That fleeting Altcoin frenzy probably isn't what you think it was. The next crypto rally won't be like the ones you remember, it's a whole new thing.

Keep reading

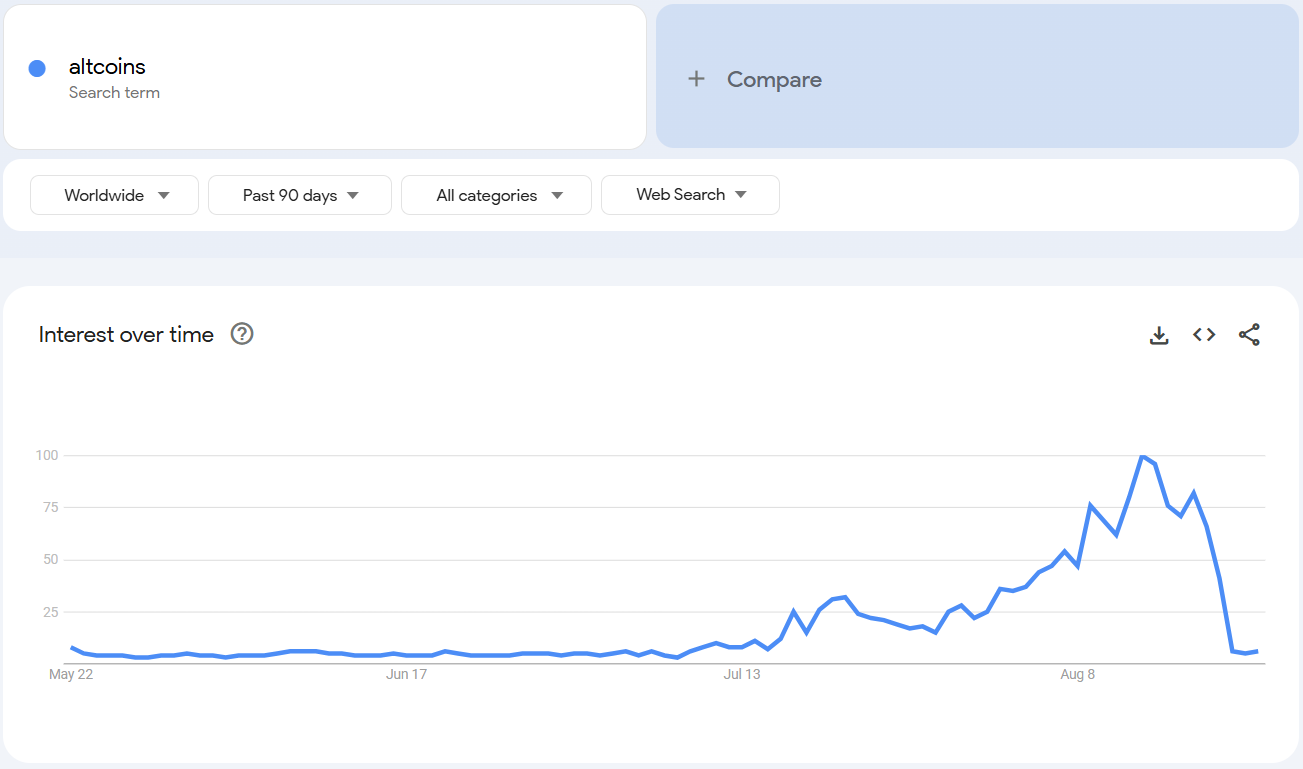

For a fleeting moment, it looked like altcoin season was finally here. Google searches for “altcoins” skyrocketed to record highs, 𝕏 was buzzing, and retail excitement seemed to return in full force. But within a week, that hype fizzled out almost as quickly as it appeared, leaving traders wondering if the long-awaited alt season was just a mirage.

A Spike That Vanished Overnight

Search interest for “altcoin” on Google Trends hit its highest score ever in early August, only to fall back to baseline levels within days. Globally, the same pattern played out, with scores dropping from 100 to just 16 in a week, mimicking a “pump and dump” pattern that you would expect from a memecoin.

