Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

Latest posts

_.png)

Let's take a dive into what is Maker and its token MKR.

MKR, the governance token fueling the network, comes from the same platform that created DAI, the algorithmic stablecoin soft-pegged to the US dollar. MKR serves both the decentralized autonomous organization, MakerDAO, and the software platform, Maker Protocol, both built on the Ethereum blockchain. These two platforms generate DAI and allow users to issue and manage the DAI stablecoin.

What is Maker (MKR)?

Developed in 2015 and officially launched in December 2017, Maker is a revolutionary project that was built to host and generate DAI, a community-managed cryptocurrency that has its value soft pegged to the US dollar. The MakerDAO forms part of the larger Maker Protocol which allows DAI to maintain its value and operate without the need for a third party. The Maker Protocol requires both tokens to operate: DAI and MKR.

To understand MKR, one must first be familiar with the DAI stablecoin. DAI serves as a loan option for borrowers, with the platform allowing users to take out a loan in DAI tokens by locking another cryptocurrency, such as ETH. When the borrower pays back the DAI that was borrowed, they are able to reclaim the collateral used for their loan. However, if its value drops below a predefined level it could automatically be sold off.

The Maker ecosystem is one of the first DeFi projects to enter the market, years before the movement took off. The DeFi sector revolves around providing decentralized financial products powered by smart contracts to the masses.

Though the DAI stablecoin is best known as a service offered by the Maker Protocol, the MKR token is actually the crypto asset that secures changes to maintain its functioning. The governance token MKR gives holders voting rights over the Maker Protocol's development, such as what cryptocurrencies can be accepted as collateral and the price at which these assets will be sold if liquidation is to occur. The MKR price appreciates in value based on the success of DAI.

The Maker protocol accepts a range of cryptocurrencies, including ETH, MANA, and BAT, as collateral.

Who created the Maker platform?

Established in 2015, the Maker Protocol was developed by a team of tech-savvy developers spearheaded by Rune Christensen. As time progressed, this collective eventually organized and formed into an official entity known as the Maker Foundation, a corporation located in the Cayman Islands.

In 2017, the Maker team raised a remarkable $12 million in funding by selling MKR tokens to some of the most influential venture capital firms at the time including Andreessen Horowitz, Polychain Capital, and 1Confirmation. A year later, another $15 million worth of MKR tokens were bought by Andreessen Horowitz, who expressed the intention to help govern the DAI system by participating in the MakerDAO.

In 2019, the project raised another $27.5 million from venture firms Paradigm and Dragonfly Capital Partners for expansion to Asia.

How does the Maker Protocol work?

When the Maker Protocol launched, 1 million MKR tokens were created. These tokens gave holders voting rights on key decisions through a process called Executive Voting.

First, the sentiment of MKR holders is measured on a new proposal through Proposal Polling before committing any changes to the software. The Executive Vote then takes place, and once the highest amount of MKR token holders commits to a proposal and the vote is passed, the winning proposal is implemented into the Maker Protocol. The number of tokens holds more president than the number of token holders, i.e. 10 holders with 1,000 tokens each will outvote 100 token holders with 50 tokens each.

Non-MKR holders also have the opportunity to participate in the vote via threads in the MakerDAO forum however the MKR holders have the final say.

DAI Savings Rate

MKR holders also have a say in how much DAI holders can earn if they save DAI tokens on the platform, known as the DAI Savings Rate. In previous years this amount has varied between 0% and 8.75%. Following the recent market crash, MKR holders voted to make the DAI Savings Rate zero to encourage holders to sell their DAI and bring the price back into equilibrium.

When the DAI price drops below $1, MKR holders can vote to raise the DAI Savings Rate to encourage more users to hold DAI which increases the price.

What is MKR?

MKR is an ERC-20 token and acts as a governance and utility token to the Maker Protocol with no fixed supply. The token gains value as the use of the Maker Protocol increases as the supply is reduced when the Protocol is working effectively and increased when governed poorly. MKR tokens are created or destroyed through surplus auctions and debt auctions.

Surplus Auctions

The Maker system holds a Surplus Auction when the fees collected exceed an amount decided by MKR holders. DAI that surpasses this threshold must be purchased with MKR in order to settle the auction. This MKR is then destroyed reducing the total supply and thus increasing the token price.

