That fleeting Altcoin frenzy probably isn't what you think it was. The next crypto rally won't be like the ones you remember, it's a whole new thing.

Keep reading

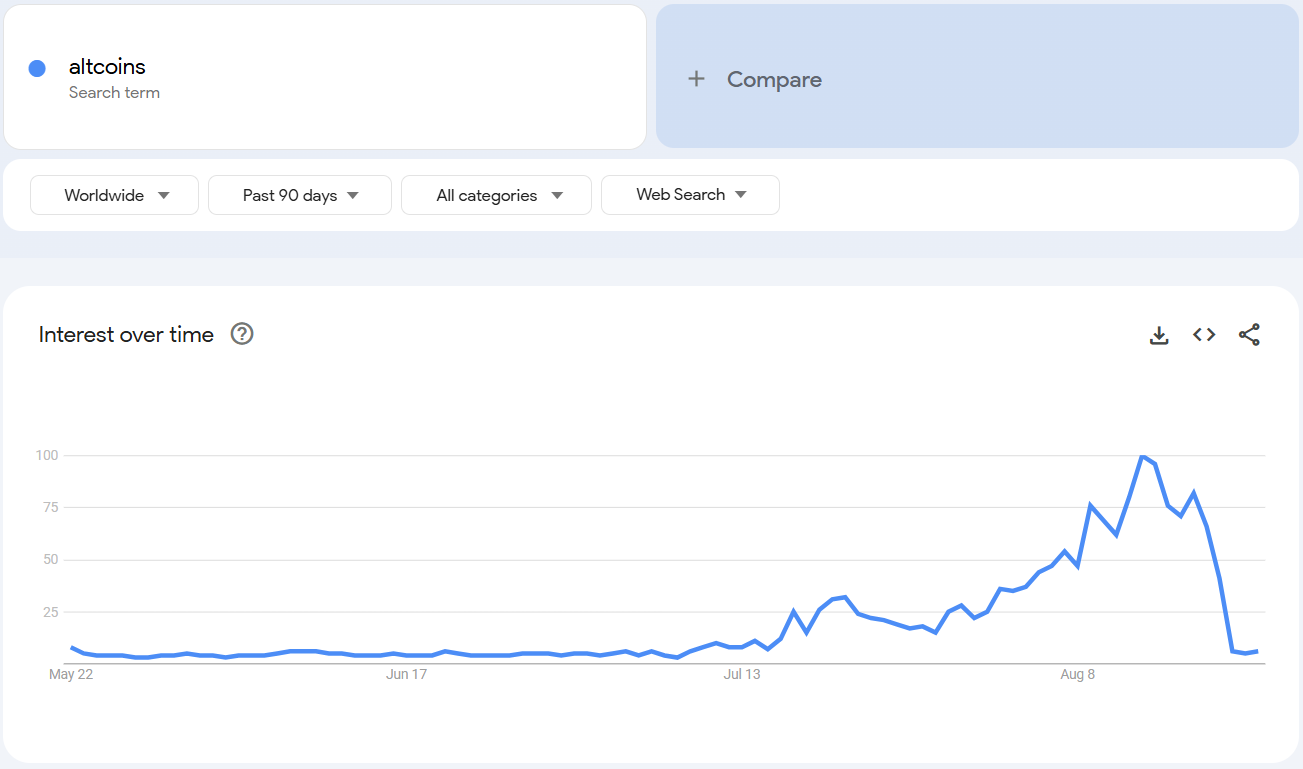

For a fleeting moment, it looked like altcoin season was finally here. Google searches for “altcoins” skyrocketed to record highs, 𝕏 was buzzing, and retail excitement seemed to return in full force. But within a week, that hype fizzled out almost as quickly as it appeared, leaving traders wondering if the long-awaited alt season was just a mirage.