Market cap data told the same story. The total value of altcoins (excluding Bitcoin and Ethereum) briefly climbed by $100 billion before giving it all back, leaving investors wondering whether the hype had any real weight behind it.

Naturally, some saw the collapse as proof that the altcoin season had ended before it really began. Others, however, like analyst Cyclop, argue the spike shows something deeper: that “altcoin” has become the mainstream term retail uses today, replacing “crypto” in 2021. In his view, this isn’t the peak. Rather, it’s just the beginning of broader interest.

Why Google Trends Doesn’t Tell the Whole Story

Relying on Google searches to measure retail demand may no longer work the way it used to. With AI tools increasingly replacing traditional search, and with concepts like “altcoins” now part of everyday investor vocabulary, Trends data might not be capturing where and how money is really flowing.

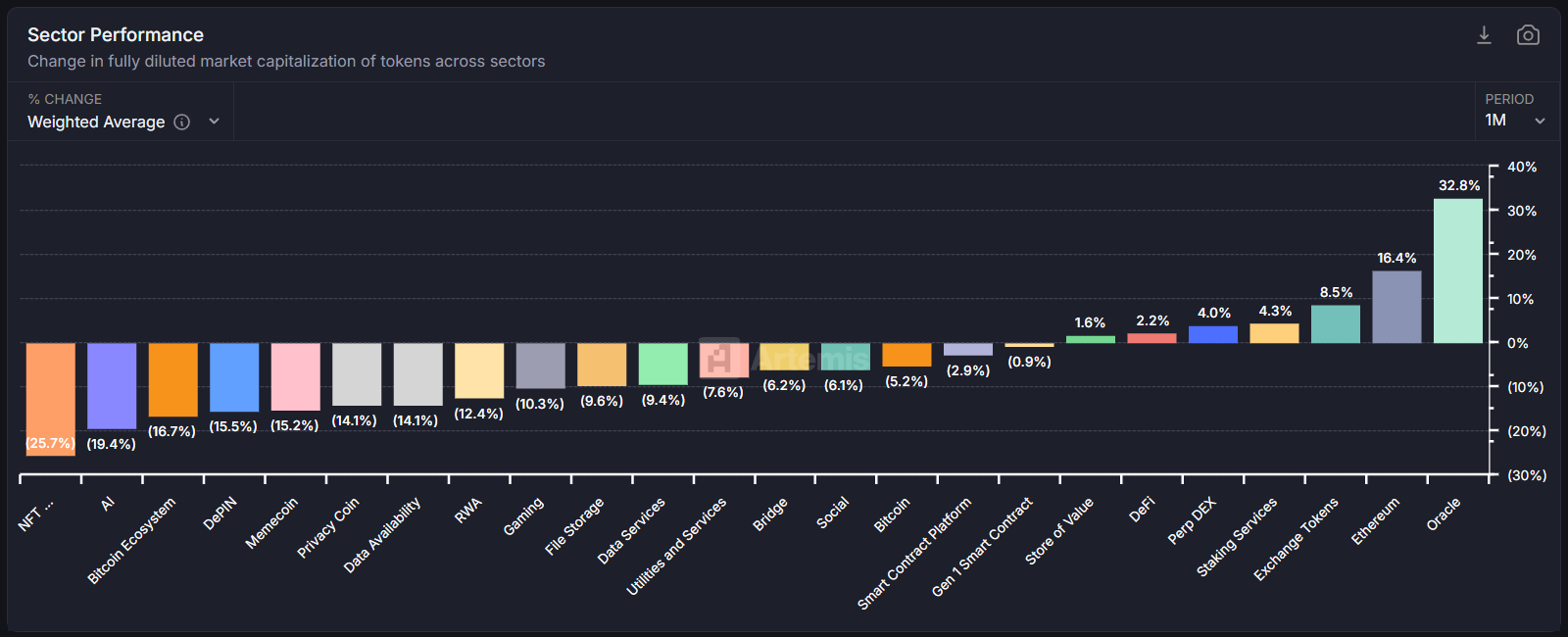

Instead, analysts point to on-chain and trading activity as better indicators of where momentum is building. And in August, that momentum was fragmented.