Debt Auctions

Conversely, if the Maker system is underperforming its locked coins are sold for a lower value than before, causing it to raise capital via a Debt Auction. Through this process, new MKR tokens are created and auctioned for DAI. This in turn increases the MKR tokens and reduces the price.

In this light, MKR holders are incentivized to keep the platform performing optimally in order for it to generate more fees and thereby reduce the MKR supply.

How can I buy Maker (MKR) tokens?

Anyone looking to add Maker MKR tokens to their crypto portfolio can securely purchase Maker tokens through the Tap app. The mobile app allows anyone with an account to conveniently and safely purchase cryptocurrencies through an effortless trading experience.

Users can buy /sell Maker MKR tokens and safely store the tokens in the unique crypto wallet integrated into the app. Download the Tap app today to tap into the Maker ecosystem today.

Understand what market capitalization (market cap) is and how it is used to measure the value of a company or a cryptocurrency.

The term market cap is short for "market capitalisation," which refers to the financial value of a company based on the total number of its outstanding shares multiplied by their price per share. For bitcoin or other cryptocurrencies, it refers to all coins mined.

All the coins (or all of them that have been mined) in a cryptocurrency add up to its market cap. The crypto market cap refers to this sum and is used as an indicator of how valuable a cryptocurrency or a portfolio of cryptocurrencies is.

The market capitalisation of a cryptocurrency (or any other company) can be calculated by multiplying the number of coins by the current price per coin.

For example: The market capitalisation of a let's call it "Xcoin" is $6.2 billion, the number supply of "Xcoins" in existence is 16,842,100 with a price per coin of $273 which indicates to us that the market cap of the "Xcoin" is equal to $1.37 billion.

These logistics are dynamic and can change depending on the price of a token at any given moment. The infinite total of tokens is a part of the strategies implemented by cryptocurrency projects to ensure no deflation of assets can occur, giving a riser to project potential and profits.

The current market capitalisation of cryptocurrencies

The market capitalisation of the crypto-market is currently above $2 Trillion as per the 17th of August 2021, with more to gain.

Most top coins have a market cap that exceeds $1 billion which means they are in the large-cap group, this includes Bitcoin with its market cap of over $885 billion and Ethereum also well above $383 billion.

This is a good sign for the market as these two coins are among the most large-cap markets and well-known cryptocurrencies. The majority of tokens in the cryptocurrencies market are in fact small caps, with over 90 percent of them currently below $1 billion.

You can view and compare trading and market capitalisation statics on Coingecko for a more in-depth look at each crypto, whether for trading purpose or simple curiosity.

Market cap, a reliable indicator?

A high market capitalization doesn't mean a cryptocurrency is doing well. A cryptocurrency that has a large market cap might be overvalued in terms of price, what it can deliver now and in the short-term future, as well as current demand.

Some coins can have a relatively high price but low volumes because they have been issued in small numbers by only one person, one of the many market capitalisation strategies. The price is largely driven by expectations and hype, rather than the number of coins out there, giving an unwarranted riser to some tokens.

These small market cap tokens have relatively high prices but a low market capitalisation due to a low total volume of their coin supply. These tokens can be particularly risky as most of them do not come with business model plans and many of them are just new (ICOs).

Price is an important factor in any financial sector, but market capitalization (market cap) is an important data point for investors seeking to analyse and compare the value of a cryptocurrency and is often used by traders to help determine the growth potential of a cryptocurrency and if they should buy or sell the specific crypto when compared to others.

The different crypto market cap categories:

Cryptocurrencies and other digital currencies are classified by their market cap into three categories, Large-cap medium-cap and small-cap. Let's get comparing:

Large-cap (capped at $10b )

Generally speaking, coins with the highest market caps are considered to be in the large-cap group. This includes Bitcoin and Ethereum. These are considered "Lower risk" by an investor as they demonstrated a track record of growth and high liquidity which means their volume of trading can withstand a high number of sell transactions without majorly affecting the price, giving a sense of securities.

