November 2025 could be a turning point for crypto. From ETFs to major network upgrades, here are six catalysts that could shape the market.

Keep reading

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

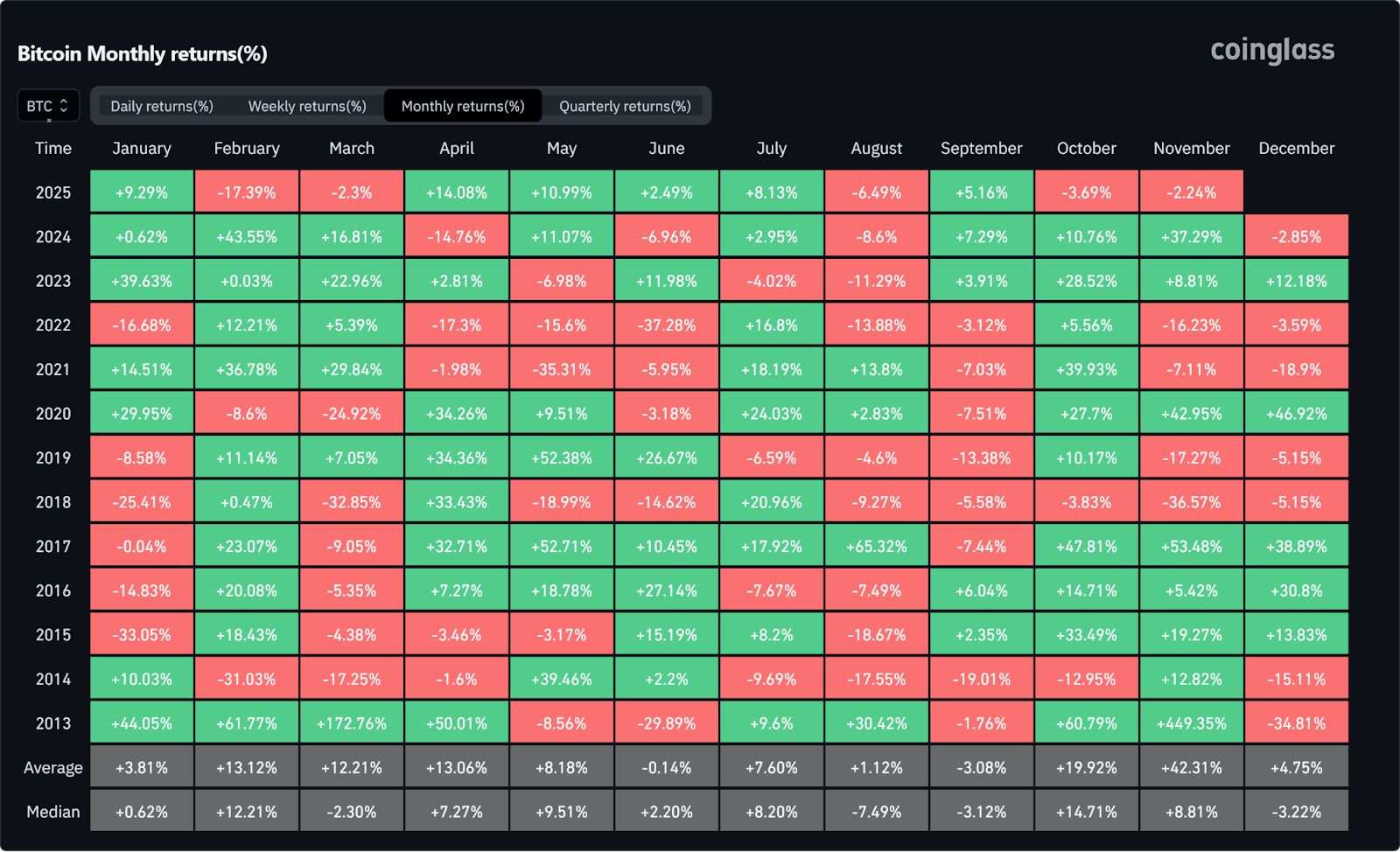

1. Seasonality & Historical Momentum Could Kick In

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

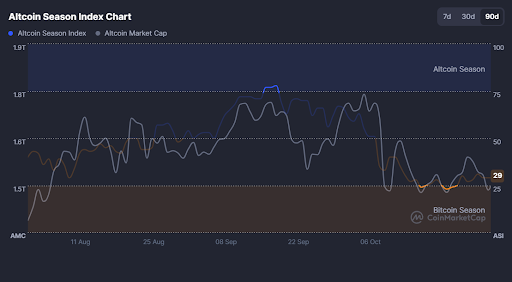

4. Altcoins at an Inflection Point

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

NEWS AND UPDATES

LATEST ARTICLE

.png)

Oavsett om du är en trogen datoranvändare eller föredrar mobilen, finns det tillfällen då du snabbt behöver skriva det brittiska pundtecknet (£) i ett mejl, dokument eller meddelande. I den här guiden visar vi hur du enkelt lägger till symbolen – oavsett om du använder Mac, PC eller smartphone.

