Learning the friendly way

Dive into our resources, guides, and articles for all things money-related. Grow your financial confidence with our experts curated tips and articles for both experienced and new investors.

Latest posts

Discover the world's weakest currencies and the factors that affect them.

As we all know, money talks. However, we should say that certain types of money speak while others just whisper. Global finance is an uneven playing field, not all currencies stand on equal footing. Some are strong like steel, and some fade like an ice-cream in the blazing heat of summer.

So, which is the weakest currency in the world? The Lebanese Pound (LBP) holds this dubious title at present. The value is so low that 1 USD = ~ 89,500 LBP. To put that in perspective, you’d need a briefcase to carry $100 in Lebanese pounds, if you could find that many actual bills, that is.

A weak currency is not simply one with a large number of zeros after the decimal point. It has more to it. It includes inflation rates, political stability, monetary policy, and investor confidence. Given that, this time, we will discuss the weakest currencies in the world as of 2025. We will understand the economics behind them and its implications on the respective countries.

Top 10 weakest currencies in the world (2025)

Here are the top 10 weakest currencies in the world. If you are travelling to any of these countries don’t be surprised if your wallet starts to feel like a sack of potatoes.

Exchange rates are approximate and fluctuate daily. Data compiled from multiple financial sources as of July 2025.

What makes a currency weak?

Now, before we go on to list all the zeroes, we first have to clarify what exactly a weak currency is. The exchange rate tells you how much of one currency is required to purchase another currency. You can use any currency as a benchmark, although most are pegged to the U.S. dollar. But here’s the thing: just because a currency has a low exchange rate doesn’t necessarily mean that it’s a sign of weakness. It’s like clothes sizes or shoe sizes. Just because it’s a bigger number doesn’t mean that it’s bad.

Now, what are the causes of a weak currency? Well, here are some:

- Persistent inflation that eats away at value

- Short-term monetary policies that undermine long-term confidence

- Trade imbalances and shrinking foreign reserves

- Political instability that rattles investor trust

A weak currency can be a sign of underlying economic pressure. But if investors get nervous, capital can shift quickly and the exchange rate is one of the first places to show the strain.

Country spotlights: case studies behind the weakest currencies

Lebanon | A financial collapse without precedent

Want a lesson in how not to manage an economy? Lebanon is the one. Currently (as of mid-2025) the exchange rate is 1 USD = 89,500 LBP. The crisis started with a banking system that was effectively a government-supported Ponzi scheme. Banks offered high interest rates to lure deposits, then invested most of the money in a highly-indebted government. Once confidence was lost, the house of cards collapsed. On top of this, the 2019 protests and the Beirut port blast in 2020 pushed the economy into a terminal spin.

Now Lebanese are living in a strange economic environment where ATMs only dispense a few dollars at a time and many shops unofficially price goods in USD. A shadow economy runs in parallel to the official one. When trust in institutions fails, people find their own workarounds.

Iran | Sanctions, inflation, and isolation

Sanctions mean Iran is unable to access the international banking system, which in turn means its oil based economy can’t get value for its largest export. It’s like having a collection of Ferraris, but not the keys to unlock them. Iran has tried to circumvent sanctions by investing in cryptocurrencies and a barter system but nothing seems to be able to arrest the rial’s slide.

Inflation is normally in excess of 40%, so Iranians have bought gold, property and U.S. dollars as a way to protect whatever purchasing power they have. The rial is a classic example of the dangers of prolonged isolation.

Vietnam | Weak by design, not disaster

The exchange rate with the dollar is 26,000 VND. The thing is, though, it’s different from the last two. That isn’t a sign of trouble, but the product of deliberate policy.

Vietnam keeps the dong weak, so that the country can sell exports more cheaply, a process known as competitive devaluation. It’s an unconventional policy, but it’s helped Vietnam become a global manufacturing hotspot for companies looking to diversify out of China. It’s as if the entire country is on perpetual sale. Foreigners like the prices, and Vietnamese factories stay busy. Everybody wins. The government just needs to balance things to avoid the inflationary pitfalls that have crippled other nations on this list.

Laos | Trapped by debt and dependency

The Laotian kip now trades at around 21,800 LAK per USD. An inflation over 25% and a debt-to-GDP ratio over 125% put a lot of pressure on the currency. Much of the debt is owed to China for infrastructure projects that haven’t yet paid off economically.

Laos is a landlocked country with limited industrial capacity, and it has high import dependence. This situation leaves its currency exposed whenever commodity prices shift. If the trajectory of the Laotian kip shows us anything, it’s the deep economic vulnerabilities Laos is subject to.

Sierra Leone | A currency redefined, but still fragile

In 2022, Sierra Leone redenominated its currency, removing three zeros from the leone to simplify transactions. But even the new leone remains weak due to decades of disruption. Civil war, the Ebola outbreak, COVID-19, and swings in diamond prices.

This is an economy that’s faced shock after shock, and its recovery is very slow. The mining sector (especially diamonds) still dominates, which leaves the currency vulnerable to commodity price drops. Healthcare challenges and limited infrastructure add even more pressure, affecting the overall productivity and increasing fiscal strain.

Why some countries choose to keep their currency weak

As we discussed, some countries, Vietnam, for example, want a weak currency for excellent reasons. It’s like wanting to drive in the slow lane. It's counterintuitive. But it works.

When a currency is weak, it’s cheaper for other people to buy things from you. It’s like a perpetual discount. German cars may be nice, but if a Vietnamese motorcycle is 70% cheaper because of currency valuations, which do you think will sell more?

Countries like China famously kept their currency artificially weak for years. It was one of the reasons they could become the factory of the world. They were so successful that people accused them of “currency manipulation.” It’s like they were so good at a game that people cried foul. But this is a double-edged sword.

First, it makes imports very expensive. That means everything from oil to smartphones becomes more expensive for people inside the country. Second, prolonged currency weakness can lead to capital outflow, as even the rich and well-off within the country start to send their money out. If your own citizens do not have faith in your currency, it may be all the more difficult to persuade others to get in.

Does a weak currency mean a weak economy?

We already know that a weak currency is not a sign of an economy’s impending doom. It could simply be a result of different economic and historical realities. Indonesia and Vietnam are perhaps the two most prominent examples of countries with technically weak currencies and economically stable economies. Despite the need for calculators to work out the value of their currencies, both have grown steadily, lowered their poverty rates, and diversified their economies.

The answer is in purchasing power parity (PPP). It doesn’t matter how many zeroes there are after the currency symbol, it matters what those zeroes can buy. That is what matters. Just because a Vietnamese worker makes 10 million dong a month, doesn’t mean they are impoverished if that money buys them a good standard of living in the context of the Vietnamese economy.

So, how should we gauge a nation's economic strength? The answer is: look at the employment rate, rate of productivity, infrastructure investments, and standard of living. A nation with a "weak" currency that offers rising wages, improving infrastructure, and increasing opportunities is more prosperous than one with a "strong" currency and shuttered factories.

What are the consequences of a weak currency?

A devalued currency leads to a higher cost of living, as the price of essentials such as food, gasoline and electronics increases. The same thing happens to savings, and capital flight increases as money flows out of the country to be converted into a more solid currency. Eventually, foreign money supplants the local one, undermining the government’s ability to steer the economy.

Final thoughts

Currency weakness is more than numbers. We’ve learnt that it can both expose deep economic flaws but also reflect deliberate strategies for growth. Lebanon and Iran highlight how instability and isolation can erode value quickly, while Vietnam shows how weakness can fuel exports and development. Each case is unique.

These disparities shape the country’s trade, capital flows, and financial stability worldwide, which causes a wider ripple effect. In a global economy, no currency moves alone; each affects the rest. And behind every weak currency there are real people navigating inflation, opportunity, or uncertainty.

Discover the world’s strongest currencies in 2025: what drives their value, why they dominate global markets, and how currency strength shapes trade, investing, and travel.

Currency strength shapes global trade, investment flows, and your real-world spending power. But strength isn’t just about flashy exchange rates. It’s backed by low inflation, investor trust, and governments that don’t spontaneously combust.

In this guide, we break down the top 10 strongest currencies in the world for 2025. You'll learn what drives their dominance, why some currencies outperform others, and what this means for markets, businesses, and travellers alike.

Spoiler: it's not always the ones you expect.

