An in-depth look at XRP’s 2025 momentum, as legal clarity, technical strength, and growing institutional interest converge for the first time since 2017.

Keep reading

This week, XRP has been building pressure at $3.30, with three powerful catalysts aligning for the first time since 2017 - setting up what could be the token's most explosive run yet.

TLDR:

- XRP price surged 21% after the SEC Ripple Labs case was officially dismissed

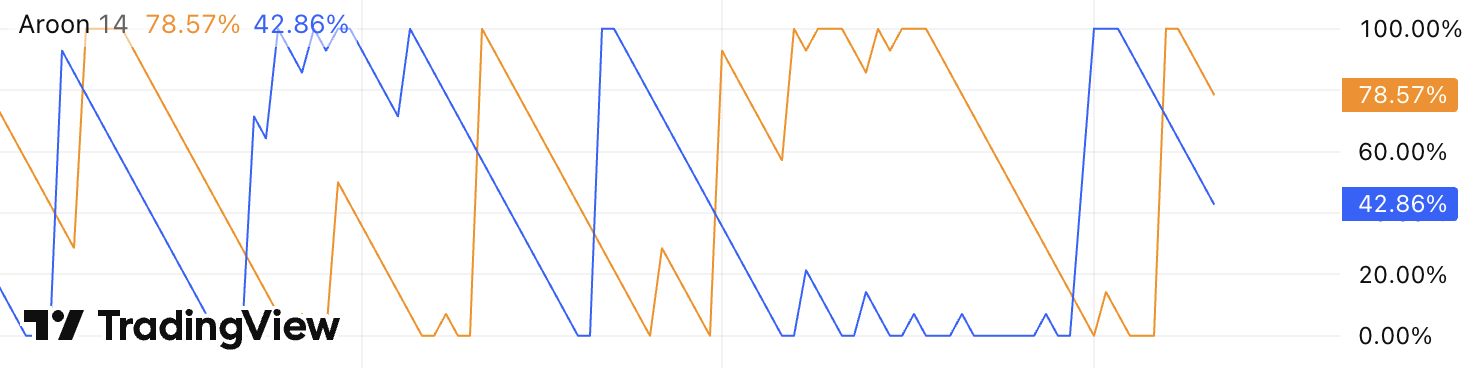

- Technical indicators show buy-side momentum peaking, with Aroon Up hitting 100%

- Nine major asset managers now have pending XRP ETF applications, with 88% market odds for 2025 approval

- CME's XRP futures launched in May have already generated over $1.6 billion in trading volume

Three big forces are hitting XRP at once: legal clarity, strong technical momentum, and rising institutional demand. In the past, this mix has sent prices soaring.

The legal victory that changes everything

The SEC's formal dismissal of its case against Ripple Labs isn't just another regulatory win - it's the removal of XRP's biggest institutional adoption barrier. After nearly five years of uncertainty, corporate treasuries and institutional investors finally have the green light they've been waiting for.

And the timing couldn't be better. Just as regulatory clouds clear, analysts are agreeing that XRP's technical setup is screaming bullish signals that haven't been seen since the 2017 run-up.

Technical momentum reaches peak levels

XRP's chart tells a compelling story of institutional accumulation disguised as consolidation:

→ For starters, the token has climbed 21% over the past seven days, hitting a recent high of $3.36 (just 8% below its ATH). Momentum indicators suggest this is just the beginning.

→ The Aroon Up line is holding at 100%, showing that buyers are consistently driving XRP to fresh highs. This sustained strength often comes before major moves - especially with the price holding above the key $3.15–$3.16 support area. *To view the current Aroon line, log into Trading View and add the indicator.

→ Market sentiment has shifted decisively bullish, with XRP's weighted sentiment score hitting a two-week high of 1.17. More telling is the token's social dominance, which has climbed to a recent high of 7.95%, meaning XRP is dominating an increasingly larger share of crypto conversations as retail interest reignites.

The institutional infrastructure is already built

While crypto X debates ETF timelines, institutional players have quietly constructed the infrastructure needed for serious XRP adoption. CME Group launched regulated XRP futures in May, providing the hedging tools institutions will need before taking major positions.

The results speak volumes: CME's XRP futures have already surpassed $1.6 billion in trading volume, signalling genuine institutional demand beyond retail speculation. These aren't just paper trades; they represent real institutional capital positioning for XRP's next move.

Nine major asset managers now have pending XRP ETF applications, including heavyweights like Grayscale, ProShares, and 21Shares. Polymarket traders are pricing in 88% odds for SEC approval by year-end, creating a feedback loop where institutional preparation drives retail anticipation.

Why this time is different

Previous XRP rallies were driven primarily by retail speculation and partnership announcements. But today's setup combines retail enthusiasm with genuine institutional infrastructure and regulatory clarity: a trifecta that hasn't existed since XRP's 2017-2018 surge.

The numbers back this up. Institutional trading volumes have spiked 208% to $12.40 billion following the SEC dismissal, while derivatives open interest climbed 15% to $5.90 billion.

