That fleeting Altcoin frenzy probably isn't what you think it was. The next crypto rally won't be like the ones you remember, it's a whole new thing.

Keep reading

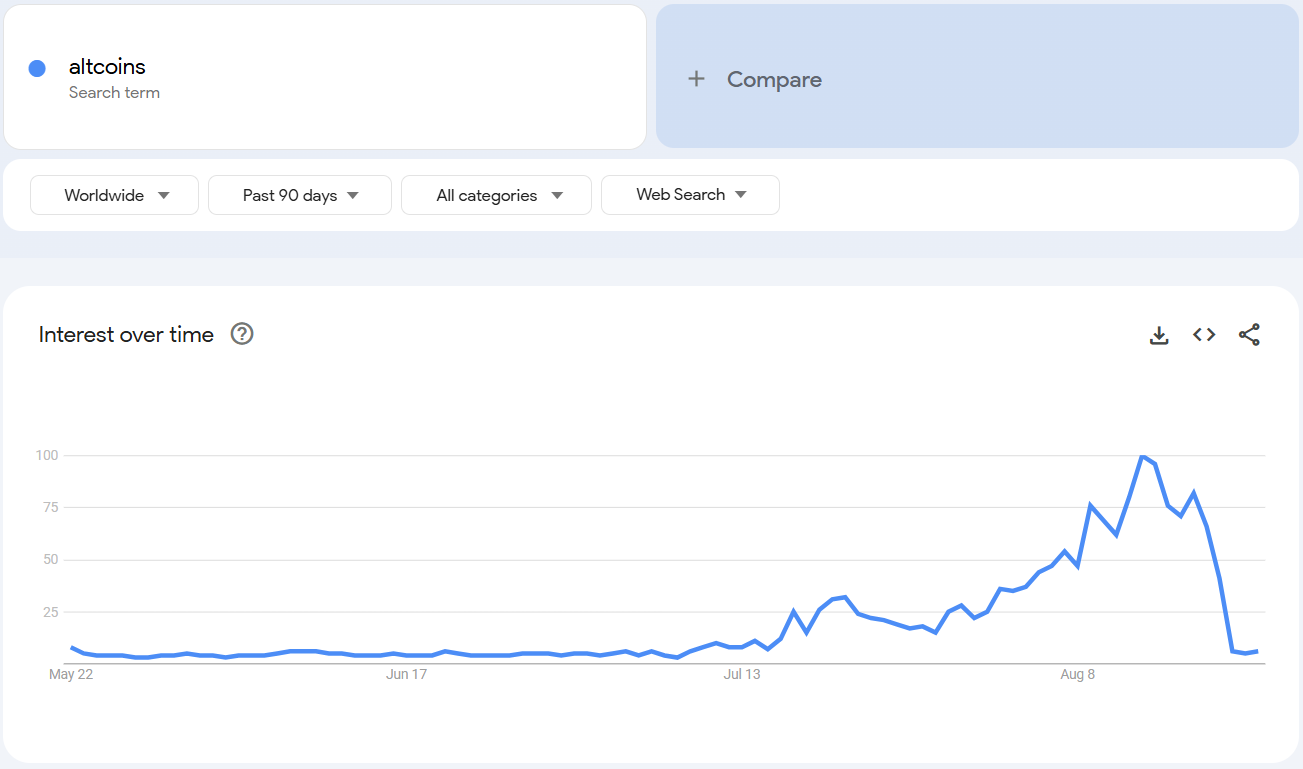

For a fleeting moment, it looked like altcoin season was finally here. Google searches for “altcoins” skyrocketed to record highs, 𝕏 was buzzing, and retail excitement seemed to return in full force. But within a week, that hype fizzled out almost as quickly as it appeared, leaving traders wondering if the long-awaited alt season was just a mirage.

A Spike That Vanished Overnight

Search interest for “altcoin” on Google Trends hit its highest score ever in early August, only to fall back to baseline levels within days. Globally, the same pattern played out, with scores dropping from 100 to just 16 in a week, mimicking a “pump and dump” pattern that you would expect from a memecoin.

Market cap data told the same story. The total value of altcoins (excluding Bitcoin and Ethereum) briefly climbed by $100 billion before giving it all back, leaving investors wondering whether the hype had any real weight behind it.

Naturally, some saw the collapse as proof that the altcoin season had ended before it really began. Others, however, like analyst Cyclop, argue the spike shows something deeper: that “altcoin” has become the mainstream term retail uses today, replacing “crypto” in 2021. In his view, this isn’t the peak. Rather, it’s just the beginning of broader interest.

