November 2025 could be a turning point for crypto. From ETFs to major network upgrades, here are six catalysts that could shape the market.

Keep reading

As we move into November 2025, the crypto-market is gearing up for one of its most intriguing phases yet. From spot-ETF momentum to narrative shifts, network upgrades and real-world asset tokenization, multiple catalysts are aligning. Here are six key developments to watch.

1. Seasonality & Historical Momentum Could Kick In

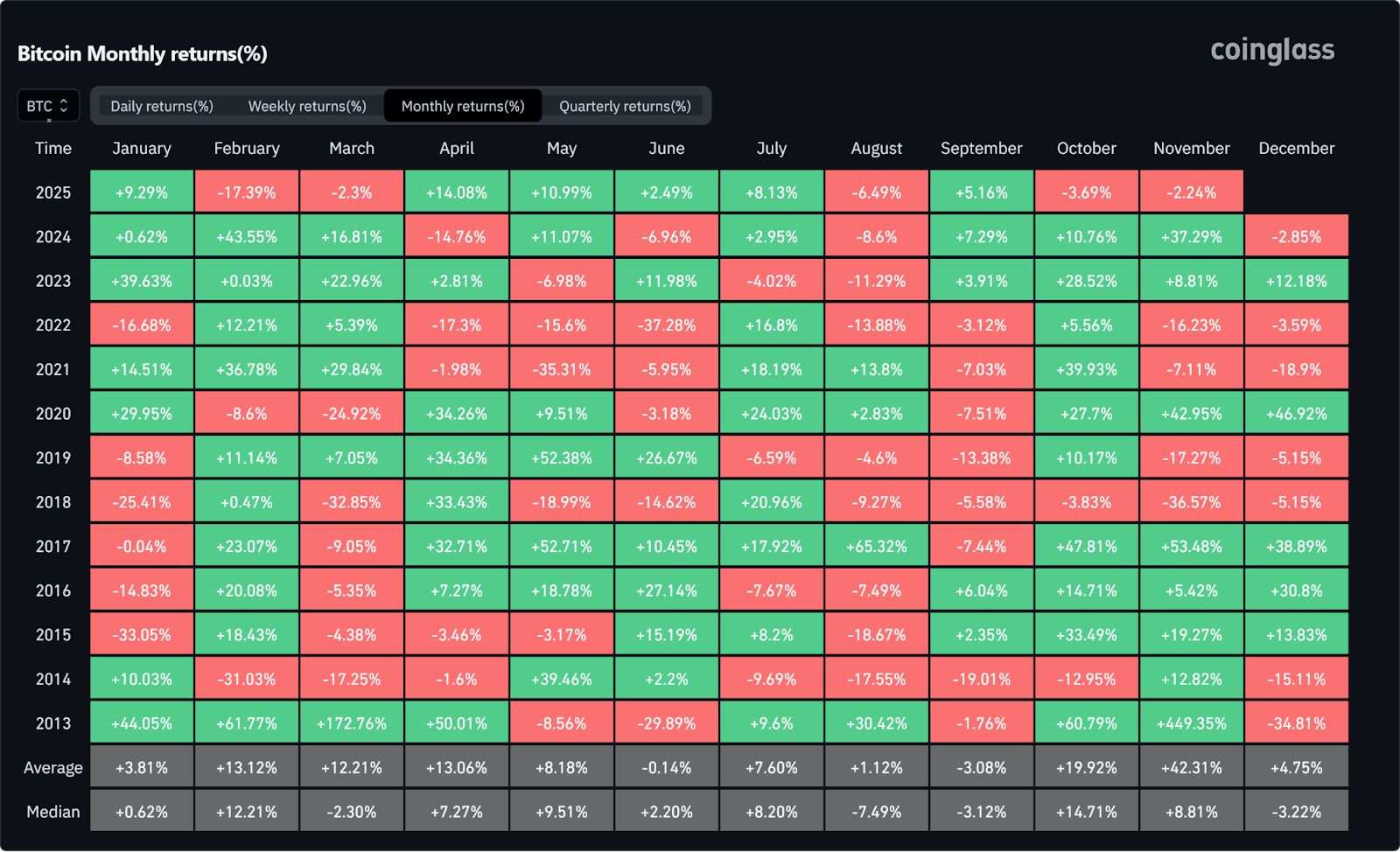

While "Uptober" fell short of expectations, November could tell a different story. Historically, it's been one of the strongest months for digital assets, with Bitcoin in particular averaging +42.31% gains in recent years.