Before we begin: Currency strength is measured by exchange rate value against major currencies like the USD and GBP, combined with factors including economic stability, inflation rates, trade balances, and investor demand.

The strongest currencies typically emerge from countries with sound fiscal policies, political stability, strong export economies, and substantial foreign reserves.

Top 10 strongest currencies in the world (2025 ranking)

The following currencies dominate global markets by exchange rate value against the USD and GBP. These rankings reflect the current market conditions at the time of writing.

1. Kuwaiti Dinar (KWD)

Exchange Rate: 1 KWD = 3.25 USD | 2.44 GBP

The Kuwaiti Dinar isn’t just strong - it’s consistently the world’s strongest. Fueled by vast oil reserves and a government that actually knows how to manage money, Kuwait punches well above its weight. A small population + massive petroleum wealth = eye-watering per capita income, and a currency that commands global respect.

Back in 2007, Kuwait ditched its US dollar peg for a currency basket, a bold move that gave it more control and resilience. Add in one of the largest sovereign wealth funds on the planet and a no-nonsense approach to spending oil money, and you’ve got a textbook case in currency strength.

2. Bahraini Dinar (BHD)

Exchange Rate: 1 BHD = 2.65 USD | 2.05 GBP

The Bahraini Dinar may not get the headlines, but it holds its ground thanks to a rock-solid USD peg and a thriving financial sector. As a gateway to the Gulf, Bahrain has built a reputation as a banking and investment hub, with the regulatory chops to back it up.

While oil still plays a role, the kingdom’s smart pivot into finance, tourism, and services has given the BHD more than one leg to stand on. Add close ties to Saudi Arabia and deep integration with the wider Gulf economy, and you've got a currency that’s quietly powerful and built to last.

3. Omani Rial (OMR)

Exchange Rate: 1 OMR = 2.60 USD | 1.92 GBP

Oman’s currency doesn’t just ride the oil wave - it’s powered by long-term vision. While crude still plays a role, the Omani Rial stands tall thanks to the country’s steady shift toward tourism, logistics, and manufacturing, all part of its ambitious Vision 2040 roadmap.

In a region known for volatility, Oman sets itself apart with political stability, disciplined fiscal policy, and a refreshingly balanced economic game plan. The result? A currency that’s not just strong, but built on more than just barrels.

4. Jordanian Dinar (JOD)

Exchange Rate: 1 JOD = ~1.41 USD | 1.08 GBP

Jordan doesn’t have oil fields or massive exports, but it does have one of the most stable currencies in the region. Pegged to the USD since 1995, the Jordanian Dinar has held firm through geopolitical shocks and economic headwinds.

What’s the secret? A central bank that plays it straight, a government that manages its books carefully, and a commitment to stability - even while supporting large refugee populations and navigating limited natural resources. In short: smart policy over raw power.

5. British Pound Sterling (GBP)

Exchange Rate: 1 GBP = 1.35 USD

As the world’s oldest currency still in circulation, the British Pound carries serious legacy power, but it’s more than just tradition. Backed by the UK’s diversified economy and London’s role as a global finance heavyweight, the pound remains one of the most widely held reserve currencies on the planet.

Let’s call a spade a spade. While Brexit brought its fair share of turbulence, the fundamentals haven’t changed: a strong legal system, deep capital markets, and world-class financial infrastructure keep the GBP firmly in the heavyweight league.

6. Cayman Islands Dollar (KYD)

Exchange Rate: 1 KYD = ~1.20 USD | 0.89 GBP

With more registered companies than people, the Cayman Islands punch way above their weight in global finance. The KYD benefits from this offshore powerhouse status, where financial services and tourism drive steady demand.

Pegged to the US dollar, the currency stays stable, while the islands’ investor-friendly regulations and tax perks keep international capital flowing. It’s a niche economy, but a well-oiled one, and the KYD reflects that strength.

7. Gibraltar Pound (GIP)

Exchange Rate: 1 GIP = 1 GBP (perfect parity)

The Gibraltar Pound holds a 1:1 peg with the British Pound, giving it the full weight of UK monetary policy with a distinctly local twist. It’s a territorial currency that does more than just mirror the GBP; it powers a compact but strategic economy.

Perched at the gateway to the Mediterranean, Gibraltar leverages its prime location and tight financial regulation to attract investment and business. The result? A stable, trusted currency backed by both geography and governance.

8. Swiss Franc (CHF)

Exchange Rate: 1 CHF = ~1.10 USD | 0.88 GBP

Listen, the Swiss Franc doesn’t just symbolise stability - it sets the standard. Backed by political neutrality, low inflation, and one of the world’s most trusted banking systems, the CHF is where capital goes when things get shaky.

The Swiss National Bank’s conservative approach and Switzerland’s strict fiscal discipline make the Franc a magnet for investors seeking security. In times of global turbulence, the CHF doesn’t flinch, it holds.

9. Euro (EUR)

Exchange Rate: 1 EUR = ~1.05 USD | 0.84 GBP

The Euro ties together 20 EU countries under one economic flag, creating a currency backed by a collective economy even bigger than the U.S. Despite political bumps and economic contrasts across member states, the EUR holds its ground as the world’s second-most traded currency.

What keeps it strong? The European Central Bank’s monetary oversight, the eurozone’s combined economic weight, and the Euro’s deep role in global trade and reserves. It’s not just shared money, it’s shared strength.

10. United States Dollar (USD)

The global standard

The USD may not top the exchange rate charts, but some might argue that it owns the global stage. Involved in nearly 88% of all forex trades and held as the primary reserve currency by central banks worldwide, the dollar is the backbone of international finance.

Its strength isn’t necessarily about value per unit, it’s about reach. From oil pricing to cross-border deals, the USD is the language of global trade, powered by the world’s largest economy and the deepest capital markets on earth.

What makes a currency strong?

Strong currencies aren’t just about optics: they’re built on trust, economic fundamentals, and global demand. The world’s top performers all share a few key traits that keep investors confident and capital flowing.

So, what drives currency strength?

At the core, it’s about stability and credibility. Countries with steady politics, transparent institutions, and clear economic policies tend to attract global investment. High interest rates - when balanced with low inflation - pull in foreign capital, while low inflation protects the currency’s real-world value.

Trade matters too. When a country exports more than it imports, global buyers need the local currency, driving demand and pushing up value. Large foreign exchange reserves also give central banks firepower to defend their currency when markets wobble.

Debt is another big one. Lower debt-to-GDP ratios signal fiscal discipline and room to manoeuvre during economic shocks, key ingredients for long-term currency trust.

Pegged vs floating exchange rates

Currencies typically fall into two camps: pegged or floating.

- Pegged currencies (like the Bahraini Dinar or Jordanian Dinar) lock their value to another, usually the US dollar - yes, just like stablecoins. This provides predictability for trade and investment, but demands strict monetary control and healthy reserves to keep the peg in place.

- Floating currencies (like the Swiss Franc or British Pound) let market forces do the work. That means more volatility, but also more flexibility when shocks hit, if central banks know what they’re doing.

Both systems have their strengths. The key is whether the country can maintain trust through smart policy, solid reserves, and consistent economic performance.

Honourable mentions

While these currencies didn’t make the top 10, they still offer stability, liquidity and are backed by solid economic fundamentals.

These currencies benefit from resource wealth, strong institutions, or strategic economic positions that support their value in global markets.

How is currency value measured?

Currency strength isn’t measured in a vacuum, it’s always relative. Exchange rates compare one currency against another (like USD/EUR), and those prices shift constantly based on supply, demand, and investor sentiment.

In deep, liquid markets, these rates reflect what the world thinks about a country’s economy, stability, and future outlook. Big trades happen fast and without much friction because major currencies have enough volume to absorb them.

Central banks keep a close eye on all this. In floating systems, they rarely intervene unless things get choppy. But day to day, it’s market forces that drive currency values, shaped by fundamentals and the collective mood of global finance.

What is the most stable currency in the world?

No drama, no surprises: the Swiss Franc is the gold standard for currency stability. Backed by political neutrality, low inflation, and ultra-consistent monetary policy, the CHF has earned its reputation as a safe-haven asset.

The Swiss National Bank doesn’t chase headlines. Instead, it focuses on one thing: price stability. And it’s done that with surgical precision for decades. Add in a political system designed for consensus and slow, steady change, and you get a currency that markets trust, especially when things get rough.