A Season of Winners and Losers

Data from Artemis showed only a few categories outperforming last month: Ethereum, exchange tokens, and oracles.

Beyond these bright spots, however, most altcoins struggled. The result? A patchwork “mini season” rather than the explosive, across-the-board surge that retail and social media had been hoping for.

Polygon’s co-founder Sandeep put it bluntly: "Retail is searching, but institutions aren't buying the narratives yet. Old altcoin seasons were driven by speculation and promises and narratives and marketing. Institutional money is smarter money. It cares about real utility and cash flows. The next "alt season" won't look like 2017 or 2021. It’ll be fewer tokens with actual usage, not just tokens with better marketing." Sandeep said.

The Road Ahead

That doesn’t mean altcoin season is dead, it probably just means it’s evolving.Coinbase has suggested that the next true wave could arrive as early as September, but that it likely won’t be a full-scale altcoin season.

Bottom line? The altcoin season isn’t gone; it’s just different. It’s maturing. And the next leg up may not belong to every token in the market, but only to the select few proving they can deliver value beyond mere speculation.

NEWS AND UPDATES

LATEST ARTICLE

.svg)

Playing an important role in the adoption of Web3, Enjin provides a platform of software products designed to allow anyone to harness the power of NFTs (non-fungible tokens) through the development, trade, monetization, and marketing of blockchain assets.

What is the Enjin platform?

The Enjin platform is an ecosystem of interconnected, blockchain-based gaming products designed for individuals, game developers and businesses to create, manage and trade virtual goods such as digital art, games, or virtual marketplaces using the Ethereum blockchain. Enjin aims to provide users with the tools to implement smart digital solutions for blockchain games within the gaming environment.

Through the platform's software development kits (SDKs) and APIs, users can build digital assets as well as seamlessly integrate them into their games and applications.

Under the Enjin umbrella is the Enjin Network, a community gaming platform that allows users to create websites, chat, and host virtual stores. Over the course of a decade, the Enjin platform has accumulated over 20 million users.

Powering the ecosystem is the Enjin Coin (ENJ), a token used to back the value of NFTs and other assets minted on the platform. When an asset is minted it locks ENJ tokens into a smart contract and effectively removes the tokens from circulation.

It’s also worth noting that Witek Radomski, Enjin's co-founder and the brainchild behind the ERC-1155 Ethereum token standard, wrote the code for the first non-fungible token (NFT). By utilizing its cutting-edge technology, Enjin is revolutionizing the future of gaming and digital assets.

Who created Enjin?

Enjin was originally founded in 2009 as a gaming community platform by Maxim Blagov and Witek Radomski. Blagov took on the responsibility of being CEO and in charge of the platform's creative direction while Radomski took on the role of CTO, leading the technical development of the platform's products.

Following Radomski's interest in Bitcoin in 2012, the platform explored incorporating blockchain technology into its business model and embraced the world of tokenized digital assets.

Radomski went on to write the ERC-1155 token standard in June 2018, a token standard used for minting both fungible, semi-fungible and non-fungible tokens using the Ethereum network. This token standard is a critical building block in the platform’s design.

In 2017, the Enjin platform launched an initial coin offering (ICO), raising $18.9 million through ENJ token sales. A year later the project went live and in September 2019, the Enjin Marketplace was launched.

How does Enjin work?

The primary goal of the Enjin network is to facilitate the management and storage of virtual goods for games, anything from in-game currencies to unique in-game items. So, how does Enjin work? The process of creating and destroying these tokens involves five steps, as outlined below.