Medium-caps (capped at $1b to $10b)

The secondary level of cryptocurrencies, mostly altcoins, are considered to be a part of the medium-cap group. They are generally more volatile, but enjoy a greater growth potential than their more traditional large-cap counterparts.

Small-caps (capped at under $1b)

This last category consists of small-cap cryptocurrencies or tokens which generally don't have a market cap exceeding $1 billion. These are most susceptible to dramatic fluctuation of price based on market sentiment. An investor may vouch for them as these fluctuations are easy to make money on, but also have high potential to lose on.

Market Cap is only one way to measure cryptocurrency value, but it is an important data point for investors to consider before purchasing a cryptocurrency. Market trends, a cryptocurrency's stability, and liquidity are also important when looking at the value of a cryptocurrency.

Coin market capitalisation conclusion

Whether you are here for trading strategy analysis, or because you want to know what people mean when they say market cap, we hope this article helped with your evaluation on the differences of each market capitalisation. It's a general recommendation to have some diversification in your portfolio, don't keep all your eggs in one basket as they say. As already stated, the market cap of a blockchain technology token does not give definitive proof of whether a project will be successful or not, it comes down to plenty of variables. Brand market, social media presence, online community, and more. The market cap trend greatly depends on how old the project is, currency market supply, marketing, and more.

It is always important to do your own research before jumping in, evaluating it the project meets your needs, the team behind it, its potential in the market, and so much more. While market cap may be of some importance, it is not the only thing that makes a project successful.

Discovering the "silver to Bitcoin's gold" and its features as a peer-to-peer cryptocurrency.

Litecoin is part of the first generation of altcoins to emerge after Bitcoin ignited the crypto revolution. This peer-to-peer cryptocurrency is a popular option when it comes to transacting in the real world and crypto-enthusiasts’ portfolios, and has been a permanent feature in the top 15 biggest cryptocurrencies by market cap for years.

What Is Litecoin?

Litecoin was launched in 2011 as an alternative to Bitcoin, providing users with a faster means of transacting money over the internet. While it was never designed to replace Bitcoin, Litecoin was created to complement the original digital money. Litecoin is often referred to as "digital silver" compared to Bitcoin being referred to as "digital gold".

Litecoin is widely considered to be one of the most successful altcoins. Created as a hard fork off of Bitcoin's blockchain, Litecoin holds many similarities in the way it functions, however, the team behind the open-source cryptocurrency incorporated several features to ensure that the network operated in a faster manner.

These include changing the amount of time it takes to process transactions, the maximum total supply, the hashing algorithm, and charging very low transaction fees. Compared to Bitcoin's 21 million total supply and 10-minute transaction processing time, Litecoin has a maximum supply of 84 million LTC and can process transactions in 2.5 minutes. It also opted to use a Scrypt hashing algorithm over the SHA-256 one.

The network is known for pioneering advanced crypto features like the Lightning Network and Segregated Witness, both of which have since been implemented by the Bitcoin network.

How Does Litecoin Work?

As Litecoin is based on Bitcoin's software, they function in very similar ways. Through the Proof-of-Work consensus, all transactions are executed through mining. When a transaction enters the mempool (pool of pending transactions) it is soon picked up by a miner who will then ensure that all the details are accurate (including valid wallet addresses and available balances).

The first miner to solve a cryptographic puzzle is awarded the task of executing the transactions and in turn, earns a reward. At the time of writing the reward was 12.5 LTC, however, after every 840,000 blocks mined the reward halves in what is known as a halving reward. This mechanism is in place to manage the supply of new tokens entering circulation as each block mined releases minted new tokens.

As mentioned above, transactions are executed in 2.5 minutes, provided there is no congestion on the network, making it attractive to merchants and other service providers. The cost of making a transaction on the Litecoin network ranges from $0.03 or $.04 US cents.

Litecoin vs blockchain technology

Litecoin, like many other cryptocurrencies, is built on blockchain technology. It relies on the blockchain as the underlying technology to facilitate secure and decentralized transactions.

Litecoin transactions are facilitated by the blockchain through a decentralized ledger. When a transaction occurs, it is grouped with other transactions into a block. Miners then validate the transactions and add the block to the Litecoin blockchain. This process ensures the transparency and integrity of Litecoin transactions.