Men först: om du vill skicka brittiska pund internationellt, erbjuder Tap – en reglerad och användarvänlig fintechplattform – snabba, smidiga överföringar med låga avgifter och konkurrenskraftiga växlingskurser. Överför pengar globalt eller gratis mellan Tap-användare, direkt i appen.

Var kommer pundtecknet ifrån?

Det brittiska pundet, symboliserat med £, har en över 1 200 år lång historia. Ursprungligen användes det som viktmått för silver i det anglosaxiska England och blev officiell valuta år 1694 under kung William III.

Pundet fick global betydelse genom det brittiska imperiets expansion, och trots historiska utmaningar – som valutadevalvering 1967 och Brexit – förblir det en stark och inflytelserik valuta.

Enligt Bank of England härstammar symbolen från bokstaven L, första bokstaven i det latinska ordet libra, som betyder "pund". Den horisontella linjen i symbolen tros ha tillkommit på 1600-talet och finns dokumenterad på ett checkexemplar från 1660.

I brittisk skrivstil placeras pundtecknet före summan – exempelvis: £10.

🎭 Kul fakta: År 1970 lanserades en ny £20-sedel med William Shakespeare, vilket lade grunden till traditionen att pryda sedlar med historiskt betydelsefulla personer.

Så skriver du £ i ett dokument

Låt oss nu gå igenom hur du faktiskt skriver pundtecknet (£) på olika enheter – oavsett om du använder Mac, PC eller mobil.

För Mac-användare

Använder du Mac? Här är det enklaste sättet:

- Håll in Option (⌥) (eller Alt) och tryck samtidigt på 3.

På vissa tangentbord kan det fungera med Shift + 3, beroende på layouten.

För Windows-användare

På en Windows-dator:

- Håll in Shift och tryck på 3 (överst på tangentbordet). På vissa tangentbord finns pundsymbolen tryckt ovanför siffran – som en visuell påminnelse.

💡 Värt att notera: Amerikanska tangentbord har oftast inte £ som standard. I så fall kan du alltid kopiera symbolen härifrån: £

För dig med smartphone eller surfplatta

På mobilen (både iOS och Android) är det ännu enklare:

- Öppna tangentbordet i meddelandet eller appen du skriver i.

- Växla till symbol- eller siffertangentbordet.

- Leta efter £, eller håll in dollartecknet ($) för att få upp fler valmöjligheter.

Inget tangentbord? Inga problem

Skriver du i Word eller Google Docs utan tillgång till tangentbord? Så här gör du:

I Microsoft Word:

- Gå till Infoga > Symbol.

- Leta upp £ i listan och klicka för att infoga.

I Google Docs:

- Gå till Infoga > Specialtecken.

- Välj Symboler > Valuta och klicka på £.

Klart!

Nu vet du hur du snabbt och enkelt skriver pundtecknet (£) – oavsett vilken enhet du använder. Spara gärna den här guiden till nästa gång du behöver lägga till symbolen i ett mejl, dokument eller meddelande.

As we delve deeper into understanding the global financial market and the investment opportunities within it, here we break down the difference between the capital market and the money market. Together, these two markets make up a large portion of what is effectively known as the financial market.

Capital market vs money market

As we break down the money market vs capital market debate, let's first cover the basics of what each entails.

The capital market is where stocks and bonds are traded between financial institutions, professional brokers, and individual investors with a focus on long-term price appreciation.

The money market centers around the exchange of short-term debt between governments, commercial banks, corporations, and other financial institutions. It entails borrowing and lending for a limited amount of time - anything from an overnight transaction to up to a year at maximum.

What is the money market, exactly?

The money market refers to the market where short-term debt securities are traded among financial institutions, commercial banks and corporations. These securities typically have maturities of one year or less and are considered to be very low-risk investments.

