That fleeting Altcoin frenzy probably isn't what you think it was. The next crypto rally won't be like the ones you remember, it's a whole new thing.

Keep reading

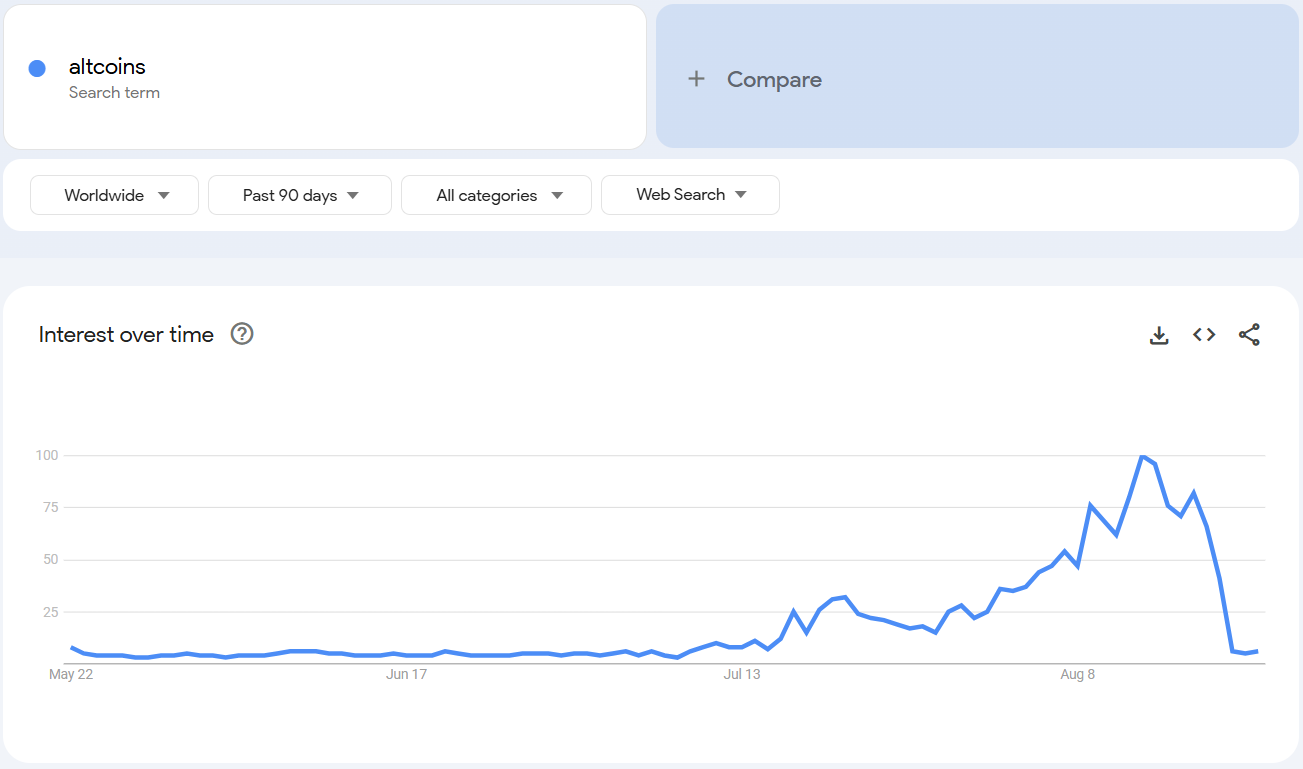

For a fleeting moment, it looked like altcoin season was finally here. Google searches for “altcoins” skyrocketed to record highs, 𝕏 was buzzing, and retail excitement seemed to return in full force. But within a week, that hype fizzled out almost as quickly as it appeared, leaving traders wondering if the long-awaited alt season was just a mirage.

A Spike That Vanished Overnight

Search interest for “altcoin” on Google Trends hit its highest score ever in early August, only to fall back to baseline levels within days. Globally, the same pattern played out, with scores dropping from 100 to just 16 in a week, mimicking a “pump and dump” pattern that you would expect from a memecoin.

Market cap data told the same story. The total value of altcoins (excluding Bitcoin and Ethereum) briefly climbed by $100 billion before giving it all back, leaving investors wondering whether the hype had any real weight behind it.

Naturally, some saw the collapse as proof that the altcoin season had ended before it really began. Others, however, like analyst Cyclop, argue the spike shows something deeper: that “altcoin” has become the mainstream term retail uses today, replacing “crypto” in 2021. In his view, this isn’t the peak. Rather, it’s just the beginning of broader interest.