Blockchain plays a crucial role in securing Litecoin transactions by providing a decentralized and immutable record of all transactional activity. Each block is linked to the previous block, forming a chain, making it extremely difficult for malicious actors to alter past transactions. The distributed nature of the blockchain network ensures that no single entity has control over Litecoin transactions, enhancing security and trust in the system.

What gives Litecoin its value?

The value of Litecoin is determined by supply and demand, often determined by trade activity on exchanges. Due to its global liquidity and finite supply, Litecoin is a deflationary currency and has witnessed price gains over the years, making it an attractive option for participants in the global financial landscape over the years.

What is Litecoin used for?

Litecoin is a peer-to-peer payment system providing both a medium of exchange and a store of value. Due to its fast transaction times and secure network, Litecoin is often favored when making transactions that are time-sensitive, i.e. paying for a coffee or at a restaurant. LTC is widely used by merchants and service providers around the world and has experienced increased crypto adoption and participation over the last decade.

Who created Litecoin?

The Litecoin project is the creation of a former Google engineer and MIT graduate named Charlie Lee. Two years after creating Litecoin, Lee would go on to become the Director of Engineering at a large cryptocurrency exchange. In 2017, Lee rejoined the team as managing director of the Litecoin Foundation, a non-profit organization dedicated to the development of the blockchain platform and its technology.

Litecoin development and community

Litecoin's development process involves a dedicated team of developers who work on improving the Litecoin software and its functionalities. It follows a transparent and open-source approach, allowing anyone to contribute to its development and propose changes.

The Litecoin software undergoes regular updates and enhancements to ensure it remains secure, efficient, and compatible with emerging technologies. These updates often introduce new features, improve performance, and address any identified vulnerabilities.

Litecoin has a vibrant and active community that actively participates in its evolution. Community members provide feedback, report bugs, and contribute to discussions on Litecoin's future development. Their contributions range from code contributions from developers to community-driven initiatives, fostering a collaborative environment and shaping the direction of Litecoin's growth.

Learn what net worth means and how it's calculated. Then, gain insights into how to manage your personal finances and secure the bag.

Ever wondered if you're winning or losing the money game? Your net worth holds the answer - and it's easier to calculate than you think.