In times of crisis, global capital flows to the Franc. That trust? It reinforces the CHF’s strength, year after year.

What is the most traded currency in the world?

Likely no surprises here either: The dollar is (currently) the backbone of the world’s financial system. Accounting for nearly 90% of all forex trading, it’s the go-to for everything from central bank reserves to international commodity pricing.

Around 60% of global foreign exchange reserves are held in USD, and even countries with no direct US ties use the dollar to price and settle trades. This widespread use creates powerful network effects - the more the dollar flows, the more stable and liquid it becomes, drawing in even more users.

It’s a self-reinforcing cycle, fueled by the sheer size and strength of the US economy.

Conclusion

Currency strength goes beyond daily exchange rates. It’s a reflection of a nation’s economic health, fiscal discipline, and political stability. While rates bounce around day-to-day, the core drivers of strength are built to last.

Knowing what fuels currency power isn’t just academic, it’s critical for smart investing, international business, and even planning your next trip. The strongest currencies aren’t just the ones with high numbers, they’re the ones backed by solid economics and trusted institutions that keep value steady over time.

Is USDT safe? Explore how Tether works, what backs it, key risks, and why it remains the most-used stablecoin despite regulatory and transparency concerns.

USDT is everywhere in crypto: powering trades, bridging platforms, and acting as a go-to safe haven when markets turn volatile. Backed by Tether, it promises the stability of a dollar with the speed of digital assets. But how secure is that promise?

In this article, we’ll unpack how USDT works, the risks beneath the surface, and why it remains a key player in the crypto economy.

What is USDT and why it matters

Think of USDT (Tether) as the crypto world's attempt to create digital cash that doesn't give you a heart attack every time you check its price. Launched back in 2014 by a company called Tether Limited, USDT was designed to be a "stablecoin" - a cryptocurrency that maintains a steady 1:1 relationship with a certain fiat currency: the US dollar. One USDT should always equal one dollar. Simple, right?.

Well, like most things in crypto, it's a bit more complicated than that.

USDT has become the utility tool of crypto, offering a fast and flexible option to move in and out of positions without cashing out to traditional fiat. It’s the common language of the crypto ecosystem, enabling smooth transfers, seamless trading, and a place to park value when markets swing.

Tether Limited, the company behind USDT, operates globally, with roots in the British Virgin Islands and operations stretching from Hong Kong to the Bahamas. Unlike central banks, Tether isn’t printing dollars, though: it issues tokens, claiming each one is backed 1:1 by assets in reserve.

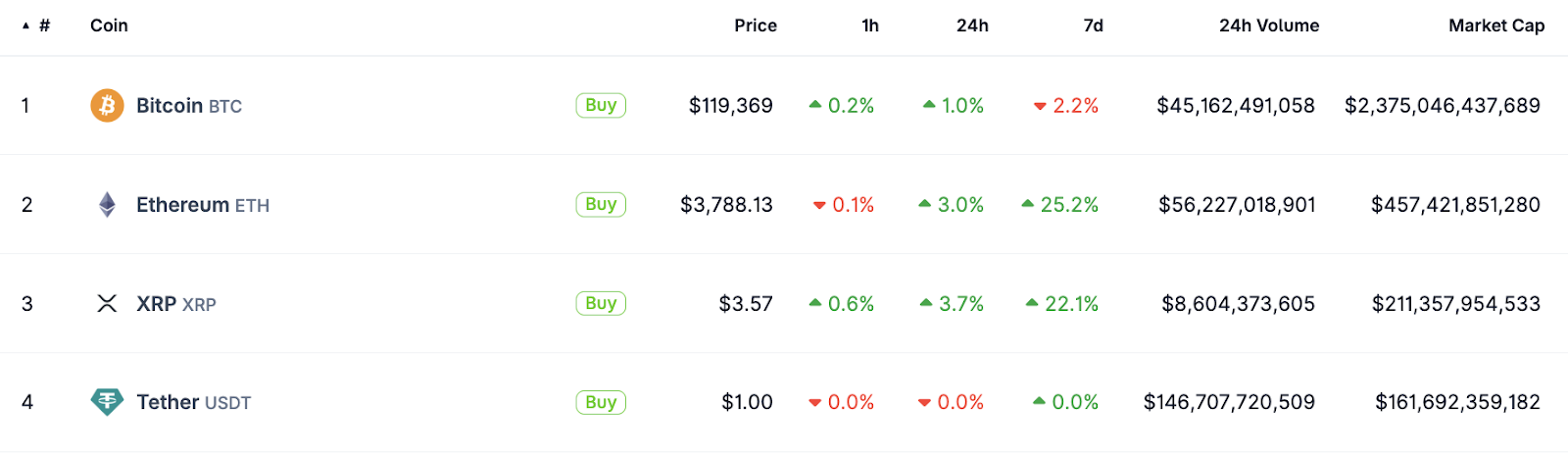

With over $160 billion in circulation as of mid-2025, USDT isn’t just a trading tool, it’s foundational infrastructure for the crypto economy. It’s also the largest stablecoin on the market, based on market cap and 24-hour trading volume.

Top cryptocurrencies by market cap at the time of writing. Source.

Is USDT safe?

The short answer? USDT exists in a grey area between "reasonably safe for what it is" and "proceed with caution."

The slightly longer answer? Here's what you need to know at a glance:

What's working:

- Maintained its dollar peg through multiple market crashes

- Backed by a mix of cash, government securities, and other liquid assets

- Most widely accepted stablecoin across exchanges and platforms

- Regular attestations from accounting firms

What's concerning:

- Limited transparency compared to some competitors

- Regulatory uncertainty and past legal issues

- Concentration risk (too big to fail, too big to save?)

- Not fully backed by cash alone

The reality check: USDT has survived crypto winters, bank runs, and regulatory pressure for nearly a decade. While it's not risk-free (nothing in crypto is), it's proven more resilient than many predicted. For short-term trading and payments, most users find it reliable. For long-term wealth storage? That's where you might want to consider your options more carefully.

How USDT is backed: understanding Tether's reserves

Here’s where things get more complex and where much of the scrutiny around Tether lies.

In simple terms, USDT operates like a digital receipt: you deposit dollars, and in return, you get tokens you can use across the entire crypto ecosystem. But what happens to those dollars? Are they sitting in a vault, or being put to work?

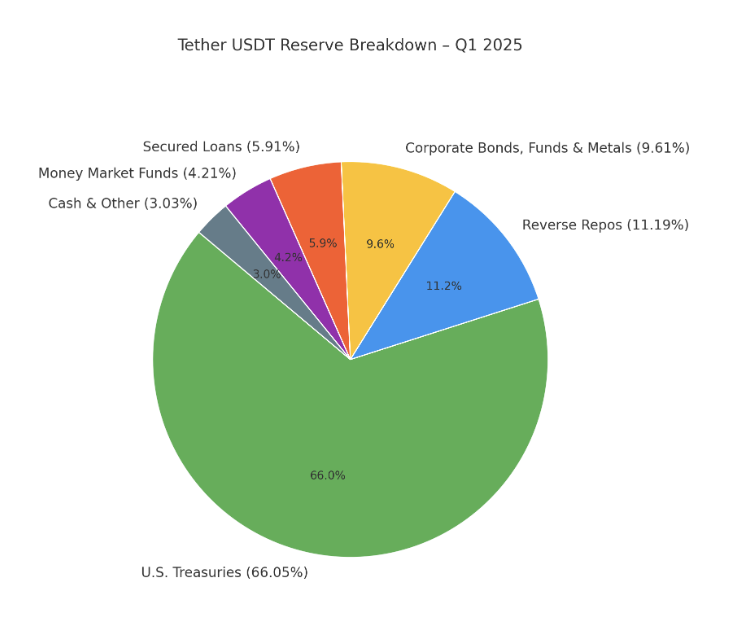

Tether has long opted for the investment route. Instead of holding pure cash, it backs USDT with a diversified portfolio of assets. According to its Q1 2025 attestation from BDO, Tether’s reserves looked roughly like this:

The shift toward U.S. Treasuries and away from riskier assets marked a significant improvement in its reserve quality. While not fully audited, Tether does publish quarterly attestations from BDO, providing some visibility into how reserves are managed. It’s not a full audit, but it’s a step forward from the opaque reporting of earlier years.