- Purchase

Developers purchase Enjin Coin. - Minting

In-game items are designed and effectively minted with the appropriate amount of ENJ locked into a smart contract. - Utilization

Players use these tokens within the game. - Trading

Players trade the tokens between fellow players or on the internal or external marketplace. - Melting

Players sell the tokens for Enjin Coin, referred to as melting. The token is destroyed and Enjin Coin is released from the smart contract.

SDKs (software development kits) come into play here, with kits designed to fulfill certain functions, such as facilitating a payment platform or being wallet-focused. These kits are designed to minimize costs and simplify the process of creating these virtual goods. APIs (application programming interfaces) work alongside the SDKs to integrate these virtual goods (digital assets) into the game.

The Enjin platform utilizes JumpNet which is integrated with other products in the ecosystem, such as the Marketplace, Enjin Beam, and the Enjin Wallet to allow for gas-free transactions for ENJ and NFTs.

The Enjin ecosystem encompasses the Enjin smart wallet that allows players to store and trade their in-game items with ease. The Enjin wallet is designed to connect all the features, from managing inventory to conducting transactions and selling these tokenized digital assets for ENJ.

What is the Enjin Coin (ENJ)?

Enjin Coin (ENJ) is the native token of the Enjin ecosystem. Built on the Ethereum blockchain and compatible with multiple gaming platforms, the Enjin Coin is an ERC-20 token that allows the in-game items created on the platform to be traded with real-world value. The ENJ token has a maximum supply of 1 billion coins.

The token also allows developers to mint these digital goods. The process requires the users to lock Enjin Coin (ENJ) into a smart contract that automatically assigns value to the in-game item. Players that later use these items can use them in the game, trade them or sell them for ENJ, equivalent to the original minting cost. Once sold, the item is destroyed (known as melting) and the ENJ that was locked in the smart contract is released to the seller.

How can I buy Enjin Coin?

Anyone can tap into the Enjin ecosystem by acquiring ENJ tokens through the Tap mobile app. Simply create an account and complete the verification process in order to gain access to your unique Enjin wallet, from where you can buy, trade and sell Enjin Coin.

Fully licensed and regulated, Tap provides a secure and convenient means of managing your funds, allowing users to manage and store both crypto and fiat currencies in one location. With a wide range of supported currencies and services, Tap is revolutionizing the financial space.

Take advantage of the power of Enjin Coin on the Tap app - the ultimate platform to buy, sell or hold ENJ. With seamless integration and an intuitive interface, trading Enjin tokens has never been easier. Stay up-to-date with the latest market trends and keep your portfolio on track by monitoring the Enjin Coin price in real-time.

In this article, we're covering what transaction fees are, and taking a look at which cryptocurrencies offer the lowest transaction fees.

While long-term traders are unlikely to get affected by transaction fees, short-term traders and people actively using cryptocurrencies are often plagued with excessive fee structures.

This complaint has led to layer 2 solutions, where transactions can most quickly and cost-effectively be executed, as well as new blockchain platforms entirely (as was the case when developers migrated away from Ethereum due to high transaction costs).

What are transaction fees?

Transaction fees are fees paid to the miner of the network to execute the transaction. While some networks differ in how they operate, transaction fees are consistent across the board. Looking at Bitcoin as an example, when a user sends BTC the transaction is entered into a pool of pending transactions known as a mempool.

The miner will then pick up a batch of transactions and validate them, checking to see whether the original wallet does in fact have the funds to send and if the wallet addresses are valid. Once the transaction is executed, the data relevant to the transaction is added to a block, which is added to the blockchain chronologically.

As compensation to the miner for their time and electricity, they earn a small crypto transaction fee from each transaction as well as a reward for adding the block, known as a miner's reward. This process also ensures the safety and integrity of the network.

When the networks are very busy, the cost of sending a transaction is increased. Users can then choose to add in a higher crypto transaction fee in order to prioritise their transaction in the mempool.

Transaction fees for smart contracts are based on how much electricity will be needed to complete the task. Typically, transaction fees on smart contracts are much higher.

Generally, the terms transaction fee and network fee can be used interchangeably. They both refer to the transaction fee necessary by the network for the transaction to get processed.