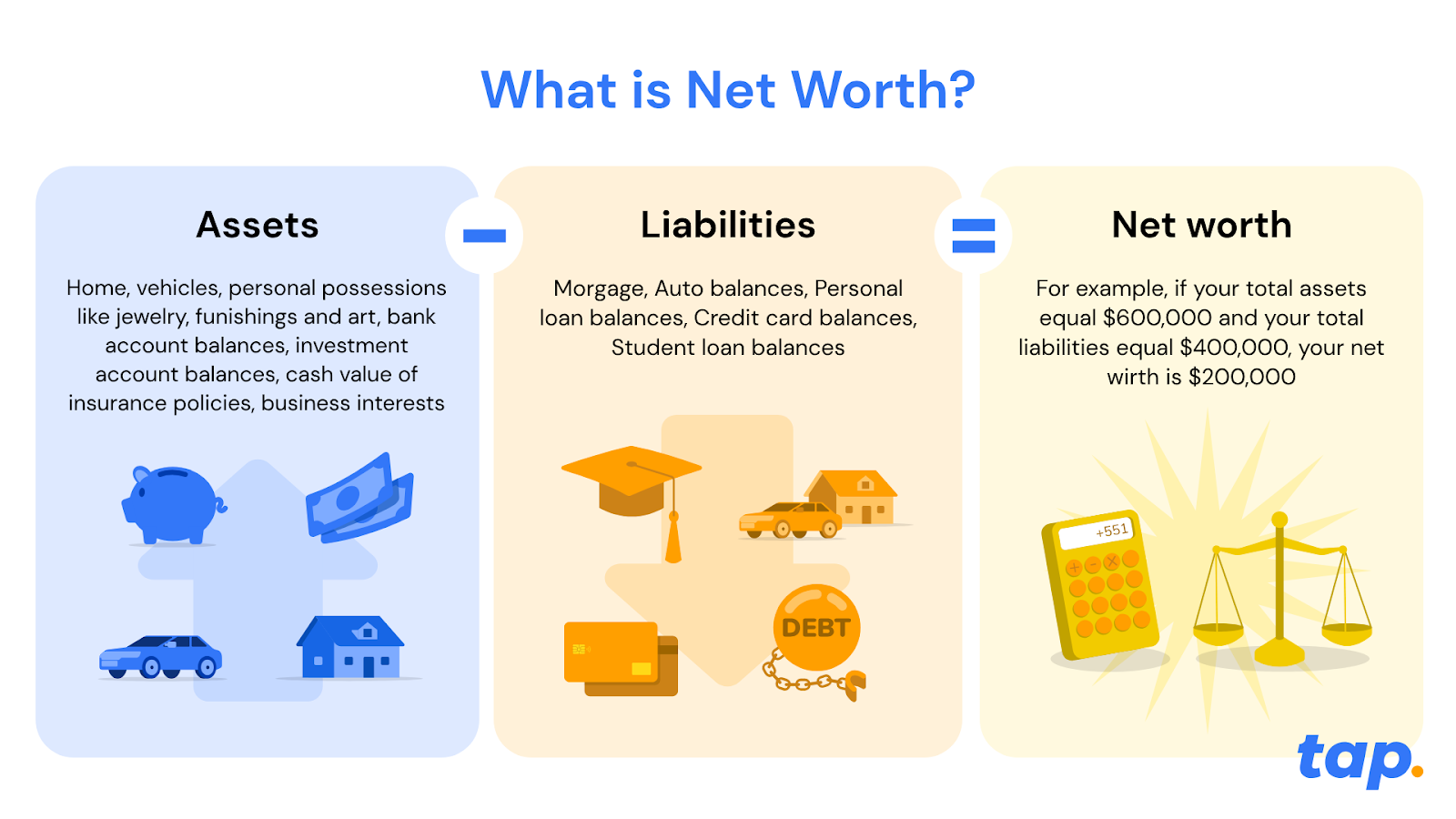

What is net worth? (and why should you care?)

Think of net worth as your financial report card. It's the ultimate measure of your financial health - not how much you earn, but how much you're actually worth.

Here's the simple truth: net worth = what you own - what you owe

Unlike your salary (which just shows your monthly income), net worth gives you the big picture. It's like comparing a snapshot to a full movie of your financial life.

Why net worth beats income every time

You might earn $100,000 a year, but if you owe $150,000 in debt with only $20,000 in assets, your net worth is actually negative $130,000. Meanwhile, someone earning $50,000 with $200,000 in assets and $50,000 in debt has a net worth of $150,000. Who's really ahead?

The net worth formula

Assets (the good stuff you own)

- Real Estate: Your home, investment properties, land

- Investments: Stocks, bonds, mutual funds, crypto

- Retirement accounts: pension funds

- Cash & savings: Bank accounts, CDs, money market accounts

- Valuable possessions: Cars, jewellery, art, collectables

- Business interests: Ownership stakes, equipment

Liabilities (what's draining your wealth)

- Mortgages: Home loans, investment property loans

- Student loans: Education debt

- Credit cards: Outstanding balances

- Auto loans: Car payments

- Personal loans: Any other borrowed money

- Outstanding bills: Medical debt, taxes owed

How to calculate your net worth (3 simple steps)

Step 1: List your assets

Add up everything valuable you own. Be honest but don't undervalue quality items.

Step 2: Total your liabilities

List every debt, loan, and outstanding balance. Yes, even that store credit card.

Step 3: Do the maths

Assets - liabilities = your net worth

Real-world examples: Meet Sarah and Mark

Sarah's success story

Assets:

- Home: $400,000

- Savings: $50,000

- Investment Portfolio: $150,000

- 401(k): $200,000

- Vehicle: $20,000

- Total Assets: $820,000

Liabilities:

- Mortgage: $200,000

- Student Loan: $30,000

- Total Liabilities: $230,000

Sarah's net worth: $590,000

Sarah's doing great! Her assets significantly outweigh her debts.

Mark's comeback journey

Assets:

- Car: $10,000

- Personal Items: $5,000

- Total Assets: $15,000

Liabilities:

- Student Loans: $50,000

- Credit Cards: $8,000

- Medical Bills: $3,000

- Total Liabilities: $61,000

Mark's net worth: -$46,000

Mark has negative net worth, but this is his starting point, not his destiny.