When combined with the renewed ETF narrative, increased whale accumulation, and a stronger appetite for risk assets, market momentum appears to be building. Participants are closely monitoring how these dynamics could influence sentiment, especially as trading volumes and key technical levels come into play. If Bitcoin maintains stability around the $100K zone and Ethereum shows signs of renewed strength, November could become a more active month for crypto markets compared to October.

2. Ether’s Next Move Could Set the Tone for Altcoins

The final weeks of 2025 may prove pivotal for Ethereum (ETH). Although retail accumulation has paused somewhat, wallet-level data shows large holders (1,000 to 100,000 ETH wallets) added roughly 1.6 million ETH in October (around $6 billion), it’s a sign that whales and larger holders are staying active as the year winds down.

If ETH begins to break out or even stabilize around current levels, it could unlock the broader altcoin market, which has been lagging for months. The playbook that many are hoping for is the following one: ETH strength leads to improved risk appetite, which in turn sparks an altcoin rotation as investors seek higher risk exposure.

Ethereum remains the accepted benchmark for gauging sentiment across the non-Bitcoin segment of the market, and its performance frequently acts as a catalyst for capital flows into smaller assets. Keeping an eye on its fundamentals (from staking yield to liquidity shifts on major exchanges) will be important. In many ways, ETH could potentially become the gatekeeper to the next phase of the market’s recovery and the tone-setter for the coming months.

3. ETF Comeback After Delays

The recent U.S. government shutdown briefly froze several crypto-spot ETF filings, leaving the “ETF narrative” in suspense. But now the pause is over for Bitwise’s Spot Solana ETF. It has finally launched with strong early inflows, and the broader momentum is returning.

With this foundation, November could reignite the ETF trade in earnest, we may finally see filings for Ethereum staking products, new spot-Bitcoin funds and renewed institutional interest. If filings begin to stack up and regulatory engagement deepens, this could mark the next major inflection for how crypto is accessed in traditional portfolios.

4. Altcoins at an Inflection Point

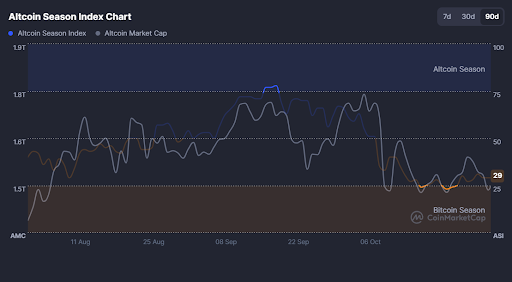

The broader altcoin sector enters November under pressure as the Altcoin Season Index sits near 29, signaling a reset after October’s downturn. But inflection points often follow pressure. If ETH sets the tone (as many are hoping for), mid-cap and high-beta altcoins (such as SOL, AVAX, NEAR) could begin to capture rotation flows.

Traders might want to watch for flow changes such as increased volumes, wallet relocations and new project launches. While caution is still prevailing, this may be the window where sentiment begins to swing back into “altcoin season”.

5. Major Network Upgrades

Technical infrastructure is not just background noise; it often creates catalyst-events. For example, Ethereum’s upcoming Fusaka Upgrade (scheduled for early December) is designed to increase layer-2 data capacity and reduce transaction costs.

Meanwhile, various Layer-2 ecosystems are preparing upgrades and cross-chain activations. One such upgrade, Shibarium Upgrade’s security overhaul on the Shiba Inu network. These events may ignite renewed network activity, developer interest and capital flows into ecosystems ready to scale.