Why Google Trends Doesn’t Tell the Whole Story

Relying on Google searches to measure retail demand may no longer work the way it used to. With AI tools increasingly replacing traditional search, and with concepts like “altcoins” now part of everyday investor vocabulary, Trends data might not be capturing where and how money is really flowing.

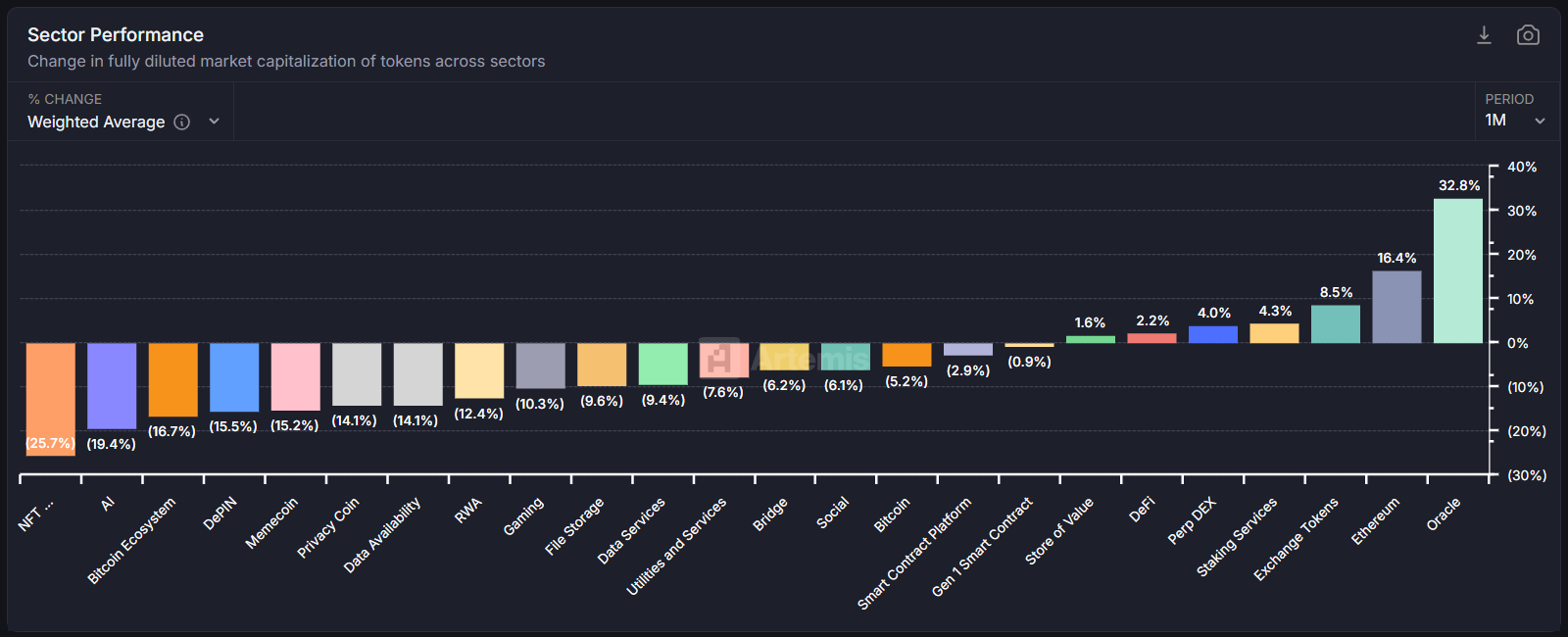

Instead, analysts point to on-chain and trading activity as better indicators of where momentum is building. And in August, that momentum was fragmented.

A Season of Winners and Losers

Data from Artemis showed only a few categories outperforming last month: Ethereum, exchange tokens, and oracles.

Beyond these bright spots, however, most altcoins struggled. The result? A patchwork “mini season” rather than the explosive, across-the-board surge that retail and social media had been hoping for.

Polygon’s co-founder Sandeep put it bluntly: "Retail is searching, but institutions aren't buying the narratives yet. Old altcoin seasons were driven by speculation and promises and narratives and marketing. Institutional money is smarter money. It cares about real utility and cash flows. The next "alt season" won't look like 2017 or 2021. It’ll be fewer tokens with actual usage, not just tokens with better marketing." Sandeep said.