6 reasons why it’s beneficial to grow your net worth

Financial security

Increasing your net worth provides a foundation of financial security. As your net worth grows, you have a greater buffer against unexpected expenses, job loss, or economic downturns. It offers a safety net to navigate through challenging times and helps you maintain stability in your financial life.

Achieving financial goals

A higher net worth enables you to achieve your financial goals and aspirations. Whether it's buying a home, starting a business, funding education, or retiring comfortably, a growing net worth provides the necessary resources and financial freedom to pursue your dreams.

Building wealth

Net worth is a measure of your wealth accumulation over time. By actively growing your net worth, you increase your overall wealth and improve your financial position. It allows you to build a stronger foundation for yourself and potentially leave a legacy for future generations.

Better financial opportunities

A higher net worth opens doors to better financial opportunities. It improves your borrowing capacity, allowing you to secure favourable loan terms and interest rates when needed. Additionally, a strong net worth can attract investment opportunities and partnerships that can further boost your wealth.

Flexibility and choices

Increasing your net worth provides you with more flexibility and choices in life. It affords you the freedom to make decisions based on what aligns with your long-term goals and values, rather than being constrained by financial limitations. A growing net worth expands your options and empowers you to take calculated risks or make life-changing decisions with confidence.

Peace of mind

Knowing that your net worth is growing can bring peace of mind. It reduces financial stress and anxiety, allowing you to focus on other aspects of your life. A positive net worth provides a sense of control over your financial well-being and offers peace of mind that you are on the right track towards a secure financial future.

Tips for increasing your net worth

Boost your income

- Level up your career: Ask for raises, pursue promotions, learn high-value skills

- Create side hustles: Freelancing, online businesses, passive income streams

- Invest in yourself: Education and skills that increase your earning power

Supercharge your assets

- Diversify smartly: Don't put all eggs in one basket

- Think long-term: Focus on assets that appreciate over time

- Get professional help: Financial advisors can spot opportunities you might miss

- Review regularly: Markets change - your strategy should too

Crush your debt

- Target high-interest debt first: Credit cards are wealth killers

- Consider consolidation: Lower interest rates = more money for you

- Create a payoff plan: Set deadlines and stick to them

- Avoid new debt: Unless it's for appreciating assets

Master the long game

- Emergency fund: 3-6 months of expenses (minimum!)

- Retirement planning: Start early, contribute consistently

- Professional guidance: Sometimes paying for advice saves you thousands

- Track progress: What gets measured gets improved

The bottom line: your financial transformation starts now

Your net worth isn't just a number; it's your financial GPS, showing exactly where you stand and where you're headed. Whether you're starting with negative net worth like Mark or building on a solid foundation like Sarah, the principles remain the same.

Remember: Every financial giant started with a single step. Your current net worth is just your starting line, not your finish line.

Start tracking your net worth today, and watch as this simple practice transforms not just your bank account, but your entire relationship with money. Your future self will thank you!

Ready to take control of your financial destiny? Calculate your net worth this week and set your first wealth-building goal. The journey to financial freedom starts with knowing where you stand.

Understanding the regulations and procedures aimed at preventing fraud and money laundering in financial transactions.

Know your customer also known as "KYC" is a regulatory requirement imposed by the Financial Crimes Enforcement Network to combat money laundering, terrorism financing, and fraud prevention. The requirements for KYC are determined on an industry-by-industry and product basis. Fintech businesses and the Banking industry typically require KYC of customers who open a new account with them.

KYC ensures that financial institutions know their customers' identity well enough to understand where funds came from for deposits or how payments will be made before starting to use the company's services. KYC is an efficient first line of defense in combating terrorism financing by verifying customer identities to help identify any problem or potential links to terrorist organizations, bribery, corruption, and individuals with a history of money laundering.

KYC is an important measure in anti-money laundering regulations, making it a safety guard for cryptocurrencies. Financial institutions and regulated service providers such as Tap boast robust KYC processes to protect our consumers so that you can feel more confident that your funds will remain secure no matter the business environment or exchange circumstances.