6. Real-World Asset (RWA) Tokenization Accelerates

The tokenization of real-world assets (RWAs), such as real estate, bonds, equities, is moving from niche to mainstream. For instance, according to Standard Chartered, this market is projected to grow to around $2 trillion by 2028. Institutional interest is burgeoning, and regulatory frameworks are emerging.

As November unfolds, we may see announcements of large tokenization initiatives or new platforms bridging DeFi and traditional finance. For crypto holders and ecosystem observers, this means the familiar “crypto only” narrative is expanding into real-asset integration, a meaningful broadening of the opportunity set.

The Verdict

November 2025 is shaping up to be more than just another month. Spot-ETFs potential, ETH’s path, altcoin rotation, seasonal tailwinds, infrastructure upgrades and RWA tokenization all sit in motion. Each one individually is significant; together they create a multi-vector setup.

For those in the crypto space, whether you're holding long-term, actively trading, or building the next wave of infrastructure, November is likely to be eventful. This isn't a month to coast on autopilot. Track where capital is flowing. Pay attention to which narratives are gaining momentum and which are fading. The players are moving, and the pieces are falling into place.

NEWS AND UPDATES

LATEST ARTICLE

In this article, we’re guiding you through the intricacies of the e-money licence: what it means, who needs one and of course, how it affects you, the consumer. This new wave of regulation has been put into place to not only safeguard the consumer but also to put measures in place to identify and stop fraudulent activity.

What Is Electronic Money (E-money)?

Before we dive into the licencing requirements, let us first take a look at what electronic money is defined as. Essentially, e-money is a digital version of cash. It maintains a monetary value that can be used to make payments and various transactions, typically over the internet, or through a phone or card.

E-money products are either software-based or hardware-based and are responsible for electronically storing the monetary value. Software-based products are used on computers and tablets and require an internet connection (like PayPal for example) while hardware-based products encompass cards that have a chip card and do not require an online connection (for example, Square).

What Is An E-money Licence?

The e-money licence is a regulatory licence that authorises an electronic money institution (EMI) to conduct business. EMIs represent the digitisation of financial services and are authorized to issue money as well as provide payment cards, e-wallets, and IBAN accounts. While banks may provide a similar service, they require an alternative licence as they are able to provide a greater range of services.

In a nutshell, an EMI is considered as such if it engages in the issuing and redeeming of electronic money (e-money), cash withdrawal, deposit and payment services, remittance services, debit or credit transfers, payment initiation and execution services, and account information services. They may conduct these services only if they have the proper licensing.

How Does It Protect The Consumer?

While regulation and consumer protection are the driving force behind e-money licences, there are also several other reasons as to why the regulatory framework has been put into place. The licence is designed to provide businesses with the opportunity to gain access to the e-money market, to facilitate innovation in secure e-money services, and to build healthy competition in a secure market.

E-money licences are obtained to safeguard a consumer’s funds should the EMI become insolvent. This operates in an entirely different manner to a banking licence. Under the proper regulation, EMI’s can choose to do either of the following options to safeguard consumer funds (funds provided by customers in exchange for the issuance of e-money):

- deposit the funds into a segregated client’s funds account with an authorised credit institution, or

- acquire insurance that will cover the risks associated with the client’s funds.

This ensures that the consumer is always protected against loss of funds, and will be compensated accordingly should the situation present itself. It is imperative that consumers only choose EMIs with the correct e-money licences.

How Much Money Is Protected With The E-Money Licence?

According to the FCA regulations, the EMI is responsible for establishing the appropriate organisational arrangements to ensure that the safeguarded funds are at all times protected.

As mentioned above, this can be done by either storing the deposited customer funds in a separate account (different from the institution’s working capital and other funds) or by ensuring that they are covered by an appropriate insurance policy or comparable guarantee.

While licenced banks work in conjunction with the Financial Services Compensation Scheme (FSCS) and only insure users up to £85,000, EMIs are required to protect 100% of the consumers’ funds.

According to the licence, EMIs are required to safeguard all funds deposited on the platform and not just a portion as per the licence required by the banks.