Large-order flows are consistently defending the $3.15 support level, suggesting institutional accumulation even during short-term volatility.

What traders are watching

Analysts are saying that technical analysis points to immediate resistance at $3.39-$3.40, with sustained bullish momentum (bolstered by institutional flows and ETF positioning) raising the odds of a breakout, particularly if the Aroon Up indicator remains high.

According to market insiders, a successful move higher could fuel a run toward the $3.50-$3.75 range, with a longer-term target of $3.66+ for a cycle high retest.

Key levels to monitor:

- Support: $3.15-$3.16 (proven institutional buying zone)

- Resistance: $3.39-$3.40 (breakout confirmation level)

- Bull target: $3.66+ (cycle high retest)

Legal clarity, a technical breakout, and rising institutional demand are all hitting XRP at once - a rare mix of fundamentals and market momentum. For holders who’ve endured years of regulatory uncertainty, some are interpreting this as a potential breakout scenario.

NEWS AND UPDATES

LATEST ARTICLE

Ethereum Name Service (ENS) är ett spännande projekt som syftar till att göra kryptovärlden, särskilt inom DeFi och Web3, mer lättillgänglig. Precis som domännamnssystemet (DNS) förenklade webben genom att ersätta IP-adresser med minnesvänliga namn, gör ENS samma sak för kryptoadresser.

Vad är Ethereum Name Service?

ENS är ett decentraliserat namnprotokoll som gör det möjligt att koppla en mänskligt läsbar domän (som t.ex. namn.eth) till en Ethereum-adress. Det innebär att man slipper långa, svårtydda teckensträngar och istället kan ta emot betalningar till ett enkelt och begripligt namn.

Till exempel: Istället för att ange en adress som 0x71C7656EC7ab88b098defB751B7401B5f6d89, kan du bara skriva dittnamn.eth.

Du registrerar domännamn via ENS Manager eller andra godkända registratorer. Domänen sparas i ENS-registret, och du blir officiellt ägare av den.

ENS använder ett hierarkiskt system, där du också kan skapa subdomäner (t.ex. wallet.dittnamn.eth) som du kan använda eller dela med andra.

Hur fungerar Ethereum Name Service?

ENS-systemet bygger på två huvudkomponenter: ENS-registret och resolvers (avkodare). Tillsammans översätter de domännamnet till rätt kryptoadress.

ENS-registret

Här registreras alla domännamn (t.ex. .eth) och information om vem som äger vad. Det är första steget när du skaffar en ENS-adress.

Resolvern

En smart kontraktlösning som kopplar domännamnet till den faktiska Ethereum-adressen. Du kan använda en standardresolver eller en egen. När någon skickar ETH till dittnamn.eth, frågar systemet resolvern efter den kopplade adressen – och voilà, transaktionen går igenom.

ENS kan även lagra annan information, som IPFS-hashar eller Swarm-länkar, vilket möjliggör länkning till decentraliserat innehåll.

Vem skapade Ethereum Name Service?

ENS föreslogs första gången 2016 av Nick Johnson, en tidigare Google-ingenjör och Ethereum Foundation-utvecklare. Projektet lanserades som ett fristående initiativ i maj 2017 och har sedan dess vuxit till att bli en grundpelare inom Ethereum-ekosystemet.

Vad är ENS-tokenen?

ENS-tokenen lanserades 2021 som ett sätt att ge användare inflytande över ENS-ekosystemets framtid. Den används inte för att betala för domänregistreringar – det sker fortfarande med ETH.

Istället är ENS-tokenen ett governance token, vilket betyder att innehavare kan rösta om viktiga förändringar i systemet.

Prisexempel för att registrera .eth-domäner:

- $5 i ETH/år för domäner med 5+ tecken

- $160 i ETH/år för domäner med 4 tecken

- $640 i ETH/år för domäner med 3 tecken

Ju kortare domän, desto högre pris – eftersom tillgången är mer begränsad.

Totalt skapades 100 miljoner ENS-token och en stor andel delades ut genom en community-airdrop vid lanseringen.

Vad är ENS DAO?

ENS DAO är en decentraliserad organisation där ENS-tokeninnehavare röstar om projektets framtid. Det kan handla om förbättringar, nya funktioner, eller policyförändringar.

DAO:n spelar en viktig roll för att se till att ENS utvecklas i linje med communityns behov – öppet och transparent, precis som det bör vara i en decentraliserad värld.

Vad är ENS Foundation?

ENS Foundation är en ideell organisation som stöttar utvecklingen och tillväxten av ENS. Den fokuserar på:

- att främja adoption

- stötta utvecklare och användare

- hålla i evenemang och finansiera projekt inom ekosystemet

Tillsammans med ENS DAO ser stiftelsen till att plattformen både växer och förblir decentraliserad.

Hur köper jag ENS-token?

Via Tap-appen kan du enkelt köpa, sälja och lagra ENS-tokens. Du kan handla ENS med fiat eller andra kryptovalutor, och allt sker tryggt via Tap:s integrerade plånbok.