How does it work?

Within the Finance sector in the global market, any company or project must meet strict rules and regulations that require them to have rigorous individual identification checks (also called regulatory compliance) such as verification of address information, and validation of residency status. Apart from verifying a customer's identity, it's also important to confirm the user's location and address.

Your identity documents will provide basic data like your name and date of birth, but more is needed to establish your residence, for example.

During a standard Know Your Customer process, you will be asked for several documents:

- A proof of identity (such as a passport, ID card, driving license)

- A proof of residence

- A selfie (to verify that it's you)

The KYC must be completed at the initial stage as well as on an ongoing basis so that businesses can deliver services or goods to clients. It is a best practice for any business offering financial services to re-verify the identity of their customers at regular intervals to ensure AML. Sometimes new customers have to go through several steps of verification before they can start any financial transaction/exchange using the service of the company.

Failing to adhere to KYC regulations can lead to reputational damage and penalties served by the body in charge.

KYC around the world

KYC regulations can vary from country to country, but there is a lot of international cooperation on the basic data information needed. For example in the United States, KYC and AML processes are driven by financial crime prevention legislations such as The Bank Secrecy Act (2001) and Patriot Act (2006).

Internationally, there's a consensus that the FATF should lead in coordinating multinational cooperation on regulatory conditions. This ensures consistency and effectiveness in combating financial crimes like money laundering and terrorist financing.

The benefits

In spite of the time it takes to set up accounts, KYC identity verification is worth it when taking into account the benefits: keeping your funds safe, and protect you from identity theft, fraud, and other illegal activities is largely the result of robust KYC control. These procedures ensure that financial service providers are not only safe but trustworthy. Trade crypto with confidence with regulated companies like Tap boasting robust KYC procedures to safeguard its customer assets and information.

In conclusion

KYC is a common regulatory requirement that financial service providers are obliged to fulfill in order for businesses to operate under the law and consumers should take KYC seriously. KYC requirements differ across the financial sector. It is a necessary measure in anti-money laundering regulations, making it an important safety guard for cryptocurrencies as well as customer assets by preventing fraudulent activity. KYC in the Fintech or Bank sector is generally imposed on new customers who open a new account and typically involve on-going monitoring.

Discover the impact of impermanent loss on your cryptocurrency holdings. Learn why understanding this concept is essential for any trader.

The DeFi scene has exploded in recent years, with a number of successful protocols contributing to the rising volume and liquidity (Uniswap, PancakeSwap, and SushiSwap to name a few). While these protocols have entirely democratized trading in the crypto space, there are still some risks associated with getting involved.

If you have experience in DeFi trading you’ve likely come across this term. Impermanent loss refers to losses made as a result of the price changes of the digital assets from when the liquidity provider deposited them into the liquidity pool to now. Below we break down how impermanent loss happens and how to manage the risk.

How does impermanent loss happen?

Impermanent loss is when the price of the digital asset changes from the time you deposited it, providing liquidity to a liquidity pool, to the time you withdrew it. The bigger this change, the bigger the loss (essentially less dollar value at the time of withdrawal). There are of course ways to mitigate impermanent loss.

Liquidity providers' exposure to impermanent loss is decreased when trading in pools with assets that have smaller price ranges, like stablecoins (a stable asset) and wrapped versions of coins for example. In these cases, liquidity providers can provide liquidity with a lower risk of impermanent loss.

In some cases, impermanent loss can also be counteracted by trading fees. Liquidity pools exposed to a high risk of impermanent loss can still be profitable thanks to lucrative trading fees.

For example, Uniswap offers liquidity providers 0.3% on every trade, so if the pool has a high trading volume, liquidity providers can still make money even if exposed to impermanent loss. This will depend on the protocol, deposited assets, specific pool, and wider market conditions.

What does impermanent loss looks like for liquidity providers in liquidity pools?

Here is an example of what impermanent loss might look like for a liquidity provider trading on automated market makers (AMM).

Say John finds an automated market maker that requires a pair of digital assets equating to the same value. For the sake of this example, say 1 ETH is equivalent to 1,000 USDT, which he deposits in a liquidity pool. The total value of his deposit, therefore, sits at $2,000.