While EMIs take several other precautions to protect consumer funds, the e-money licence ensures that the most fundamental legal requirements are met, granting the company the right to legally operate.

For all those curious about the crypto industry ready to dip their toe in the water, this one is for you. Below we share a warm welcome to the industry with a range of helpful resources covering everything from what cryptocurrency actually is to how to buy and store it. For individuals and businesses alike, let's get into it.

What Is Cryptocurrency?

A great place to start for any people who are crypto-curious, let's cover the basics. Cryptocurrency is essentially digital cash that can be transferred from one person to another without having to rely on an authoritative entity (like a bank or government or financial institution).

This peer to peer cash system is supported by blockchain technology, a technology that facilitates the transactions and essentially acts as a giant public ledger where anyone can view any transactions that have been made on the network.

Through the use of blockchain, a decentralised network (meaning that no one is in charge, rather everyone follows the same protocol) of computers is responsible for verifying and executing transactions. Depending on the network this can be done in a few seconds or up to a few minutes, causing big waves in the traditional financial sector.

If you take away just four points from the above, let it be

- Digital cash

- Peer to peer

- Blockchain technology

- Decentralised

Cryptocurrency gets its name from cryptography currency, as it uses encrypted code (cryptography) to secure and maintain the network.

Each cryptocurrency will have a value, based on what it was last traded for, a market capitalisation, a circulating supply and a ticker symbol. The ticker symbol would be BTC for Bitcoin and ETH for Ethereum.

Let's Take A Look At The Three Biggest Cryptocurrencies

You've definitely heard of Bitcoin, but what about the other top cryptocurrencies? Below we give a very quick breakdown of the other big projects on the scene based on the biggest market caps. When learning about new coins we strongly advise that you do your own research before making any purchases.

Bitcoin (BTC)

A digital cash system that facilitates the quick and cheap cross-border transfer of money.

Ethereum (ETH)

A blockchain platform that allows developers to create their own decentralised applications on top of theirs.

Tether (USDT)

A stablecoin, meaning that its value is pegged to a fiat currency, in this case, the US dollar. 1 USDT will always be worth $1. Stable coins are a great way to enter the market as they are less volatile than traditional cryptocurrencies.

How To Store Cryptocurrency

Similar to fiat currencies, cryptocurrencies need to be stored in a wallet. As the currencies are entirely digital, so too must the wallet be. Each cryptocurrency operates off a different network, requiring one wallet for each network.

For instance, you cannot store Bitcoin in an Ethereum wallet as Bitcoin runs off a separate blockchain. Different to fiat wallets, digital wallets are how transactions take place. From your wallet, you will enter the crypto wallet address of the recipient and execute the transaction from there.

To purchase and accumulate cryptocurrency, you will first need a wallet. There are a few different types of wallets, but let's keep it simple for now. On Tap, a fully regulated crypto app, users are automatically given a range of wallets, one for each supported cryptocurrency on the network. This allows users to buy, sell, trade, store and manage many cryptocurrencies from one secure app. Simply head to the Tap website and conveniently download the relevant app from there.

How To Buy Cryptocurrency

Buying cryptocurrency used to be a complicated endeavor however with new products on the market it has become simpler and easier to do. Tap's mobile app is a classic example. Buying crypto Tap has never been so easy all you need to do is to create an account.

You will then be asked to confirm your identity through a process known as KYC (Know Your Customer). This is a common practice required by any entity facilitating the sale of cryptocurrencies. The process is entirely integrated and will require you to submit a picture of an identification document and a selfie of you, easy stuff.

Once your account is created, you can then deposit funds. This can be done through debit card or bank transfer. Simply load your fiat wallet with the currency of your choice for free, using a debit card or a bank transfer as a payment method of your choice.

With a loaded fiat wallet, you are then able to go shopping! Under Assets on the home screen, select Crypto, then find the cryptocurrency you would like to purchase. Simply click Options, then Buy once you are on the cryptocurrency you would like to purchase. The process is as simple and easy as it sounds.