A Spike That Vanished Overnight

Search interest for “altcoin” on Google Trends hit its highest score ever in early August, only to fall back to baseline levels within days. Globally, the same pattern played out, with scores dropping from 100 to just 16 in a week, mimicking a “pump and dump” pattern that you would expect from a memecoin.

Market cap data told the same story. The total value of altcoins (excluding Bitcoin and Ethereum) briefly climbed by $100 billion before giving it all back, leaving investors wondering whether the hype had any real weight behind it.

Naturally, some saw the collapse as proof that the altcoin season had ended before it really began. Others, however, like analyst Cyclop, argue the spike shows something deeper: that “altcoin” has become the mainstream term retail uses today, replacing “crypto” in 2021. In his view, this isn’t the peak. Rather, it’s just the beginning of broader interest.

Why Google Trends Doesn’t Tell the Whole Story

Relying on Google searches to measure retail demand may no longer work the way it used to. With AI tools increasingly replacing traditional search, and with concepts like “altcoins” now part of everyday investor vocabulary, Trends data might not be capturing where and how money is really flowing.

Instead, analysts point to on-chain and trading activity as better indicators of where momentum is building. And in August, that momentum was fragmented.

A Season of Winners and Losers

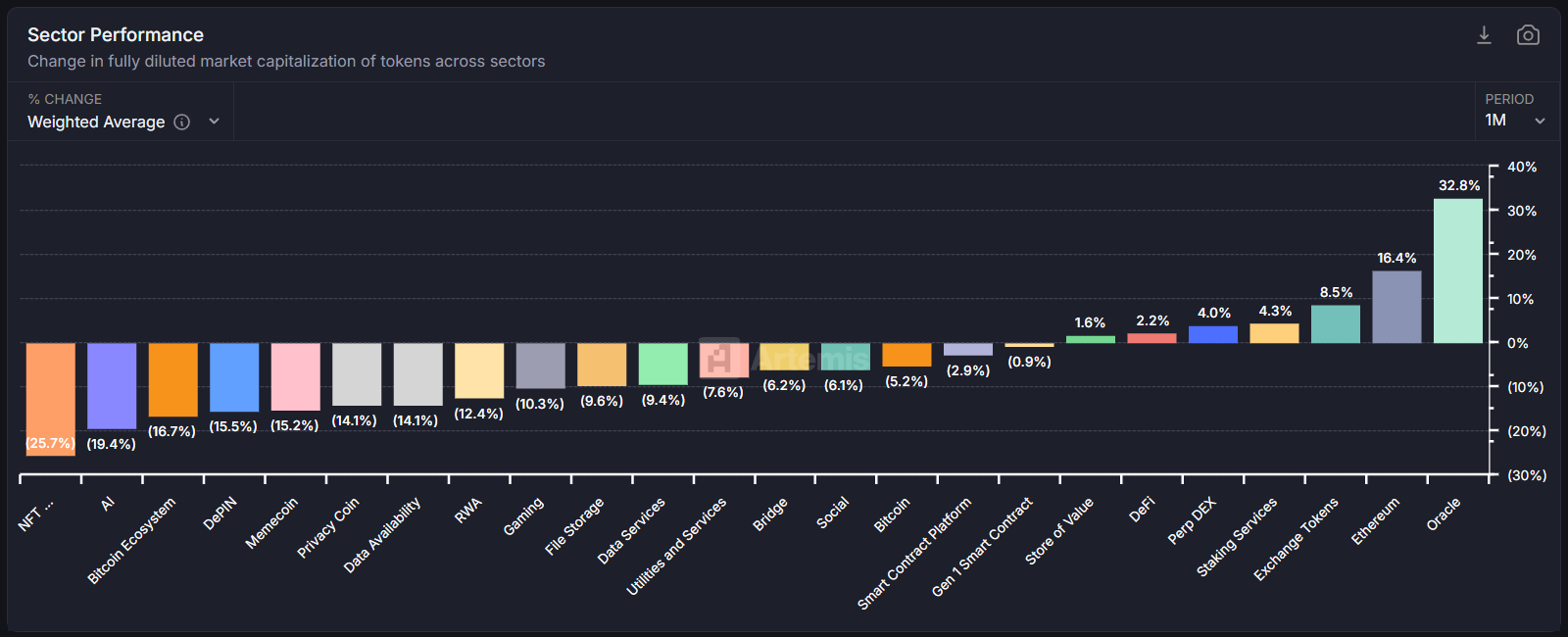

Data from Artemis showed only a few categories outperforming last month: Ethereum, exchange tokens, and oracles.

Beyond these bright spots, however, most altcoins struggled. The result? A patchwork “mini season” rather than the explosive, across-the-board surge that retail and social media had been hoping for.

Polygon’s co-founder Sandeep put it bluntly: "Retail is searching, but institutions aren't buying the narratives yet. Old altcoin seasons were driven by speculation and promises and narratives and marketing. Institutional money is smarter money. It cares about real utility and cash flows. The next "alt season" won't look like 2017 or 2021. It’ll be fewer tokens with actual usage, not just tokens with better marketing." Sandeep said.

The Road Ahead

That doesn’t mean altcoin season is dead, it probably just means it’s evolving.Coinbase has suggested that the next true wave could arrive as early as September, but that it likely won’t be a full-scale altcoin season.

Bottom line? The altcoin season isn’t gone; it’s just different. It’s maturing. And the next leg up may not belong to every token in the market, but only to the select few proving they can deliver value beyond mere speculation.

NEWS AND UPDATES

LATEST ARTICLE