Why Google Trends Doesn’t Tell the Whole Story

Relying on Google searches to measure retail demand may no longer work the way it used to. With AI tools increasingly replacing traditional search, and with concepts like “altcoins” now part of everyday investor vocabulary, Trends data might not be capturing where and how money is really flowing.

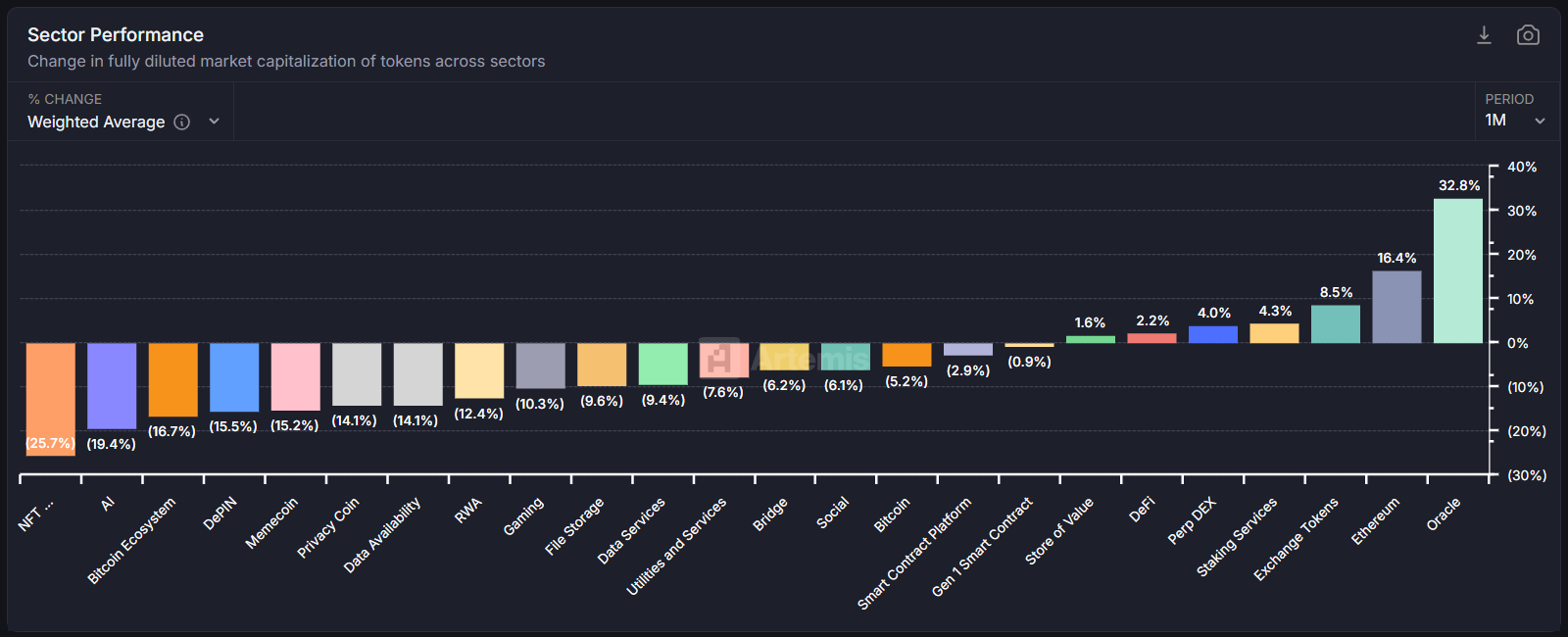

Instead, analysts point to on-chain and trading activity as better indicators of where momentum is building. And in August, that momentum was fragmented.

A Season of Winners and Losers

Data from Artemis showed only a few categories outperforming last month: Ethereum, exchange tokens, and oracles.

Beyond these bright spots, however, most altcoins struggled. The result? A patchwork “mini season” rather than the explosive, across-the-board surge that retail and social media had been hoping for.

Polygon’s co-founder Sandeep put it bluntly: "Retail is searching, but institutions aren't buying the narratives yet. Old altcoin seasons were driven by speculation and promises and narratives and marketing. Institutional money is smarter money. It cares about real utility and cash flows. The next "alt season" won't look like 2017 or 2021. It’ll be fewer tokens with actual usage, not just tokens with better marketing." Sandeep said.

The Road Ahead

That doesn’t mean altcoin season is dead, it probably just means it’s evolving.Coinbase has suggested that the next true wave could arrive as early as September, but that it likely won’t be a full-scale altcoin season.