After buying crypto, the funds will be deposited into your wallet in a fraction of a second once the transaction has been confirmed. Not too complicated, was it? Submerge yourself into the world of crypto today with the Tap app, head to your Google Play or Apple app stores to get started straight away.

If you're looking to earn extra money from anywhere online you've come to the right place. Making money online has certainly become more accessible and easier over the years, and in this blog, we're reviewing several ideas to do so without having to invest.

Whether you're looking to make some money on the side, or as a full-time pursuit, remember that as with most things in life: consistency is key. On this page, you'll find a number of beginner options requiring no particular skillset (only a bank account) for you to look into, relevant everywhere from the United Kingdom to the European Union to Australia. Each method varies in financial contribution, which we've highlighted at the end with a rating of the start-up costs.

Top 5 ways to make money online for beginners

1. Affiliate marketing

Affiliate marketing involves an individual earning money through promoting another business's product. This can be done through your own platform which might range from a blog to a website, social media, email campaigning or simply Google Ads.

All you need is a working internet connection, a bank account and a reliable browser. Each time a friend or family clicks and signs up for the product, you bank a commission.

Many companies these days offer this service, try to find one that you and your network might be interested in and see the opportunities that they present.

Start-up Costs: $

2. Dropshipping

This will require a substantial amount of effort, however, the returns will be that much greater. Dropshipping involves selling a product online that you do not need to keep an inventory of, instead, the company that you are buying the goods from sends them directly to the customer.

You act as the middleman between the manufacturer and the consumer and make money from the margin that you add. The start-up costs will be for your online website and marketing.

Start-up Costs: $$

3. Freelance your skills

You can hire out your skills on sites like Upwork or Fiverr. Users create profiles expressing their skills, anything from writing to graphic design to music creation, and can apply to jobs requiring these skills.

These sites will typically allow employers to connect with employees, and once the work is completed the funds are deposited directly into your account. This is also a great way to start a side hustle in your area of expertise without having to tuck into your savings.

Start-up Costs: zero

4. Explore the world of cryptocurrencies

Engaging with cryptocurrencies has gained significant attention in recent years. Before diving in, it’s important to educate yourself thoroughly to grasp the complexities involved. Our blog section on how to learn about crypto is a great place to begin. The cryptocurrency market is known for its high volatility, which presents both risks and opportunities. Whether you're active daily or only occasionally, understanding the landscape is key. To get started, consider signing up for a reputable and regulated platform like Tap, which can help you manage your funds securely.

Start-up Costs: $$

5. Participate in online surveys

Online surveys are a popular way for beginners to make money online. Companies are always looking for feedback on their products and services, and they are willing to pay for it. There are several websites that offer paid online surveys, such as Swagbucks, Survey Junkie, and Toluna.

To get started, simply sign up for an account, complete your profile, and start taking surveys. You'll earn points or cash for each survey you complete, which can be redeemed for gift cards or PayPal payments. Keep in mind that surveys may have specific demographics, so you may not qualify for every survey. However, with some patience and consistency, you can earn a decent amount of extra income in your spare time.

Start-up Costs: zero

Earn money online from anywhere in the world

Of course, this list is only a small portion of the ways you can make money online, simplified down to the top 5. If you have more time at your disposal you can engage in market surveys, beta testing, becoming a virtual assistant, or even coaching.

The opportunities are endless, with a wide range of start-up costs, time management, returns and the amount of effort required are to be considered. Ensure you do adequate research in order to learn about your next venture before diving in. At the end of the day, anyone can earn money online, the first step is just to get started. Good luck, may you have only lucrative experiences.

5 tips on how to manage your money

Now that you’ve established your income stream/s, here are 5 tips on how to manage the money you’re making. Whether you’re doing this as a side hustle or a full time job, consider implementing the following 5 steps in order to build your finances. .

- Build an Emergency Fund

Just like in personal finance, building an emergency fund is crucial for making money online. This fund will act as a safety net in case you hit a rough patch, and it will allow you to continue your online work without financial stress.

- Create a Budget

Budgeting is another essential aspect of making money online. Creating a budget will help you keep track of your income and expenses, and it will allow you to make informed decisions about where to allocate your resources.