Exchange fees refer to something else entirely. Exchange fees are fees charged by the exchange in order to conduct the service. Be sure to check before conducting a transaction on an exchange as you might be required to pay a transaction fee (or network fees) as well as exchange fees.

How to pay less for transaction fees

A transaction fee is imperative to your transaction getting executed so it cannot be avoided entirely, however, there are ways to reduce the amount you need to pay.

Transaction fees increase when the network is busy, so sending your transaction while the network is quieter is a great way to reduce the transaction fee. Typically the busier periods are during business hours in the United States.

Look out for the Lightning Network for Bitcoin and layer-2 scaling solutions for Ethereum as these will provide a cost-effective solution to high transaction costs on those networks.

Which cryptocurrency has the lowest average transaction fee?

Let's take a look at some of the most popular cryptocurrencies and the average transaction fee associated with their platforms.

XRP - $0.0002 per transaction

Developed by Ripple Labs, XRP is optimised for fast, affordable cross-border payments, with a focus on serving financial institutions and remittance providers. Thanks to its unique architecture, XRP has cemented its status as a key player in the payment processing space.

XRP's minimal costs and 4-second transaction times make it a preferred choice for users and institutions alike.

Solana (SOL) - $0.00025 per transaction

Solana’s transaction fees cost just fractions of a cent ($0.00025), with complex transactions also coming in incredibly cheap. The network stands out for its lightning-fast transactions, typically wrapping up in about 2.5 seconds. Thanks to its scalable design, Solana can handle many transactions simultaneously, making it a hit for dapps and big blockchain projects.

This efficiency, coupled with its rapid speed, has made Solana a favourite among both developers and users, and a permanent feature in the top 10 biggest cryptocurrencies based on market cap (currently number 5).

Litecoin (LCH) - $0.0025 per transaction

Litecoin stands out as one of the cheapest crypto options out there, costing around $0.0025 per transfer. As an early pioneer in the space, Litecoin was designed with fast, affordable payments in mind, borrowing and refining Bitcoin's underlying technology. Litecoin's speedy 2.5-minute transaction times add to this appeal.

The minimal fees on Litecoin are a huge plus, with its efficiency and speed making Litecoin an attractive choice for those seeking a cost-effective crypto.

Bitcoin Cash (BCH) - $0.01 per transaction

Bitcoin Cash makes it onto the list with an attractive $0.01 average transaction fee. As a Bitcoin offshoot, BCH was engineered for faster, more affordable transfers via larger block sizes.

The cost-effective fees on Bitcoin Cash have made BCH a viable option for those looking for a low-cost market entry and equally impressive low-cost transaction fees.

Dogecoin (DOGE) - $0.04 per transaction

Dogecoin, born in 2013 as a playful take on crypto, has surprisingly become a significant player in the crypto space. Despite its lighthearted meme-inspired origins, Dogecoin's enthusiastic community and celebrity endorsements have propelled it into the mainstream.

Its low $0.04 average transaction fees and fast 1-minute transaction times make it practical for frequent micro-transactions like tipping and donations, blending fun and function.

Trade smart, trade with Tap

Users can trade all the tokens mentioned above with equally low exchange fees directly on the Tap app. Adding to the cost-effective nature of the platform, it also offers heightened security and added convenience. It's time to trade smarter, download the Tap app and get started today.

We're thrilled to share that our fintech company has just celebrated its third anniversary! It's been an incredible journey so far, and we're so grateful for the opportunity to serve our users every day.

When we first launched our platform three years ago, we had a clear mission in mind: to provide an innovative, user-friendly, and accessible way for people to manage their money, trade cryptocurrencies, and access financial services. It was a big goal, and we knew that we had a lot of hard work ahead of us.

But we were determined to succeed. Our small team of passionate and dedicated individuals worked tirelessly, day in and day out, to bring our vision to life. We poured our hearts and souls into this project, and we knew that we were onto something special.