The Road Ahead

That doesn’t mean altcoin season is dead, it probably just means it’s evolving.Coinbase has suggested that the next true wave could arrive as early as September, but that it likely won’t be a full-scale altcoin season.

Bottom line? The altcoin season isn’t gone; it’s just different. It’s maturing. And the next leg up may not belong to every token in the market, but only to the select few proving they can deliver value beyond mere speculation.

NEWS AND UPDATES

LATEST ARTICLE

It's no secret that trading any financial market is hard work. Traders need to keep calm, level-headed, and observant at all times while staying on top of the market's ever-changing movements.

While making mistakes is part of the game, we've outlined 5 of the biggest common mistakes you can avoid while you navigate the often turbulent waters of any trading system and technical analysis.

What is technical analysis?

Technical analysis (TA) is one of the most popular methods for analyzing financial markets. At its core, it uses previous price action and volume data to predict future market behavior by identifying trends and favorable trading opportunities.

It can be applied to the chart patterns of any kind of market, including stocks, forex, commodities, and cryptocurrencies. While the basics are not too difficult to understand it takes a lot of practice to become an expert technical analyst.

This form of analysis typically looks at historical price action, while fundamental analysis (FA) looks at multiple factors affecting the price of an asset.

5 common mistakes made when it comes to using technical analysis

- Know when to cut your losses

No matter how big or small, always prioritize protecting your investment. In the world of trading and investing, this is non-negotiable if you want to see any returns. A great way to approach trading is to start out with the following mindset: you're not here to win, you're here not to lose.

Start with small positions, set up a stop-loss, and know when to cut your losses.

2. Don't ignore extreme market conditions

While the markets are typically governed by supply and demand, there are cases where extreme conditions like black swan events can throw your carefully curated technical analysis to the curb. Sometimes emotion and mass psychology can cause periods of extreme market conditions, and you will need to adjust your trading strategy accordingly.

If you make decisions based solely on readings from technical tools, you run the risk of losing money, especially during black swan events when it can be tough to understand what's happening. Keep in mind that market conditions can change rapidly and without warning, so it's always important to consider other factors before making any decisions and risking real funds.

3. Avoid revenge trading

Revenge trading is a term used to describe when a trader tries to immediately recover a significant loss through making alternative trades. Infringing the golden rule of not making trades based off emotions, revenge trading is a no-no.

Harness your inner zen and attempt to stay calm through both big and small mishaps. Sticking to your trading plan will be the best thing you can do, and make adjustments as need be based off of logical thinking and an analytical approach.

Immediate trading after a severe loss often leads to more losses. Therefore, some traders take a break from trading altogether for a while after they lose big. By taking this breather, they can come back with fresh mindsets and restart their trading journey.

4. Remind yourself (constantly) that TA is a game of probabilities

Technical analysis is all about probabilities and not absolutes. This means that no matter what technical approach you’re using, there’s never a 100% guarantee that the market will behave as you expect. Even if your analysis suggests that there’s a very high probability of the market moving up or down, it's still not set in stone.

As you're getting your trading strategies together, there's one aspect you always need to keep in mind: don't think the market will go how your analysis predicts. This is a mistake even experienced traders make, and it leads to bad decisions like betting too much money on one outcome instead of spreading it out. That puts you at risk of losing a lot financially if things don't go your way.

5. Don't blindly follow anyone's trading strategies

A great way to learn how to trade the financial markets is by observing experienced technical analysts and traders. However, in order to master your own skills you will need to establish what your own strengths are and how to leverage them.

Observing other traders doesn't present a fool-proof trading strategy as something that works for one trader might not work for another. With countless ways to make money off of the markets, find your own trading style that is best suited to you.

Initially, you might get lucky by making trades based off of another person's opinion. However, if you continue down this road without comprehending why they made that choice, it will only lead to detrimental consequences in the future.

Learning from others is key, but it is more important that you think for yourself and agree with the trade before moving forward. Do not let anyone else make decisions for you blindly, no matter their experience level.

In conclusion

While trading isn't easy and there is certainly no quick fix to success, the above are some helpful starting points to consider when entering the world of technical analysis.

Remember that it takes practice, and while approaching trading with a longer-term mindset is a great way to start, ideally, you want to build habits that allow you to be in control of your trading decisions and avoid common mistakes.

Constantly manage your risks and learn from your mistakes when you make them in order to capitalize on your strengths and improve. This advice serves both professional traders and newbies.