Ladda ner appen, skapa ett konto, verifiera din identitet – sen är du redo att börja använda ENS och andra kryptotillgångar, smidigt och säkert.

Crypto wallets are a critical tool for anyone looking to use, store, and manage crypto assets. Crypto wallets come in various forms, with different features and security options that cater to the needs of different users. Finding the right crypto wallet is essential if you want to get the most out of your cryptocurrency investments.

No matter what type of crypto wallet you choose, it’s important to do your research before making a decision since each one comes with its own set of advantages and disadvantages. It’s also important that you keep your private keys safe so no one else can access them, this will ensure that only you have control over your funds and crypto assets.

What is a crypto wallet?

A crypto wallet is a digital wallet that stores manages and facilitates the use of various cryptocurrencies. In order to store and use crypto assets, one needs a digital wallet. Unlike traditional wallets that simply hold your cash or cards, crypto wallets facilitate transactions as well as store your funds.

Each crypto wallet has a public and private key which are unique alphanumeric codes that grant the user access to the funds. Public keys are wallet addresses to which other users can send you cryptocurrencies, similar to your bank account number, while private keys are akin to a pin number and should not be shared with anyone.

In essence, crypto wallets act as secure interfaces for users to access, store and transfer funds across different blockchain networks. In essence, it’s like a bank account for digital currencies.

The different types of crypto wallets

Crypto wallets can be divided into two main categories: hot wallets and cold wallets.

Internet connectivity is the defining factor between hot wallets and cold wallets. Hot wallets are connected to the internet, making them less secure but much more user-friendly. On the other hand, cold wallets are stored completely offline and do not require any internet connection. This provides a higher level of security, which makes them ideal for individuals who plan on storing their crypto assets long-term.

Each of these categories can be further broken down into varying wallets. Under the hot wallets umbrella, there are desktop wallets, mobile wallets, and web wallets, while under the cold wallets umbrella, there are hardware and paper wallets.

Hot wallets

As a hot wallet is easy to set up and constantly connected to the internet they are ideal for users looking to make daily or frequent transactions. Typically with hot wallets, funds are quickly accessible and they tend to be very straightforward to operate. Below we look at the three main types of hot wallets: desktop wallets, mobile wallets, and web wallets.

Desktop wallet

A desktop wallet is a cryptocurrency storage solution that allows users to store, send, and receive crypto assets from their personal computers with the crypto wallet stored on the device’s hard drive.

It is generally considered to be a secure way of managing crypto assets as it does not require the user to store their funds on an exchange, instead giving control over the private keys associated with the hot wallet to the user.

The downside however is that it may be vulnerable to computer viruses should someone gain access to your desktop.

Mobile wallet

Mobile wallets are digital crypto wallets that allow users to manage their cryptocurrencies directly on their mobile devices. These crypto wallets are very convenient and secure compared to carrying large amounts of money around or keeping it in a traditional bank account.

Mobile wallets provide users instant access with more control over their funds and are particularly useful for quick payments that require a scan of a QR code. When downloading this type of hot wallet ensure that you use a link from the website directly to ensure that you are not falling for a fake wallet. This goes for all hot wallets and cold wallets listed here.

Mobile wallets are typically the best crypto wallets for users actively spending their crypto assets.

Web wallet

Web wallets are hosted by third-party services, which act as custodians for users' private keys. Web wallets provide an easy way to manage digital currencies, allowing users to quickly send and receive payments without having to download or install any software.

Additionally, web wallets offer enhanced security features such as two-factor authentication and multi-signature transactions. With these features in place, web wallets can provide a secure environment for storing cryptocurrencies regardless of the user's level of technical expertise, an added bonus for hot wallets.

Cold wallets

Cold wallets are hack resistant and therefore are considered the best crypto wallets for hodlers. In order to facilitate trades, cold wallets need to connect to the internet in order to trade directly from their cold storage devices.

Hardware wallet

Hardware wallets store private keys on a physical device like a USB drive or an external hard drive. A common example of this is the Ledger Nano X, while secure it retails for roughly $150.

These crypto wallets provide maximum security but require more effort to set up and use compared to other types of crypto wallets. They typically are also more expensive as one needs to buy a physical device.

Paper wallet

Finally, paper wallets are simply printed copies of public/private key pairs which allow you to securely store funds offline without having any digital device at all. While these are considered to be the best crypto wallets in terms of security, if the paper gets damaged then the funds are lost.

Finding the right crypto wallet for you

In order to find the right crypto wallet you will need to establish what specifically you wish to do with your funds. If you are looking to hold them long-term, cold wallets are by far the more secure solution, however, if you are making payments and using cryptocurrencies in your day-to-day life, a hot wallet or even a mobile wallet might be better suited to your needs.

Many crypto users utilize a combination of two or three, using the more secure crypto wallet option to hold their funds long-term while also having a portion of funds in a preferred hot wallet allowing them quick and easy access to their funds when they need them.

Index funds are an increasingly popular form of investment that offers investors a low-cost, passive way to gain exposure to a broad range of assets. With minimal management fees and no need for active trading decisions, index funds can provide investors with higher returns at lower costs than more traditional forms of investing.