Fast forward three years, and we're proud to say that we've come a long way. We've built a platform that we believe in, and we're constantly striving to improve it. We've listened to feedback from our users, and we've added new features and services that meet their needs. And we've built a community of passionate and engaged users who share our vision for a better way to manage their finance everyday.

One of the things that sets our company apart is our commitment to transparency and user experience. We believe that managing your finances should be easy, intuitive, and stress-free. That's why we've built our platform to be as user-friendly as possible, with clear and straightforward interfaces that make it easy to manage your money and digital assets.

But our success wouldn't be possible without our amazing users. We're so grateful for your continued support, feedback, and encouragement. You've helped us to shape our platform into something truly special, and we're committed to continuing to serve you and improve our platform to meet your needs.

As we celebrate our third anniversary, we're excited to look back on how far we've come and to look forward to all the exciting things that the future holds. We're proud of what we've accomplished, but we know that there's always more work to be done. We're committed to continuing to innovate and improve, and we're grateful to have you along for the ride.

Thank you for being part of our journey. Here's to many more years of growth, success, and innovation!

Du kanske redan har testat att köpa och sälja kryptovalutor – men har du koll på airdrops? En airdrop är en marknadsföringsstrategi som används för att skapa uppmärksamhet och bygga upp ett starkare nätverk kring ett kryptoprojekt.

I den här guiden går vi igenom vad airdrops är, hur de fungerar och varför de har blivit ett populärt sätt att engagera communityn – ofta med riktiga tokenbelöningar.

Vad är en krypto-airdrop?

En krypto-airdrop innebär att ett projekt delar ut sina egna tokens gratis till användare. Målet? Att skapa hype, öka spridningen av sina tokens och locka nya användare – ofta i ett tidigt skede innan projektet listas på en börs.

I vissa fall krävs det små insatser, som att följa projektets sociala medier eller gå med i en Telegram-kanal. I andra fall får man tokenbelöningen utan att behöva göra något alls.

Airdrops blev särskilt populära under ICO-boomen 2017 och används fortfarande idag. Och även om tokenen ges bort gratis, kan dess värde öka med tiden – vilket gör airdrops potentiellt intressanta för användare.

När projekten delar ut tokens ökar också decentraliseringen, vilket ofta ses som ett positivt tecken på att projektet är community-drivet.

Hur fungerar en krypto-airdrop?

En airdrop finns ofta med i ett projekts roadmap och startar när vissa kriterier är uppfyllda. Det kan handla om att uppnå ett antal användare, genomföra en marknadskampanj eller lansera en viss funktion.

Tokens delas vanligtvis ut i små mängder till många olika plånböcker. Dessa tokens bygger ofta på blockkedjor som Ethereum eller andra smarta kontraktsplattformar.

För att kvalificera sig kan man behöva:

- Hålla ett visst antal tokens i sin plånbok

- Gå med i en community

- Utföra enkla marknadsföringsuppgifter (t.ex. gilla ett inlägg)

En lyckad airdrop leder ofta till att användare själva sprider ordet och skapar intresse kring projektet.

Airdrop vs ICO – vad är skillnaden?

Både airdrops och ICO:er handlar om nya kryptoprojekt, men det finns en tydlig skillnad:

- Airdrop: Tokens delas ut gratis som en form av marknadsföring.

- ICO (Initial Coin Offering): Tokens säljs till användare till ett fast pris – som ett sätt att samla in kapital.

Man kan säga att ICO är ett crowdfunding-verktyg, medan airdrops är ett marknadsföringsgrepp.

Vilka typer av airdrops finns?

Det finns olika typer av airdrops – här är de tre vanligaste:

🎯 Exklusiva airdrops

Riktade mot aktiva medlemmar eller early adopters. Tokens skickas endast till utvalda plånböcker.

Exempel: Uniswap skickade 400 UNI till varje användare som använt plattformen innan ett visst datum.

🪙 Bounty airdrops

Användare måste utföra uppgifter, t.ex. gilla inlägg, dela tweets eller tagga vänner. Vissa projekt ber om bevis innan distribution.