Bottom line? The altcoin season isn’t gone; it’s just different. It’s maturing. And the next leg up may not belong to every token in the market, but only to the select few proving they can deliver value beyond mere speculation.

NEWS AND UPDATES

LATEST ARTICLE

Understanding what fiat on-ramps and off-ramps are will play a pivotal role for those looking to incorporate cryptocurrencies into their day-to-day lives. These “ramps” ensure a seamless experience integrating the use of both fiat currencies and cryptocurrencies. In this article, we explore the difference between the two and why they play such an important role in cryptocurrencies going mainstream, as well as the greater crypto ecosystem.

What is a fiat on-ramp?

Fiat on-ramps serve as important gateways that make it possible to convert traditional fiat currency (e.g. Euros or US dollars) into cryptocurrencies (e.g. Bitcoin or Ethereum). They act as bridges, connecting the world of fiat money with the exciting world of digital assets.

Through exchanges, brokerage services, and peer-to-peer platforms, these on-ramps provide convenient and accessible ways for individuals to enter the world of crypto. When using a fiat on-ramp, it's crucial to keep a few key considerations in mind. You'll want to ensure the security of your transactions, be aware of any fees involved, and fulfil any necessary verification requirements.

A fiat on-ramp can also be referred to as a fiat gateway or a crypto on-ramp.

The advantages of fiat on-ramps

Fiat on-ramps come with a range of benefits that make them a great choice for those entering the crypto world. One major advantage is the ease that an on-ramp can offer newcomers, providing a simple way to dive into the crypto market without needing extensive technical knowledge.

Additionally, an on-ramp typically opens up a wide array of cryptocurrencies to explore, expanding investment opportunities.

The disadvantages of fiat on-ramps

However, it's essential to be aware of the potential challenges and risks involved. Things like regulatory compliance and the risk of encountering fraudulent platforms or scams can pose concerns. To stay safe, it's important to do thorough research, read user reviews, and choose a reputable fiat on-ramp with strong security measures and regulatory compliance.

What is a fiat off-ramp?

Fiat off-ramps play an equally vital role as on-ramps in the world of cryptocurrencies by providing a way to convert digital assets back into fiat currency. Essentially, they serve as exit points from the crypto market, allowing users to cash out their investments and sell crypto.

Through crypto exchanges, peer-to-peer platforms, and even cryptocurrency debit cards, fiat off-ramps facilitate the seamless conversion of cryptocurrencies into fiat money. However, it's important to consider a few key factors when using an off-ramp.

Factors such as withdrawal limits, fees, which fiat currencies are supported and tax implications can impact the overall experience. Being mindful of these considerations ensures a smooth transition from the crypto world back to fiat currency while optimizing returns.

Fiat off-ramps can also be referred to as fiat gateways or crypto off-ramps and refer to the same off-ramp solution.

The advantages of fiat off-ramps

Fiat off-ramps offer several benefits that make them valuable for cryptocurrency users. One key benefit is the liquidity they offer, providing a way to convert digital assets into fiat currency whenever needed. This accessibility provided by a fiat off-ramp allows users to access their digital currency funds easily and use them in the real world.

Another advantage of an off-ramp is the ability to realize profits from cryptocurrency investments quickly, turning virtual gains into tangible returns. However, it's important to be aware of potential challenges and risks.

The disadvantages of fiat off-ramps

Several considerations to take when looking at using an off-ramp center around transaction fees and regulatory concerns. Note that transaction fees can eat into profits, and regulatory considerations may affect the ease of converting cryptocurrencies into fiat currency. To navigate these challenges, it's wise to choose a reliable fiat off-ramp by conducting thorough research, reading user reviews, and ensuring they comply with regulations. By doing so, individuals can make the most of fiat off-ramps while effectively managing associated risks.

The connection between fiat on-ramps and off-ramps

Fiat on-ramps and off-ramps are tightly interconnected within the cryptocurrency ecosystem, forming a crucial link in the cycle of converting between fiat currencies and digital currencies. The availability and efficiency of an on-ramp and off-ramp significantly influence the overall liquidity and adoption of cryptocurrencies.

Seamless on-ramps enable easy entry into the crypto market, attracting more users and boosting liquidity. Likewise, efficient off-ramps allow investors to convert their digital assets back to fiat money, providing the necessary flexibility and enhancing the adoption of cryptocurrencies in everyday transactions.

Reputable platforms like Tap exemplify this connection, offering both on-ramp and off-ramp functionalities to facilitate smooth conversions and foster a thriving crypto ecosystem. With a wide range of supported cryptocurrencies and fiat currencies, the platform caters to users around the world looking for a seamless ramp solution.