What is an index fund?

An index fund is a type of mutual fund or exchange-traded fund (ETF) composed of a basket of stocks or bonds that tracks a specific stock market index such as the S&P 500 or Dow Jones Industrial Average. These might also be referred to as index mutual funds.

Unlike actively managed funds, which attempt to beat their respective benchmarks through security selection, index funds strive to replicate their underlying market indexes by holding all (or substantially all) of their components in similar proportions.

This makes index mutual funds more cost-effective than actively managed funds since they incur fewer trading costs and require less research and fewer management fees. On top of that, since they track established indexes, investors can benefit from the diversification within the asset class without having to pick individual stocks themselves.

Index funds provide an easy way for investors with any level of experience or resources to access some of the market's best-performing assets at a minimal cost. Index mutual funds are also favored for long-term investment strategies such as retirement funds.

How do index funds work?

Index funds, also commonly referred to as "indexing", follows a passive form of investing (unlike traditional mutual funds that are typically actively managed funds). Instead of fund managers actively trading a variety of stocks, index funds are built by mirroring the securities of a particular index and holding them.

The key notion is that by mirroring the profile of the index or stock market, the fund will match its overall performance. For example, over the last thirty years, the S&P 500 has grown an average of 10.7% per annum, which its index mutual fund will mimic.

While the most popular index fund tracks the S&P 500, other prominent index mutual funds include:

The Bloomberg U.S. Aggregate Bond Index

Which tracks the bond market.

The MSCI EAFE Index

Which tracks foreign stocks in Europe, Australasia, and the Far East.

The Dow Jones Industrial Average (DJIA)

Which tracks 30 large-cap companies listed on the stock exchange.

The index fund portfolio holdings will remain as is unless there is a significant change in the market's benchmark index. Benchmarks are used to measure the performance of the market indexes and will influence whether any changes to the composition of the portfolio need to be made. If changes are necessary, managers will rebalance the percentage of securities as necessary.

Passive vs actively managed funds

Both mutual funds and index funds are great investments, however, they differ slightly in how they operate and the returns one can expect. As with any investment endeavor, investing involves risk.

Actively managed funds

An actively managed investment fund offers investors access to an experienced team of financial professionals or simply a fund manager who makes knowledgeable decisions about where and how to allocate the funds across asset classes. This generally enables larger returns than traditional passive investing.

Typically, many mutual funds are actively managed funds, however, it's best not to assume a fund is actively or passively managed simply based on the fund type. There are plenty of funds that break this rule, like actively managed exchange-traded funds.

The advantages of an actively managed fund are that it can earn higher returns and beat the market index. It's important to note that this is not a guarantee so it's best to check the history of the fund you wish to invest in beforehand and the performance of the team managing it.

It's also worth noting that when the mutual fund sells individual stocks it incurs fees and taxes which will affect the fund's performance. Investors are also required to pay a flat fee despite the performance of the actively managed mutual funds, which could result in the mutual fund underperforming the market index.

Passively managed funds

On the other hand, a passively invested fund mimics a market index and does not have a fund manager or team of fund managers making decisions on what and when to invest.

With passive funds, there are fewer decisions to be made and trades to execute, which allows for less effort and lower fees. Automating the bulk of a passively managed index mutual fund makes it much more cost-effective than paying professionals to determine when and what should be bought or sold.

Typically, an index fund will fall into this category as it does not require full-on management. Once the index on which it will mimic is established, the shares are purchased and the index fund continues with little to no input.

Index funds vs mutual funds

Investors looking to build a portfolio have two popular fund options: index funds and mutual funds. Both types of funds are created by offering diversification through a curated range of stocks and bonds and access to professionally managed investments, but there are some key differences between index funds and mutual funds that investors should be aware of before making their choice.

Index funds typically carry lower fees than mutual funds, but they also come with fewer features and tend to be more passive in nature.

Actively managed mutual funds on the other hand provide more flexibility when it comes to customization, as well as access to professionally-managed portfolios which may yield higher returns over time. Understanding how both index and mutual funds work will help investors make an informed decision about which type is right for them.

Is it worth investing in index funds?

Financial professionals will typically agree that index funds are a great way for investors to invest passively in the stock market. Not only do they require little input, but they also offer a low-cost option with a strongly diversified portfolio. Index funds also offer a good investment option for long-term investors.

However, it's important to remember that all investments come with risks, and individual financial situations can vary widely. Before making any investment decisions, it is highly recommended to consult a professional financial advisor who can assess your specific circumstances and provide tailored advice. Their expertise will help you make informed choices aligned with your financial goals and risk tolerance.

Freelancing is a popular career choice that has grown significantly in recent years due to the rise of the gig economy and the increasing availability of remote work opportunities. The freelance market is made up of self-employed individuals who work independently and provide their services to clients on a project-by-project basis.

This type of work provides a great deal of flexibility and control over one's own schedule, workload, and earning potential. However, like any career choice, freelancing has both ups and downs. Below we explore what a freelance career might look like, and provide tips on how to be your own boss and a successful freelancer.