That being said, past controversies still shape how Tether is perceived. In 2019, Tether admitted that USDT was not fully backed by cash at all times and revealed it had lent $850 million to Bitfinex, its sister company. This led to a high-profile settlement with the New York Attorney General in 2021, requiring Tether to improve transparency and cease operations in New York.

Again, to put it in simple terms: imagine your bank quietly loaning out customer deposits to a related company without clearly telling you. Not necessarily illegal, but definitely a breach of trust for users expecting a 1:1 backed stablecoin.

Regulatory scrutiny & legal risks

If USDT were a person, it would probably have a thick file folder in regulatory offices around the world. Sure, being the largest stablecoin makes you a big target, but Tether has also found itself in the crosshairs of regulators who are still figuring out how to handle the crypto revolution.

In the United States, Tether operates in something of a regulatory twilight zone. The company has faced pressure from agencies like the Commodity Futures Trading Commission (CFTC), which fined Tether $41 million in 2021 for making false statements about being fully backed by US dollars.

The European Union is taking a more structured approach with its Markets in Crypto-Assets (MiCA) regulation, which will require stablecoins to be backed by highly liquid assets. This could actually work in Tether's favour, as they've already been moving in that direction.

Emerging markets present their own challenges. Some countries have embraced USDT as a hedge against local currency instability, while others have banned it outright, not far from a global game of regulatory whack-a-mole.

For users, the regulatory risks are real but indirect. If major jurisdictions crack down hard on Tether, it could affect the token's liquidity and usability. However, a complete overnight shutdown seems unlikely given USDT's deep integration into the crypto ecosystem.

The bigger risk might be increased compliance requirements that could make using USDT more cumbersome, similar to how traditional banking has become more regulated over time.

How safe is USDT for holding assets?

This is where we need to have an honest conversation about what "safe" means in crypto land.

For short-term use (days to weeks):

USDT works pretty well. If you're trading crypto or need to park funds briefly between investments, it's like using a decent hotel - not your forever home, but comfortable enough for a short stay.

The peg has held remarkably well through various market conditions, and liquidity is excellent across most major platforms.

For medium-term holdings (months):

Here's where things get a bit more nuanced. USDT has survived multiple "stress tests", including the Terra Luna collapse, FTX implosion, and various banking sector scares. However, you're essentially trusting that Tether's reserve management continues to work smoothly and that no major regulatory bombshell disrupts operations.

For long-term wealth storage (years):

This is where many experts start raising eyebrows. Holding large amounts in any stablecoin for extended periods comes with risks that compound over time. You're exposed to regulatory changes, potential company mismanagement, and the general "unknown unknowns" that come with relatively new financial instruments.

Essentially, USDT is like keeping money in a foreign bank account. It might work great for a while, but you're subject to the laws, regulations, and business practices of entities outside your home jurisdiction.

The key insight from the crypto community is diversification. Even USDT supporters rarely recommend putting all your eggs in the Tether basket.

Security best practices when using USDT

Using USDT safely isn't just about trusting Tether - it's also about protecting yourself from the various ways things can go wrong in the crypto world.

Platform risk management: Remember, USDT is only as safe as the platform you're using it on. The token itself might be fine, but if you're holding it on a sketchy exchange that gets hacked or goes bankrupt, you could lose everything. Stick to regulated platforms only.

Diversification strategies: Many crypto users often split their stablecoin holdings across multiple tokens and platforms. Think of it as not putting all your digital eggs in one digital basket. As an example, some might hold 40% USDT, 40% USDC, and 20% in other stablecoins or traditional assets.

For crypto beginners: Start small, learn the ropes, and, if you wish, gradually increase your holdings as you become more comfortable. Use well-established exchanges for your first purchases, enable two-factor authentication on everything, etc. Treat your crypto security like you would your online banking, that's essentially what it is.

USDT vs other stablecoins

The stablecoin world isn't a one-horse race, and understanding the alternatives helps put USDT's safety in perspective.

USDT vs USDC

USDT dominates in usage and global liquidity. It's the most widely accepted stablecoin across exchanges, DeFi platforms, and payment rails. But it has faced criticism over the years for a lack of full audits and historical opacity around reserves.

USD Coin (USDC), issued by Circle, takes a different approach. It’s often seen as the “regulated” stablecoin, with monthly attestations and a conservative reserve mix (primarily cash and short-term U.S. Treasuries).

- USDT is ideal for fast-moving markets and broad platform compatibility.

- USDC appeals to those who prioritise transparency and regulatory oversight.

USDT vs DAI

DAI takes a completely different route. Issued by MakerDAO, it’s a decentralised stablecoin backed by overcollateralised crypto assets like ETH, not fiat. There’s no single company behind it, just smart contracts and community governance.

While DAI offers full on-chain transparency and avoids centralised custodians, it also comes with higher complexity and potential risks tied to smart contract bugs or extreme market conditions.

- USDT provides speed and simplicity, backed by a traditional corporate structure.

- DAI offers a decentralised alternative, ideal for DeFi-native users.

USDT vs BUSD

BUSD, once a major player backed by Binance and Paxos, was phased out in 2024 due to regulatory pressure. It serves as a reminder that centralised stablecoins depend on both market forces and compliance frameworks, and can be wound down unexpectedly.

While USDT remains standing, BUSD’s sunset reinforces the importance of evaluating who’s behind the stablecoin and how stable their operations really are.

What happens if Tether fails?

Let's play out a hypothetical scenario: what if USDT actually collapsed?

Given USDT's role as the primary trading pair and liquidity source for much of the crypto market, a Tether failure would be like removing a major highway from a city's transportation network. The immediate effects would likely include:

Market chaos: Traders scrambling to exit USDT positions would create massive selling pressure across crypto markets. We're talking about potentially the largest fire sale in crypto history, as billions of dollars worth of USDT holders try to convert to other assets simultaneously.

Liquidity crisis: Many smaller cryptocurrencies rely heavily on USDT trading pairs. Without this liquidity, some tokens might become effectively untradeable, at least temporarily.

Contagion effects: Other stablecoins might face runs as confidence in the entire sector erodes. Even well-managed stablecoins could struggle if everyone tries to redeem at once.

The silver lining: The crypto ecosystem has become more resilient over time. Alternative stablecoins like USDC have grown substantially, providing some redundancy. Additionally, the market has survived previous "extinction-level events" and adapted.

Conclusion: Is USDT worth the risk?

USDT isn’t perfect, but it’s proven its place in the crypto ecosystem. With high liquidity and global acceptance, it’s a practical choice for trading, payments, and short-term value storage.

However, concerns around transparency and regulatory clarity mean it’s not ideal for long-term holding or users who prioritise full visibility. But like any financial tool, its value depends on how you use it.

The smart approach is to understand the trade-offs, diversify across stablecoins, and align your choices with your goals and risk tolerance. As the space evolves, USDT remains useful, but it’s just one part of a broader digital finance strategy.

Learn how Ethereum gas fees work, why they fluctuate, and how to save on costs using smart timing, Layer 2s, and upcoming network upgrades.

Every move on Ethereum (sending crypto, minting an NFT, using a dapp) comes with a cost. That cost is called gas. It’s not just a fee - it’s the fuel that keeps the network running.

Knowing how gas works means you’re not just using Ethereum, you’re using it smarter. You can time transactions, avoid peak congestion, and cut your costs. Here we explore how it works and how to take control in a simple and easy-to-understand way.

What are Ethereum gas fees?

Let’s start with the basics: gas fees are the cost of using the Ethereum network. Any time you do something - like send ETH or swap tokens - you’re asking the network to do work. That work takes computing power, and gas fees are what you pay to get it done.

These fees serve three critical functions:

- Compensate validators for their work

- Secure the network from spam attacks, and

- Prioritise transactions during busy periods.

When the network buzzes with activity, the fees naturally rise as users compete for limited block space. Picture Ethereum as a busy highway during rush hour. More traffic means higher tolls, but the road remains secure and functional for everyone willing to pay the current rate.

How Ethereum gas fees work

Every gas fee breaks down into a simple formula that establishes your specific transaction cost:

Total fee = (base fee + priority fee) × gas limit

Let’s break it down:

- The base fee is the minimum cost to get your transaction into a block. It goes up when the network is busy and is burned (destroyed) to help reduce ETH supply.

- The priority fee (tip) is an extra amount you add to speed things up (like tipping for faster service).

- The gas limit is how much work your transaction needs. Bigger, more complex actions need a higher limit.