In conclusion

We've explored what a fiat on-ramp and off-ramp are, and the crucial role that they play in the world of crypto assets. We discussed the key points, including how an on-ramp facilitates easy entry into the crypto market and an off-ramp allows crypto users to convert digital assets back into fiat currency.

It's essential for cryptocurrency users and investors to understand these concepts as they provide liquidity, investment opportunities, and the ability to realize profits (in fiat currency). Looking ahead, the future of fiat on-ramps and off-ramps appears promising. As the cryptocurrency landscape continues to evolve, we can anticipate exciting advancements in these gateways, making crypto assets more accessible and further driving their adoption into mainstream use.

Arbitrage är en alternativ handelsstrategi där investerare köper en tillgång på en marknadsplats och säljer den på en annan – till ett högre pris. Strategin används inom allt från aktiemarknader som New York Stock Exchange till råvaruhandel och kryptovalutor. Rätt genomförd kan det vara en lukrativ metod, men som alltid finns det risker att känna till.

Här går vi igenom vad arbitrage innebär, hur det fungerar i praktiken och vilka risker du bör ha koll på.

Vad är arbitrage?

Arbitrage innebär att utnyttja prisskillnader på samma tillgång mellan olika marknader genom att köpa billigt på en plats och sälja dyrare på en annan – samtidigt. Prisskillnaderna uppstår på grund av ineffektivitet i marknaderna, något som arbitragehandlare både drar nytta av och indirekt hjälper till att rätta till.

De som ägnar sig åt detta kallas arbitrageörer och fokuserar ofta på ett specifikt tillgångsslag eller geografiskt område. Ett klassiskt exempel är att köpa en aktie på Londonbörsen och sälja den samtidigt på New Yorkbörsen – och på så sätt tjäna på prisskillnaden.

Även om det kan låta enkelt krävs både marknadskännedom och förmågan att snabbt identifiera möjligheter. Det är en avancerad metod som lämpar sig bäst för mer erfarna handlare.

Vilka risker finns det?

Arbitragehandel kan verka riskfri på ytan, men det finns flera saker som kan gå fel om man inte har full förståelse för hur marknaderna fungerar. Här är några av de vanligaste riskerna:

Felbedömningar i prisskillnader

Eftersom hela affären bygger på att upptäcka rätt prisskillnad i rätt ögonblick kan minsta felsteg göra att du blir sittande med en tillgång som inte längre går att sälja med vinst. Därför behöver arbitrageörer vara pålästa och följa nyhetsflödet noga.

Avgifter och växlingskurser

Avgifter från mäklare, transaktionskostnader och valutaväxlingar kan äta upp vinsten från en arbitrageaffär. Det är viktigt att räkna in dessa kostnader i förväg för att förstå om affären är värd att genomföra.

Timing

Timing är avgörande i arbitragehandel. Om du inte agerar tillräckligt snabbt kan prisskillnaden försvinna innan affären är genomförd. Det kräver både snabbhet och precision.

Hur börjar man med arbitrage?

Eftersom arbitrage ofta innebär handel mellan internationella marknader är första steget att övervaka och analysera dem noggrant. Du behöver hålla utkik efter tillfälliga prisskillnader och vara redo att agera direkt – köpa billigt på en marknad och samtidigt sälja på en annan.

Ett exempel på arbitrage

Låt oss säga att du följer ett bilföretags aktie som handlas på både Londonbörsen (LSE) och Tokyobörsen (TYO). Vid ett tillfälle ser du att aktien kostar motsvarande 100 USD i London och 75 USD i Tokyo.

Du köper aktien i Tokyo till det lägre priset och säljer den i London till det högre. Prisskillnaden – i detta fall 25 USD – blir din potentiella vinst per aktie.

Men i verkligheten tillkommer valutaskillnader och avgifter, vilket påverkar den faktiska vinsten. Ju fler aktier du hanterar, desto större blir möjligheterna – men även riskerna.

Är arbitragehandel något för mig?

Det finns potential för vinst, men det kräver tid, analys och noggranna beräkningar. Arbitrage är ingen genväg till snabba pengar – det är en strategi som kräver tålamod och förståelse. Om du är villig att lära dig och jobba aktivt med din analys kan det vara värt att utforska.

In this article, we delve into the distinction between revenue and profit, essential for businesses aiming to thrive financially. In a nutshell, revenue represents the total income generated from core operations, while profit is what remains after deducting all expenses. Join us as we explore the nuances between these two crucial concepts and their significance in business success.

What is revenue?

Revenue represents the total income earned by a business through its core operations, such as sales of goods or services. It can also be referred to as the top line of an income statement. It's essential for covering expenses, investing in growth, and generating profits.