What is the gig economy?

The gig economy is a labor market where temporary or flexible jobs are common, and independent workers work on a project or task basis rather than being employed by a company or traditional employer on a long-term basis.

This type of work is often conducted through digital platforms or apps that connect workers with clients who need their services. Freelance platforms include the likes of Upwork, Fiverr, and Freelancer.com for instance.

Gig economy jobs can range from driving for ride-hailing services to performing freelance writing or design work. The freelance business allows individuals to work when and where they want, providing them with a great deal of flexibility and control over their work schedules, essentially making them their own boss.

However, it also comes with challenges such as a lack of job security, no benefits or protections, and potential fluctuations in income. While freelance work sounds attractive, it’s important to consider the skill set needed and whether the ups outweigh the downs in relation to your specific needs and wants.

Being realistic about freelancing

The freelance business has gained a reputation for offering a very attractive lifestyle, but it still takes work and requires a number of skills and commitments that you, and you alone, will need to front.

Organization skills

For a successful freelancer, being organized and managing your time effectively is crucial. This means staying on top of your tax obligations, keeping your documents in order, and ensuring that you meet all deadlines.

Multitasking

In addition, multitasking is a necessary skill for most freelance workers, as you'll likely have to juggle multiple projects simultaneously. This requires effective task prioritization and the ability to switch between different topics seamlessly.

Strong communication

Good communication skills are also essential for success, as you'll need to handle difficult clients and know how to ask for guidance when needed. Effective communication is also crucial to a successful freelance career as you will likely need to take the initiative and approach potential clients for work. Promoting your skills and putting yourself out there also requires courage and self-confidence.

Self-discipline

Perhaps the most crucial for a freelancer freelancing in this day and age is self-discipline. No matter what line of work you pursue, you'll need to stay focused and avoid distractions while working independently, whether it's the temptation of a nap or a social interaction.

The freelance lifestyle may sound flexible, but in reality (more often than not) it is still a full-time job as you are essentially running your own business.

Handle criticism

Being able to handle constructive criticism is an important trait for freelancers, as you'll often need to accept and respond to feedback that isn't always positive. Remember, even talented freelancers producing high-quality work receive negative feedback.

Self-motivation

Being self-motivated is key when working as a freelancer, as you'll be responsible for managing your own work schedule and meeting deadlines without the guidance of a manager. If you prefer a more social work environment, freelancing may not be the best fit for you as it often involves working independently.

Financial resilience

Finally, new freelancers should be prepared to have a certain level of financial resilience as there can be uncertainty about when their next paycheck will arrive. When they start freelancing, quiet periods of contract work can be anxiety-inducing for some people.

The upside of freelancing

On the positive side, freelancing allows individuals to work from anywhere, giving them the flexibility and autonomy to balance work and personal life.

One of the primary advantages of freelancing is the ability to take control of your work schedule. You have the freedom to choose when and where you work, making it much easier to balance your professional and personal commitments.

Freelancers having the freedom to select their own projects means that they have a great deal of control over the type of work they do, far more than a regular job. You can choose to work on projects you enjoy and are passionate about, and have the ability to set your own rates and choose clients that align with their values.

Additionally, freelancers have the potential to earn more money than traditional full-time employees as they have the ability to work with multiple clients simultaneously and charge higher rates for their specialized skills.

Another benefit is that your earnings are directly related to your effort and the quality of your work, which gives you a real sense of achievement that you might not feel working in a traditional office environment.

When done right, freelancing can offer a great deal of professional and personal fulfillment. Before you start full-time freelancing, however, be sure to understand the bigger picture of what is required.

The downside of freelancing

One of the most significant challenges for many freelancers is that it can be financially unpredictable, as one's income can fluctuate from month to month, paired with a lack of job security. Additionally, there are no paid vacation days, sick leave, or other benefits that traditional employees enjoy.

As a freelancer, you'll need to ensure that you're always available to communicate with your clients, which can require a certain level of flexibility. On top of that, freelancers might also need to continuously search for new clients and projects on online marketplaces to maintain their income.

If you venture into the world of freelancing, it’s important to note that you will also be responsible for all administrative tasks, including accounting, invoicing, tax obligations, and chasing payments, which can be time-consuming and require a great deal of attention to detail.

Another issue is the isolation that can come with working independently, as freelancers often work from home or their local coffee shop and may not have the same social connections as traditional employees.

Overall, freelancing can be a rewarding career choice, but it requires a significant amount of self-discipline, motivation, and business acumen to be successful. It's important for individuals considering freelancing to weigh the benefits and drawbacks carefully before making the leap.

If you’re unsure whether freelancing is for you, consider slowly taking on one or two freelancing jobs while still working your traditional 9-5. This way you can test the waters with first-hand experience and see if this is something you would like to pursue full-time.

10 steps to kickstart your successful freelancer career

If you’ve decided to take on a slow transition or full-time shift to freelancing, we’ve put together these 10 steps for you to take in order to build up your portfolio. From finding work on freelancing websites to managing the workload and establishing pricing, here are the tools you’ll need to build your freelance business.