Slippage plays an important role in trading cryptocurrencies for retail investors as it determines the difference between the amount that you expected to pay in a transaction and the amount the trade was executed at. Below we're uncovering what slippage in crypto is, explaining how it can contribute to risk, and providing some practical examples on how to avoid it.

What Is Slippage In Trading?

Slippage is when an investor opens a trade but between creating the trade and the trade executing, the price changes due to price movements in the greater market. This can often be a costly problem in the financial sector and particularly when trading digital currencies on crypto exchanges.

How Does Slippage Occur?

The two main causes of slippage are volatility and liquidity, outlined in more information below.

Volatility is when the price changes rapidly, as is common in cryptocurrency markets, and as a result the price changes between the time of creating the buy or sell order and the time of execution.

Liquidity concerns on the other hand are when the coin you are trading is not traded very often and the range between the lowest ask and the highest bid is wide. This can cause sudden and dramatic price changes, resulting in slippage. Fewer people trading an asset results in fewer asking prices, resulting in less favourable prices.

This is common among altcoins with low volume and liquidity. While slippage can occur in forex and stock markets too, it is much more prevalent in crypto markets, particularly on decentralised exchanges (DEXs).

There are two types of slippages:

Positive Slippage

Positive slippage is when a trader creates a buy order and the executed price is lower than the price initially expected. This will result in the trader getting a better rate. The same is true for a sell order that experiences a higher price point at trade execution, resulting in more favourable value for the trader. Positive slippage banks profits.

Negative Slippage

Negative slippage is when the trader loses out on the trade, with the price of the buy order higher than expected at the time of execution. The opposite is true for sell orders, meaning that the execution price is lower at the time of execution, similarly resulting in losses for the trader.

Can Slippage Be Avoided? How To Avoid Slippage

While one can't eradicate slippage entirely, there are several measures one can take to better manage slippage, as regularly falling victim to negative slippages can result in losing a lot of money.

- Create limit orders

Instead of creating market orders, traders can instead create limit orders as these types of trades don't settle for unfavourable prices. Market orders are designed to execute a trade service as quickly as possible at the current available price.

- Set a slippage percentage

Traders can create a slippage percentage that eliminates trades happening outside of the predetermined range. This can range from 0.1% to 5%, however, if the slippage percentage is too low this could lead to the trade not being executed and the trader missing out on large drops/jumps.

