. Laws surrounding digital assets and inheritance are rapidly evolving, and what’s compliant today may not be tomorrow.

Common Inheritance Pitfalls

Even the best intentions can go wrong. Here are the most frequent mistakes to avoid:

- Including seed phrases directly in your will. As we mentioned before, this makes them public and vulnerable.

- Neglecting to educate heirs. Without guidance, even secure plans can fail.

- Relying solely on exchanges. Centralized platforms can fail or freeze funds.

Planning isn’t just about distributing wealth; it’s about ensuring continuity. A clear inheritance strategy preserves your crypto’s value and prevents it from becoming part of the estimated $100 billion in lost digital assets worldwide.

Protecting More Than Just Coins

Preparing a crypto inheritance plan isn’t merely about money; it’s about legacy. For all the talk about decentralization and autonomy, responsibility and forward-thinking remain at the heart of crypto ownership. By taking the time to plan ahead, you safeguard not only your wealth but also your family’s peace of mind.

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

1. Seasonality & Historical Momentum Could Kick In

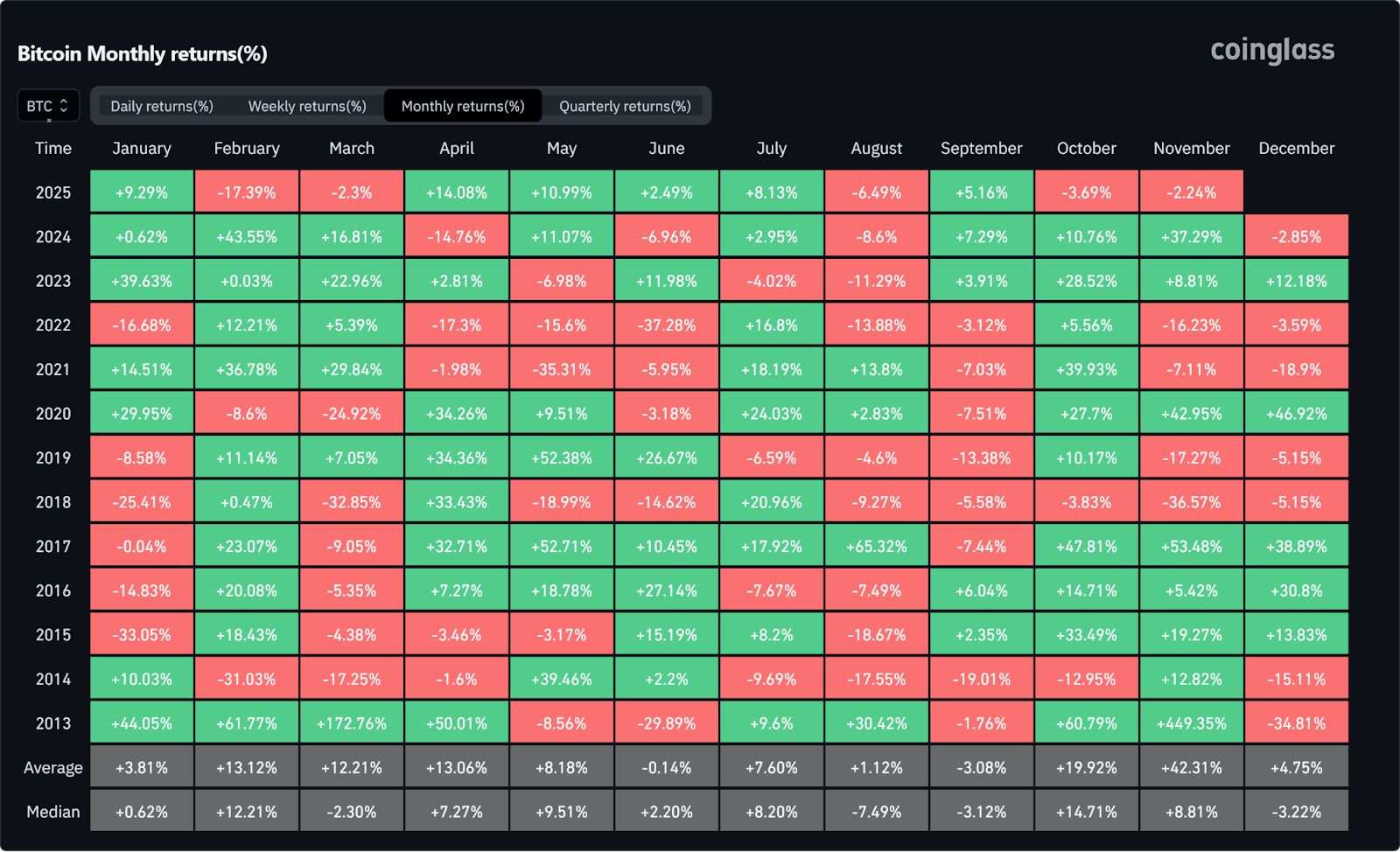

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

4. Altcoins at an Inflection Point

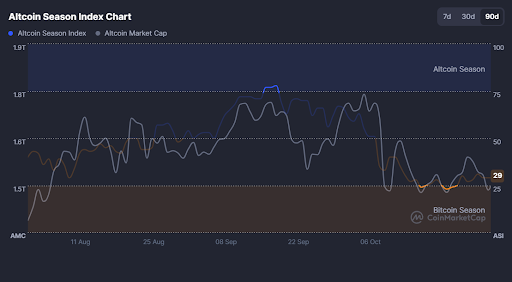

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

Currency volatility is a challenge that businesses operating across borders can’t afford to ignore. Exchange rate fluctuations can erode profits, increase costs, and create financial uncertainty, making it difficult for companies to plan effectively.