.svg)

One of the largest and oldest dapps in the DeFi (decentralized finance) space, Compound Finance has built a reliable reputation among traders looking for lending and borrowing services. Compound operates using its native ERC-20 COMP tokens which provide community governance as well as other services.

What is the Compound protocol (COMP)?

Built on the Ethereum blockchain, the Compound protocol provides liquid money markets offering services such as lending and borrowing. Supporting a number of crypto assets, the Compound protocol allows users to deposit crypto into lending pools providing capital for borrowers on the network and allowing them to earn interest in return.

After depositing funds into the lending pool, lenders are issued "cTokens" (cETH, cDAI, cBAT) which represent the deposit made. These tokens can then be traded or transferred within the platform, or redeemed for the original cryptocurrency deposited. This process is conducted by smart contracts and operates entirely automatically with interest rates algorithmically assigned based on the activity in its liquidity pools.

The Compound protocol also uses the ERC-20 native COMP token which is distributed to traders that utilize the Compound market, i.e. borrowing, withdrawing or repaying the asset. COMP tokens are distributed each time an Ethereum block is mined proportional to the interest collected from each asset. The COMP cryptocurrency grants COMP token holders governance and voting rights.

Following notable investments from the likes of consulting firm Bain Capital Ventures, Andreessen Horowitz, and Polychain, the platform has grown and established a strong reputation within the decentralized finance space and the greater crypto world.

The history of Compound and who created it

Compound was founded in 2017 by Robert Leshner and Geoffrey Hayes, who both previously held high-profile jobs at PostMates, an online food delivery service. Leshner holds the CEO position while Hayes remains the CTO at Compound Labs, Inc, the software development firm behind the Compound protocol. Compound Labs is an open-source software development firm creating cutting-edge tools, products, and services for the innovative DeFi ecosystem.

In 2018, the platform raised $8.2 million from notable venture capital firms Bain Capital Ventures and Andreessen Horowitz. A year later, Compound raised an additional $25 million from many of the same investors along with new ones including Paradigm Capital.

How does Compound work?

The Compound protocol leverages the power of Ethereum smart contracts and cryptocurrency incentives to benefit lenders and borrowers. Lend and borrow services make up the two main use cases for the platform, as outlined below.

Interest rates on Compound are dynamically managed based on the supply and demand of particular crypto assets within the coin pools. The higher the liquidity, the lower the interest rate. Prices are determined by using the Open Price Feed based on Chainlink's oracles which collect the data from numerous exchanges.

In order to use the Compound DeFi protocol to engage in lending or borrowing services, you will need to connect one of the supported crypto wallets. Currently, the app supports MetaMask, Ledger, WalletConnect, and Tally Ho. The interface has been designed to be user-friendly and easy to navigate, perfect for traders new to the space as well as seasoned DeFi participants.

Lending/supplying

The process of lending on the Compound platform is called supplying. Lenders are able to earn interest on their cryptocurrency by depositing cryptocurrencies into the Compound platform. Borrowers are also required to deposit digital assets into the protocol, which can earn interest but cannot be withdrawn for the duration of the borrowing period.

The platform currently supports roughly 20 crypto assets, from Basic Attention Token (BAT) to Wrapped Bitcoin (WBTC), with Ethereum (ETH) and a number of stablecoins (DAI, USDC, and USDT) being the most actively used.

Once users lend assets to the platform, they are issued with ERC-20-based cTokens corresponding to the cryptocurrency deposited (i.e. cETH, cDAI, etc.). These tokens confirm the liquidity providers' deposits and offer a number of other incentives.

Borrowing

After depositing a particular cryptocurrency into the decentralized finance protocol, users are assigned a "borrowing capacity". This is a limit set in USD based on the rate of the crypto asset which is determined by the Open Price Feed. When depositing multiple cryptocurrencies, the borrowing capacity will factor this in.

Users can also borrow cryptocurrencies supported by the protocol based on a coin's collateral ratio. For instance, if DAI has a collateral ratio of 70%, users can borrow DAI up to 70% of the total amount deposited. Typically, collateral ratios are between 60% and 85%.

Similar to the lending process, when borrowing cryptocurrency borrowers are issued cTokens. So when borrowing DAI for instance, borrowers will be issued cDAI tokens, with the interest payable based on these tokens as well.