Step 1: Find your first job

Freelance work can be found through online freelancing platforms, which are a popular option for both freelancers and clients, with recent data showing that 75% of freelancers find work this way. Explore the various freelancing platforms and find which one best caters to your needs.

Step 2: Build a portfolio of freelance work

To create a successful freelance profile, it needs to make a strong impression and showcase your skills, experience, and personality to potential clients. Consider taking on smaller projects in the beginning that will display your skill set to gain experience. The more you can show, the more interest you can attract.

Knowing which freelance projects to take on and how to write a winning proposal can be crucial in securing steady work and building a reputation in the industry.

Step 3: Establish your pricing formula

One of the most common questions that freelancers have is how to price their work, as it can be challenging to balance fair compensation with the risk of losing clients to competitors.

There is a fine line between overcharging and scaring away potential business and selling yourself short. Use trial and error to figure out specifically where your skill set lies, and don’t be afraid to check out what other freelancers offering similar skills are charging.

Remember: Your work is valuable, and your expertise, experience, and dedication deserve to be rewarded.

Step 4: Discuss the job parameters with the client before beginning

Before starting work on a project, it's important to discuss and agree on details with the client, including deadlines, the scope of work, and payment terms. This step is vital and should never be skipped.

Be sure to understand what the client wants and effectively communicate your requirements before spending any time on the project you’ve just landed on.

Step 5: Manage client expectations

Freelancers need to manage client expectations and maintain a positive working relationship through effective communication and a clear contract. Always start on the right foot by being polite, assertive, and transparent.

Each client will be different so ensure that you navigate these relationships in a tailor-made manner. Ideally, you want to establish a strong client relationship and meet (or hopefully exceed) their expectations.

Step 6: Manage your time effectively

You’ve landed the job, now it's time to do the work. Time management is key to productivity and success as a freelancer. Ensure that you are scheduling work during productive hours, using time-tracking software if necessary, and effectively using your time to balance the workload of multiple projects.

Take the time to explore various tips and tricks for managing your time between projects, and build a winning formula that works specifically to your needs. The primary goal here is to maximize your productivity.

Step 7: Get paid

Getting paid as a freelancer can involve choosing the right payment options, dealing with fees and invoicing, and learning the best course of action for receiving international payments. Tap provides a winning formula that caters to both crypto and top fiat currency payments.

Unfortunately, this is also the time to learn how to address and handle non-payment issues.

Step 8: Manage your finances

Freelancers need to manage their finances carefully, as income can vary and benefits and tax obligations are the sole responsibility of the freelancer.

Be sure to stay up to date with policies like health and disability insurance, and learn about investing and passive income solutions for retirement and other savings goals.

Step 9: Level up your freelance career

As a freelancer, there are many opportunities to grow your career and income, such as becoming an agency with other people working under you or teaching others your skills and experience through online courses.

Step 10: If in doubt, start small

It's possible to balance freelancing with a day job, but it takes planning, determination, and persistence to make it work. This is also a great way to test the market and see if the freelancing life is for you.

How to navigate the freelance business as a newbie

Now that you have a clear understanding of what freelancing entails, and a to-do list of steps to take to pave your new career path, below are some tips for anyone starting out or looking to become a freelancer. These will come in handy as you navigate the space and ensure that you don’t sell yourself short.

Be selective about what jobs you take

To showcase your skills and present yourself as an expert, it's important to choose freelance projects that align with your skills and interests, rather than accepting every job that comes your way.

Establish a good pricing formula

Finding the right pricing balance can be tricky - charging too little can make you appear less experienced while overcharging can lead clients to seek out more affordable options. Researching market rates can help you find the right pricing balance.

Keep checking in with clients

Following up with clients after completing a project can lead to more work and strengthen your professional relationship. Consider suggesting additional projects that could benefit the client's business and make a note to check in again in a few months.

Always get a signed contract before starting

Before starting work on a project, always ensure you have a signed contract that outlines the obligations on both sides, including payment terms. Although it may feel awkward to request a contract, it can save time and hassle down the line.

Outsource administrative tasks if necessary

Administrative tasks such as invoicing, accounting, and tax management are important but can be time-consuming.

Consider delegating or automating these tasks to free up more time for paid work. Several millionaires interviewed in a study said that one of their keys to success was recognizing their weaknesses and delegating accordingly.

Structure your day

To manage your time effectively, create a routine that allows you to balance work and other commitments. Scheduling work during your most productive hours and avoiding leaving work until the last minute can help you maximize productivity.

Stay motivated

Freelancing can be challenging at the beginning, but it's important to persevere and not give up. With experience, you'll gain more confidence and find it easier to secure work and manage your business.

Best of luck with your new venture if you decide to start freelancing.

Kyber Network was launched in 2018 with the aim of being the main liquidity hub for the DeFi space. KyberSwap is the platform's interface, a decentralized exchange (DEX) aggregator that provides convenient and secure value exchange within the crypto market. Overall, the Kyber Network platform provides a smooth token-swapping experience while boosting earnings for liquidity providers.