Revenue comes from various sources like product sales, service fees, subscriptions, licensing, and advertising. Understanding and managing revenue streams are crucial for sustaining operations, attracting investors, and ensuring long-term viability in competitive markets. Thus, revenue serves as a vital performance indicator for businesses of all sizes and industries.

What is profit?

Profit refers to the financial gain a business achieves after deducting all expenses from its total revenue. On an income statement, profit is typically known as net income, however, the term "bottom line" is more commonly used. Profits appear on an organisation's income statement in a variety of ways and are used for various purposes and are a key metric indicating a company's financial health and efficiency.

There are two main types of profit:

Gross profit

Gross profit equals revenue minus the cost of goods sold, which consists of the direct material and labour expenses related to creating a company's products.

Operating profit

Operating profit equals gross profit minus other business expenses that are associated with running the company, such as rent, utilities, and payroll.

Essentially, profit is calculated by subtracting total expenses from total revenue. It's vital for business sustainability, expansion, and rewarding stakeholders and accurately measuring and maximising profit margins is essential for achieving long-term success and competitiveness in the market.

Revenue vs profit

When people refer to a company's profit, they are usually referring to the net income, which is what's left after expenses. It is possible for a company to make money but still have a net loss.

In an example below illustrating the importance of understanding revenue and profit, say a company producing light bulbs makes $10 million in the income generated. This sounds great, however, if the company's core business operations and debt add up to $12 million, the company is making a loss. Let's take a look at this example in greater detail below:

Business revenue or Total Net Sales: $10 million

Gross Profit: $4 million (total revenue of $10 million minus COGS of $6 million)

Operating Profit: $2 million (gross profit minus other business expenses such as rent, utilities, and payroll)

Profit or Net income: –$2 million (illustrating that the company is making a loss)

Profit will always be lower than revenue as this amount is determined after deducting all the operating and other costs.

A look at expenses

Operating expenses, including salaries, rent, marketing, direct costs, and utilities, which are necessary for day-to-day operations, and non-operating expenses, like interest payments or one-time costs, can impact profitability differently. By adequately controlling all expenses, businesses can maximise profit margins, reinvest in growth initiatives, and provide returns to stakeholders.

Overspending on unnecessary costs or failing to budget properly can significantly reduce profit margins, hampering long-term success. Therefore, monitoring and optimising expenses are integral parts of financial management strategies aimed at ensuring profitability and competitiveness in the market. With an effective strategy in place to measure and manage expenses, the price of goods and total sales will hopefully increase.

The importance of financial metrics

Financial metrics encompass a range of indicators used to assess a company's performance, including revenue growth rate, profit margin, and return on investment (ROI). These metrics provide insights into the effectiveness of business operations, helping organisations gauge their financial health and make informed decisions.

For instance, the revenue growth rate indicates the pace at which a company's sales are increasing over time, while the profit margin measures the proportion of revenue that translates into profit. Additionally, ROI assesses the efficiency of investments by comparing the gains or losses relative to the initial investment, aiding businesses in evaluating their investment strategies and maximising returns.

How to measure business performance

Measuring how well a business is doing means looking at both its revenue and profit. Revenue is all the money a business makes from selling things, while profit is what's left after taking away all the costs. By finding ways to make more money and spend less, a business can increase its financial health. Keeping an eye on important numbers like sales growth and profit margins helps a business see where it's doing well and where it can improve. This helps the business stay strong and competitive in the long run.

In conclusion

Companies base their success on two very important metrics: revenue and profit. While revenue is referred to as the top line, a company's profit is what really matters and is referred to as the bottom line.

It is crucial for investors to take both revenue and profit into account when making investment decisions, and to review the company's income statement in order to get a full view of the company's financial health.

In conclusion, revenue is the income a company makes without factoring in expenses such as debts, taxes, and other business costs. Profit, on the other hand, factors in all company expenses and operating costs.

When trading, market liquidity offers a measure of how quickly an asset can be converted to cash. The more market liquidity an asset has, the more easily it can be traded for cash. This comes into play when looking at its price point: the more tradable an asset, the less impact the trade will have on the asset's price.

Other factors to look out for include trading volume, technical indicators, and volatility. Liquidity is important for everything across the stock market and digital asset market to a company's liquidity, with liquid assets always being preferable. Let's first take a look at what liquidity is, the most liquid assets and the key takeaways liquidity refers to.

What does liquidity mean, exactly?