Withdrawing

After paying back the borrowed debt, users can redeem their deposited funds. Without having to deal with other traders, the protocol seamlessly utilizes a dynamically maintained set of liquidity pools. The platform also does not charge any withdrawal penalties or hold users to minimum investment times.

When users redeem their funds, the cTokens issued are added to the accumulated interest and converted back to the originally deposited cryptocurrency. These funds can then be withdrawn into the connected wallet.

Account Health

The Compound platform uses a system called "account health" to establish whether accounts are in risk of liquidation. This system measures the sum of the deposited funds against the total amount borrowed. If a user's account health falls dangerously low, the account could be liquidated, and some of the collateral forfeited.

This process is managed in a decentralized way where platform users act as liquidators and monitor for risky accounts. Should they liquidate an account they earn a portion of the liquidated funds.

What is the COMP token?

The COMP token is the Compound platform's native token which mainly serves as a governance token, with a built-in incentive for users holding the token. Holders of COMP tokens are able to vote on all important decisions pertaining to the protocol, including interest rates. Much like the cTokens, COMP tokens are based on Ethereum’s ERC-20 token standard.

Compound tokens have a total supply of 10,000,000 tokens, of which over 70% of Compound coins are in circulation (at the time of writing).

How can I buy COMP tokens?

With Tap's mobile app, users can easily acquire COMP tokens and store them in the integrated wallet with confidence, either to hold long-term, sell, trade or use on other DeFi platforms. Not only does Tap provide an effortless way of trading digital assets, but also a safe space to keep your investments secure over long periods of time.

In order to access the mobile app users will need to download the app and create an account. After a quick verification process, users have access to a wide range of vetted cryptocurrencies as well as fiat wallets where funds can be safely stored or used in the real world. Whether you're looking to buy Compound or sell Compound coins, Tap provides a seamless solution to your crypto needs.

We are delighted to announce the listing and support of Compound (COMP) on Tap!

COMP is now available for trading on the Tap mobile app. You can now Buy, Sell, Trade or hold COMP for any of the other asset supported on the platform without any pair boundaries. Tap is pair agnostic, meaning you can trade any asset for any other asset without having to worries if a "trading pair" is available.

We believe supporting COMP will provide value to our users. We are looking forward to continue supporting new crypto projects with the aim of providing access to financial power and freedom for all.

Built on the Ethereum blockchain, the Compound protocol provides liquid money markets offering services such as lending and borrowing. Supporting a number of crypto assets, the Compound protocol allows users to deposit crypto into lending pools providing capital for borrowers on the network and allowing them to earn interest in return.

The COMP token is the Compound platform's native token which mainly serves as a governance token, with a built-in incentive for users holding the token. Holders of COMP tokens are able to vote on all important decisions pertaining to the protocol, including interest rates. Much like the cTokens, COMP tokens are based on Ethereum’s ERC-20 token standard.

Get to know more about Compound (COMP) in our dedicated article here.

The process of investing involves putting your money or capital into something with the aim of earning more money and making a profit. Investment strategies are sets of principles, rules, and approaches that an investor follows to manage their investment portfolio. A sound investment strategy can help an investor achieve their financial goals, manage risk, and maximize returns.

In this article, we will provide a beginner's guide to investment strategies, including its definition, benefits, types, and key principles. We will also discuss various investment terms and jargon that a new investor should know.

What are investment strategies?

Investment strategies are plans of action that an investor follows to manage their investment portfolio. It involves selecting investments that align with their financial goals, risk tolerance, and time horizon. Good investment strategies takes into account market conditions, diversification, and risk management techniques.

The primary goal of investment strategies is to help investors maximize their returns while minimizing potential losses. These strategies can be created by the investor themselves or by a financial advisor and used across varying markets, from the stock market to the crypto market.

The benefits of having an investment strategy

Having an investment strategy can help you achieve various financial goals, whether they be generating income, building wealth, or funding retirement. It also helps you manage risk, reduce potential losses, and maximize returns. Strong investment strategies consider each investor's specific investment objectives, time horizon, risk tolerance, and market conditions.

Various types of investment strategies

There are several types of investment strategies that investors can implement during the investing process depending on their unique circumstances (risk tolerance, capital, financial goals, etc.). From value investing to income investing, we cover the most popular investment strategies below.

Value investing

Value investing is a strategy that involves buying stocks that are undervalued compared to their intrinsic value. This approach seeks to identify companies that are trading on the stock market at a discount price and have strong fundamentals.