Another important element to understand is that gas prices are measured in Gwei, where 1 Gwei equals 0.000000001 ETH. A typical token swap might use 30,000 gas units. If the current base fee sits at 25 Gwei and you add a 5 Gwei tip, your total cost becomes:

(25 + 5) × 30,000 = 900,000 Gwei = 0.0009 ETH

Let’s say at $2,500 per ETH, that transaction would cost $2.25.

Why Ethereum gas fees fluctuate

Gas fees move with the rhythm of the network. When demand is low, fees drop. When things heat up, they spike.

Big events like new token launches, NFT drops, or market surges can therefore clog the network. More users = more competition for space. That’s when the base fee goes up (remember the formula above: total fee = (base fee + priority fee) × gas limit).

The base fee adjusts with every block (around every 15 seconds). It rises when blocks are more than 50% full and drops when they’re under that threshold.

The type of transaction also matters:

- A simple ETH transfer uses about 21,000 gas units.

- A complex smart contract call: +/-200,000.

- A typical Uniswap swap costs 3–5x more than a basic transfer.

And don’t forget ETH’s price. Even if gas stays steady in Gwei, rising ETH makes each transaction more expensive in dollars.

Quick Tip: Check gas trackers before major transactions. A few minutes of timing can save significant money.

How to check Ethereum gas prices in real time

Active users monitor gas prices like traders watch market charts. There are several tools that provide real-time visibility into the network’s condition.

- Etherscan’s gas tracker (for deep analytics)

Etherscan provides in-depth gas analytics including real-time rates, historical charts, and insights into average and peak fees. It also offers optimisation tips like identifying “safe low‑cost windows” for transactions. - Rabby wallet (for user-friendly alerts)

Rabby’s mobile and browser wallet features built-in gas monitoring, showing current prices and offering “Gas Top Up” functionality. It also supports push notifications (via its GasAccount feature) for favourable conditions. - MetaMask (for fully integrated wallet visibility)

MetaMask displays live gas rates directly in its interface and dashboard. You'll see options like Low, Market, or Aggressive for gas speeds, and it even shows fiat equivalents beside token balances.

Most gas trackers display slow, standard, and fast fee tiers, helping you balance cost and speed.

It’s also worth knowing that slow transactions may take 5-10 minutes but can save you 20-30% on fees, while fast ones aim to process within a couple of minutes, at a premium price.

Gas prices also follow weekly patterns. Fees are usually lower on weekends, when institutional and high-frequency trading slows down. And if you’re not in a rush, consider transacting during early morning hours (2–6 AM EST), often the cheapest window of the day.

Ethereum gas fees before and after the merge

Over the years, Ethereum has gone through major upgrades that changed how gas fees work, though granted not always in the ways people expected.

In 2021, the London Hard Fork introduced EIP-1559, swapping chaotic gas auctions for a more predictable pricing model: a base fee + tip. It made fee estimates more stable, but didn’t necessarily make them cheaper.

Then came The Merge in 2022, shifting Ethereum to proof-of-stake. It cut energy use and made block processing more efficient. But despite common belief, it didn’t slash gas fees overnight.

However, The Merge did lay the groundwork for future upgrades (like sharding and rollups) that will unlock real, lasting fee reductions at scale.

Looking ahead, upgrades like Proto-Danksharding aim to scale Ethereum and bring fees down for good.

How to reduce ETH gas fees

Despite what some might tell you, cutting gas fees isn’t about luck, it’s more about smart choices and good timing. Here are some options:

Use Layer 2s

Networks like Arbitrum, Optimism, and Base offer the biggest savings, sometimes up to 90–95% cheaper than the Ethereum mainnet. For example, a $50 swap on mainnet might cost just $2-$5 on these platforms, with the same level of security. (More on this below).

Simulate before you send

Tools like Tenderly and DeFi Saver let you test complex transactions first, helping you avoid failed attempts that still burn gas.

Pick your moment

As mentioned above, prices drop when the network is quiet. Use gas trackers to spot the best times to transact.

Batch when you can

Some protocols let you combine multiple actions into one transaction, so you pay one base fee instead of several.

Layer 2 solutions that cut gas costs

Layer 2 networks are the future of Ethereum scaling. They can handle thousands of transactions off-chain, then settle them on Ethereum in one go, cutting costs and speeding things up.

- Arbitrum leads in total value locked. It offers fast transactions for just $0.10-$0.50 and supports most major DeFi apps, making it feel like a cheaper version of the mainnet.

- Optimism offers similar savings, with bonus perks like token rewards for developers through its RetroPGF program, driving growth and innovation.

- Base combines low fees with easy fiat onramps. It’s great for beginners moving from exchanges into DeFi.

These networks are able to do what they do by using rollups, a tech that bundles hundreds of transactions into one. Think of it like carpooling: everyone shares the cost of the ride, but still gets where they need to go.

Who receives Ethereum gas fees?

Since The Merge, Ethereum handles gas fees in a smart split between rewards and supply control.

- Validators (who secure the network) earn priority fees - tips from users that reward them for processing transactions. This keeps the network safe and running smoothly.

- Base fees, on the other hand, are burned (permanently removed from circulation). When the network is busy, more ETH is burned, which can reduce supply and make ETH more valuable over time.

Will Ethereum gas fees ever go down?

Ethereum’s roadmap promises big fee cuts, but the biggest changes will take time.

- Proto-Danksharding (EIP-4844) is expected in upcoming upgrades. It will slash Layer 2 costs by 10-100x by creating dedicated space for rollup data. This upgrade is the closest major step toward lower fees.

- Full Danksharding, further down the line, will boost Ethereum’s capacity massively, making tiny, sub-penny transactions on Layer 2 networks a reality without sacrificing security or decentralisation.

- Ethereum’s founder, Vitalik Buterin, envisions the mainnet as a secure settlement layer, while Layer 2s handle most daily transactions quickly and cheaply.

If all goes as planned, popular Layer 2s could offer fees under one cent within 2-3 years, opening the door for micro-transactions and true global use.

Comparison: Ethereum vs other chains

Blockchain networks take different paths when balancing cost, security, and decentralisation, and fees reflect those choices. Let’s take a look at its biggest competitors.

Solana vs Ethereum

Solana offers super low, sub-penny fees and processes around 3,000 transactions per second (far more than Ethereum’s +/-15 TPS). This speed comes from different architectural choices, but with tradeoffs like higher hardware requirements and occasional network outages.

Ethereum, meanwhile, prioritises security and decentralisation, scaling through Layer 2 solutions to keep fees competitive.

Binance Smart Chain vs Ethereum

Binance Smart Chain (BSC) delivers low fees, typically $0.10–$0.50 per transaction, but it sacrifices decentralisation by relying on fewer validators and tighter connections to centralised infrastructure.

Ethereum maintains a more decentralised network while scaling costs through Layer 2s, keeping security front and centre.

Avalanche vs Ethereum

Avalanche strikes a balance with moderate fees ($0.50–$2.00), high throughput, and strong security. However, its ecosystem remains smaller than Ethereum’s rich DeFi landscape, which benefits from Layer 2 scaling and a strong focus on decentralisation.

Final thoughts

Understanding Ethereum gas fees puts you in control, allowing you to save money and utilise the network more efficiently. While fees can fluctuate, smart timing, Layer 2 solutions, and upcoming upgrades promise a future of faster, cheaper transactions.

While Ethereum continues to prioritise security and decentralisation, its gas fee roadmap reflects a careful balance between innovation and accessibility, paving the way for broader adoption and everyday use.

.webp)

ChatGPT has become the AI everyone's talking about, but with multiple plans and price points, which version actually delivers the best bang for your buck in 2025?

Unless you’ve been living under a rock, you’ve probably heard about ChatGPT… this almighty, em dash-loving AI assistant that seems to pop up in every conversation nowadays regarding productivity and technology.

It truly is everywhere, and honestly, it lives up to the hype.

Think of it as a chatty, super-smart friend you can tap into anytime, whether you’re fine-tuning an email, researching, or tackling coding questions late at night.

But one thing many newcomers don’t quickly realize: not all ChatGPT plans are created equal. The differences between the free version and paid tiers can be striking, from a helpful but occasionally busy assistant to a premium version that's always ready to go deep on your tasks. With multiple plans, variable costs, and constant updates, it’s not always clear which version offers the best value for one's specific needs.