Money market securities include instruments such as Treasury bills, commercial paper, certificates of deposit (CDs), and repurchase agreements (repos). These securities are issued by governments, corporations, and financial institutions as a way to raise capital quickly and at a relatively low cost.

How to participate in the market

Investors can participate in the money market by purchasing these financial assets directly or through a money market mutual fund. Money market funds invest in a variety of short-term debt instruments and are designed to provide a safe and liquid investment option for individuals and institutions looking to park their cash reserves or earn a modest return while maintaining a high level of liquidity.

What is the capital market, exactly?

The capital market refers to the market where long-term securities, such as stocks, bonds, and other financial instruments, are bought and sold among investors and institutions. Unlike the money market, which deals with short-term debt securities, the capital market deals with longer-term investments that typically have maturities of more than one year.

The primary market and secondary market are two different stages of the capital market where securities are bought and sold.

Stages: primary market and secondary market

The primary market is where securities, such as stocks, bonds, and other financial instruments, are first issued by companies or governments to raise capital. This is often referred to as an initial public offering (IPO) or a new issue. In the primary market, the securities are sold directly to investors through underwriters or investment banks.

The secondary market, on the other hand, is where previously issued securities are bought and sold among investors. This market allows investors to buy and sell securities with other retail investors, rather than directly with the issuing company. Stock exchanges such as the New York Stock Exchange is an example of a secondary market where investors can trade stocks that are listed on the exchange.

Equity market

The capital market can be divided into two main segments: the equity market and the debt market. The equity market, also known as the stock market, is where shares of publicly traded companies are bought and sold.

Investors can purchase shares of stocks, which represent ownership in a company and entitle the shareholder to a portion of the company's profits, known as dividends. Investors can also profit from capital appreciation, which is the increase in the value of the stock over time.

Debt market

The debt market, on the other hand, is where companies and governments issue bonds to raise capital. Bonds are essentially loans made by investors to the issuer, which promises to pay back the principal amount with interest over a specified period. Bonds are generally considered to be less risky than stocks, but they also offer lower returns.

How to participate in the market

Investors can participate in the capital market through various means, such as buying capital market instruments like stocks or bonds directly, investing in mutual funds or exchange-traded funds (ETFs), or through alternative investment vehicles such as private equity or hedge funds.

The key differences between the capital market and money markets

The capital market can be more volatile than the money market due to the longer-term nature of investments, but it can also offer the potential for higher returns over time. It is an important component of the global financial system and can play a significant role in economic growth and development.

On the other hand, the money market can be an attractive option for investors who prioritize safety and liquidity over high returns. Because money market securities are short-term and typically low-risk, they offer a lower yield than other investments, such as stocks or corporate bonds.

However, money market instruments can be an important component of a diversified investment portfolio, particularly for those who are looking to minimize risk and maintain a stable source of income in the financial market.

Which is best for you?

Determining which market to engage in will depend on each person’s financial goals, risk management levels, and interest in the markets. Speak to your financial advisor or conduct the research on your own to establish which investment options best align with your needs and goals. Both options present strong pros and cons, the ultimate decision will come down to your unique preferences.

Money talks, wealth whispers. In the age of flashy displays of wealth and conspicuous consumption, a new trend has emerged that challenges our conventional notions of showcasing financial success. Stealth wealth, as it is commonly referred to, goes beyond the idea of being frugal and understated. It involves consciously avoiding overt displays of money while still enjoying the benefits of financial prosperity.

In this article, we'll explore what stealth wealth is, how it manifests itself, and why it has become a growing phenomenon. The idea of stealth wealth can assist you in saving more money, making smarter investments, and cutting down on spending.

What is stealth wealth?

Stealth wealth is essentially the art of living a life of financial prosperity without drawing too much attention to it. It's about keeping a low profile even if you have the means to indulge in extravagant displays of wealth. Picture someone who drives a modest car, lives in a modest house, and dresses in an unassuming manner, despite being financially well-off. It's a deliberate choice to prioritize financial security and freedom over materialistic shows of opulence.

What does stealth wealth look like?

A person practicing stealth wealth focuses on essentials rather than indulging in conspicuous luxury. They lead a simple lifestyle and prioritize experiences and personal growth over material possessions

Stealth wealth enthusiasts carefully manage their finances, prioritizing long-term financial goals such as retirement savings, investments, and building wealth rather than spending lavishly on temporary gratification.

They might enjoy certain luxuries but do so in a discreet manner. For example, they may splurge on a nice vacation, but won't go out of their way to flaunt it on social media or discuss it in conversations.