Other liquidity providers have contributed a combined offering of 10 ETH and 10,000 USDT into the liquidity pool, meaning that John holds a 10% share of the overall liquidity pool.

Let's say that the price of ETH rises to 4,000 USDT. During this time, arbitrage traders will contribute USDT to the liquidity pool and remove ETH until the ratio reflects the price increase. Note that AMMs don't have order books. Instead, the price of assets is determined by the ratio between them in the liquidity pool, meaning that while the liquidity remains constant, the ratio of assets in it changes.

In this case, if the price of ETH is now worth 4,000 USDT then the arbitrage traders will work to ensure that the liquidity pool now holds 5 ETH and 20,000 USDT. The liquidity pool's total liquidity is now worth $40,000.

If John decides to withdraw his funds, he's entitled to 10% of the liquidity pool's share based on his initial deposit and the size of the liquidity pool. He, therefore, is entitled to withdraw 0.5 ETH and 2,000 USDT, equating to $4,000 in value. However, if he'd kept the initial 1 ETH and 1,000 USDT this would be worth $5,000 now.

In this case, John would have made bigger returns had he hodled instead of using the liquidity pool and this is what impermanent loss is all about.

This example does not incorporate trading fees that John might have earned for providing liquidity to the liquidity pool. In many cases, these fees would cancel out the losses and make the process profitable. Either way, understanding what impermanent loss is, is imperative before providing liquidity in the DeFi space.

A look at impermanent loss vs price increases (excl trading fees)

So, impermanent loss happens when the price of the cryptocurrency assets in the liquidity pool changes. But how much is it exactly? Note that it doesn’t account for fees earned for providing liquidity.

Here is an overview of the impermanent losses incurred due to asset price increases (note that trading fees are not factored in here). Impermanent loss examples:

1.25x price change = 0.6% loss

1.50x price change = 2.0% loss

1.75x price change = 3.8% loss

2x price change = 5.7% loss

3x price change = 13.4% loss

4x price change = 20.0% loss

5x price change = 25.5% loss

Note that impermanent loss happens whether the price both increases or decreases as it is calculated by the price ratio relative to the time of the initial deposit into the liquidity pool. Unfortunately in these cases, price volatility leads liquidity providers to lose money.

The risks associated with becoming a liquidity provider

Realistically, impermanent loss isn't the best name. The losses are known as "impermanent" because they only become evident when you withdraw your coins from the liquidity pool. However, the "temporary loss" then becomes pretty permanent. Although the fees might be able to compensate for those losses, it does seem like a somewhat deceptive title.

When you put cryptocurrency assets into an AMM, be cautious. Some liquidity pools are far more vulnerable to fleeting losses than others, as we've discussed above. As a general rule, the more volatile the assets in the liquidity pool are, the greater your chance of being exposed to impermanent loss. It's also preferable to start by depositing a little bit of money in a liquidity pool to see the returns before exposing a lump sum.

Another thing to keep in mind is to look for more established, tried-and-true AMMs. It's fairly simple to fork an existing AMM and make a few modifications thanks to DeFi. However, this might introduce bugs that lock your funds in the liquidity pool indefinitely. If a liquidity pool promises exceptionally high returns, there's more than likely a tradeoff taking place and there's likely to be much higher risk associated. Be sure to understand the ins and outs of any liquidity pool before making any deposits.

News and updates

Bitcoin December Outlook: Will BTC Deliver a Holiday Rally Before 2026?

Bitcoin rebounded and now sits at a crossroads. Discover what whale accumulation, macro developments, and key technical levels signal for the end of 2025.

Bitcoin's Comeback: Three Forces That Could Make or Break it

Bitcoin is a long way from reclaiming its all-time high and stuck under $92,000, but three powerful forces could flip the script sooner than you think.

The Surge After the Storm: What’s Next for Bitcoin and the Market

After a brutal October sell-off, crypto just staged one of its most dramatic comebacks yet. Here's what the market's resilience signals for what comes next.

Decoding the disconnect: America's cautious approach to crypto

Bitcoin and the broader crypto market have soared to a staggering $2.1 trillion in value, but why does skepticism still linger among so many Americans? Here is a deep dive into the current trust gap.