Whether you're watching your budget or ready to upgrade your productivity, knowing which plan aligns with your needs will help you make the best choice. So, let’s dive in.

ChatGPT Pricing Plans Explained

Let’s break down what each subscription tier offers and what you're actually paying for:

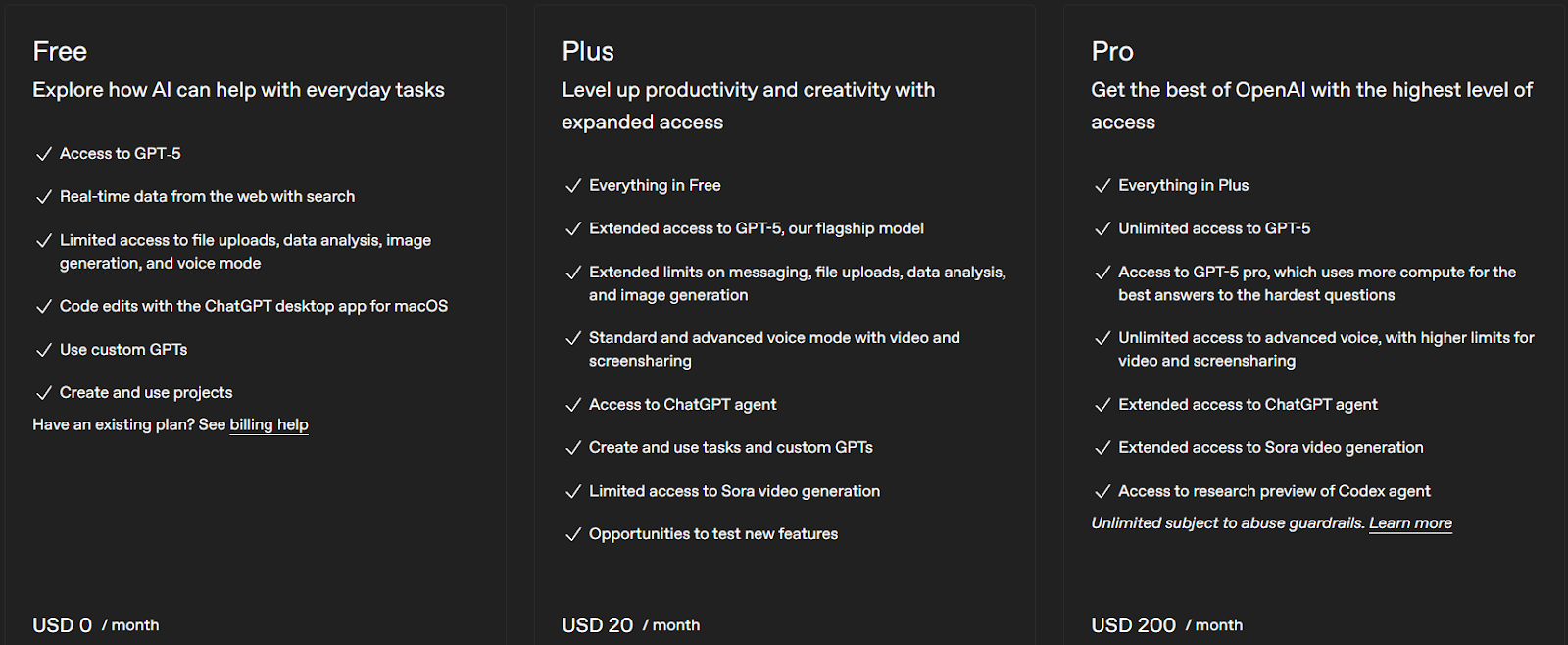

ChatGPT Free Plan

- Access to GPT-5 (automatic fast/reasoning mode) with standard performance.

- Features: voice mode, file uploads, image generation, web browsing, basic analysis.

- Best for: New users exploring ChatGPT’s capabilities without commitment. Offers solid functionality for casual use, though access and speed can be limited during high demand.

ChatGPT Plus ($20/month)

- Priority access to GPT-5 with faster responses.

- Advanced voice mode, early feature access, GPT-4o, custom GPTs.

- Best for: Individuals like freelancers or students needing reliable performance and enhanced features.

ChatGPT Pro ($200/month)

- Unlimited GPT-5 access in "Pro" mode offering deeper, more complex reasoning.

- Premium compute power and research-grade performance.

- Best for: Power users; researchers, engineers, and professionals requiring high-level reasoning and uninterrupted access.

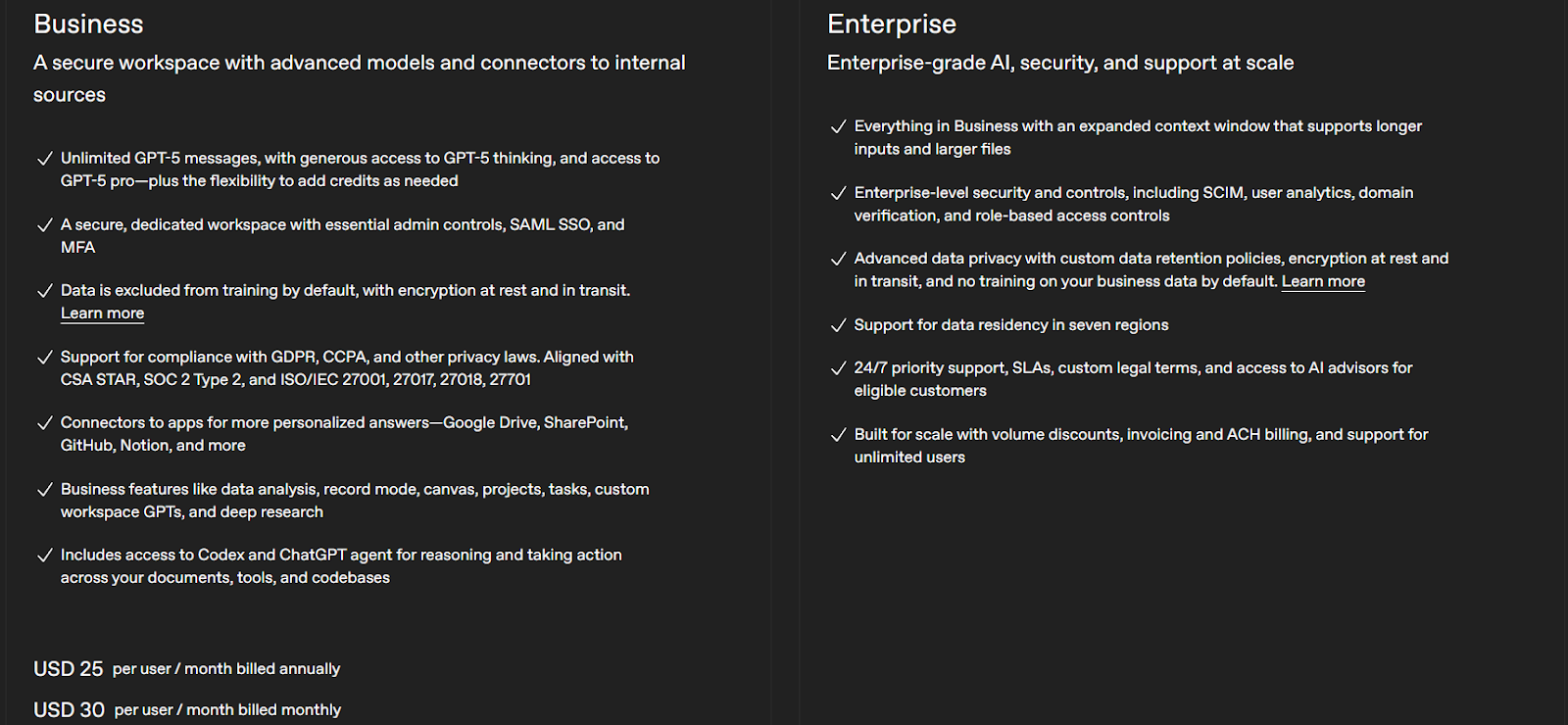

ChatGPT Team ($25–30 per user/month)

- All Plus features plus team-focused tools.

- Collaboration workspace, admin controls, privacy (OpenAI won’t train on your data), shared GPTs.

- Best for: Small teams or startups that value collaboration with enhanced security.