- Understand the coin's volatility

When in doubt, get educated. Learn about the coin's volatility as well as the volatility on the trading platform you are using. Understanding more about previous patterns can assist in making more informed decisions on when to open and close a position, and avoiding negative slippages.

How To Calculate Slippage

Slippage can be calculated in two ways, either in dollar amount or percentage. Although to work out the percentage, you will first need the dollar amount. This is calculated by subtracting the price you expected to pay from the price you actually paid. This amount will indicate if you incurred a positive or negative slippage.

Most exchanges express this amount in percentages. This is calculated by dividing the dollar amount of slippage by the difference between the price you expected to get and the limit price. Then multiply that by 100.

For example, say you are looking to buy Bitcoin for $50,000, but are not willing to pay more than $50,500. When the price is at $50,000 you will create a limit order of $50,500, however, the order executes when the price reaches $50,250. This will result in a $250 slippage.

To calculate the percentage, divide $250 by $500 (the difference between the price you expected to pay and the limit order). 0.5 multiplied by 100 equals 50%.

In this case, your slippage was $250 or 50%.

Want to know more about cryptocurrencies and trading? Check out all our other educational articles here.

Sitting among the 30 biggest cryptocurrencies by market cap, Stellar is focused on bridging the gap between the business of blockchain and the traditional financial institutions. The platform provides a means for users to send assets and money through the blockchain, utilising a decentralised network of authenticators.

Redefining the financial landscape, Steller presents a digital transformation on the traditional services users have become accustomed to. Merging innovation with a practical application, the network is able to help users around the world, as well as financial industries, achieve a more streamlined service. Let's explore what Stellar is.

What is Stellar (XLM)?

Before we dive into the "what", let's first stipulate that one stellar is known as a lumen and uses the ticker XLM. Stellar launched in July 2014 and soon afterwards changed its strategy to be more focused on integrating blockchain technology into financial institutions.

The concept behind Stellar is to provide a space in which users can transfer everything from traditional crypto and fiat currencies to tokens representing new and existing assets, increasing their transaction performance by using lumens.

Similar to the Ripple XRP network, Stellar is designed to cater to both payment providers and financial institutions, building a bridge between the blockchain and traditional financial sector. Developing on the Ripple concept, Stellar has also positioned itself as an exchange as its ledger has an inbuilt order book that keeps track of all the assets on the network.

Who Created Stellar?

The founders of Stellar are Jed McCaleb and Joyce Kim, both previously employees at Ripple. McCaleb, who founded and was acting CTO of Ripple, and lawyer Joyce Kim, decided to create Stellar after they left the Ripple team in 2013 following a disagreement on the direction that Ripple was taking. McCaleb is also credited with creating the first successful Bitcoin exchange, Mt Gox.

McCaleb described Stellar's aim as giving people a means of moving their fiat into crypto and more seamlessly conducting international payments. The network provides cross border transactions with low transaction fees and fast executions. With leading technology and innovative problem solving, the network has made a healthy impression on both institutions and investors alike.

How Does Stellar Work?

Stellar is a hard fork off of the Ripple network with several similarities in design and functionality, however, the platform set itself apart by building in several key features. The platform is secured through the Stellar Consensus Protocol which revolves around these core business concepts: decentralised control, flexible trust, low latency, and asymptotic security.

The biggest upgrade launch came in 2015 when the platform replaced its consensus mechanism with a concept called federated Byzantine agreement. This required nodes to vote on transactions until quorums are reached. Anyone is able to join the consensus, and there are measures in place to inhibit bad actors operating with ill intent on the network.

The software behind the platform is called Stellar Core and can be altered to adhere to the needs of the operation using it. The nodes making up the network can be created to function as either Watchers, Archivers, Basic Validators or Full Validators. For example, watchers can only submit transactions while Full Validators can vote on which transactions are valid and maintain a ledger of all node activity.