Instead of trying to impress others with material possessions, stealth wealth embraces the importance of genuine relationships and connections. They focus on building meaningful connections, fostering friendships, and helping others in unique ways.

Why is stealth wealth an up-and-coming trend?

More and more people are recognizing the importance of financial independence. By adopting a stealth wealth lifestyle, individuals can accumulate wealth without the pressure to maintain an extravagant lifestyle, allowing them to have greater control over their financial future.

The rise of social media and the desire for privacy have made people rethink their approach to displaying wealth. Stealth wealth allows individuals to keep a lower profile, avoiding unnecessary attention and potentially increasing security.

As society becomes more conscious of overconsumption, and materialism, many individuals are reevaluating their own values and priorities. Stealth wealth aligns with the desire for a simpler and less materialistic approach to life.

Traditional markers of success, such as fancy cars or designer clothing, are being questioned. People are starting to realize that true success lies in financial security, personal fulfillment, and the ability to live life on one's own terms.

In conclusion

Stealth wealth is a rising trend that challenges our societal norms of displaying wealth. It's about finding a balance between financial prosperity and leading a modest, understated lifestyle. By prioritizing financial independence, privacy, and personal values, individuals embracing stealth wealth are redefining what it means to be successful.

So, if you find yourself drawn to the idea of a more discreet and restrained approach to wealth, consider joining the ranks of the stealthy and prosperous.

While everyone's wants and needs might be different, there is always a clear line in the sand between the two. When getting to grips with one's personal finance, distinguishing the key differences between the two becomes important.

Needs encompass basic needs like food while wants lean more toward things one desires, like luxury goods. Being able to distinguish between the two, and acting on this, is imperative to one's healthy financial standing.

In this article, we take a look at these two categories and assist you in differentiating between the two.

What falls under NEEDS?

The need category looks at living expenses that one needs to stay healthy in their day-to-day living. These include everything from rent to the utility bill, medication and healthcare needs as well as food, commuting, and any work-related expenses.

These are the basics required by one in order to function, and these should make up the bulk of your expenses. These expenses are also used to determine the amount you'll need when establishing your emergency fund. It is generally accepted that emergency funds should cover six months living expenses.

What falls under WANTS?

The wants category is likened to goods we could live without but choose to buy. These are not required for day-to-day living, however, when funds allow they can provide a more enjoyable quality of life. These include vacations, buying a house or car, entertainment, memberships, streaming accounts, etc.

How to determine needs from wants

While some needs will be glaringly obvious, it's often the case that some wants sneak into the needs category. Here are three simple tools to help you distinguish between the two.

Form vs function

If in doubt, consider how a product or service will be used. Clothing for instance: if the clothing will be worn to work it falls into the need category, however, if it's a clothing item centered around going out or recreation use, this will fall into the want category.

Embrace brand variety

Needs and wants will differ from person to person, so it's best to have a solid grounding on what falls into needs and wants specifically for you. For instance, if you were looking to upgrade your smartphone, someone working in the tech or digital marketing space might be required to have a certain product, while in other cases getting the latest and greatest will fall into the want category. In this case, it might be best to explore other devices that have a lower total value.

Should you split expenses?

Grocery shops will more often than not fall into the need category, as feeding yourself is essential to survival. However, if the grocery shop consists of wine, chocolate, and other treats, this will fall into the wants category.

While we don't expect you to scour through each grocery bill, be mindful of what you're spending your money on and try to balance shops between the two. For instance, if you splurge on a grocery shop one week with wants but register it in the needs category, consider adding the next week's grocery bill to the wants category.

Is saving a want or a need?

Saving for long-term financial objectives like settling debt, retirement plans, and emergency situations might be tough for someone who makes less money. Because these costs are not immediate, they are not always recognized as a necessity.

However, settling debt can be a necessity to ease the financial strain. Furthermore, an emergency may strike at any moment, and during that time, an emergency fund will save one from falling into further (if not crippling) debt. As a result, it's vital to understand that even if your earnings are low, saving is beneficial in the long run, therefore, savings fall into the need category.

How to navigate spending between wants and needs

Here are two easy steps to help you navigate your spending habits:

Create a budget

Establish a realistic budget and decipher how much you can spend on wants, needs, and savings. By creating a framework you can stick to, you can easily avoid any financial problems and still enjoy a good quality of life.

A common ratio used in the budgeting world is the 50:30:20 method. Use 50% of your income on needs (rent, food, bills), 30% on wants, and put the remaining 20% straight into your savings.