ChatGPT Enterprise (Custom pricing)

- Advanced security, enterprise-grade privacy, integrations (e.g., Google Drive, SharePoint), and dedicated support.

- Best for: Large organisations embedding AI into their core infrastructure with full admin and compliance controls.

Which ChatGPT Plan Is Right for You?

Choosing the right plan is like picking a mobile phone tariff. You want features that fit your needs without overpaying:

- Students: Start with Free; upgrade to Plus if peak usage becomes a drag.

- Freelancers / Pros: Plus is your professional toolkit; it’s reliable, responsive, and worth every dollar.

- Developers / Tech Users: Plus covers light work; Pro fits deep coding or complex data tasks.

- Small Teams / Startups: Team plan adds collaboration and privacy; it’s critical for joint projects.

- Large Enterprises: Enterprise plan solidifies AI as a business workflow pillar.

ChatGPT Hidden Costs & Limitations to Know

Even beyond the listed prices, here are some caveats to keep in mind:

- API Usage: If you use ChatGPT APIs, you'll pay extra per token. For example, GPT-4o mini input tokens cost significantly less than full models.

- Message Limits & Throttling: Paid plans have generous but not infinite usage. Pro handles higher loads; Free can be restrictive.

- Feature Rollouts: Some features debut first to higher plans. Free users may get them later, like being in general admission while Plus users enjoy VIP access.

- Storage Limits: File sizes and frequency may be capped, depending on the plan.

Cost-Saving Tips

- Annual billing: Check for annual pricing discounts, especially on Team plans. Savings of 15–20% are common.

- Track usage: Keep an eye on how many messages or uploads you consume. Some plans never reveal that data clearly.

- Bundle savings: If your organization qualifies, inquire about nonprofit discounts. OpenAI sometimes offers 20–50% off Business or Enterprise plans.

ChatGPT Alternatives: Is There a Better Deal?

ChatGPT isn’t the only tool in town. Here’s a quick look at the competition:

- Claude AI (Anthropic): great at deep reasoning and handling longer contexts

- Perplexity AI: excels in web search, complete with cited sources

- DeepSeek: lower cost, decent performance for budget-conscious users

- Google Gemini: seamless if you already heavily use Google’s ecosystem

Each platform brings its own strengths. ChatGPT remains very versatile, but depending on your needs, one of these may outperform it.

Final Thoughts: Is ChatGPT Worth the Price in 2025?

The value comes down to your personal use. The Free plan is surprisingly capable for casual use. For most professionals, the $20 Plus plan soon pays for itself. For teams and businesses, Team or Enterprise plans consolidate productivity, compliance, and privacy in one package.

The good news is you're not stuck with one choice forever. Experiment with free versions of ChatGPT, Claude, or Perplexity, and upgrade when the fit and features match your workflow. Try them all out. Get crazy with those chats!

We're still figuring out this whole AI conundrum, but one thing's clear, these tools are becoming as essential as e-mail or Google Drive. The question is not whether you'll use AI, it's whether you’ll find a way to make it fit your current needs… knowing you can always level up later.

A look into fintech's role in empowering the unbanked communities around the world, how far we've come, and what's still ahead.

The financial revolution isn't happening in Wall Street's landmark buildings, it's exploding through smartphone screens in rural villages, urban apartments, and immigrant communities worldwide. And while traditional banks still ask for three forms of ID and a pristine credit score, fintech is rewriting the rules of who gets to participate in the global economy.

Here's the reality: 1.4 billion adults globally remain unbanked, locked out of basic financial services that most of us take for granted. In the U.S. alone, roughly 5.4% of households (about 5.6 million families) have no relationship with a bank or credit union. These aren't just statistics; they're people paying check-cashing fees, carrying cash everywhere, and building zero credit history despite working multiple jobs.

But here's where it gets interesting: fintech isn't just offering band-aid solutions. It's fundamentally disrupting how financial services work, creating pathways to economic participation that bypass traditional gatekeepers entirely.

From mobile banking apps that require no minimum balance to blockchain-based lending that ignores credit scores, technology is democratising finance in ways that seemed impossible just a decade ago.

The question isn't whether fintech can help the unbanked, it's already happening. The real question is how fast this transformation can scale and whether it can reach the communities that need it most.

Why so many people remain unbanked

Let's dive into the barriers that keep millions locked out of traditional banking. It's not just about money, though, of course, that’s a part of it.

The most obvious culprit? Banks themselves. Traditional institutions have built their entire business model around risk assessment, which typically means credit scores, employment verification, and documentation requirements that exclude huge swaths of the population.

If you're an immigrant without an established credit history, a gig worker with irregular income, or someone who's been burned by predatory lending in the past, good luck getting a simple checking account with credit facilities.

Geographic accessibility plays a massive role, too. Rural communities have watched bank branches disappear at an alarming rate: since 2009, over 10,000 bank branches have closed across the UK. When the nearest bank is 50 miles away and you're working two jobs just to stay afloat, maintaining a traditional banking relationship becomes practically impossible.

Then there's the trust factor. Many unbanked individuals come from communities where banks have historically been extractive rather than supportive. Why would you trust an institution that charges overdraft fees designed to trap you in cycles of debt? For many, cash-only transactions feel safer and more transparent than navigating hidden fees and complex terms of service.

Digital literacy creates another layer of exclusion. While fintech promises mobile-first solutions, those solutions still require smartphone access, internet connectivity, and the technical knowledge to navigate increasingly complex apps. For older adults or those without consistent internet access, digital banking can feel more like a barrier than a bridge.

The demographic impact tells the whole story: immigrants, young adults building their first financial identity, gig workers whose income doesn't fit traditional employment models, and rural populations where infrastructure lags behind urban centres. These aren't fringe communities, they represent the fastest-growing segments of the workforce.

Traditional banking's limitations

Here's the uncomfortable truth about traditional banking: it was designed for a different era, when employment was stable, credit histories were linear, and financial relationships lasted decades. Today's economy doesn't work that way, but banks haven't caught up.

The FICO credit scoring system perfectly exemplifies this disconnect. Created in 1989, it treats credit like a single number that defines your financial worth, ignoring factors like consistent rent payments, utility bill history, or mobile phone payment patterns. If you've never had a credit card or traditional loan, you're effectively invisible to the system that determines whether you can access basic financial services.

Fee structures reveal even deeper problems. The average overdraft fee has climbed to $35, while monthly maintenance fees can easily cost $200+ annually for basic checking accounts.

For someone living paycheck to paycheck, these fees aren't just inconvenient, they can be financially devastating. Banks profit billions annually from overdraft fees alone, creating perverse incentives to trap rather than support their most vulnerable customers.

Bureaucracy adds another layer of exclusion. Opening a bank account requires documentation that many people simply don't have readily available: proof of address, employment verification, Social Security numbers, and often a minimum deposit. For undocumented immigrants, frequent movers, or those between jobs, these requirements create insurmountable barriers.

Traditional banks also struggle with personalisation at scale. They're built to serve middle-class customers with predictable income patterns, not gig workers whose earnings fluctuate wildly or small business owners who need flexible lending options. The result? Financial products that don't match real-world financial lives.

How fintech is changing the game

Sure, fintech isn’t a cure-all, but it is revolutionising finance by flipping the model: instead of forcing people to fit outdated systems, it builds systems that fit how people actually live and work.

Mobile banking & digital wallets

Mobile banking apps like Chime, Venmo, and Cash App have obliterated traditional barriers to entry. Chime offers fee-free banking with no minimum balance requirements and early direct deposit features that get workers paid up to two days faster than traditional banks.

That might not sound revolutionary until you realise that for someone living paycheck to paycheck, getting paid two days early can mean the difference between making rent on time or facing late fees.

Venmo transformed peer-to-peer payments from a complicated wire transfer process into something as simple as sending a text message. Cash App went further, adding investing features, Bitcoin purchases, and small business payment processing to a single app that anyone can download for free.

Increasingly, platforms like Tap are also stepping in - not just as digital wallets, but as integrated ecosystems that combine spending, saving, and cross-border access for underserved users. These aren't just simplified versions of traditional banking, they're entirely different approaches that prioritise accessibility and user experience over profit maximisation through fees and complexity.

Peer-to-peer lending & credit building

The lending revolution is even more dramatic. Platforms like Avant, Earnest, and newer crypto-lending protocols are using alternative data sources and AI-driven risk assessment to make lending decisions that traditional banks couldn't even consider.