In its simplest form, liquidity looks at how easily and quickly an asset can be converted to another asset (bought or sold) without affecting its price. Liquidity can also sometimes be referred to as a cash ratio or marketable securities. A liquidity ratio helps investors determine whether something is a liquid asset or not and how easy it will be to convert assets.

When an asset has good market liquidity, this means that it can easily be traded for cash or other assets with no effect on the asset's market price. Referred to as liquid assets, these would include currencies, marketable securities, and money market instruments. This provides peace of mind to investors that have other financial obligations.

On the other hand, low liquidity means that the asset cannot be as easily bought or sold and any transaction that takes place will affect the asset's trading price. Real estate, rare items, and exotic cars present examples of illiquid assets, meaning that they may take longer to be sold, and not necessarily at the price the seller is expecting to receive.

What is the most liquid asset?

In terms of financial liquidity, cash is considered to be the most liquid asset.

Think of liquidity as a spectrum - on the one hand, you have cash (highly liquid) and on the other, you have rare items. Consider where on the spectrum an asset might fall to get an idea of its liquidity.

Types of liquidity

In a general sense, there are two types of liquidity: market liquidity and accounting liquidity used to measure the current ratio of an asset or company.

What is market liquidity?

The first of the two types of liquidity is market liquidity, defined as the ease with which a financial asset may be bought and sold at fair prices. These are the prices that are most similar to the assets' actual value, known as their intrinsic value.

Intrinsic value in this case refers to the lowest price a seller is willing to accept (ask) and the highest price a buyer is willing to pay for it (bid). The bid-ask spread, also known as the trading spread, is the difference between these two values. The lower the bid-ask, the greater the liquid asset.

What is accounting liquidity?

Accounting liquidity describes a company's ability to pay its short-term debts and liabilities with its current assets and cash flow. In other words, it reflects the company's financial health: the higher the company's accounting liquidity the more liquid the company's capital.

Most commonly, you'll hear accounting liquidity mentioned in relation to businesses and their balance sheet. This has less to do with liquid assets and more to do with businesses, and the company's financial health, as a whole.

What is a bid-ask spread?

The bid-ask spread refers to the difference between the highest bid and the lowest ask price. As you would expect, a low bid-ask spread is preferred in liquid marketplaces. It implies that the market has sufficient liquidity since traders continuously bring the high and low prices back into balance.

A wide bid-ask spread, on the other hand, generally indicates illiquidity in an asset and a substantial gap between what buyers are willing to pay and what sellers are willing to accept.

The bid-ask spread plays a valuable role for arbitrage traders as they attempt to take advantage of minor disparities in the bid-ask spread over and over again.

While they make money, their activities help to support the market as they reduce the bid-ask spread, and other traders will have better trade execution as a result of their activity.

Arbitrage traders also make sure that the same market pairs do not have significant price disparities on various exchanges. Have you ever seen how the Bitcoin price is roughly similar across the most liquid markets? This is due in large part to arbitrage traders who exploit small variances between prices on different exchanges to profit.

Why liquidity plays an important role in the markets

Bigger stocks and digital currencies tend to have more liquid markets due to their higher trading volume and market efficiency.

The amount of money traded per day, otherwise known as liquidity, varies depending on the market. For example, some markets may only have a few thousand dollars of trading volume while others have billions.

Assets from large companies or establishments don't usually have issues with liquidity since there are many buyers and sellers in their respective markets. However, this isn't the case for less traded assets which often lack significant liquidity.

When building your portfolio ensure that you incorporate (or stick to) liquid markets so that you can always know that should you wish to liquidate the asset you will get a good price. Sometimes with smaller assets, you might not be able to exit the market at your desired price leaving you with an invaluable asset or one traded at a significantly lower price.

This is known as slippage and can result from trying to fill a large order in an illiquid market. Slippage is the difference between the price you intended to sell at and at what price your trade is actually executed.

High slippage indicates that your transaction was completed at a significantly different price than you intended. This usually occurs because there aren't enough orders in the order book near to where you wanted to execute them. This can be avoided by only using limit orders, but this runs the risk that your order may not be filled.

The market conditions significantly affect liquidity. For example, in a financial crisis, different traders might respond by either selling their assets or withdrawing cash.

Final thoughts

When it comes to the markets, liquidity refers to the ease of trading in a market. Traders often favor liquid markets because they provide convenient access for entering and exiting positions. The level of liquidity can influence the efficiency and effectiveness of trading strategies. Depending on your preferences, you might consider including highly liquid assets in your portfolio, which can have benefits in terms of flexibility.

Porter’s 5 forces is a model that helps to identify the weaknesses and strengths of an industry, empowering the potential investor with insights. In fact, the model is used by more than just investors, companies and analysts also make use of its structure, allowing them to analyze the competitive forces in an environment and build an appropriate business strategy.