Be realistic about your wants

If you're looking to save more money or are working on building your emergency fund, consider adjusting your spending on wants. Being more strict with what you can and cannot buy or lowering your standards somewhat can assist you in saving money and rather allocating the funds to a retirement fund for example. Other ways to reduce spending habits are to get a roommate or use public transport.

In conclusion

Spending intelligently is without a doubt one of the most important ways to make your money go further. The principles, on the other hand, are focused on saving more, spending moderately on necessities, and sparingly on wants. Paying more attention to desires might lead to issues and limit financial development.

Consider carefully what your needs and wants are and then gradually attempt to lower your standard of living. By focusing on your essential needs without disregarding the importance of saving, you'll be on the fast track to financial ease in no time.

While Bitcoin remains ahead of the pack by a mile, that doesn't mean that it's the only cryptocurrency worth investing in. With thousands of coins on the market, there is plenty of innovative solutions and impressive technology to go around. In this article, we're outlining the 7 crypto coins you should know about, providing a range of Bitcoin alternatives that hold statistical significance.

Money in the bank is nice, but will it grow to the heights that we've witnessed in the digital currency markets? The answer is probably not. With the right portfolio, an adequate amount of research and solid trading strategies, you could be seeing impressive returns when compared to other assets in the financial sector. Consider the information below to be a strong starting point, and take it from there.

Ethereum (ETH)

Ethereum has the biggest market capitalization in the crypto industry after Bitcoin and has held this position for quite some time. The decentralised platform has made headlines in recent months as it shifts from a Proof of Work to a Proof of Stake network, requiring less energy to operate and a new means of rewarding the users for verifying transactions.

Ethereum is highly regarded in the industry for providing the first platform on which developers can create decentralized applications (dapps) and smart contracts. This allowed anyone the chance to build any app across any industry while harnessing blockchain technology. Providing a giant leap forward for blockchain development, Ethereum remains on the cutting edge of innovation.

Cardano (ADA)

Cardano was created by one of the Ethereum founders and is celebrated for being academically driven. While the project launched without a whitepaper (an unusual beginning for any cryptocurrency), at the time of launching there were over 90 academic papers written by a team of mathematicians, cryptography experts and engineers supporting the project. To this day all upgrades are rigorously tested through peer reviews before being implemented onto the blockchain.

Cardano offers developers a platform on which to build dapps and smart contracts using a proof of stake consensus. With lower fees and faster transactions, this eco-friendlier platform has been well received in the blockchain development community.

Polkadot (DOT)

Polkadot is a blockchain platform working toward blockchain operability, meaning that it allows various blockchains and oracles to exchange data and value in a secure manner. Through an intricate blockchain structure involving a relay chain and numerous parachains, the proof of stake network provides an innovative solution to connectivity and interoperability in the industry.

Polkadot was created by one of the Ethereum founders, Gavin Wood, and launched in 2020, quickly making its way to the top of the biggest cryptocurrencies on the market.

Litecoin (LTC)

One of the original hard forks off of the Bitcoin network, Litecoin is a long-standing payment focused cryptocurrency. Created by a former Google engineer in 2011, Litecoin went on to become an excellent Bitcoin alternative.

Through several changes to its predecessor's blockchain, the platform offers faster and more cost-effective value transactions over the internet.

Dogecoin (DOGE)

You will struggle to read cryptocurrency headlines without at least a few mentions of Dogecoin. Dogecoin is the original meme token and has been around since 2013. Designed to poke fun at the seriousness of the crypto industry, Dogecoin went on to become a massive cult favourite and accumulate some big fans along the way.

The blockchain is a hard fork off of the Litecoin network and provides fast, easy and cheap transactions. Typically sued for micropayments, such as tipping content creators on social media platforms, Dogecoin has seen massive success due to the tweets of Elon Musk and his favourable attitude toward the cryptocurrency.

Tether (USDT)

Tether is the first stablecoin to enter the market and one of the most successful. Currently ranking as the third biggest cryptocurrency by market cap, Tether sits behind Bitcoin and Ethereum. Designed to combat market volatility, Tether's value is pegged to the US dollar and is always valued at $1.

Tether was created in 2014 and is managed by a Hong Kong-based company of the same name. The blockchain platform provides not only an effective means of entering the crypto market but a payment solution for companies and individuals looking to conduct fast international payments without the risk of volatility.