For businesses that deal with international transactions, traditional solutions like foreign exchange (forex) hedging can be expensive and complicated. Thankfully now, there's a smarter, more efficient alternative—stablecoins.

Stablecoins offer businesses a way to bypass the unpredictability of currency fluctuations by providing a digital asset pegged to stable currencies like the US dollar. The black and white of it is that they make cross-border payments faster, cheaper, and more reliable.

In this article, we’ll explore why stablecoins are an ideal solution for tackling currency volatility in global financial management.

The challenges of currency volatility in global finance

Global businesses are constantly exposed to currency risks, for a range of reasons, including:

- Geopolitical events – Trade wars, conflicts, or political instability can impact currency values.

- Inflation and interest rate changes – Central bank policies can cause sudden shifts in exchange rates.

- Market speculation – Traders and investors can drive rapid price swings.

For businesses, currency volatility can lead to higher transaction costs, as moving money internationally becomes more expensive. It can also result in unpredictable revenue, making it difficult for companies operating in multiple countries to manage pricing. Additionally, if a currency depreciates suddenly, businesses may face financial losses as profits shrink overnight.

Many businesses use forex hedging strategies (such as forward contracts and options) to manage risk, but these methods are often costly, complex, and require expert knowledge. A simpler, more efficient solution is needed—and that’s where stablecoins come in.

Why stablecoins are the perfect hedge for businesses

Stablecoins offer a practical way for businesses to protect themselves against currency volatility. Unlike traditional cryptocurrencies (which are often highly volatile), stablecoins are pegged to a fiat currency providing a reliable and steady value.

Key benefits for businesses:

- Price stability – With stablecoins, businesses don’t have to worry about sudden exchange rate swings affecting their revenue or costs.

- Fast, low-cost transactions – International payments using stablecoins settle in minutes, not days, with significantly lower fees than traditional banking systems.

- No dependence on banks – Unlike wire transfers, stablecoin payments don’t require intermediaries, reducing delays and extra costs.

- Transparent and secure transactions – Built on blockchain technology, stablecoins ensure auditable, tamper-proof payments, adding an extra layer of security.

For businesses engaging in global trade, payroll, treasury management, or e-commerce, stablecoins offer a modern financial tool to streamline operations and avoid currency-related risks.

Choosing the right stablecoin for your business needs

Not all stablecoins are created equal. Businesses need to choose the right one based on factors like trust, regulation, and network efficiency.

Top stablecoins to consider:

💰 USDT (Tether) – The most widely used stablecoin, but with some concerns around transparency.

💰 USDC (USD Coin) – Fully backed by regulated financial institutions, making it a trusted option.

💰 DAI – A decentralized stablecoin, offering stability without relying on a central issuer.

💰 EUROC (Euro Coin) – A fully backed euro-denominated stablecoin issued by Circle, providing a stable digital alternative for euro transactions.

Key considerations:

- Regulatory compliance – Ensure the stablecoin follows financial regulations in your operating regions.

- Blockchain network – Some stablecoins operate on multiple blockchains (Ethereum, Tron, Solana). Choosing the right network affects transaction speed and fees.

- Liquidity and acceptance – Businesses should opt for stablecoins with high liquidity and broad industry adoption.

Choosing the right stablecoin is essential for seamless global transactions while ensuring stability and security.

The future of stablecoins in global finance

Stablecoins are no longer just a niche tool—they are gaining mainstream acceptance among businesses, financial institutions, and regulators.

Growing adoption – Companies like PayPal and Visa are integrating stablecoins into their payment systems.

Institutional backing – Banks and investment firms are exploring stablecoin use for settlements and asset management.

Regulation on the rise – Governments are working on stablecoin frameworks, aiming to balance innovation with security.

Emerging financial products – Stablecoin-based loans, savings accounts, and remittance services are expanding the financial ecosystem.

As stablecoins evolve, their role in global financial management will only grow, making them a key tool for businesses worldwide.

Conclusion

Currency volatility remains a major challenge for businesses operating globally, as traditional hedging strategies are often expensive and inefficient, leaving companies searching for a better way to manage financial risk.

As outlined above, stablecoins offer a simple, effective, and low-cost solution to tackling currency fluctuations. By providing price stability, fast transactions, and reduced banking dependency, stablecoins empower businesses to operate seamlessly across borders.

For companies looking to future-proof their global financial operations, stablecoins are an answer worth considering. Now is the time to explore how they can be integrated into your business strategy: and we’re here to help.