Another element to the network is the Stellar Anchors. These gateways are responsible for accepting deposits of currencies and assets and issuing depictions of these on Stellar.

What Is XLM?

Known as lumens, XLM is the native cryptocurrency to the Stellar platform. XLM acts as an intermediary currency for transactions taking place on the network. With cost-effective experience priorities, every transaction on the Stellar network costs 0.00001 XLM, a fraction of a dollar (at the time of writing).

When the platform launched in 2014, 100 billion lumens were minted, programmed to increase by 1% annually until the total supply reached 105 billion. Five years later the Stellar uses voted to end this process.

That same year, in 2019, the Stellar Development Foundation (a non-profit organisation) reduced its share of XLM in order to regulate the Stellar economy. This brought the total supply down to 50 billion. At the time of writing, roughly 49% of this total supply is in circulation.

Risk in trading is the chance that something might negatively impact an investment. Before engaging in any trading activities it is important to evaluate your appetite for risk, determining whether you are able to handle more risk or are more risk averse.

Measuring risk will be dependent on the type of asset you are investing in, the amount of capital you have to use, and the time frames in which you expect to see results. Different assets and trading strategies hold different amounts of risk.

For example, investing in an index fund is considered a low-risk investment and is better advised to investors looking to make a slow and steady return over a longer period of time. Index funds aggregate the performance of the 100 companies listed on a particular stock exchange and pay back dividends accordingly. Because they are large companies the growth is often more likely to be smaller yet consistent.

With a little more appetite for risk, in the crypto markets, the same could be said about choosing to invest in an emerging altcoin versus established cryptocurrencies like Bitcoin or Ethereum. An emerging asset would encompass a higher risk higher reward ratio, however, no returns are guaranteed.

You can speak to a financial advisor to get a sense of your risk appetite.

Solana är en högpresterande blockkedja som använder en unik konsensusmekanism för att uppnå både höga transaktionshastigheter och säkerhet. Tack vare sin användarvänliga design används plattformen redan av stora aktörer runt om i världen. Här går vi igenom vad Solana (SOL) är, dess ambitioner, framgångar, och varför det så ofta kallas för en av de största utmanarna till Ethereum.

Sedan Bitcoin introducerades 2009 har ett helt ekosystem av kryptovalutor vuxit fram — värt nära 1,2 biljoner dollar i skrivande stund. Medan Bitcoin skapades som ett alternativt betalningssystem för att lösa problem i det traditionella finanssystemet, har plattformar som Ethereum, och numera Solana, tagit steget längre genom att möjliggöra utvecklingen av hela blockkedjeindustrin med hjälp av programmerbara funktioner.

Vad är Solana (SOL)?

Solana har snabbt seglat upp som en av de mest populära protokollen inom DeFi (decentraliserad finans). Plattformen ger utvecklare möjlighet att bygga decentraliserade applikationer (dApps) och smarta kontrakt — ungefär som Ethereum. Det som gör Solana extra intressant är dock den imponerande transaktionshastigheten och de låga avgifterna.

Bakom projektet står två huvudaktörer: Solana Foundation, en ideell organisation baserad i Schweiz som arbetar med att främja plattformen och skapa internationella samarbeten, och Solana Labs, med säte i San Francisco, som driver den tekniska utvecklingen framåt.

Solana strävar även efter att göra kryptovärlden lite grönare. Plattformen använder nämligen både en Proof-of-Stake-mekanism för att säkra nätverket och en banbrytande innovation kallad Proof-of-History (PoH), framtagen av en av grundarna själv.

PoH fungerar som ett slags tidsstämpel inuti nätverket och gör det möjligt att behandla upp till 65 000 transaktioner per sekund. Som jämförelse hanterar Ethereum ungefär 30 transaktioner i sekunden. Kort sagt hjälper PoH till att hålla koll på tidsflödet i datan — en riktig gamechanger.