Bitcoin Cash (BCH)

Another fork off of the Bitcoin network, Bitcoin Cash was created in 2017 as a result of a disagreement within the Bitcoin community. With several members torn over the direction of the Bitcoin network, several members chose to create a new blockchain and implement the changes they saw best for the network.

This resulted in a new payment focused blockchain platform offering a faster and cheaper means of the transaction value. Bitcoin Cash remains a strong Bitcoin alternative, with high daily trading volumes.

Create a well-rounded crypto portfolio

By considering these 7 alternative cryptocurrencies listed above, you have the opportunity to create a well-rounded crypto portfolio conveniently from your own home. All of these coins can be accessed through the Tap mobile application. You can easily view their market prices and engage in buying and selling digital currencies directly from your mobile device.

.png)

With inflation rates soaring across all corners of the globe, the rising cost of living is taking its toll on everyone involved. Before we dive into how you can stay afloat in these uncertain times, let's first cover the basics.

When inflation occurs, the prices of goods and services go up, which in turn decreases the buying power of consumers. This leads to a decline in economic growth as people now have less spending power and high costs to contend with.

Everything is more costly than it was a year ago—and even a few months ago. The cost of living has been going up dramatically, with costs for basic expenses like household goods and services on the rise. So, how can you stay ahead of the curve?

Below we cover three important steps to take in order to stay ahead of the rising cost of living. Protect your finances and protect your livelihood with these three top tips:

1. Safeguard your finances from inflation

While saving is vital to anyone's financial health, in periods of increasing inflation it's best to diversify and not keep all your savings in a fiat currency. This is due to fiat currencies depreciating in value during inflation, equating to a reduced amount of money in several weeks or months.

Instead, try to move some of your savings into vetted investments, this allows you to keep your funds safe and grow their value at the same time. This might also lead to capital appreciation and dividends, should you invest in dollar-based investments.

Explore alternative options that protect your funds from inflation but also allow them to grow.

2. Increase your income

For a while now, consumer prices have been increasing steadily. It's unfortunate but it doesn't look like things will be getting any cheaper in the near future. You can't keep waiting and hoping for a better situation - you need to take action.

The best way to do this is by focusing on ways to increase your income. Here are three options below, however, there are plenty more available online. Consider spending some time exploring this avenue.

Apply for a promotion

Ask for an increase/promotion: If you're currently earning a salary, it's probably time to talk to your employer about boosting your earnings. Make a thorough account of what you've achieved and why you deserve a raise—and present it to the correct person. Look for resources on how to ask for a raise if you don't feel confident to do so right now.

Learn a new skill

Add a new skill to your resume: With thousands of free tools online, look for a new skill that both interests you and leverages your current skillset. Learning a new skill is not only great for your mind but can also contribute to that promotion you are after or a high-paying job. Find an in-demand skill and get learning.

Monetize new skill

Turn your skill into an income: Whether it's your new skill or something you're naturally talented in, consider turning your skills into income-generating products. From creating online classes to consulting to publishing online books, turn your skill/s into money. Again, there are plenty of resources online that can assist you in this endeavor.

Focus on building wealth through avenues already accessible to you, from asking for a raise to creating an online course, these new avenues of income can help you stay afloat in periods of inflation.

3. Be wise with your money

This goes without saying, but no matter how much money you make, you want to stick to your budget and follow your financial plan. Now isn't the time to be spending lavishly. Also ensure that you have the resources in place to fall back on should you experience any unexpected hard times, like losing a job or emergency. healthcare costs

A great 3-step plan for preparing for, and then overcoming, inflation is to:

- Create a budget to cover basic expenses and lifestyle expenses, and stick to it.

- Pay off debt. Interest rates are going to increase meaning that you will be paying more for your current loan.

- Keep building your emergency fund. This is the first port of call when starting to save. Aim to have six months of living expenses saved up in an accessible account.

What is the cost of living index?

A cost-of-living index is a price index that measures the relative cost of living over time or in different regions. The index takes into account changes in prices for goods and services, as well as substitution with other items when prices vary.

As an example from the U.S. according to the Consumer Price Index (CPI), between March 2021 and March 2022, the cost of living index rose by 8.5% (before seasonal adjustment). This is the highest 12-month increase that has been reported since December 1981.

The bottom line on the cost of living

While inflation doesn't need to cause mass hysteria, it is a time to be more consistent and cautious with your money. Be mindful of what you're spending your money on, be aware that loan repayments will increase, and be prepared for increases in everyday goods and services. By following these three steps above (safeguard, increase, and be wise with your money), you should be able to stay ahead of the curve.