🔒 Holder airdrops

Belöningar till befintliga innehavare av projektets token. Projekten tar en "snapshot" av alla plånböcker och skickar belöningar till dem som uppfyller kriterierna.

Exempel: 2016 airdroppade Stellar 3 miljarder XLM till Bitcoin-innehavare för att locka användare till sin plattform.

Finns det risker med airdrops?

Ja – precis som allt annat i krypto finns det risker att känna till:

- Bedrägliga projekt kan skicka tokens till din plånbok – men när du försöker använda dem kan plånboken bli tömd.

- Phishing-sajter kan efterlikna riktiga projekt och be dig ansluta din plånbok – och i värsta fall stjäla dina tillgångar.

- Ingen legitim airdrop kommer någonsin kräva din seed phrase eller att du skickar pengar för att "låsa upp" en token.

En annan nackdel är att distributionen kan ge falska intryck. Tusentals tokens i tusentals plånböcker kan få ett projekt att se större ut än det egentligen är.

👉 Tips: Kontrollera alltid att projektet har verklig handelsvolym – inte bara många innehavare.

In the age of neobanking, it seems counter-intuitive to be locked into a long-term relationship with an establishment that hasn’t changed in 300 years. With outdated processes and tedious hoops to jump through, it’s high time you said goodbye to the traditional financial institution and treated your finances with the love and respect they deserve.

From an outdated bank to an even more outdated credit union, you don't need to settle for financial institutions that make the rules and take your money. It's 2022, you have options. And we know, the process to switch from your current bank is tedious, but with the technological advancements of today, that's a thing of the past.

You deserve better from your financial institution

Knowing you deserve better is the first step toward claiming back your power. It’s time to say goodbye to high, complicated fee structures and hello to transparency, minimal fees, and knowing exactly where your money goes.

As the world rapidly transitions into a more digital space, why keep the management of your finances stuck in the dark age? Fintechs are making big strides in providing the masses with new-age financial services with faster processing times and more transparent fees. Your financial livelihood deserves better.

Neobanking vs traditional banks

Let’s take a moment to define neobanking. Neo comes from the Greek word “new”, literally meaning “new bank”. These financial technology companies (fintechs) offer users access to financial services through online digital platforms, an online bank of sorts. While not all fintechs are created equal, the majority require special licensing and provide something similar to a checking account with web and mobile services.

A traditional financial institution refers to the age-old establishment that in all likelihood is the same bank that our grandparents used in their days. Innovation in the traditional bank sector has been stagnant over the last several decades, and little has changed in these money-making corporations. They also tend to have deep political, financial, and social roots in their countries of operation. Not to mention poor customer service.

- Neobanking companies are largely like a digital online baking providers, whereas traditional banks have a physical presence alongside online banking services.

- Fintechs offer standard services such as checking and savings accounts, money transfer and payment services, low to no overdraft fees and some financial education tools (budgeting tools, etc). On the other hand, traditional credit unions present a much wider selection of options like lines of credit, financial advisors, credit cards, etc.

- While all traditional banks are fully licensed and chartered, many fintechs do own different as significant licenses such as EMI licenses. In some cases, in order to insure their products, neobanks do choose to partner with a primary bank.

- Many banks focus more on developing strong, lasting relationships while neobanks typically provide more flexible accounts than just a simple bank account, which require less paperwork and can be used worldwide.

- Online banks tend to overwhelm clients with a variety of complicated fees while neobanks charge much lower fees for their services, including for most : no monthly maintenance fee.

- While banks provide you with a face to face agent, fintechs do not, however they still provide quality customer service representatives ready to help you online with anything you might need. In short both boast different yet great excellent customer service.

Fintech do provides a new-age approach with fewer fees and more transparency, but with all, if not most, of the bells and whistles that your current banking platform provides.

With growing pressure to "have it all figured out" consider that since the start of their careers, millennials have seen slower economic growth than any other generation in the United States' history. Living through two recessions wreaks havoc on not only one's career path but finance success too.