Tack vare sin snabbhet har Solana byggt upp ett troget community. Plattformen används av företag inom allt från finans till resor, och intresset för SOL-token, plattformens egna kryptovaluta, är stort.

Nyckelfunktioner hos Solana

Solana har flera starka kort på handen som gör att den sticker ut:

Skalbarhet

Solana kan hantera tusentals transaktioner per sekund tack vare avancerad teknik som parallell bearbetning och så kallade TPUs.

Smarta kontrakt

Plattformen stödjer smarta kontrakt och ger utvecklare friheten att skapa decentraliserade appar.

Konsensus via Proof of Stake (PoS)

Solanas unika PoS-system kombineras med Proof-of-History för snabba transaktioner, effektiv validering och snabba blockbekräftelser.

Decentraliserad finans (DeFi)

Med snabba och prisvärda transaktioner har Solana blivit en favorit inom DeFi-världen — perfekt för utlåning, handel, och mycket mer.

Vem skapade Solana?

Bakom Solana står mjukvaruingenjören Anatoly Yakovenko. Han började utveckla projektet redan 2017 tillsammans med sina tidigare kollegor Greg Fitzgerald och Eric Williams. Med hjälp av sitt team byggde de tillsammans det programmerbara nätverk vi ser idag.

Yakovenko är även hjärnan bakom PoH-protokollet som har gett Solana dess unika skalbarhet och effektivitet. Hans tekniska kunnande har satt ett tydligt avtryck i blockkedjevärlden.

Hur skiljer sig Solana från Ethereum?

En av Solanas huvudambitioner är att förbättra flera av Ethereums tekniska funktioner. Plattformen gör transaktioner betydligt snabbare, samtidigt som den ökar kapaciteten och sänker kostnaderna — något som gjort Solana till ett populärt val för dem som söker effektivitet.

Skalbarhet

Solana har kapacitet att hantera cirka 65 000 transaktioner per sekund idag, och målsättningen är att klara upp till 700 000 när nätverket växer. Jämförelsevis klarar Ethereum omkring 30 TPS.

Det är dessutom en av få plattformar på denna nivå som kan erbjuda sådan kapacitet utan att förlita sig på så kallade "off-chain"-lösningar eller extra lager.

Kostnad

Transaktionskostnaderna på Solana är dessutom betydligt lägre. En genomsnittlig transaktion ligger runt 0,000125 dollar, jämfört med Ethereums cirka 0,0005 dollar vid skrivande stund.

Vad är SOL?

SOL är Solanas egna kryptovaluta som driver nätverket och hjälper till att hålla transaktionskostnaderna nere. SOL fungerar som ett så kallat utility token — det används för att betala transaktionsavgifter på nätverket och för att säkra nätverket via staking.

Eftersom SOL är en proof-of-stake-token innebär det att nätverkets deltagare är med och säkrar systemet genom att låsa sina SOL-tokens. Värdet på SOL påverkas av flera faktorer: projektuppdateringar, marknadsaktivitet, sentiment, och även tokenekonomiska faktorer som inflationstakt, burn rate och hur snabbt ekosystemet växer.

Hur köper man SOL?

Om du är nyfiken på Solana och vill lägga till SOL i din portfölj, så är du i rätt sällskap. Med Tap-appen kan du enkelt köpa, sälja, byta och lagra SOL — både med kryptovaluta och traditionella valutor. På så sätt kan du bli en del av Solanas växande blockkedjeuniversum. Vill du veta mer om hur man handlar Solana? Läs vidare på Tap-webbplatsen.

Stocks are essentially shares in a company that the company sells to shareholders in order to raise money. Shareholders are then entitled to dividends if the company succeeds, and might also receive voting rights when the company makes big decisions (depending on the company).

What are stocks?

Stocks play an important role in the global economy, assisting both companies (in raising capital) and individuals (in potentially earning returns). Traders can buy and sell stocks through stock trades facilitated by various stock exchanges. The stock price is determined by supply and demand, largely influenced by the company's success and media representation.