- Focus on Your Niche

To make the process of making money online more enjoyable consider focusing on a specific niche that you are passionate about. Whether it's writing, graphic design, or web development, become an expert in your field and provide value to your clients.

- Network and Build Relationships

Building relationships with other professionals in your industry is a valuable step when making money online. Networking can help you find new clients, build your reputation, and even lead to new business opportunities.

- Stay Consistent and Persistent

Making money online takes time and effort, and it's important to stay consistent and persistent. Set realistic goals for yourself, create a schedule, and stick to it. Remember that success doesn't happen overnight, so don't get discouraged if you don't see results right away.

So, what are you waiting for?

Whether dissecting crypto or fiat currencies, the foundations remain the same: the currency must serve as a store of value and function as a medium of exchange for goods and services. While both these currency options tick those boxes, cryptocurrencies tend to also be followed by a dark cloud of volatility in the financial sector.

Market volatility is a natural byproduct of a developing market, however, it can also cause many losses if not managed correctly. When the crypto markets go through high levels of market volatility they tend to get discredited with being a viable payment option. After paying withness to the Bitcoin market swings, several individuals recognised this flaw in the digital currency space and created a solution, "the stablecoin".

In this article we establish what is a stablecoin is, how it fits into the financial landscape and explore the pros and cons of these digital currencies.

What Is A Stablecoin?

Stablecoins are digital currencies that harness the benefits of being a decentralized, blockchain-operated currency without volatility. Backed by any currency or commodity, stablecoins are pegged to the value of their underlying asset and managed and secured by their relevant platforms. For instance, Tether is pegged to the US dollar while Tether Gold is pegged to the price of gold and Tether EURt is backed by the Euro.

These currencies operate like any other cryptocurrency, using blockchain technology to maintain and operate the network, but do not fluctuate in value based on supply and demand. Rather the price remains consistent with the asset it is pegged to, providing a better tool for digital payment transactions.

How Do Stablecoins Maintain Their Price?

While we've established that stablecoins are pegged to a commodity and reflect that price, let's cover how exactly that is achieved. Using fiat-backed stablecoins as examples, the companies behind these coins are required to hold a US dollar equivalent for each coin in circulation (or Euro if the stablecoin is pegged to it).

These funds, also referred to as reserves, are either held in bank accounts or can be a combination of cash and short-term U.S. Treasury bonds. Most of the companies issuing stablecoins conduct third-party audits to prove that their reserves are at the correct levels and release this information to assure users that their coins are always worth $1 (or the currency-backed equivalent).

Why Have Stablecoins Become so Popular?

The first stablecoin to enter the market was Tether in 2014, pegged to the US dollar. Tether is currently the third-largest cryptocurrency based on market capitalization, illustrating its vast popularity. The second biggest stablecoin currently on the market is USD Coin, also backed by the US dollar, which sits in the top 5 biggest cryptocurrencies with an equally impressive trade volume. Both these coins have provided valuable talking points within the industry as their market caps and adoption increase and they climb the ranks of the biggest cryptocurrencies.

Due to their resistance towards volatility, stablecoins have increased in popularity and are more widely used for conducting business around the world and executing cross border payments.

The Pros Of Stablecoins

Stablecoins are popular options for both businesses and individuals conducting business across borders. Below we outline the top benefits that stablecoins present to the market:

Digital Currency

The obvious first benefit of stablecoins is that they are maintained by blockchain technology and able to conduct international transactions in a much shorter time frame and for less cost than fiat currencies. The fast settlement times make these currencies an excellent, cross-border medium of exchange. They are also easy to use as they operate from wallets in similar ways to traditional cryptocurrencies.

Zero Volatility

Due to the nature of stablecoins being pegged to a fiat currency or commodity, they typically experience little to no high volatility trading periods resulting in a more reliable currency with the benefits of blockchain technology. Pertinent to increasing its adoption.