Growth investing

The growth investment strategy is one of the best investment strategies as it focuses on investing in companies with high growth potential, even if they are currently trading at a premium. This growth investing strategy is designed around identifying companies with strong earnings growth, innovative products, or dominant market positions. Growth stocks will typically encompass both mature and emerging companies.

Income investing

The income investing strategy focuses on generating regular income from investments, such as dividend stocks, bonds, or real estate investment trusts (REITs). Here the aim is to provide a steady stream of income for investors, especially those who are retired or seeking passive income.

Index investing

Index investing is also one of the more common investment strategies that seeks to replicate the performance of a particular market index, such as the S&P 500 or the NASDAQ. This approach offers investors broad exposure to the market at a low cost.

Momentum investing

Momentum investing is a strategy that involves buying stocks that have shown strong performance in the past and continue to outperform the market. The aim here is to capitalize on the trend of rising prices and momentum in the market.

Contrarian investing

Contrarian investing is a stock market focused strategy that involves buying stocks that are out of favor with the market or have fallen out of favor. This strategy centers around identifying companies that are undervalued by the market and have the potential for a turnaround.

Active investing

Active investing is a strategy that involves actively managing a portfolio, often through the frequent buying and selling of assets. This strategy generates higher returns than passive investing but requires more time, research, and expertise.

The key principles of investment strategies

Regardless of which of the different investment strategies one chooses, here are some key principles that every investor should follow.

Set investment goals

Before you start investing, you should have clear investment goals and a plan to achieve them. Your investment goals should be specific, measurable, achievable, relevant, and time-bound.

Diversify your portfolio

Diversification is the process of spreading your investments across different asset classes, sectors, and regions. Diversification helps reduce risk by minimizing the impact of any single investment or market event on your portfolio.

Manage risk

Remember that all investments carry some level of risk, and it is important to manage risk to avoid potential losses. You should assess your risk tolerance and invest accordingly. You can also use risk management techniques, such as stop-loss orders, to limit your potential losses.

The long-term investment strategy

Investing is a long-term game, and you should be patient and disciplined in your investment approach. Playing the long game and investing in long term investments is more likely to deliver financial independence.

Control your emotions

Emotions can cloud your judgment and lead to irrational investment decisions. It is important to control your emotions and stick to your investment strategy, even during market downturns or volatility.

Focus on fundamentals

When selecting investments, it is crucial to focus on the fundamentals of the underlying companies or assets. This includes factors such as revenue growth, earnings, valuation, and competitive advantage.

Stay informed

The investment landscape is constantly changing so ensure that you stay informed about market trends, economic indicators, and company news. This can help you make more informed investment decisions and adjust your strategy as needed.

Investment terms that every investor should know

As a new investor, you may encounter various investment terms and jargon that can be confusing. Here are some of the most common investment terms and their definitions:

Stock: A stock represents ownership in a company and gives the holder a claim on a portion of its assets and earnings.

Bond: A bond is a debt security that represents a loan made by an investor to a borrower, typically a corporation or government.

Mutual funds: mutual funds are a type of investment vehicle that pools money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets.

ETF: An ETF, or exchange-traded funds, tracks a particular market index and can be bought and sold on an exchange like a stock.

Asset allocation: Asset allocation is the process of dividing your portfolio among different asset classes, such as stocks, bonds, and cash, to achieve your investment goals and manage risk.

Market capitalization: Market capitalization refers to the total value of a company's outstanding shares of stock, calculated by multiplying the number of shares by the current market price.

Dividend: A dividend is a distribution of a portion of a company's earnings to its shareholders, typically paid out in cash or additional shares of stock.

Expense ratio: The expense ratio is the annual fee charged by a mutual fund or ETF to cover its operating expenses, expressed as a percentage of the fund's assets.

P/E ratio: The price-to-earnings ratio compares a company's current stock price to its earnings per share, indicating how much investors are willing to pay for each dollar of earnings.

Yield: Yield refers to the income generated by an investment, typically expressed as a percentage of its price or face value.

Market order: A market order is an instruction to buy or sell a security at the current market price, regardless of the price level.

Limit order: A limit order is an instruction to buy or sell a security at a specific price level or better.

Stop-loss order: A stop-loss order is an instruction to sell a security if its price falls below a specified level, designed to limit potential losses.

Bull market: A bull market is a period of rising stock prices and optimistic investor sentiment.

Bear market: A bear market is a period of declining stock prices and pessimistic investor sentiment.