What is Kyber Network (KNC)?

Kyber Network is a decentralized multi-chain liquidity hub that provides instant, secure transactions on any decentralized application (dapp). Its main goal is to provide deep liquidity pools that offer the best rates for DeFi dapps, decentralized exchanges (DEXs), and other users. Kyber Network is built on the Ethereum blockchain and makes use of intricate smart contracts.

KyberSwap is its flagship DEX aggregator and liquidity platform. KyberSwap sources liquidity from multiple DEXes to provide the best swap rates for traders in DeFi. KyberSwap is decentralized and permissionless, allowing users to conduct transactions on any of its supported 12 chains, including Ethereum and Binance Smart Chain.

Kyber Network seeks to solve the liquidity issue in the DeFi industry by allowing developers to build products and services using the platform's protocol, while KyberSwap acts as the trustless trading platform that also provides rewards for liquidity providers. With over $1 billion in total volume from over 1 million user transactions, Kyber Network is a growing player in the DeFi space.

Kyber Network's governance structure is managed by holders of its native Kyber Network Crystals (KNC) token through a decentralized autonomous organization (DAO) called KyberDAO. This allows KNC token holders to have a say in the network's decision-making processes and contribute to its development and growth.

Who created Kyber Network?

Kyber Network was founded by Loi Luu, Victor Tran, and Yaron Velner in 2017. The project created 226 million KNC tokens, most of which were sold to buyers and investors during its initial coin offering. This raised Kyber Network 200,000 ETH (roughly $50 million at the time) to launch the platform. The protocol went live on the Ethereum blockchain in February 2018, with Vitalik Buterin as an advisor.

In October 2017, the Kyber Network burned over 10 million KNC tokens, bringing the maximum supply down to roughly 215 million KNC.

Victor Tran is the current CEO of Kyber Network, while Loi Luu is the current Chairman. Yaron Velner stepped down as CTO in October 2019 but remains as an advisor. The Kyber team has over 50 employees globally, and its headquarters is in Singapore, with a large presence in Vietnam.

How does Kyber Network work?

Kyber Network is a decentralized protocol that enables users to instantly trade tokens without intermediaries. KyberSwap is the user interface for Kyber Network, with two protocols: Classic and Elastic.

Classic features the Dynamic Market Maker (DMM) protocol and the Amplification (AMP) programmable price curve. Elastic is a tick-based AMM (automated market maker) with concentrated liquidity, allowing liquidity providers to specify the price range for adding liquidity and earn fees for swaps processed at a specific price.

KyberSwap also has features like the Reinvestment Curve, multiple fee tiers, JIT Protection, and liquidity mining farms. The Kyber Network aggregates liquidity from various sources into a single liquidity pool on its network, and anyone can provide liquidity. The protocol is integrated into dApps (decentralized applications), DeFi (decentralized finance) platforms, and crypto wallets, enabling users to utilize any Kyber Network-supported token and allowing platforms to receive payment in their preferred token.

The Kyber Network protocol relies on reserves to provide liquidity for its decentralized exchange platform, KyberSwap. When a user initiates a trade, the platform searches for available reserves to find the best available rate being offered by takers.

There are three main types of reserves: Price Feed Reserves (PFR), Automated Price Reserves (APR), and Bridge Reserves. PFRs use price feeds to calculate conversion rates using smart contracts acting as an alternative to market makers, APRs provide rates for available crypto assets through smart contracts, and Bridge Reserves access other decentralized exchanges to deepen liquidity.

Previously, reserves were required to participate in the Kyber protocol by staking KNC to pay for network fees, but a recent upgrade removed this requirement, making it easier for reserves to participate. Kyber Network collects fees in ETH, with a portion of them going to reserves based on the amount of liquidity they provide.

The reserves model is a critical component of KyberSwap, enabling the platform to offer fast and competitive token trading services to its users.

What is the Kyber Network Crystal (KNC) token?

Kyber Network Crystal (KNC) is the native coin for the platform and acts as both a utility and governance token. Users can stake it to vote on upgrades and policies or delegate their tokens to other validators and earn a portion of the block reward.

Users who stake KNC receive rewards in ETH, and network fees paid in KNC will be burned over time, gradually reducing its supply. KNC holders can participate in the DAO and governance proposals by staking their assets or delegating their vote.

They can also earn liquidity-mining rewards by staking their tokens in eligible Rainmaker farming pools or participating in various activities such as Trading Contest, Gleam Giveaway, and AMAs.

How can I buy KNC tokens?

Tap's mobile app offers a user-friendly platform for users to purchase, trade, and safely store Kyber Network's KNC token in an integrated wallet. The app supports a variety of cryptocurrencies and fiat currencies, which can be used for buying and selling KNC tokens. The app also makes use of a smart router which finds the best Kyber Network price at any given time.

Additionally, users can securely store not only KNC tokens but also other digital assets on the app. Downloading the Tap mobile app provides users with access to verified cryptocurrencies and fiat wallets, allowing them to take advantage of a wide range of investment opportunities.