Below we outline how the Porter’s five forces model works, where it came from, and how you can use it to your advantage.

What is the Porter's Five Forces model?

Porter’s Five Forces focuses on identifying and analyzing five competitive forces within an industry that can be used to establish what the industry’s strengths and weaknesses are. The five forces analysis can be applied to any segment of the economy and can determine a company’s business strategy, level of competition, or long-term industry profitability.

The Five Forces are:

- Competitive forces in the industry

- Potential of new entrants into the industry

- Power of suppliers

- Power of customers

- The threat of substitute products

This model is designed to help analysts and managers comprehend the competitive landscape that a particular company faces and how the company is positioned within it.

Where did Porter’s Five Forces model come from?

The five forces analysis model was created by and named after Michael E. Porter, an established Harvard Business School professor. The model was introduced in Porter’s book, Competitive Strategy: Techniques for Analyzing Industries and Competitors.

Developed in 1979, the five forces analysis model was created to provide industry outsiders with insight and knowledge into the positioning and competitive strength of an organization. The business analysis model has become an important tool in the financial sector and is still widely used today, over 40 years later.

Breaking down Porter’s Five Forces

Below is a breakdown of the Five Forces analysis model which is universal across almost every market and industry in the world. The model looks at the company’s positioning within the market to determine how much power it holds.

1. The competition in the industry

The first of Porter's Five Forces analysis model focuses on the number of competitors a company has and its ability to undercut them. The more existing competitors and competitive rivalry a company has, along with the number of similar products and services they offer, the less power the company holds.

When the company has a high level of competitive rivalry, suppliers and buyers will gravitate toward the lower prices, while when competition is low, companies have more control over the prices they charge and the terms of their deals.

More power equates to a competitive advantage which typically equates to more sales and profits. Hence, why industry competition and competitive forces shape strategy.

2. The potential of new entrants into an industry

Of course, new entrants into the market also pose a threat to a company’s power. This can be measured by looking at the amount of time and cost it would take to be a potential competitor. The more resources needed, the more established the company’s position.

The stronger the barriers to entry, the better for companies already positioned in the market.

3. The power of suppliers

This point in Porter's five forces analysis model looks at the power the suppliers hold in terms of driving up the costs of resources. This can be determined by looking at the number of suppliers available, how unique their products are, and the cost of a company switching to another supplier.

The fewer the number of suppliers, the more a company depends on them in turn driving up the supplier’s power. The supplier then has more control over their input costs which can result in lower profits for the company.

4. The power of customers

The power of customers looks at how much control the consumer has to drive a company’s prices down. This looks at the number of customers a company has, the impact of each customer, and the cost of finding new customers or markets to sell to.

The smaller the customer base, the more power they have to negotiate lower prices. While a larger customer base with many smaller clients is able to charge higher prices and in turn increase profitability.

5. The threat of substitutes

The final of Porter’s Five Forces analysis model is the threat of substitutes and looks at the threat that substitutes goods and services can pose to a company. The more unique and more difficult a product or service is to substitute, the better the company’s positioning. As consumers will have little else to turn to, the company automatically accumulates more power.

These Five Forces analysis can assist a company in building a strategy that ensures well-utilized resources and boosted profits, however, this strategy will need to be consistently visited to ensure that any changes in the external environment are factored in.

What are the downsides of Porter’s Five Forces?

The most pressing downside of the Five Forces model is that it was designed to look at an individual company, as opposed to the wider industry. Additionally, this proves difficult when the company falls into two or more industries, making the framework less impactful.

The final downside is that the model is designed to measure all five aspects equally against each other which isn’t always the case. Some factors might be more prevalent in one industry but less relevant in another.

Porter's Five Forces Model vs SWOT analysis

Another tool used in the business sector is SWOT analysis, which looks at the strengths, weaknesses, opportunities, and threats of existing companies. When comparing the two the most prominent differentiation is that Porter’s Five Forces model tends to examine the external environment and competitive strategy of a company while SWOT looks at the internal aspects of an organization.

In conclusion

This business analysis model aids in assessing the competitive landscape within a company's industry. The level of influence a company wields across these factors could potentially shape future profitability.

Porter’s Five Forces forces company’s to look beyond their organization and at the greater industry structure in order to map out future plans and strategies. While this framework still plays a valuable role in the business sector, it should not be the only tool used by a company to determine its strategy.

In line with our how-to-budget pieces, today we're looking at how to monitor your spending. There's no good in building an impressive budget without keeping track of whether you're sticking to it or not. Yes, it might sound tedious, but it is always worth it, especially during the festive season when things tend to get a little out of control.