Conclusion

Investing can be a complex and challenging endeavor, especially for those new to it. While understanding the different types of investment strategies, key principles, and terms is important, it can be extremely beneficial to consult a qualified financial advisor. An experienced financial advisor can provide personalized guidance to help you build an investment strategy tailored to your specific financial goals, risk tolerance, and life situation.

They can offer professional expertise in areas like asset allocation, portfolio diversification, tax optimization, and risk management. Working with a financial advisor takes the guesswork out of investing and can increase your chances of achieving your long-term financial objectives. Remember, investing is a journey, and having the right professional partner can make a significant difference in navigating that path successfully.

IBAN-nummer (International Bank Account Numbers) infördes av Europeiska centralbanken för att förenkla internationella betalningar. Idag används systemet över hela världen och har blivit en självklar del av det moderna banksystemet.

I den här guiden går vi igenom vad ett IBAN-nummer är, hur det ser ut, skillnaden mellan IBAN och SWIFT-koder – och hur du hittar ditt eget IBAN.

Vad är ett IBAN-nummer?

IBAN står för International Bank Account Number och är ett unikt kontonummer som används för att identifiera bankkonton vid internationella överföringar. IBAN fungerar som ett slags kontrollsystem som säkerställer att uppgifterna stämmer innan pengarna skickas mellan banker i olika länder.

Systemet skapades för att standardisera internationella betalningar, minska fel och öka säkerheten – och har varit särskilt effektivt inom EU. Sedan IBAN infördes har felfrekvensen vid internationella överföringar minskat till så lite som 0,1 %.

Hur ser ett IBAN-nummer ut?

Ett IBAN-nummer är en alfanumerisk kod på upp till 34 tecken. Det är inte samma sak som ditt vanliga kontonummer – IBAN innehåller flera delar:

- Ett landskod på två bokstäver

- Två kontrollsiffror

- Bankens identifieringskod

- Ett nationellt kontonummer (kallas BBAN – Basic Bank Account Number)

Exempel på ett brittiskt IBAN:

GB28VBCD12345612345678

Här betyder:

- GB = land (Storbritannien)

- 28 = kontrollsiffror

- VBCD = bankkod

- 123456 = clearingnummer

- 12345678 = kontonummer

Observera att formatet varierar beroende på land.

Skillnaden mellan IBAN och SWIFT-koder

Du kanske undrar: vad är skillnaden mellan en IBAN-kod och en SWIFT-kod?

- SWIFT-kod (även kallad BIC): Identifierar den specifika banken eller finansinstitutet. En SWIFT-kod består av 8 eller 11 tecken och innehåller information om bankens namn, plats och land.

- IBAN-nummer: Identifierar det specifika kontot i det aktuella landet och används vid internationella överföringar. Det innehåller landkod, kontrollsiffror och BBAN.

I korthet: SWIFT berättar vilken bank, IBAN berättar vilket konto. Ofta används båda i kombination för att säkerställa att pengarna hamnar rätt.

Hur hittar man sitt IBAN-nummer?

Du kan hitta ditt IBAN-nummer på flera sätt. Här är några enkla metoder att börja med:

1. Kontrollera ditt kontoutdrag

IBAN brukar finnas angivet på ditt kontoutdrag, både digitalt och i pappersform.

2. Logga in på internetbanken

Gå in i din bankapp eller på internetbanken. Under dina kontouppgifter hittar du ofta både IBAN och SWIFT-kod.

3. Kontakta banken

Om du inte hittar numret digitalt eller på utdraget – ring eller mejla din bank. De kan ge dig numret om du uppger kontonummer och legitimerar dig.

Tänk på att inte alla länder använder IBAN-systemet. Om du skickar eller tar emot pengar från ett land utanför IBAN-zonen kan det krävas andra typer av kontouppgifter.

IBAN-nummer kan dessutom skilja sig i både längd och format beroende på land och bank – så dubbelkolla alltid att du har rätt uppgifter innan du skickar pengar.

Tap och IBAN för företagskonton

När du öppnar ett företagskonto i Tap-appen får du automatiskt tillgång till ett eget IBAN-nummer. Det gör det enkelt att ta emot internationella betalningar och sköta affärer globalt.

Tap-kontot stödjer flera valutor och är utformat för att passa olika branscher och tjänster – från frilansare till växande företag.