Hedge Against Failing Markets

Stablecoins have become increasingly popular for traders to hedge against other cryptocurrencies when markets experience a decline in price. Stablecoins allow traders to quickly liquidate their digital assets and easily reenter the market when the price stabilizes.

The Cons Of Stablecoins

Centralisation

While blockchain technology and cryptocurrencies celebrate the notion of being decentralised, stablecoins do bring in a nature of centralisation, particularly when it comes to the backing of the assets. Ensuring that each coin in circulation is backed by an equal reserve value requires a team that leans the operation more toward a centralized structure.

Transparency

Several stablecoins have been called out publicly for not being transparent with their reserves. Tether, for example, has seen much public outcry concerning whether the company has the correct amount of reserves, leading to fines and regulations imposed by the US government. They have since released a report on the current reserve holdings of the company.

In Conclusion

Many traders have incorporated stablecoins into their portfolios, to have as a hedge against falling crypto markets or falling fiat markets. These digital assets are also used by businesses around the world to conduct payments with the benefits of digital currencies and without the risk of volatility. Through the Tap app, users can now access and purchase USD Coin (USDC) as well as Tether (USDT). The sleek design of the app interface makes it easy for users who want to buy or sell cryptocurrencies with fiat currency through their phones in a click.

When it comes to choosing a stablecoin, consider the projects behind it, the liquidity and the ease of use in terms of wallet compatibility.

Saving and investing are two key elements to managing one's personal wealth. In this article, we explore the benefits and downfalls of both these tools and give you a broader understanding of the topics.

What Does saving entail?

Saving money is an imperative step in building one's wealth and involves putting money away on a consistent basis, consistency is key. These funds are usually kept in an interest-bearing account, allowing the value to increase passively over the years.

In the United Kingdom, there are different types of ISA (individual savings accounts) that offer tax-free savings options.

In order to save, one must be spending less than they're earning.

What does investing entail?

Investing involves buying an asset with the intention for it to accumulate in value. This typically comes after saving, although the earlier the better. People invest in the likes of stocks, cryptocurrencies, property and even themselves (education, capital for a business) in the hopes of generating returns.

What's the difference between saving and investing?

The biggest difference between the two is the varying returns you can earn. Saving money in a bank account typically provides returns of 0.5 - 0.8%, while the return potential on cryptocurrencies and stock is much greater.

The other main difference between saving and investing is the risk. So, while earning higher returns on investments might sound much more appealing, the risk is usually greater. Savings accounts carry minimal risk and are usually insured while investment portfolios will rise and fall with the market and are only insured if the investment company fails. Investors should balance the options and establish which risk level they are comfortable with.

In light of these risks, savings are recommended for short term goals while investments cater better to long term financial objectives. This is because long term investments will ride out the ebb and flow of markets and recover even if there is a drop over a certain period. Savings on the other hand are more easily accessible and won't be "interrupted" if the funds are used for an emergency.

However, savings are also susceptible to inflation as the interest rates are seldom higher than the inflation rates. For example, if your bank is offering a 0.6% interest on your savings account and inflation rose 2%, your savings would have actually decreased in value. Investing typically beats inflation.

The similarities between savings and investing

As both tools are excellent at building and creating more wealth, there are bound to be similarities between the two.

The main similarity between the two is that both options are best started now, whether you're in them for the long or short term benefits. This is due to compounding. Compounding is the process where the interest you earn on an investment or savings account is continuously reinvested, increasing the base sum each period.

For example, if you put $1,000 into a compounding savings account and earned 2% interest each year. The next year you will be earning 2% interest on the lump sum plus the interest earned, $1,020. The next year you would earn $1,020.40 ($1,020 interest earned, $20.40). This doesn't sound like too much, but over a ten-year period, you would have amassed $219.20 without having done a thing.

Before you get started

Before getting started on either of these options, ensure that you have a positive cash flow and are debt-free. You'll also need to establish what your risk tolerance is, your short term and long term financial requirements, and when you would like to access the money.

If you don't have one already, you'll want to establish an Emergency Fund that can cover your living expenses for 3 - 6 months. Should you lose your job you can then fall back on this loan and not have to rely on credit cards with high-interest rates.