These "units of ownership" are sold through exchanges, like Nasdaq or the London Stock Exchange, under the guidance of regulatory bodies, such as the Securities and Exchange Commission (SEC) in the United States. These regulatory bodies set specific regulations on how companies can distribute and manage their stocks.

What are the different types of stocks?

There are two types of stocks, common stocks and preferred stocks, as outlined below.

Common Stock

Shareholders of common stock typically have voting rights, where each shareholder has one vote per share. This might grant them access to attending annual general meetings and being able to vote on corporate issues like electing people to the board, stock splits, or general company strategy.

Preferred Stock

For investors more interested in stability and receiving regular payments rather than voting on corporate issues, preferred stocks are often the security of choice. Preferred stock are shares that provide dividends but without the voting rights. Like bonds, there are a number of features that make them attractive investments. For example, many companies include clauses allowing them to repurchase shares at an agreed-upon price.

Stock vs bond

Although both stocks and bonds signify an investment, they vary in how they operate. With bonds, you're essentially lending money to the government or a company and collecting interest as a return while with stocks you're buying part-ownership of a company. Another key difference is that bondholders usually have more protection than stockholders do.

In contrast to stocks, bonds are not normally traded on an exchange, but rather over the counter (the investor has to deal straight with the issuing company, government, or other entity).

Stocks vs futures and options

Futures and Options contrast stocks in that they are derivatives; their value is reliant on other assets like commodities, shares, currencies, and so on. They are contracts established off the volatility of underlying assets instead of ownership of the asset itself.

Stocks vs cryptocurrencies

While stocks provide a unit of ownership in a company, cryptocurrencies are digital assets that operate on their own network. Cryptocurrencies are decentralised, meaning that no one entity is in charge, while stocks are shares in companies that are heavily centralised and held accountable for their price movements. Both the stock price and the price of cryptocurrencies are determined by supply and demand.

Another key difference is that stocks are regulated while, at present, cryptocurrencies are not.

Where did stock trading originate?

The first recorded instance of stock-like instruments being used was by the Romans as a way to involve their citizens in public works. Businesses contracted by the state would sell an instrument similar to a share to raise money for different ventures. This method was called 'lease holding.'

The 1600s gave rise to the East India Company (EIC), which is considered by many the first joint-stock company in history. The EIC increased its notoriety by trading various commodities in the Indian Ocean region. Today, we see the limited liability company (LLC) as a watered-down version of the joint-stock company.

How does the stock market work?

The 'stock market’ is an umbrella term that refers to the various exchanges where stocks in public companies are bought, sold, and traded.

The stock market is composed of similar yet different investment opportunities that allow investors to buy and sell stocks, these are called "stock exchanges." The best-known exchanges in the United States are the New York Stock Exchange (NYSE), Nasdaq, Better Alternative Trading System (BATS), and the Chicago Board Options Exchange (CBOE).

Together, these organisations form what we call the U.S. stock market. Other financial instruments like commodities, bonds, derivatives, and currencies are also traded on the stock market.

An example: the New York Stock Exchange

The New York Stock Exchange (NYSE) is the largest equity exchange in the world, and it has a long and rich history. Established in 1792, it was originally known as the "Buttonwood Agreement" between 24 stockbrokers who gathered at 68 Wall Street to sign an agreement that called for the trading of securities in an organised manner.

Since then, the NYSE has become a global leader in financial markets, with more than 2,400 companies listed and nearly $26.2 trillion in market capitalization. The exchange has an average daily trade volume of $123 billion.

Investing in common stock or preferred stock on the NYSE can be done through a broker or online stock trading platform. When trading on the NYSE, investors have access to a wide range of products and services, including stocks, bonds, mutual funds and ETFs (exchange-traded funds).