Below we've listed the 5 golden financial tips that every millennial should know when it comes to managing their personal finance. From things you can do now to planning for the future, these simple and actionable steps will assist in making your financial situation that much more of a financial success.

1. Be prepared for hard times: emergency fund edition

While none of us enjoy emergencies, they are an unfortunate and inescapable part of reality. The best way to deal with them is by being prepared, and this means putting in the work ahead of time. By having a plan in place, you can minimize the stress and damage that these situations cause.

While rule number 1 of financial health is getting yourself out of debt, rule number two is creating an emergency fund. This is considered to be six months' worth of living expenses saved in a savings account so should something go wrong - from unemployment to medical bills to car or household repairs - this doesn't take a negative toll on your personal finance.

While this is not something one can typically create overnight, consider your budget and how much you can allocate to your emergency fund each month. Then start putting the money aside, even if it takes you a year or two to get there.

Consider if something went wrong and you needed access to cash fast, would you instead use the money from your emergency fund, or take out high-interest debt in the form of a credit card or personal loan? Note that taking funds from your retirement savings was not an option, and nor should it ever be.

In your path to financial success, always have a plan to fall back on.

2. Living large is fun, but can your personal finance really afford it?

Before making big money decisions, you must ask yourself difficult questions.

Before you upgrade your car, consider whether you can really afford it. Aside from the car, there is also insurance and gas and services, can your budget afford to take these on?

Or when moving apartments, is the upgrade totally necessary, and can your budget handle it? As millennials, we love to live the high life, but just make sure that your budget isn't taking strain and that everything you buy is well within your means.

3. It's ok to say no sometimes (and avoid credit card debt)

Celebrating with friends and family is a big part of life, but you don't have to say yes to everything, especially if these celebrations are taking a toll on your personal finances.

When planned ahead of time, one can usually budget for these, but last-minute surprise events come with added pressure. Also, consider that all these functions and events add up, don't get caught off guard "living in the moment" only for your finances (and financial goals) to suffer later.

Create a budget that outlines exactly what your financial obligations are to establish what you can spend on entertainment and socializing each month. Then, and most importantly, stick to it. If a last-minute event falls outside of this budget, you're well within your means to politely decline.

Having fun with friends and family is special, but taking a financial knock will only hurt you in the long run. Prioritize your social calendar and don't live beyond your means.

4. Watch out for direct debits (except to your savings account)

Living in the digital age we find ourselves in now is designed to be stress-free and seamless. Companies are making payments effortless through automatic payments, aka direct debits, but are you entirely aware of all the payments going off your checking account each month? It's very easy to lose track of your expenses when they're all automated.

When building your budget make sure you go through old statements to make sure that no direct debits are going off your account for services that you no longer use. Ideally, do this quarterly to ensure that you're always on top of your expenses.

The most NB direct debits should be to your emergency fund, savings account, and any investments (including your retirement fund). These are not considered expenses but are deposits into your future.

5. Don't be fooled into thinking that retirement is light years away

Your retirement is closer than you think, don't get caught out. Many millennials have seen their parents and grandparents struggle with no retirement planning, break the cycle and make sure that you are prepared with a plan and a solid retirement account.

Don't wait until you're old, start preparing now and reap the rewards when you finally get there. A great way to prepare is to start putting money into long-term investments with compounded interest. These types of accounts ensure that your money works for you. Also, look to passive income options to help you build your retirement account.

Alleviate some of the grey hairs by getting your financial planning started today.

Closing thoughts on achieving financial success

While the economic cycles haven't been good to us, we are resilient and strong and will rise above it. Consider these 5 golden financial tips and build a financial strategy to ensure that you're covered for everything from an emergency to retirement. The first steps to taking the reigns of your personal finance are to write out a monthly budget, allocate funds as necessary, and then stick to your spending frameworks.

If in doubt, contact a financial advisor who can assist with furthering your financial education and provide more in-depth money tips.