.svg)

PAX Gold (PAXG) är en banbrytande lösning som förenar det bästa av två världar: blockkedjebaserad handel och värdet av fysiskt guld. Den här kryptovalutan ger tillgång till äkta guldtillgångar – utan behovet av att själv hantera, förvara eller transportera guldet.

Vad är PAX Gold?

PAX Gold är den största digitala tillgången som backas av fysiskt guld. Varje PAXG-token motsvarar en troy ounce (ca 31,1 g) av ett 400-ounce London Good Delivery-guldtacka.

Priset på PAXG följer det aktuella guldpriset, vilket gör den till en mer stabil kryptotillgång än många andra alternativ på marknaden.

Tokenen ges ut av Paxos Trust Company, och alla PAXG-tokens är fullt täckta av fysiskt guld som förvaras i säkra valv – ungefär som hur stablecoins backas av fiatvaluta.

För att säkerställa transparens genomför Paxos regelbundna månadsaudits som visar att varje token motsvarar en verklig guldreserv. Tillsynen sker under övervakning av New York State Department of Financial Services.

Användare har också möjlighet att växla sina tokens mot riktiga guldtackor, eller för mindre kvantiteter, via ett globalt nätverk av guldåterförsäljare.

Vem ligger bakom PAX Gold?

Paxos Trust Company grundades 2012 av Charles Cascarilla och Rich Teo, med målet att skapa säkrare och mer tillgängliga sätt att hantera tillgångar.

Cascarilla har bakgrund inom finans och kapitalförvaltning, och har varit aktiv i både traditionella och blockkedjebaserade investeringsprojekt.

År 2018 lanserade bolaget Paxos Standard (PAX), en stablecoin knuten till den amerikanska dollarn. Den omprofilerades 2021 till Pax Dollar (USDP).

PAX Gold lanserades 2019 som ett digitalt guld – reserverna hålls i valv säkrade av Brinks, och oberoende revisorer granskar månatligen att reserverna motsvarar antalet tokens i omlopp.

Paxos har fått stöd från flera stora investerare, däribland PayPal Ventures, Oak HC/FT och Mithril Partners.

Hur fungerar PAX Gold?

PAXG är en ERC-20-token byggd på Ethereum-nätverket, vilket gör den kompatibel med många decentraliserade appar och plattformar inom DeFi.

Varje token motsvarar en troy ounce av fysiskt guld, och varje enhet är kopplad till ett specifikt guldtacka med unikt serienummer – som användare kan spåra via ett lookup-verktyg från Paxos.

Tokenen kan växlas till:

- Fysiskt guld

- Fiatvalutor

- Andra kryptovalutor

För att skapa eller lösa in PAXG tas en liten avgift ut (0,02 %), utöver de vanliga nätverksavgifterna (gas fees) för Ethereum-transaktioner.

Tack vare att PAXG är delbar med upp till 18 decimaler blir det möjligt för användare att äga en bråkdel av en guldtacka – utan att hantera det fysiska guldet.

Säkerheten tas på allvar: Paxos använder avancerade verktyg för att övervaka transaktioner och motverka bedrägeri och penningtvätt. Kodbasen granskas också löpande via smart contract-audits.

Vad är PAXG-tokenen?

PAXG är en digital tillgång som kombinerar stabiliteten i guld med tekniken i Ethereum. Varje token representerar en troy ounce av ett fysiskt guldtacka – vilket gör den spårbar, växlingsbar och tillgänglig.

Tokenen ger användare möjlighet att exponera sig mot guldpriset på ett mer flexibelt och tillgängligt sätt än att köpa fysiskt guld.

Alla tillgångar som backar PAXG förvaras säkert av Paxos och kontrolleras via månatliga rapporter som är tillgängliga på deras webbplats.

Hur köper jag PAX Gold (PAXG)?

Om du vill få tillgång till värdet av fysiskt guld – utan att behöva köpa, hantera eller förvara guldtackor själv – kan PAXG vara ett smidigt alternativ.

Via Tap-appen kan du enkelt köpa, sälja, handla och lagra PAX Gold-tokens. Det är bara att:

- Ladda ner appen

- Skapa ett konto

- Slutföra en snabb verifiering

Därefter får du tillgång till säkra kryptoplånböcker och marknader där PAXG finns tillgänglig.

Appen erbjuder inte bara handel med kryptovalutor – du kan även göra fiatbetalningar direkt från appen, eller använda Tap-kortet för att spendera dina tillgångar i vardagen – oavsett om det är i guld, krypto eller traditionella valutor.