Investors can also take advantage of the numerous benefits that come with trading on the NYSE, such as access to real-time information and the ability to buy and sell quickly. The trading platform is regulated by the U.S. Securities and Exchange Commission (SEC).

How to navigate stock market volatility

Stock market volatility, characterised by rapid and unpredictable changes in stock prices, is influenced by economic indicators, geopolitical events, and investor sentiment. To manage this volatility, investors can diversify their portfolios, set clear investment goals, and maintain a long-term perspective.

Regular portfolio reviews and seeking guidance from financial advisors can also help when it comes to making informed decisions during volatile periods. Investors who stay informed about market trends and use strategic approaches can navigate market fluctuations more effectively, which better positions them for long-term success in stock investing.

The importance of diversification when investing

Diversification is key when investing, and the stock market is no exception. The "don't put all your eggs in one basket" approach offers benefits like risk reduction and the potential for higher returns. Strategies for diversification include investing across different sectors, industries, and asset classes.

By spreading investments, investors can manage risk effectively, ensuring their portfolio isn't overly exposed to any single asset or market sector. This helps cushion against market downturns and enhances the overall stability of the investment portfolio.

Terminology associated with the stock market

- Broker: A broker is someone who buys and sells assets on behalf of another person, charging a commission for their services.

- Stockholders equity: The value of a company's stock can be better understood by this metric, which is the company's assets remaining after all bills are covered (liabilities).

- Stock splits: Conducting a stock split is one way that companies make their stocks more accessible to investors. Although it won't change the market capitalisation or value of shares, it will increase the number available.

- Short selling: If an investor wants to bet on a stock's price going down, they can take a "short" position. To do this, they must borrow the stock from either a broker or a financial institution.

- Blue-chip stocks: Companies that are large and have a lot of capital typically fall into the blue-chip category. They usually trade on famous stock exchanges, like the NYSE or Nasdaq.

- Pink sheet stocks: 'Penny' or 'pink-sheet' stocks are those that trade below the $5 threshold and are typically OTC (over the counter). These can be high risk.

- Buying on margin: Buying on margin is using borrowed money to buy stocks, bonds, or other investments in the hopes of making big returns and paying off the loan.

- Market order: When placing an order for a trade, the investor needs to pick from several types of orders. A market order is executed at whatever the next price is, which can be risky if there's a big gap between what buyers and sellers are offering.

- Limit order: A limit order is an order to buy or sell a security at a specified price, with a maximum amount decided on before executing the trade.

- Stop order: A stop order, also referred to as a stop-loss order, is an order placed with a broker to buy or sell once the stock reaches a predetermined price.

In conclusion

Shares, or stock, are units of fractional ownership in a company that investors buy to gain capital appreciation and tap into a company's earnings if the company's stock pays dividends. Companies, through listing their stock on an exchange, can raise capital to further develop the business.

Stock is traded on an exchange, and the stock prices are determined by supply and demand.

Used across all markets, the spread is the difference between the buy (offer) and sell (bid) prices of an asset. Spreads provide an additional opportunity to traders to make money through buying and selling assets.

The spread of an asset will depend on the current demand or an asset and the market’s volatility and is presented in either a percentage or value form. Assets with markets displaying higher levels of demand will typically have smaller spreads and usually higher price points.

As an example, when you look at an order book for Bitcoin you will usually see prices reflected in green and red reflecting the offer prices and bid prices. The spread will then be indicated above the most recent trades. As another example, consider foreign exchange counters where the buy and sell prices are different, this difference is known as the spread. Market makers use spreads to generate money from transactions completed at market prices.

Let's put this in context: George buys 100 shares for a £2 ask price in “ABC” a publicly listed company. George pays £200 in return for 100 shares. If he decides to sell the shares back at the same price he bought them for, he would sell the 100 shares for the bid price at £1.95 and would receive £1.95 each instead of £2. This would mean he gets a return of £195 and loses £5, which would be paid to the market maker.