Paving the road from good intentions to excellent outcomes, tracking your spending is imperative.

Why tracking expenses is important (use your bank account to save money)

Before we get started, let's first cover the bases of why this step is so vital. First and foremost, it's essential to hold yourself accountable to your proposed budget. There's no good assigning each dollar you earn to a specific function only to disregard the budget entirely and spend impulsively.

If you're not tracking your expenses you'll land up in square one where you started a month ago. Monitoring your spending habits will show you exactly where your money is really going, and help you to make more informed decisions. The best part is that after a month or two you will get the hang of it and the process will become a lot less tiresome and feel like more of a habit.

Keeping an inventory of your expenses (and income)

First, you'll need to create your budget. Once this is established and the time frame you've set it out for has started, it's time to get tracking. You can do this through a budgeting app, a spreadsheet, or a piece of paper if that makes you most comfortable.

Step 1: track your income

In your income section, confirm all income in the columns provided. If you make money in an unexpected avenue, be sure to add this in too. This step is particularly important for those that earn irregular income through freelancing or side hustles.

Ideally, you would have listed your income avenues as a low estimate, so revel in adding the higher amounts into the columns provided. You can then enjoy reallocating those funds to various items in your expenses column. Don't think you need to be a robot with your finances, you're allowed to enjoy them too.

Step 2: track your expenses

For this step you need to track every single time money leaves your account. For the entire month. From emergency fund allocations to debt payments to monthly expenses, and any payments on a separate spending account. Each time you spend money, record it in the relevant expense categories.

When you buy groceries, add this to your grocery expenses; when you eat out, add this to your entertainment expense. Make sure that your budget is updated to reflect the new total so that you and your checking account are always in the know.

For example, if your grocery budget is $100 and you spend $23, add the $23 as an expense item under the title and ensure that your new grocery total reflects as $77.

There are plenty of expense tracker apps out there if this helps you stay on track. If you are using a budgeting app be sure to check in and review how each category is doing so that you can make informed decisions on what you spend your money on.

Step 3: make it a habit

You might like to do this daily or biweekly at first until you get the hang of it. Make yourself a nice cup of tea and make it a pleasant habit, instead of something you resent and put off. Understanding your cash flow is imperative to understanding your spending patterns and to better manage money. This is where the magic happens (and how financial goals are achieved).

Different methods of tracking your expenses

Below we outline the four most common methods used to track expenses, looking at the advantages and disadvantages of each of them. Whether you prefer paper receipts or accounting software, settle for the expense-tracking method that works for you.

1. Handwritten

There's nothing wrong with the old-school pen and paper option, if this feels right to you then go for it! Make sure you store it in a safe space.

Advantage: studies suggest that writing things down increases your retention of the information and boosts your ability to make more informed decisions. While typing is probably the preferred method, writing is actually more efficient when it comes to learning.

Disadvantage: this option is more time-consuming and will require you to physically remember all your purchases and retain your slips. Alternatively, you could sit with a printout of your bank accounts and manually write out each expense.

2. The cash process

This step requires you to withdraw the cash outlined in each budgeted category and store it in an envelope. Every time you make a transaction, you use the cash from the relevant envelope and replace it with the receipt. For debit orders, you can use your imagination. While the envelope method might be considered an old-school option for money management, if it works for you then go with it.

Advantage: using this method of tracking monthly expenses you can physically see how well your budget is going and how much you have left to spend.

Disadvantage: in these modern times paying with cash isn't always very practical.

3. Spreadsheet

Probably the more common option when it comes to tracking your expenses, using a spreadsheet can be practical and it does the maths for you.

Advantage: with tons of templates, the ability to quickly customize or revise your budget and the automated calculator, spreadsheets are a great option.

Disadvantage: you'll need to physically sit down with your laptop when tracking all your transactions. This will become more challenging the longer you leave it so ideally you;ll need to make this a daily occurrence. Remember, without monitoring your expenses your budget is simply a plan.

4. Budgeting apps

There are several budgeting apps available (for free) that can link to your bank account and automatically track all your expenses.

Advantage: It's all done for you, in real-time. Some apps might require you to assign the transaction to a category while others might automatically categorize it for you, either way, it requires minimal effort and can be regularly updated.

Disadvantage: You still need to monitor your spending, even if you're not physically putting it in. If you've reached your grocery budget, you need to be aware as the app is not going to cut your spending for you.

In conclusion

Whichever method you opt for, tracking your expenses is imperative to sticking to your budget and getting you one step closer to your financial goals.