Experts also recommend setting up a retirement fund, with automated monthly contributions. Once your emergency and retirement funds are established, you can consider a short term savings account or long term investment, or both.

Pros and cons of saving and investing

Below we highlight the pros and cons of both tools:

Saving

Pro: Money is accessible and can easily be withdrawn.

Pro: Exempt from market volatility.

Con: Cannot leverage on market gains (potentially missing out on large compound interest benefits).

Con: Susceptible to inflation.

Investing

Pro: Longer time frames allow for favourable compounding interest.

Pro: Could tap into large market gains.

Con: Exposed to more risk as markets are susceptible to drops.

Con: May incur a penalty if the money is withdrawn too soon.

The bottom line

Both savings and investment options carry their own set of risks and rewards and it's ultimately best for you to speak to a financial adviser who is able to provide you with calculated professional advice.

Disclaimer: This article is intended for communication purposes only, you should not consider any such information, opinions or other material as financial advice. The information herein does not constitute an offer to sell or the solicitation to purchase/invest in any assets and is not to be taken as a recommendation that any particular investment or trading approach is appropriate for any specific person. There is a possibility of risk in investing as investors are exposed to fluctuations in all markets. This communication should be read in conjunction with Tap's Terms and Conditions.

Day, Month,2021, LONDON: TAP Global has been shortlistedin the ‘Best Use of Crypto in Financial Services’ in the Emerging Payments Awards(EPA) 2021.

Now in its 14th year, the Emerging Payments Awardscelebrate innovation and collaboration by recognising companies thathave made significant impact in supporting and providing payment solutions forconsumers and businesses.

It is one of the most recognized awards within the UK payments industry with an independentpanel of 58 judges including this year:

· Anna Maj FinTech Leader, Senior Advisor, Truffle Capital, SeniorLecturer CFTE

· Jill Docherty [ of Business Development, UK & Ireland, Visa

· Martha Mghendi-Fishe Founder & Executive Board Chair, EWPN

· Mark Walker Co-founder & COO Editorial Director, The FintechPower 50 and The Fintech Times

· Joanne Dewar CEO, Global Processing Services

· Nikki Evans CEO EMEA, EML

Tap Global wasshortlisted for The ‘Best Use of Cyrpto inFinancial Services’ category based on criterias such as the benefits it providesto its end-users, how TAP stands out from its competitors due to its featuresand innovation, and the proven evidence of its success in the market.

“‘Tap was one of the first companies to launch a crypto prepaidpayment card with Mastercard in the EU’ in 2020 and our cryptocurrency-to-fiat prepaidMastercard and smartphone app give users the

power to instantly trade all major cryptocurrencies to fiat, andto make purchases with their cryptocurrency”, comments David Carr, CEO atTAP GLOBAL.

“Tap’s proprietary AI Middlewareconnects to multiple exchanges simultaneously, automatically validatingavailable liquidity and selecting the most competitive prices whilefacilitating trades in a matter of seconds. Users can convert their cryptocurrency assets to fiat instantly,allowing them to pay for goods or use an ATM anywhere Mastercard is accepted.

Through the smartphone app, users can securely send and receivecryptocurrencies and fiat, view their transaction history, lock and unlocktheir card in case of loss and instantly view their PIN. Tap offers its usersfull EEA coverage for card, banking and cryptocurrencies and a named EUR IBANand/or GBP Sort Code and Account Number, as well as secure, offline, coldstorage behind a multi-signature wallet with the highest grade security for allcryptocurrency assets”, he further adds.

“It’s an honour to be shortlisted for this award which furtherrecognizes the added value TAP brings to market and the benefits for our end-users.None of this would have been achievable without the hard work of our teams andthe support of our partners”, says David.

Commenting on theannouncement, Kriya Patel, CEO at Transact Payments adds, “The EPAawards are some of the most prestigious awards in our industry recognisingcompanies that are making a real difference in driving innovation in payments.We’re delighted to be working with TAP Global and being shortlisted for thisaward.”