Investing is a great way to grow your wealth and reach financial goals, but it is important to understand the potential risks as well as the rewards. Knowing how to identify capital gains and losses in investments is essential for any investor who wants to make informed decisions about their money.

Gains and losses will determine whether or not an investment has been successful, so understanding them is critical to making wise choices when investing. Not only that but being able to recognize capital gains and losses can help investors decide when it’s time to get out of an investment before they incur too much damage.

By learning to spot a gain or loss quickly, investors can protect their funds from unnecessary harm while reaping the benefits of investing. Here we break down how to calculate capital gains and losses.

The basics: how to calculate capital gains/loss

Investors will need to first identify the original cost or purchase price of the investment in order to calculate the percentage capital gain on an investment. You can get this from your broker, or any electronic trade confirmations you might have received.

The next step is to subtract the original cost of the same investment from the selling purchase price (current value) to arrive at the gain or loss amount. If the amount is negative, this will indicate a loss while a positive amount will illustrate the profit.

Then take this amount (the gain or loss) and divide it by the original purchase price. Multiply this by 100 and this will establish your gain or loss as a percentage.

Gain/loss ($ amount) = selling price - purchase price

Gain/loss percentage = [(selling price- purchase price) / purchase price] x 100

When the market value of an investment is lower than its cost basis, leading to a negative percentage return, it constitutes a loss on that particular asset.

When the market value or selling price surpasses your initial investment, you'll get a positive percentage that reflects this gain.

Why calculating gain/loss is important

Calculating the loss or gains you've made on an investment is crucial not only for staying on top of your financial situation but also when it comes to monitoring your investment strategy. If you are continuously making losses on an investment it might be time to change course, however, you will only know this by doing the calculations.

Calculating the capital gains or losses on an investment as a percentage is important because it shows how much was earned as compared to the amount needed to achieve the gain.

Additionally, calculating the gains or losses of an investment are important when calculating any capital gains tax. Having a clear understanding of the financial situation will ensure that you are not underpaying or overpaying on capital gains tax. Be sure to check the capital gains tax rate in your jurisdiction as this will change from area to area.

Additional aspects to consider

As with anything, there are additional costs to factor in. For investments, this might be commissions, broker fees, taxes, etc. Below we look at how to factor in transaction costs, dividends, and trading fees.

Transaction Costs

Take your final gain/loss amount and subtract and transaction costs incurred from this amount.

Gain/loss ($ amount) = (purchase price - selling price) - transaction costs

Dividends

When calculating your gains, any additional income or distributions should be factored in. Dividends, whether from specific stocks or mutual funds, are the most common form of investment income and are paid to investors on a per-share basis. Not all shares pay out dividends so be sure to confirm this prior to making the trade.

Say an investor owns 100 shares and the company pays out $5 per share annually, this equates to $500 in dividends in a single year. Let's say that each share was bought at $20 and is now worth $40.

Gain/loss percentage

= [((selling price - purchase price) + dividends) / purchase price] x 100

= [(($4,000 - $2,000) + $500) / $200] x 100

= 125%

Therefore, the dividends payout increased the gains on this investment by 25%. In this example, we have not included trading fees, commissions, etc.

Trading fees

Trading fees or brokerage fees are often an unavoidable aspect of trading and should be factored into your investment calculations. Using the above example, let's say the broker charges $50 in fees for its services and any transaction costs incurred. This amount will need to be subtracted from the original gain/loss amount before dividing it by the original purchase cost.

Gain/loss percentage

= [((selling price- purchase price) - fees) / purchase price] x 100

= [(($4,000 - $2,000) - $50) / $2,000] x 100

= 97.5%

Here the trading fees dropped the investment gains by 2.5% from 100% to 97.5%.

Capital gains tax rate and mutual funds

Calculating capital gains or losses in a mutual fund is important for several reasons, but one key example is for tax purposes, known as capital gains taxes.

When an investor sells shares of a mutual fund, they may realize a capital gain or loss, which is the difference between the sale price and the purchase price of the shares. If the sale price is higher than the purchase price, the investor realizes a capital gain, and if the sale price is lower than the purchase price, the investor realizes a capital loss.

Capital gains are typically taxable, meaning that the investor must pay capital gains tax on the amount of the gain. However, if the shares were held for more than one year before being sold, the gain may be taxed at a lower rate known as the long-term capital gains rate, depending on the specific tax laws in your country. In contrast, capital losses can be used to offset capital gains, reducing the investor's overall tax liability.

Calculating capital gains or losses in a mutual fund can be more complex than for individual stocks, as mutual funds may buy and sell securities frequently, resulting in multiple tax lots with different purchase prices and holding periods. To accurately calculate gains or losses, investors must track each tax lot and determine the cost basis of each lot, which is the original purchase price plus any reinvested dividends or capital gains distributions.

Failing to properly calculate capital gains or losses on one's investments can result in overpaying or underpaying taxes, which can be costly and potentially lead to penalties. Therefore, it is important for investors to carefully track their mutual fund investments and accurately calculate their capital gains or losses for tax purposes.