Instead of relying solely on FICO scores, these platforms analyse everything from social media activity to mobile phone payment patterns to assess creditworthiness. They're building credit profiles for people who were previously invisible to the traditional system, creating pathways to financial growth that didn't exist before.

Peer-to-peer lending removes banks from the equation entirely, connecting borrowers directly with individual lenders or pools of capital. This creates more competitive interest rates and more flexible terms, especially for borrowers who don't fit traditional risk profiles.

Micro-investment & wealth-building tools

Investment platforms like Robinhood, Acorns, and international players like Nutmeg have democratised wealth building by eliminating minimum investment requirements and complex fee structures. Acorns rounds up everyday purchases and invests the spare change, allowing people to build investment portfolios with literally pennies.

These platforms reimagine what investing looks like for people who aren't already wealthy. Educational resources, simplified interfaces, and fractional share ownership mean that someone making minimum wage can start building long-term wealth with the same tools previously only reserved for high-net-worth individuals.

DeFi & blockchain for financial access

Decentralised finance represents the most radical reimagining of financial services yet. Ethereum-based platforms allow people to lend, borrow, and earn interest without any traditional financial institution involvement. Smart contracts automatically execute financial agreements, eliminating the need for banks, credit checks, or geographical restrictions.

Crypto wallets provide financial services to anyone with a smartphone and internet connection, regardless of their documentation status, credit history, or location. While still nascent and volatile, DeFi protocols are processing billions in transactions and proving that alternative financial systems can operate at scale.

Benefits fintech brings to the unbanked

The advantages aren't just theoretical, they're transforming lives in measurable ways.

Accessibility leads the list.

Fintech services operate 24/7 from any smartphone, eliminating the geographical and temporal constraints that keep people away from traditional banks. Someone working night shifts or multiple jobs can manage their finances during a break, not during banking hours that conflict with their work schedule.

Affordability follows closely.

Most fintech platforms operate with dramatically lower overhead costs than traditional banks, allowing them to offer services with minimal or no fees. When you're not paying for physical branches, armies of tellers, and legacy IT systems, you can pass those savings to customers who need them most.

Speed transforms financial emergency management.

Traditional loan applications can take weeks while fintech platforms often provide decisions in minutes. When your car breaks down and you need to get to work tomorrow, that speed difference isn't convenience - it's survival.

Transparency. Transparency. Transparency.

Fintech apps typically show real-time transaction data, clear fee structures, and straightforward terms of service. No more surprise fees or hidden charges that drain accounts without warning.

Using data instead of old patterns.

Data-driven personalisation means financial products that actually match individual circumstances. Instead of one-size-fits-all banking products, AI-powered platforms can offer customised solutions based on spending patterns, income volatility, and financial goals.

Safety from the loan sharks.

Perhaps most importantly, fintech reduces exposure to predatory lending practices. Transparent algorithms and competitive marketplaces make it harder for bad actors to exploit vulnerable populations with payday loans and other extractive financial products.

Case studies & real-world applications

The real proof lies in how these technologies are working in practice across different communities and regions.

U.S. gig workers have embraced fintech payroll advances and flexible banking solutions. Uber and Lyft drivers use apps like Earnin to access their earnings before payday, eliminating the need for expensive payday loans.

DoorDash partnered with DasherDirect to offer delivery workers immediate access to their earnings plus cashback rewards on gas purchases = financial services designed specifically for the gig economy.

Africa's mobile money revolution provides the most compelling example of fintech leapfrogging traditional banking infrastructure. M-Pesa in Kenya processes more transactions annually than Western Union globally, allowing people to send money, pay bills, and access microloans through basic mobile phones.

Over 80% of Kenyan adults now use mobile money services, creating a more financially inclusive society than many developed nations.

Latin America's neobank adoption is exploding as traditional banks struggle to serve growing populations. Brazil's Nubank has over 70 million customers, offering fee-free banking and credit building to people previously excluded from traditional financial services.

Mexico's Clip provides small business payment processing to street vendors and micro-entrepreneurs who couldn't access traditional merchant services.

These aren't isolated success stories: they're proof of concept for global financial inclusion through technology.

Barriers fintech still faces

Despite the revolutionary potential, significant obstacles remain.

Digital literacy and smartphone access create fundamental barriers. While smartphone penetration continues growing globally, reliable internet connectivity and the technical skills needed to navigate financial apps remain unevenly distributed. Older adults and rural populations often struggle with interfaces designed by young urban developers.

Regulatory hurdles complicate expansion and innovation. Know Your Customer (KYC) compliance requirements, anti-money laundering regulations, and licensing requirements vary dramatically across jurisdictions, making it difficult for fintech companies to scale globally. Regulatory uncertainty around crypto and DeFi creates additional complications for even the most innovative solutions.

Infrastructure gaps in developing regions limit fintech's reach. While mobile money works well in areas with basic cellular coverage, more sophisticated fintech services require robust internet infrastructure that many rural and low-income areas still lack.

Crypto and DeFi adoption scepticism remains high, particularly among the very populations these technologies could most benefit. Volatility concerns, complexity, and association with scams and fraud make many potential users hesitant to embrace blockchain-based financial services.

Cultural barriers also persist. In communities where cash has been king for generations, shifting to digital-first financial services requires not just technological adoption but cultural change. Trust must be earned through consistent, reliable service over time.

What the future holds: innovations & inclusion

The next wave of fintech innovation promises even more dramatic transformation.

Artificial intelligence will enable hyper-personalised financial services that adapt in real-time to individual circumstances. AI-powered financial advisors will provide wealth management services previously available only to millionaires, while machine learning algorithms will create more accurate and inclusive credit assessment models.

Open banking regulations will force traditional financial institutions to share customer data with fintech competitors, accelerating innovation and competition. This means better services, lower costs, and more options for consumers who have been underserved by traditional banks.

Regulatory evolution will create clearer frameworks for fintech innovation while protecting consumers. Central bank digital currencies (CBDCs) may provide government-backed alternatives to both traditional banking and cryptocurrencies, potentially reaching populations that current solutions miss.

Blockchain-based financial identity systems could eliminate documentation barriers that currently exclude millions from financial services. Decentralised identity solutions would allow people to build financial reputations independent of traditional credit systems or government documentation.

The convergence of fintech with other technologies (Internet of Things sensors for supply chain financing, augmented reality for financial education, 5G networks for real-time global payments) will likely create financial services we can barely imagine today.

Conclusion

Fintech isn't just disrupting traditional banking: it's democratising economic participation on a global scale.

From mobile money transforming African economies to gig worker payment solutions in American cities, technology is proving that financial inclusion isn't just morally right, it's economically inevitable.

However, the transformation isn't complete, and significant barriers still remain. But the trajectory is clear: financial services are becoming more accessible, affordable, and aligned with how people actually live and work in the 21st century.

The most exciting developments will emerge from collaboration between fintech innovators, government regulators, and community organisations that understand local needs.

This isn't a zero-sum game between technology and tradition—it's an opportunity to build financial systems that serve everyone, not just those who were lucky enough to be born into existing networks of economic privilege.

The unbanked aren't waiting for permission to participate in the global economy. They're already using whatever tools they can access to build financial stability and opportunity. Fintech's job is to make sure those tools are powerful, accessible, and designed with their real needs in mind.

The financial revolution is happening whether traditional institutions join it or not. The question is whether we'll build a system that includes everyone or leaves millions behind. The technology exists. The demand is obvious. Now it's up to us to make financial inclusion a reality, not just a promise.

News and updates

Bitcoin December Outlook: Will BTC Deliver a Holiday Rally Before 2026?

Bitcoin rebounded and now sits at a crossroads. Discover what whale accumulation, macro developments, and key technical levels signal for the end of 2025.

Bitcoin's Comeback: Three Forces That Could Make or Break it

Bitcoin is a long way from reclaiming its all-time high and stuck under $92,000, but three powerful forces could flip the script sooner than you think.

The Surge After the Storm: What’s Next for Bitcoin and the Market

After a brutal October sell-off, crypto just staged one of its most dramatic comebacks yet. Here's what the market's resilience signals for what comes next.

Decoding the disconnect: America's cautious approach to crypto

Bitcoin and the broader crypto market have soared to a staggering $2.1 trillion in value, but why does skepticism still linger among so many Americans? Here is a deep dive into the current trust gap.